$GBIRYY -U.K Inflation Rate (October/2025)ECONOMICS:GBIRYY 3.6%

October/2025

source: Office for National Statistics

- The UK’s annual inflation rate eased to 3.6% in October,

its lowest in four months, down from 3.8% in each of the previous three months.

The figure matched expectations from both the Bank of England and market analysts,

supported by a slowdown in gas and electricity prices.

Unitedkingdom

$GBGDPQQ - U.K GDP Growth Disappoints (Q3/2025)ECONOMICS:GBGDPQQ

Q3/2025

source: Office for National Statistics

- The UK economy grew 0.1% in Q3 2025,

easing from 0.3% in Q2 and falling short of market expectations of 0.2%.

Gains in investment, consumption, and net trade were partly offset by falling inventories. Annually, GDP rose 1.3%, slightly below expectations.

$GBINTR - Britain Interest Rates (November/2025) ECONOMICS:GBINTR 4%

November/2025

source: Bank of England

- The Bank of England voted by a majority of 5–4 to keep the Bank Rate steady at 4%,

in line with expectations.

However, four policymakers voted to reduce borrowing costs by 25bps.

The central bank said inflation has likely peaked and risks of persistent price pressures have diminished. It added that, if disinflation continues, the Bank Rate will probably decline gradually.

$GBINTR - B.o.E Leaves Rates Unchanged (August/2025)ECONOMICS:GBINTR

August/2025

source: Bank of England

- The Bank of England voted by a majority of 7-2 to hold its benchmark Bank Rate at 4% today, following a 25 bps cut in August, and in line with expectations, as it navigates slow growth alongside still-elevated inflation.

Policymakers noted that a gradual and cautious approach to further easing monetary restraint remains appropriate.

The central bank will also slow the pace of bond sales to £70 billion from £100 billion and will move away from sales of longer gilts.

$GBIRYY -U.K Inflation Rate Flat at 3.8% (August/2025)ECONOMICS:GBIRYY

August/2025

source: Office for National Statistics

- The UK’s annual inflation rate held steady at 3.8% in August 2025, unchanged from July and remaining near the highs last seen in January 2024, in line with expectations.

Lower airfares and easing services inflation were offset by higher motor fuel costs and rising prices for restaurants and hotels and food.

Meanwhile, annual core inflation rate slowed to 3.6% from 3.8%.

$GBIRYY - U.K Inflation Hits 18-Month High (July/2025)ECONOMICS:GBIRYY

July/2025

source: Office for National Statistics

- The UK’s annual inflation rate rose to 3.8% in July 2025 from 3.6% in June,

the highest since January 2024 and slightly above forecasts of 3.7%.

The uptick was led by higher transport costs linked to school summer holidays, with additional pressure from motor fuels, restaurants and hotels, and food and non-alcoholic beverages.

On a monthly basis, CPI rose 0.1%,

defying forecasts of a 0.1% decline but slowing from June’s 0.3% gain.

Core inflation inched up to 3.8% from 3.7%.

GBGDPQQ -Great Britain GDP (Q2/2025)ECONOMICS:GBGDPQQ

Q2/2025

source: Office for National Statistics

- The British economy grew 0.3% qoq in Q2 2025, slowing from a 0.7% expansion in Q1 but surpassing forecasts of just 0.1%, according to preliminary estimates.

The moderation partly reflects activity being brought forward to February and March ahead of April’s stamp duty changes and the announcement of new US tariffs.

In Q2, growth was fuelled by a 0.4% rise in services, led by computer programming and consultancy (+4.1%).

Construction climbed 1.2%, while production fell 0.3% due to utilities (-6.8%) and mining (-0.3%), partly offset by a 0.3% increase in manufacturing.

On the expenditure side, growth was driven mainly by a 1.2% rise in government consumption, particularly in health (vaccinations) and public administration and defence.

Gross capital formation increased on the back of higher changes in valuables, inventories, and alignment adjustments, but business investment slumped 4%.

Household spending rose a modest 0.1% and exports increased 1.6%, outpacing the 1.4% rise in imports.

$GBINTR -BoE Cuts Rates as Expected (August/2025)ECONOMICS:GBINTR

August/2025

source : Bank of England

- The Bank of England voted by a 5–4 majority to cut the key Bank Rate by 25bps to 4% in August, in line with expectations.

