Ferrari RACE Technicals Led Entry With 100% Upside in 2026

RACE is in a measured correction after its July 2025 ATH (~$517). A repeat of prior ~35% corrections (2018/19; 2022) implies a symmetry target near ~$336 (35% off $516), creating a high-quality “buy the pullback” setup for smart investors willing to scale in before fundamentals re-assert. With the current price around ~$400, a full 35% retrace would complete near the low-$330s; prior cycles then delivered outsized recoveries. We view the $330–$360 zone as a strategic accumulation area for 100%+ multi-year upside potential, with a 2026 bull target >$700 assuming backlog support, margin resilience, and successful new product execution. ATH/price data cross-checked from market sources.

________________________________________

Executive Summary

• Thesis: Ferrari remains the purest “luxury-automotive as luxury-goods” equity: scarce supply, sold-out order book into 2026, rising personalization, and a carefully staged electrification roadmap supported by the new Maranello e-building. Even with macro or tariff noise, Ferrari’s brand, pricing power, and capital discipline underpin premium multiples.

• Why now: The stock’s technical correction is doing the valuation work for you. Into weakness, we favor staged entries ahead of 2026 catalysts EV debut & deliveries; new model cadence; ongoing buybacks.

• Key risks we underwrite: macro wealth shocks; execution on first BEV; regulatory/tariff volatility; FX EUR/USD; and luxury demand rotation. Offsetting: backlog visibility, personalization mix, and buybacks.

________________________________________

Ferrari (RACE) Catalyst Scorecard and 2026 Outlook

1) 🏎 New Model Launches & Portfolio — 9/10

Fresh models e.g., Roma Spider, 296 family, 12Cilindri plus track-focused/limited series sustain mix and ASPs. Purosangue remains capacity-constrained by design ≤~20% of shipments, supporting scarcity. Notes: media and management have repeatedly referenced Purosangue caps and order pauses. Rumor watch: the market expects additional halo launches into 2026; specifics beyond official IR should be treated as provisional.

2) 🔌 EV & Hybrid Transition — 9/10

Ferrari’s e-building went live in 2024 to manufacture ICE, hybrid, and the first BEV, enabling in-house e-axles/battery work and flexible capacity. Management reiterated an EV unveiling in October 2025 with sales beginning 2026; external reporting often cites incremental capacity of ~6,000 units management hasn’t fixed a public number. Strategy: electrify without diluting brand character.

3) 💰 Pricing Power & Personalization — 9/10

Personalizations are a structurally expanding, high-margin revenue stream—running ~~20% of revenues by 2025 commentary—while ultra-limited models e.g., Daytona SP3, 499P Modificata add mix tailwinds. Ferrari consistently emphasizes “quality of revenues over volume.”

4) 🌍 Global Demand & Wealth Resilience — 8/10

Order visibility remains exceptional, with management and financial press citing books effectively filled into 2026 even amid tariffs and China softness; U.S./EU/Middle East wealth pools anchor demand. Hybrids already approach half of deliveries, de-risking compliance.

5) 📈 Order Backlog & Supply Discipline — 8/10

Production is deliberately capped; Purosangue constrained to protect exclusivity. Backlog sold-out deep into 2026 reduces cyclicality and protects margins through mix and scarcity.

6) 💵 Shareholder Returns & Capital Allocation — 7.5/10

Ferrari is methodically executing a multi-year €2bn buyback through 2026 alongside dividends, while maintaining heavy R&D and capex for electrification and new platforms. Recent IR updates confirm ongoing tranches.

7) ⚖ Tariffs & Trade — 7/10

The 2025 U.S.–EU deal reduced tariff pressure versus prior peaks, a modest tailwind to margins and pricing optics for EU autos; Ferrari has shown ability to pass costs to clientele.

8) 🏆 Brand & Competitive Moat — 9/10

Ferrari’s moat resembles top luxury houses more than automakers: waiting lists, repeat/collector buyers, F1 halo, and unrivaled pricing power. This underpins luxury-goods-like multiples and high returns. (Multiple third-party and IR references.)

9) ⚔ Competition & Luxury Peers — 6/10

Peers Lamborghini, McLaren, Rimac, etc. lack Ferrari’s breadth/brand equity. Luxury EV entrants pose incremental risk, but Ferrari’s pacing plus customer loyalty mitigate. General industry assessment; monitor EV launches from peers.

