Just In: Chagee Holdings Limited (CHA) Set for 160% BreakoutThe price of Chagee Holdings Limited (NASDAQ; NASDAQ:CHA ) is gearing for a 160% breakout amidst breaking out of a falling wedge.

The stock has been in an enclosed falling wedge since Early March this year. However, growing interest reveals the stock is set to go parambolic with eyes on the $30 resistant point.

Currently up 1.20% in Friday's premarket session with the RSI at 54, NASDAQ:CHA stock is poised for the 160% surge.

Financial Performance

In 2024, Chagee Holdings's revenue was 12.41 billion, an increase of 167.35% compared to the previous year's 4.64 billion. Earnings were 1.44 billion, an increase of 172.35%.

Analyst Summary

According to 5 analysts, the average rating for CHA stock is "Buy." The 12-month stock price target is $31.18, which is an increase of 120.67% from the latest price.

About CHA

Chagee Holdings Limited, through its subsidiaries, owns, operates, and franchises teahouses under the CHAGEE brand name in the People’s Republic of China and internationally. The company engages in sale of tea drinks and related raw materials, packaging, teahouse equipment and other supplies. It operates through online platforms. The company was founded in 2017 and is based in Shanghai, the People’s Republic of China.

Charting

$SPY & $SPX Scenarios — Wednesday, Nov 26, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Wednesday, Nov 26, 2025 🔮

🌍 Market-Moving Headlines

🧱 Growth check pre holiday: Weekly jobless claims and durable goods hit together at 8 30 AM, giving a clean read on labor and business demand.

📦 Capex and manufacturing pulse: The delayed September durable goods numbers update the heavy-industry side of the economy before year end.

📘 Fed Beige Book: Afternoon release colors in how businesses are actually feeling about demand, pricing, and hiring across districts.

📊 Key Data & Events (ET)

⏰ 8 30 AM

• Initial Jobless Claims (Nov 22): 225,000 vs 220,000

• Durable Goods Orders (Sept, delayed): 0.5 percent vs 2.9

• Durable Goods ex Transportation (Sept, delayed): 0.4 percent

⏰ 2 00 PM

• Federal Reserve Beige Book — anecdotal read on growth, wages, and pricing

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #macro #jobs #durablegoods #BeigeBook #stocks #bonds #markets #investing

$SPY & $SPX Scenarios — Tuesday, Nov 25, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Tuesday, Nov 25, 2025 🔮

🌍 Market-Moving Headlines

🧾 Backlog data hits at once: Delayed Sept Retail Sales + PPI finally print, giving a clearer view of demand and pipeline inflation.

📉 Cooler demand, firm prices: Sales miss old expectations while PPI stays positive, not the clean disinflation combo bulls want.

🏠 Housing and confidence: Case Shiller, Confidence, and Pending Home Sales update how higher rates are hitting owners and buyers into holiday season.

📊 Key Data & Events (ET)

⏰ 8 30 AM block — Sept backlog

• Retail Sales (delayed): 0.3 percent vs 0.6 old forecast

• Retail Sales ex Auto: 0.3 percent vs 0.7

• PPI (delayed): 0.3 percent | YoY 2.6 percent

• Core PPI: 0.3 percent | YoY 2.8 percent

⏰ 9 00 AM

• Case Shiller 20 City Home Prices (Sept): 1.3 percent vs 1.6

⏰ 10 00 AM

• Business Inventories (Aug, delayed): 0.0 percent vs 0.2

• Consumer Confidence (Nov): 93.2 vs 94.6

• Pending Home Sales (Oct): 0.0 percent

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #stocks #macro #PPI #retailsales #consumer #housing #inflation #markets #investing

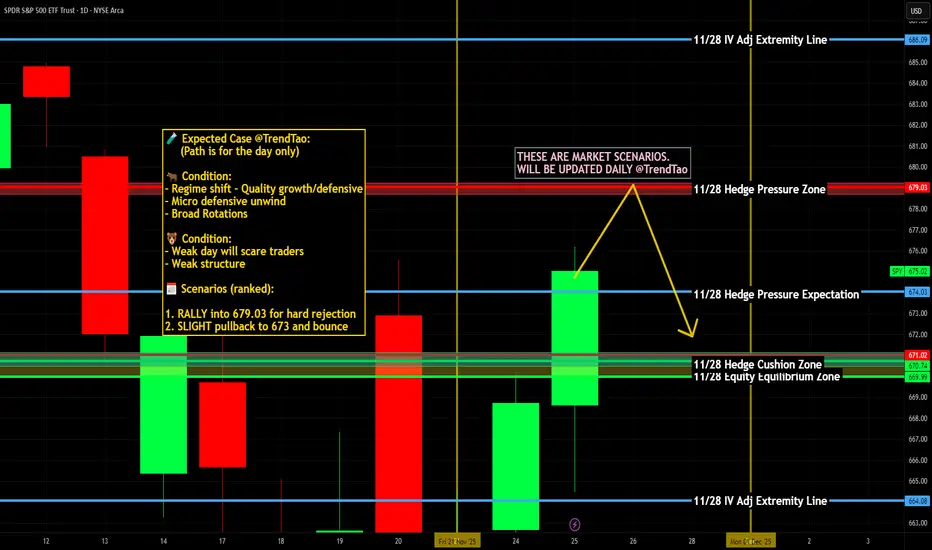

$SPY and $SPX Scenarios — Week of Nov 24 to Nov 28, 2025🔮 AMEX:SPY and SP:SPX Scenarios — Week of Nov 24 to Nov 28, 2025 🔮

🌍 Market-Moving Headlines

📉 Shutdown backlog week: Most major September reports finally drop on Tuesday and Wednesday — Retail Sales, PPI, Durable Goods — all of which normally move markets but are arriving late due to the October shutdown.

