Ultra Clean Holdings | UCTT | Long at $27.32Like Ichor Holdings NASDAQ:ICHR , Ultra Clean Holdings NASDAQ:UCTT is a prominent developer and supplier of critical subsystems, high-purity components, and specialized services, primarily for the semiconductor industry. I believe this is a very undervalued area in the semiconductor industry.

Growth

Earnings per share expected to more than triple between 2025 and 2028 and revenue is expected to be on the rise.

Health

Debt-to-equity: 0.9x (healthy)

Quick Ratio: 1.9 (great)

Altman's Z Score: 2.7 (good)

Action

Unless the semiconductor market implodes (or the company), the future looks bright for NASDAQ:UCTT in the next 2-3 years. It may dip into the low $20's in the near-term to close a few price gaps, but with a float of 44 million, it may get interesting at some point soon. Thus, at $27.32, NASDAQ:UCTT is in a personal buy zone.

Targets into 2029

$35.00 (+64.7%)

$60.00 (+119.6%)

Semiconductorindustry

Ichor Holdings | ICHR | Long at $20.41Ichor Holdings NASDAQ:ICHR is a major supplier in the semiconductor industry, specifically focused on the semiconductor capital equipment sector rather than directly manufacturing chips themselves. I believe this is a very undervalued area in the semiconductor industry. The other major competitor is Ultra Clean Technologies NASDAQ:UCTT .

Insiders

Buying between $14 and $17 share.

Growth

Earnings per share expected to more than double between 2026 and 2028 and revenue on the rise.

Health

Debt-to-equity: 0.2x (healthy)

Quick Ratio: 1.3 (good)

Altman's Z Score: 2.8 (good)

Action

Unless the semiconductor market implodes (or the company), the future looks bright for NASDAQ:ICHR in the next 2-3 years. With a float of 32 million, it may get interesting at some point soon. Thus, at $20.41, NASDAQ:ICHR is in a personal buy zone.

Targets into 2029

$32.00 (+56.8%)

$42.00 (+105.8%)

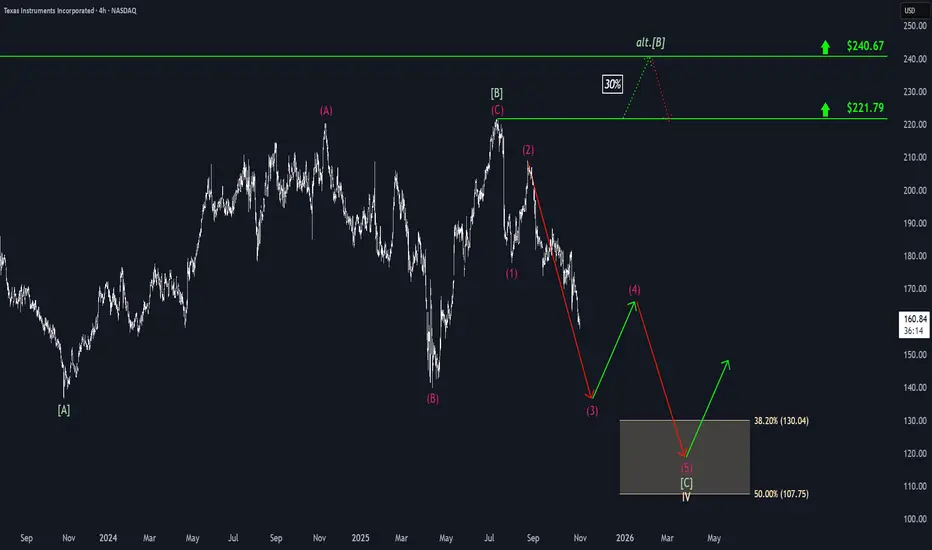

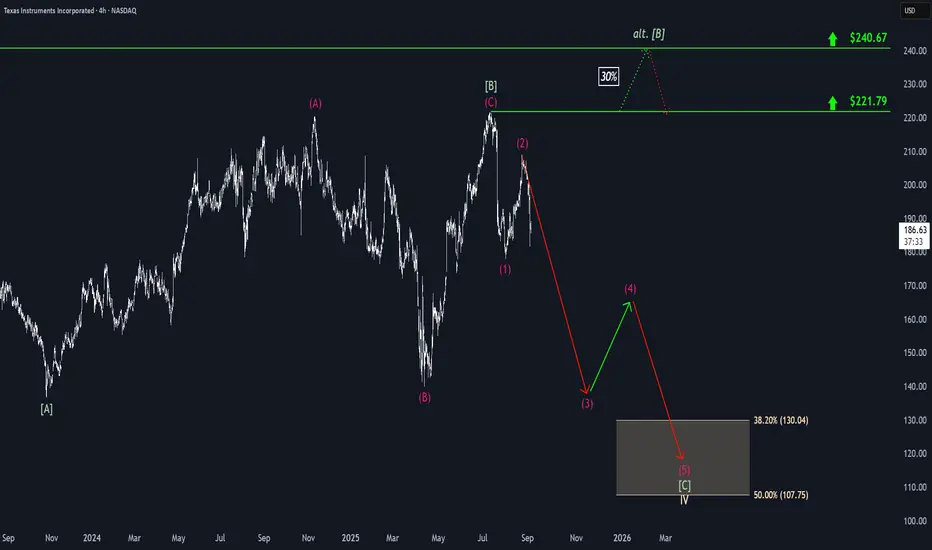

Texas Instruments: Extending DeclinesDespite some interim countermoves, Texas Instruments continued to see further sell-offs, advancing our primary scenario. Currently, we still see additional downside potential in magenta wave (3) before expecting a temporary rebound in wave (4). With wave (5), TXN is likely to dip into our beige Target Zone between $130.04 and $107.75, completing the broader correction of beige wave IV. There remains a 30% chance that a new (corrective) high in green wave alt. could still materialize, delaying the end of the correction. In this scenario, price would first move above resistance at $221.79 before reversing at the higher $240.67 level.

Texas Instruments: Rebound Underway, But Downside Still in PlayTexas Instruments initially continued its decline but has recently shown early signs of a rebound. Nonetheless, we still see greater downside potential in magenta wave (3), and expect the broader bearish magenta impulse to ultimately extend into the beige zone between $130.04 and $107.75. Should a new (corrective) high occur in green wave alt. above $221.79, it could temporarily postpone the anticipated sell-off. However, even in this 30% likely scenario, price would likely reverse no later than at the higher resistance level at $240.67.

Texas Instruments: Second Leg Down CompleteTexas Instruments has experienced sharp sell-offs, leading us to confirm the top of magenta wave (2). This suggests that the stock has completed the second stage of the ongoing magenta downward impulse. The current wave (3) still presents significant downside potential in the near term. After a brief recovery in wave (4), wave (5) is expected to reach our beige Target Zone between $130.04 and $107.75. A new corrective high in green wave alt. above $221.79 could delay this process. However, in this 30% likely scenario, TXN should reverse course at the latest by the $240.67 level.

Is Samsung's Chip Bet Paying Off?Samsung Electronics is navigating a complex global landscape, marked by intense technological competition and shifting geopolitical alliances. A recent $16.5 billion deal to supply advanced chips to Tesla, confirmed by Elon Musk, signals a potential turning point. This contract, set to run until late 2033, underscores Samsung's strategic commitment to its foundry business. The agreement will dedicate Samsung's new Texas fabrication plant to producing Tesla's next-generation AI6 chips, a move Musk himself highlighted for its significant strategic importance. This partnership aims to bolster Samsung's position in the high-stakes semiconductor sector, particularly in advanced manufacturing and AI.

The deal's economic and technological implications are substantial. Samsung's foundry division has faced profitability challenges, experiencing estimated losses exceeding $3.6 billion in the first half of the year. This large-scale contract is expected to help mitigate those losses, providing a much-needed revenue stream. From a technological standpoint, Samsung aims to accelerate its 2-nanometer (2nm) mass production efforts. While its 3nm process faced yield hurdles, the Tesla collaboration, with Musk's direct involvement in optimizing efficiency, could be crucial for improving 2nm yields and attracting future clients like Qualcomm. This pushes Samsung to remain at the forefront of semiconductor innovation.

Beyond the immediate financial and technological gains, the Tesla deal holds significant geopolitical and geostrategic weight. The dedicated Texas fab enhances U.S. domestic chip production capabilities, aligning with American goals for supply chain resilience. This deepens the U.S.-South Korea semiconductor alliance. For South Korea, the deal strengthens its critical tech exports and may provide leverage in ongoing trade negotiations, particularly concerning potential U.S. tariffs. While Samsung still trails TSMC in foundry market share and faces fierce competition in High-Bandwidth Memory (HBM) from SK Hynix, this strategic alliance with Tesla positions Samsung to solidify its recovery and expand its influence in the global high-tech arena.