Bear flag on weekly chart, Further breakdown?- NYSE:CRM is forming bear flag on weekly chart.

- It could break down further and test some support underneath around $195

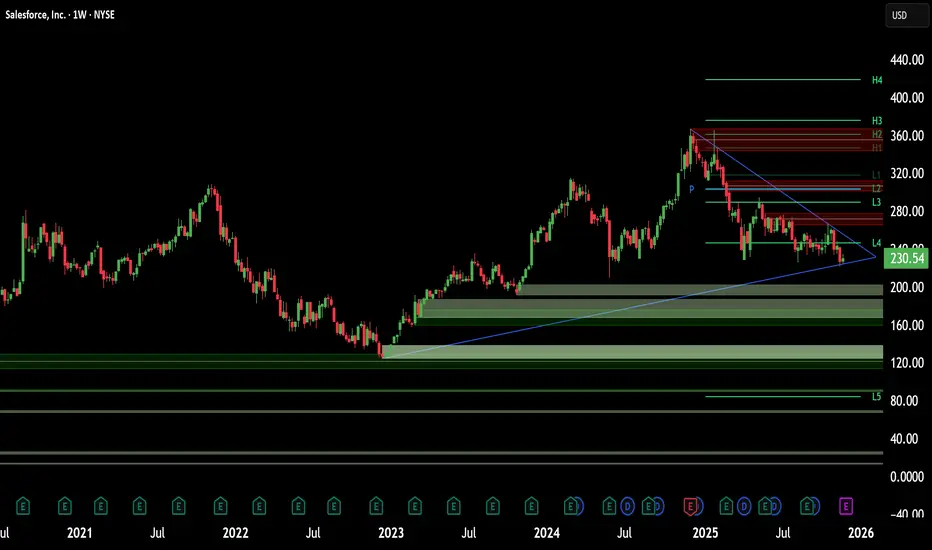

CRM

CRM - Minor Downtrend Line Broken!CRM - CURRENT PRICE : 260.57

CRM previously entered a downtrend following a double-top reversal , which pushed the stock into a prolonged bearish trend. However, current price action shows early signs of trend change as CRM successfully breaks above the minor downtrend line with strong momentum.

Momentum indicators are confirming the shift:

⚡RSI has turned bullish and moved decisively above 50

⚡MACD shows a bullish crossover with improving histogram

With improving trend structure and bullish indicators, CRM may continue its upward recovery. Price may extend toward 278.00 and 296.00 as long as it stays above 242.00 (near EMA 50).

ENTRY PRICE : 260.57

FIRST TARGET : 278.00

SECOND TARGET : 296.00

SUPPORT : 242.00

CRM HIGH PROBABILITY LONG SETUP SOON!!!🚨 CRM HIGH PROBABILITY BUY SETUP 🚨

* Here We Can See Clearly The Next Potential Moves For CRM Coming Hours/Days.

* Keep Your Eyes Close On Your Trading Positions.

* Happy PIP Hunting Traders.

FXKILLA.

Salesforce’s AI Pivot: The Rise of the Agentic EnterpriseSalesforce (CRM) stands at a pivotal intersection of software legacy and artificial intelligence innovation. Despite a year-to-date stock correction of 32%, the company’s fundamentals tell a story of aggressive evolution. The cloud pioneer is systematically re-engineering its DNA to dominate the "Agentic Era." Investors focusing solely on the current share price of $227 may miss the underlying structural shift. With Q3 earnings approaching, we analyze the multi-domain drivers fueling Salesforce’s fundamental ascent.

Financial Resilience: Economics & Business Models

The subscription economy remains Salesforce's financial fortress.

In Q2 Fiscal 2026, the company generated $10.2 billion in revenue, a 10% annual increase. Crucially, $9.7 billion of this flowed from stable subscriptions and support. This recurring revenue model insulates the company against macroeconomic volatility. Furthermore, management’s focus on operational efficiency drove adjusted earnings per share (EPS) to $2.91, beating prior periods. This discipline balances aggressive R&D spending with shareholder returns, a vital equilibrium in high-interest rate environments.

