OPTIMAL super trend tripple confirm for leverage. Ai implemented for higher r:r still a work in progresss

Bands and Channels

J12Matic Builder by galgoomA flexible Renko/tick strategy that lets you choose between two entry engines (Multi-Source 3-way or QBand+Moneyball), with a unified trailing/TP exit engine, NY-time trading windows with auto-flatten, daily profit/loss and trade-count limits (HALT mode), and clean webhook routing using {{strategy.order.alert_message}}.

Highlights

Two entry engines

Multi-Source (3): up to three long/short sources with Single / Dual / Triple logic and optional lookback.

QBand + Moneyball: Gate → Trigger workflow with timing windows, OR/AND trigger modes, per-window caps, optional same-bar fire.

Unified exit engine: Trailing by Bricks or Ticks, plus optional static TP/SL.

Session control (NY time): Evening / Overnight / NY Session windows; auto-flatten at end of any enabled window.

Day controls: Profit/Loss (USD) and Trade-count limits. When hit, strategy HALTS new entries, shows an on-chart label/background.

Alert routing designed for webhooks: Every order sets alert_message= so you can run alerts with:

Condition: this strategy

Notify on: Order fills only

Message: {{strategy.order.alert_message}}

Default JSONs or Custom payloads: If a Custom field is blank, a sensible default JSON is sent. Fill a field to override.

How to set up alerts (the 15-second version)

Create a TradingView alert with this strategy as Condition.

Notify on: Order fills only.

Message: {{strategy.order.alert_message}} (exactly).

If you want your own payloads, paste them into Inputs → 08) Custom Alert Payloads.

Leave blank → the strategy sends a default JSON.

Fill in → your text is sent as-is.

Note: Anything you type into the alert dialog’s Message box is ignored except the {{strategy.order.alert_message}} token, which forwards the payload supplied by the strategy at order time.

Publishing notes / best practices

Renko users: Make sure “Renko Brick Size” in Inputs matches your chart’s brick size exactly.

Ticks vs Bricks: Exit distances switch instantly when you toggle Exit Units.

Same-bar flips: If enabled, a new opposite signal will first close the open trade (with its exit payload), then enter the new side.

HALT mode: When day profit/loss limit or trade-count limit triggers, new entries are blocked for the rest of the session day. You’ll see a label and a soft background tint.

Session end flatten: Auto-closes positions at window ends; these exits use the “End of Session Window Exit” payload.

Bar magnifier: Strategy is configured for on-close execution; you can enable Bar Magnifier in Properties if needed.

Default JSONs (used when a Custom field is empty)

Open: {"event":"open","side":"long|short","symbol":""}

Close: {"event":"close","side":"long|short|flat","reason":"tp|sl|flip|session|limit_profit|limit_loss","symbol":""}

You can paste any text/JSON into the Custom fields; it will be forwarded as-is when that event occurs.

Input sections — user guide

01) Entries & Signals

Entry Logic: Choose Multi-Source (3) or QBand + Moneyball (pick one).

Enable Long/Short Signals: Master on/off switches for entering long/short.

Flip on opposite signal: If enabled, a new opposite signal will close the current position first, then open the other side.

Signal Logic (Multi-Source):

Single: any 1 of the 3 sources > 0

Dual: Source1 AND Source2 > 0

Triple (default): 1 AND 2 AND 3 > 0

Long/Short Signal Sources 1–3: Provide up to three series (often indicators). A positive value (> 0) is treated as a “pulse”.

Use Lookback: Keeps a source “true” for N bars after it pulses (helps catch late triggers).

Long/Short Lookback (bars): How many bars to remember that pulse.

01b) QBands + Moneyball (Gate -> Trigger)

Allow same-bar Gate->Trigger: If ON, a trigger can fire on the same bar as the gate pulse.

Trigger must fire within N bars after Gate: Size of the gate window (in bars).

Max signals per window (0 = unlimited): Cap the number of entries allowed while a gate window is open.

Buy/Sell Source 1 – Gate: Gate pulse sources that open the buy/sell window (often a regime/zone, e.g., QBands bull/bear).

