Volatility + Momentum Breakout Signals

**Volatility + Momentum Breakout Signals**

---

## 🎯 **Purpose**

This indicator is designed to **identify potential breakout opportunities** — both **bullish** and **bearish** — by combining **volatility expansion** with **momentum direction**.

Breakouts are often more reliable when both volatility and momentum agree. This tool helps detect such alignments early.

---

## 📐 **How It Works**

The indicator uses **3 key components**:

### 1. **Average True Range (ATR)**

* Measures **market volatility** — how wide the price is moving.

* If ATR is **rising**, it means price is swinging more — indicating energy buildup.

### 2. **Bollinger Band Width (BB Width)**

* Measures the **distance between upper and lower Bollinger Bands**.

* If BB Width is **increasing**, the bands are expanding — signaling a possible breakout after a tight range.

### 3. **Relative Strength Index (RSI)**

* Measures **momentum** of price direction.

* If RSI is **above 50 and rising**, the trend is bullish.

* If RSI is **below 50 and falling**, the trend is bearish.

---

## 📈 **Signal Conditions**

### ✅ **Bullish Breakout Signal** (Buy)

* **ATR is rising**

* **BB Width is rising**

* **RSI is above 50 and rising**

🟢 If all three occur, a **Buy Signal** is plotted with a green triangle at the bottom of the chart.

---

### 🚫 **Bearish Breakout Signal** (Sell)

* **ATR is rising**

* **BB Width is rising**

* **RSI is below 50 and falling**

🔴 If all three occur, a **Sell Signal** is plotted with a red triangle at the top of the chart.

---

## 📊 **What Is Plotted**

* **RSI line** with 30, 50, and 70 reference levels.

* **BB Width (%)** — shows how wide the Bollinger Bands are (orange line).

* **ATR** — the actual range of price movement (purple area).

* **Buy/Sell Markers** when conditions align.

---

## 🛠️ **Usage**

This indicator is ideal for:

* **Breakout traders** — to catch sharp price moves.

* **Swing traders** — to identify strong momentum continuation.

* **Volatility-based entry strategies**.

Volatility

Buy/Sell Indicator (RSI, MACD, ATR) v6+Buy Sell indicators based on EMA, Volume and MACD Has buy and sale flag indicators

Fear and Greed Indicator [DunesIsland]The Fear and Greed Indicator is a TradingView indicator that measures market sentiment using five metrics. It displays:

Tiny green circles below candles when the market is in "Extreme Fear" (index ≤ 25), signalling potential buys.

Tiny red circles above candles when the market is in "Greed" (index > 75), indicating potential sells.

Purpose: Helps traders spot market extremes for contrarian trading opportunities.Components (each weighted 20%):

Market Momentum: S&P 500 (SPX) vs. its 125-day SMA, normalized over 252 days.

Stock Price Strength: Net NYSE 52-week highs (INDEX:HIGN) minus lows (INDEX:LOWN), normalized.

Put/Call Ratio: 5-day SMA of Put/Call Ratio (USI:PC).

Market Volatility: VIX (VIX), inverted and normalized.

Stochastic RSI: 14-period RSI on SPX with 3-period Stochastic SMA.

Alerts:

Buy: Index ≤ 25 ("Extreme Fear - Potential Buy").

Sell: Index > 75 ("Greed - Potential Sell").

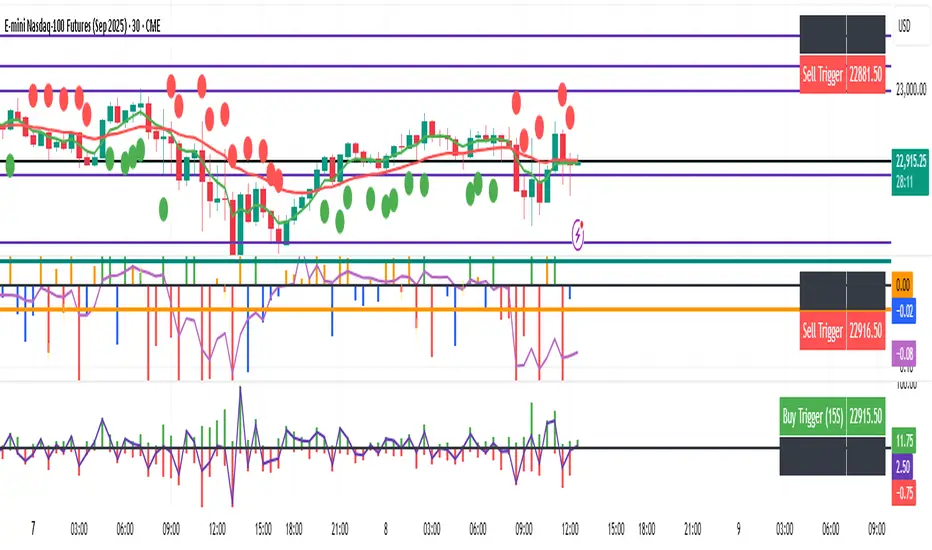

HL/OL Histogram + (Close-Open)🧠 Core Concept

This indicator is designed to detect meaningful directional intent in price action using a combination of:

Intrabar candle structure (high - open, open - low)

Net price momentum (close - open)

Timed trigger levels (frozen buy/sell prices based on selected timeframe closes)

The core idea is to visually separate bullish and bearish energy in the current bar, and to mark the price at which momentum flips from down to up or vice versa, based on a change in the close - open differential.

🔍 Components Breakdown

1. Histogram Bars

Green Bars (high - open): Represent bullish upper wicks, showing intrabar strength above the open.

Red Bars (open - low): Represent bearish lower wicks, showing pressure below the open.

Plotted as histograms above and below the zero line.

2. Close–Open Line (White)

Plots the difference between close and open for each bar.

Helps you visually track when momentum flips from negative to positive, or vice versa.

A bold black zero line provides clear reference for these flips.

3. Buy/Sell Signal Logic

A Buy Trigger is generated when close - open crosses above zero

A Sell Trigger occurs when close - open crosses below zero

These trigger events are one-shot, meaning they’re only registered once per signal direction. No retriggers occur until the opposite condition is met.

📈 Trigger Price Table (Static)

On a signal trigger, the close price from a lower timeframe (15S, 30S, 1, 2, 3, or 5 min) is captured.

This price is frozen and displayed in a table at the top-right of the pane.

The price remains fixed until the opposite trigger condition fires, at which point it is replaced.

Why close price?

Using the close from the lower timeframe gives a precise, decisive reference point — ideal for planning limit entries or confirming breakout commitment.

🛠️ Use Cases

Momentum traders can use the histogram and line to time entries after strong open rejection or close breakouts.

Scalpers can quickly gauge intrabar sentiment reversals and react to new momentum without waiting for candle closes.

Algo builders can use the frozen price logic as precise entry or confirmation points in automated strategies.

High-Low Range % – poslední 2 periodyHere’s a ready-to-use **English description** for publishing your script on TradingView:

---

## 📈 **High-Low Range % – Last 2 Periods**

This indicator calculates and visualizes the **percentage range** between the **High and Low** of the last **two closed periods** (daily, weekly, or monthly – user selectable).

### 🔍 Features:

* Displays the **High–Low range in %** for each of the **two most recent completed candles**.

* **Highlights** the range label if it exceeds a user-defined threshold (e.g., 10%).

* Allows switching between **daily, weekly, or monthly** timeframe bases.

* User controls for:

* Range threshold

* Label color (normal and highlighted)

* Label text size

* Vertical label offset above the High

### ⚙️ Inputs:

* **Timeframe**: Select between `"D"`, `"W"`, or `"M"` to define the range period.

* **Threshold (%)**: If the range exceeds this value, the label changes color.

* **Highlight Color**: Color for ranges above the threshold.

* **Normal Color**: Color for ranges below the threshold.

* **Text Size**: Tiny → Huge label size.

* **Offset**: Distance in ticks to place the label above the period's High.

### 🖼 Visual Output:

* A label placed **just above the High** of the respective candle.

* High and Low levels of the selected period are plotted as horizontal lines.

* Only the **two most recent closed periods** are displayed to keep the chart clean.

---

Let me know if you'd also like a **screenshot description** or **tags** for publication (e.g., `volatility`, `range`, `BTC`, `weekly`, etc.).

Shavarie Gordon’s Phantom Trigger The Phantom Trigger is a precision-engineered confluence indicator developed by Shavarie Gordon — the result of 7 years of trading experience distilled into one clean, powerful tool.

This system filters out noise and focuses only on high-quality trades, combining three powerful elements:

🔹 Momentum Bend Detection – custom logic to detect shifts in directional strength

🔹 Delta Volume Pressure – smoothed order flow showing who’s in control (buyers vs sellers)

🔹 RSI Bend Confirmation – micro-level reversal insight from RSI (length 1 by default)

When all three align, the Phantom Trigger activates:

📈 Line bends up → high-probability buy

📉 Line bends down → high-probability sell

Key Features:

Built for confluence-based traders who want sniper accuracy

Filters out random or weak setups — no low-quality trades

Perfect for scalping, swing, or smart intraday positioning

Lightweight, non-repainting, and easy to read

👑 Final Note:

This tool isn’t for guessing — it’s for traders who wait, confirm, and strike.