🏠 Housing and consumer read-through: Case Shiller, Consumer Confidence, and Pending Home Sales give traders a real-time read on the health of housing and spending as the holiday season begins.

📉 Liquidity thinning: Thanksgiving week historically brings lighter volume and sharper moves when data surprises.

📊 Key Data and Events (ET)

Below are only the trader-relevant items, with delayed reports clearly marked.

TUESDAY, NOV 25 — The Big Data Dump

⏰ 8:30 AM — Retail Sales (Delayed Sept)

Actual: 0.3 percent (vs 0.6 forecast)

⏰ 8:30 AM — Retail Sales ex-Autos (Delayed Sept)

Actual: 0.3 percent (vs 0.7 forecast)

⏰ 8:30 AM — Producer Price Index PPI (Delayed Sept)

Actual: 0.3 percent

Year over year: 2.6 percent

⏰ 8:30 AM — Core PPI (Delayed Sept)

Prior: 0.3 percent

Current: Not available due to shutdown

⏰ 8:30 AM — Core PPI Year over Year

Actual: 2.8 percent

⏰ 9:00 AM — Case Shiller Home Price Index, 20-City (Sept)

Actual: Not available

Forecast: 1.6 percent

⏰ 10:00 AM — Business Inventories (Delayed Aug)

Actual: 0.1 percent

⏰ 10:00 AM — Consumer Confidence (Nov)

Actual: 93.4 (vs 94.6 forecast)

⏰ 10:00 AM — Pending Home Sales (Oct)

Actual: 0.0 percent

WEDNESDAY, NOV 26

⏰ 8:30 AM — Initial Jobless Claims (Nov 22)

Actual: 225,000 (vs 220,000 forecast)

⏰ 8:30 AM — Durable Goods Orders (Delayed Sept)

Actual: 0.3 percent (vs 2.9 percent prior)

⏰ 8:30 AM — Durable Goods ex-Transportation (Delayed Sept)

Actual: 0.4 percent

THURSDAY, NOV 27

🦃 Thanksgiving — No economic releases

FRIDAY, NOV 28

⏰ 9:45 AM — Chicago PMI (Nov)

Forecast: 43.8

⚠️ Note: Many September reports are still delayed due to the federal government shutdown from Oct 1 to Nov 12. All delayed items are explicitly labeled above.

⚠️ Disclaimer: Educational and informational only. Not financial advice.

📌 #SPY #SPX #macro #trading #stocks #inflation #consumer #PPI #retailsales #housing #markets

$SPY & $SPX Scenarios — Friday, Nov 21, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Friday, Nov 21, 2025 🔮

🌍 Market-Moving Headlines

📊 Flash PMIs take center stage: These are the first real-time reads on November growth — high-impact for equities, yields, and recession-tracking.

🧭 Consumer sentiment + inventories wrap the week: UMich final reading offers clues on spending resilience; wholesale inventories remain a shutdown-delayed report.

⚠️ Shutdown backlog: Wholesale inventories (Aug) is still delayed due to the Oct 1–Nov 12 shutdown.

📊 Key Data & Events (ET)

⏰ 9:45 AM — S&P Flash PMIs (Nov)

• Services: 54.5 (vs 54.8 forecast)

• Manufacturing: 52.0 (vs 52.5 forecast)

One of the most important releases of the day — markets move off this.

⏰ 10:00 AM — Consumer Sentiment (Final, Nov)

Actual: 51.0

Low sentiment continues to weigh on forward demand expectations.

⏰ 10:00 AM — Wholesale Inventories (Aug, delayed report)

Actual: 0.1 percent

⚠️ Delayed due to the federal shutdown — low relevance, but still part of the data backlog.

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #SPY #SPX #trading #macro #PMI #consumer #markets #stocks #investing

$SPY & $SPX Scenarios — Thursday, Nov 20, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Thursday, Nov 20, 2025 🔮

🌍 Market-Moving Headlines

📉 Dual labor signals hit premarket: The delayed September employment report and weekly jobless claims land at the same time — a rare setup that can jolt both yields and equities.

🛒 Housing + recession gauges follow shortly after, giving traders a full macro pulse before midday.

⚠️ Reminder: Some October data (leading indicators) may still be affected by shutdown delays.

📊 Key Data & Events (ET)

⏰ 8:30 AM — U.S. Employment Report (Delayed Sept)

• Payrolls: 50,000

• Unemployment Rate: 4.3%

• Wages: 0.3% m/m, 3.7% y/y

Treat this like a fresh NFP — major market mover.

⏰ 8:30 AM — Initial Jobless Claims (Nov 15)

Actual: 227,000

Weekly update on cooling/tightening labor conditions.

⏰ 8:30 AM — Philadelphia Fed Manufacturing (Nov)

Actual: 1.5 vs –12.8 prior

Important for gauging demand softness vs stabilization.

⏰ 10:00 AM — Existing Home Sales (Oct)

Actual: 4.10M vs 4.06M forecast

Clean read on rate-sensitive housing momentum.

⏰ 10:00 AM — Leading Economic Indicators (Oct)

Actual: –0.3%

⚠️ May still be subject to shutdown-related reporting delays.