Trigger Pulse Mode (Buy/Sell): How to detect a trigger pulse from the trigger sources (Change / Appear / Rise>0 / Fall<0).

Trigger A/B sources + Extend Bars: Primary/secondary triggers plus optional extension to persist their pulse for N bars.

Trigger Mode: Pick S2 only, S3 only, S2 OR S3, or S2 AND S3. AND mode remembers both pulses inside the window before firing.

02) Exit Units (Trailing/TP)

Exit Units: Choose Bricks (Renko) or Ticks. All distances below switch accordingly.

03) Tick-based Trailing / Stops (active when Exit Units = Ticks)

Initial SL (ticks): Starting stop distance from entry.

Start Trailing After (ticks): Start trailing once price moves this far in your favor.

Trailing Distance (ticks): Offset of the trailing stop from peak/trough once trailing begins.

Take Profit (ticks): Optional static TP distance.

Stop Loss (ticks): Optional static SL distance (overrides trailing if enabled).

04) Brick-based Trailing / Stops (active when Exit Units = Bricks)

Renko Brick Size: Must match your chart’s brick size.

Initial SL / Start Trailing After / Trailing Distance (bricks): Same definitions as tick mode, measured in bricks.

Take Profit / Stop Loss (bricks): Optional static distances.

05) TP / SL Switch

Enable Static Take Profit: If ON, closes the trade at the fixed TP distance.

Enable Static Stop Loss (Overrides Trailing): If ON, trailing is disabled and a fixed SL is used.

06) Trading Windows (NY time)

Use Trading Windows: Master toggle for all windows.

Evening / Overnight / NY Session: Define each session in NY time.

Flatten at End of : Auto-close any open position when a window ends (sends the Session Exit payload).

07) Day Controls & Limits

Enable Profit Limits / Profit Limit (Dollars): When daily net PnL ≥ limit → auto-flatten and HALT.

Enable Loss Limits / Loss Limit (Dollars): When daily net PnL ≤ −limit → auto-flatten and HALT.

Enable Trade Count Limits / Number of Trades Allowed: After N entries, HALT new entries (does not auto-flatten).

On-chart HUD: A label and soft background tint appear when HALTED; a compact status table shows Day PnL, trade count, and mode.

08) Custom Alert Payloads (used as strategy.order.alert_message)

Long/Short Entry: Payload sent on entries (if blank, a default open JSON is sent).

Regular Long/Short Exit: Payload sent on closes from SL/TP/flip (if blank, a default close JSON is sent).

End of Session Window Exit: Payload sent when any enabled window ends and positions are flattened.

Profit/Loss/Trade Limit Close: Payload sent when daily profit/loss limit causes auto-flatten.

Tip: Any tokens you include here are forwarded “as is”. If your downstream expects variables, do the substitution on the receiver side.

Known limitations

No bracket orders from Pine: This strategy doesn’t create OCO/attached brackets on the broker; it simulates exits with strategy logic and forwards your payloads for external automation.

alert_message is per order only: Alerts fire on order events. General status pings aren’t sent unless you wire a separate indicator/alert.

Renko specifics: Backtests on synthetic Renko can differ from live execution. Always forward-test on your instrument and settings.

Quick checklist before you publish

✅ Brick size in Inputs matches your Renko chart

✅ Exit Units set to Bricks or Ticks as you intend

✅ Day limits/Windows toggled as you want

✅ Custom payloads filled (or leave blank to use defaults)

✅ Your alert uses Order fills only + {{strategy.order.alert_message}}

THE BATATAH SAUCE BTC.PERP TRADING STRAT12hr hour is the sweet spot

great profit factor

decent risk management avg losing (back tested for 5 yrs and does alright till even 2018)trade 8.21% vs avg winning 174.87% (back tested for 5 yrs and does alright since even start2018)