Every signal reflects the precision and patience of a 7-year trading journey.

Disclaimer:

This indicator is for educational and informational purposes only and does not constitute financial advice. Use at your own discretion and always apply risk management.

Rob Hoffman IRB Strategy by SniffDog30 Min Bonk Strategy. Not sure if this is beneficial for other tokens/coins. Use at you own risk.

Good strategy for starter in Rob Hoffman style of indicators.

NOTE:

1) Switch to 30 mins

2) adjust to your exchange and quantity of trade

ATR as % of Close (Daily)Sometimes, ATR is more comparable and meaningful when we express it in % rather than dollar. This is a quickly developed version (using ChatGPT), so review it and use it with caution, although the calculation is quite straightforward.

VIX-Price Covariance MonitorThe VIX-Price Covariance Monitor is a statistical tool that measures the evolving relationship between a security's price and volatility indices such as the VIX (or VVIX).

It can give indication of potential market reversal, as typically, volatility and the VIX increase before markets turn red,

This indicator calculates the Pearson correlation coefficient using the formula:

ρ(X,Y) = cov(X,Y) / (σₓ × σᵧ)

Where:

ρ is the correlation coefficient

cov(X,Y) is the covariance between price and the volatility index

σₓ and σᵧ are the standard deviations of price and the volatility index

Enjoy!

Features

Dual Correlation Periods: Analyze both short-term and long-term correlation trends simultaneously

Adaptive Color Coding: Correlation strength is visually represented through color intensity

Market Condition Assessment: Automatic interpretation of correlation values into actionable market insights

Leading/Lagging Analysis: Optional time-shift analysis to detect predictive relationships

Detailed Information Panel: Real-time statistics including current correlation values, historical averages, and trading implications

Interpretation

Positive Correlation (Red): Typically bearish for price, as rising VIX correlates with falling markets. This is what traders should be looking for.

Negative Correlation (Green): Typically bullish for price, as falling VIX correlates with rising markets

How to use it

Apply the indicator to any chart to see its correlation with the default VIX index

Adjust the correlation length to match your trading timeframe (shorter for day trading, longer for swing trading)

Enable the secondary correlation period to compare different timeframes simultaneously

For advanced analysis, enable the Leading/Lagging feature to detect if VIX changes precede or follow price movements

Use the information panel to quickly assess the current market condition and potential trading implications

Non-Repainting RSI 30/70 SignalA simple buy and sell indicator that relies on overbought and oversold areas that you enter whenyou get either a buy or sold signal.

EdgeXplorer - Momentum EngineMomentum Engine by EdgeXplorer

Momentum Engine is a precision-driven oscillator and trend framework engineered to track market momentum with adaptive clarity. Unlike traditional momentum indicators, this engine blends ATR-based envelope logic, multi-mode oscillator scaling, and real-time directional overlays—all in one responsive system.

Designed for intraday traders and swing strategists alike, Momentum Engine offers a streamlined way to visualize momentum direction, impulse strength, and volatility-adaptive trend zones—with minimal noise and maximum context.

⸻

🔍 What Does Momentum Engine Do?

Momentum Engine visualizes market energy through a volatility-aware oscillator and accompanying trend overlays. It adapts dynamically to price behavior and enables traders to:

• Detect momentum waves with real-time visual cues

• Confirm directional bias using trend overlays and impulse zones

• Switch between Regular and Normalized oscillator modes

• See heatmap-based signal confirmation for crossovers

• View optional info panels, labels, and trend bar colors for clarity

It’s a compact yet powerful system built for discretionary and systematic use.

⸻

⚙️ How It Works – Technical Breakdown

1. Trend Envelope Logic

At its core, Momentum Engine constructs a price envelope using:

• The average of the highest closes and highs (Baseline Length)

• The average of the lowest closes and lows

• A multiplied ATR to scale the distance between upper and lower bounds

These bounds determine trend bias:

• Price above the short side of the channel → Bullish

• Price below the long side → Bearish

• In-between → Neutral

A dynamic midline tracks the central channel axis.

2. Oscillator Wave Calculation

The momentum oscillator reacts to price positioning relative to the envelope:

• In Regular Mode, it shows raw price deviation from the trend channel

• In Normalized Mode, it maps price movement into a 0–100 scale with historical scaling logic

Both modes use smoothing (Smoothing) to reduce noise.

