Regional & Country-Specific Global Markets1. North America

United States

The U.S. is the world’s largest economy and the beating heart of global finance. It hosts the New York Stock Exchange (NYSE) and NASDAQ, two of the biggest stock exchanges globally. The U.S. dollar serves as the world’s reserve currency, making American financial markets a benchmark for global trade and investment.

Strengths:

Deep and liquid capital markets

Technological innovation hubs (Silicon Valley, Boston, Seattle)

Strong consumer demand and advanced services sector

Risks:

High national debt levels

Political polarization affecting policy stability

Trade tensions with China and other countries

Key industries include technology, healthcare, energy, defense, and finance. U.S. policies on interest rates (through the Federal Reserve) ripple across every global market.

Canada

Canada’s economy is resource-heavy, with strengths in energy (oil sands, natural gas), mining (nickel, copper, uranium), and forestry. Toronto hosts a vibrant financial sector, and Canada’s stable political environment attracts global investors.

Strengths: Natural resources, stable banking sector

Challenges: Heavy reliance on U.S. trade, vulnerability to oil price swings

Mexico

As a bridge between North and Latin America, Mexico has growing manufacturing and automotive industries, heavily integrated with U.S. supply chains (especially under USMCA trade agreement). However, crime, corruption, and political risks remain concerns.

2. Europe

Europe is home to some of the world’s oldest markets and remains a global hub for trade, technology, and finance.

European Union (EU)

The EU is the world’s largest single market, with free movement of goods, people, and capital across 27 member states. The euro is the second-most traded currency globally.

Strengths: High levels of economic integration, advanced infrastructure, strong institutions

Weaknesses: Aging population, energy dependency (especially after the Russia-Ukraine war)

Germany

Germany is the powerhouse of Europe, leading in automobiles, engineering, chemicals, and renewable energy. Frankfurt is a major financial hub.

Opportunities: Transition to green energy, high-tech industries

Risks: Export dependency, demographic challenges

France

France blends industrial strength with luxury, fashion, and tourism industries. Paris is also a growing fintech hub.

United Kingdom

Post-Brexit, the UK operates independently of the EU, but London remains a global financial center. Britain leads in finance, pharmaceuticals, and services.

Eastern Europe

Countries like Poland, Hungary, and Romania are emerging as manufacturing hubs due to lower labor costs, attracting supply chain relocations from Western Europe.

3. Asia-Pacific

Asia-Pacific is the fastest-growing region, driven by China, India, and Southeast Asia.

China

China is the world’s second-largest economy and a manufacturing superpower. It dominates global supply chains in electronics, textiles, and increasingly, electric vehicles and renewable energy.

Strengths: Huge domestic market, government-led industrial policy, global export strength

Challenges: Debt, slowing growth, geopolitical tensions with the U.S.

Markets: Shanghai Stock Exchange, Shenzhen Stock Exchange, and Hong Kong as a global financial hub

India

India is one of the fastest-growing major economies, with strong potential in IT services, pharmaceuticals, digital payments, manufacturing, and renewable energy.

Strengths: Young population, digital transformation, strong services sector

Challenges: Infrastructure gaps, unemployment, bureaucratic hurdles

Markets: NSE and BSE, with rising global investor participation

Japan

Japan has a mature economy with global leadership in automobiles, electronics, and robotics. The Tokyo Stock Exchange is one of the largest in the world.

Strengths: Advanced technology, innovation, strong corporate governance

Challenges: Aging population, deflationary pressures

South Korea

South Korea is a global leader in semiconductors (Samsung, SK Hynix), automobiles (Hyundai, Kia), and consumer electronics. The KOSPI index reflects its market vibrancy.

Southeast Asia

Countries like Vietnam, Thailand, Indonesia, and Malaysia are emerging as new growth centers, benefiting from supply chain shifts away from China.

Vietnam: Manufacturing hub for electronics and textiles

Indonesia: Rich in resources like nickel (critical for EV batteries)

Singapore: Leading global financial and logistics hub

4. Latin America

Latin America’s markets are resource-driven but often volatile due to political instability and inflation.

Brazil

The largest economy in Latin America, Brazil is a major exporter of soybeans, coffee, iron ore, and oil. It also has a growing fintech and digital economy sector.

Argentina

Argentina struggles with recurring debt crises and inflation, but it has strong potential in lithium reserves, agriculture, and energy.

Chile & Peru

Both are resource-rich, particularly in copper and lithium, making them crucial for the global clean energy transition.

Mexico

(Already covered under North America, but plays a dual role in Latin America too.)

5. Middle East

The Middle East’s economies are largely oil-driven, but diversification is underway.

Saudi Arabia

Through Vision 2030, Saudi Arabia is reducing reliance on oil by investing in tourism, renewable energy, and technology. The Tadawul exchange is gaining global importance.

United Arab Emirates (UAE)

Dubai and Abu Dhabi are major global hubs for trade, logistics, and finance. Dubai International Financial Centre (DIFC) attracts global capital.

Qatar & Kuwait

Strong in natural gas exports and sovereign wealth investments.

Israel

Israel is a “startup nation,” leading in cybersecurity, AI, fintech, and biotech. Tel Aviv has a vibrant capital market.

6. Africa

Africa is rich in natural resources but has underdeveloped capital markets. Still, its youthful population and growing middle class present opportunities.

South Africa

The most advanced African economy with a diversified market in mining, finance, and retail. The Johannesburg Stock Exchange (JSE) is the continent’s largest.

Nigeria

Africa’s largest economy, dependent on oil exports, but also growing in fintech (mobile payments, digital banking).

Kenya

A leader in mobile money innovation (M-Pesa) and a gateway to East Africa.

Egypt

Strategically located, with a mix of energy, tourism, and agriculture. Cairo plays an important role in the region’s finance.

Opportunities & Risks Across Regions

Opportunities

Emerging markets (India, Vietnam, Nigeria) offer high growth potential.

Green energy and digital transformation create cross-border investment avenues.

Regional trade blocs (EU, ASEAN, USMCA, AfCFTA) enhance integration.

Risks

Geopolitical conflicts (Russia-Ukraine, U.S.-China tensions)

Currency fluctuations and debt crises in emerging markets

Climate change disrupting agriculture and infrastructure

Inflation and interest rate volatility

Conclusion

Regional and country-specific global markets together form the backbone of the international economic system. While North America and Europe remain financial powerhouses, Asia-Pacific is the fastest-growing engine, the Middle East is transforming from oil dependency to diversification, Latin America is leveraging its resources, and Africa stands as the future growth frontier.

For investors and businesses, the key lies in understanding the unique strengths, weaknesses, and risks of each market while recognizing their global interconnectedness. The future will likely see more multipolarity—where not just the U.S. and Europe, but also China, India, and regional blocs shape the course of the global economy.

Tradingideas

Market Analysis & Risk GloballyPart 1: Foundations of Global Market Analysis

1.1 What is Market Analysis?

Market analysis is the process of studying market conditions to understand demand, supply, pricing, growth potential, and risk. Globally, it covers:

Macroeconomic indicators (GDP growth, inflation, interest rates, unemployment).

Sectoral performance (energy, technology, finance, manufacturing, etc.).

Trade flows (imports, exports, balance of payments).

Capital flows (FDI, portfolio investment, cross-border lending).

Policy frameworks (monetary and fiscal policies, trade agreements, taxation).

Sentiment indicators (consumer confidence, investor sentiment, market volatility).

Global market analysis differs from domestic market study because it requires factoring in cross-border interactions and systemic risks.

1.2 Levels of Global Market Analysis

Macro-Level (Country/Region Analysis)

GDP growth trends.

Sovereign credit ratings.

Fiscal and monetary stability.

Political stability.

Meso-Level (Industry/Sector Analysis)

Technology adoption.

Energy transitions.

Healthcare innovation.

Financial market growth.

Micro-Level (Company/Asset Analysis)

Firm profitability.

Market share.

ESG compliance.

Global supply chain dependencies.

1.3 Drivers of Global Markets

Globalization & Trade Agreements – WTO, regional FTAs, BRICS cooperation.

Monetary Policy Coordination – Fed, ECB, BoJ, PBoC influence liquidity.

Technology & Innovation – AI, blockchain, automation.

Energy Transition – Shift from fossil fuels to renewables.

Demographics – Aging populations in developed nations, young workforce in emerging markets.

Geopolitics – Conflicts, sanctions, alliances, and trade wars.

Part 2: Types of Global Market Risks

2.1 Financial Risks

Currency Risk – Fluctuations in exchange rates. Example: USD strength impacts emerging markets’ debt repayment.

Interest Rate Risk – Rising global rates increase borrowing costs.

Credit Risk – Default risk for sovereign and corporate bonds.

Liquidity Risk – Difficulty in converting assets to cash during crises.

2.2 Economic Risks

Recession Risk – Global slowdowns like the 2008 crisis or 2020 pandemic.

Inflation Risk – High inflation erodes consumer purchasing power.

Commodity Risk – Oil, gold, or food price volatility.

Trade Risk – Tariffs, supply chain disruptions, protectionism.

2.3 Political & Geopolitical Risks

Wars & Conflicts – Russia-Ukraine, Middle East tensions.

