BBAI BigBear ai Holdings Options Ahead of EarningsIf you haven`t bought BBAI before the massive rally:

Now analyzing the options chain and the chart patterns of BBAI BigBear ai Holdings prior to the earnings report this week,

I would consider purchasing the 3usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $1.35.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

BBAI

BBAI - Perfect time for some Options Premiums?I love BBAI from a premiums perspective. It's a great stock to trade for those without a massive amount of capital.

I've been in and out of BBAI for ages. Looking to buy around $3-5 and offloading between $6-8.

It's back on my radar today as it's:

1. bounced off the 200 day moving average

2. touched the bottom trendline

3. The RSI is kind of mimicking the last drop in September.

I'm happy to start adding here, If it bounces, cool. If it drops more, I'll just keep adding.

Low end of short term support looks to be $4 (lots of volume).

Like almost always, I'll be entering this play via options.

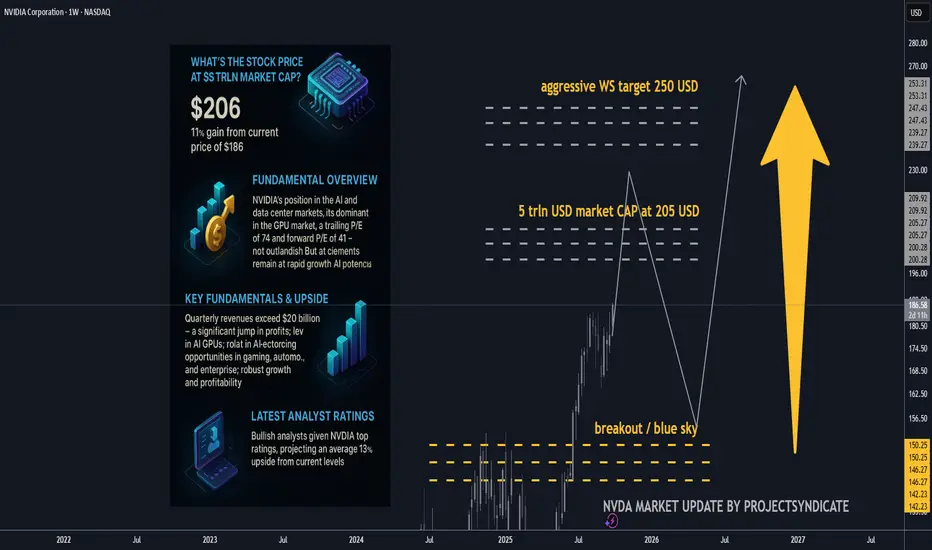

NVDA 5 trln USD market cap up next? Key fundamentals and upside.Is $5T reasonable for NVDA?

• Mechanically, yes: The market only needs ~10% near-term appreciation from today’s levels to print $5T. That’s within one strong quarter or a guidance beat.

• Fundamentally, the math works if (a) FY26–27 revenue tracks the guide/Street trajectory (TTM already $165B with Q3 guide $54B), (b) non-GAAP GMs hover low-to-mid-70s, and (c) opex discipline holds. Under those, forward EPS path supports ~35× at $5T, a premium but not outlandish for a category-defining compute platform.

• Free-cash optionality: With ~$48B net cash and massive FCF, NVDA can keep funding buybacks (already $60B fresh authorization) and capacity, smoothing cycles.

________________________________________

• Stock price at $5T market cap: ≈ $205.8 per share (on ~24.3B shares).

• Gain needed from $186.6: +$19.2 (~+10.3%).

The quick math (market cap ⇒ price)

• Shares outstanding (basic): ~24.3 B (as of Aug 22, 2025, per 10-Q).

• Stock @ $5T market cap: $5,000,000,000,000 ÷ 24.3B ≈ $205.8/share.

• From today’s price $186.6: needs +$19.2 or ~+10.3%.

That also implies P/E (TTM) at $5T of roughly ~56× (using TTM EPS ~3.68). Today’s trailing P/E is ~50–53× depending on feed.

________________________________________

Core fundamentals snapshot 🧩

Latest quarter (Q2 FY26, reported Aug 27, 2025)

• Revenue: $46.7B (+56% y/y; +6% q/q).

