Alexandria Real Estate (Revised) | ARE | Long at $45.00**This is a revised analysis from January 13, 2025:

I am still in that position ($97.41) but adding heavily now that the price has entered my selected "crash" simple moving average zone.

Technical Analysis

The trading price of Alexandria Real Estate NYSE:ARE has now reentered the "crash" simple moving average zone. The price first entered this zone back in October 2023. This rare, long-term double entry into this zone is often a (at least short-term) bottom indicator. But I remain heavily cautious here given the financials of this company. My reentry is an exit plan since this is a company I do not wish to hold longer than I have to.

Pros:

Fair value: $103.00

Intrinsic Value: $96.00

Forward P/E: 31x (current P/E in the negative)

Annual Dividend: 6.37% (Quarterly dividend just cut by 45%, so hopefully bad news is done for now...)

Debt-to-Equity: .8x (not bad)

Cons:

Bankruptcy risk is high: Altman's Z Score = .7

Inability to pay recent bills is high: Quick ratio = 3.5

REIT sector is in rough shape

More dividend cuts?

Action:

I originally underestimated the downfall of the REIT sector. This company's financials are questionable. From a technical analysis perspective, a short-term bottom may be in. However, there is more room to fall and the next support zone is down in the $30's. My hope is that the shift in interest rates will push more investors into dividend / value plays. While most investors would cut their losses and be out here, I'm not. Personally, *as long as NYSE:ARE doesn't keep cutting its dividend and the fundamentals do not get worse,* I am cost averaging down to hopefully escape soon. There are much better investments out there than NYSE:ARE , but patience often pays - or allows you to break even. I'll be the contrarian.

Targets into 2028:

$53.00 (+17.8%)

$69.00 (+53.3%)

Reit

Potential outside week and bearish potential for CQEEntry conditions:

(i) lower share price for ASX:CQE below the level of the potential outside week noted on 4th/5th December (i.e.: below the level of $3.01).

Stop loss for the trade would be:

(i) above the high of the outside week on 3rd December (i.e.: above $3.18), should the trade activate.

VICI Investment ThesisVICI looks like a very interesting setup right now following its recent pullback to roughly $27.73. Even though the company delivered a beat-and-raise quarter in Q3 2025 and announced a transformative $1.16 billion transaction with Golden Entertainment in November, the stock has de-rated. It is currently trading at an 11.7x P/AFFO multiple. This is a significant discount to its historical trading range, which is typically 14x–16x.

In my view, the market is mispricing just how resilient this business is. With 100% occupancy, 40 year Weighted Average Lease Term (WALT) and a fully covered 6.5% dividend yield VICI is pretty good stock of the gaming sector. I'm initiating my outlook with "Buy" rating and around 4 month price target of $35.00 which means 26% upside.

Regarding Funds From Operations, VICI grew AFFO per share by 5.3% YoY in Q3 2025 to reach $0.60. This growth was because of rent escalators and the funding of the Venetian investment. VICI raised its FY2025 guidance to $2,510–$2,520 million which signaling confidence in continued cash flow expansion.

The recent stock drop, which was roughly a 10-12% correction in November and December is because of broader rate volatility or sector rotation rather than company fundamentals in my opinion. I view this as a technical capitulation point.

Bearish potential detected for ASKEntry conditions:

(i) lower share price for ASX:ASK along with swing of DMI indicator towards bearishness and RSI downwards, and

(ii) observing market reaction around the share price of $1.37 (open of 26th August).

Depending on risk tolerance, the stop loss for the trade would be:

(i) above the potential prior resistance of $1.43 from the open of 7th November, or

(ii) above the potential prior resistance of $1.45 from the open of 19th September, or

(iii) above the recent swing high of $1.48 from 24th October.

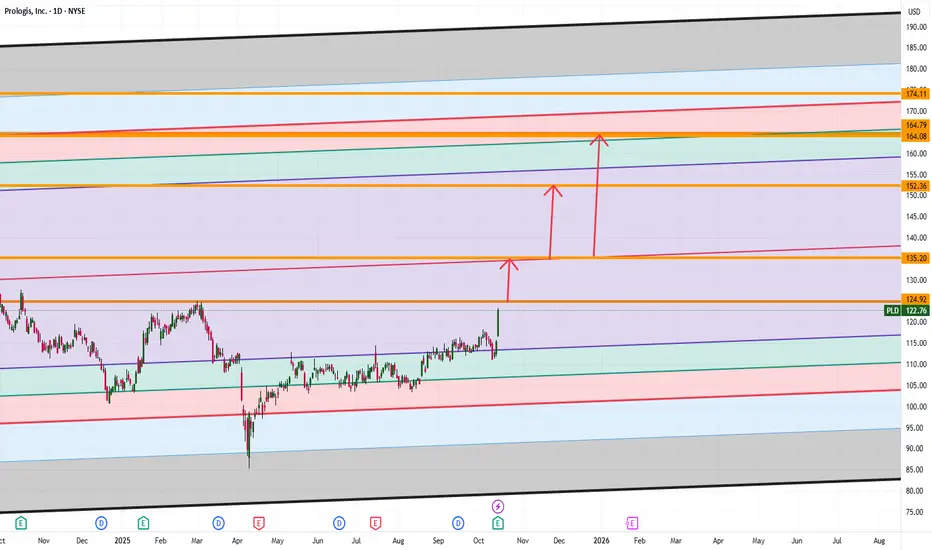

Prologis (PLD) Simple Market Breakdown!PLD’s been showing solid momentum lately 📈 and here’s the key zone I’m watching:

✅ If we break and hold above 124.92, the next target zone is around 135.20.

⚠️ At that level, we could see some correction or sideways movement (a bit of rest before the next move).

🚀 But if PLD breaks above 135.20 and holds, that could set up the next big leg toward 152, and possibly 164.

💡 So short-term; watch for a small pause. Long-term; momentum still looks strong if we keep closing higher.

Want to see how I’m mapping out the next levels and what signals I’m tracking for confirmation?

💬 DM me “PLD” and I’ll send you the full chart breakdown directly.

Mindbloome Exchange

Trader Smarter Live Better

Agree Realty | ADC | Long at $72.37Agree Realty NYSE:ADC

Summary: A "boring" REIT with a 4.2% dividend, ~68% investment-grade tenants, high occupancy (~99%), average lease terms of 10+ years, which include major tenants Walmart (top tenant), Dollar General, Tractor Supply, Best Buy, Dollar Tree, TJ Maxx, O'Reilly Auto Parts, CVS, Kroger, Lowe's, Hobby Lobby, Burlington, Sherwin-Williams, Sunbelt Rentals, Wawa, Home Depot....

Technical Analysis: Cup and handle formation may be forming off the recent double bottom (bullish). Two open price gaps remain on the daily chart since 2020 (down near $59) - chance these may get closed if the market turns in the near-term. However, REITs average +30% returns within 16 months post-Fed rate cuts, so patience may benefit investors here.

Follow the Money : Insiders buying .

Company Financial Health: Strong. $2.3B liquidity, no material debt maturities until 2028, and investment-grade balance sheet (A- rating from Fitch). Debt-to-assets ~40%, covered by stable net-lease rents. Macro risks (e.g., tenant bankruptcies like At Home, consumer slowdown) exist but are mitigated by diversification. Altman Z-Score suggests low distress and no near-term catalysts for insolvency.

Earnings and Revenue Growth: ~4% between 2025 and 2027 (slow growth, but good/steady for a REIT).

Thus, at $72.37, NYSE:ADC is in a personal buy zone for a likely move up given the high probability of lower interest rates in the future. A near-term risk of a drop to $59 could occur, but REITs often move higher within 1-2 years after interest rates cuts. It's a solid company financially with a good dividend.

Targets into 2028:

$80.00 (+10.5%)

$90.00 (+24.3%)

Americold Realty Trust | COLD | Long at $13.28Americold Realty Trust NYSE:COLD

Technical Analysis:

The price is currently touching the top of my "crash" historical simple moving average bands (green lines). This area is often reserved for share accumulation and can signal a bottom. The price, however, may extend to the bottom of "crash" bands which is currently near $11.80. These bands don't always signal a bottom - there is a still a "major crash" zone - but with interest rates likely dropping in the next 1-2 months, REIT's are poised to benefit as money flows into dividend-paying stocks ( NYSE:COLD dividend is just over 6%).

Earnings and Revenue Growth

EPS and revenue growth are expected between 2025 and 2028 (while REITs are rarely high-growth, the future appears relatively good for the company - especially if their debt levels drop)

www.tradingview.com

Health

Debt-to-Equity: 1.29x (not great, but not terrible)

Altman's Z-Score/Bankruptcy Risk: .5 (high risk - likely higher than 50% chance the company could go bankrupt in the next 24 months *if* interest rates don't drop, but ....)

Market Niche

NYSE:COLD operates in a specialized sector with high barriers to entry due to the capital-intensive nature of building and maintaining temperature-controlled facilities.

The company is an esential service - critical for food safety and pharmaceutical integrity, providing stable demand even in economic downturns.

The company's extensive network ( NASDAQ:KHC , NYSE:CAG , NYSE:WMT , etc) and global footprint (facilities in the US, Australia, New Zealand, Canada, and Europe give it a competitive edge over smaller players.

Insiders

$2 million in recent insider purchases near $17.

openinsider.com

Action

Due to the high likelihood of interest rate lowering and the market niche NYSE:COLD has as a REIT, I am personally going long at $13.28 and will liekly add more share in the $11 range *if* fundamentals improve. Major warning is bankruptcy risk.

Targets in 2028

$15.00 (+12.9%)

$18.60 (+40.1%)

Bullish potential detected for HDNEntry conditions:

(i) breach of the upper confines of the Darvas box formation for ASX:HDN

- i.e.: above high of $1.31 of 9th May (most conservative entry), and

(ii) swing up of indicators such as DMI/RSI along with a test of prior level of resistance of $1.31 from 31st October 2022.

Stop loss for the trade (based upon the Darvas box formation) would be:

(i) below the support level from the low of 15th May (i.e.: below $1.24).

Potential outside week and bullish potential for CQREntry conditions:

(i) higher share price for ASX:CQR above the level of the potential outside week noted on 6th June (i.e.: above the level of $4.10).

Stop loss for the trade would be:

(i) below the low of the outside week on 2nd June (i.e.: below $3.91), should the trade activate.

Bullish potential detected for ABGEntry conditions:

(i) higher share price for ASX:ABG along with swing up of indicators such as DMI/RSI.

Depending on risk tolerance, the stop loss for the trade would be:

(i) a close below the 50 day moving average (currently $1.148), or

(ii) below previous resistance (now support) of $1.14 from the open of 28th March, or

(iii) below previous support of $1.09 from the open of 9th April / 14th January.

Bullish potential detected for WPREntry conditions:

(i) higher share price for ASX:WPR along with swing up of indicators such as DMI/RSI.

Stop loss for the trade would be:

(i) a close below the 200 day moving average (currently $2.49), or

(ii) a close below the 50 day moving average (currently $2.42), or

(ii) below the support level from the open of 2nd January (i.e.: below $2.34), depending on risk tolerance.

Bullish potential detected for RGNEntry conditions:

(i) higher share price for ASX:RGN along with swing up of indicators such as DMI/RSI, and

(ii) observation of market reaction at the potential resistance level at $2.23 (from the open of 10th April) after closing above 50 day and 200 day MAs.

Stop loss for the trade would be, dependent on risk tolerance:

(i) a close below the 50 day moving average (currently $2.11), or

(ii) below the support level from the open of 13th January (i.e.: below $2.06), or

(iii) below the support level from the open of 17th March (i.e.: below $2.03).

Bullish potential detected for BWPEntry conditions:

(i) higher share price for ASX:BWP along with swing up of indicators such as DMI/RSI.

Stop loss for the trade would be:

(i) a close below the 200 day moving average (currently $3.43), or

(ii) below the support level from the open of 28th November 2023 (i.e.: below $3.35), depending on risk tolerance.

Medical Properties Trust | MPW | Long at $4.30Medical Properties Trust NYSE:MPW is a beaten down medical facility REIT currently in a price consolidation phase. The company's stock price is at a level not seen since the 2008-2009 financial crisis - but this doesn't mean it's a "steal" right now for investors. Here's why (from Wiki):

"In 2022, The Wall Street Journal reported that Medical Properties Trust had made multiple loans to its largest tenant Steward Health Care and paid above market value to Steward for property that Steward then leased from Medical Properties. The article alleged that this was done to help Steward pay off debts to Cerberus Capital Management, while Medical Properties claimed that the amounts paid for the properties were fair based on its underwriting and internal appraisals for the properties. MPT referenced Steward’s dependability in paying approximately $1.2 billion in rent and interest since 2016 as further evidence of prudent underwriting. MPT also cited its 2022 sale of a 50% stake in the Massachusetts real estate it bought from Steward as validation of its strategy. In March 2022, Macquarie Infrastructure Partners V entered into a $1.7 billion partnership with MPT to own eight hospitals leased to Steward, resulting in a 47% gain on sale of real estate for MPT. Another Wall Street Journal report also claimed that the company engaged in risky acquisitions with tenants who were likely to default on rent payments later while the compensation of executives of the company was partially linked to the volume of acquisitions they could make. The company clarified that it does not directly compensate executives for acquisition volume, and that its compensation plan provides for reducing executive compensation if acquisitions do not increase the company's per-share value."

On September 11, 2024, NYSE:MPW announced a settlement agreement with Steward Health Care that ended their relationship and restored NYSE:MPW 's control over its real estate. So, it's a highly risky investment, but the cat may be out of the bag and a turnaround may be ahead (?). The country's need for medical facilities will be dire as the baby-boom generation gets older. With a 7% dividend and *potential* change in business profitability ahead, NYSE:MPW is at a personal buy zone of $4.30. Warning: It may take several years for a recovery, though, or bankruptcy is ahead.

Target #1 = $6.15

Target #2 = $8.00

Target #3 = $9.75

Bearish potential detected for WPREntry conditions:

(i) lower share price for ASX:WPR along with swing up of the DMI indicators and swing down of the RSI indicator, and

(ii) observation of market reaction at the support level at $2.34.

Stop loss for the trade would be:

(i) above the resistance level from the open of 12th December (i.e.: above $2.42), or

(ii) above the resistance level from the open of 27th December (i.e.: above $2.47), depending on risk tolerance.

Alexandria Real Estate | ARE | Long at $97.41Alexandria Real Estate NYSE:ARE

Pros:

Pays a high and reliable dividend of 5.56%

Earnings are forecast to grow 18.52% per year

Revenue rose from $1.5 billion to $3 billion by Q3 2024

Insiders recently awarded a large amount of options in January 2025

Historically cyclical and bottom cycle may be ending soon

Cons:

Debt is not well covered by operating cash flow

P/E of 57.93x

May see further near-term declines in share price with poor earnings ($60s-$70s, bottom is unconfirmed)

Targets (into 2027)

$120.00

$140.00

$149.00

$199.00

$220.00 (long-term outlook)

LRHC Possibilities and Areas of InterestGood afternoon everyone, hope yah had a great New Years. In this 2025 we are looking at LRHC possible move to the upside with POSSIBLE targets at $1.13 & $2.08. There is a major gap to the downside in which we might not fill just yet until $1.13 gets filled (higher probability).

$2.08 seems like also a possibility, but that is more long-term and another analysis would be required once further data makes its way into the charts.

Nonetheless, Happy New Years everyone and have a blessed day!

CAPITALAND Investments (9C1) - BUY!BUY: $2.8 - $2.95

TP:

$3.44

$3.68

CapitaLand Investment will be a major beneficiary of lower rates from income growth for its REIT holdings and enabling accretive fee transactions. Another positive is the massive re-rating of China following the recent monetary stimulus by the central bank and support by the Politburo will benefit the economy indirectly. Similar to the Fed’s quantitative easing, it will be the wealth effect of higher equity and bond prices that boosts confidence and spending. It also encourages borrowing as households and private enterprises are deleveraging despite the record-low interest rates.

Personally. I am buying and holding for my long term dividends portfolio.

MPW Medical Properties Trust concerning float short of 34.96% Medical Properties Trust, a real estate investment trust specializing in acquiring and developing net-leased hospital properties since 2003, currently has a concerning float short of 34.96% as of June 20.

This high short interest signals significant bearish sentiment among investors.

For the first quarter of FY2024, MPW reported a stark decline in total revenue, dropping to $271.3 million from $350.2 million in the previous year. The company also faced a staggering net loss of $736 million, or $1.23 per share. This substantial loss was primarily due to $693 million in impairments related to the Steward Health Care System.

Adding to the company's woes, Prospect Medical Holdings, one of MPW's largest and struggling tenants, revealed it had received a subpoena last year from the Justice Department. This development further underscores the potential risks and challenges facing Medical Properties Trust.

I'm looking at purchasing the $3 strike price puts expiring on January 17, 2025, currently priced at $0.40.

NetSTREIT - Bullish ChartNTST broke the descending trend line/2D SMMA that was holding the price since August 2021, and retested it forming a daily bullish engulfing.

I will become even more bullish if the NTST price confirms above $19.

That setup could give good gains in the medium term.

Has MPW Bottomed Out?NYSE:MPW has pumped 19.60%+ today, and I received a great question about whether MPW has bottomed out. There was an opportunity to buy within the buy zone, and MPW had a strong rebound out of this buy zone. The momentum is currently bullish, and there is the possibility that MPW continues trending up towards the light blue trendline, which gives a price target around $6-7 price levels. This pump is caused by bullish news that Steward is selling assets to reduce its debt, which is a scenario that I've been discussing in past updates. It is possible for a selloff after this news, and for now MPW is at a $4.60 resistance level. It is important to monitor this resistance level to see if MPW gets a rejection or break here. With a rejection, I think there can be more buying opportunities around $3-4 price levels. MPW had a strong rebound off the orange zone, flipping it from resistance into support. I think MPW could retest this orange zone at some point, and I still think MPW could retest the green buy zone during a fed pivot.

O Realty Income Corporation Options Ahead of EarningsAnalyzing the options chain and the chart patterns of O Realty Income Corporation prior to the earnings report this week,

I would consider purchasing the 50usd strike price Puts with

an expiration date of 2024-9-20,

for a premium of approximately $2.53.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

ABR Arbor Realty Trust Options Ahead of EarningsAnalyzing the options chain and the chart patterns of ABR Arbor Realty Trust prior to the earnings report this week,

I would consider purchasing the 13usd strike price Puts with

an expiration date of 2024-3-15,

for a premium of approximately $1.87.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.