Patrones de entrada/salida V.1.0 -BETA-Este algoritmo intenta identificar patrones o fractales dentro de los movimientos de precios para dar señales de compra o venta de activos.

Search in scripts for "Fractal"

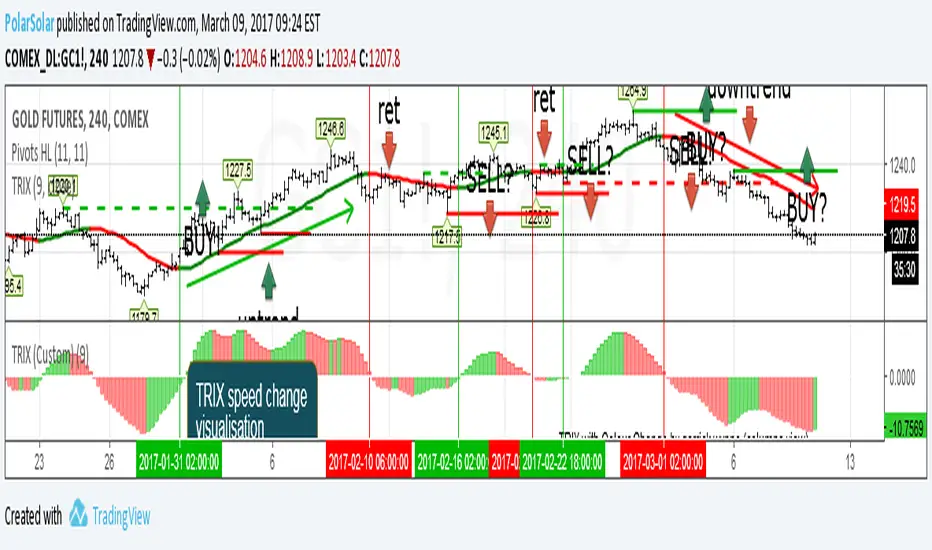

Triple Exponental Moving Average (overlay)TRIX Overlay + TRIX change Histogramm = simplest tactic to trade.

Just use last counter trend fractal to place delayed order

A counter trend fractal is a fractal down on TRIX uptrend or fractal up on TRIX downtrend.

Use TRIX speed change histogramm to seek divergence

Automatic Quadrant Lines📊 DETAILED EXPLANATION

Overview:

Automatic Quadrant Lines is a sophisticated pivot-based trading system that identifies key support and resistance levels, entry points, and price targets automatically. Based on fractal pivot analysis, this indicator creates a complete trading framework by mapping out potential long and short opportunities with precise entry and exit levels.

What Each Line Means:

Pivot Lines (Dark Red - Solid):

R1 (Resistance 1): The most recent pivot high - a key resistance level where price previously reversed downward

S1 (Support 1): The most recent pivot low - a key support level where price previously reversed upward. This line is thicker (weight 3) to emphasize its importance as the foundation for long setups

Entry Lines (Green/Red - Dashed or Solid):

L/E (Long Entry - Green Dashed): The trigger price for entering long positions. This is set at a strategic point above the pivot low, marking where bullish momentum is confirmed

S/E (Short Entry - Red Solid): The trigger price for entering short positions. This is set at a strategic point below the pivot high, marking where bearish momentum is confirmed

Long Target Lines (Green/Yellow/Cyan - Dashed):

Yellow Dashed Line (50%): First profit target for long positions - equal to one full range above the long entry

Cyan Dashed Line (75%): Second profit target for long positions - two full ranges above the long entry

Green Dashed Line (Long Target): Final profit target for long positions - three full ranges above the long entry, displayed with a dark green label showing the exact price

Short Target Lines (Red/Yellow/Cyan):

Yellow Line (50%): First profit target for short positions - equal to one full range below the short entry

Cyan Line (75%): Second profit target for short positions - two full ranges below the short entry

Red Line (Short Target): Final profit target for short positions - three full ranges below the short entry, displayed with a deep red label showing the exact price

Additional Lines:

Breakdown Target (Dark Green - Dashed): A support breakdown level located one range below S1, useful for managing risk if long positions fail

Technical Components:

Pivot Detection:

The indicator uses a configurable length (default 20) to identify swing highs and lows. A pivot high forms when the current high is the highest value over the specified length period on both sides. A pivot low forms when the current low is the lowest value over the specified period on both sides.