10) 📉 Macro & Economic Cycle — 6/10

Ferrari isn’t immune to wealth drawdowns; however, backlog and personalization provide buffers. Management has historically protected price/mix by flexing volumes if needed.

________________________________________

2026 Outlook What Must Go Right

• EV milestone: Successful first-BEV launch & deliveries with waitlists experience parity with hybrids; no brand dilution.

• Mix strength: Purosangue/12Cilindri/hyper/limited series maintain ASPs and margins; personalization share inches higher.

• Financial delivery: Hitting or beating upgraded plan markers into 2026 after Ferrari indicated it is tracking ahead on profitability versus the original 2026 targets.

• Capital returns: Continued cadence on the €2bn buyback; dividend growth within FCF discipline.

________________________________________

Valuation Snapshot

• Quality context: Ferrari’s 2024 print and IR commentary emphasize expanding mix/personalization and ahead-of-plan profitability into 2025/26. Refer to FY24 results + CMD updates.

• Peer framing: Treat RACE as luxury Hermès-like scarcity rather than auto OEM. This justifies premium EV/EBITDA and P/E vs mass OEMs, provided growth/margins hold.

• Multiple work: On pullbacks to the mid-$300s, implied 2026E EV/EBITDA compresses to attractive territory vs luxury comps assuming consensus-style growth/margins investors should plug house estimates.

________________________________________

Scenarios & Targets

• Bull ($700–$750) — Successful BEV introduction, backlog conversion, personalization >20% of sales, steady buybacks, and benign macro.

• Base ($580–$620) — Order book carries revenues; margins hold with disciplined volumes; EV ramps without profit drag.

• Bear ($350–$400) — Wealth shock or EV stumble; cancellations rise, mix weakens; tariff/FX pressure re-rates the multiple. Risk case consistent with technical $330s correction.

________________________________________

Entry & Risk Management Plan

• Where to buy: Scale in $360–$380; add aggressively $330–$360 35% measured-move zone.

• Sizing: For a diversified HNWI book, a core 1.5–3.0% NAV position, with room to add +100–150 bps on capitulation into the $330s.

• Stops/hedges: Soft stop on a decisive weekly break <$320; hedge via short auto-luxury basket or long USD if EUR strength risks translation.

• Time horizon: 18–30 months through 2026 catalysts.

________________________________________

Near-Term Catalyst Timetable rolling 12–18 months

• Oct 2025–1H 2026: First Ferrari BEV unveil → initial deliveries watch order intake, waitlist depth, option take-rate, margin commentary.

• Ongoing 2025–26: Buyback tranches; monitor IR posts for pace/size.

• Quarterlies/Capital Markets updates 2025–26: Mix/personalization trajectory; backlog commentary; Purosangue allocation discipline.

Ferrari

Ferrari (RACE) Catalyst Scorecard AND 2026 OutlookFerrari (RACE) Catalyst Scorecard AND 2026 Outlook

________________________________________

1. 🏎 New Model Launches & Portfolio (9/10)

Ferrari’s 2023–26 lineup is packed with high-end launches. Recent additions include the Roma Spider, SF90 XX, 296 Challenge, and 499P Modificata. Demand for the Purosangue SUV has been overwhelming, with early orders suspended and deliveries backlogged into 2026. Coming next: the 849 Testarossa plug-in hybrid deliveries H2 2025/Q1 2026 and the F80 hybrid hypercar limited series, ~1,200 hp. These models should sustain ASP growth and keep exclusivity intact.

________________________________________

2. 🔌 EV & Hybrid Transition (9/10)

Ferrari is phasing electrification deliberately. After hybrids like the SF90 and 296, Ferrari will unveil its first fully electric car in October 2025 deliveries start 2026. A new “e-building” in Maranello is ready to expand capacity by ~6,000 units annually. Ferrari is building in-house motors and batteries while still pledging to keep V12 ICE alive as long as possible. This balance between heritage and compliance ensures both regulatory cover and customer enthusiasm.

________________________________________

3. 💰 Pricing Power & Personalization (9/10)

Ferrari’s bespoke strategy fuels unmatched pricing power. Recent results showed hundreds of millions in incremental profit from high-priced halo models Daytona SP3, 499P Modificata and personalization demand. Personalization now represents nearly one-fifth of revenues. Carefully managed price hikes on core models, combined with ultra-limited editions, cement Ferrari’s position as the most profitable automaker per unit.