High-Tech & Science: The "Agentic" Shift

Salesforce is redefining the science of work. CEO Marc Benioff envisions an "Agentic Enterprise" where human workers and AI agents collaborate seamlessly. This is not theoretical; the Data & AI division’s revenue more than doubled to $1.2 billion last quarter. The company’s proprietary platform, Agentforce, utilizes advanced Large Language Models (LLMs) to automate complex workflows. This moves beyond simple chatbots to autonomous agents capable of executing multi-step tasks in sales and service.

Patent Analysis: We anticipate a surge in IP filings regarding "autonomous agent orchestration" as Salesforce builds a legal moat around this technology.

Strategic M&A: Technology & Cyber

Data is the fuel for AI, and Salesforce just bought a bigger pipeline. The recent acquisition of Informatica secures critical cloud data management infrastructure. This strategic move allows Salesforce to ingest, clean, and secure vast datasets from disparate sources.

Cybersecurity Implication: By controlling the data layer, Salesforce offers a "walled garden" for enterprise clients. This reduces cyber risk and ensures data governance, a primary concern for Fortune 500 CIOs adopting AI.

Geopolitics & Geostrategy: Middle East Expansion

Salesforce is aggressively diversifying its geographic footprint. The recent launch of an Arabic version of Agentforce signals a strategic pivot toward the Middle East. This region is currently investing heavily in digital transformation to diversify away from oil dependence. By providing localized, AI-driven automation, Salesforce embeds itself into the infrastructure of emerging economic powers. This reduces reliance on Western markets and taps into sovereign wealth capital flowing into technology.

Management & Leadership: Culture of Innovation

Leadership is driving a forced evolution. Benioff is pivoting the company culture from "Cloud First" to "Agent First." This cultural shift is difficult but necessary to avoid obsolescence. The integration of Informatica and the push for $60 billion in revenue by 2030 demonstrate a long-term commitment to growth. Management is willing to sacrifice short-term margins for long-term dominance in the AI application layer.

Outlook: The December Catalyst

All eyes turn to Wednesday, December 3. Salesforce will release its Q3 2025 earnings after the bell. Analysts expect revenue of $10.27 billion and further EPS growth. The market will scrutinize the adoption rates of Agentforce and cloud subscription metrics. A positive report could validate the "Agentic" strategy and reverse the stock's recent bearish trend. For the strategic investor, Salesforce represents a disconnect between current sentiment and fundamental reality.

$CRM SALESFORCEA technical examination of Salesforce's ( NYSE:CRM ) price chart reveals a compelling and potentially decisive consolidation pattern currently in play. The prevailing structure points towards a bearish inclination, but it is also setting the stage for a significant breakout move in either direction.

1. The Prevailing Bearish Evidence: Descending Triangle & ABCD Pattern

The primary pattern of note is a Descending Triangle. This is typically considered a bearish continuation pattern, formed by a flat support level at the bottom and a series of lower highs creating a descending trendline at the top. For NYSE:CRM , the key support floor appears to be around the $230 - $235 level, which price has tested and held multiple times. The descending resistance trendline, currently near $260, acts as a ceiling that is progressively lowering.

Adding further weight to the bearish case is the presence of a completed bearish ABCD pattern within the larger triangle. This harmonic pattern signifies a corrective (bearish) move followed by a retracement, suggesting that the path of least resistance prior to the breakout may be to the downside.

2. The Impending Breakout: Two Scenarios

The significance of a descending triangle lies in the eventual breakout, which can be explosive. The market is coiling, and a decisive move above resistance or below support will dictate the next major trend.