Entry Point Calculation:

Entry points are not placed at the pivot itself, but at strategic exit points of the pivot candle pattern. For long entries, the system identifies the high of the candle that preceded the pivot low. For short entries, it identifies the low of the candle that preceded the pivot high. This ensures entries occur on momentum confirmation rather than at turning points.

Target Calculation (Quadrant System):

The indicator calculates targets based on the range between the entry and the pivot (S1 for longs, R1 for shorts). It then projects this range upward (for longs) or downward (for shorts) in equal increments:

1x range = 50% target

2x range = 75% target

3x range = 100% target (Final Target)

Fractal Energy Filter:

The indicator incorporates a Fractal Energy (FE) calculation that measures market efficiency and trend strength. This helps filter entry signals, ensuring trades are taken only when market structure supports directional movement. The FE threshold can be adjusted in settings.

🎯 HOW TO USE (TRADER-FRIENDLY GUIDE)

📌 QUICK START GUIDE (IMPORTANT - Read This First!)

For optimal label visibility:

After adding this indicator to your chart for the first time, follow these ONE-TIME steps to ensure L/E and S/E labels are always visible:

Wait for the indicator to load and display L/E or S/E labels

Hover your mouse over any L/E or S/E label

Right-click on the label

Select "Bring to Front" or adjust "Visual Order" to bring it above price bars

Repeat for the other label type if needed

✅ You only need to do this ONCE - TradingView will remember this setting for all future labels!

If you ever want the labels to appear behind price bars again, simply right-click and select "Send to Back".

📈 For Long Trades:

Wait for Setup: The indicator automatically identifies a pivot low (S1 - thick dark red line) and calculates a long entry level (L/E - green dashed line with green label)

Entry Signal: When price crosses above the green L/E line, consider entering a long position. The system has confirmed bullish momentum

Profit Targets: Scale out of your position at the three target levels:

First target: Yellow dashed line (take 1/3 profit)

Second target: Cyan dashed line (take another 1/3 profit)

Final target: Green dashed line with "LONG TARGET" label (exit remaining position)

Stop Loss: Place your stop loss below the S1 level (thick dark red line). If price breaks below the dark green "Breakdown Target" line, consider exiting immediately

📉 For Short Trades:

Wait for Setup:

The indicator automatically identifies a pivot high (R1 - dark red line) and calculates a short entry level (S/E - red solid line with red label)

Entry Signal: When price crosses below the red S/E line, consider entering a short position. The system has confirmed bearish momentum

Profit Targets: Scale out of your position at the three target levels:

First target: Yellow line (take 1/3 profit)

Second target: Cyan line (take another 1/3 profit)

Final target: Red line with "SHORT TARGET" label (exit remaining position)

Stop Loss: Place your stop loss above the R1 level (dark red line)

💡 Key Trading Tips:

Color Coding: Remember GREEN = LONG, RED = SHORT throughout the entire system

Scaling Out: The three-target system allows you to lock in profits progressively while letting winners run

New Signals: When a new pivot forms, the indicator recalculates all levels. Old setups become invalid

Labels: The L/E and S/E labels mark the exact starting point of each entry line for easy identification

Price Display: Target labels show exact prices with proper comma formatting for easy reference

Timeframe: Works on any timeframe, but higher timeframes (4H, Daily) tend to produce more reliable signals

Customization: Adjust the Pivot Length (default 20) to make the system more responsive (lower number) or more stable (higher number)

⚠️ Risk Management:

Never risk more than 1-2% of your account per trade

The distance from entry to S1/R1 gives you a natural stop loss distance

Consider the full target distance when calculating position size

Not all setups will reach the final target - scaling out helps lock in profits

🔧 TROUBLESHOOTING

Q: My L/E or S/E labels are hidden behind candles

A: Right-click the label → "Bring to Front". This is a TradingView chart setting, not a script limitation. You only need to do this once.

Q: Can I hide the labels?

A: Yes! Uncheck "Show Labels" in the indicator settings.

Q: Can I adjust the label sizes?

A: Yes! Use the "Target Label Size" setting to adjust LONG/SHORT TARGET labels between Small, Normal, and Large.