Sanctions – U.S. vs China or Iran sanctions impacting trade.

Regulatory Risks – Antitrust rules, tech regulations, ESG norms.

Nationalism & Populism – Rising protectionist policies.

2.4 Environmental & Climate Risks

Climate Change – Extreme weather, rising sea levels.

Energy Transition – Stranded fossil fuel assets.

Carbon Taxes & ESG Pressures – Costs for polluting industries.

2.5 Technological Risks

Cybersecurity Threats – Attacks on financial systems.

Disruption by AI & Automation – Job losses, structural unemployment.

Digital Currency Risks – Volatility of cryptocurrencies and CBDC adoption challenges.

2.6 Systemic Risks

Global Financial Contagion – Domino effects of crises.

Banking Failures – 2008 Lehman Brothers scenario.

Shadow Banking & Derivatives – Hidden risks in opaque markets.

Part 3: Tools & Frameworks for Global Market Analysis

3.1 Fundamental Analysis

GDP, CPI, PMI, balance of trade.

Sovereign bond yields.

Corporate earnings across regions.

3.2 Technical Analysis (Global Indices & Commodities)

Nifty, Dow Jones, FTSE, Nikkei, Shanghai Composite.

Oil, gold, copper, wheat charts.

Volume profile and volatility indexes (VIX).

3.3 Sentiment & Behavioral Analysis

Fear & Greed Index.

Global consumer sentiment surveys.

Hedge fund positioning reports.

3.4 Risk Management Tools

Hedging Instruments: Futures, options, swaps.

Diversification: Across geographies and asset classes.

Value-at-Risk (VaR): Measuring downside risk.

Stress Testing: Scenario analysis of global shocks.

Part 4: Regional Perspectives in Market Risk

4.1 United States

Largest economy, reserve currency issuer.

Risks: Fed tightening, tech regulation, political polarization.

4.2 Europe

Eurozone debt crisis memories.

Brexit aftershocks.

Energy dependency on imports.

4.3 Asia

China: Property crisis, tech crackdown, geopolitical tensions.

India: High growth but vulnerable to oil shocks.

Japan: Aging population, yen volatility.

4.4 Emerging Markets

High growth, high volatility.

Dollar debt risk.

Vulnerability to capital flight.

4.5 Middle East & Africa

Oil dependency.

Political instability.

Transition to non-oil economies.

Part 5: Case Studies of Global Market Risks

5.1 2008 Global Financial Crisis

Trigger: U.S. housing bubble, Lehman Brothers collapse.

Risk lesson: Leverage + complex derivatives = systemic collapse.

5.2 COVID-19 Pandemic (2020)

Trigger: Health crisis turned economic crisis.

Risk lesson: Black swan events can halt global trade overnight.

5.3 Russia-Ukraine War (2022 onwards)

Trigger: Geopolitical conflict.

Risk lesson: Commodity shocks + sanctions reshape supply chains.

5.4 China Property Crisis (Evergrande)

Trigger: Overleveraged real estate.

Risk lesson: Emerging market debt crises have global spillovers.

Part 6: Mitigating Global Market Risks

6.1 For Investors

Diversification across regions.

Use of derivatives for hedging.

Regular portfolio rebalancing.

ESG-aligned investing for long-term resilience.

6.2 For Corporations

Hedging currency & commodity exposure.

Building resilient supply chains.

Geographic diversification of operations.

Cybersecurity investments.

6.3 For Policymakers

Coordinated monetary & fiscal responses.

Transparent regulations.

Climate-resilient policies.

Stronger global institutions (IMF, WTO, G20).

Part 7: Future of Global Market Risks

De-globalization vs. Re-globalization – Supply chains may shorten, but digital globalization accelerates.

Climate Emergency – Strongest long-term risk to global markets.

Rise of Multipolar World – U.S., China, India, and EU competing for dominance.

Digital Finance Expansion – AI, blockchain, CBDCs reshaping finance.

Black Swan Events – Pandemics, cyberwars, or systemic collapses cannot be ruled out.

Conclusion

Global market analysis and risk management are intertwined disciplines. The world economy is no longer a sum of separate markets but a single interconnected system. A shock in one corner—whether it be a pandemic, war, financial collapse, or natural disaster—spreads rapidly across others.

To thrive in such an environment, investors, companies, and governments must adopt dynamic risk management strategies, embrace diversification, and remain vigilant about macro and micro-level changes.

Ultimately, global market analysis is not about predicting the future with certainty but about building resilience against uncertainty.

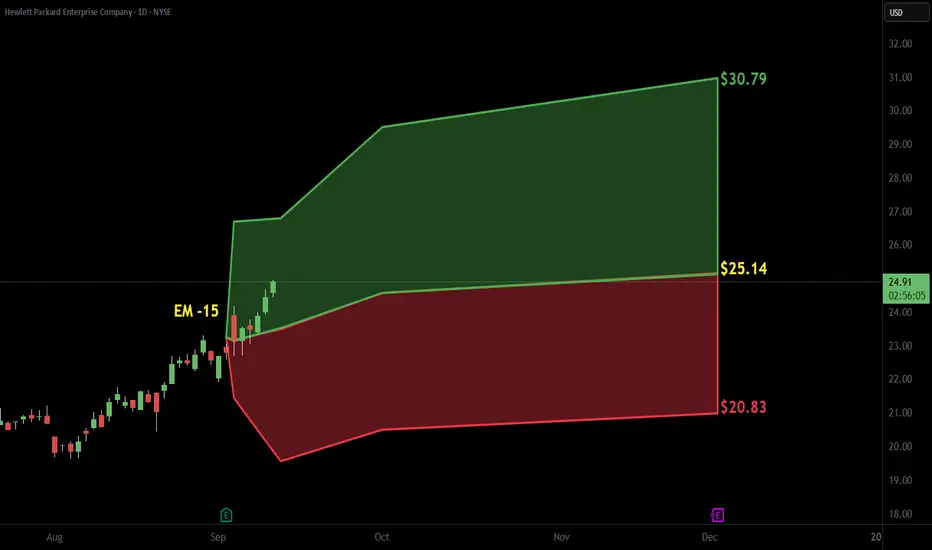

$HPE with a bullish outlook following its earnings #StocksThe PEAD projected a bullish outlook for NYSE:HPE after a positive over reaction following its earnings release, with an expected accuracy of 57.14%.

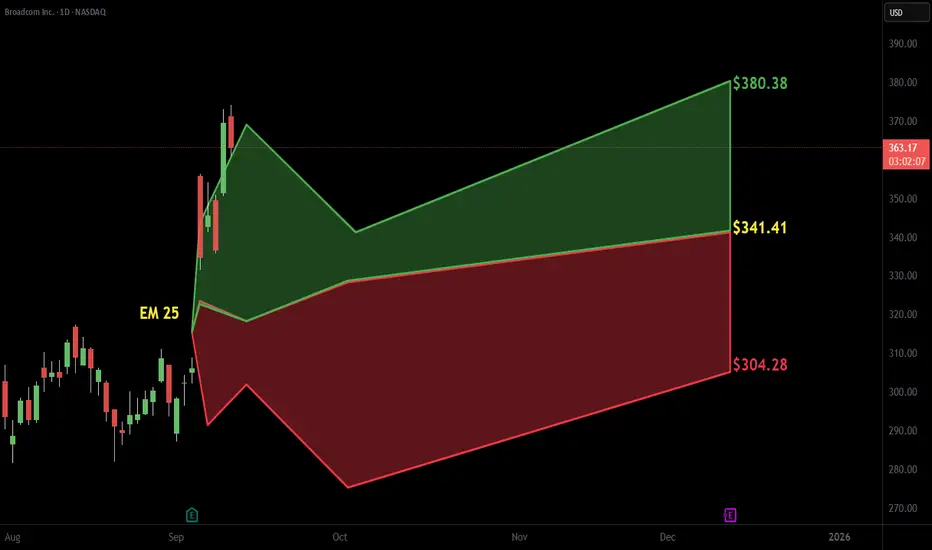

$AVGO with a bullish outlook following its earnings #StocksThe PEAD projected a bullish outlook for NASDAQ:AVGO after a positive over reaction following its earnings release, with an expected accuracy of 84%.

Gold Backing worldwidePart 1: The Origins of Gold as Money

Ancient Civilizations

Gold was used by Egyptians as early as 2600 BCE for jewelry, trade, and as a symbol of wealth.

In Mesopotamia, gold was valued as a unit of exchange in trade agreements.

Ancient Greeks and Romans minted gold coins, which spread across Europe and Asia.

Gold as Universal Acceptance

Because of its rarity, durability, and divisibility, gold became the universal standard of value across cultures. Unlike perishable goods or barter items, gold retained value and was easily transferable. This laid the foundation for gold to back economies centuries later.

Part 2: The Rise of the Gold Standard

19th Century Development

The classical gold standard emerged in the 19th century. Countries fixed their currencies to a certain amount of gold, ensuring stability in exchange rates. For example:

Britain officially adopted the gold standard in 1821.

Other major economies — Germany, France, the U.S. — followed by late 19th century.

How It Worked

Governments promised to exchange paper currency for a fixed quantity of gold.

This restrained governments from printing excessive money, keeping inflation low.