Scenario A: Bullish Breakout (Upside Target)

A decisive and high-volume break above the $260 descending resistance trendline would invalidate the immediate bearish outlook and signal a powerful shift in momentum. In this case, the pattern's measuring implications project a move upward. Using Fibonacci extension levels from the pattern's height, the primary upside price targets would be:

First Target (0.382 Fib): $280.92

Second Target (0.5 Fib): $297.74

Extended Target (0.618 Fib): $314.56

A move to the $297 level would also often align with a retest of the triangle's upper boundary, now acting as new support.

Scenario B: Bearish Breakout (Downside Target)

If the bearish implications of the pattern hold true and the crucial support at $230 - $235 is broken with conviction, it would confirm a continuation of the prior downtrend. The measured move target for a descending triangle breakdown is typically calculated by projecting the height of the pattern's widest point downward from the point of breakdown. This projects a significant decline toward the $200 psychological support level. This area represents a key long-term value zone and would likely be a major test for the stock's health.

Conclusion and Key Levels to Watch

In summary, NYSE:CRM is at a critical technical juncture, compressed within a descending triangle. While the internal patterns suggest a bearish bias, the outcome is not confirmed until a breakout occurs.

Bullish Trigger: A break and close above $260. Confirmation would be a follow-through move above this level with strong volume.

Bearish Trigger: A break and close below the $230 - $235 support zone.

Neutral Stance: Until one of these levels is breached, the stock is likely to continue its sideways consolidation within the triangle.

Traders and investors should monitor these key levels closely, as the breakout will likely determine NYSE:CRM 's directional bias for the medium term.

ServiceTitan Deep Dive - The Hidden SaaS GemHey everyone,

ServiceTitan is a founder-led SaaS platform revolutionizing how trades businesses operate - think plumbers, electricians, HVAC contractors, and roofers. This is a classic "picks and shovels" play on a massive $1.5 trillion market that's been historically underserved by technology.

I don't want to bother you with too much text, so here are the bullet points:

Market Opportunity & Position

Total addressable market: $650B actively targeted (out of $1.5T total trades market)

Current penetration: Only 5% of addressable market ($75B GMV)

15,000+ contractors on platform with 110%+ net dollar retention for 13 straight quarters

First-mover advantage in providing an end-to-end integrated platform for the fragmented trades industry

Financial Metrics (TTM)

Revenue: $866M (FY2026E: $939M, +17.7% 2-yr CAGR)

Gross Margin: 67.4%

Operating Margin: -28.9% GAAP, but 12% non-GAAP (targeting 25% long-term), this is great

Free Cash Flow: Positive at 6% margin ($52M FCF)

Cash Position: $471M with negative net debt (-$313M). This is also great

Valuation Metrics

EV/Sales: 10.9x TTM, 9.4x NTM (premium but justified by growth)

P/FCF: 186.6x TTM, 145.4x NTM (improving as FCF scales)

EV/EBITDA: 69.3x NTM (currently negative TTM)

Forward P/E: 125x (transitioning to profitability)

Analyst Consensus: $136.20 price target

Economic Moat Sources

Scale Economies: Operating margins improved 510 bps YoY as platform scales

Switching Costs: Deep integration with Pro products and AI automation creates lock-in

Counter-Positioning: Specialized trades focus vs. general enterprise software

Key Growth Catalysts

AI-Powered Automation: Virtual agent "Phin" and Contact Center Pro driving 30%+ attach rates

Vertical Expansion: Commercial and roofing segments showing strong traction

Pro Products: Higher-margin add-ons increasing customer lifetime value

Strategic Partnerships: Ford fleet management, Roto-Rooter deals validate enterprise credibility

Insider Confidence

Vahe Kuzoyan (Co-founder/President): 7.3M shares (7.8% ownership, $771M value)

Dave Sherry (CFO): 348K shares ($40M value)

Total insider ownership: 8.3% demonstrating strong alignment

Why Investing Now?