Q: The labels moved when I clicked them

A: Labels are positioned automatically. If you accidentally moved them, simply refresh your chart.

Q: No signals are appearing

A: The indicator requires sufficient price history to detect pivots. Make sure you have at least 20+ bars on your chart. Try adjusting the Pivot Length setting.

DarkPool FlowDarkPool Flow is a professional-grade technical analysis tool designed to align retail traders with the dominant "smart money" flow. Unlike standard moving average crossovers that often generate false signals during consolidation, this script employs a multi-layered filtering engine to isolate high-probability trends.

The core philosophy of this indicator is that Trends are fractal. A sustainable move on a lower timeframe must be supported by momentum on a higher timeframe. By comparing a "Fast Signal Trend" against a "Slow Anchor Trend" (e.g., Daily vs. Weekly), the script identifies the market bias used by institutional algorithms.

This edition features a Smart Recovery Engine, ensuring that valid trends are not missed simply because momentum started slowly, and a Dynamic Cloud that visually represents the strength of the trend spread.

Key Features

1. Auto-Adaptive Timeframe Logic

The script eliminates the guesswork of Multi-Timeframe (MTF) selection. By enabling "Auto-Adapt," the indicator detects your current chart timeframe and automatically maps it to the mathematically correct institutional pairings:

Scalping (<15m): Uses 15-Minute Trend vs. 1-Hour Anchor.

Day Trading (15m - 1H): Uses 4-Hour Trend vs. Daily Anchor.

Swing Trading (4H - Daily): Uses Daily Trend vs. Weekly Anchor (The classic "Golden" setup).

Investing (Weekly): Uses 21-Week EMA vs. 50-Week SMA (Bull Market Support Band logic).

2. Smart Recovery Signal Engine

Standard crossover scripts often miss major moves if the specific breakout candle has low volume or weak ADX. This script utilizes a state-machine logic that "remembers" the trend direction. If a trend begins during low volatility (gray candles), the script waits. The moment volatility and momentum confirm the move, a Smart Recovery Signal is triggered, allowing you to enter an existing trend safely.

3. Chop Protection (Gray Candles)

Preservation of capital is the priority. The script analyzes the Average Directional Index (ADX) and Volatility (ATR).

Colored Candles (Green/Red): The market is trending with sufficient strength. Trading is permitted.

Gray Candles: The market is in a low-energy chop or consolidation (ADX < 20). Trading is discouraged.

4. Dynamic Trend Cloud

The space between the Fast and Slow trends is filled with a dynamic cloud.

Darker/Opaque Cloud: Indicates a widening spread, suggesting accelerating momentum.

Lighter/Transparent Cloud: Indicates a narrowing spread, suggesting the trend may be weakening or consolidating.

5. Pullback & Retest Signals (+)

While triangles mark the start of a trend, the Plus (+) signs mark low-risk opportunities to add to a position. These appear when price dips into the cloud, finds support at the "Fair Value" zone, and closes back in the direction of the trend with confirmed momentum.

User Guide & Strategy

Setup

Add the indicator to your chart.

For Beginners: Enable "Auto-Adaptive Timeframes" in the settings.

For Advanced Users: Disable Auto-Adapt and manually configure your Fast/Slow pairings (Default is Daily 50 EMA / Weekly 50 EMA).

Signal Mode: Choose "First Breakout Only" for a cleaner chart, or "All Signals" if you wish to see re-entry points during choppy starts.

Long Entry Criteria (Buy)

Trend: The Cloud must be Green (Fast Trend > Slow Trend).

Signal: A Green Triangle appears below the bar.

Confirmation: The signal candle must not be Gray.

Re-Entry: A small Green (+) sign appears, indicating a successful test of the cloud support.

Short Entry Criteria (Sell)

Trend: The Cloud must be Red (Fast Trend < Slow Trend).

Signal: A Red Triangle appears above the bar.

Confirmation: The signal candle must not be Gray.

Re-Entry: A small Red (+) sign appears, indicating a successful test of the cloud resistance.

Stop Loss & Risk Management

Stop Loss: A standard institutional stop loss is placed just beyond the Slow Trend Line (the outer edge of the cloud). If price closes beyond the Slow Trend, the macro thesis is invalid.

Take Profit: Target liquidity pools or use a trailing stop based on the Fast Trend line.