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #SPY #SPX #trading #macro #jobs #housing #labor #markets #PMI #investing #stocks

SPY & SPX Scenarios — Wednesday, Nov 19, 2025🔮 SPY & SPX Scenarios — Wednesday, Nov 19, 2025 🔮

🌍 Market-Moving Headlines

📉 Manufacturing + housing cluster hits premarket: Philly Fed, Starts, and Permits all drop at 8:30 — a rare combo that can shift the recession narrative quickly.

⚠️ Shutdown-lag still in play: Housing Starts, Building Permits, and the delayed Trade Balance report may not publish due to the Oct 1–Nov 14 shutdown backlog.

📘 FOMC Minutes in the afternoon: Markets focus on cut-timing language, inflation persistence, and financial-conditions assessment.

📊 Key Data & Events (ET)

⏰ 8:30 AM — Philadelphia Fed Manufacturing (Nov)

Forecast: 3.0 vs –12.8 prior

One of the top-tier regional recession indicators.

⏰ 8:30 AM — Housing Starts (Oct)

⏰ 8:30 AM — Building Permits (Oct)

⚠️ Both reports may be delayed due to ongoing data backlog from the federal shutdown.

If released, they move rates, homebuilders, and cyclicals.

⏰ 8:30 AM — U.S. Trade Deficit (Aug, delayed report)

Forecast: –$61.0B vs –$78.3B prior

Lower impact due to being a stale report, but can still nudge GDP tracking.

⏰ 2:00 PM — FOMC Minutes (Oct Meeting)

The day’s biggest confirmed market catalyst.

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #SPY #SPX #trading #macro #recession #housing #rates #manufacturing #FOMC #markets #investing

SPY & SPX Scenarios — Tuesday, Nov 18, 2025🔮 SPY & SPX Scenarios — Tuesday, Nov 18, 2025 🔮

🌍 Market-Moving Headlines

⚠️ Shutdown backlog still unresolved: Several October reports scheduled for Tuesday (Import Prices, Industrial Production, Capacity Utilization) remain at high risk of delay, which keeps macro visibility muddy and makes equities more sensitive to yields + positioning.

🏠 Housing sentiment check: Homebuilder confidence is one of the few confirmed releases, giving the market a clean read on construction demand and rates pressure.

📊 Key Data & Events (ET)

⏰ 8:30 AM — Import Price Index (Oct)

⏰ 8:30 AM — Import Price Index ex-Fuel (Oct)

⏰ 9:15 AM — Industrial Production (Oct)

⏰ 9:15 AM — Capacity Utilization (Oct)

⚠️ All four reports remain at risk of non-release due to the Oct 1–Nov 14 shutdown impact.

If they publish, they directly affect inflation expectations and recession probabilities.

⏰ 10:00 AM — Factory Orders (Aug, delayed report)

Older data, but could matter slightly since it’s been stuck in the backlog.

⏰ 10:00 AM — Homebuilder Confidence (Nov)

Forecast: 37 (prior 37)

The only fresh and confirmed economic print of the morning.

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #SPY #SPX #trading #macro #inflation #housing #manufacturing #markets #rates #investing

SPY & SPX Scenarios — Week of Nov 17 to Nov 21, 2025🔮 SPY & SPX Scenarios — Week of Nov 17 to Nov 21, 2025 🔮

🌍 Market-Moving Headlines

📉 Shutdown fallout still clearing: Several reports from October remain at risk of delay (especially import prices, industrial production, housing data). Markets may react more to yields and tech leadership while waiting for the data stream to fully normalize.

🏠 Housing + manufacturing week: The middle of the week clusters the biggest releases — Philly Fed, Housing Starts, Permits, and FOMC Minutes. This is where volatility can show up.

📉 Labor digest Thursday: Claims + the delayed September employment report hit at the same time — rare setup that can move both bonds and equities.

📊 Key Data & Events (ET)

Below are only the events that actually matter for traders

(all shutdown-risk items marked ⚠️)

MONDAY, NOV 17

⏰ 8:30 AM — Empire State Manufacturing (Nov)

Forecast: 5.5 vs 10.7 prior

Regional but can influence sentiment on macro slowdown.

TUESDAY, NOV 18

⏰ ⚠️ 8:30 AM — Import Price Index (Oct)

⏰ ⚠️ 9:15 AM — Industrial Production & Capacity Utilization (Oct)

Both may still be delayed due to the prior shutdown.

These matter for inflation inputs and growth pulse if they print.

WEDNESDAY, NOV 19 — Biggest Day of the Week

⏰ 8:30 AM — Philadelphia Fed Manufacturing (Nov)

Forecast: 3.0 vs –12.8 prior

High-impact regional gauge — often leads ISM.

⏰ ⚠️ 8:30 AM — Housing Starts & Building Permits (Oct)

Shutdown-risk remains; key for housing cycle momentum.

⏰ 2:00 PM — FOMC Minutes (Oct Meeting)

Top-tier macro catalyst of the week.

Markets focus on: cuts timeline, inflation language, financial conditions.

THURSDAY, NOV 20 — Labor Cluster

⏰ 8:30 AM — Delayed Employment Report (Sept)

• Nonfarm Payrolls: 22,000

• Unemployment Rate: 4.3%

• Wages: 0.3% m/m

Extremely important — markets treat this like a fresh NFP.

⏰ 8:30 AM — Initial Jobless Claims (Nov 15)

Forecast: 225,000

Matters even more because CPI/PPI were delayed.