This marks the fifth rate cut since August of last year and brings borrowing costs to their lowest level since March 2023.

However, the decision followed an initial three-way split, the first time that two rounds of voting were required to reach a conclusive decision on interest rates.

$GBIRYY - U.K Inflation Rises to a 2024 High (June/2025)ECONOMICS:GBIRYY

June/2025

source: Office for National Statistics

- The annual inflation rate in the UK rose to 3.6% in June, the highest since January 2024, up from 3.4% in May and above expectations that it would remain unchanged.

The main upward pressure came from transport prices, mostly motor fuel costs, airfares, rail fares and maintenance and repair of personal transport equipment.

On the other hand, services inflation remained steady at 4.7%.

Meanwhile, core inflation also accelerated, with the annual rate reaching 3.7%.

$GBINTR - Steady Rates by BoE (June/2025)ECONOMICS:GBINTR

June/2025

source: Bank of England

- The Bank of England voted 6-3 to keep the Bank Rate steady at 4.25% at its June meeting, amid ongoing global uncertainty and persistent inflation.

The central bank noted inflation is expected to remain at current rates for the rest of the year before easing back toward the target next year,

indicating that a gradual and cautious approach to further monetary policy easing remains appropriate.

GBIRYY - U.K Inflation (May/2025)ECONOMICS:GBIRYY

May/2025

source: Office for National Statistics

-The annual inflation rate in the UK edged down to 3.4% in May 2025 from 3.5% in April, matching expectations.

The largest downward contribution came from transport prices (0.7% vs 3.3%), reflecting falls in air fares (-5%) largely due to the timing of Easter and the associated school holidays, as well as falling motor fuel prices.

Additionally, the correction of an error in the Vehicle Excise Duty series contributed to the drop; the error affected April’s data, but the series has been corrected from May.

Further downward pressure came from cost for housing and household services (6.9% vs 7%), mostly owner occupiers' housing costs (6.7% vs 6.9%).

Services inflation also slowed to 4.7% from 5.4%. On the other hand, the largest, upward contributions came from food and non-alcoholic beverages (4.4% vs 3.4%), namely chocolate, confectionery and ice cream, and furniture and household goods (0.8%, the most since December 2023).

Compared to the previous month, the CPI rose 0.2%.

$GBIRYY - U.K Inflation Rate Accelerates (April/2025)ECONOMICS:GBIRYY

April/2025

source: Office for National Statistics

- The annual inflation rate in the UK jumped to 3.5% in April, the highest since January 2024, from 2.6% in March and above forecasts of 3.3%.

The main upward pressure came from higher electricity and gas prices after the Ofgem price cap increase, while new Vehicle Excise Duty on electric cars lifted transport costs, and food inflation also picked up.

Meanwhile, core inflation accelerated to 3.8%, the highest in a year.

$GBGDPQQ -UK GDP Growth Above Expectations (Q1/2025)ECONOMICS:GBGDPQQ

Q1/2025

source: Office for National Statistics

- The British economy expanded 0.7% on quarter in Q1 2025, compared to 0.1% in Q4 and forecasts of 0.6%, preliminary figures showed. It is the strongest growth rate in 3 quarters, with the largest contribution coming from the services sector, gross fixed capital formation and net trade. Year-on-year, the GDP expanded 1.3%.