________________________________________

4. 🌍 Global Demand & Wealth Resilience (8/10)

About three-quarters of Ferrari’s sales go to repeat customers, and nearly half to collectors owning multiple Ferraris. The expanding global wealthy class adds to the demand pool. Ferrari’s sales are well balanced across regions; China is only ~10%, limiting exposure to that slowdown. Wealth concentration in the U.S., Europe, and the Middle East provides resilience against macro shocks.

________________________________________

5. 📈 Order Backlog & Supply Discipline (8/10)

Ferrari’s order book is sold out through 2026/early 2027. The company deliberately caps production e.g. Purosangue SUV shipments limited to ~20% of total to preserve scarcity. This ensures pricing discipline and supports margin expansion. With supply tightly managed, Ferrari avoids the discounting and inventory overhangs that plague mass-market automakers.

________________________________________

6. 💵 Shareholder Returns & Capital Allocation (7.5/10)

Ferrari’s capital return story is strong. Annual dividends and share buybacks together exceed €750 million. The €2 billion buyback program through 2026 is ongoing. At the same time, Ferrari invests aggressively in R&D e-building, hybrid/EV systems without margin erosion. The balance between shareholder distributions and future growth spending is a key investor confidence driver.

________________________________________

7. ⚖ U.S./EU Tariffs & Trade (7/10)

A recent U.S.–EU deal cut auto tariffs, enabling Ferrari to avoid planned price hikes in the U.S. and improving margins slightly. Regulatory pressure on emissions is real, but Ferrari’s measured EV roadmap addresses compliance. Trade risks are less critical for Ferrari than for volume automakers, but favorable deals add incremental margin upside.

________________________________________

8. 🏆 Brand & Competitive Moat (9/10)

Ferrari’s brand power is unmatched. It combines scarcity, desirability, and F1 heritage to justify luxury-goods multiples more in line with Hermès than Porsche. The brand enables Ferrari to command unmatched ASPs and maintain margins north of 25%. Ferrari’s intangible moat protects it against both cyclical demand dips and competitive threats.

________________________________________

9. ⚔ Competition & Luxury Peers (6/10)

Direct competitors—Lamborghini, McLaren, Rimac—lack Ferrari’s scale, heritage, and breadth. Luxury EV entrants pose some risk, but Ferrari’s controlled rollout and customer loyalty limit the threat. Peer comparisons place Ferrari firmly alongside high-end luxury brands, not mass-market automakers, underscoring its unique positioning.

________________________________________

10. 📉 Macro & Economic Cycle (6/10)

Ferrari is somewhat insulated but not immune. A sharp global downturn or wealth destruction could dampen orders. However, its backlog, exclusivity, and personalization revenue provide cushions. Even in recessions, Ferrari can slow production and still maintain pricing power.

________________________________________

Catalyst Scorecard

Rank Catalyst Score

1 New Model Launches & Portfolio 9.0

2 EV & Hybrid Strategy 9.0

3 Pricing Power & Personalization 9.0

4 Brand & Competitive Moat 9.0

5 Global Demand & Wealth Trends 8.0

6 Order Book & Supply Discipline 8.0

7 Shareholder Returns 7.5

8 U.S./EU Tariffs & Trade 7.0

9 Competition & Luxury Peers 6.0

10 Macro & Economic Cycle 6.0

________________________________________

Valuation Scenarios

• Bull Case ($700–$750): Successful EV debut, robust demand for new models, strong margins, continued buybacks.

• Base Case ($580–$620): Order backlog supports steady revenue growth, modest EV contribution, pricing discipline.

• Bear Case ($350–$400): Macro downturn or execution missteps lead to cancellations and lower margins.

Is Ferrari's stock still bullish?Is Ferrari's stock still bullish?