⏰ 10:00 AM — Existing Home Sales (Oct)

Forecast: 4.08M

Secondary but helps gauge consumer + housing softness.

FRIDAY, NOV 21

⏰ 9:45 AM — S&P Flash PMIs (Nov)

• Services: 54.8

• Manufacturing: 52.5

Fastest high-freq read of growth — always matters.

⏰ 10:00 AM — UMich Consumer Sentiment (Final, Nov)

Forecast: 51.0

Low sentiment keeps pressure on consumer outlook.

⚠️ Reports that may be delayed:

• Import Prices

• Industrial Production & CapU

• Housing Starts / Permits

• A small chance of lingering delays on later October data

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #SPY #SPX #trading #macro #inflation #jobs #housing #markets #PMI #FOMC #investing

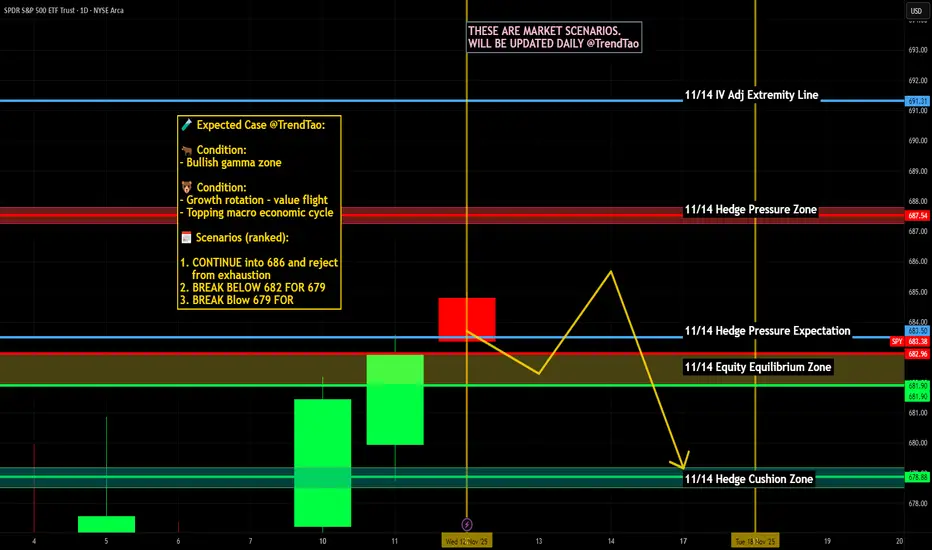

SPY & SPX Scenarios — Friday, Nov 14, 2025🔮 SPY & SPX Scenarios — Friday, Nov 14, 2025 🔮

🌍 Market-Moving Headlines

🚨 Shutdown disruption continues: The entire Retail Sales + PPI complex — normally one of the biggest monthly movers — is still at risk of nondelivery. Markets will trade on expectations, not prints.

📉 Volatility watch: With CPI, Claims, and Retail Sales all in backlog, positioning remains thin and reactive to yields + global risk sentiment.

💵 Bond market tone dominates: Without fresh inflation data, Treasury moves may guide SPX levels more than usual.

📊 Key Data & Events (ET)

All major data below is shutdown-risk flagged.

⏰ ⚠️ 8:30 AM — Retail Sales (Oct)

Forecast: -0.2%

Shutdown delay risk — high

⏰ ⚠️ 8:30 AM — Retail Sales ex-Auto (Oct)

Forecast: +0.2%

Shutdown delay risk — high

⏰ ⚠️ 8:30 AM — Producer Price Index (PPI, Oct)

Headline: +0.1%

Core: +0.3%

Shutdown delay risk — high

⏰ ⚠️ 10:00 AM — Business Inventories (Sept)

Forecast: +0.2%

Shutdown delay risk — medium

👉 All above data normally moves markets, especially Retail Sales + PPI.

Today, traders only get the reaction if the numbers publish.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #inflation #PPI #RetailSales #macro #economy #Fed #markets #risk #shutdown

$SPY $SPX Scenarios — Thursday, Nov 13, 2025🔮 AMEX:SPY SP:SPX Scenarios — Thursday, Nov 13, 2025 🔮

🌍 Market-Moving Headlines

🚨 Inflation spotlight (⚠️ delay risk): October CPI and Jobless Claims — both subject to government shutdown delay — were originally scheduled for release this morning. Markets may stay cautious or reactive to leaks and private inflation trackers in the absence of official prints.

💬 Fed rotation continues: A packed Fed lineup — Mary Daly, John Williams, Kashkari, Hammack, and Bostic — will steer tone across the day, shaping expectations for December guidance.

📉 Budget check: A fresh federal deficit report (-$215B) adds to the fiscal backdrop narrative, though reaction may stay muted if major data doesn’t hit.