• Data Center revenue: $41.1B (+56% y/y).

• GAAP gross margin: 72.4%; non-GAAP 72.7%; Q3 guide ~73.3–73.5%.

• GAAP EPS: $1.08 (non-GAAP: $1.05; excl. $180M inventory release: $1.04).

TTM scale & profitability

• Revenue (TTM): ~$165.2B.

• Net income (TTM): ~$86.6B.

• Diluted EPS (TTM): ~$3.5–3.7.

• Cash & marketable securities: $56.8B; debt: ~$8.5–10.6B ⇒ net cash ≈ $48B.

Capital returns

• $24.3B returned in 1H FY26; new $60B buyback authorization (no expiration). Remaining buyback capacity ~$71B as of Aug 26.

________________________________________

Valuation read (today vs. $5T)

Using widely watched metrics:

• P/E (TTM): ~50–53× today; at $5T it rises to ~56× (assuming flat TTM EPS).

• Forward P/E: Street FY27 EPS ≈ $5.91 → ~31–33× today; ~35× at $5T — still below many AI hyper-growth narratives that trade at 40–50× forward when growth visibility is high.

• EV/EBITDA (TTM): EV ≈ market cap – net cash. Today EV ~$4.45T; EBITDA TTM ≈ $98–103B ⇒ EV/EBITDA ~43–45×; at $5T EV/EBITDA drifts to ~48–50×.

• P/S (TTM): ~27× today (at $4.5T) and ~30× at $5T on $165.2B TTM revenue.

• FCF yield: TTM FCF range $60.9–72.0B ⇒ ~1.35–1.60% today; ~1.22–1.44% at $5T.

Takeaway: $5T doesn’t require a heroic repricing — it’s ~10% above spot and implies ~35× forward earnings if consensus holds. That’s rich vs. the S&P (~22.5× forward) but arguably reasonable given NVDA’s growth, margins, and quasi-platform status in AI compute.

________________________________________

What must be true to justify $5T (and beyond) ✅

1. AI capex “supercycle” persists/expands. Citi now models $490B hyperscaler AI capex in 2026 (up from $420B) and trillions through 2029–30. A sustained 40–50% NVDA wallet share across compute+networking underwrites revenue momentum and margin sustainment.

2. Annual product cadence holds. Blackwell today → Rubin in 2026 with higher power & bandwidth, widening the perf gap vs. AMD MI450 — supports pricing power and mix.

3. Margins stay “mid-70s” non-GAAP. Company guides ~73.3–73.5% near term; sustaining 70%+ through transitions offsets any unit price compression.

4. Networking, software & systems scale. NVLink/Spectrum, NVL systems and CUDA/Enterprise subscriptions deepen the moat and smooth cyclicality; attach expands TAM (improves EV/EBITDA vs. pure-GPU lens).

5. China/export workarounds do not derail mix. Q2 had no H20 China sales; guidance and commentary frame this as manageable with non-China demand and limited H20 redirection.

________________________________________

A contrarian check (where the model could break) 🧨

• Power & grid bottlenecks. Even bulls (Citi) note AI buildouts imply tens of GW of incremental power; slippage in datacenter electrification can defer GPU racks, elongating deployments (and revenue recognition).

• Debt-funded AI spend. Rising share of AI DC capex is being levered (Oracle’s $18B bonds; neoclouds borrowing against NVDA GPUs). If credit windows tighten, orders could wobble.

• Customer consolidation & vertical ASICs. Hyperscalers iterating custom silicon could cap NVDA’s mix/price in some workloads; edge inference may fragment.

• China policy volatility. Export rules already forced product pivots; rebounds are uncertain and not fully in NVDA’s control.

• Multiple risk. At ~50× TTM and >40× EV/EBITDA, any growth decel (unit or pricing) can de-rate the multiple faster than earnings make up the gap.

Bottom line of the bear case: If AI capex normalizes faster (say +10–15% CAGR instead of +25–35%), forward EPS still grows, but the stock would likely need multiple compression (toward ~25–30× forward), making $5T less sticky near-term.