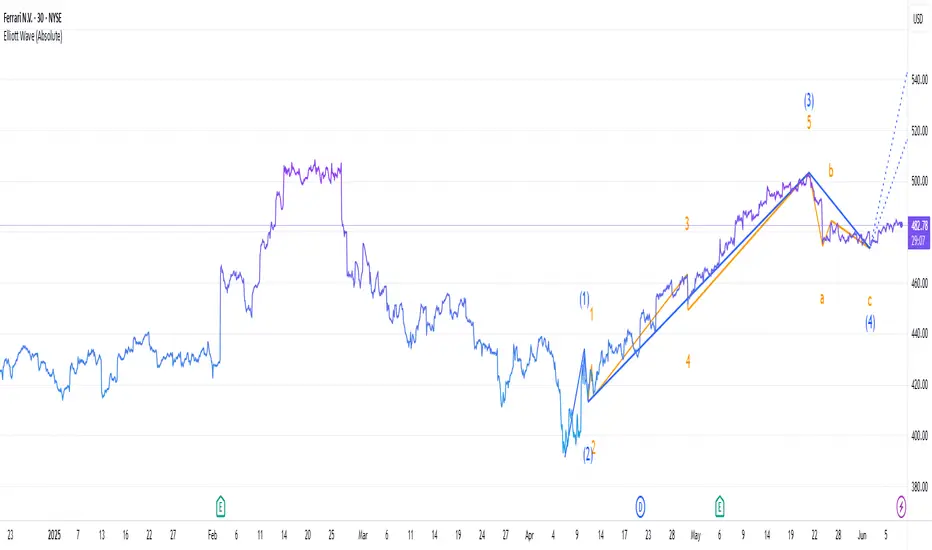

Technical Outlook

Elliot Wave theory suggests a cautious bullish stance. The present correction seems to be a temporary setback, likely driven by guidance and tariff fears, but sets the stage for a potential rally to $520-$540 if support is not broken. However, risks of a deeper correction (i.e., to $420-$440) persist if pressures from the outside intensify.

The stock is currently trading above all three of its major EMA levels — daily, weekly, and monthly — that is a good technical signal. The rising daily EMA at 479.98 suggests that short-run momentum remains healthy. The weekly EMA at 461.77 provides medium-term support, while the monthly EMA at 421.08 supports the longer-term trend solidly.

Positive Sentiment Factors

Ferrari reported robust Q1 2025 results, with net revenues of €1.79 billion (up 13% YoY), an operating profit of €542 million (up 22.7%), and a net profit of €412 million (up 17%). Adjusted earnings per share were €2.30, surpassing analyst expectations of €2.28. This shows Ferrari’s strong pricing power and demand for personalized vehicles.

Analyst Sentiment: Optimism remains for Ferrari among some analysts. UBS raised its price target to $560 from $520, maintaining a Buy rating, with the new Ferrari Elettrica a major catalyst, the company said. Bernstein and RBC Capital maintained Outperform ratings on the stock at $575 and €500, respectively. Barclays upgraded Ferrari to Overweight, calling it a "safe haven" in a shaky European automotive environment.

Brand Strength and Strategic Positioning: Ferrari’s luxury brand and high demand for models like the Roma Spider, 296 GTS, SF90 XX, and Purosangue bolster its market position.

Neutral Sentiment Factors

Market and Industry Context: The broader market has been volatile due to trade developments and tariff relief rallies. Ferrari’s stock has been influenced by these macroeconomic factors, but its luxury positioning makes it less sensitive than mass-market automakers.

Formula 1 Performance: Ferrari’s underwhelming Formula 1 season, with McLaren significantly outscoring Ferrari in points poses some concern among investors. While this does not directly impact stock performance, it may indirectly affect brand sentiment among enthusiasts.

Negative Sentiment Factors

Tariff Concerns: Ferrari shares have been sensitive to Trump's U.S. tariff policies. A tariff increase would add up to $50,000 to the price of an average Ferrari, potentially cutting sales volumes in the U.S., which accounts for 28.8% of net sales. JPMorgan warned that tariff impacts might be "worse" for Ferrari, lowering the price target to $460 from $525

Conclusion

Ferrari stock has a bullish but cautious bias, supported by solid fundamentals, favorable technical momentum, and positive analyst sentiment on upcoming product releases such as the Ferrari Elettrica. Macro risks, however, including U.S. trade policy and market volatility, are still major overhangs.

RACE (Ferrari) LONG SET UPEntry 1 $450.00

Entry 2 $440.00

Stop loss $430.00

Take profit 1- $460

(Close 33%)

Take profit 2- $480.00

(Close 66%)

Take profit 3-$500.00

(Close 100%)

RACE (Ferrari) – Quality has its PriceMIL:RACE has a technically interesting setup that also fits well with the weekly setup that I presented a few weeks ago.

