Cloudflare: The Edge AI Infrastructure PowerhouseCloudflare recently shattered Q4 2025 analyst expectations with surging revenue and robust guidance. The company reported significant growth fueled by AI demand. Investors responded with enthusiasm, driving shares higher. Analysts like Guggenheim promptly raised price targets to $140. Cloudflare now stands as a primary beneficiary of the AI infrastructure boom.

The Patent Moat and Technical Edge

Cloudflare dominates the edge computing landscape through relentless innovation. Its proprietary "Workers" platform remains a patent-protected goldmine for the firm. Recent acquisitions of Astro and Human Native expand these technical capabilities. These moves integrate high-performance web development with AI-ready content streams.

The company aggressively secures intellectual property that optimizes global data routing. This patent strategy creates a formidable moat against legacy competitors. Their VMFE templates further streamline developer workflows at the edge. Cloudflare transforms the network into a programmable, intelligent fabric.

Geostrategy and Geopolitical Resilience

Data sovereignty now dictates global technology strategy. Cloudflare’s massive distributed network addresses these geopolitical shifts effectively. They provide localized security in an increasingly fragmented digital world. This geostrategy reduces latency while ensuring strict regulatory compliance.

The company acts as a neutral digital bridge across borders. Their infrastructure protects critical assets against state-sponsored cyber threats. This positioning makes Cloudflare essential to national digital defenses. They turn geopolitical volatility into a structural market advantage.

Industry Trends: The Rise of Agentic AI

Agentic AI represents the next major technological frontier. Cloudflare positions itself as the essential infrastructure for these autonomous agents. Industry trends favor decentralized, low-latency processing for real-time AI. The "Connectivity Cloud" meets this demand by moving compute closer to the user.

They are no longer just a content delivery network. Cloudflare provides the "neurons" for the global AI brain. Large language models require the speed that only edge networks provide. This shift secures Cloudflare’s relevance for the next decade.

Management, Leadership, and Culture

Matthew Prince leads with a clear, long-term vision. The leadership team prioritizes engineering excellence over short-term marketing gains. This culture fosters rapid product development and seamless deployment. They maintain a competitive edge through agile, founder-led decision-making.

Management demonstrates disciplined capital allocation and impressive operational leverage. They successfully transitioned from a self-service model to enterprise dominance. This leadership stability reassures institutional investors during market swings. Their internal culture attracts top-tier talent in a competitive field.

Macroeconomics and Business Model

The SaaS business model delivers high margins and recurring revenue. Upselling existing clients remains a core economic driver for the company. Cloudflare thrives even as businesses tighten their overall budgets. Cybersecurity and AI infrastructure remain non-discretionary expenses for modern firms.

High-tech integration remains their primary engine for economic growth. The company’s "freemium" funnel efficiently captures the next generation of giants. This creates a self-sustaining cycle of growth and market penetration. Cloudflare hedges against inflationary pressures through essential service pricing.

Cybersecurity and the Science of Defense

Cyber threats evolve with increasing speed and terrifying complexity. Cloudflare utilizes advanced machine learning to preempt these sophisticated attacks. Their scientific approach to network traffic analysis remains unparalleled. They turn massive global data sets into actionable security intelligence.

The company thwarts record-breaking DDoS attacks with automated precision. This technical superiority protects the fundamental integrity of the internet. By securing the edge, they protect the entire digital ecosystem. Cloudflare remains the definitive shield for the modern enterprise.

Aiinfrastructure

DigitalOcean (DOCN) — AI-Native Cloud for Developers & StartupsCompany Overview

DigitalOcean NYSE:DOCN is a developer-first cloud riding surging AI infra demand. Its Gradient AI Agentic Cloud simplifies building, deploying, and scaling AI apps—positioning DOCN as a cost-efficient alternative to hyperscalers for startups and SMBs.

Key Catalysts

Explosive AI Momentum: Direct AI revenue more than doubled YoY for 5 straight quarters (Q3’25)—evidence of sticky developer adoption.

Topline Acceleration: Revenue +16% YoY with record ARR increase; management raised 2026 growth outlook to 18–20%.

Partner Ecosystem: Strategic AI partnerships expand model access, tooling, and go-to-market, reinforcing platform pull.