International trade was simplified because exchange rates were fixed by gold parity.

Benefits

Stability of currency.

Encouraged trade and investment.

Limited inflation due to money supply constraints.

Drawbacks

Restricted economic growth during crises.

Countries with trade deficits lost gold, forcing painful economic adjustments.

Part 3: Gold Backing in the 20th Century

World War I Disruptions

Most nations suspended the gold standard to finance military spending.

Post-war, many tried to return, but economic instability weakened confidence.

The Interwar Gold Exchange Standard

A modified version emerged in the 1920s, allowing reserve currencies (like the U.S. dollar and British pound) to be backed by gold.

This proved unstable and collapsed during the Great Depression.

Bretton Woods System (1944 – 1971)

After World War II, a new system was established at the Bretton Woods Conference.

The U.S. dollar became the anchor currency, convertible into gold at $35 per ounce.

Other currencies pegged themselves to the dollar.

This system created a gold-backed dollar world order where gold indirectly supported most global currencies.

Collapse of Gold Convertibility (1971)

In 1971, President Richard Nixon suspended gold convertibility (“Nixon Shock”).

Reasons: U.S. trade deficits, inflation, and inability to maintain gold-dollar balance.

This marked the beginning of fiat currency dominance.

Part 4: Gold’s Role in Modern Economies

Even though direct gold backing ended, gold remains vital:

1. Central Bank Reserves

Central banks worldwide hold gold as part of their foreign exchange reserves.

Provides diversification, stability, and acts as insurance against currency crises.

Major holders include the U.S., Germany, Italy, France, Russia, China, and India.

2. Store of Value & Inflation Hedge

Gold is a safe haven during economic or geopolitical crises.

Investors flock to gold when fiat currencies weaken.

3. Confidence in Currencies

Though fiat currencies are no longer backed by gold, the size of gold reserves adds credibility to a nation’s financial system.

4. Gold-Backed Financial Instruments

Exchange-traded funds (ETFs) backed by gold bullion.

Gold-backed digital currencies (such as tokenized assets on blockchain).

Part 5: Global Gold Reserves – Who Holds the Most?

According to World Gold Council data (2025 estimates):

United States: ~8,133 tonnes (largest holder, ~70% of reserves in gold).

Germany: ~3,350 tonnes.

Italy: ~2,450 tonnes.

France: ~2,435 tonnes.

Russia: ~2,300 tonnes (massively increased in past decade).

China: ~2,200 tonnes (increasing steadily to challenge U.S. dominance).

India: ~825 tonnes (also a large private gold ownership nation).

Smaller nations also hold gold as part of strategic reserves, although percentages vary.

Part 6: Regional Perspectives on Gold Backing

United States

No longer directly gold-backed, but U.S. gold reserves underpin the dollar’s strength.

Fort Knox remains symbolic of America’s monetary power.

Europe

The European Central Bank (ECB) and eurozone nations collectively hold significant gold.

Gold gives the euro credibility as a global reserve currency.

Russia

Increased gold reserves significantly to reduce dependence on the U.S. dollar amid sanctions.

Gold is a strategic geopolitical weapon.

China

Gradually building reserves to strengthen the yuan’s role in global trade.

Gold accumulation aligns with ambitions of yuan internationalization.

India

Holds large reserves at the central bank level and even larger amounts privately.

Gold plays a cultural, economic, and financial safety role.

Middle East

Gulf countries with oil wealth also diversify with gold reserves.

Some are exploring gold-backed digital currencies.

The Future of Gold Backing

Possible Scenarios

Status Quo – Fiat currencies dominate, gold remains a reserve hedge.

Partial Gold Return – Nations introduce partial gold-backing to increase trust.

Digital Gold Standard – Blockchain-based systems tied to gold reserves gain traction.

Multipolar Currency Order – Gold used more in BRICS or Asia-led alternatives to the dollar.

Likely Outcome

While a full gold standard is unlikely, gold’s role as a stabilizer and insurance policy will remain or even grow in uncertain times.

Conclusion

Gold backing has shaped global finance for centuries — from the classical gold standard to Bretton Woods and beyond. Although modern currencies are no longer directly convertible into gold, the metal continues to influence monetary policy, global reserves, and investor behavior. Central banks across the world still trust gold as the ultimate hedge against uncertainty.

In an age of rising geopolitical tensions, inflationary pressures, and digital finance, gold’s importance may even increase. Whether as part of central bank reserves, through gold-backed tokens, or as a foundation for regional trade systems, gold remains deeply woven into the fabric of the global monetary order.

Strategies & Styles in Global TradingPart 1: Foundations of Global Trading Strategies

1.1 Strategic Thinking in Trading

Trading strategies aim to answer three critical questions:

What to trade? (stocks, forex, commodities, indices, crypto, bonds).

When to trade? (entry and exit timing based on analysis).

How much to risk? (position sizing and risk management).

Without a defined strategy, trading becomes speculation driven by emotions.

1.2 Key Influences on Strategy

Global strategies are shaped by:

Market type: Developed (US, EU, Japan) vs. Emerging (India, Brazil, South Africa).

Time horizon: Long-term investments vs. intraday moves.

Information source: Technical analysis, fundamental analysis, quantitative models, or macroeconomic data.

Technology: Algorithmic trading, AI-driven predictions, and blockchain-based platforms.

Part 2: Major Trading Styles

2.1 Day Trading

Definition: Buying and selling within the same day, closing all positions before market close.

Features: Relies on volatility, liquidity, and rapid decision-making.

Tools Used: Intraday charts (1-min, 5-min, 15-min), moving averages, volume profile, momentum indicators.

Global Example: US tech stocks like Tesla or Nvidia are favorite day-trading instruments due to volatility.

Pros: Quick profits, no overnight risk.

Cons: High stress, requires constant monitoring, heavy brokerage costs.

2.2 Swing Trading

Definition: Holding trades for several days or weeks to capture medium-term price swings.

Basis: Combines technical chart patterns with macro/fundamental cues.

Global Example: Trading EUR/USD currency pair during central bank policy cycles.

Pros: Less stressful than day trading, better reward-to-risk ratio.

Cons: Requires patience; risk of overnight news shocks.

2.3 Position Trading

Definition: Long-term strategy, holding positions for months or years.

Basis: Fundamental analysis (earnings, economic cycles, interest rates).

Global Example: Long-term bullish positions in gold as an inflation hedge.

Pros: Less frequent monitoring, aligns with macro trends.

Cons: Requires strong conviction and capital lock-in.

2.4 Scalping

Definition: Ultra-short-term trading strategy, aiming for small profits on many trades.

Basis: Order flow, bid-ask spreads, micro-movements.

Global Example: Forex scalpers trade EUR/USD, GBP/USD due to high liquidity.

Pros: Rapid compounding of profits, no overnight risk.

Cons: High transaction costs, requires lightning-fast execution.

2.5 Algorithmic & Quantitative Trading

Definition: Using computer models, AI, and algorithms to trade automatically.

Methods: Statistical arbitrage, mean reversion, machine learning models.

Global Example: Hedge funds like Renaissance Technologies use quant models to outperform markets.

Pros: Emotion-free, scalable, works 24/7 in multiple markets.

Cons: Requires advanced coding skills, backtesting, and infrastructure.

2.6 High-Frequency Trading (HFT)

Definition: Subset of algorithmic trading using microsecond execution speed.

Basis: Profiting from inefficiencies in order books, arbitrage, spreads.

Global Example: Chicago Mercantile Exchange (CME) futures and US equities.

Pros: Can generate huge volumes of small profits.

Cons: Expensive technology, regulatory scrutiny, highly competitive.

2.7 Event-Driven Trading

Definition: Trading based on news, earnings reports, central bank decisions, or geopolitical events.

Global Example: Buying oil futures after OPEC production cuts; trading GBP during Brexit votes.

Pros: High potential returns.

Cons: High volatility, unpredictable outcomes.

2.8 Arbitrage Strategies

Definition: Profiting from price discrepancies between markets.

Types:

Spatial arbitrage (same asset, different markets).

Triangular arbitrage (currency mismatches).

Merger arbitrage (M&A deals).

Global Example: Simultaneously buying and selling Bitcoin on different exchanges.

Pros: Low-risk if executed correctly.

Cons: Requires speed, capital, and advanced systems.

Part 3: Global Trading Strategies by Asset Class

3.1 Equity Trading Strategies

Value Investing: Buying undervalued stocks (Warren Buffett approach).

Growth Investing: Targeting high-growth sectors like AI or EVs.

Momentum Trading: Riding the wave of strong price trends.

Pairs Trading: Long one stock, short another in the same sector.

3.2 Forex Trading Strategies

Carry Trade: Borrowing in low-interest currency, investing in high-interest currency.

Breakout Trading: Entering positions after a currency breaks key levels.

Range Trading: Buying low, selling high in sideways markets.

News Trading: Trading during central bank announcements or data releases.

3.3 Commodity Trading Strategies

Trend Following: Using moving averages for oil, gold, wheat.

Seasonal Strategies: Trading based on harvests or demand cycles.

Hedging: Producers using futures to lock in prices.

Spread Trading: Buying one commodity and selling another related one (e.g., crude oil vs. heating oil).