Fed rate cuts boosting home buying/renovation activity

Management raised guidance twice in FY2026

Margin inflection point with path to 25% operating margins

AI capabilities are creating competitive separation

Only 5% market penetration with a massive runway

Risk Factors

Valuation Risk: Trading at 10.9x EV/Sales with GAAP losses

Growth Management: Rapid expansion could strain resources

Industry Cyclicality: Trades sensitive to economic downturns

Competition: Potential entry from Salesforce, ServiceNow

Profitability Timeline: Still burning cash on GAAP basis

Investment Strategy

I will start by allocating 1% of my portfolio to the stock, and add more if the price drops. NOTE that this is a high-risk play.

Rating: BUY | Risk: High | Conviction: 7.5/10

Quick note: I'm just sharing my journey - not financial advice! 😊

Salesforce: Trading SidewaysSalesforce has struggled to gain clear momentum in either direction over the past two weeks, which has resulted in mostly sideways trading. Looking ahead, we continue to anticipate renewed downward pressure in the near term, which could push the stock into our blue Target Zone between $187.75 and $150.42, thereby completing the broader correction of blue wave (II). After this move, we expect a new upward trend to emerge, which makes the blue zone an attractive entry point for long positions. For risk management, a stop can be placed 1% below the lower boundary of the zone. However, there remains a 36% chance that CRM will not reach our Target Zone and instead will break out directly above resistance at $312, potentially surpassing the higher $378.16 level as well. In that scenario, we would place the stock in a broader (green) upward impulse.

CRM - Salesforce - Earnings Beat, Shares Down? $286 Retest?We're currently watching the last stages down into this Ascending Wedge as we approach a very key and important load-up zone at the $227s. Looking for consolidation, bounce out wedge back north to retest those $287s.

CRM reported an earnings beat, guidance lower for Q3 than Street expects, but ultimately has been beatened down by the Rise of AI and it's incrouchment on Software Business Models with the Likes of a Customizable CRM. Their challenge will be continuing to leverage their Einstein AI which has brought a revolutionary approach to the CRM space in itself.

Salesforce | CRM | Long at $242.42Salesforce NYSE:CRM : firing their workforce... migrating toward an AI-driven Agentforce platform, instating a $20 billion increase to its share buyback program (now totaling $50 billion), and strong growth in regions like the UK, France, Canada, and Asia Pacific (particularly among small and medium businesses). The CEO recently declared significant productivity gains (e.g., 30% in engineering) through digital labor and expressed optimism about supporting U.S. government efficiency with Agentforce.

What's good for business isn't necessarily good for the common people. Welcome to AI, folks!

It looks like NYSE:CRM is moving toward a future of full AI. Even if revenue dips due to a slowing economy, I except earnings to soar higher and higher by dropping the humans from the payroll...

Thus, at $242.42, NYSE:CRM is in a personal buy zone as it bounces within my historical simple moving average band. Near-term, I think the price may dip into the low $200's if the US economy continues to show signs of weakening. But AI is only going to boost returns... fortunately for investors, but unfortunately for the workforce...

Targets into 2028:

$306.00 (+26.2%)

$350.00 (+44.3%)

CRM Earnings BEAR PLAY--$235 Put Target→Don’t Miss Out

## 💣 CRM Earnings Bear Play 🚨 | Put \$235 Setup (Sep 5 Expiry) 📉🔥

### 📊 Summary

CRM earnings setup skews **bearish** despite durable cash flow:

* **Fundamentals:** Strong margins & FCF, but **revenue slowing (7.6% TTM)** + high bar for AI guidance.

* **Options Flow:** Heavy put OI at **\$230–240** vs scattered calls → institutions hedging downside.

* **Technicals:** Price under 50/200-day MA, RSI overbought (71). Short-term bounce inside longer downtrend.

* **Macro:** Rising VIX + risk-off tone = higher downside sensitivity.