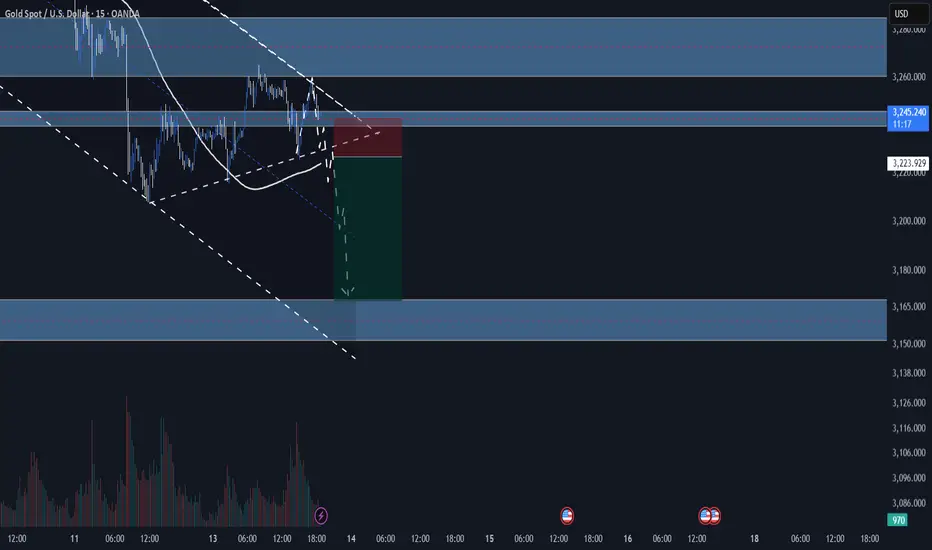

XAUUSD SHORTIt's a beautiful setup , as we see here gold is going down since 6TH of may and it forms a bearish channel , it just tested the lower high of the channel and a resistance . I'm waiting for the market to break and retest the trendline beneath it , then i'll take a short position targeting this support level

$GBINTR -BoE Cuts Rates as Expected (May/2025)ECONOMICS:GBINTR

May/2025

source: Bank of England

- The Bank of England cut the Bank Rate by 25 basis points to 4.25%,

matching expectations but revealing a split 5–4 vote.

Two policymakers favored a deeper 50 bps cut, while two others wanted to hold at 4.5%.

It was the fourth cut since August 2024, amid concerns over slowing growth linked to Trump-era tariffs.

$GBIRYY - U.K CPI (March/2025)ECONOMICS:GBIRYY 2.6%

March/2025

source: Office for National Statistics

- The annual inflation rate in the UK slowed to 2.6% in March 2025 from 2.8% in February and below market and the BoE's forecasts of 2.7%.

The largest downward contributions came from recreation and culture (2.4% vs 3.4%), mainly games, toys and hobbies (-4.2%) and data processing equipment (-5.1%). Transport also contributed to the slowdown (1.2% vs 1.8%), largely due to a 5.3% fall in motor fuel prices.

In addition, prices rose less for restaurants and hotels (3%, the lowest since July 2021 vs 3.4%), mostly accommodation services (-0.6%); housing and utilities (1.8% vs 1.9%); and food and non-alcoholic beverages (3% vs 3.3%).

In contrast, the most significant upward contribution came from clothing and footwear (1.1% vs -0.6%), with prices usually rising in March as spring fashions continue to enter the shops.

Compared to the previous month, the CPI edged up 0.3%, slightly below both the previous month’s increase and expectations of 0.4%.

Annual core inflation slowed to 3.4% from 3.5%.

$GBIRYY -U.K Inflation Rate (February/2025)ECONOMICS:GBIRYY

February/2025

source: Office for National Statistics

- The annual inflation rate in the UK fell to 2.8% in February 2025 from 3% in January, below market expectations of 2.9%, though in line with the Bank of England's forecast.

The largest downward contribution came from prices of clothing which declined for the first time since October 2021 (-0.6% vs 1.8%), led by garments for women and children's clothing.

Inflation also eased in recreation and culture (3.4% vs. 3.8%), particularly in live music admission and recording media, as well as in housing and utilities (1.9% vs. 2.1%), including actual rents for housing (7.4% vs. 7.8%).

In contrast, food inflation was unchanged at 3.3% and prices rose faster for transport (1.8% vs 1.7%) and restaurants and hotels (3.4% vs 3.3%).

Meanwhile, services inflation held steady at 5%.

The annual core inflation rate declined to 3.5% from 3.7%.

Compared to the previous month, the CPI increased 0.4%, rebounding from a 0.1% decline but falling short of the expected 0.5% increase.

$GBINTR - U.K Interest Rates (March/2025)ECONOMICS:GBINTR

March/2025

source: Bank of England

- The Bank of England voted 8-1 to keep the Bank Rate at 4.5% during its March meeting,

as policymakers adopted a wait-and-see approach amid stubbornly high inflation and global economic uncertainties. The bank highlighted that, given the medium-term inflation outlook, a gradual and cautious approach to further withdrawal of monetary policy restraint remains appropriate.

CPI inflation increased to 3.0% in January, and while global energy prices fell,

inflation is expected to rise to 3¾% by Q3 2025.

Also, the MPC noted that global trade policy uncertainties and geopolitical risks increased, with financial market volatility rising. source: Bank of England

$GBIRYY -U.K Inflation Rate (December/2024)ECONOMICS:GBIRYY

December/2024

source: Office for National Statistics

-Annual inflation rate in the UK unexpectedly edged lower to 2.5% in December 2024 from 2.6% in November, below forecasts of 2.6%. However, it matched the BoE's forecast from early November.

Prices slowed for restaurants and hotels (3.4%, the lowest since July 2021 vs 4%), mainly due to a 1.9% fall in prices of hotels.

Inflation also slowed for recreation and communication (3.4% vs 3.6%) and services (4.4%, the lowest since March 2022 vs 5) and steadied for food and non-alcoholic beverages (at 2%). Meanwhile, prices decreased less for transport (-0.6% vs -0.9%) as upward effects from motor fuels and second-hand cars (1%) partially offset a downward effect from air fare (-26%).

Also, prices rose slightly more for housing and utilities (3.1% vs 3%). Compared to November, the CPI rose 0.3%, above 0.1% in the previous period but below forecasts of 0.4%.

The annual core inflation rate also declined to 3.2% from 3.5% and the monthly rate went up to 0.3%, below forecasts of 0.5%.

$GBINTR -U.K Interest RatesECONOMICS:GBINTR

(December/2024)

source: Bank of England

The Bank of England left the benchmark bank rate steady at 4.75% during its December 2024 meeting,

in line with market expectations, as CPI inflation, wage growth and some indicators of inflation expectations had risen, adding to the risk of inflation persistence.

The central bank reinforced that a gradual approach to removing monetary policy restraint remains appropriate and that monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further.

The central bank will continue to decide the appropriate degree of monetary policy restrictiveness at each meeting.

$GBIRYY -U.K CPI (November/2024)ECONOMICS:GBIRYY

(November/2024)

source: Office for National Statistics

- The annual inflation rate in the UK edged up for a second month to 2.6% in November 2024 from 2.3% in October, matching forecasts.

It is the highest inflation rate in eight months,

with prices rising at a faster pace for recreation and culture (3.6% vs 3% in October),

mostly admission fees to live music events and theaters and computer games;

housing and utilities (3% vs 2.9%), particularly actual rents for housing; and food and non-alcoholic beverages (2% vs 1.9%).

In addition, transport prices fell much less (-0.9% vs -1.9%) as upward effects from motor fuels and second-hand cars were partially offset by a downward effect from air fares.

Meanwhile, services inflation was steady at 5%.

Compared to the previous month, the CPI edged up 0.1%, less than 0.6% in October and matching forecasts.

The core CPI rose 3.5% on the year from 3.3% in October but below forecasts of 3.6%.

On the month, core prices stalled.

$GBIRYY -U.K Inflation Rate Above Forecasts (October/2024)ECONOMICS:GBIRYY 2.3%

October/2024

source: Office for National Statistics

- Annual inflation rate in the UK went up to 2.3% in October 2024, the highest in six months, compared to 1.7% in September.

This exceeded both the Bank of England's target and market expectations of 2.2%.

The largest upward contribution came from housing and household services (5.5% vs 3.8% in September), mainly electricity (-6.3% vs -19.5%) and gas (-7.3% vs -22.8%), reflecting the rise of the Office of Gas and Electricity Markets (Ofgem) energy price cap in October 2024.

Also, prices rose faster for restaurants and hotels (4.3% vs 4.1%) and rebounded for housing and utilities (2.9% vs -1.7%). Prices of services increased slightly more (5% vs 4.9%), matching estimates form the central bank.

On the other hand, food inflation was steady at 1.9% and the largest offsetting downward contribution came from recreation and culture (3% vs 3.8%).

Compared to the previous month, the CPI increased 0.6%. Finally, annual core inflation edged up to 3.3% from 3.2%.

$GBINTR -B.o.E Cuts RatesECONOMICS:GBINTR

(November/2024)

source: Bank of England

-The Bank of England lowered its key interest rate by 25 bps to 4.75%, in line with expectations, following a hold in September and a quarter-point cut in August.

The U.S Fed ECONOMICS:USINTR is also expected to cut rates by 25bps today, following a larger 50bps reduction in September.

Traders are keen for signals on future policy, particularly after Trump’s re-election.