Its alright on daily as well as 6hr but lower just gets more noisy

Energy Across TimePrivate Use-Only Version

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Sed euismod, lectus nec varius dictum, nibh arcu imperdiet augue, ac tristique odio nulla nec ligula. Vivamus ac odio nec lorem faucibus posuere. Proin sed sapien dignissim, laoreet velit vitae, vehicula justo. Curabitur et viverra lectus. Ut sit amet rhoncus ligula. Nullam nec posuere nisl. Morbi faucibus mattis sem, nec faucibus neque tristique vitae. Praesent malesuada nisl nec lectus congue, sit amet fringilla mauris vulputate. Ut quis felis vitae arcu varius ultrices non vel metus. Duis ac posuere nulla. Sed quis odio arcu. Etiam sodales eros libero, eget finibus elit bibendum nec. Cras ac justo sed justo facilisis suscipit. Nullam faucibus tortor vitae lorem eleifend, ut rhoncus lacus imperdiet.

Vestibulum ante ipsum primis in faucibus orci luctus et ultrices posuere cubilia curae; Integer sagittis mi ut leo efficitur, vel feugiat nibh suscipit. Morbi sed vulputate risus, eu volutpat massa. Vestibulum luctus, nisl non posuere vehicula, enim urna bibendum est, sit amet luctus libero sapien a massa. Nullam blandit nulla non massa pretium, nec fermentum turpis vestibulum. Pellentesque habitant morbi tristique senectus et netus et malesuada fames ac turpis egestas. Nam condimentum congue feugiat. Donec commodo, libero nec congue finibus, augue mi malesuada mi, sed suscipit erat sem ut orci. Phasellus dictum justo at ligula tincidunt, nec dictum libero scelerisque. Nulla et faucibus nulla, id aliquet magna. Fusce congue, justo in luctus iaculis, lectus dolor ultrices nunc, nec euismod lectus lorem ac lectus.

Pellentesque habitant morbi tristique senectus et netus et malesuada fames ac turpis egestas. Nam dictum sapien non mattis aliquet. Integer semper venenatis libero, sit amet posuere magna laoreet at. Aliquam erat volutpat. Aenean congue luctus felis, vel blandit velit posuere nec. Aenean feugiat, purus at vulputate posuere, ipsum nulla dignissim arcu, nec sollicitudin quam est sed purus. Aenean bibendum, ligula a luctus venenatis, erat nisl sagittis eros, id ultrices purus nibh ac nunc. Sed egestas sodales dui, vitae volutpat mauris facilisis vitae. Nam sit amet dolor ac lorem luctus luctus. Morbi iaculis fringilla bibendum. Mauris ut ullamcorper leo. Sed fringilla fermentum nunc, eget egestas orci porttitor a. Aenean sit amet mi ligula. Suspendisse sed efficitur odio. Quisque in turpis eget mauris ullamcorper faucibus. Sed euismod turpis ut arcu posuere tincidunt.

EMA and BB Analysis for US100 V250829This TradingView strategy generates buy and sell signals based on exponential moving average (EMA) crossovers, limited by other factors such as Bollinger Bands, volume, and EMA distance.

It uses EMAs of 16, 24, 32, and 64 periods, as well as the angles of each of these EMAs.

Entry Conditions:

EMA Crossover Entry:

When EMA16 crosses EMA64 and the following conditions are met:

EMA16, EMA24, EMA32 are aligned — for a buy signal:

EMA16 > EMA24

EMA24 > EMA32

EMA32 > EMA48

(and the opposite for a sell signal)

EMA Angles:

The angles of the EMAs must also follow the same alignment.

Divergence Entry:

When the distance between EMAs 16, 24, 32, and 48 increases.

Entry Limitations:

Once an entry is detected, it is filtered by several conditions:

When the distance between the entry candle and EMA96 is more than two candles of the maximum size over three periods.

The stop loss is set as two candles of the maximum size over three periods. If this stop loss exceeds 6,000 points (adjustable parameter), the entry is invalid.

When the price is at the edge of the Bollinger Band with a 1200-period setting (equivalent to a 1-hour Bollinger Band).

When the Bollinger Band's middle line is descending and a buy signal is triggered (and vice versa).

When volume drops below a certain threshold.