3.4 Bond & Fixed Income Trading Strategies

Yield Curve Strategies: Positioning based on steepening or flattening yield curves.

Credit Spread Trading: Exploiting risk premiums between corporate and government bonds.

Duration Hedging: Managing sensitivity to interest rate changes.

3.5 Cryptocurrency Trading Strategies

HODLing: Long-term holding of Bitcoin, Ethereum.

DeFi Yield Farming: Earning interest from decentralized lending protocols.

Arbitrage: Spot vs. futures arbitrage.

Momentum & Volatility Plays: Crypto thrives on extreme price swings.

Part 4: Risk Management & Psychology in Strategies

4.1 Risk Management Tools

Stop-Loss & Take-Profit Orders.

Position Sizing (1–2% capital per trade rule).

Diversification across assets and geographies.

Hedging with options/futures.

4.2 Psychological Styles in Trading

Aggressive vs. Conservative traders.

Discretionary vs. Systematic approaches.

Risk-seeking vs. Risk-averse behaviors.

Trading psychology (discipline, patience, emotion control) often defines whether a strategy succeeds or fails.

Part 5: Regional Differences in Global Trading Styles

US Markets: Heavy focus on tech stocks, options trading, and HFT.

Europe: Strong in forex, bonds, and energy trading.

Asia (Japan, China, India): Retail-dominated, rising algo-trading adoption.

Middle East: Commodity-heavy (oil, petrochemicals).

Africa & Latin America: Emerging markets, currency and commodity-driven.

Part 6: The Future of Global Trading Strategies

AI & Machine Learning: Automated strategies learning from big data.

Blockchain & Tokenization: 24/7 trading, decentralized exchanges.

Sustainable Trading: ESG-based strategies, carbon credits.

Cross-Asset Strategies: Linking equities, commodities, crypto, and derivatives.

Conclusion

Global trading is not just about buying and selling—it is about choosing the right strategy and style that aligns with one’s goals, risk tolerance, and market conditions.

From short-term scalping to long-term investing, from algorithmic arbitrage to macro-driven positioning, traders worldwide adapt strategies to seize opportunities across stocks, currencies, commodities, bonds, and cryptocurrencies.

The winning formula is not a single "best" style—it’s about discipline, adaptability, risk management, and continuous learning. Markets evolve, and so must strategies.

Trading Instruments in global market 1. Equities (Stocks)

Definition

Equities, also called stocks or shares, represent ownership in a company. By buying a share, an investor becomes a partial owner of that company and is entitled to a portion of profits (dividends) and potential capital appreciation.

Key Characteristics

Ownership: A share means holding equity in a company.

Voting rights: Common stockholders can vote in company decisions.

Returns: Gains come from dividends and share price appreciation.

Liquidity: Highly liquid, especially in large stock exchanges like NYSE, NASDAQ, NSE, and LSE.

Types of Equities

Common Stock – Offers voting rights and dividends.

Preferred Stock – Fixed dividends but limited/no voting rights.

Blue-Chip Stocks – Shares of large, stable companies.

Growth Stocks – Companies with high potential for expansion.

Penny Stocks – Low-priced, high-risk speculative shares.

Global Relevance

Equities are among the most popular instruments globally because they allow both short-term trading and long-term wealth creation. For example:

The US stock market is worth over $50 trillion.

Emerging markets like India, Brazil, and China are attracting growing investor interest due to rapid economic growth.

2. Fixed-Income Securities (Bonds)

Definition

A bond is essentially a loan made by an investor to a borrower (government, corporation, or institution). The borrower promises to pay interest (coupon) and return the principal on maturity.

Key Characteristics

Low risk (relative to stocks), especially in government bonds.

Predictable returns in the form of interest.

Variety of maturities (short, medium, and long-term).

Types of Bonds

Government Bonds (Treasuries, Gilts, Sovereign Bonds) – Issued by national governments.

Corporate Bonds – Issued by companies to raise capital.

Municipal Bonds – Issued by cities or states.

High-Yield (Junk) Bonds – Riskier but offer higher returns.

Inflation-Indexed Bonds – Adjust payouts with inflation rates.

Global Relevance

The US Treasury market is the largest bond market in the world and a global benchmark for interest rates.

Countries issue bonds to finance deficits, making them a cornerstone of international trade and finance.

3. Currencies (Foreign Exchange or Forex)

Definition

Currencies are the most liquid instruments globally, traded in the foreign exchange (forex) market, which has a daily turnover of over $7.5 trillion (2025 est.).

Key Characteristics

24-hour trading (Monday–Friday).

High leverage availability for traders.

Paired trading (e.g., USD/INR, EUR/USD, GBP/JPY).

Heavily influenced by macroeconomic policies, central banks, and geopolitics.

Major Currency Pairs

Major Pairs: EUR/USD, GBP/USD, USD/JPY, USD/CHF.

Minor Pairs: EUR/GBP, AUD/JPY.

Exotic Pairs: USD/INR, USD/TRY.

Uses

Businesses hedge against currency fluctuations.

Central banks maintain stability.

Traders speculate on price movements.

4. Commodities

Definition

Commodities are physical goods that are traded on exchanges, often used as raw materials in production.

Types of Commodities

Metals – Gold, Silver, Copper, Platinum.

Energy – Crude Oil, Natural Gas, Coal.

Agricultural Products – Wheat, Coffee, Cotton, Soybeans.

Livestock – Cattle, Hogs.

Key Characteristics

Hedging tool against inflation (gold, oil).

Geopolitical sensitivity (oil prices surge in wars/conflicts).

Global trade-driven demand and supply.

Global Relevance

Oil is the most traded commodity, central to global energy.

Gold acts as a safe-haven asset during economic uncertainty.

Agricultural commodities impact food security and global trade.

5. Derivatives

Definition

Derivatives are contracts whose value is derived from an underlying asset (stocks, bonds, currencies, or commodities).

Types of Derivatives

Futures – Agreements to buy/sell at a future date at a set price.

Options – Rights (not obligations) to buy/sell at a specific price.

Swaps – Contracts to exchange cash flows (e.g., interest rate swaps).

Forwards – Customized contracts between two parties.

Key Characteristics

Used for hedging risk (e.g., airlines hedge fuel prices).

Allow speculation on future price movements.

Offer leverage, amplifying gains/losses.

Global Relevance

The derivatives market is massive—worth quadrillions in notional value.

Exchanges like CME, ICE, and NSE are major global hubs.

6. Exchange-Traded Funds (ETFs) & Mutual Funds

ETFs

Traded like stocks on exchanges.

Track indexes, sectors, or commodities (e.g., SPDR S&P 500 ETF).

Offer diversification at low cost.

Mutual Funds

Actively managed investment vehicles.

Pool money from investors to buy diversified securities.

Suitable for long-term investors.

Global Relevance

ETFs have become highly popular among retail investors.

India and Asia are seeing a surge in passive investing via ETFs.

7. Real Estate Investment Trusts (REITs)

Definition

REITs are companies that own, operate, or finance income-generating real estate (offices, malls, warehouses).

Benefits

Provide exposure to real estate without direct ownership.

Offer dividends from rental income.

Highly liquid compared to physical property.

Global Relevance

REITs are major in the US, Singapore, and Australia, while India has introduced them in recent years for commercial real estate.

8. Hedge Funds & Private Equity Instruments

Hedge Funds

Pool money from wealthy investors to take aggressive positions.

Use derivatives, leverage, and short-selling.

Private Equity (PE)

Invests directly in private companies or buyouts.

Long-term, illiquid, but high potential returns.

Global Relevance

Hedge funds influence markets with speculative bets.

PE drives business growth, restructuring, and IPOs.

9. Cryptocurrencies & Digital Assets

Definition

Cryptocurrencies are decentralized digital currencies using blockchain technology.

Examples

Bitcoin (BTC) – The most popular crypto.

Ethereum (ETH) – Smart contracts and decentralized apps.

Stablecoins (USDT, USDC) – Pegged to fiat currencies.

Central Bank Digital Currencies (CBDCs) – Being developed by governments.

Characteristics

Volatile and speculative.

24/7 global trading.

Used for payments, remittances, and decentralized finance (DeFi).

Global Relevance

Cryptos are gaining institutional acceptance.

Some countries (El Salvador) have adopted Bitcoin as legal tender.

CBDCs could reshape global payment systems.

10. Alternative Trading Instruments

Carbon Credits – Traded to offset emissions.

Weather Derivatives – Used by agriculture/energy companies to hedge risks.

Art & Collectibles – NFTs and physical art as investment assets.

VIX Futures – Trading volatility index as a fear gauge.

Conclusion

The global market is a vast ocean of trading instruments, each serving a distinct purpose. From the stability of bonds to the high-risk-high-reward world of derivatives and cryptocurrencies, these instruments cater to every kind of investor—risk-averse savers, speculative traders, hedging corporates, and long-term wealth builders.

Understanding these instruments is crucial because the modern financial world is deeply interconnected. A shift in interest rates affects bonds, currencies, equities, and commodities simultaneously. Similarly, geopolitical events ripple across forex, oil, and stock markets.

For traders and investors, the key lies in:

Selecting the right mix of instruments.

Managing risks using diversification and hedging.