Value Proposition: Simple pricing, lower TCO, and a curated stack for agentic/LLM apps drive share gains vs. complex large-cloud offerings.

Investment Outlook

Bullish above: $45–$46

Target: $80–$82 — supported by sustained AI revenue compounding, raised guide, and a durable niche in SMB/AI-native workloads.

📌 DOCN — the pragmatic AI cloud for builders who want speed, simplicity, and savings.

Palantir - Inverse Head & ShouldersNot the prettiest I seen. But it could do 🧑🏻🚀 Would still have to break the neckline. But I think it could rally with the rest of the stockmarket.

Aussie Bull Run: Why AUD Futures Are the 2026 Trade to WatchThe March 2026 Australian dollar (A6H26) futures have emerged as a premier opportunity for currency traders. As of late December 2025, prices have surged to new contract highs, supported by a perfect storm of technical and fundamental catalysts. For the modern trader, the "Aussie" is no longer just a proxy for copper; it is a sophisticated bet on global technology and fiscal shifts.

Technical Mastery and MACD Momentum

The daily bar chart for A6H26 reveals a textbook bullish trend. Prices recently breached key resistance, establishing a solid floor for further appreciation. Technical analysts point to the Moving Average Convergence Divergence (MACD) , which remains in a strong posture. The MACD line sits comfortably above the signal line, with both trending higher.

The path of least resistance is clearly upward. A sustained move above the. 6729 contract high activates a buy signal for many institutional desks. Traders are now eyeing a primary price objective of 6950 . To manage risk, professional stops are typically placed just below support 6625 , ensuring a disciplined approach to this high-conviction setup.

Macroeconomics: The Fed’s Dovish Pivot

A primary driver for the Australian dollar's strength is the diverging path of global central banks. The U.S. Federal Reserve has transitioned toward a more accommodative stance to support labor markets. Lower U.S. interest rates naturally weigh on the Greenback, making high-yielding currencies like the AUD more attractive to international carry traders.

Conversely, the Reserve Bank of Australia (RBA) maintains a hawkish bias. Persistent domestic inflation and a resilient job market have forced Australian policymakers to keep rates elevated. This widening interest rate differential acts as a powerful magnet for global capital, fueling the "long Aussie" trade into 2026.

Geostrategy: Powering the AI Revolution

Australia’s geostrategy has shifted from traditional mining to securing the "Green and Digital" transition. The nation is a critical supplier of lithium, copper, and rare earths , the literal building blocks of AI data centers and renewable energy. As global demand for computing power explodes, Australia’s trade balance benefits from a structural "AI premium."

Furthermore, the Australian government is aggressively implementing blockchain-based supply chain tech . These innovations reduce friction at the border and enhance the security of resource exports. By leading in "High-Tech Mining," Australia ensures its currency remains a vital asset in the global technological race.

Professional Note: Success in AUD futures requires monitoring both the RBA’s tone and China’s industrial demand. While the technicals suggest a move to .6950, stay alert for any sudden shifts in global risk appetite that could spark short-term volatility.

Can Power Infrastructure Outmaneuver Silicon in the AI Race?The reported SoftBank acquisition of DigitalBridge represents a fundamental shift in the AI value chain from semiconductors to the physical infrastructure that powers them. DigitalBridge's 20.9 gigawatt portfolio positions it as the gatekeeper to AI scaling, addressing what has become the industry's primary bottleneck: grid-connected power capacity. While chip availability has stabilized, the 3-5 year interconnection queue delays and PJM's capacity auction surge from $29 to $329 per megawatt-day reveal that electricity access now dictates competitive advantage. SoftBank's "Project Izanagi," a $100 billion AI semiconductor initiative, requires immediate deployment infrastructure that cannot be built within a commercially viable timeframe, making DigitalBridge's existing "power bank" an irreplaceable strategic asset.

The transaction thesis extends beyond real estate fundamentals to geopolitical positioning in the Sovereign AI era. DigitalBridge's diversified global footprint through Vantage, Switch, and Scala provides the territorial distribution that nation-states increasingly demand for data sovereignty. Switch's Tier 5 Platinum facilities, fortified by over 950 patent claims covering thermal management and security protocols, create a defensible moat around mission-critical government workloads. However, CFIUS scrutiny presents material execution risk; foreign ownership of infrastructure hosting DoD-classified data will likely require operational ring-fencing or potential divestiture of sensitive assets. The regulatory path mirrors SoftBank's Sprint precedent but operates in a heightened national security environment where data centers are now classified alongside telecommunications as critical infrastructure.