The current consolidation has once again reached the lower zone and should find support from here one more time. Recently, a significant bounce was achieved from here several times. In addition, Ferrari is moving at the daily SMA 200 line and has bounced upwards from this (as well as from the horizontal support). In the 4h chart we see a nice RSI divergence as well as a breakout from a falling wedge. Both bullish signals.

Fundamentally, Ferrari is not cheap, but quality has its price. The backlog extends years into the future, the pre-order lists are full to bursting, the line-up presented is technically flawless and in demand and the cash flow is immense. In addition, the company is still family-owned (which secures the share price) and the current F1 season with Hamilton and Leclerc as the team should also be interesting.

We are initially targeting the area around EUR 438 and then the previous ATH at EUR 457. This results in an ROI of 10%. Should the daily closing price fall below EUR 400, the trade would be disqualified and closed.

Target zones

438 EUR

457 EUR

Support Zones

400 EUR

Ferrari - Don't Miss Out on 50% ROI!Very strong setup here. Ferrari respects the SMA200 for years and did touch the SMA200 and bounce from it. It also respected the current trendline and the SMA200 and trendline bounce did happen at the 23rd Fib retrace level. Very bullish setup.

--

🐂 Trade Idea: Long - RACE

🔥 Account Risk: 20.00%

📈 Recommended Product: Stock

🔍 Entry: +/- 426,00

🐿 DCA: No

😫 Stop-Loss: 390,00

🎯 Take-Profit #1: 600.00 (50%)

🎯 Trail Rest: Yes

🚨🚨🚨 Important: Don’t forget to always wait for strong confirmation once possible entry zone is reached. Trade ideas don’t work all the time no matter how good they look. Do not get a victim of FOMO, there is always another trade idea waiting. 🚨🚨🚨

If you like what you see don’t forget to leave a comment 💬 or smash that like ❤️ button!

—

Ferrari is a super strong brand. Backlog is huge and current waiting time is measured in years not months. Luxury stocks were punished during the last months because of fear of growth and a weak consumer but Ferrari is somewhat else. Misconceptions regarding shipments and China are putting pressure on Ferrari's shares since the third-quarter announcement. Nevertheless, the shipments' decline is a result of an ERP transition, and the reduction in China is intentional.

Don't forget, people who buy Ferraris do not care about inflation or the economic situation of a country. Also, you can't lease a Ferrari, you can only buy it. This gives the manufacturer a strong cashflow. In addition, Ferrari's unique market position, strong brand, and prudent management justify its high valuation and promise market-beating returns.

—

Disclaimer & Disclosures pursuant to §34b WpHG

The trades shown here related to stocks, cryptos, commodities, ETFs and funds are always subject to risks. All texts as well as the notes and information do not constitute investment advice or recommendations. They have been taken from publicly available sources to the best of our knowledge and belief. All information provided (all thoughts, forecasts, comments, hints, advice, stop loss, take profit, etc.) are for educational and private entertainment purposes only.

Nevertheless, no liability can be assumed for the correctness in each individual case. Should visitors to this site adopt the content provided as their own or follow any advice given, they act on their own responsibility.

Ferraci Stock $RACE swing long-term investment at weekly demandFerrari Stock NYSE:RACE swing long-term investment at weekly demand. The stock has reached a decent weekly demand level at $428 per share and it's trying to create a new bullish leg.

RACE (Ferrari N.V.) BUY TF M15 TP = 479.50On the M15 chart the trend started on Oct.3. (linear regression channel).

There is a high probability of profit taking. Possible take profit level is 479.50

This level, which I have outlined above, is certainly not a “finish” level. But it is the level that has the “highest percentage of hits on target.”

Using a trailing stop is also a good idea!

Please leave your feedback, your opinion. I am very interested in it. Thank you!

Good luck!

Regards, WeBelievelnTrading

Can a Prancing Horse Outrun an Electric Future?In the ever-evolving landscape of luxury automobiles, Ferrari stands as a beacon of innovation and exclusivity. The recent upgrade from J.P. Morgan, elevating Ferrari's status from "Neutral" to "Overweight," underscores the company's resilience and strategic prowess in navigating complex market dynamics. This vote of confidence, coupled with a substantial increase in the price target to $525, reflects Ferrari's unique position in the luxury sector and its ability to maintain growth even in the face of global economic challenges.