Settings Overview

Mode Selection: Toggle between Auto-Adaptive logic or Manual control.

Manual Configuration: Define the specific Timeframe, Length, and Type (EMA, SMA, WMA) for both Fast and Slow trends.

Signal Logic: Toggle "Show Pullback Signals" on/off. Switch between "First Breakout" or "All Signals."

Quality Filters: Toggle individual filters (ATR, RSI, ADX) to adjust sensitivity. Turning these off makes the script more responsive but increases false signals.

Visual Style: Customize colors for Bullish, Bearish, and Neutral (Gray) states. Adjust cloud transparency.

Disclaimer

Risk Warning: Trading financial markets involves a high degree of risk and is not suitable for all investors. You could lose some or all of your initial investment.

Educational Use Only: This script and the information provided herein are for educational and informational purposes only. They do not constitute financial advice, investment advice, trading advice, or any other recommendation.

No Guarantee: Past performance of any trading system or methodology is not necessarily indicative of future results. The "Institutional Trend" indicator is a tool to assist in technical analysis, not a crystal ball. The creators of this script assume no responsibility or liability for any trading losses or damages incurred as a result of using this tool. Always perform your own due diligence and consult with a qualified financial advisor before making investment decisions.

Elite S&D [By:CienF]Elite Supply & Demand

Description

Elite Supply & Demand is not just another zone indicator; it is a complete institutional trading system designed to identify high-probability imbalances in the market. Unlike standard indicators that flood the chart with weak zones, this script applies rigorous Price Action rules to filter, score, and validate only the most significant areas of interest.

The core philosophy of this tool is "Anormality". Institutional activity leaves a footprint in the form of explosive volatility relative to the recent context. This indicator detects these footprints, measures their intensity, and validates them against market structure.

Key Features

🔥 Dynamic Quality Scoring (The "Elite" Feature) The indicator doesn't just draw boxes; it rates them. It calculates a Volumetric Ratio comparing the explosive move against the historical average at the moment of creation.

Contextual Intelligence: It continues to track the initial move. If the momentum continues after a small pause, the score updates in real-time.

Visual Grades:

🔥 Fire: High Anormality (Institutional Imbalance).

⚡ Lightning: Moderate Anormality (Decent strength).

No Icon: Standard move.

🏗️ Advanced Structure Validation Includes a unique "Eventual Break" filter.

Latent Zones: You can choose to hide zones that haven't broken structure yet.

Auto-Validation: The zone remains invisible/transparent until price breaks a recent High/Low or Fractal Pivot. Once the break occurs, the zone "activates" on your chart.

🧠 Smart Mitigation Logic

No Zombie Zones: Once a zone is mitigated (touched), it is strictly processed. It can either turn gray (History Mode) or be removed instantly.

Priority Handling: Mitigated zones are never re-colored or re-validated, keeping your chart clean and accurate.

🚀 Performance Optimization

Date Lookback: Includes a "Days Back" filter to prevent the script from calculating thousands of historical candles, ensuring smooth performance even on lower timeframes (1m, 5m).

🔔 Integrated Alerts

Creation: Get notified immediately when a potential zone forms.

Validation: Get notified specifically when a latent zone breaks structure and becomes active.

How It Works ( The Logic)

Phase 1: The Base (Indecision): Identifies candles with small bodies (≤ 50% of range) representing equilibrium/accumulation.

Phase 2: The Explosion (Imbalance): Looks for a strong breakout candle (≥ 60% body) that moves away from the base.

Phase 3: The Follow-up: Verifies that the move continues. It allows for "Smart Pauses" (single indecision candles) within the trend but invalidates the zone if a reversal occurs immediately.

Phase 4: Structure Check: Verifies if the move broke the Recent Range (High/Low) or Fractal Pivots.

Settings & Configuration

1. Base & Exit Rules

Max % Body: Threshold to define an indecision candle (Default: 50%).

Explosive Min: Minimum strength required for the exit candle.

2. Structure Validation

Structure Type: Choose between Recent Range (more fluid) or Fractal Pivots (stricter).

Filter Eventual Break: Highly Recommended. If checked, zones appear only after they prove their strength by breaking structure.

3. Scoring (Quality)

High Quality Ratio: The multiplier required to earn the 🔥 icon (e.g., 2.0x larger than average).