Staying updated on global economic and geopolitical trends.

In essence, trading instruments are not just tools of profit—they are the lifeblood of the global financial system. Mastering them is mastering the art of navigating global markets.

Global Supply Chain Shifts & Trade RoutesPart 1: Understanding Supply Chains and Trade Routes

What is a Supply Chain?

A supply chain is the complete journey of a product, from sourcing raw materials to manufacturing, distribution, and finally reaching consumers. It includes:

Raw materials (e.g., lithium for batteries, crude oil for fuel).

Manufacturing & assembly (factories, plants, workshops).

Logistics & transport (shipping, trucking, railways, air cargo).

Warehousing & distribution (storage, retail, e-commerce hubs).

End consumers (you and me).

What are Trade Routes?

Trade routes are the physical pathways (land, sea, or air) that connect countries and regions for commerce. Historically, these routes were shaped by geography and politics—like the Silk Road or the Spice Route. Today, they are dominated by major shipping lanes, railways, and digital trade corridors.

Part 2: Historical Evolution of Global Trade Routes

Ancient Trade Networks

Silk Road connected China with Europe, spreading silk, spices, and culture.

Maritime Spice Routes linked India, Southeast Asia, and the Middle East.

Trans-Saharan Routes carried gold, salt, and slaves across Africa.

Colonial Era & Maritime Dominance

European powers built sea empires, controlling trade in spices, tea, and cotton.

The discovery of sea routes around Africa and to the Americas reshaped global trade.

Colonization integrated global economies but created exploitative patterns.

Industrial Revolution & Global Integration

Railways and steamships shortened trade times.

The Suez Canal (1869) and Panama Canal (1914) became game-changers.

New manufacturing hubs emerged, fueling trade growth.

20th Century & Globalization

After World War II, institutions like WTO, IMF, and World Bank promoted open trade.

Containerization in the 1950s revolutionized logistics.

Asia, particularly China, became the world’s factory.

Part 3: Modern Supply Chains – How They Work

Modern supply chains are highly globalized and interdependent. For example:

An iPhone involves design in the U.S., chip production in Taiwan, assembly in China, and raw materials from Africa.

A car may have parts from Germany, software from India, steel from Japan, and be assembled in Mexico.

Features of Modern Supply Chains

Just-In-Time (JIT) Systems – reduce inventory costs but create vulnerabilities.

Multi-Country Production – different stages spread worldwide.

Specialization – each region focuses on what it does best (e.g., Vietnam in textiles, Taiwan in semiconductors).

Speed & Efficiency – enabled by digital tracking, AI, and automation.

Part 4: Major Shifts in Global Supply Chains

Global supply chains are not static. Recent decades have seen shifts driven by multiple forces:

1. Geopolitical Realignments

US-China trade war led to tariffs, restrictions, and diversification.

Countries like Vietnam, India, and Mexico became alternative manufacturing hubs.

New blocs (e.g., BRICS+, ASEAN) are reshaping trade patterns.

2. Pandemic Disruptions

COVID-19 exposed vulnerabilities: shipping delays, factory shutdowns, semiconductor shortages.

“Resilience” became a buzzword, with firms adopting China+1 strategies.

3. Technological Advancements

Automation, AI, and robotics reduce reliance on cheap labor.

Digital supply chains improve tracking and forecasting.

3D printing could localize production.

4. Environmental Pressures

Climate change affects shipping (melting Arctic routes, droughts in Panama Canal).

Push for green supply chains with lower carbon footprints.

ESG regulations are changing corporate strategies.

5. Regionalization & Nearshoring

Companies are moving closer to consumer markets.

Example: U.S. firms shifting from China to Mexico (nearshoring).

Europe considering North Africa and Eastern Europe.

Part 5: Key Global Trade Routes Today

1. Maritime Routes (80% of world trade by volume)

Suez Canal (Egypt) – shortcut between Europe and Asia.

Panama Canal (Central America) – connects Atlantic and Pacific.

Strait of Malacca – vital for oil and goods between Asia & the Middle East.

Strait of Hormuz – critical chokepoint for global oil supply.

2. Land Routes

China’s Belt and Road Initiative (BRI) – massive rail, road, and port infrastructure across Eurasia.

Trans-Siberian Railway – links Europe to Asia.

North-South Transport Corridor (Russia-Iran-India) – an emerging alternative.

3. Air Routes

Used mainly for high-value goods (electronics, medicines, luxury products).

Major hubs: Dubai, Singapore, Hong Kong, Frankfurt, Chicago.

4. Digital Routes

Undersea fiber-optic cables connect internet trade.

Digital trade is growing faster than physical trade.

Conclusion

The world’s supply chains and trade routes are in the middle of a historic transformation. Globalization once pushed for efficiency, low costs, and interconnectedness. Now, resilience, security, sustainability, and regional balance are the new priorities.

The Silk Roads of the past have evolved into today’s digital highways and maritime super-routes. As countries compete for influence, companies adapt strategies, and technologies redefine possibilities, the global supply chain will remain both a driver of prosperity and a barometer of geopolitical shifts.

The coming decades will not eliminate globalization but reshape it—making trade networks more regional, sustainable, and technologically advanced. In this new era, supply chains will not only determine economic success but also shape the balance of global power.

Global Currency Movements (Dollar, Euro, Yen, Yuan)Part 1: The U.S. Dollar (USD) – The Global Kingpin

1.1 Historical Background

The U.S. dollar has been the undisputed global reserve currency since World War II. Before that, the British pound held the crown during the height of the British Empire. But after the Bretton Woods Agreement (1944), the dollar became the anchor of the global monetary system, pegged to gold at $35 per ounce. Even after the Nixon Shock (1971) ended the gold standard, the dollar retained its dominance because of America’s economic size, deep financial markets, and political power.

1.2 Why the Dollar is So Dominant

Reserve Currency Status: Over 58% of global foreign exchange reserves are in USD.

Petrodollar System: Oil and many other commodities are priced and traded in dollars.

Financial Markets: U.S. bond markets are the deepest and most liquid, attracting global investors.

Military and Political Power: The U.S. exerts influence through sanctions, trade deals, and global institutions.

1.3 Movements of the Dollar

The dollar index (DXY) tracks the USD against a basket of currencies (EUR, JPY, GBP, CAD, SEK, CHF). It rises during:

Tight U.S. monetary policy (higher interest rates attract foreign capital).

Global crises (investors flee to dollar as a safe-haven).

Weakness in other currencies (especially Euro and Yen).

It falls during:

Loose monetary policy (printing money, quantitative easing).

High U.S. deficits and debt concerns.

Strong growth abroad (capital flows shift to emerging markets).

1.4 Impact of Dollar Movements

Strong Dollar: Bad for U.S. exporters, good for U.S. consumers (cheaper imports). Hurts emerging markets with dollar-denominated debt.

Weak Dollar: Boosts U.S. exports, fuels inflation at home, but supports global liquidity.

Part 2: The Euro (EUR) – The Challenger

2.1 Birth of the Euro

The Euro was launched in 1999 as a bold project of European integration. Today, 20 of 27 EU nations use the Euro, making it the second-most traded currency after the dollar.

2.2 Strengths of the Euro

Large Economy: The Eurozone has a GDP close to the U.S.

Trade Power: Europe is a major exporter of machinery, luxury goods, and chemicals.

Reserves: Around 20% of global reserves are in euros.

2.3 Weaknesses of the Euro

Lack of Fiscal Unity: Different countries, different budgets, but one currency.

Debt Crises: The 2010–2012 Eurozone debt crisis (Greece, Italy, Spain) exposed structural flaws.

Political Tensions: Brexit and rising nationalism pose risks.

2.4 Euro Movements

The euro’s value against the dollar (EUR/USD) is the world’s most traded currency pair. It rises when:

The European Central Bank (ECB) raises rates.

Europe has strong trade surpluses.

Dollar weakens due to U.S. deficits.

It falls when:

Debt crises or recessions hit Europe.

Energy shocks raise import costs (Europe imports lots of oil & gas).

ECB follows looser monetary policy compared to the Fed.

2.5 Impact of Euro Movements

Strong Euro: Hurts European exports but reduces import costs.

Weak Euro: Boosts exports but fuels inflation (especially energy prices).

Part 3: The Japanese Yen (JPY) – The Safe Haven

3.1 Historical Role

Japan became a global economic powerhouse in the 1970s–80s. The yen was seen as a strong currency due to Japan’s trade surpluses, technological dominance, and manufacturing exports.

3.2 Why Yen is a Safe Haven

High Current Account Surplus: Japan consistently exports more than it imports.

Political Stability: Despite slow growth, Japan is politically stable.

Low Inflation: The yen has maintained purchasing power compared to many currencies.

3.3 Yen Movements

The yen is often linked to carry trades:

Japan keeps ultra-low interest rates.

Investors borrow cheaply in yen and invest in higher-yielding assets abroad.

When global risk sentiment worsens, investors unwind trades, repurchasing yen → yen strengthens.

So the yen tends to:

Strengthen in crises (safe-haven flows).

Weaken when global markets are bullish (carry trades flourish).

3.4 Impact of Yen Movements

Strong Yen: Hurts Japanese exporters like Toyota, Sony, and Panasonic. But lowers import costs (energy, raw materials).

Weak Yen: Helps exporters, boosts inflation, but reduces Japanese consumers’ purchasing power.

Part 4: The Chinese Yuan (CNY/RMB) – The Rising Power

4.1 Historical Transformation

Before the 2000s, the yuan was tightly controlled and not relevant globally. But as China opened up, became the world’s factory, and the second-largest economy, its currency gained importance.

In 2016, the IMF included the yuan in its SDR (Special Drawing Rights) basket, alongside the dollar, euro, yen, and pound—cementing its status as a global currency.

4.2 Controlled Currency

Unlike the dollar, euro, or yen, the yuan is not fully free-floating. The People’s Bank of China (PBOC) sets a daily reference rate and allows it to trade within a band.

4.3 Yuan Movements

The yuan rises when:

China’s trade surplus is strong (exports booming).

PBOC supports stability to attract global investors.

Global demand for Chinese bonds and equities grows.

It weakens when:

China faces capital outflows.

U.S. imposes tariffs or sanctions.

Domestic economy slows down (property crisis, low growth).

4.4 China’s Strategy

China actively promotes the yuan in trade (especially with Belt & Road partners). Many oil deals with Russia, Iran, and Middle Eastern countries are increasingly settled in yuan—challenging the petrodollar system.

4.5 Impact of Yuan Movements

Strong Yuan: Makes Chinese exports less competitive but strengthens China’s global financial credibility.

Weak Yuan: Helps exports but risks capital flight and global accusations of “currency manipulation.”

Part 5: Interplay Between Dollar, Euro, Yen, and Yuan

Currencies don’t move in isolation—they interact.

Dollar vs Euro: Often a mirror image. If dollar rises, euro falls (and vice versa).

Dollar vs Yen: Sensitive to Fed and Bank of Japan interest rate policies.

Dollar vs Yuan: Politically charged, linked to U.S.-China trade tensions.

Euro vs Yen/Yuan: Reflects Europe’s role in Asia trade.

These currencies dominate Forex trading:

EUR/USD → most traded.

USD/JPY → second most traded.

USD/CNY → increasingly important.

Conclusion

The U.S. Dollar, Euro, Yen, and Yuan are not just symbols on forex screens—they are reflections of global power, trade, and politics. The dollar remains king, the euro is a strong but fractured challenger, the yen is a safe haven, and the yuan is the ambitious rising star.

Currency movements will continue to shape the global economy—deciding who gains, who loses, and how wealth shifts across borders. For traders, policymakers, and everyday citizens, watching these four currencies is key to understanding the world’s financial heartbeat.

US Federal Reserve Policy & Global Interest RatesPart I: The Role of the Federal Reserve

1. Origin and Mandate

The Federal Reserve was created in 1913 to stabilize the U.S. financial system after frequent banking crises. Today, its core mandate, often referred to as the dual mandate, is:

To maintain price stability (control inflation).

To achieve maximum employment.

Unlike some central banks (e.g., ECB, which focuses mainly on inflation), the Fed balances growth and stability.

2. Policy Tools

The Fed has three primary tools:

Federal Funds Rate (FFR): The short-term interest rate at which banks lend to each other. Adjustments to the FFR ripple through the economy, affecting borrowing costs for mortgages, auto loans, and corporate credit.

Open Market Operations (OMO): Buying or selling government securities to manage liquidity in the financial system.

Reserve Requirements: Minimum reserves banks must hold (rarely changed now).

Since the 2008 financial crisis, new unconventional tools have been added:

Quantitative Easing (QE): Large-scale bond purchases to inject liquidity and lower long-term interest rates.

Forward Guidance: Communicating future policy intentions to shape market expectations.

Part II: How Fed Policy Shapes Global Interest Rates

1. The Dollar’s Dominance

The U.S. dollar is used in over 85% of global foreign exchange transactions and is the world’s leading reserve currency. This means when the Fed changes rates, it directly impacts the global cost of capital.

2. Capital Flows and Emerging Markets

When U.S. interest rates are low, investors look abroad for higher yields, often pouring money into emerging markets (India, Brazil, Indonesia, etc.). When the Fed raises rates, capital tends to flow back into the U.S., pressuring emerging market currencies and raising borrowing costs.

Example: The 2013 Taper Tantrum, when the Fed hinted at reducing QE, triggered massive outflows from emerging markets, weakening their currencies and forcing many to raise domestic interest rates to protect stability.

3. Global Bond Yields

U.S. Treasury bonds are the global benchmark for “risk-free” assets. If U.S. yields rise (due to Fed tightening), global bond yields also tend to rise as investors demand comparable returns. This impacts corporate debt, mortgages, and sovereign bonds worldwide.

4. Exchange Rates and Trade

Higher U.S. rates make the dollar stronger. This hurts exporters in countries like Japan, South Korea, and India (whose currencies weaken), but helps U.S. consumers by making imports cheaper.

Part III: Historical Case Studies

1. The Volcker Era (1979–1987)

Paul Volcker, then Fed Chairman, famously raised interest rates to nearly 20% to combat runaway inflation. This caused a U.S. recession but restored price stability. Globally, developing nations faced debt crises because their dollar-denominated loans became unpayable at higher rates.

2. Dot-Com Bubble and 2001 Recession

After the dot-com crash, the Fed cut rates sharply to support the economy. Low global interest rates encouraged borrowing and fueled asset bubbles in housing markets around the world.

3. 2008 Global Financial Crisis

The Fed slashed rates to near zero and launched QE. This flooded the world with cheap liquidity, boosting global markets but also encouraging excessive risk-taking in emerging economies.

4. 2013 Taper Tantrum

When the Fed signaled an end to QE, global markets panicked. Emerging market currencies crashed, and many central banks had to raise interest rates defensively.

5. COVID-19 Pandemic (2020–2022)

The Fed again cut rates to zero and launched massive QE, injecting trillions into the system. This stabilized markets but also fueled inflation globally.

6. Inflation and Rate Hikes (2022–2024)

As inflation surged to multi-decade highs, the Fed raised rates aggressively from near zero to over 5%. This had global consequences:

Borrowing costs rose worldwide.

Currencies like the Indian Rupee and Japanese Yen weakened.

Dollar-denominated debt in developing nations became more expensive.

Part IV: Global Interdependence of Interest Rates

1. Major Central Banks and Fed Influence

ECB (Eurozone): Often follows Fed moves but balances inflation with fragile growth in southern Europe.

BoJ (Japan): Maintains ultra-low rates due to deflationary pressures, but Fed hikes force it to intervene to protect the yen.

PBoC (China): Sets its own path but faces currency depreciation when the Fed tightens.

RBI (India): Often compelled to adjust policy to stabilize the rupee and control imported inflation when Fed acts.

2. Interest Rate Differentials

Investors exploit differences between U.S. and global rates through carry trades (borrowing in low-yielding currencies like yen, investing in higher-yielding assets). Fed policy shifts can reverse these flows quickly, destabilizing markets.

3. Debt Vulnerability

Many emerging nations borrow in U.S. dollars. When Fed hikes occur:

Dollar strengthens.

Debt servicing costs rise.

Sovereign default risks increase (e.g., Sri Lanka in 2022).

Part V: Current Global Dynamics (2024–2025 Context)

High U.S. Rates: As of 2025, Fed policy remains restrictive, keeping rates elevated to ensure inflation is under control.

Divergence Across Economies:

U.S. and Europe are tightening.

Japan is only slowly exiting negative interest rates.

Emerging markets are balancing between growth and inflation pressures.

Global Debt Stress: Record-high global debt (over $300 trillion) makes the world highly sensitive to Fed policy.

Dollar Liquidity Premium: With global uncertainty, investors continue to seek U.S. assets, reinforcing the Fed’s influence.

Part VI: Risks and Challenges

1. Inflation vs. Recession

The Fed’s challenge is to cool inflation without causing a deep recession. If it overtightens, global growth suffers.

2. Currency Wars

Countries may intervene in foreign exchange markets to protect competitiveness when the dollar strengthens.

3. Financial Stability

High rates can trigger bank collapses (as seen in Silicon Valley Bank 2023) and strain weaker economies.

4. Geopolitical Factors

Wars, trade tensions, and energy crises interact with Fed policy, complicating interest rate alignment globally.

Conclusion

The U.S. Federal Reserve’s policies are the anchor of the global financial system. Whether through rate hikes, cuts, or balance sheet operations, Fed decisions ripple across borders, influencing global interest rates, capital flows, exchange rates, and debt sustainability.

History shows that when the Fed tightens, global borrowing costs rise and emerging markets feel the pinch. When it loosens, liquidity floods the world, sometimes fueling bubbles.

As of 2025, the Fed’s balancing act between inflation control and economic stability continues to define the trajectory of global interest rates. For investors, policymakers, and businesses worldwide, keeping a close eye on the Fed is not optional—it is essential.