________________________________________

Street positioning (latest bullish calls) 📣

• KeyBanc: $250 (Overweight) — Rubin cycle deepens moat → ~+34% implied upside.

• Barclays: $240 (Overweight) — AI infra wave; higher multiple to 35×. ~+29% upside.

• Bank of America: $235 (Buy). ~+26% upside.

• Bernstein: $225 (Outperform). ~+21% upside.

• Citi: $210 (Buy) — reiterates annual cadence & rising AI capex.

• Morgan Stanley: $206–210 (Overweight). ~+11–13% upside; 33× CY25 EPS framework.

• Consensus: Avg 12-mo PT ~$211, ~+13% from here.

________________________________________

________________________________________

Extra color you can trade on 🎯

• Where bulls may be too conservative:

o Networking/NVLink attach could outgrow GPUs as Blackwell/Rubin systems standardize on NVIDIA fabric, defending blended margins longer.

o Software monetization (CUDA ecosystem, NIMs, enterprise inference toolchains) is still under-modeled in many sell-side DCFs.

• Where bulls may be too aggressive:

o China rebound timing & magnitude.

o Power/real-estate constraints delaying deployments into 2026.

o Credit-driven AI capex — watch for any signs of tightening in private credit / neocloud financing that uses GPUs as collateral.

________________________________________

________________________________________

Sources: NVIDIA IR & 10-Q; Yahoo Finance stats; StockAnalysis (TTM financials); company Q2 FY26 press release and CFO commentary; recent analyst notes from KeyBanc, Citi, Barclays, BofA, Morgan Stanley; financial media coverage (WSJ/FT).

BigBear (BBAI) — Expanding AI Leadership in Defense IntelligenceCompany Overview:

BigBear.ai Holdings, Inc. NYSE:BBAI is a leading provider of AI-powered decision intelligence for defense, supply chain, and digital identity markets—offering investors exposure to the rapidly growing AI and analytics sector focused on mission-critical applications.

Key Catalysts:

Defense expansion: New U.S. Navy partnership for UNITAS 2025 and strategic alliance with Tsecond strengthen BigBear.ai’s role in real-time, edge-based AI processing via ConductorOS and BRYCK platforms.

Long-term contracts: Over $178 million in multi-year defense deals provide strong revenue visibility and recurring income stability.

Strategic momentum: Growing adoption across national security agencies underscores BigBear.ai’s position in U.S. defense modernization efforts.

Investment Outlook:

Bullish above: $6.80–$7.00

Upside target: $17.00–$18.00, supported by defense partnerships, scalable AI deployment, and national security demand.

#BigBearAI #ArtificialIntelligence #DefenseTech #NationalSecurity #EdgeComputing #AIAnalytics #Investing #BBAI

Looking for a daytrade on BBAI! OptionsMastery:

🔉Sound on!🔉

📣Make sure to watch fullscreen!📣

Thank you as always for watching my videos. I hope that you learned something very educational! Please feel free to like, share, and comment on this post. Remember only risk what you are willing to lose. Trading is very risky but it can change your life!

My long buy for BigBear AIMy long buy for BigBear AI.

BigBear.ai (BBAI) rose today largely due to a mix of speculative and fundamental factors.

Investors are also reacting positively to the company’s deployment of biometric passenger processing technology at major ports and its positioning to benefit from rising government and defense spending on AI solutions.

Although BigBear.ai’s recent financial results showed revenue declines and reduced guidance, today’s surge reflects strong market optimism about its future opportunities rather than immediate earnings strength.

My Buy View:

Entry: $6.3

Target TP: $9.5

Expected return: approx 50%

Mid to long-term holding: 3 months or more

BBAI HIGH PROBABILITY SETUP SOON!!🚨 BBAI HIGH PROBABILITY BUY SETUP 🚨

* Here We Can See Clearly The Next Potential Move For BBAI Coming Hours/Days.

* Keep Your Eyes Close On Your Trading Positions.

* Happy PIP Hunting Traders.