Allow Pause: Allows the algorithm to capture larger moves even if there is a single small candle in the middle of the explosive leg.

4. Performance

Days Back: Limits how far back the indicator draws. Reduce this number on low timeframes to speed up loading.

Usage Recommendations

For Trend Trading: Look for "Follow-up" zones. If you see a 🔥 zone forming in the direction of the higher timeframe trend, it is a high-probability entry.

For Reversals: Use the "Filter Eventual Break" feature. Wait for the indicator to reveal a zone that has broken a major structure point.

Stop Loss Placement: The indicator draws the zone covering the entire "Base" (wicks included). A safe stop is typically just beyond the distal line (33% recommended) of the box.

🔔 How to Set Up Alerts

Since this indicator uses the dynamic alert() function to send detailed messages (Entry Price, Stop Zone, Type), you must configure it correctly:

Add the indicator to your chart and adjust the settings to your preference.

Click the "Create Alert" button (Clock Icon) on the right toolbar or press Alt + A.

Condition: Select "Elite S&D " from the dropdown menu.

Trigger (CRITICAL): You must select "Any alert() function call".

Note: Do not select "Crossing" or other standard conditions, or the alerts will not trigger.

Expiration: Select "Open-ended" (if you have a Premium plan) or set a future date.

Alert Actions: Choose where you want to receive the alert (Notify on App, Show Popup, Send Email, etc.).

Message: You can leave this default. The script automatically generates a detailed message with the Ticker, Timeframe, Zone Type, and Coordinates.

Click Create.

Disclaimer: This tool is designed to assist in technical analysis and does not constitute financial advice. Always use proper risk management.

PyraTime Harmonic 369Concept and Methodology PyraTime Harmonic 369 is a quantitative time-projection tool designed to apply Modular Arithmetic to market analysis. Unlike linear time indicators, this tool projects non-linear integer sequences derived from Digital Root Summation (Base-9 Reduction).

The core logic utilizes the mathematical progression of the 3-6-9 constants. By anchoring to a user-defined "Origin Pivot," the script projects three distinct harmonic triads to identify potential Temporal Confluence—moments where mathematical time cycles align with price action.

Technical Features This script focuses on the Standard Scalar (1x) projection of the Digital Root sequence:

The Root-3 Triad (Red): Projects intervals of 174, 285, 396. (Mathematical Sum: 1+7+4=12→3)

The Root-6 Triad (Green): Projects intervals of 417, 528, 639. (Mathematical Sum: 4+1+7=12→3, inverted)

The Root-9 Triad (Blue): Projects intervals of 741, 852, 963. (Mathematical Sum: 7+4+1=12→3... completion to 9)

How to Use

Set Anchor: Input the time of a significant High or Low in the settings.

Select Resolution: This tool is optimized for 1-minute (Micro-Harmonics) and 15-minute (Intraday Harmonics) charts.

Analyze Clusters: The vertical lines represent calculated harmonic intervals. Traders look for "Clusters" where a Root-3 and Root-9 cycle land on adjacent bars, indicating a high-probability pivot.

System Architecture & Version Comparison This script represents the foundational layer of the PyraTime ecosystem.

This Script (PyraTime Harmonic 369):

Scalar: Standard 1x Multiplier only.

Focus: Intraday & Micro-structure (1m, 15m).

Engine: Core Digital Root Integers.

PyraTime Harmonic Matrix (Advanced Edition):

Scalar Engine: Unlocks Quad-Fractal (4x), Tri-Fractal (3x), and Bi-Fractal (2x) multipliers for institutional cycle analysis.

Apex Logic: Auto-detection of the "963" Completion Sequence (Gold Highlight).

Event Horizon: Includes a live Predictive Dashboard that calculates the time-delta to the next harmonic event across all scalar groups.

Disclaimer This tool is for the educational analysis of Number Theory in financial markets. It projects time intervals and does not predict price direction. Past performance does not guarantee future results.

SR-ZnV2There are many support and resistance scripts out there. I was unable to find one that met all of my needs so I have expanded on the closest ones that I was able to discover. The ability to show persistent S/R levels by volume at various time frames automates much of the process for the user with unique and customizable features, the lastest dated of which are displayed by its time frame support/resistance strength and extend toward the right of the screen where they can be seen more clearly by price .