3. Overlay Channel (Optional)

• Displays trend floors (bull) and ceilings (bear) on the price chart

• Color-coded trend shifts appear as pulse circles

• Optionally, bars themselves can be recolored for instant trend recognition

4. Heatmap Signal Zones

The background dynamically changes based on oscillator crossovers:

• Bullish signal → Yellow heatmap

• Bearish signal → Blue heatmap

These zones signal momentum ignition, especially helpful for early entries.

⸻

📈 What You See on the Chart

Element Meaning

Green Momentum Wave Bullish pressure (oscillator > midline or >50)

Red Momentum Wave Bearish pressure (oscillator < midline or <50)

Zero Line Base reference in Regular mode

Gray Guide Lines (Normalized) Bands for Overbought (85), Oversold (15), and Neutral (33–50)

Channel Lines Trend bias boundaries (bull/bear zones)

Pulse Marker (Circle) Trend direction change

Bar Colors (Optional) Bull or bear bar overlays for added clarity

Background Heatmap Bullish or bearish impulse confirmation

Info Table (Optional) Real-time trend and oscillator data panel

Debug Labels (Optional) Inline oscillator readings per bar

⸻

📊 Inputs & Settings

Engine Settings

Input Description

Timeframe Optional custom timeframe override

Baseline Length Determines envelope size (larger = smoother trend)

Multiplier Factor Controls ATR-based range expansion

Momentum Wave Settings

Input Description

Mode Regular = raw wave, Normalized = 0–100 scaling

Bull/Bear Colors Wave color customization

Line Width & Smoothing Visual clarity adjustments

Overlay Channel

Input Description

Show Overlay Toggle trend ceilings/floors on chart

Channel Colors Separate bull/bear lines

Trend Bar Color Recolors candle bodies based on trend bias

Signal Heatmap

Input Description

Enable Heatmap Background impulse shading toggle

Bull / Bear Colors Adjust visual tone of crossover zones

Add-ons

Input Description

Show Debug Labels View oscillator values at each bar

Show Info Panel Display current trend, oscillator value, and mode

⸻

🧠 How to Use Momentum Engine

Regular Mode

• Oscillator above 0 = Bullish bias

• Oscillator below 0 = Bearish bias

• Use zero line as your confirmation threshold

Normalized Mode

• 85 → Overbought / exhaustion

• <15 → Oversold / reversal watch

• Crossing 50 → Momentum ignition

• 33–50 → Neutral zone / ranging phase

Visual Interpretation Tips

• Green wave + yellow heatmap = Bull momentum confirmation

• Red wave + blue heatmap = Bear momentum confirmation

• Pulse marker = New trend — evaluate strength with wave slope

• Trend bar coloring = Scan trend alignment at a glance

⸻

🧪 Use Cases & Strategy Ideas

• ⚡ Scalping Impulse Moves

Use oscillator + heatmap crossover to catch directional bursts

• 🔁 Pullback Continuation

Wait for momentum to reset near neutral zone, then re-enter trend

• 📉 Reversal Triggers

Look for divergence or Normalized wave flipping at extremes

• 🎯 Multi-timeframe Confirmation

Set custom timeframe and layer on top of a higher or lower TF structure

GARCH Volatility [Trading Signals]This is a GARCH-like indicator rather than a full academic GARCH model

Current Strengths:

Current Strengths:

Captures core volatility clustering (alpha + beta)

Provides actionable signals

Lightweight for TradingView

When to Use This vs True GARCH:

Use This For: Real-time trading signals, visual market analysis

Use Full GARCH For: Risk modeling, quantitative research

Buy Sell Magic Rework

A version of the legendary Forex indicator Buy Sell Magic for TradingView, with optional additional filtering in the settings.

A simple yet very effective trend-following tool — I personally used it for trading gold 14 years ago, and it still works great today!

✅ Subscribe to my profile to get new useful Pine Script tools soon!

💡 Want a custom version?

I can build private Pine Script indicators & strategies tailored exactly for you — scalping signals, trend or reversal strategies, custom filters for crypto, forex, stocks, or any pairs you trade.

I can also improve or fix your existing scripts.

If you want a unique, high-quality and profitable tool — contact me anytime!

📩 Telegram 👉 t.me

Time-Specific Volume AverageA volume indicator based on historic volume.

Checks for the average volume in the past few days at the same time of day. This helps you determine when there is truly volume in the markets.