FXKILLA

BBAI BigBear ai Holdings Options Ahead of EarningsIf you haven`t bought BBAI before the previous earnings:

Now analyzing the options chain and the chart patterns of BBAI BigBear ai Holdings prior to the earnings report this week,

I would consider purchasing the 7usd strike price Calls with

an expiration date of 2025-8-15,

for a premium of approximately $0.77.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Is BigBear.ai the Next Titan of Defense AI?BigBear.ai (NYSE: BBAI) is emerging as a significant player in the artificial intelligence landscape, particularly within the critical national security and defense sectors. While often compared to industry giant Palantir, BigBear.ai carves its niche by intensely focusing on modern warfare applications, including guiding unmanned vehicles and optimizing missions. The company has recently garnered considerable investor attention, evidenced by its impressive 287% rally over the past year and a notable surge in public interest. This enthusiasm stems from several key factors, including a substantial 2.5x increase in backlog orders to $385 million by March 2025 and a significant ramp-up in research and development spending, signaling robust foundational growth.

BigBear.ai's technological prowess underpins its rising profile. The company develops sophisticated AI and machine learning models for diverse applications, from facial recognition systems deployed at major international airports like JFK and LAX to AI-augmented shipbuilding software for the U.S. Navy. Its Pangiam® Threat Detection and Decision Support Platform enhances airport security by integrating with advanced CT scanner technology, while its ConductorOS platform facilitates secure communication and coordination for drone swarm operations under the U.S. Army's Project Linchpin. These cutting-edge solutions position BigBear.ai at the forefront of AI-driven advancements crucial for evolving geopolitical landscapes and increasing defense AI investments.

Strategic collaborations and a favorable market environment further fuel BigBear.ai's ascent. The company recently formed a significant partnership in the UAE with Easy Lease and Vigilix Technology Investment to accelerate AI adoption across key industries like mobility and logistics, marking a major step in its international expansion. Additionally, multiple contracts with the U.S. Department of Defense, including those for J-35 fleet management and geopolitical risk assessment, underscore its vital role in government initiatives. While BigBear.ai faces challenges, including revenue stagnation, escalating losses, and stock volatility, its strategic market position, growing backlog, and continuous innovation in mission-critical AI solutions present a compelling high-risk, high-reward investment opportunity in the burgeoning defense AI sector.

BBAI Breakout Continuation Pattern ConfirmedWe enter BBAI at $5.11 look for confirmation above the $5.20 which we expect to confirm support after consolidation of this morning's breakout (if it even recedes from this point), with a price target of $8.35 which would provide the potential for a ~65% Gain on the potential trade and continuation. We have a stop set for $4.06 on the trade.

This comes after the company announced deploying their Biometric Software at Major US Airports & Ports of Entry, which helped prop up the company's stock to push back to those potential highs to retest the $10.49 even. No company-specific information has been released in the past week.

$BBAI setting up for a monster move! 200% UpsideNYSE:BBAI - If it flagged once, it will flag again...⛳️

🎯$5.20🎯$6.75🎯$9.40

- H5_L Bullish Cross

- Volume Shelf Launch

- WR% Swinging Green to Red 🧲

$BBAI upside targets $8-10?NYSE:BBAI looks set to run higher here. As you can see, we've broken out of the bottoming formation and have now retested support.

As long as we're able to stay above support, we should see a large move higher up to the two resistance levels.

Let's see how high we end up going. Think it's very likely that we end up going to the top of the range.

OptionsMastery: A potential swing on BBAI!🔉Sound on!🔉

📣Make sure to watch fullscreen!📣

Thank you as always for watching my videos. I hope that you learned something very educational! Please feel free to like, share, and comment on this post. Remember only risk what you are willing to lose. Trading is very risky but it can change your life!

BBAI overviewBuy low, sell high. Levels where buyers are happy to buy and sellers are happy to sell. Just connect the dots.

BBAI BigBear ai Holdings Options Ahead of EarningsIf you haven`t bought BBAI before the massive rally:

Now analyzing the options chain and the chart patterns of BBAI BigBear ai Holdings prior to the earnings report this week,

I would consider purchasing the 5.50usd strike price Calls with

an expiration date of 2025-6-20,

for a premium of approximately $1.10.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

No pain no gain. Buy Zone front your eyes. The pain may last for another 3 trading days. No pain no gain. Before the price returns to the $7.50 area and accelerates to the $10.36 peak in March 2026. Open the $7, $8, $9 BUY CALL at any expiration, while they are still cheap.