📊 Key Data and Events (ET)

⏰ 8:00 AM — Mary Daly (San Francisco Fed) speech

⏰ ⚠️ 8:30 AM — Consumer Price Index (Oct) | +0.3% MoM | +3.1% YoY (subject to delay)

⏰ ⚠️ 8:30 AM — Core CPI (Oct) | +0.3% MoM | +3.1% YoY (subject to delay)

⏰ ⚠️ 8:30 AM — Initial Jobless Claims (Nov 8) | 225,000 forecast (subject to delay)

⏰ 9:20 AM — John Williams (NY Fed) welcoming remarks

⏰ 10:25 AM — Neel Kashkari (Minneapolis Fed) opening remarks

⏰ 12:15 PM — Alberto Musalem (St. Louis Fed) speech

⏰ 12:20 PM — Beth Hammack (Cleveland Fed) speech

⏰ 2:00 PM — Monthly U.S. Federal Budget (Oct) | -$215B deficit vs -$257.5B prior

⏰ 3:20 PM — Raphael Bostic (Atlanta Fed) speech

⚠️ Note:

CPI and Jobless Claims carry the highest market impact this week — but both remain at risk of delay due to the ongoing federal data blackout. Fed speakers and any CPI proxies (like Cleveland Fed’s nowcast) will drive intraday volatility instead.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #CPI #inflation #Fed #Williams #Bostic #Musanlem #Hammack #macro #markets #yields #shutdown

$SPY $SPX Scenarios — Wednesday, Nov 12, 2025🔮 AMEX:SPY SP:SPX Scenarios — Wednesday, Nov 12, 2025 🔮

🌍 Market-Moving Headlines

💬 Fed marathon day: Six Fed officials speak across the day, led by Williams, Waller, and Bostic — giving markets multiple reads on the Fed’s reaction to soft labor data and upcoming inflation prints.

📉 Policy sensitivity rising: With no major macro releases this week, investors are hypersensitive to tone shifts in Fed commentary — especially regarding rate-cut timing and balance sheet guidance.

🧩 Positioning churn: After a light Tuesday session, liquidity normalizes as equities digest global risk appetite and pre-CPI setups.

📊 Key Data and Events (ET)

⏰ 9:20 AM — John Williams (NY Fed)

⏰ 10:00 AM — Anna Paulson (Philadelphia Fed)

⏰ 10:20 AM — Chris Waller (Fed Governor)

⏰ 12:15 PM — Raphael Bostic (Atlanta Fed)

⏰ 12:30 PM — Stephen Miran (Fed Governor)

⏰ 4:00 PM — Susan Collins (Boston Fed)

⚠️ Note:

No economic data releases today — markets will key off Fed tone and Treasury yield movement ahead of Thursday’s CPI and jobless claims (both still at risk of delay).

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #Fed #Williams #Waller #Bostic #Miran #Collins #macro #inflation #yields #markets

$SPY $SPX Scenarios — Tuesday, Nov 11, 2025🔮 AMEX:SPY SP:SPX Scenarios — Tuesday, Nov 11, 2025 🔮

🌍 Market-Moving Headlines

🇺🇸 Veterans Day — U.S. bond market closed, equities open but expect thin liquidity and lower volume.

💬 Fed focus: Fed Governor Michael Barr headlines the day’s lone major event, speaking mid-morning on financial stability and supervision.

📉 Small-business sentiment dips: The NFIB Optimism Index slipped to 98.2 from 98.8, reflecting softer hiring plans and higher cost concerns.

⚠️ Shutdown delays: Broader federal data remains constrained this week — investors will continue watching Fed commentary for policy cues.

📊 Key Data and Events (ET)

⏰ 6:00 AM — NFIB Small Business Optimism (Oct) | 98.2 vs 98.8 prior

⏰ 10:25 AM — Michael Barr (Fed Governor) speech

📉 Bond market closed for Veterans Day; expect quieter sessions and possible afternoon drift in equities.

⚠️ Note:

No Tier-1 data today. With lighter volume and no Treasury trading, price action will likely be headline-driven. Keep an eye on Barr’s tone for any hints on post-shutdown policy or liquidity support.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #Fed #MichaelBarr #NFIB #VeteransDay #markets #macro #liquidity #bonds

$SPY $SPX Scenarios — Week of Nov 10–14, 2025🔮 AMEX:SPY SP:SPX Scenarios — Week of Nov 10–14, 2025 🔮

🌍 Market-Moving Headlines

🚩 Shutdown overhang persists: Key October inflation and retail reports remain at risk of delay due to limited government data releases. Market direction may rely on Fed commentary and positioning shifts more than fresh data.

📉 Inflation in focus: The CPI (Thursday) remains the main event — if it releases — as traders gauge whether cooling prices justify the market’s aggressive rate-cut bets.

💬 Fed blitz: Nearly a dozen Fed officials speak this week, including Waller, Williams, Miran, and Bostic, providing clues on how close the Fed feels to easing.

🏦 Veterans Day week rhythm: With Tuesday’s bond market closure, liquidity may thin until the CPI print, creating potential for sharp post-data reactions.

📊 Friday volatility setup: Retail Sales and PPI (if released) will shape the final inflation read-through for Q4 spending momentum.

📊 Key Data and Events (ET)

MONDAY, Nov 10

— No major releases scheduled

TUESDAY, Nov 11 (Veterans Day, bond market closed)

⏰ 6:00 AM — NFIB Optimism Index (Oct)

⏰ 10:25 AM — Michael Barr (Fed Gov) speech

WEDNESDAY, Nov 12

⏰ 9:20 AM — John Williams (NY Fed) speech

⏰ 10:00 AM — Anna Paulson (Philadelphia Fed) speech

⏰ 10:20 AM — Chris Waller (Fed Gov) speech

⏰ 12:15 PM — Raphael Bostic (Atlanta Fed) speech

⏰ 12:30 PM — Stephen Miran (Fed Gov) speech

⏰ 4:00 PM — Susan Collins (Boston Fed) speech

THURSDAY, Nov 13 — CPI Day (High Impact)