We will see often see sustained volume above the average during a clear trend. If you see spikes in volume without it being sustained above the average, it is very likely that the trend will die off quickly.

This is very helpful in determining whether to trade based on a trend following system, or a range based system.

Settings are below:

Days to average: Number of days to look back(tradingview has limits depending on your plan)

SMA Length: Number of "volume averages" to look at. Keep this at 1 if you want the average volume at the exact moment in the day. If you increase it, will also average in the past few candles of "volume averages".

SMA Multiplier: Multiplies the SMA by this amount(helps to get higher quality trends)

Dynamic Ray BandsAbout Dynamic Ray Bands

Dynamic Ray Bands is a volatility-adaptive envelope indicator that adjusts in real time to evolving market conditions. It uses a Double Exponential Moving Average (DEMA) as its central trend reference, with upper and lower bands scaled according to current volatility measured by the Average True Range (ATR).

This creates a dynamic structure that visually frames price action, helping traders identify areas of potential trend continuation, overextension, or mean reversion.

How It Works

🟡 Centerline (DEMA)

The central yellow line is a Double Exponential Moving Average, which offers a smoother, less laggy trend signal than traditional moving averages. It represents the market’s short- to medium-term “equilibrium.”

🔵 Outer Bands

Plotted at:

Upper Band = DEMA + (ATR × outerMultiplier)

Lower Band = DEMA - (ATR × outerMultiplier)

These bands define the extreme bounds of current volatility. When price breaks above or below them, it can signal strong directional momentum or overbought/oversold conditions, depending on context. They're often used as trend breakout zones or to time exits after extended runs.

🟣 Inner Bands

Plotted closer to the DEMA:

Inner Upper = DEMA + (ATR × innerMultiplier)

Inner Lower = DEMA - (ATR × innerMultiplier)

These are preliminary volatility thresholds, offering early cues for potential expansion or reversal. They may be used for scalping, tight stop zones, or pre-breakout positioning.

🔁 Dynamic Width (Bands are Dynamically Adjusted Per Tick)

The width of both inner and outer bands is based on ATR (Average True Range), which is recalculated in real time. This means:

During high volatility, the bands expand, allowing for wider price fluctuations.

During low volatility, the bands contract, tightening range expectations.

Unlike fixed-width channels or standard Bollinger Bands (which use standard deviation), this per-tick adjustment via ATR enables Dynamic Ray Bands to reduce false signals in choppy markets and remain more reactive during trending conditions.

⚙️ Inputs

DMA Length — Period for the central DEMA.

ATR Length — Lookback used for ATR volatility calculations.

Outer Band Multiplier — Controls sensitivity of extreme bands.

Inner Band Multiplier — Controls proximity of inner bands.

Show Inner Bands — Toggle for plotting the inner zone.

🔔 Alerts

Alert conditions are included for:

Price closing above/below the outer bands (trend momentum or overextension)

Price closing above/below the inner bands (early signs of strength/weakness)

🧭 Use Cases

Breakout detection — Catch price continuation beyond the outer bands.

Volatility filtering — Adjust trade logic based on band width.

Mean reversion — Monitor for snapbacks toward the DEMA after price stretches too far.

Trend guidance — Use band slope and price position to confirm direction.

⚠️ Disclaimer

This script is intended for educational and informational purposes only. It does not constitute financial advice or a recommendation to trade any specific market or security. Always test indicators thoroughly before using them in live trading.

Volatility Zones (STDEV %)This indicator calculates and visualizes the relative price volatility of any asset, expressed as a percentage of standard deviation over a rolling window.

🧠 How it works:

- Calculates rolling standard deviation of price (close) as a percentage of the current price.

- Classifies market into three volatility regimes :

• Low Volatility (≤2%) → Blue zone

• Medium Volatility (2–4%) → Orange zone

• High Volatility (>4%) → Red zone

📊 Why it matters:

Volatility structure reflects the underlying regime of the market — ranging, expanding, or trending. This tool helps traders:

- Spot optimal low-risk entry conditions

- Avoid chop zones or highly erratic moves

- Time breakouts or trend initiations

🛠 Usage:

- Works on any timeframe and instrument

- Adjustable lookback period

- Best used alongside trend filters or entry signals (e.g., SuperTrend, EMAs, etc.)

Convergence [by Oberlunar]

The Convergence Indicator by Oberlunar is a multi-timeframe analysis tool that identifies and visualizes trend convergence across up to 10 configurable timeframes using advanced customizable moving averages, including Hull, OberX (a Hull mod), THMA, EMA, and SMA, with an optional pseudo-Hilbert Transform.