Tempus Ai is not done yet! 70% UpsideNASDAQ:TEM

Called the DIP, Now calling the RIP!

$115 Inbound! 🎯

- Volume Shelf

- Retesting previous highs to flip into support

- WCB Creating support and bottom

- H5 is GREEN with BUY SIGNAL

- Down on market weakness

Not financial advice

$BBAI back on track to break the $10.00 resistanceAfter the crash in sync with PTLR yesterday due to Trump's Defense spending cuts. If you don't cut losses, and still hold tight, even DCA to load more share below $8.00, especially the $6.80 - $7.00 area. Congratulations! Profits are in sight.

Most of the popular indicator is

Option trading ideas:

Buy Call $10, exp 3/21

Buy Call $11 and $12, exp 4/17

Most popular indicators are supporting this bullish momentum. BUT!!! Watch out for profit-taking pressure near the upcoming ER 3/6. BBAI's valuation is already too high compared to its projected earnings, so be careful!

Disclaimer

$BBAI next target $11 - $12 in the last week of Feb 2025Please see the sample chart I shared. The bullish flag pattern appears once again. So if BBAI can hold the support level of $8.00 - $8.50, it is likely to rise to $11 - $12 in the next push. The most ideal entry point is the price zone of $7.80 - $8.00. However, I am not sure that this can happen when the profit-taking pressure is too strong at the $9.xx area. My confidence level is only 66% for the bullish case. And 33% possibility of a decline to the price zone of $7.00 - $7.50. So, Stop Loss must be setup or hold tight up to you. Good luck Bigbear brothers!

Can AI Weather the Storm of Volatility?BigBear.ai has captured the market's attention with its dramatic stock performance, navigating through a sea of volatility with recent gains fueled by significant contract wins and positive AI sector developments. The company's journey reflects a broader narrative in the tech industry: the high stakes of betting on AI innovation. With its stock soaring over 378% in the last year, BigBear.ai demonstrates the potential for rapid growth in an era where AI is increasingly central to strategic sectors like defense, security, and space exploration.

However, the narrative isn't without its twists. Analyst warnings about cyclical business patterns and valuation concerns introduce a layer of complexity to the investment thesis. BigBear.ai's ability to secure pivotal contracts with the U.S. Department of Defense showcases its technological prowess, yet the challenge lies in converting this into sustainable profitability. This scenario invites investors to ponder the delicate balance between innovation, market sentiment, and financial stability in the AI landscape.

The strategic acquisition of Pangiam and partnerships like the one with Virgin Orbit illustrate BigBear.ai's ambition to not only ride the wave of AI hype but also to steer it into new territories. These moves are about expanding market presence and redefining what AI can achieve in practical, real-world applications. As BigBear.ai continues to evolve, it challenges us to consider how far AI can go in reshaping industries and whether the market can keep pace with such rapid technological advancements. This saga of BigBear.ai is a microcosm of the broader AI investment landscape, urging us to look beyond immediate gains to the long-term vision and viability of AI-driven companies.

$BBAI - No hibernation for this BEAR!NYSE:BBAI

The next parabolic AI name?!

NASDAQ:TEM NASDAQ:SOUN NASDAQ:PLTR 2.0

Breakout = 🎯$5.20🎯$6.75🎯$8.80

Not financial advice

BBAI - Big Bear Big Volume!NYSE:BBAI

This name has periods of strong spikes up followed by massive crashes. BUT, the volume here is a lot better than it has been.

If they are able to maintain this level of volume then we could see a break above the $5/$6 resistance

Not financial advice

BBAI BigBear ai Holdings Options Ahead of EarningsAnalyzing the options chain and the chart patterns of BBAI BigBear ai Holdings prior to the earnings report this week,

I would consider purchasing the 2usd strike price Calls with

an expiration date of 2025-1-17,

for a premium of approximately $0.40.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.