⏰ 8:30 AM — Consumer Price Index (Oct) ⚠️ Subject to shutdown delay

• Headline CPI: +0.2% expected

• Core CPI (YoY): TBD

⏰ 8:30 AM — Initial Jobless Claims (Nov 8) ⚠️ May be delayed

⏰ 9:20 AM — John Williams (NY Fed) speech

⏰ 12:15 PM — Alberto Musalem (St. Louis Fed) speech

⏰ 12:20 PM — Beth Hammack (Cleveland Fed) speech

⏰ 2:00 PM — Federal Budget Statement (Oct) | $257.5B deficit

⏰ 3:20 PM — Raphael Bostic (Atlanta Fed) speech

FRIDAY, Nov 14 — Retail & PPI (High Impact)

⏰ 8:30 AM — Retail Sales (Oct) ⚠️ May be delayed

⏰ 8:30 AM — Producer Price Index (Oct) ⚠️ May be delayed

⏰ 10:05 AM — Jeff Schmid (Kansas City Fed) speech

⏰ 2:30 PM — Lorie Logan (Dallas Fed) speech

⚠️ Note:

All starred data (CPI, Jobless Claims, Retail Sales, PPI, Business Inventories) remain subject to delay under the continuing government shutdown. Markets may trade on Fed tone and yield movement in the absence of these releases.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #Fed #CPI #RetailSales #inflation #bonds #macro #yields #markets #shutdown #Bostic #Waller #Williams #Logan

$SPY $SPX Scenarios — Friday, Nov 7, 2025🔮 AMEX:SPY SP:SPX Scenarios — Friday, Nov 7, 2025 🔮

🌍 Market-Moving Headlines

🚩 Jobs Day: The October Employment Report headlines Friday, with payrolls expected at -60,000 and the unemployment rate rising to 4.5% — signaling labor market cooling.

📉 Policy implications: A weak print would reinforce expectations for multiple rate cuts in early 2026, while upside surprises could stall the dovish momentum.

💬 Fed watch: Morning remarks from Williams and Jefferson set the tone before the data drop; Miran rounds out the week with a late-day speech.

⚠️ Shutdown delays: The Employment Report and related labor metrics are at risk of delay pending government data releases, adding uncertainty to Friday’s open.

📊 Sentiment & credit check: U-Mich Consumer Sentiment and Consumer Credit round out the macro picture.

📊 Key Data and Events (ET)

⏰ 3:00 AM — John Williams (NY Fed) speech

⏰ 7:00 AM — Philip Jefferson (Fed Vice Chair) speech

⏰ 🚩 8:30 AM — U.S. Employment Report (Oct) — subject to delay

• Nonfarm Payrolls: -60,000

• Unemployment Rate: 4.5%

• Hourly Wages (MoM): 0.3%

⏰ 10:00 AM — UMich Consumer Sentiment (Prelim, Nov) | 53.0 expected

⏰ 3:00 PM — Consumer Credit (Sept) | $10.0B expected

⏰ 3:00 PM — Stephen Miran (Fed Gov) speech

⚠️ Note:

The Employment Report, Unemployment Rate, and Wage Data are flagged at risk of delay due to the government shutdown. All other releases are expected on time. Market volatility will hinge on whether the data prints or is postponed.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #JobsReport #NFP #Fed #Jefferson #Williams #inflation #yields #macro #shutdown

$SPY $SPX Scenarios — Wednesday, Nov 5, 2025🔮 AMEX:SPY SP:SPX Scenarios — Wednesday, Nov 5, 2025 🔮

🌍 Market-Moving Headlines

🚩 First clean data of the week: After delays in earlier reports, Wednesday brings ADP Employment and ISM Services — the first confirmed macro prints to gauge real economic momentum.

📉 Labor tone check: ADP’s private payroll growth of 22,000 vs -32,000 prior suggests continued softness but potential stabilization ahead of Friday’s NFP.

💼 Services resilience: ISM Services expected to tick up slightly to 50.5, hovering near the expansion line — a critical signal for Q4 GDP trajectory.

💬 Market tone: With shutdown-delayed data still missing, traders focus on rate-cut odds, yields, and Treasury auctions for directional cues.

📊 Key Data and Events (ET)

⏰ 8:15 AM — ADP Employment (Oct) | +22,000 vs -32,000 prior 🚩

⏰ 9:45 AM — S&P Final U.S. Services PMI (Oct) | 55.2

⏰ 10:00 AM — ISM Services (Oct) | 50.5 expected, 50.0 prior 🚩

⚠️ Note:

Unlike earlier-week reports, all of Wednesday’s data are confirmed to release on schedule — making this the first meaningful macro catalyst since the FOMC. Expect intraday volatility around 8:15 AM (ADP) and 10:00 AM (ISM).

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #ADP #ISM #PMI #yields #Fed #inflation #bonds #economy #macro

$SPY $SPX Scenarios — Wednesday, Nov 5, 2025🔮 AMEX:SPY SP:SPX Scenarios — Wednesday, Nov 5, 2025 🔮

🌍 Market-Moving Headlines

🚩 First clean data of the week: After delays in earlier reports, Wednesday brings ADP Employment and ISM Services — the first confirmed macro prints to gauge real economic momentum.

📉 Labor tone check: ADP’s private payroll growth of 22,000 vs -32,000 prior suggests continued softness but potential stabilization ahead of Friday’s NFP.

💼 Services resilience: ISM Services expected to tick up slightly to 50.5, hovering near the expansion line — a critical signal for Q4 GDP trajectory.

💬 Market tone: With shutdown-delayed data still missing, traders focus on rate-cut odds, yields, and Treasury auctions for directional cues.