Financial markets initially mispriced DigitalBridge as a transitional REIT rather than a utility-grade infrastructure platform, with the stock trading below intrinsic value estimates of $25-35 before the 50% surge. Fee-Related Earnings grew 43% year-over-year in Q3 2025, reflecting institutional capital allocation into digital infrastructure that the market overlooked amid GAAP complexity. The strategic validation extends beyond SoftBank; any acquirer recognizes that replicating 21 GW of secured power capacity would cost multiples of DigitalBridge's enterprise value. Whether the deal consummates or not, the "SoftBank put" has established a valuation floor, signaling that in 2025's AI industrialization phase, land is sold by the megawatt, not the acre.

LUMN: entering important resistance zonePrice held the support zone outlined in the September update and has since followed through in line with the suggested trend structure, now approaching a key mid-term resistance area at 8.40–9.70, where some form of topping behavior might develop.

Further clarity on potential mid-term support zones will emerge once there’s evidence of a top forming. For now, as long as the price remains above key EMAs (8/21 dEMA), upside momentum remains intact, with the potential to reach higher resistance levels — or even stage a blow-off move toward the November 2024 highs.

Chart:

Previously:

On support and upside potential (Sep 29):

Chart:

www.tradingview.com

CleanSpark (CLSK)— Bridging Bitcoin Mining and AI InfrastructureCompany Overview:

CleanSpark, Inc. NASDAQ:CLSK is a leading Bitcoin mining and high-performance computing (HPC) company leveraging sustainable energy to power scalable digital infrastructure—offering investors exposure to both the crypto mining and AI computing sectors.

Key Catalysts:

Strong financial performance: Bitcoin holdings exceed 13,000 BTC, while Q3 2025 revenue surged 90.8% YoY to $198.6M, underscoring robust execution and institutional demand.

AI and HPC expansion: Strategic buildout of Georgia data centers positions CleanSpark at the crossroads of AI and blockchain, tapping into multi-trillion-dollar infrastructure opportunities.

Financial strength: A $500M Bitcoin-backed credit facility enhances liquidity and scalability while maintaining capital discipline and shareholder value.

Investment Outlook:

Bullish above: $17.00–$18.00

Upside target: $38.00–$40.00, driven by AI integration, operational scale, and Bitcoin price leverage.

#CleanSpark #BitcoinMining #AIInfrastructure #HPC #Crypto #SustainableEnergy #Blockchain #Investing #CLSK