When a sideways market movement is detected.

All these entry limitations are configurable parameters and can be enabled or disabled.

BOLL Omakase 2.0testing own {

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}

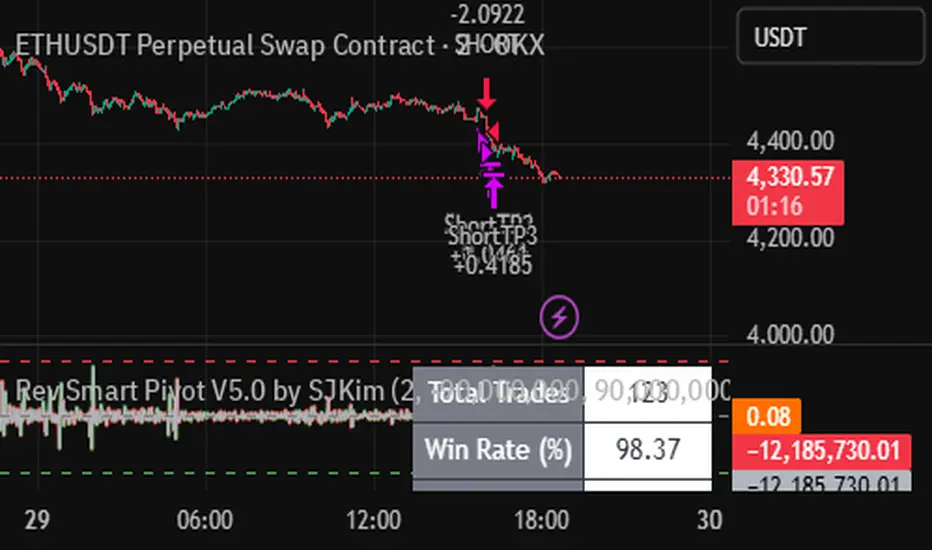

Nor Smart Pivot V5.0 by SJKimNor Smart Pivot V5.0 by SJKim.

Nor Smart Pivot V5.0 by SJKim.

Nor Smart Pivot V5.0 by SJKim.

Gaussian Fusion v1.0A versatile trading framework that blends Gaussian channel dynamics with a smoothing filter to capture directional moves with clarity.

Highlights:

Dual-band logic for flexible signal generation

Adaptive confirmation layer to reduce noise

Designed as a balance between trend capture and noise reduction, this strategy adapts to shifting market conditions while keeping the logic simple and practical.

Estrategy EURUSD M3 Scalping Estrategia para operar el EURUSD en temp de 3 min, indica sl y tp 6 pips sl y 10 pips tp

Twin Range Filter StrategyClarity Over Confusion: See price action through a全新的 lens. Watch as erratic, choppy movements are smoothed into a clear, actionable trajectory. The path of least resistance becomes obvious.

Confidence Over Hesitation: Receive high-probability entry and exit signals with a proven logic that waits for the market to commit before you do. No more second-guessing.

Discipline Over Emotion: Our algorithm enforces a systematic approach, helping you avoid emotional FOMO chasing and panic selling. Stick to the plan and execute with precision.

What Can You Expect?

Dynamic Adaptability: Unlike static indicators, continuously adapts to volatility. It widens its filter in turbulent markets to avoid whipsaws and tightens it in trending markets to capture more of the move.

The Power of Two: By synthesizing data from two distinct market perspectives, it confirms strength and filters out weakness, providing a confluence that standalone indicators simply cannot match.

Clean, Unambiguous Signals: We’ve eliminated the clutter. The software provides clear visual alerts (Green Arrows for Long, Red Arrows for Short) right on your chart, telling you exactly when the equilibrium has shifted.

Who is this for?

Swing Traders looking to capture the heart of a trend and avoid false breakouts.

Day Traders needing a reliable filter to navigate volatile intraday action.

Systematic Traders seeking a robust logic layer to add to their automated strategy.