📊 Key Data and Events (ET)

⏰ 8:15 AM — ADP Employment (Oct) | +22,000 vs -32,000 prior 🚩

⏰ 9:45 AM — S&P Final U.S. Services PMI (Oct) | 55.2

⏰ 10:00 AM — ISM Services (Oct) | 50.5 expected, 50.0 prior 🚩

⚠️ Note:

Unlike earlier-week reports, all of Wednesday’s data are confirmed to release on schedule — making this the first meaningful macro catalyst since the FOMC. Expect intraday volatility around 8:15 AM (ADP) and 10:00 AM (ISM).

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #ADP #ISM #PMI #yields #Fed #inflation #bonds #economy #macro

$SPY $SPX Scenarios — Tuesday, Nov 4, 2025🔮 AMEX:SPY SP:SPX Scenarios — Tuesday, Nov 4, 2025 🔮

🌍 Market-Moving Headlines

🚩 Jobs data on deck: Tuesday’s focus is on labor demand — the JOLTS report remains a key barometer for wage pressure, though it may not print due to the shutdown.

⚠️ Data blackout continues: The Trade Balance and Factory Orders are both delayed government releases, keeping markets dependent on Fed tone and price action.

💬 Fed-speak pre-jobs: Vice Chair Bowman’s early-morning remarks will frame policy bias ahead of ADP and Friday’s NFP.

💻 Volatility compression: With few confirmed reports, traders watch AMEX:SPY ’s range behavior and TVC:VIX positioning before the labor-data surge mid-week.

📊 Key Data and Events (ET)

⏰ 6:35 AM — Michelle Bowman (Fed Vice Chair) speech

⏰ ⚠️ 8:30 AM — U.S. Trade Deficit (Sept) — may not print

⏰ ⚠️ 10:00 AM — Factory Orders (Sept) — may not print

⏰ ⚠️ 10:00 AM — Job Openings (JOLTS, Sept) — may not print

⚠️ Note:

All three macro reports are subject to delay under the continuing government shutdown. Expect headline-driven trading and low data-volume volatility until Wednesday’s ADP and ISM Services releases.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #Fed #Bowman #JOLTS #TradeBalance #FactoryOrders #bonds #yields #economy #shutdown #macro

$SPY $SPX Scenarios — Week of Nov 3 → Nov 7, 2025🔮 AMEX:SPY SP:SPX Scenarios — Week of Nov 3 → Nov 7, 2025 🔮

🌍 Market-Moving Headlines

🚩 Post-FOMC digestion: After Powell’s Oct 29 presser, traders watch whether yields and the dollar cool or extend higher.

📈 Labor-week spotlight: Friday’s Jobs Report (NFP, wages, unemployment) anchors the week — rate-path odds hinge on those prints.

💬 Fed tone in focus: Multiple governors and regional presidents hit the circuit after the FOMC — every nuance matters for December guidance.

⚠️ Shutdown watch: Several BEA and Census releases (Factory Orders, Trade Balance, GDP components) may not print on time if the government remains partially shuttered.

💻 Earnings taper off: Final big-cap names and sector leaders wrap Q3 results, shaping sentiment into mid-November.

📊 Key Data and Events (ET)

Mon Nov 3

⏰ ⚠️ 8:30 AM — Durable Goods Orders (Sept) | Ex-transportation subset — BEA report; possible delay

⏰ 10:00 AM — Factory Orders (Sept) ⚠️ possible delay

Tue Nov 4

⏰ 9:00 AM — S&P Case-Shiller Home Price Index (Aug)

⏰ 10:00 AM — Consumer Confidence (Oct) 🚩

Wed Nov 5

⏰ ⚠️ 8:30 AM — Advanced Trade Balance in Goods (Sept) | Retail and Wholesale Inventories — Census; may be delayed

⏰ 10:00 AM — Pending Home Sales (Sept)

⏰ 🚩 2:00 PM — FOMC Rate Decision

⏰ 🚩 2:30 PM — Fed Chair Powell Press Conference

Thu Nov 6

⏰ 🚩 8:30 AM — Initial Jobless Claims (Oct 25) expected on schedule

⏰ 🚩 8:30 AM — GDP (Q3, Advance) ⚠️ BEA data; delay possible

⏰ 9:55 AM — Fed Vice Chair Michelle Bowman speaks

Fri Nov 7

⏰ 🚩 8:30 AM — PCE and Core PCE (Sept) along with Personal Income, Spending, and Employment Cost Index ⚠️ BEA risk

⏰ 9:45 AM — Chicago PMI (Oct)

⏰ 12:00 PM — Cleveland Fed President Hammack and Atlanta Fed President Bostic remarks

⚠️ Note:

Shutdown risk applies to BEA and Census releases marked with ⚠️

Confirmed live data include Jobless Claims, FOMC decisions, and Fed speeches — these will drive most of the week’s price action.

Friday’s PCE print (if released) remains the key inflation gauge.

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #Fed #Powell #FOMC #PCE #GDP #JoblessClaims #inflation #bonds #yields #economy #macro

$SPY / $SPX Scenarios — Week of Oct 20 → Oct 24, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Week of Oct 20 → Oct 24, 2025 🔮

🌍 Market-Moving Headlines

🚩 Inflation week: The delayed CPI release on Friday could be the first key data drop since the shutdown began — all eyes on price momentum and Fed expectations.