// Original script is thanks to tommyf1001, synapticex and additional modifications is thanks to Lij_MC. Credit to both of them for most of the logic behind this script. Since then I have made many changes to this script as noted below.

// Changed default S/R lines from plots to lines, and gave option to user to change between solid line, dashed line, or dotted line for both S/R lines.

// Added additional time frame and gave more TF options for TF1 other than current TF. Now you will have 4 time frames to plot S/R zones from.

// Gave user option to easily change line thickness for all S/R lines.

// Made it easier to change colors of S/R lines and zones by consolidating the options under settings (rather than under style).

// Added extensions to active SR Zones to extend all the way right.

// Added option to extend or not extend the previous S/R zones up to next S/R zone.

// Added optional time frame labels to active S/R zones, with left and right options as well as option to adjust how far to the right label is set.

// Fixed issue where the higher time frame S/R zone was not properly starting from the high/low of fractal. Now any higher time frame S/R will begin exactly at the High/Low points.

// Added to script a function that will prevent S/R zones from lower time frames displaying while on a higher time frame. This helps clean up the chart quite a bit.

// Created arrays for each time frame's lines and labels so that the number of S/R zones can be controlled for each time frame and limit memory consumption.

// New alert options added and customized alert messages.

Stochastic Enhanced [DCAUT]█ Stochastic Enhanced

📊 ORIGINALITY & INNOVATION

The Stochastic Enhanced indicator builds upon George Lane's classic momentum oscillator (developed in the late 1950s) by providing comprehensive smoothing algorithm flexibility. While traditional implementations limit users to Simple Moving Average (SMA) smoothing, this enhanced version offers 21 advanced smoothing algorithms, allowing traders to optimize the indicator's characteristics for different market conditions and trading styles.

Key Improvements:

Extended from single SMA smoothing to 21 professional-grade algorithms including adaptive filters (KAMA, FRAMA), zero-lag methods (ZLEMA, T3), and advanced digital filters (Kalman, Laguerre)

Maintains backward compatibility with traditional Stochastic calculations through SMA default setting

Unified smoothing algorithm applies to both %K and %D lines for consistent signal processing characteristics

Enhanced visual feedback with clear color distinction and background fill highlighting for intuitive signal recognition

Comprehensive alert system covering crossovers and zone entries for systematic trade management

Differentiation from Traditional Stochastic:

Traditional Stochastic indicators use fixed SMA smoothing, which introduces consistent lag regardless of market volatility. This enhanced version addresses the limitation by offering adaptive algorithms that adjust to market conditions (KAMA, FRAMA), reduce lag without sacrificing smoothness (ZLEMA, T3, HMA), or provide superior noise filtering (Kalman Filter, Laguerre filters). The flexibility helps traders balance responsiveness and stability according to their specific needs.

📐 MATHEMATICAL FOUNDATION

Core Stochastic Calculation:

The Stochastic Oscillator measures the position of the current close relative to the high-low range over a specified period:

Step 1: Raw %K Calculation

%K_raw = 100 × (Close - Lowest Low) / (Highest High - Lowest Low)

Where:

Close = Current closing price

Lowest Low = Lowest low over the %K Length period

Highest High = Highest high over the %K Length period

Result ranges from 0 (close at period low) to 100 (close at period high)

Step 2: Smoothed %K Calculation

%K = MA(%K_raw, K Smoothing Period, MA Type)

Where:

MA = Selected moving average algorithm (SMA, EMA, etc.)

K Smoothing = 1 for Fast Stochastic, 3+ for Slow Stochastic

Traditional Fast Stochastic uses %K_raw directly without smoothing

Step 3: Signal Line %D Calculation

%D = MA(%K, D Smoothing Period, MA Type)

Where:

%D acts as a signal line and moving average of %K

D Smoothing typically set to 3 periods in traditional implementations

Both %K and %D use the same MA algorithm for consistent behavior

Available Smoothing Algorithms (21 Options):

Standard Moving Averages:

SMA (Simple): Equal-weighted average, traditional default, consistent lag characteristics

EMA (Exponential): Recent price emphasis, faster response to changes, exponential decay weighting