Anyone overwhelmed by indicator overload and craving a single, trusted source of truth on their chart

Script_Algo - ORB Strategy with Filters🔍 Core Concept: This strategy combines three powerful technical analysis tools: Range Breakout, the SuperTrend indicator, and a volume filter. Additionally, it features precise customization of the number of candles used to construct the breakout range, enabling optimized performance for specific assets.

🎯 How It Works:

The strategy defines a trading range at the beginning of the trading session based on a selected number of candles.

It waits for a breakout above the upper or below the lower boundary of this range, requiring a candle close.

It filters signals using the SuperTrend indicator for trend confirmation.

It utilizes trading volume to filter out false breakouts.

⚡ Strategy Features

📈 Entry Points:

Long: Candle close above the upper range boundary + SuperTrend confirmation

Short: Candle close below the lower range boundary + SuperTrend confirmation

🛡️ Risk Management:

Stop-Loss: Set at the opposite range boundary.

Take-Profit: Calculated based on a risk/reward ratio (3:1 by default).

Position Size: 10 contracts (configurable).

⚠️ IMPORTANT SETTINGS

🕐 Time Parameters:

Set the correct time and time zone!

❕ATTENTION: The strategy works ONLY with correct time settings! Set the time corresponding to your location and trading session.

📊 This strategy is optimized for trading TESLA stock!

Parameters are tailored to TESLA's volatility, and trading volumes are adequate for signal filtering. Trading time corresponds to the American session.

📈 If you look at the backtesting results, you can see that the strategy could potentially have generated about 70 percent profit on Tesla stock over six months on 5m timeframe. However, this does not guarantee that results will be repeated in the future; remain vigilant.

⚠️ For other assets, the following is required:

Testing and parameter optimization

Adjustment of time intervals and the number of candles forming the range

Calibration of stop-loss and take-profit levels

⚠️ Limitations and Drawbacks

🔗 Automation Constraints:

❌ Cannot be directly connected via Webhook to CFD brokers!

Additional IT solutions are required for automation, thus only manual trading based on signals is possible.

📉 Risk Management:

Do not risk more than 2-3% of your account per trade.

Test on historical data before live use.

Start with a demo account.

💪 Strategy Advantages

✅ Combined approach – multiple signal filters

✅ Clear entry and exit rules

✅ Visual signals on the chart

✅ Volume-based false breakout filtering

✅ Automatic position management

🎯 Usage Recommendations

Always test the strategy on historical data.

Start with small trading volumes.

Ensure time settings are correct.

Adapt parameters to current market volatility.

Use only for stocks – futures and Forex require adaptation.

📚 Suitable Timeframes - M1-M15

Only highly liquid stocks

🍀 I wish all subscribers good luck in trading and steady profits!

📈 May your charts move in the right direction!

⚠️ Remember: Trading involves risk. Do not invest money you cannot afford to lose!

MA20 Crossover Strategy with Threshold and Color ChangeMột chiến lược cơ bản dựa trên EMA20. Giá cắt lên MA20 hay EMA20 thi báo mua và ngược lại

RSI Bands With RSI - ATR Trend StrategyRSI Bands With RSI-ATR Trend Line Strategy

Overview

A trend-following strategy that combines RSI regime detection with a smoothed baseline and ATR bands. Works similar to Supertrend: the line flips bullish or bearish only when price closes beyond the band, aiming to filter noise and catch clean moves.

How It Works

RSI above 50 = bullish bias, below 50 = bearish bias

A dynamic baseline is calculated from RSI and price range, then smoothed

ATR bands expand/contract with volatility

Close above the upper band → bullish flip → long entry

Close below the lower band → bearish flip → short entry

Between bands → prior trend continues

Features

Automatic Buy/Sell entries on confirmed flips

Configurable RSI, Smoothing, ATR, and Multiplier inputs

Visual trend line (green = bull, red = bear)

Backtest ready with initial capital and commission settings

Best Use Cases

Trending markets across Forex, Crypto, Indices, Commodities

Works on multiple timeframes (higher TFs = cleaner flips)

Flexible settings for conservative swing trading or aggressive scalping

⚠️ For testing/education only. Always manage risk and confirm with higher-timeframe or structure filters.