It provides a clear visual overlay through gradual fill areas that highlight bullish and bearish trends while offering a fully configurable dynamic table to monitor live trend states across all selected timeframes with user-defined colors and positioning.

This tool is designed for traders who seek to pinpoint multi-timeframe convergence points to enhance their decision-making process in trend-following and breakout strategies.

Oberlunar 👁️⭐

Adaptive Causal Wavelet Trend FilterThe Adaptive Causal Wavelet Trend Filter is a technical indicator implementing causal approximations of wavelet transform properties for better trend detection with adaptive volatility response.

The Adaptive Causal Wavelet Trend Filter (ACWTF) applies mathematical principles derived from wavelet analysis to financial time series, providing robust trend identification with minimal lag. Unlike conventional moving averages, it preserves significant price movements while filtering market noise through signal processing that i describe below.

I was inspired to build this indicator after reading " Wavelet-Based Trend Identification in Financial Time Series " by In, F., & Kim, S. 2013 and reading about Mexican Hat wavelet filters.

The ACWTF maintains optimal performance across varying market regimes without requiring parameter adjustments by adapting filter characteristics to current volatility conditions.

Mathematical Foundation

Inspired by the Mexican Hat wavelet (Ricker wavelet), this indicator implements causal approximations of wavelet filters optimized for real-time financial analysis. The multi-resolution approach identifies features at different scales and the adaptive component dynamically adjusts filtering characteristics based on local volatility measurements.

Key mathematical properties include:

Non-linear frequency response adaptation

Edge-preserving signal extraction

Scale-space analysis through dual filter implementation

Volatility-dependent coefficient adjustment, which I love

Filter Methods

Adaptive: Implements a volatility-weighted combination of multiple filter types to optimize the time-frequency resolution trade-off

Hull: Provides a causal approximation of wavelet edge detection properties with forward-projection characteristics

VWMA: Incorporates volume information into the filtering process for enhanced signal detection

EMA Cascade: Creates a multi-pole filter structure that approximates certain wavelet scaling properties

Suggestion: try all as they will provide slightly different signals. Try also different time-frames.

Practical Applications

Trend Direction Identification: Clear visual trend direction with reduced noise and lag

Regime Change Detection: Early identification of significant trend reversals

Market Condition Analysis: Integrated volatility metrics provide context for current market behavior

Multi-timeframe Confirmation: Alignment between primary and secondary filters offers additional confirmation

Entry/Exit Timing: Filter crossovers and trend changes provide potential trading signals

The comprehensive information panel provides:

Current filter method and trend state

Trend alignment between timeframes

Real-time volatility assessment

Price position relative to filter

Overall trading bias based on multiple factors

Implementation Notes

Log returns option provides improved statistical properties for financial time series

Primary and secondary filter lengths can be adjusted to optimize for specific instruments and timeframes

The indicator performs particularly well during trend transitions and regime changes

The indicator reduces the need for using additional indicators to check trend reversion

RSI- RSI 8 Level Indicator

- Finally, The Bullish and Bearish 8 Level Power Zone indicator with alerts on each level!

Customize the colors however you like and remember if you need to set alerts you can also do that in the alerts section of the indicator. Just make sure what level the alert is for, and always look out for regular divergence, hidden divergence, and exaggerated divergence using this indicator that goes along with the power zones. :)

- RSI Strategy

Trading Bullish & Bearish Power Zones using regular divergence, hidden divergence, and exaggerated divergence.

P.s.

90, 80, 50, 40 Bullish Power Zones in green

65, 55, 30, 20 Bearish Power Zones in red

Capital Risk OptimizerCapital Risk Optimizer 🛡️

The Capital Risk Optimizer is an educational tool designed to help traders study capital efficiency, risk management, and scaling strategies when using leverage.

This script calculates and visualizes essential metrics for managing leveraged positions, including:

Entry Price – The current market price.

Stop Loss Level – Automatically derived using the 30-bar lowest low minus 1 ATR (default: 14-period ATR), an approach designed to create a dynamic, volatility-adjusted stop loss.

Stop Loss Distance (%) – The percentage distance between entry and stop.

Maximum Safe Leverage – The highest leverage allowable without risking liquidation before your stop is reached.

Margin Required – The amount of collateral necessary to support the desired position size at the calculated leverage.

Position Size – The configurable notional value of your trade.

These outputs are presented in a clean, customizable table overlay so you can quickly understand how position sizing, volatility, and leverage interact.