At the heart of Ferrari's success lies a paradoxical strategy that defies conventional wisdom: deliberately producing fewer cars than the market demands. This approach, rooted in the vision of founder Enzo Ferrari, has cultivated an environment of perpetual desire and scarcity. With a staggering backlog of 24 to 30 months, Ferrari has not only engineered exceptional vehicles but has also orchestrated an "underappreciated cultural evolution" within the company. This disciplined approach to growth, combined with the power to command premium prices, provides unparalleled visibility into future earnings and sets Ferrari apart from its luxury peers.

As the automotive industry races towards electrification, Ferrari is poised to redefine the boundaries of performance and sustainability. The company's foray into the electric vehicle market, promising an "incredible driving experience" that remains true to the Ferrari ethos, demonstrates its commitment to innovation while preserving its core values. However, this journey is not without obstacles. Ferrari must navigate challenges such as an ongoing investigation into its chairman and the conclusion of a key partnership with Santander. Yet, with strong financial performance, positive investor sentiment, and a clear strategic vision, Ferrari appears well-equipped to maintain its pole position in the luxury automotive market, promising a future as thrilling and exclusive as its storied past.

Ferrari Reported an Increase in Core Earnings Stock Down 0.61%Ferrari reported a 13% increase in core earnings in the first quarter of 2021, but its shares fell as the luxury sports car maker failed to excite investors. The Italian company said its quarterly results were boosted by pricing power, the mix of product sales, and a greater contribution from personalized vehicles. It also cited rising deliveries of its 2 million euro ($2.2 million) limited-series Daytona SP3 model. CEO Benedetto Vigna said Ferrari ( NYSE:RACE ) had produced double-digit growth for both revenue and profits despite stable car deliveries.

The company's adjusted earnings before interest, tax, depreciation and amortization (EBITDA) reached 605 million euros in January-March, in line with analyst expectations. However, shipment fell by seven units to 3,560, dragged by a 20% drop in the China, Hong Kong, and Taiwan region. Ferrari confirmed its forecast for full-year adjusted EBITDA to increase to at least 2.45 billion euros in 2024.

The company's net revenues of Euro 1,585 million, up 10.9% versus the prior year, with total shipments of 3,560 units $1flat versus Q1 2023. Adjusted EBIT(1) of Euro 442 million, up 14.8% versus the prior year, with adjusted EBIT(1) margin of 27.9%. Adjusted net profit of Euro 352 million and adjusted diluted EPS(1) at Euro 1.95 were up 12.7% versus the prior year, with adjusted EBITDA(1) margin of 38.2%.

The product portfolio in the quarter included nine internal combustion engine (ICE) models and four hybrid engine models, which represented 54% and 46% of total shipments, respectively. Revenues from Cars and spare parts were Euro 1,382 million, up 11.4% or 13.5% at constant currency(1). Sponsorship, commercial, and brand revenues reached Euro 145 million, up 11.6% or 12.0% at constant currency(1) attributable to new sponsorships, partially offset by lower Formula 1 ranking in 2023 vs. 2022. Other revenues were flat, with higher revenues from financial services activities offset by the decreased contribution from the Maserati contract which expired in 2023.

Currency had a negative net impact of Euro 26 million, mostly related to the Chinese Yuan, Japanese Yen, and US Dollar. Q1 2024 Adjusted EBITDA reached Euro 605 million, up 12.7% versus the prior year and with an Adjusted EBITDA(1) margin of 38.2%. Industrial free cash flow for the quarter was strong at Euro 321 million, driven by the increased Adjusted EBITDA, partially offset by capital expenditures of Euro 195 million and the increase in working capital, provisions, and other of Euro 71 million. As of March 31, 2024, the company was in a Net Industrial Cash position of Euro 38 million for the first time, compared to Net Industrial Debt of Euro 99 million as of December 31, 2023, also reflecting share repurchases of Euro 136 million.

Ferrari Races Higher, Bulls Eye $550 After Key Resistance BreakBuckle up, Ferrari (RACE) fans! The Italian Stallion is back in the driver's seat, and I am bullish after a crucial resistance level was shattered.