VWAP Executor — v6 (VWAP fix)tarek helishPractical scalping plan with high-rate (sometimes reaching 70–85% in a quiet market)

Concept: “VWAP bounce with a clear trend.”

Tools: 1–3-minute chart for entry, 5-minute trend filter, VWAP, EMA(50) on 5M, ATR(14) on 1M, volume.

When to trade: London session or early New York session; avoid 10–15 minutes before/after high-impact news.

Entry rules (buy for example):

Trend: Price is above the EMA(50) on 5M and has an upward trend.

Entry zone: First bounce to VWAP (or a ±1 standard deviation channel around it).

Signal: Bullish rejection/engulfing candle on 1M with increasing volume, and RSI(2) has exited oversold territory (optional).

Order: Entry after the confirmation candle closes or a limit close to VWAP.

Trade Management:

Stop: Below the bounce low or 0.6xATR(1M) (strongest).

Target: 0.4–0.7xATR(1M) or the previous micro-high (small return to increase success rate).

Trigger: Move the stop to breakeven after +0.25R; close manually if the 1M candle closes strongly against you.

Filter: Do not trade if the spread widens, or the price "saws" around VWAP without a trend.

Sell against the rules in a downtrend.

Why this plan raises the heat-rate? You buy a "small discount" within an existing trend and near the institutional average price (VWAP), with a small target price.

مواقعي شركة الماسة للخدمات المنزلية

شركة تنظيف بالرياض

نقل عفش بالرياض

Scott's DBOthis is a unique version of a daily breakout strategy, using custom signals, special handling of trading logic, and built to work with traders post for actual trading. Credit to: for the base indicator

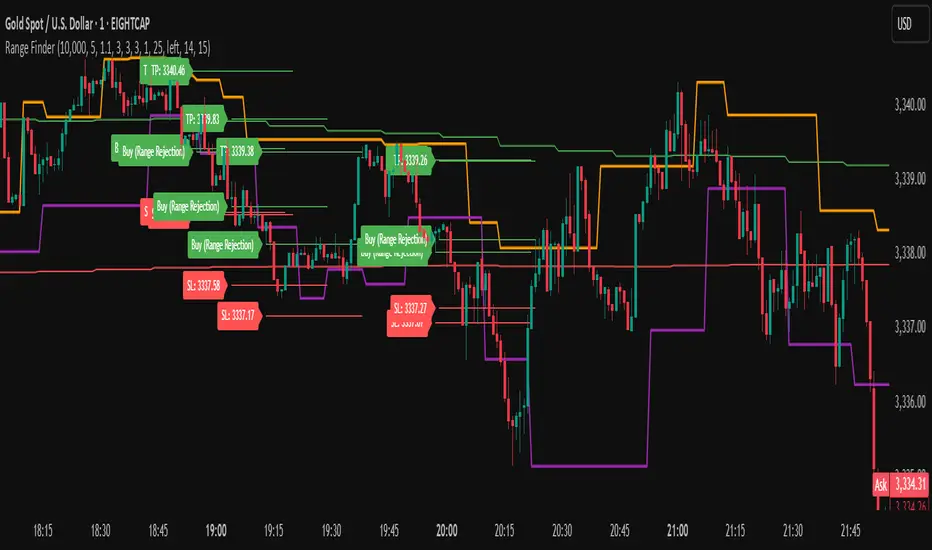

Range FinderRange Finder Strategy for TradingView

Overview

The Range Finder Strategy is a sophisticated trading system designed for forex and cryptocurrency markets, leveraging dynamic range detection, wick-based rejection patterns, and EMA confluence to execute high-probability trades. This strategy identifies key price ranges using pivot points and triggers trades when price rejects from these boundaries with significant wick formations, aligning with the broader market trend as confirmed by EMA crossovers. It incorporates robust risk management, customizable parameters, and visual aids for clear trade visualization, making it suitable for both manual and automated trading on platforms like Bitget via webhook alerts.