By default, the script uses a 14-period ATR combined with the lowest low of the past 30 bars, providing an optimal balance between sensitivity and noise for defining stop placement. This methodology helps traders account for market volatility in a systematic way.

The Capital Risk Optimizer is particularly useful as a portfolio management tool, supporting traders who want to study how to scale into positions using risk-adjusted sizing and capital efficiency principles. It pairs best with backtested strategies, and does not directly produce signals of any kind.

How to Use:

Set your desired position size.

Adjust the ATR and lookback settings to fine-tune stop loss placement.

Study the resulting leverage and margin requirements in real time.

Use this information to simulate and visualize potential trade scenarios and capital allocation models.

Disclaimer:

This script is provided for educational and informational purposes only. It does not constitute financial advice and should not be relied upon for live trading decisions. Always do your own research and consult with a qualified professional before making any trading or investment decisions.

PRO Investing - ATR Quant.algo by proinvesting.coATR Quant.algo by PROInvesting.co

A powerful and visually intuitive trend-following system designed to capture high-momentum moves and avoid market chop.

Quant.algo combines a dynamic trend-following EMA with multi-level ATR volatility zones to provide a complete trading framework with clear entry signals, stop-loss levels, and take-profit targets.

Key Features:

Dynamic Trend EMA: A thick baseline that turns Green for uptrends and Red for downtrends. Only trade in the direction of the trend.

Multi-Level ATR Zones: Automatically adapting channels that define ideal zones for entries, stops, and profit-taking.

Volatility Filter: A smart filter that tints the background when volatility is expanding, helping you avoid sideways markets and only trade when the market is ready to move.

Pullback Entry Signals: Clear BUY and SELL arrows appear after a pullback to the EMA, providing high-probability entry points.

Simple Trading Rules:

Go LONG: When the baseline is Green, wait for a Green BUY arrow, and aim for the upper TP Zone. Place your stop below the orange Stop Zone line.

Go SHORT: When the baseline is Red, wait for a Red SELL arrow, and aim for the lower TP Zone. Place your stop above the orange Stop Zone line.

Best For:

Traders: Swing Traders & Position Traders.

Timeframes: 4-Hour (H4) and Daily (D1).

Assets: Trending markets (Indices, Forex, Crypto).

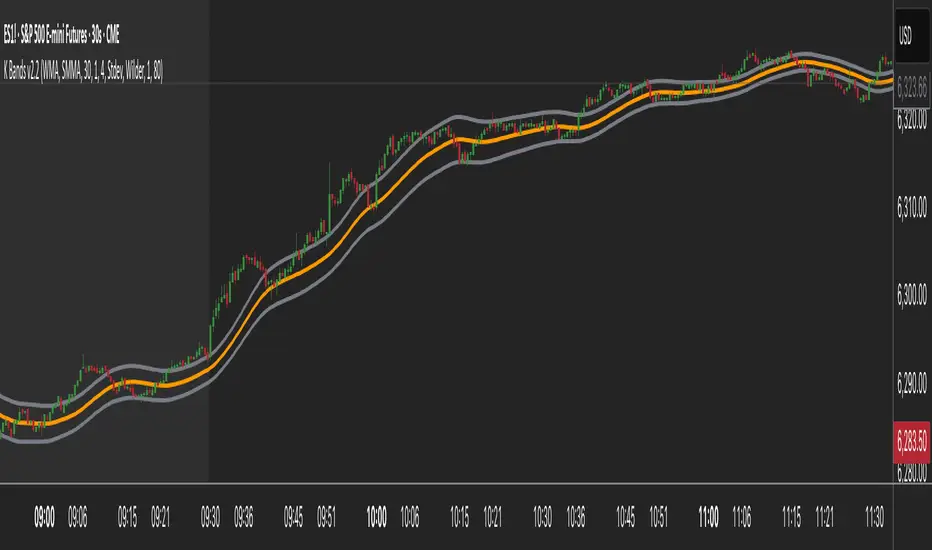

K Bands v2.2K Bands v2 - Settings Breakdown (Timeframe Agnostic)

K Bands v2 is an adaptive volatility envelope tool designed for flexibility across different trading

styles and timeframes.

The settings below allow complete control over how the bands are constructed, smoothed, and how

they respond to market volatility.

1. Upstream MA Type

Controls the core smoothing applied to price before calculating the bands.

Options:

- EMA: Fast, responsive, reacts quickly to price changes.

- SMA: Classic moving average, slower but provides stability.

- Hull: Ultra smooth, reduces noise significantly but may react differently to choppy conditions.