Ferrari stock surged past $370 resistance, a key technical hurdle that has capped the stock's potential for some time. This breakout suggests a bullish trend could be taking hold, with some expert analysts eyeing a potential surge to $550 in the coming months.

Ferrari Sets New Record Highs On Earnings

Ferrari (NYSE: NYSE:RACE ), the iconic luxury sports car manufacturer, is making headlines once again as its stock ( NYSE:RACE ) catapults to all-time highs, fueled by impressive Q4 earnings and the potential signing of Formula 1 legend Lewis Hamilton. The renowned racing driver, a seven-time World Drivers' Championship winner, could be donning the iconic red suit for Ferrari in the 2025 season, signaling a significant shift in the F1 landscape.

Earnings Triumph:

Ferrari ( NYSE:RACE ) reported Q4 adjusted earnings of 1.62 euros per share, exceeding forecasts with a 33% year-over-year increase. Net revenues for the quarter surged by 11% to 1.52 billion euros, surpassing FactSet analysts' expectations. The company delivered 1,493 cars to the EMEA market, while deliveries to the Americas rose by 6%. Despite a 25% drop in deliveries to China, Hong Kong, and Taiwan, Ferrari's ( NYSE:RACE ) overall performance paints a robust picture.

Full-year shipments rose by 3% to 13,663 vehicles, although China deliveries experienced a 4% decline. Notably, cars and spare parts revenue jumped by 12% to 1.29 billion euros for the quarter, showcasing the brand's enduring appeal and solid financial performance.

Strategic Guidance:

Ferrari ( NYSE:RACE ) provided optimistic guidance for 2024, expecting earnings to increase nearly 9% to 7.5 euros per share or more, with revenue projected to grow by about 7% to 6.4 billion euros or greater. Analysts at FactSet anticipate adjusted earnings of 7.53 euros per share on 6.45 billion euros in revenue, aligning with Ferrari's ( NYSE:RACE ) bullish outlook.

Lewis Hamilton's Potential Move:

In a surprising turn of events, reports suggest that Lewis Hamilton, a stalwart with Mercedes, might be on the verge of joining Ferrari ( NYSE:RACE ) for the 2025 season. The seven-time World Champion, who currently holds the record for the most Grand Prix victories at 103 wins, could form a formidable alliance with Ferrari's rising star, Charles Leclerc.

Hamilton's potential move adds an extra layer of excitement to the F1 narrative, as the partnership aims to challenge Red Bull's Max Verstappen, the current driver behind F1's dominance. If the speculated move materializes, it could mark a historic moment in the world of motorsports, bringing together one of the greatest drivers with one of the most iconic teams in the sport's history.

Market Reaction:

Investors responded swiftly to the positive earnings report and the Hamilton news, propelling Ferrari ( NYSE:RACE ) stock to a 12% surge to all-time highs. The move has positioned NYSE:RACE stock into a buy zone. The stock's strong ascent has also propelled it above its 50-day moving average, signaling continued market enthusiasm.

Conclusion:

Ferrari's ( NYSE:RACE ) record-breaking performance, both on the financial front and the potential addition of Lewis Hamilton to its roster, underscores the brand's enduring appeal and strategic vision for F1 dominance. As the luxury carmaker revs up for the future, investors and racing enthusiasts alike are eagerly anticipating the unfolding chapters in Ferrari's ( NYSE:RACE ) storied history. The convergence of financial success and high-profile partnerships positions Ferrari as a driving force in both the automotive and motorsports industries.

FERRARI: GARTLEY detected + Monitor GapsFERRARI: GARTLEY detected + Monitor Gaps

On the rise:

-possible rebound on the GAP around 327

On the decline :

-return to the EMA.50 around 314

-Then Gap, around 311

-and then EMA.200 around 288.

Pay attention to the GAP at the bottom, around 208

#RACE What recession? Ferrari racing away!i0.wp.com

Stock has broken out of this broadening pattern to reach new all-time highs with a measured target of at least $360.00 after beating expectations and and raising guidance.

Ferrari Stock Is on Track to Hit All-Time Highs — WSJ

Nov 3, 202321:31 GMT+2

RACE

+1.78%

By Hardika Singh

The company that makes some of the hottest cars in the world has a hot stock.