📉 Jobless Claims live feed: The only consistent macro signal right now — still reporting despite shutdown; any uptick could rattle yields and growth sentiment.

💬 Fed tone matters more: Policymakers continue to speak through the data void; expect market sensitivity to even minor policy hints.

💻 Earnings peak week: Roughly 80+ S&P 500 names report, including several mega-caps — likely to set the tone for AMEX:SPY and $QQQ.

📊 Key Data & Events (ET)

Mon 10/20

⏰ No major scheduled data

Tue 10/21

⏰ No major scheduled data

Wed 10/22

⏰ No major scheduled data

Thu 10/23

⏰ 🚩 8:30 AM — Initial Jobless Claims (Oct 18) — only active weekly macro indicator

⏰ 10:00 AM — Existing Home Sales (Sept) (may be delayed due to shutdown)

Fri 10/24

⏰ 🚩 8:30 AM — Consumer Price Index (CPI & Core CPI, Sept) (delayed release expected)

⚠️ Note:

With most official data frozen, Jobless Claims and CPI carry extra weight. Expect sharp intraday swings on any surprise readings or leaks.

⚠️ Disclaimer: Educational / informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #CPI #JoblessClaims #Fed #inflation #bonds #yields #shutdown #earnings #economy #megacaps #datawatch

$SPY / $SPX Scenarios — Friday, Oct 17, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Friday, Oct 17, 2025 🔮

🌍 Market-Moving Headlines

🚩 Data blackout risk: Friday was set for key housing and production reports — but the ongoing shutdown means most prints (Housing Starts, Industrial Production, Import Prices) may not be released.

📉 Macro vacuum: With no confirmed data, traders lean on positioning and bond moves to gauge growth sentiment into the weekend.

💬 Earnings carry the weight: Corporate results take the spotlight as macro inputs dry up.

💻 Technical tone: AMEX:SPY and NASDAQ:QQQ watchlist rotation continues — watch volatility pockets if liquidity fades mid-session.

📊 Key Data & Events (ET)

⏰ 8:30 AM — Housing Starts & Building Permits (Sept) — scheduled but may not print

⏰ 8:30 AM — Import Price Index (Sept) — scheduled release

⏰ 9:15 AM — Industrial Production & Capacity Utilization (Sept) — scheduled but may not print

⚠️ Note: Friday wraps a quiet macro week dominated by missing data and Fed commentary. Expect a headline-driven close with limited participation ahead of weekend risk.

⚠️ Disclaimer: Educational / informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #housing #IndustrialProduction #ImportPrices #Fed #bonds #economy #shutdown #yields #equities

$SPY / $SPX Scenarios — Thursday, Oct 16, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Thursday, Oct 16, 2025 🔮

🌍 Market-Moving Headlines

🚩 Big macro day — if it happens: Retail Sales & PPI headline the morning, but both reports may be delayed under the ongoing shutdown. Markets will trade on expectation and reaction instead of prints.

📈 Consumer + price pulse: These two data points were expected to test the “soft-landing” narrative — inflation vs. spending resilience.

💬 Fed-speak heavy: Barkin, Waller, Bowman, and Miran dominate the lineup; tone on inflation stickiness may shape yields.

🏠 Housing check: Homebuilder Confidence offers a softer read on the real-economy drag from higher mortgage rates.

📊 Key Data & Events (ET)

⏰ 8:00 AM — Tom Barkin (Richmond Fed) remarks

⏰ 8:30 AM — Retail Sales (Sept) & PPI (Sept) — scheduled but may not print

⏰ 8:30 AM — Initial Jobless Claims (Oct 11) — scheduled release

⏰ 9:00 AM — Stephen Miran & Christopher Waller (Fed Govs) speeches

⏰ 10:00 AM — Michelle Bowman (Fed Gov) remarks + Homebuilder Confidence (Oct)

⏰ 12:45 PM / 4:30 PM — Tom Barkin (Richmond Fed) speeches

⚠️ Disclaimer: Educational / informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #RetailSales #PPI #Fed #Barkin #Waller #Bowman #Miran #inflation #bonds #shutdown #economy #yields #housing

$SPY / $SPX Scenarios — Wednesday, Oct 15, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Wednesday, Oct 15, 2025 🔮

🌍 Market-Moving Headlines

🚩 Growth pulse check: The Empire State Manufacturing Survey kicks off the day — a real-time test of factory sentiment post-summer slowdown.

📘 Fed Beige Book afternoon drop: Key read on regional activity and inflation anecdotes — markets often reposition after release.

💬 Fed parade continues: Bostic, Miran, and Waller keep rate-cut expectations in focus ahead of Thursday’s data risk.

⚠️ Shutdown overhang: Broader data (CPI/PPI/Retail) still paused — traders key off qualitative signals like Beige Book tone.

📊 Key Data & Events (ET)

⏰ 🚩 8:30 AM — Empire State Manufacturing Survey (Oct)

⏰ 12:10 PM — Raphael Bostic (Atlanta Fed) speech

⏰ 12:30 PM — Stephen Miran (Fed Gov) speech

⏰ 1:00 PM — Christopher Waller (Fed Gov) speech

⏰ 🚩 2:00 PM — Fed Beige Book

⚠️ Note: Shutdown continues to delay most federal data releases. Beige Book offers the only official economic snapshot this week — high read-through for inflation, wages, and business conditions.

⚠️ Disclaimer: Educational / informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #Fed #BeigeBook #EmpireState #Waller #Bostic #Miran #bonds #yields #inflation #shutdown #economy