- GeoMean: Geometric mean smoothing, creates a unique, slightly smoother line.

- SMMA: Wilder-style smoothing, balances noise reduction and responsiveness.

- WMA: Weighted Moving Average, emphasizes recent price action for sharper responsiveness.

2. Smoothing Length

Lookback period for the upstream moving average.

- Lower values: Faster reaction, captures short-term shifts.

- Higher values: Smoother trend depiction, filters out noise.

3. Multiplier

Determines the width of the bands relative to calculated volatility.

- Lower multiplier: Tighter bands, more signals, but increased false breakouts.

- Higher multiplier: Wider bands, fewer false signals, more conservative.

4. Downstream MA Type

Applies final smoothing to the band plots after initial calculation.

Same options as Upstream MA.

5. Downstream Smoothing Length

Lookback period for downstream smoothing.

- Lower: More responsive bands.

- Higher: Smoother, visually cleaner bands.

6. Band Width Source

Selects the method used to calculate band width based on market volatility.

Options:

- ATR (Average True Range): Smooth, stable bands based on price range expansion.

- Stdev (Standard Deviation): More reactive bands highlighting short-term volatility spikes.

7. ATR Smoothing Type

Controls how the ATR or Stdev value is smoothed before applying to band width.

Options:

- Wilder: Classic, stable smoothing.

- SMA: Simple moving average smoothing.

- EMA: Faster, more reactive smoothing.

- Hull: Ultra-smooth, noise-reducing smoothing.

- GeoMean: Geometric mean smoothing.

8. ATR Length

Lookback period for smoothing the volatility measurement (ATR or Stdev).

- Lower: More reactive bands, captures quick shifts.

- Higher: Smoother, more stable bands.

9. Dynamic Multiplier Based on Volatility

Allows the band multiplier to adapt automatically to changes in market volatility.

- ON: Bands expand during high volatility and contract during low volatility.

- OFF: Bands remain fixed based on the set multiplier.

10. Dynamic Multiplier Sensitivity

Controls how aggressively the dynamic multiplier responds to volatility changes.

- Lower values: Subtle adjustments.

- Higher values: More aggressive band expansion/contraction.

K Bands v2 is designed to be adaptable across any market or timeframe, helping visualize price

structure, trend, and volatility behavior.

Supertrend AT v1.0📌 Supertrend AT v1.0 — Strategy Overview

Overview

Supertrend AT v1.0 is a fully automated trading strategy based on the Supertrend indicator.

It identifies trend reversals and places long or short entries accordingly, with built-in position sizing, stop-loss/take-profit management, and commission-aware calculations.

🚀 Key Features

✅ Entry Signals Based on Trend Reversals

Long entry when Supertrend changes from downtrend to uptrend

Short entry when Supertrend changes from uptrend to downtrend

✅ Risk-Based Position Sizing

Calculates position size so that a stop-loss only risks a fixed percentage (RPT) of total capital

✅ Reward/Risk Ratio-Based Target Price Calculation

Take-profit price is computed not by price difference, but by actual loss and desired reward-to-risk (RR) ratio

✅ Fully Commission-Aware

Commission is factored into entry, stop-loss, and take-profit price calculations

Ensure commission settings match in both the input panel and the strategy properties tab

✅ Dual Language Support

Switch between English and Korean interface

✅ Visual Trade Levels & Info Display

Entry, stop, and target prices plotted on the chart

Real-time open PnL and equity shown in an on-screen table

⚙️ How to Use

Apply Strategy to Chart

Load the strategy and configure the following parameters in both the Input tab and the Properties tab:

Commission rate (e.g., 0.05%)

Market decimal precision (e.g., 4 for 0.0001)

Adjust Entry Parameters

RPT: Risk per trade as a percentage of your total equity (e.g., 2%)

RR: Reward-to-risk ratio (e.g., 3 = target profit is 3× the potential loss)

Choose whether to allow Long or Short trades

For Auto-Trading Integration

Make sure the minimum order size is valid for your exchange

If the calculated quantity is below the exchange's minimum unit, it may result in errors

⚠️ Important Notes

❗ Non-Repainting — Supertrend is based on confirmed candles and does not repaint

❗ Backtest-Only — The strategy is for signal generation only and does not execute real trades without external automation

❗ Margin-Based Calculations — Default settings assume margin trading; adjust accordingly

📄 License & Disclaimer

This strategy is licensed under the Mozilla Public License 2.0.

This script is not financial advice. Use at your own risk.

Always test thoroughly with backtesting and paper trading before using in live markets.