Strategy Components

1. Dynamic Range Detection

Pivot Points: The strategy identifies range boundaries using pivot highs and lows, calculated with a user-defined Pivot Length (default: 5 bars left/right). These pivots mark significant swing points, defining the upper (range high) and lower (range low) boundaries of the price range.

Visualization: The range high is plotted as an orange line, and the range low as a purple line, using a broken line style (plot.style_linebr) to show only confirmed pivot levels, providing a clear visual of the trading range.

2. Wick-Based Rejection Pattern

Wick Detection: The strategy looks for rejection candles at the range boundaries, characterized by significant wicks. A wick is considered valid if its size is at least the user-defined Wick to Body Ratio (default: 1.1, or 10% larger than the candle body).

Sell Signal: Triggered when the high exceeds the range high, the candle closes bearish (close < open), and the upper wick meets the ratio requirement.

Buy Signal: Triggered when the low falls below the range low, the candle closes bullish (close > open), and the lower wick meets the ratio requirement.

Purpose: These wicks indicate strong rejection at key levels, often signaling a reversal back into the range, providing high-probability entry points.

3. EMA Trend Confirmation

EMA Calculation: Uses two Exponential Moving Averages (EMAs) calculated on a user-selectable timeframe (default: 5-minute):

EMA 200: Long-term trend indicator (plotted in red).

EMA 50: Short-term trend indicator (plotted in green).

Crossover Logic:

A bullish trend is confirmed when the EMA 50 crosses above the EMA 200 (ema_trend_up = true).

A bearish trend is confirmed when the EMA 50 crosses below the EMA 200 (ema_trend_down = true).

Confluence Requirement: Trades are only executed when the wick rejection aligns with the EMA trend (e.g., sell signals require close < ema200 and bearish trend; buy signals require close > ema200 and bullish trend).

4. Risk Management

Position Sizing: Calculated based on the user-defined Account Balance (default: $10,000) and Risk Per Trade (default: 2%). The position size is determined as risk_amount / stop_distance, where stop_distance is derived from the Average True Range (ATR, default period: 14).

Stop Loss (SL): Set using an ATR-based multiplier (SL Multiplier, default: 9.0). For sells, SL is placed above the high; for buys, below the low.

Take Profit (TP): Set using an ATR-based multiplier (TP Multiplier, default: 6.0) scaled by the Risk:Reward Ratio (default: 6.0), ensuring a favorable reward-to-risk profile.

Example: For a $10,000 account with 2% risk, if ATR is 0.5, the position size is 400 units, with SL and TP dynamically adjusted to market volatility.

5. Trade Execution

Sell Entry: Triggered on a wick rejection above the range high, with bearish EMA confluence (ema_trend_down and close < ema200). Enters a short position with calculated SL and TP.

Buy Entry: Triggered on a wick rejection below the range low, with bullish EMA confluence (ema_trend_up and close > ema200). Enters a long position with calculated SL and TP.

Exit Logic: Uses strategy.exit to set SL and TP levels, closing trades when either is hit.

6. Visual Feedback

Lines and Labels: Upon trade entry, the strategy plots:

Red SL line and label (e.g., "SL: 123.45").

Green TP line and label (e.g., "TP: 120.00").

Entry line (red for sell, green for buy) labeled with "Sell (Range Rejection)" or "Buy (Range Rejection)".

Customization: Users can adjust the Line Length (default: 25 bars) for how long lines persist and Label Position (left or right) for optimal chart visibility.

7. Alert Conditions

Webhook Integration: Generates alerts for Bitget webhook integration, providing JSON-formatted messages with trade details (action, contracts, market position, size, price, symbol, and timestamp).

Usage: Traders can set up automated trading by connecting these alerts to trading bots or platforms supporting webhooks.

Estrategia IBEX 35 OptimizadaEstrategia IBEX 35 Optimizada

Para utilizar en largo y corto ibex35 en timeframe 45 min

Imbalance RSI Divergence Strategy# Imbalance RSI Divergence Strategy - User Guide

## What is This Strategy?

This strategy identifies **imbalance** zones in the market and combines them with **RSI divergence** to generate trading signals. It aims to capitalize on price gaps left by institutional investors and large volume movements.

