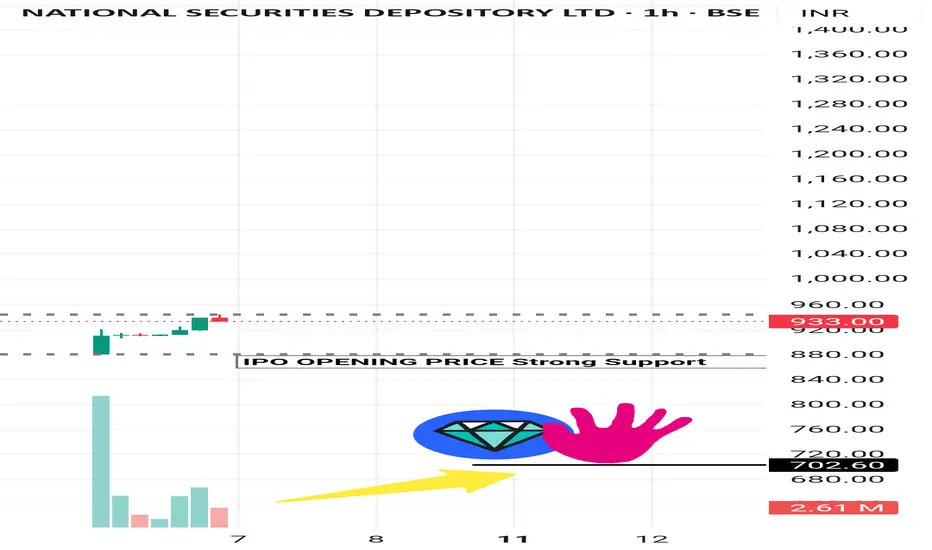

NSDL | Post‑Listing Surge Near ₹1,425Summary

After listing at ₹880 on Aug 6, NSDL rallied to ~₹1,425 within four sessions before profit‑taking; near‑term P/E ~77–79 vs peer CDSL ~66, so momentum may pause into the Aug 12 results.

Chart Thesis

Structure: Parabolic advance from ₹880 to ₹1,425, followed by intraday rejection—first meaningful pullback likely to set a higher low above ₹1,200 if the trend is to continue.

Levels:

Long zone: ₹1,200–₹1,250

Invalidation: Close <₹1,160

Targets: ₹1,360 → ₹1,400–₹1,425

Note: Event risk—board meets Aug 12 to consider Q1 FY26; expect swings.

Fundamentals

FY25 revenue +~12% to ₹1,420–1,535cr; PAT ₹343cr (+~25% YoY); near‑duopoly advantages but valuation now full post‑rally.

Plan

Avoid chasing strength; buy dips only with tight risk and take partials near prior highs. Investors with IPO gains can book some profits and hold a core for the long term.

Disclaimer: Educational, not investment advice. Manage risk.

Nsdl

NSDL (INTRESTING STOCK )👉🏻 NSDL – Equity Snapshot 👈🏻

🕛 Conclusion ⏱️

NSDL stands at a strategic inflection point — evolving from an institutionally heavy, legacy infrastructure provider to a retail and digitally agile depository. With a zero-debt model, strong cash flows, and clear retail growth plans underway, NSDL shows potential for steady earnings expansion and margin improvement over the next few years. The foundation is strong; execution will now drive the delta.

🙋🏻 Introduction

India’s largest depository by value, with over ₹450 lakh crore in Assets Under Custody (AUC).

Founded in 1996, primarily serving institutional and corporate clients.

Known for stability, trust, and core infrastructure services in the capital market.

🌸 Financial Performance (FY25)🌸

Total Revenue: ₹1,535 crore.

Depository Business Revenue: ₹660 crore (Approx. 43% share).

Operating Margin (Core Business): ~50%.

Net Margin: 22% – 24%.

Net Profit: ₹330+ crore.

Free Cash Flow: ₹558 crore+.

Debt: Zero (Fully debt-free).

Capital Expenditure: ~₹74 crore only (Low capex model).

🌸 Market Position🌸

Dominates in value terms (highest AUC in India).

Client base includes mutual funds, banks, insurers, and corporates.

Retail demat accounts: ~4 crore (behind CDSL’s 15+ crore).

High average demat account size (~₹1,100 crore) vs CDSL’s retail-heavy base.

Gaining ground in retail via partnerships with Zerodha, Groww, Angel One, etc.

🌸 Future Growth Focus🌸

Aggressively entering retail segment through schemes like ‘YUVA Plan’.

Enabling paperless, digital onboarding for faster account growth.

Investing in blockchain, T+1 settlements, and smart compliance tools.

Actively participating in SEBI & RBI-led digitization (e-KYC, e-insurance, GIFT city).

Expanding subsidiaries (NDML, NPBL) to boost recurring income beyond core biz.

🌸 Key Positives🌸

Strong free cash flow, high annuity-based revenue visibility.

Lean, tech-driven operations with low employee cost base.

Well-positioned to benefit from India’s growing retail investor base.

Diversified, recurring revenue streams through subsidiaries.

Digital-first strategy ensures scalable, low-cost growth ahead.

CDSL | Flagpole | NSDL Files for IPO

• NSDL has filed its DHRP, leading to market concerns that investors might shift their funds to NSDL, potentially affecting CDSL.

(We'll be sharing a detailed comparison for NSDL and CDSL in the comments section below. Feel free to follow us for the updates.)

Now CDSL:

• In the last 13 months, it's formed a beautiful Flag Pole pattern. The breakout of which is already done.

• The 1000 level + 50% Fibo level provided support during its momentum.

• Volumes increased during the rally, which is a positive sign.

• It faces a crucial resistance zone the break and sustenance of which will be necessary.

• Now if you are worried about the funds flowing to NSDL, Remember what happened to BSE when NSE announced its IPO – it literally doubled in value. NSDL's valuation will play a crucial role in boosting CDSL's momentum.

• Duopolies, like Ola and Uber, Airtel and Jio, Swiggy and Zomato, Amazon and Flipkart, tend to fare well. CDSL and NSDL too can coexist.

• Do you know who else can and must Coexist? YOU and WE! Follow us for such interesting Case studies.

Have Insights or Questions? Let us know in the comments below.👇

While you do that, how about a boost for some motivation 🚀

⚠️Disclaimer: We are not registered advisors. The views expressed here are merely personal opinions. Irrespective of the language used, Nothing mentioned here should be considered as advice or recommendation. Please consult with your financial advisors before making any investment decisions. Like everybody else, we too can be wrong at times ✌🏻