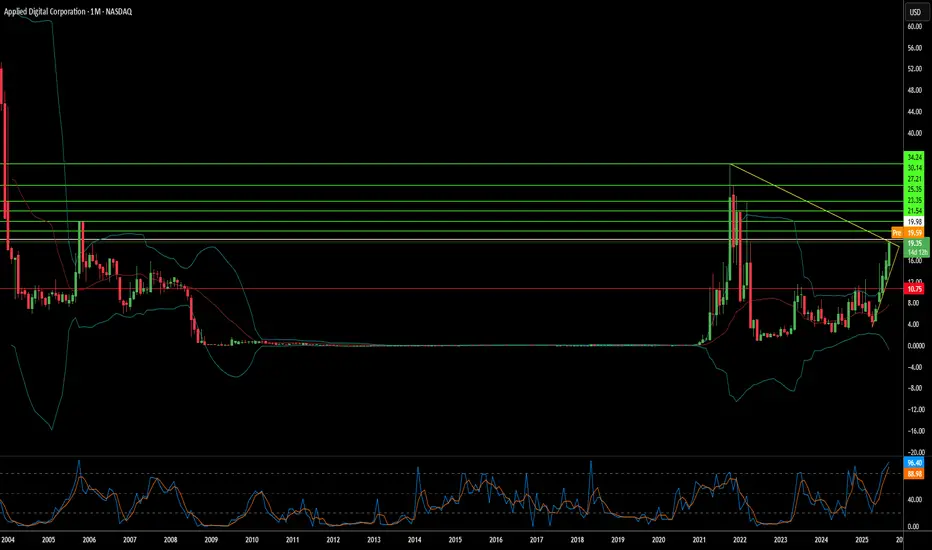

Can a Crypto Miner Become an AI Infrastructure Giant?Applied Digital Corporation has undergone a dramatic transformation, pivoting from cryptocurrency mining infrastructure to become a key player in the rapidly expanding AI data center market. This strategic shift, completed in November 2022, has resulted in extraordinary stock performance with shares surging over 280% in the past year. The company has successfully repositioned itself from serving volatile crypto clients to securing long-term, stable contracts in the high-performance computing (HPC) sector, fundamentally de-risking its business model while capitalizing on the explosive demand for AI infrastructure.

The company's competitive advantage stems from its purpose-built approach to AI data centers, strategically located in North Dakota to leverage natural cooling advantages and access to abundant "stranded power" from renewable sources. Applied Digital's Polaris Forge campus can achieve over 220 days of free cooling annually, significantly outperforming traditional data center locations. This operational efficiency, combined with the ability to utilize otherwise curtailed renewable energy, creates a sustainable cost structure that traditional operators cannot easily replicate through simple retrofitting of existing facilities.

The transformative CoreWeave partnership represents the cornerstone of Applied Digital's growth strategy, with approximately $11 billion in contracted revenue over 15 years for a total capacity of 400 MW. This massive contract provides unprecedented revenue visibility and validates the company's approach to serving AI hyperscalers. The phased buildout schedule, commencing with a 100 MW facility in Q4 2025, provides predictable revenue growth while the company pursues additional hyperscale clients to diversify its customer base.

Despite current financial challenges including negative free cash flow and steep valuation multiples, institutional investors holding 65.67% of the stock demonstrate confidence in the long-term growth narrative. The company's success will ultimately depend on the execution of its buildout plans and ability to capitalize on the projected $165.73 billion AI data center market by 2034. Applied Digital has positioned itself at the intersection of favorable macroeconomic trends, geostrategic advantages, and technological innovation, transforming from a volatile crypto play into a strategic infrastructure provider for the AI revolution.

Credo Technology Group (CRDO) – Powering the AI Data Center BoomCompany Snapshot:

Credo Technology NASDAQ:CRDO is a rising star in AI infrastructure, delivering high-speed, low-power connectivity solutions that are mission-critical to modern data centers.

Key Catalysts:

AI Infrastructure Tailwinds 🧠🏢

Direct exposure to Active Electrical Cables (AEC) and PCIe retimers

Positioned for rapid demand acceleration from AI, cloud, and hyperscale data centers

AEC chip market expected to grow 15x from $68M (2023) to $1B+ by 2028

Sticky Software + Hardware Model 🧩

PILOT software platform offers real-time diagnostics and performance tuning

Enables a recurring revenue model and strengthens customer retention

Scalable, Energy-Efficient Portfolio ⚡🌐

High-bandwidth, low-power design aligns with sustainability goals of large data centers

Integrated solutions are already seeing early adoption momentum

Investment Outlook:

✅ Bullish Above: $51.00–$52.00

🚀 Upside Target: $90.00–$92.00

📈 Growth Drivers: AI infrastructure demand, software expansion, chip market scale

💡 Credo isn’t just riding the AI wave—it’s building the rails for it. #CRDO #AIInfrastructure #Semiconductors

Can Small Reactors Solve Big Energy Problems?Oklo Inc. has recently captured significant attention in the nuclear energy sector, propelled by anticipated executive orders from President Trump to accelerate the development and construction of nuclear facilities. These policy shifts are designed to address the US energy deficit and reduce its reliance on foreign sources for enriched uranium, signaling a renewed national commitment to atomic power. This strategic pivot creates a favorable regulatory and investment environment, positioning companies like Oklo at the forefront of a potential nuclear renaissance.

At the core of Oklo's appeal is its innovative "energy-as-a-service" business model. Unlike traditional reactor manufacturers, Oklo sells power directly to customers through long-term agreements, a strategy lauded by analysts for its potential to generate sustained revenue and mitigate project development complexities. The company specializes in compact, fast, small modular reactors (SMRs) designed to produce 15-50 megawatts of power, ideally suited for powering data centers and small industrial areas. This technology, coupled with high-assay, low-enriched uranium (HALEU), promises enhanced efficiency, extended operational life, and reduced waste, aligning perfectly with the escalating energy demands of the AI revolution and the burgeoning data center industry.

