GRAB Holdings Options Ahead of EarningsIf you haven`t bought the dip on GRAB:

Now analyzing the options chain and the chart patterns of GRAB Holdings prior to the earnings report,

I would consider purchasing the 7usd strike price in the money Calls with

an expiration date of 2028-1-21,

for a premium of approximately $0.73.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Grabholdings

GRAB Holdings Options Ahead of EarningsIf you missed buying GRAB before the rally:

Now analyzing the options chain and the chart patterns of GRAB Holdings prior to the earnings report,

I would consider purchasing the 7usd strike price in the money Calls with

an expiration date of 2028-1-21,

for a premium of approximately $0.84.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

I’m extremely bullish on GRAB Holdings, the leading super-app in Southeast Asia powering ride-hailing, food and parcel deliveries, fintech, and more.

With strong growth, improving fundamentals, and powerful long-term tailwinds, GRAB looks well positioned for significant upside heading into 2026.

Here’s why:

1️⃣ Path to Sustained Profitability:

GRAB has recently turned profitable, marking a major inflection point in its business model.

Adjusted EBITDA continues to improve, supported by strong execution and disciplined cost control.

Management guides toward segment-level breakeven, including Financial Services, by H2 2026.

Revenue growth remains solid at 15–20%+ YoY, while earnings are projected to grow at ~39.5% annually, significantly outpacing industry averages.

This shift from growth-at-all-costs to profitable growth is a key re-rating driver.

2️⃣ Analyst Upgrades and Strong Consensus:

Wall Street sentiment is clearly improving.

HSBC upgraded GRAB to “Buy” in January 2026.

Benchmark reiterated its “Buy” rating, citing a constructive FY2026 outlook.

Overall consensus sits at Buy / Strong Buy, with average price targets in the $6.38–$6.96 range, implying 25–40%+ upside from recent levels.

Firms such as Mizuho have raised targets to $7, reflecting growing confidence in execution and margin expansion.

3️⃣ Uber’s Strategic Stake:

Uber remains GRAB’s largest individual shareholder, holding approximately 13–14% of the company.

While reduced from the original 27.5%, this stake still provides:

Strong external validation

Strategic alignment

Long-term optionality

GRAB effectively capitalized on Uber’s regional exit to become the dominant mobility and delivery platform in Southeast Asia.

4️⃣ Strategic Acquisitions and Forward-Looking Partnerships:

GRAB is actively investing in next-generation logistics and mobility.

January 2026: Acquisition of Infermove, an AI-enabled robotics company aimed at improving first- and last-mile delivery efficiency.

Partnerships with May Mobility and Momenta to explore autonomous mobility and robotaxi deployments targeted for 2026.

EV fleet expansion agreements, including a deal with GAC International for up to 20,000 electric vehicles.

These initiatives strengthen GRAB’s tech moat and position the company for leadership in AI-driven, sustainable transportation.

5️⃣ Bullish Technical Setup:

From a technical perspective, GRAB is also starting to align.

Breakout from a long-term consolidation range

Holding key macro support levels

Momentum indicators remain constructive

If fundamentals continue to deliver, charts suggest potential continuation toward $7–$8+ in the medium term — with pullbacks offering attractive entry opportunities.

🔚 Bottom Line:

GRAB sits at the intersection of profitability inflection, analyst upgrades, strategic execution, and long-term secular growth in Southeast Asia.

With improving margins, expanding earnings power, and multiple catalysts ahead, GRAB looks increasingly attractive as a 2026 upside play.

GRAB | The Time Has Come | LONGGrab Holdings Ltd. engages in the provision of millions of people each day to access its driver- and merchant-partners to order food or groceries, send packages, hail a ride or taxi, pay for online purchases or access services such as lending, insurance, wealth management and telemedicine, all through a single "everyday everything" app. The firm operates in food deliveries and mobility and by TPV in the e-wallets segment of financial services in Southeast Asia. It operates across the deliveries, mobility and digital financial services sectors in eight countries namely: Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam. The company was founded by Anthony Tan Ping Yeow and Tan Hooi Ling in 2012 and is headquartered in Singapore.