**📈 Net View:** 🔴 **Moderate Bearish (74% confidence)** → downside risk outweighs upside into earnings.

---

### 📝 Trade Plan

* 🎯 **Instrument:** CRM

* 🔀 **Direction:** Put

* 💵 **Entry:** \$2.61

* 📅 **Expiry:** 2025-09-05

* 🎯 **Profit Target:** \$7.83 (+200%)

* 🛑 **Stop Loss:** \$1.305 (-50%)

* 📈 **Strike:** \$235

* ⏰ **Timing:** Enter **pre-earnings close** (Sep 4, AMC earnings).

⚠️ **Exit:** Within 2 hours post-print — avoid IV crush & second-day reversal.

---

### 🚀 Hashtags (TradingView Viral)

\#CRM #EarningsPlay #OptionsTrading #PutOptions #BearishSetup #WeeklyOptions #EarningsTrade #GammaFlow #IVCrush #StocksToWatch #HighRiskHighReward #SmartMoneyFlow #TechnicalAnalysis

CRM Salesforce Options Ahead of EarningsIf you ahven`t bought CRM before the rally:

Now analyzing the options chain and the chart patterns of CRM Salesforce prior to the earnings report this week,

I would consider purchasing the 300usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $7.52.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

Snowflake Melt Up! NYSE:SNOW had an extraordinary breakout on earnings.

Raising their FY 2026 guidance by 100M

Today our members closed our $220 Oct 17 call options for a monster gain.

We are looking to roll profits up and out into farther strike and date.

This price action should see some consolidation, so let the momentum digest itself.

A clear weekly pattern is taking hold of this ticker, so allow it lots of time to play out.

CRMHere’s the latest snapshot for **Salesforce, Inc. (CRM)**:

## Stock market information for Salesforce Inc (CRM)

* Salesforce Inc is a equity in the USA market.

* The price is 248.29 USD currently with a change of 2.33 USD (0.01%) from the previous close.

* The latest open price was 245.78 USD and the intraday volume is 6694286.

* The intraday high is 249.52 USD and the intraday low is 243.44 USD.

* The latest trade time is Saturday, August 23, 03:59:57 +0400.

---

## CRM Stock — Snapshot & Context (As of August 22–23, 2025)

### 1. Market Performance

* **Closing Price**: \$248.29 — up **+1.00%**. However, this was below the broader market gains (S\&P 500 +1.52%, Dow Jones +1.89%) ( ).

* **52‑Week Range**: From a low near **\$226.48** to a high of **\$369.00** (achieved on December 4). CRM is currently **\~32–36% below** its peak ( ).

* **Trading Activity**: Volume was **6.3 million**, slightly below the 50-day average of 7.6 million shares ( ).

---

### 2. Recent Drivers & Investor Sentiment

* **AI Adoption Challenges**

Salesforce's AI product, *Agentforce*, is facing headwinds. Enterprise customers reportedly suffer from "decision fatigue" amid a flood of new AI tools, leading to slower adoption. Complex pricing and unclear ROI are cited as additional deterrents ( , ).

* **Pressure from Activist Investor**

Starboard Value, an activist fund, boosted its stake in Salesforce by nearly **50% in Q2 2025**, now holding about **1.3 million shares**. Amid the stock’s \~30% year-to-date decline, this move fuels speculation of renewed pressure on management to enhance performance ( ).

Following this, Salesforce shares rose **\~3.7% to \$242.08**, and analyst Gil Luria upgraded his rating to "Neutral" with a \$225 target ( ).

* **Strong Earnings & Strategic Acquisition**

In Q1 FY2026, Salesforce posted better-than-expected results:

* Revenue: **\$9.83B**, up 8% YoY

* Adjusted EPS: **\$2.58/share**

As a result, it raised its full-year forecast to **\$41–41.3B**, and EPS to **\$11.27–11.33**. It also announced plans to acquire **Informatica for \$8B**, bolstering its AI and data capabilities ( , ).

* **Macro Trends Impacting SaaS Valuation**

A broader market concern is that SaaS giants like Salesforce may face valuation pressure due to slowing top-line growth—from >20% in 2021–2022 to an expected \~9% in 2025—as competition from agile AI startups intensifies ( ).

* **Recent Volatility**

On August 21, CRM’s weakness contributed to a **318-point drop in the Dow Jones**, pulling the index down roughly 69 points ( ).

---

### 3. Company Overview (Snapshot)

* **Founded**: March 1999 by Marc Benioff and co‑founders ( ).

* **Nature**: A leading cloud-based CRM and enterprise software provider. Member of the S\&P 500 and Dow Jones Industrial Average ( ).

* **Business**: Offers Sales Cloud, Service Cloud, Marketing Cloud, Commerce Cloud, AI tools (like Agentforce and prior Einstein-based AI features), Slack, Tableau, MuleSoft, and more ( ).

---

### Summary Table

| Category | Key Highlights |

| ------------------------ | ---------------------------------------------------------------------------------------- |

| **Price & Range** | \~\$248.29; \~32–36% below 52-week high |

| **Recent Momentum** | +1% Friday; Outperformed peers on Aug. 13 (+2.32%) ( , ) |

| **AI Tool Adoption** | Agentforce growth slowed by decision fatigue & unclear ROI |

| **Activist Involvement** | Starboard boosted its stake—potential catalyst |

| **Earnings & Outlook** | Q1 beat; raised FY26 guidance; acquiring Informatica |

| **Valuation Risk** | Slowing growth in SaaS sector amid rising AI competition |

| **Sector Influence** | Contributed significantly to Dow’s decline on Aug. 21 |

---

### Final Thoughts

Salesforce (CRM) stands at a crossroads. Its foundational strength in enterprise cloud software and AI investments—boosted by a strategic acquisition—are clear long-term advantages. Yet, growth is tempered by cautious customers, heightened competition, and investor pressure. Activist involvement and upgraded guidance showcase potential upside, but execution—especially on AI adoption and margin improvement—remains crucial.

SALESFORCE - CRM - Fractal found and applied to the chart - LONGThis is not a trade call. I am new to fractals trading. ;-)

In addition to what I see a strong bullish move from a seasonal perspective.

Trade is active with a 7% stopploss which is historically the max drawdown for a CRM trade starting from today until early October.

Cheers and good luck!

Vibe coding a risk to Salesforce moatSalesforce (CRM) is facing structural disruption. Not cyclical. Structural. The threat isn’t from Microsoft or Oracle. It’s from culture. From code.

Vibe coding, fast, open-source, AI-native development, is gaining speed. It’s cheaper, faster and skips bloated architecture. It’s not about replacing CRM software. It’s about rethinking workflows.

Salesforce is vulnerable at the bottom. SMEs don’t want complex SaaS stacks. They want modular tools, cheap, fast, scalable. This is where vibe code thrives. No legacy clients. No enterprise red tape.

As SMEs shift, the threat creeps upstream. Large corporates follow. Once adoption takes hold, momentum builds.

This is the Innovator's Dilemma. The incumbent is too invested to pivot. Too big to self-disrupt. So the change is ignored until it’s too late.

Yes, Salesforce has scale and capital. But it's built to sell software, not to be software. Culture eats strategy. Code eats incumbents.

Technicals are cracking. CRM is trading below its 200-day moving average. RSI is drifting lower. No panic, just quiet decay. Valuation isn't reassuring either, CRM trades at roughly 23–26× forward earnings, a discount to its historical average. That signals caution, not comfort.

Disrupt or be disrupted.

The risk isn’t earnings. It’s irrelevance.

The forecasts provided herein are intended for informational purposes only and should not be construed as guarantees of future performance. This is an example only to enhance a consumer's understanding of the strategy being described above and is not to be taken as Blueberry Markets providing personal advice.

CRM Salesforce Options Ahead of EarningsIf you haven`t bought CRM before this rally:

nor sold this top:

Now analyzing the options chain and the chart patterns of CRM Salesforce prior to the earnings report this week,

I would consider purchasing the 250usd strike price Puts with

an expiration date of 2025-6-20,

for a premium of approximately $5.15.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

Breaking key resistance — could $BGM repeat $RGC’s 100x rally?Let me introduce a stock that has already generated a profit of nearly 40% and I have no intention of selling it yet. Because both the chart and fundamentals suggest the stock seems to be approaching the point of potential explosion, and it is even possible to increase several times.

This stock is NASDAQ:BGM , a traditional Chinese pharmaceutical chemical company but now it has transformed into an AI productivty platform. More on that later—let’s first take a look at the technicals, which I always pay close attention to.

Firstly,the uptrend remains intact.

Since last year’s stock split, the price has been climbing steadily within a clear uptrend. After breaking above $8.50, it has consistently held above that level for months, showing strong momentum. (I bought in when it dipped back to $8.50 earlier this year and have held since.)

In the recent days, the stock price has successfully broken through the upper limit of the consolidation range that has persisted for nearly 3 months, and has stabilized above $12.

This is a significant breakthrough, and it may indicate that the stock price could potentially start a significant upward rally at any time.

Secondly,the stock is almost fully controlled by the market maker.

There’s a saying in trading: “Volume precedes price.” Since December 2024, BGM’s trading volume has clearly increased, with each spike in volume followed by a small price uptick—money was buying.

Interestingly, each rise is followed by a pullback, but on much lower volume. This volume pattern—rising on gains and shrinking on pullbacks—suggests that the maket maker have accumulated most of the shares and now have strong control. The dips are likely just shakeouts to flush weak hands before a bigger breakout.

Thirdly, low short interest means minimal resistance to a price surge.

According to Nasdaq's data, BGM’s short position was 34,466 shares by 31th March, but dropping to 18,889 shares by April 30,the number of short positions has significantly decreased.

This was showing that as the stock price rose, short sellers mostly exited or turned bullish—clearing major obstacles for further gains.

Technically, everything is set—just waiting for the trigger. Pull the trigger could spark a massive rally, and that trigger may come anytime as the company nears to complete a key transformation.

Yes, the company is transforming from a traditional pharmaceutical firm into a leading AI tech ecosystem. Since last year, it has been actively acquiring companies to enter AI-driven healthcare, insurance, and wellness sectors, aiming to become an industry leader.

①In December 2024, BGM acquired RONS Tech and Xinbao Investment, integrating the AI insurance platform “Duxiaobao” (powered by Baidu’s NASDAQ:BIDU technology). Leveraging 704 million monthly active users, they aim to disrupt traditional insurance sales and drive exponential customer growth.

②In April 2025, BGM acquired YX Management to boost AI applications in insurance and transportation, accelerating the “pharma-insurance-health” ecosystem.

③In May 2025, BGM acquired HM Management and its two subsidiaries—SHUDA Technology and New Media Star—strengthening its algorithm optimization、data modeling and traffic-driven customer acquisition capabilities

After several acquisitions, the company has initially completed its transformation plan. So the "trigger" we are pursuing might emerge during the next major acquisition by the company to complete the final transformation.This is an important milestone. According to reliable sources, the company's next acquisition is likely to take place in the coming June. Let's wait and see.

Another "trigger" may be the company’s next earnings report, which will include the “Duxiaobao” AI insurance business for the first time, expected to add over $5 million in revenue, might to confirm the initial success of the company's transformation. And this is potentially spark a strong stock rally.

These two potential "triggers" are both approaching soon.

If all goes well, how far could this rally go? Let’s refer to the recent strong gains of Chinese stocks like $RGC.

Technically, RGC saw a clear volume increase and price rise around July-August 2024. Then it had a six-month shakeout with low volume pullback (similar to BGM’s current pattern). In March 2025, it launched a major rally, rising over tenfold.

In May, RGC surged again, supported by fundamental news: the company announced FDA approval for its new neurostimulation chip and a Parkinson’s study with Mayo Clinic. From the start to the peak, RGC gained over 100 times in a short period!

Looking at BGM again: after the breakout, the stock will likely first test resistance near $15, which may not be a big hurdle. The real test could be at $24—the pre-split high and the upper boundary of the current “megaphone” consolidation.

Even if the price only reaches around $24 , current investors could nearly double their money. After the company’s fundamental transformation, its revenue and profits potential could grow beyond RGC. So, how high can BGM’s stock go? Let’s wait and see.

Salesforce: Further ProgressDue to continued downward pressure, Salesforce has made further progress in realizing our primary scenario. During the ongoing green wave , we still expect the stock to sell off below the support at $274. However, if the price imminently climbs above the resistance at $312, we will have to reconsider the structure of the ongoing decline and reckon with a magenta five-wave downward move. We currently assign this alternative scenario a 36% probability.

$CRM short setup part two. $280 target.Check out my recent post on $CRM. This name is down from it’s highs already 11% or so but 20% is correction territory so I can see this name hitting $280 area. $280-$285. Multi day put swing.

WSL

$CRM lower guidance, weak numbers, AI poopieNYSE:CRM should see sell pressure into the $285 zone and if it doesn’t hold expect $270’s.

WSL

Salesforce (CRM) – Bullish Setup AnalysisWeekly Chart – Cup and Handle Formation

• The stock has formed a classic cup and handle pattern on the weekly timeframe.

• Moving Averages (20 & 150) are trending upwards, supporting bullish momentum.

• After breaking out, CRM retested the breakout level as support and is now showing signs of continuation.

• The potential long-term target stands at +60% upside, aligning with the measured move projection.

Daily Chart – Consolidation & Breakout Retest

• The stock is currently trading within a converging channel, stabilizing near the breakout level.

• A wick rejection at the breakout price suggests strong demand at this level.

• Stochastic oscillator is turning upwards, indicating the start of a potential bullish cycle.

Final Thoughts

If momentum continues, CRM has the potential for a strong bullish move. Watching for confirmation and volume increase on continuation.

What’s your take on this setup? Let me know in the comments!

$FROG - About to fly! 129% Upside potentialNASDAQ:FROG

As I've been calling out for the past month Tech Services and SaaS companies are the next phase of Ai and very hot right now based on the massive moves after meh to good earnings from the likes of NASDAQ:TEAM NASDAQ:MNDY NYSE:NET NASDAQ:CFLT

I believe this trend continues and this small 4B Mkt Cap company could really get going after earnings on Thursday!

- CupnHandle forming while Bull Flag breaking out

- Two year trendline is our safety net

- Massive Volume Shelf with GAP

- H5 Indicator made bullish cross and is GREEN

- WCB has formed

PTs: $43/ $57/ $67/ $84

NOT FINANCIAL ADVICE

Don't miss the Next AI Gold Rush! WATCH NOW!In this video, we delve into the next phase of artificial intelligence and explore the companies set to benefit the most. From giants like Microsoft and Salesforce to rising stars like Snowflake and CrowdStrike, we break down how each company is harnessing AI to revolutionize their industries. Don't miss out on this deep dive into the tech titans leading the AI charge and shaping the future. Subscribe and hit the bell icon to stay updated on the latest in AI advancements! NASDAQ:CRWD NYSE:CRM NYSE:SNOW NASDAQ:MSFT NASDAQ:TEAM NYSE:PATH NYSE:SHOP NASDAQ:DDOG NYSE:NET NASDAQ:MDB

What companies are you positioned in or ready to start a position in?

Let me know in the comments below!