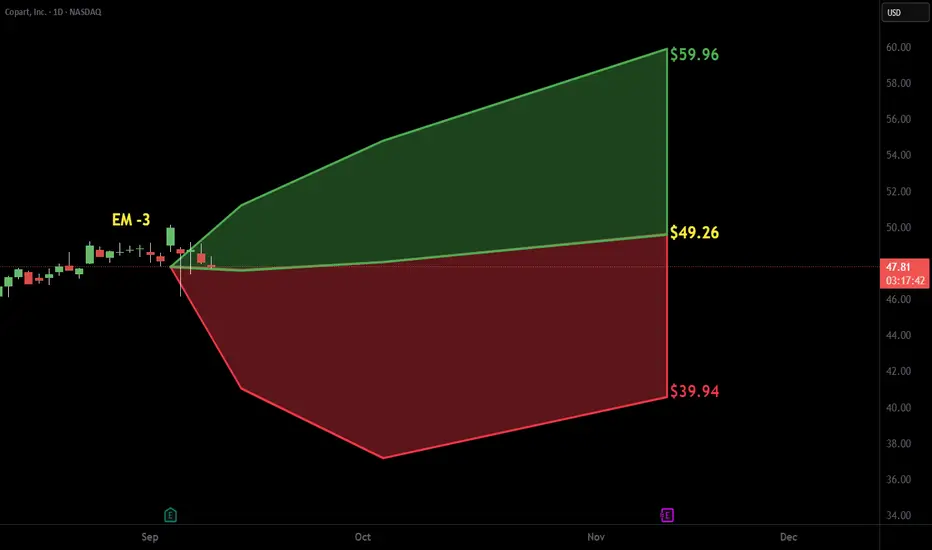

$CPRT with a bullish outlook following its earnings #StocksThe PEAD projected a bullish outlook for NASDAQ:CPRT after a Negative Over Reaction following its earnings release, with an expected accuracy of 70%.

$LULU with a bullish outlook following its earnings #StocksThe PEAD projected a bullish outlook for NASDAQ:LULU after a negative under reaction following its earnings release, with an expected accuracy of 75%.

GOLD WEEKLY CHART MID/LONG TERM ROUTE MAPWeekly Chart Update

Please see update on our weekly chart idea.

Sunday we stated that we had the weekly body close above the channel top at 3576 and now opened the door to the larger 3659 long-term gap target.

- this target is now complete

We will now look for a close above 3659 for a continuation or failure to lock will follow with a rejection into lower levels for support.

🔹 Range Support Levels

3576 and 3482 now act as layered support levels to keep the bullish case intact within this range.

Updated Levels to Watch

📉 Support – 3482 & 3576

Key supports for this new range. Holding above 3576 strengthens the case for continuation toward 3659. A failure back below 3576 puts 3482 into play as the next defensive level.

📈 Resistance – 3732

This becomes the next upside objective if structure holds above 3659.

Thanks as always for your support,

Mr Gold

GoldViewFX

GOLD 4H CHART ROUTE MAP UPDATEHey Everyone,

This is a follow up update on our 4H chart idea that we shared Sunday stating that we still had the final gap in the range left.

EMA5 cross and cross and lock above 3561 left 3615 open.

- This target was hit this week now completing our 4H chart idea.

Keep an eye out for our NEW 4H chart idea with updated levels and route map.

BULLISH TARGET

3424 - DONE

EMA5 CROSS AND LOCK ABOVE 3424 WILL OPEN THE FOLLOWING BULLISH TARGETS

3499 - DONE

EMA5 CROSS AND LOCK ABOVE 3499 WILL OPEN THE FOLLOWING BULLISH TARGET

3561 - DONE

EMA5 CROSS AND LOCK ABOVE 3561 WILL OPEN THE FOLLOWING BULLISH TARGET

3615 - DONE

As always, we will keep you all updated with regular updates throughout the week and how we manage the active ideas and setups. Thank you all for your likes, comments and follows, we really appreciate it!

Mr Gold

GoldViewFX

Dogecoin A potential explosive move is comingWe are currently observing the formation of a Symmetrical Triangle, suggesting the market is coiling up for a significant move.

A bullish breakout to the upside would likely target the upper resistance zone 0.2454 and 0.25593.

In the event of a bearish breakdown, we could see a decline towards the lower support at 0.18940 and 0.14262.

Let’s keep a close eye on this pattern for a confirmed direction.

please note :

this is not financial advice — it reflects only my personal opinion.

PLEASE always do your own research before trading .. Good luck with your trades.

International Payment Systems (SWIFT, CBDCs)Part I: The Evolution of International Payment Systems

1. The Early Days of Cross-Border Payments

Historically, cross-border payments were facilitated through:

Gold and Silver Settlements: Merchants exchanged precious metals, which were universally recognized as stores of value.

Bills of Exchange: Used in medieval trade, these paper instruments allowed merchants to settle accounts without moving physical assets.

Correspondent Banking: In the 19th and 20th centuries, banks built networks of correspondent relationships to settle payments across borders.

These methods were slow, costly, and prone to risks such as fraud, counterparty default, and political instability.

2. The Bretton Woods System and Beyond

After World War II, the Bretton Woods Agreement (1944) created the U.S. dollar–centric system, where the dollar was convertible into gold and became the dominant reserve currency. This system enhanced cross-border payments but still relied heavily on correspondent banks.

Following the collapse of Bretton Woods in 1971, fiat currencies began floating freely, further complicating international payments as exchange rate volatility increased.

3. The Rise of Electronic Payment Systems

The digital era of the late 20th century transformed payments:

CHIPS (Clearing House Interbank Payments System) in the U.S.

TARGET2 in Europe.

Fedwire for domestic U.S. transfers.

SWIFT, which emerged as the global financial messaging system connecting thousands of banks.

Part II: SWIFT – The Backbone of Global Financial Messaging

1. What is SWIFT?

Founded in 1973 and headquartered in Belgium, SWIFT (Society for Worldwide Interbank Financial Telecommunication) is not a payment system itself but a secure messaging network that enables banks and financial institutions worldwide to exchange standardized financial messages.

Key functions include:

Transmitting payment instructions (wire transfers, securities transactions, trade finance documents).

Enabling standardization through message formats (MT/MX messages).

Providing security with encrypted and authenticated communication channels.

2. How SWIFT Works

Participants: Over 11,000 institutions in 200+ countries.

Message Types: SWIFT MT (Message Type) and newer ISO 20022 MX formats.

Process:

A bank initiates a payment request via SWIFT.

The message is sent securely to the counterparty bank.

Actual fund settlement occurs separately through correspondent banking or clearing systems.

3. Why SWIFT Became Dominant

Global Reach: No other network connected as many banks worldwide.

Security: High encryption standards and authentication.

Neutrality: As a cooperative owned by member institutions, SWIFT is not tied to any single nation-state (though geopolitics complicates this claim).

Efficiency: Faster than telex, fax, or older systems.

4. SWIFT’s Economic and Political Significance

Handles millions of messages daily, representing trillions of dollars in transactions.

Acts as a gatekeeper of the international financial system.

Has been used as a tool of geopolitical leverage, with nations being excluded (e.g., Iran, Russia).

5. Limitations of SWIFT

Not instant: Settlement still depends on correspondent banking, which can take 2–5 days.

Expensive: Multiple intermediaries add costs (correspondent bank fees, FX spreads).

Opaque: Hard for individuals and small businesses to track payments in real time.

Geopolitical risk: Heavy influence from the U.S. and EU raises questions of neutrality.

Part III: Central Bank Digital Currencies (CBDCs) and the Future of Payments

1. What are CBDCs?

Central Bank Digital Currencies (CBDCs) are digital forms of sovereign money issued directly by central banks. Unlike cryptocurrencies (Bitcoin, Ethereum) or stablecoins (USDT, USDC), CBDCs are:

Legal tender, backed by the state.

Centralized, controlled by the central bank.

Stable in value, tied to fiat currencies.

CBDCs can be classified into:

Retail CBDCs: For use by the general public (e.g., digital yuan wallet).

Wholesale CBDCs: For interbank and institutional settlements.

2. Motivations for CBDC Development

Central banks globally are exploring CBDCs for reasons including:

Faster and cheaper payments (especially cross-border).

Financial inclusion for unbanked populations.

Reduced reliance on private intermediaries (Visa, Mastercard, SWIFT).

Geopolitical sovereignty (reducing dollar dependency).

Improved monetary policy tools (programmable money, negative rates).

3. CBDCs in Cross-Border Payments

CBDCs offer potential solutions to SWIFT’s limitations:

Instant settlement: Peer-to-peer transfers between central banks.

Lower cost: Eliminates correspondent banking layers.

Transparency: Real-time tracking of payments.

Programmability: Smart contracts for automated compliance.

4. Leading CBDC Projects Worldwide

China: Digital Yuan (e-CNY) already in pilot across multiple cities and tested for cross-border use.

Europe: The European Central Bank is developing a Digital Euro.

India: The Reserve Bank of India launched pilot programs for the Digital Rupee in 2022.

USA: The Federal Reserve is researching a Digital Dollar, though progress is slower.

Multi-CBDC Platforms: Projects like mBridge (BIS, China, UAE, Thailand, Hong Kong) aim to build interoperable cross-border CBDC networks.

Part IV: SWIFT vs. CBDCs – Collaboration or Competition?

1. Will CBDCs Replace SWIFT?

Possibility: If central banks interconnect CBDCs directly, the need for SWIFT messages may decline.

Reality: Transition will be slow; SWIFT’s vast network is difficult to replicate overnight.

2. SWIFT’s Response

SWIFT is experimenting with CBDC interoperability solutions, connecting multiple digital currencies through its network.

Focus on ISO 20022 standardization to ensure compatibility with CBDC systems.

Partnerships with central banks to ensure relevance in the digital era.

3. Coexistence Scenario

In the short to medium term, SWIFT and CBDCs may coexist:

SWIFT remains dominant for traditional bank-to-bank messaging.

CBDCs gain traction for specific corridors, especially in Asia and emerging markets.Part I: The Evolution of International Payment Systems

1. The Early Days of Cross-Border Payments

Historically, cross-border payments were facilitated through:

Gold and Silver Settlements: Merchants exchanged precious metals, which were universally recognized as stores of value.

Bills of Exchange: Used in medieval trade, these paper instruments allowed merchants to settle accounts without moving physical assets.

Correspondent Banking: In the 19th and 20th centuries, banks built networks of correspondent relationships to settle payments across borders.

These methods were slow, costly, and prone to risks such as fraud, counterparty default, and political instability.

2. The Bretton Woods System and Beyond

After World War II, the Bretton Woods Agreement (1944) created the U.S. dollar–centric system, where the dollar was convertible into gold and became the dominant reserve currency. This system enhanced cross-border payments but still relied heavily on correspondent banks.

Following the collapse of Bretton Woods in 1971, fiat currencies began floating freely, further complicating international payments as exchange rate volatility increased.

3. The Rise of Electronic Payment Systems

The digital era of the late 20th century transformed payments:

CHIPS (Clearing House Interbank Payments System) in the U.S.

TARGET2 in Europe.

Fedwire for domestic U.S. transfers.

SWIFT, which emerged as the global financial messaging system connecting thousands of banks.

Part II: SWIFT – The Backbone of Global Financial Messaging

1. What is SWIFT?

Founded in 1973 and headquartered in Belgium, SWIFT (Society for Worldwide Interbank Financial Telecommunication) is not a payment system itself but a secure messaging network that enables banks and financial institutions worldwide to exchange standardized financial messages.

Key functions include:

Transmitting payment instructions (wire transfers, securities transactions, trade finance documents).

Enabling standardization through message formats (MT/MX messages).

Providing security with encrypted and authenticated communication channels.

2. How SWIFT Works

Participants: Over 11,000 institutions in 200+ countries.

Message Types: SWIFT MT (Message Type) and newer ISO 20022 MX formats.

Process:

A bank initiates a payment request via SWIFT.

The message is sent securely to the counterparty bank.

Actual fund settlement occurs separately through correspondent banking or clearing systems.

3. Why SWIFT Became Dominant

Global Reach: No other network connected as many banks worldwide.

Security: High encryption standards and authentication.

Neutrality: As a cooperative owned by member institutions, SWIFT is not tied to any single nation-state (though geopolitics complicates this claim).

Efficiency: Faster than telex, fax, or older systems.

4. SWIFT’s Economic and Political Significance

Handles millions of messages daily, representing trillions of dollars in transactions.

Acts as a gatekeeper of the international financial system.

Has been used as a tool of geopolitical leverage, with nations being excluded (e.g., Iran, Russia).

5. Limitations of SWIFT

Not instant: Settlement still depends on correspondent banking, which can take 2–5 days.

Expensive: Multiple intermediaries add costs (correspondent bank fees, FX spreads).

Opaque: Hard for individuals and small businesses to track payments in real time.

Geopolitical risk: Heavy influence from the U.S. and EU raises questions of neutrality.

Part III: Central Bank Digital Currencies (CBDCs) and the Future of Payments

1. What are CBDCs?

Central Bank Digital Currencies (CBDCs) are digital forms of sovereign money issued directly by central banks. Unlike cryptocurrencies (Bitcoin, Ethereum) or stablecoins (USDT, USDC), CBDCs are:

Legal tender, backed by the state.

Centralized, controlled by the central bank.

Stable in value, tied to fiat currencies.

CBDCs can be classified into:

Retail CBDCs: For use by the general public (e.g., digital yuan wallet).

Wholesale CBDCs: For interbank and institutional settlements.

2. Motivations for CBDC Development

Central banks globally are exploring CBDCs for reasons including:

Faster and cheaper payments (especially cross-border).

Financial inclusion for unbanked populations.

Reduced reliance on private intermediaries (Visa, Mastercard, SWIFT).

Geopolitical sovereignty (reducing dollar dependency).

Improved monetary policy tools (programmable money, negative rates).

3. CBDCs in Cross-Border Payments

CBDCs offer potential solutions to SWIFT’s limitations:

Instant settlement: Peer-to-peer transfers between central banks.

Lower cost: Eliminates correspondent banking layers.

Transparency: Real-time tracking of payments.

Programmability: Smart contracts for automated compliance.

4. Leading CBDC Projects Worldwide

China: Digital Yuan (e-CNY) already in pilot across multiple cities and tested for cross-border use.

Europe: The European Central Bank is developing a Digital Euro.

India: The Reserve Bank of India launched pilot programs for the Digital Rupee in 2022.

USA: The Federal Reserve is researching a Digital Dollar, though progress is slower.

Multi-CBDC Platforms: Projects like mBridge (BIS, China, UAE, Thailand, Hong Kong) aim to build interoperable cross-border CBDC networks.

Part IV: SWIFT vs. CBDCs – Collaboration or Competition?

1. Will CBDCs Replace SWIFT?

Possibility: If central banks interconnect CBDCs directly, the need for SWIFT messages may decline.

Reality: Transition will be slow; SWIFT’s vast network is difficult to replicate overnight.

2. SWIFT’s Response

SWIFT is experimenting with CBDC interoperability solutions, connecting multiple digital currencies through its network.

Focus on ISO 20022 standardization to ensure compatibility with CBDC systems.

Partnerships with central banks to ensure relevance in the digital era.

3. Coexistence Scenario

In the short to medium term, SWIFT and CBDCs may coexist:

SWIFT remains dominant for traditional bank-to-bank messaging.

CBDCs gain traction for specific corridors, especially in Asia and emerging markets.

Part V: Risks, Challenges, and Opportunities

1. Risks of CBDCs

Privacy concerns: Central banks could track every transaction.

Cybersecurity threats: Centralized systems are high-value hacking targets.

Financial disintermediation: Banks may lose deposits if individuals prefer CBDCs.

Geopolitical fragmentation: Competing CBDC blocs (U.S.-led vs China-led) could split the financial system.

2. Risks of SWIFT

Sanctions weaponization undermines neutrality.

Inefficiency relative to new technologies.

Exposure to cyberattacks (e.g., Bangladesh Bank heist in 2016).

3. Opportunities

For SWIFT: Remain the global connector by facilitating CBDC interoperability.

For CBDCs: Create a more inclusive, efficient, and sovereign financial system.

For Businesses and Consumers: Faster remittances, lower costs, better transparency.

Conclusion

International payment systems are undergoing one of the most profound transformations since the Bretton Woods era. SWIFT, the dominant global financial messaging system for decades, remains crucial but faces challenges from new technologies and shifting geopolitics. Meanwhile, CBDCs represent both an opportunity and a threat—promising faster, cheaper, and more sovereign payment infrastructures but also raising risks of fragmentation, surveillance, and competition.

The likely future is not a complete replacement of SWIFT by CBDCs, but rather a hybrid system where SWIFT evolves to act as an interoperability layer while CBDCs gain prominence in specific cross-border corridors.

Ultimately, the future of international payments will depend not only on technological innovation but also on political will, global cooperation, and the balance of power among major economies. The contest between SWIFT and CBDCs is not just about efficiency—it is about who controls the financial arteries of the 21st-century global economy.

Shipping, Freight, and Logistics Trading (Baltic Index)1. Foundations of Global Shipping and Freight

1.1 The Role of Shipping in Global Trade

Shipping is the engine of globalization. Over 80% of international trade by volume is carried by sea. Ships transport crude oil, natural gas, coal, iron ore, grains, fertilizers, automobiles, and countless other goods.

Without shipping, modern trade would collapse. It provides:

Cost efficiency: Shipping is the cheapest way to transport large quantities over long distances.

Accessibility: Oceans cover 70% of the earth, linking producers and consumers across continents.

Flexibility: Different vessel types (tankers, bulk carriers, container ships, LNG carriers) handle specific cargo needs.

1.2 Freight: The Price of Shipping

In simple terms, freight is the cost of transporting cargo from one point to another. Freight rates vary depending on:

Type of cargo (dry bulk, liquid, containerized)

Distance and route (short haul vs. long haul)

Vessel size and availability

Market conditions (supply of ships vs. demand for goods)

Freight costs are crucial because they directly affect commodity prices, corporate profits, and inflation worldwide.

1.3 Logistics and Its Broader Scope

While shipping focuses on transport, logistics covers the entire chain: storage, warehousing, customs clearance, last-mile delivery, and supply chain management. Logistics companies such as Maersk, DHL, FedEx, and MSC coordinate multi-modal transport systems that integrate shipping, trucking, rail, and air.

2. The Baltic Exchange and Baltic Index

2.1 History of the Baltic Exchange