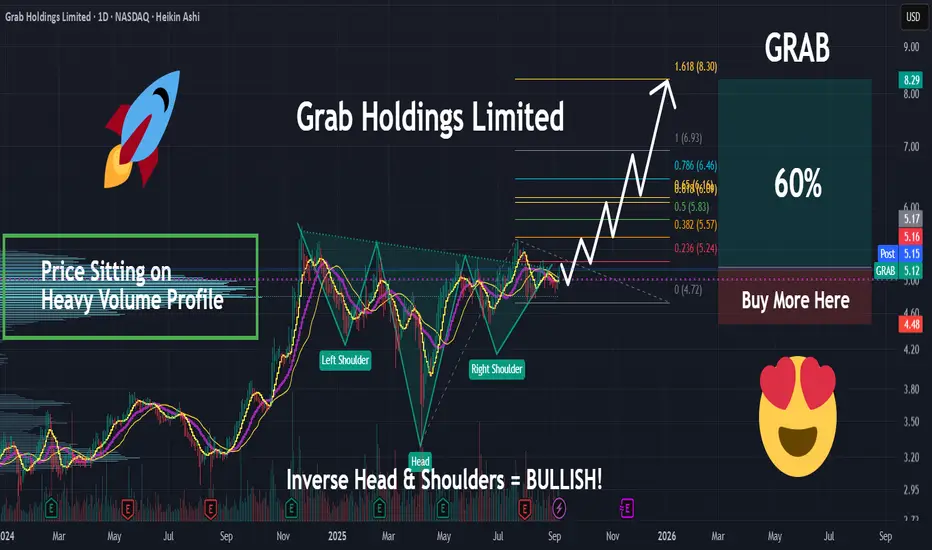

GRAB — Breakout Confirmation and Strong Upside PotentialGrab Holdings (GRAB) is currently forming a promising technical setup supported by a breakout from long-term consolidation. After printing a strong low and breaking out of a multi-year range, the price action confirms a bullish reversal with clear structure.

Technical Analysis

– Trendline breakout and bullish market structure shift

– Price is consolidating above the breakout level, forming a continuation zone

– Valid entries: market execution above $4.50 or limit orders near $4.00 support

– First profit target: $6.60 (around 40% growth)

– Second target: $10.15 (over 100% from entry)

The setup suggests increasing bullish momentum. A clean consolidation above previous resistance strengthens the case for a breakout continuation toward $6.60 and potentially $10.15.

Fundamental Backdrop

Grab is a Southeast Asian tech leader operating across ride-hailing, food delivery, and digital payments. The company continues to reduce losses, improve margins, and expand its fintech arm. With rising digital adoption in the region and a shift toward profitability, GRAB is gaining investor attention. Its most recent earnings report showed improving revenue trends and narrowing net losses — a strong signal of long-term sustainability.

Conclusion

Grab Holdings presents a well-aligned opportunity from both a technical and fundamental perspective. With a clear structure, breakout confirmation, and fundamental turnaround, this setup fits both swing and midterm investment strategies. Risk management is still key — stops should be placed below consolidation lows or key structure levels.

$GRAB yourself some GAINS!NASDAQ:GRAB yourself some GAINS!

The longer the base, the higher the space!

Lots of retail and super investors buying this name.

A train that goes in motion stays in motion...

- Wr% is in motion to the Green Support Beam.

Typically, this name would probably pull back with the direction of the Wr%, BUT... this stock is getting hyped up by a lot of super investors and retail investors right now. I think this week we will see a large move upward as HYPE creates FOMO which takes the stock HIGHER!

Staying patient here...

Not financial advice

GRAB Holdings Options Ahead of EarningsIf you haven`t bought GRAB ahead of the previous earnings:

Then analyzing the options chain and the chart patterns of GRAB Holdings prior to the earnings report this week,

I would consider purchasing the 3usd strike price in the money calls with

an expiration date of 2023-10-20,

for a premium of approximately $0.45.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

GRAB Holdings Options Ahead Of EarningsAnalyzing the options chain of GRAB Holdings prior to the earnings report this week,

I would consider purchasing the 4usd strike price Calls with

an expiration date of 2024-1-19,

for a premium of approximately $0.50.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Looking forward to read your opinion about it.

GRAB Holdings Options Ahead Of EarningsLooking at the GRAB Holdings options chain ahead of earnings , I would buy the $3.50 strike price Calls with

2023-3-17 expiration date for about

$0.32 premium.

If the options turn out to be profitable Before the earnings release, I would sell at least 50%.

Looking forward to read your opinion about it.

Grab- First target of 50% rewardTypical cup and handle pattern. Let's wait until it break through the resistance. A reachable upward profit targeting for at least 50% gain.

GRAB Grab Holdings Limited Options Ahead Of EarningsLooking at the GRAB Grab Holdings Limited options chain, i would buy the $4 strike price Puts with

2022-9-16 expiration date for about

$0.30 premium.

Looking forward to read your opinion about it.