### Main Settings

- **RSI Period (14)**: Period used for RSI calculation. Lower values = more sensitive, higher values = more stable signals.

- **ATR Period (10)**: Period for volatility measurement using Average True Range.

- **ATR Stop Loss Multiplier (2.0)**: How many ATR units to use for stop loss calculation.

- **Risk:Reward Ratio (4.0)**: Risk-reward ratio. 2.0 = 2 units of reward for 1 unit of risk.

- **Use RSI Divergence Filter (true)**: Enables/disables the RSI divergence filter.

### Imbalance Filters

- **Minimum Imbalance Size (ATR) (0.3)**: Minimum imbalance size in ATR units to filter out small imbalances.

- **Enable Lookback Limit (false)**: Activates historical lookback limitations.

- **Maximum Lookback Bars (300)**: Maximum number of bars to look back.

### Visual Settings

- **Show Imbalance Size**: Displays imbalance size in ATR units.

- **Show RSI Divergence Lines**: Shows/hides divergence lines.

- **Divergence Line Colors**: Colors for bullish/bearish divergence lines.

### Volatility-Based Adjustments

- **Low volatility markets**:

- Minimum Imbalance Size: 0.2-0.4 ATR

- ATR Stop Loss Multiplier: 1.5-2.0

- **High volatility markets**:

- Minimum Imbalance Size: 0.5-1.0 ATR

- ATR Stop Loss Multiplier: 2.5-3.5

### Risk Tolerance

- **Conservative approach**:

- Risk:Reward Ratio: 2.0-3.0

- RSI Divergence Filter: Enabled

- Minimum Imbalance Size: Higher (0.5+ ATR)

- **Aggressive approach**:

- Risk:Reward Ratio: 4.0-6.0

- Minimum Imbalance Size: Lower (0.2-0.3 ATR)

###Market Conditions

- **Trending markets**: Higher RSI Period (21-28)

- **Sideways markets**: Lower RSI Period (10-14)

- **Volatile markets**: Higher ATR Multiplier

## Recommended Testing Procedure

1. **Start with default settings** and backtest on 3-6 months of historical data

2. **Adjust RSI Period** to see which value produces better results

3. **Optimize ATR Multiplier** for stop loss levels

4. **Test different Risk:Reward ratios** comparatively

5. **Fine-tune Minimum Imbalance Size** to improve signal quality

## Important Considerations

- **False positive signals**: Imbalances may be less reliable during low volatility periods

- **Market openings**: First hours often produce more imbalances but can be riskier

- **News events**: Consider disabling strategy during major news releases

- **Backtesting**: Test across different market conditions (trending, sideways, volatile)

## Recommended Settings for Beginners

**Safe settings for new users:**

- RSI Period: 14

- ATR Period: 14

- ATR Stop Loss Multiplier: 2.5

- Risk:Reward Ratio: 3.0

- Minimum Imbalance Size: 0.5 ATR

- RSI Divergence Filter: Enabled

## Advanced Tips

### Signal Quality Improvement

- **Combine with market structure**: Look for imbalances near key support/resistance levels

- **Volume confirmation**: Higher volume during imbalance formation increases reliability

- **Multiple timeframe analysis**: Confirm signals on higher timeframes

### Risk Management

- **Position sizing**: Never risk more than 1-2% of account per trade

- **Maximum drawdown**: Set overall stop loss for the strategy

- **Market hours**: Consider avoiding low liquidity periods

### Performance Monitoring

- **Win rate**: Track percentage of profitable trades

- **Average R:R**: Monitor actual risk-reward achieved vs. target

- **Maximum consecutive losses**: Set alerts for strategy review

This strategy works best when combined with proper risk management and market analysis. Always backtest thoroughly before using real money and adjust parameters based on your specific market and trading style.

Keltner Alım Stratejisi v6 (10, 0.5)sadece keltner kanal girdilerinin değiştirilmesiyle oluşturulmuş bir göstergedir

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades