Can Robots Win America's Deep-Sea Mineral Race?Nauticus Robotics (NASDAQ: KITT) has pivoted from a speculative energy services company into a strategic asset positioned at the intersection of national security and resource independence. The company's transformation centers on autonomous underwater robotics designed to extract critical minerals from the deep seabed, a response to China's near-monopoly (80%+ control) over rare earth elements essential for defense systems and the green energy transition. Following President Trump's April 2025 Executive Order declaring seabed minerals a "core national security interest," Nauticus secured a $250 million equity facility. They announced its entry into deep-sea mineral exploration, positioning itself as the technological enabler for U.S. interests in what the report terms the "Blue Cold War."

The company's technological moat rests on its proprietary Aquanaut platform. This transformer-style autonomous underwater vehicle transitions from streamlined cruising to a hoverable work configuration paired with the electric Olympic Arm manipulator and ToolKITT software operating system. This technology stack offers 30-40% cost reductions over traditional crewed operations by eliminating expensive support vessels and replacing human labor with autonomous systems. Nauticus recently achieved critical milestones, including successful testing at 2,300-meter depths, NASDAQ compliance restoration (December 2025), and integration of its software into third-party ROVs, validating both technical capability and commercial viability. The licensing of ToolKITT to retrofit existing underwater vehicles represents a high-margin revenue opportunity across thousands of legacy assets.

However, significant execution risks temper this strategic positioning. The company burned $134.9 million in 2024 and posted only $2 million in Q3 2025 revenue, relying heavily on dilutive equity financing through its $250M facility (capped at 19.99% of shares). The pivot to deep-sea mining remains unproven at commercial scale. Surveying nodules differs vastly from extraction, and regulatory frameworks continue to evolve amid environmental controversies. Nauticus faces competition from well-capitalized Chinese state-owned enterprises and traditional dredging giants while navigating cybersecurity requirements (CMMC compliance) for defense contracts. The company remains under NASDAQ "Panel Monitor" status through December 2026, with any future violation triggering immediate delisting. Success depends on synchronized execution across technology scaling, government contract acquisition, and favorable policy momentum, making Nauticus a high-variance bet on whether autonomous robotics can indeed break China's stranglehold on critical minerals while surviving the precarious journey to profitability.

Deepseamining

Can One Company Own the Ocean Floor?Kraken Robotics has emerged as a dominant force in subsea intelligence, riding three converging megatrends: the weaponization of seabed infrastructure, the global energy transition to offshore wind, and the technological obsolescence of legacy sonar systems. The company's Synthetic Aperture Sonar (SAS) technology delivers range-independent 3cm resolution, 15 times superior to conventional systems. At the same time, its pressure-tolerant SeaPower batteries solve the endurance bottleneck that has plagued autonomous underwater vehicles for decades. This technological moat, protected by 31 granted patents across 19 families, has transformed Kraken from a niche sensor manufacturer into a vertically integrated subsea intelligence platform.

The financial metamorphosis validates this strategic positioning. Q3 2025 revenue surged 60% Year-Over-Year to $31.3 million, with gross margins expanding to 59% and adjusted EBITDA growing 92% to $8.0 million. The balance sheet fortress of $126.6 million in cash, up 750% from the prior year, provides the capital to pursue a dual strategy: organic growth through NATO's Critical Undersea Infrastructure initiative and strategic acquisitions, such as the $17 million purchase of 3D at Depth, which added subsea LiDAR capabilities. The market's 1,000% re-rating since 2023 reflects not speculative excess but a fundamental recognition that Kraken controls critical infrastructure for the emerging blue economy.

Geopolitical tensions have accelerated demand, with the Nord Stream sabotage serving as an inflection point for defense procurement. NATO's Baltic Sentry mission and the alliance-wide focus on protecting 97% of internet traffic carried by undersea cables create sustained tailwinds. Kraken's technology participated in seven naval teams at REPMUS 2025, demonstrating platform-agnostic interoperability that positions it as the universal standard. Combined with exposure to the offshore wind supercycle (250 GW by 2030) and potential deep-sea mining operations valued at $177 trillion in resources, Kraken has positioned itself as the indispensable "picks and shovels" provider for multiple secular growth vectors simultaneously.

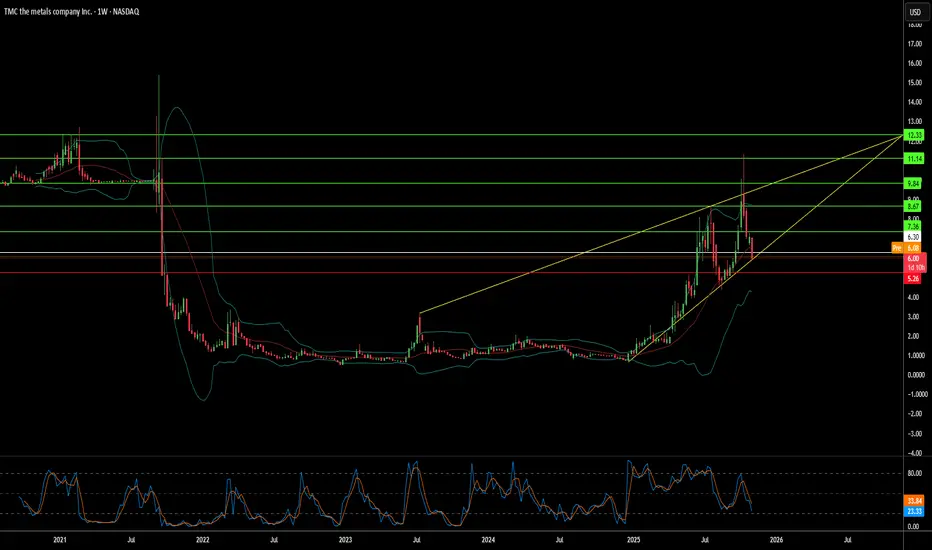

Can Geopolitics Justify a 53x Premium?The Metals Company (TMC) has experienced an extraordinary 790% surge year-to-date, achieving a Price-to-Book ratio of 53.1x, more than twenty times the industry average of 2.4x. This remarkable valuation for a pre-revenue company reflects not conventional profitability metrics, but rather a strategic bet on geopolitical leverage and resource scarcity. The catalyst driving this premium is the April 2025 reactivation of the Deep Seabed Hard Mineral Resources Act (DSHMRA), which enables TMC's U.S. subsidiary to pursue commercial deep-sea mining licenses independent of the United Nations' International Seabed Authority. This unilateral policy shift positions TMC as the primary instrument for U.S. critical mineral independence, bypassing years of international regulatory uncertainty.

The investment thesis centers on converging macroeconomic tailwinds and technological readiness. TMC controls massive polymetallic nodule reserves in the Clarion-Clipperton Zone containing an estimated 340 million tonnes of nickel and 275 million tonnes of copper—critical materials for electric vehicle batteries and renewable energy systems. Global demand for these minerals is projected to triple by 2030 under current policies and potentially quadruple by 2040 if net-zero goals are pursued. The company has successfully demonstrated technical feasibility through 2022 deep-sea collection trials that retrieved over 3,000 tonnes of nodules from depths of 4,000-6,000 meters, establishing a high-tech operational moat. An $85.2 million strategic investment from Korea Zinc at a premium price further validates both the technical viability of processing these nodules and the strategic importance of the resource base.

However, significant risks temper this optimistic narrative. TMC operates with zero revenue and persistent net losses, facing substantial dilution risk through warrants and a $214.4 million shelf registration signaling future equity raises. The company's DSHMRA strategy creates direct conflict with international law, as the ISA rejects any commercial exploitation outside its authorization as a violation of UNCLOS. The market is essentially engaging in regulatory arbitrage, betting that U.S. domestic legal frameworks will prove sufficiently robust despite potential enforcement actions from UNCLOS member states. Additionally, environmental concerns persist regarding the largely unknown deep-sea ecosystems, though TMC's Life Cycle Assessments position nodule collection as environmentally superior to terrestrial mining. The extreme valuation ultimately represents a calculated wager that U.S. strategic policy and the imperative for independent mineral supply will overcome both international legal challenges and scientific uncertainty surrounding deep-sea environmental impacts.

Fugro - Touch down, in UptrendInteresting Fugro opportunity.

1. Trendlines

2. Financials

3. Advises

4. Taking Positions

1. Trendlines

Bottom trendlines upwards (5Year), and top trendline downwards (10 Year) are crossing each other this week.

- The next 1-2 weeks is going to be an important in which direction the share will develop.

- Last 4 - 5 years minor trend line is trending up. Indicating most likely an upward trend following the latest trend and signals.

- The strong down trend line range from 10+ years breach needs to be confirmed.

This was tested the last week and the result looks promissing for an upward trend.

This test is the 3th time in the last year, and it's still holding exactly at the time it's crossing the lines.

Uptrend movements

Following past trendlines the potential for the coming 2-3 months can be 'quickly' reached at a stock price of 25,50 for new trend up tests. The potential here is around 20% depending on the moment you step in.

If this share is going up, probably you'll be to late. The trends up have shown big investors know where to step in at important moments. Take position with a good stop-loss.

2. Financials

- The last 5 year revenue and earning have shown an interesting upwards trend. Not placing al the numbers here. But it's going from a negative to positive an a straight and strong line each year.

- After a period where Fugro had to take it's time to make the business capable for a healthy future, 2024 was the fist year (after 5) to provide shareholders with Dividend (1,91%).

- Dept has been decreased with 50% the last 5 years and remains steady.

- Free Cash flow and equivelents is showing an healthy trend up.

3. Advises

- 7 analyst giving a strong buy advise with an avarage price target of 31,28 in 1 year. There are not any other advises then strong buy.

-The forecast for the coming 5 years is almost a double in revenue and earnings per share.

- The previous high at 25,50 (about 20%) can be reached in a couple of months and will be tested.

4. Taking Position

I have taken position at 20,04, but with a share price of 20,94 it's still worth the risk.

If you are in doubt place a stop - loss. There is great potential in this stock

============

What's in my mind in general what is Fugro about.

- Deepsea mining investigations is good for Fugro.

This is an hot toppic in the world. If US and Europe, Etc wants to be "less depending" on china's mining operations i.e. on Cobalt. there needs to happening something. And this is happening now..

- Fugro had broughtened it's market with Windmills and onshore activities . Making the risk for depending on orders in a specific marked lower.