Ferrari shares recently rose 2.4% to $331 Friday, on course to set at a record high, after the Italian sports-car maker on Thursday reported earnings (www.wsj.com) that exceeded expectations.

The company raised its full-year guidance after profit jumped 45% and revenue grew 24% in the third quarter from a year ago, thanks to a better sales mix and higher demand for vehicle customization.

Ferrari shares are up 54% this year.

Ferrari to Start Accepting Crypto Payments in U.S: ReutersFerrari (RACE) will start accepting cryptocurrency as a payment method in the U.S., according to a report by Reuters on Saturday.

The Maranello, Italy-based luxury sports car manufacturer will subsequently extend the scheme to Europe in response to demand from its wealthy customers, Reuters reported, citing Chief Marketing and Commercial Officer Enrico Galliera.

Ferrari will use crypto payments provider BitPay to process transactions in bitcoin (BTC), ether (ETH) and stablecoin USD coin (USDC) in the initial rollout in the U.S.

Some are young investors who have built their fortunes around cryptocurrencies," Galliera said. "Some others are more traditional investors, who want to diversify their portfolios."

Despite crypto's popularity as an investment tool, for major companies to accept it as method of payment remains rare. In February 2021, Elon Musk's electric-car company Tesla (TSLA) began accepting bitcoin payments but discontinued the service only three months later, citing environmental concerns over the electricity usage involved in bitcoin mining.

Neither Ferrari nor BitPay immediately responded to CoinDesk's request for comment.

Ferrari begins accepting crypto currency as means of paymentThis is huge for Ferrari and we are expecting a surge in price for the RACE Ferrari stock

Race Ferrari:Hitting the Brakes on a Volatile Day

Race Ferrari (NYSE) presents an enticing opportunity for investors looking to go long in the luxury automotive sector. Ferrari, known for its iconic brand and high-performance vehicles, has demonstrated resilience amid economic uncertainties.

One compelling reason to consider a long position is Ferrari's strong brand loyalty and demand for its premium cars, which has shown no signs of waning. Additionally, as the global economy recovers, luxury car sales tend to rebound strongly.

With a track record of steady growth and a commitment to sustainability, Ferrari is well-poised for future success. Its expansion into electric vehicles and continued focus on innovation ensures it remains at the forefront of the automotive industry.

Furthermore, technical analysis reveals positive signals, including moving averages and relative strength index (RSI), supporting a bullish outlook.

While no investment is without risks, Ferrari's unique market position and promising future prospects make it an attractive choice for those considering a long-term investment strategy in the automotive industry.

FERRARI ($RACE) at the resistance area!From a technical point of view, Ferrari ( NYSE:RACE ) Stock Trend is bullish, but at the same time it has reached an important resistance area around $300/320, and from here it could trigger a short-term corrective structure. The minor structure 12345 might be completed, but as we can see from the chart, it might be a wave 5 of 3 (major), so once the correction is completed, I don't rule out a new bullish leg.

Trade with care!

Like if my analysis is useful.

Cheers!

Ferrari Rising Wedge in Long TermWhen we look at the Ferrari graph on an annual basis, we see a rising wedge. Generally, assuming the wedge has broken downwards, the next target will be the $150 level. If we need to support this technical analysis with fundamental analysis, it is striking that especially the PEG ratio is too high. As long as the wedge doesn't break higher ($218), I will keep the $150 level as a target. When it reaches the $150 level, I will analyze the target again on my page for a buying opportunity.

RACE-Ferrari Ferrari symbol in the stock market.

The price has broken the downtrend line and will correct.

To notify the analysis, follow me and contact me if you have any comments or questions.

RACE- Ferrari N.VI analyzed the Ferrari symbol in the stock market.

Follow me, like, comment, and ask questions.

For the Long-term time frame, there is still an upward trend.

However, the price in the mid-term time frame is corrected in a wedge.

So it can find an entry zone to buy after the end of the correction.

Observe the money management and the stop loss.

RACE | Ferrari A Ditching CarMy position and play is marked on the chart. Expecting selling to continue and target is the bottom zone at $206-$209 level.

FERRARI (RACE) in support Ferrari (RACE) is near 192€ former resistance, that should work as a support this time. It's also at the bottom of a 3 year channel.

Could be an entry point if we see any interesting pattern.