While Oklo remains a pre-revenue company, its substantial market capitalization of approximately $6.8 billion provides a strong foundation for future capital raises with minimal dilution. The company targets the commercial deployment of its first SMR by late 2027 or early 2028, a timeline potentially accelerated by the new executive orders streamlining regulatory approvals. Analysts, including Wedbush, have expressed increasing confidence in Oklo's trajectory, raising price targets and highlighting its competitive edge in a market poised for significant growth.

Oklo represents a high-risk, high-reward investment, with its ultimate success contingent on the successful commercialization of its technology and continued governmental support. However, its unique business model, advanced SMR technology, and strategic alignment with critical national energy and technological demands present a compelling long-term opportunity for investors willing to embrace its speculative nature.

Core Scientific (CORZ) – Mining Bitcoin to Powering AICompany Snapshot:

Core Scientific NASDAQ:CORZ is evolving from a crypto miner into a high-density colocation provider, strategically pivoting into the explosive AI infrastructure space.

Key Catalysts:

Strategic Shift to AI Infrastructure 🧠📡

$1.2B agreement with CoreWeave expands AI compute colocation footprint

Signals institutional validation of CORZ’s infrastructure capabilities

Massive Power Footprint ⚡

1,300 MW capacity across North America

Ideal for power-hungry AI training and inference workloads

AI & HPC Market Tailwinds 🚀

AI infrastructure demand is surging; CORZ is positioned as a first-mover

Colocation demand outpacing supply = pricing power & revenue upside

Transformation Narrative 📈

Transitioning from volatile crypto dependence to stable, high-margin AI hosting

Increased diversification and enterprise appeal

Investment Outlook:

✅ Bullish Above: $8.75–$9.00

🚀 Upside Target: $15.00–$16.00

📈 Growth Drivers: Strategic AI pivot, large-scale power assets, and long-term demand for compute

💡 Core Scientific – No longer just mining blocks, now powering breakthroughs. #CORZ #AIInfrastructure #DigitalTransformation

$SMCI: Super Micro Computer – AI Server Surge or a Pit Stop?

NASDAQ:SMCI : Super Micro Computer – AI Server Surge or a Pit Stop?

AI infrastructure’s hotter than a July barbecue, with revenue up 110% to $14,989.2 million in 2024! But with internal control concerns, is this tech beast charging up or taking a breather? Let’s dive in!

(1/9)

Good morning, everyone! ☀️ NASDAQ:SMCI : Super Micro Computer – AI Server Surge or a Pit Stop?

AI infrastructure’s hotter than a July barbecue, with revenue up 110% to $14,989.2 million in 2024! But with internal control concerns, is this tech beast charging up or taking a breather? Let’s dive in! 🔍

(2/9) – PRICE PERFORMANCE 📊

• Fiscal 2024: Net sales soared 110.4% to $14,989.2 million 💰

• Server Systems: Up 115.9%, GPU servers leading the charge 📏

• Sector Trend: AI demand’s skyrocketing 🌟

It’s a wild ride, fueled by AI’s hunger! ⚙️

(3/9) – MARKET POSITION 📈

• Market Cap: $2.4B, based on shares outstanding 🏆

• Holdings: Servers, storage, and AI solutions ⏰

• Trend: International sales steady at 32%, showing global appetite 🎯

Firm, carving a niche in AI infrastructure! 🚀

(4/9) – KEY DEVELOPMENTS 🔑

• 10-K Filing: Dropped Feb 25, 20

25, dodged NASDAQ delisting 🔄

• Revenue Driver: GPU servers for AI workloads 🌍

• Market Reaction: Shares jumped 19.8% after-hours 📋

Adapting, with investors cheering the comeback! 💡

(5/9) – RISKS IN FOCUS ⚡

• Internal Controls: Audit flagged issues, per Feb 25 filing 🔍

• Competition: Big players in AI server space 📉

• Volatility: High-growth sectors swing hard ❄️

Tough, but risks loom! 🛑

(6/9) – SWOT: STRENGTHS 💪

• Revenue Boom: 110% growth, $14,989.2 million in sales 🥇

• AI Focus: GPU servers crushing it 📊

• Global Reach: 32% international sales 🔧

Got rocket fuel in the tank! 🏦

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES ⚖️

• Weaknesses: Internal control concerns, per audit 📉

• Opportunities: AI infrastructure demand keeps soaring 📈

Can it fix the cracks and ride the wave? 🤔

(8/9) – 📢 SMCI’s revenue up 110%, with AI demand exploding, your take? 🗳️

• Bullish: Shares to $50+ soon, AI’s unstoppable 🐂

• Neutral: Steady, risks balance growth ⚖️

• Bearish: $35 looms, controls spook 🐻

Chime in below! 👇

(9/9) – FINAL TAKEAWAY 🎯

SMCI’s revenue surge to $14,989.2 million screams AI potential 📈, but control issues add a pinch of caution 🌿. Volatility’s our friend—dips are DCA gold 💰. Grab ‘em low, climb like pros! Gem or bust?

Is This $1B Tech Deal the Dawn of a New AI Infrastructure Era?In a move that redefines the landscape of enterprise AI infrastructure, Hewlett Packard Enterprise has emerged victorious in securing a transformative $1 billion deal with X, Elon Musk's social media platform. This landmark agreement represents one of the largest AI server contracts to date and signals a pivotal shift in how major tech companies approach their AI computing needs.

The implications of this deal extend far beyond its monetary value. By outmaneuvering industry titans Dell Technologies and Super Micro Computer in a competitive bidding process, HPE has demonstrated that traditional leaders no longer dominate the AI hardware market. This disruption suggests a new era where technological innovation and cooling efficiency may prove more crucial than established market positions.

The timing of this partnership is particularly significant as it coincides with a dramatic surge in data center infrastructure spending, which reached $282 billion in 2024. HPE's success in securing this contract, despite being considered a relative newcomer in the AI server space, challenges conventional wisdom and opens up intriguing possibilities for future market dynamics. As enterprises worldwide grapple with their AI infrastructure needs, this deal may serve as a blueprint for the next wave of major tech investments, marking the beginning of a new chapter in the evolution of AI computing infrastructure.

F5, Inc. (FFIV) AnalysisCompany Overview:

F5, Inc. NASDAQ:FFIV is a market leader in application delivery and cybersecurity, providing solutions that ensure seamless and secure digital experiences for enterprises globally. The company's evolution from a hardware-centric model to one focused on software and security solutions reflects its agility in adapting to market dynamics and customer needs.

Key Growth Drivers

AI Infrastructure Integration:

F5’s partnership with MinIO, a leading high-performance object storage platform, enhances its presence in the AI infrastructure space.

This collaboration integrates MinIO’s storage capabilities with F5’s advanced traffic management and security solutions, creating a compelling value proposition for enterprises embracing AI and data-intensive workloads.

Shift to Software and Security:

F5’s strategic pivot from hardware to software-driven and security-focused solutions broadens its market reach.

This shift positions F5 to capitalize on increasing enterprise demand for application security, cloud migration, and edge computing.

Strong Financial Foundation:

Recurring Revenue Dominance: 76% of total revenue ($2.1 billion) is now recurring, providing financial stability and predictable cash flows.

Stock Buyback Program: The $1 billion repurchase initiative demonstrates management’s confidence in the company’s growth trajectory and commitment to enhancing shareholder value.

Customer-Centric Innovation:

F5’s solutions are vital for enterprises navigating the complexities of modern multi-cloud environments and ensuring robust cybersecurity for applications.

Investment Outlook

Bullish Case:

We are bullish on F5, Inc. (FFIV) above the $220.00-$222.00 range, given its robust recurring revenue base, strategic partnerships, and expanding market opportunities in cybersecurity and AI infrastructure.

Upside Potential:

Our upside target is $360.00-$365.00, reflecting the company’s ability to sustain long-term growth through innovation, market leadership, and strong financial management.

🚀 FFIV—Redefining Digital Security and Application Delivery in the Age of AI. #Cybersecurity #Cloud #AIInfrastructure