RMA (Rolling/Wilder's): Smoothed average used in RSI, less reactive than EMA

WMA (Weighted): Linear weighting favoring recent data, moderate responsiveness

VWMA (Volume-Weighted): Incorporates volume data, reflects market participation intensity

Advanced Moving Averages:

HMA (Hull): Reduced lag with smoothness, uses weighted moving averages and square root period

ALMA (Arnaud Legoux): Gaussian distribution weighting, minimal lag with good noise reduction

LSMA (Least Squares): Linear regression based, fits trend line to data points

DEMA (Double Exponential): Reduced lag compared to EMA, uses double smoothing technique

TEMA (Triple Exponential): Further lag reduction, triple smoothing with lag compensation

ZLEMA (Zero-Lag Exponential): Lag elimination attempt using error correction, very responsive

TMA (Triangular): Double-smoothed SMA, very smooth but slower response

Adaptive & Intelligent Filters:

T3 (Tilson T3): Six-pass exponential smoothing with volume factor adjustment, excellent smoothness

FRAMA (Fractal Adaptive): Adapts to market fractal dimension, faster in trends, slower in ranges

KAMA (Kaufman Adaptive): Efficiency ratio based adaptation, responds to volatility changes

McGinley Dynamic: Self-adjusting mechanism following price more accurately, reduced whipsaws

Kalman Filter: Optimal estimation algorithm from aerospace engineering, dynamic noise filtering

Advanced Digital Filters:

Ultimate Smoother: Advanced digital filter design, superior noise rejection with minimal lag

Laguerre Filter: Time-domain filter with N-order implementation, adjustable lag characteristics

Laguerre Binomial Filter: 6-pole Laguerre filter, extremely smooth output for long-term analysis

Super Smoother: Butterworth filter implementation, removes high-frequency noise effectively

📊 COMPREHENSIVE SIGNAL ANALYSIS

Absolute Level Interpretation (%K Line):

%K Above 80: Overbought condition, price near period high, potential reversal or pullback zone, caution for new long entries

%K in 70-80 Range: Strong upward momentum, bullish trend confirmation, uptrend likely continuing

%K in 50-70 Range: Moderate bullish momentum, neutral to positive outlook, consolidation or mild uptrend

%K in 30-50 Range: Moderate bearish momentum, neutral to negative outlook, consolidation or mild downtrend

%K in 20-30 Range: Strong downward momentum, bearish trend confirmation, downtrend likely continuing

%K Below 20: Oversold condition, price near period low, potential bounce or reversal zone, caution for new short entries

Crossover Signal Analysis:

%K Crosses Above %D (Bullish Cross): Momentum shifting bullish, faster line overtakes slower signal, consider long entry especially in oversold zone, strongest when occurring below 20 level

%K Crosses Below %D (Bearish Cross): Momentum shifting bearish, faster line falls below slower signal, consider short entry especially in overbought zone, strongest when occurring above 80 level

Crossover in Midrange (40-60): Less reliable signals, often in choppy sideways markets, require additional confirmation from trend or volume analysis

Multiple Failed Crosses: Indicates ranging market or choppy conditions, reduce position sizes or avoid trading until clear directional move

Advanced Divergence Patterns (%K Line vs Price):

Bullish Divergence: Price makes lower low while %K makes higher low, indicates weakening bearish momentum, potential trend reversal upward, more reliable when %K in oversold zone

Bearish Divergence: Price makes higher high while %K makes lower high, indicates weakening bullish momentum, potential trend reversal downward, more reliable when %K in overbought zone

Hidden Bullish Divergence: Price makes higher low while %K makes lower low, indicates trend continuation in uptrend, bullish trend strength confirmation

Hidden Bearish Divergence: Price makes lower high while %K makes higher high, indicates trend continuation in downtrend, bearish trend strength confirmation

Momentum Strength Analysis (%K Line Slope):

Steep %K Slope: Rapid momentum change, strong directional conviction, potential for extended moves but also increased reversal risk

Gradual %K Slope: Steady momentum development, sustainable trends more likely, lower probability of sharp reversals

Flat or Horizontal %K: Momentum stalling, potential reversal or consolidation ahead, wait for directional break before committing

%K Oscillation Within Range: Indicates ranging market, sideways price action, better suited for range-trading strategies than trend following

🎯 STRATEGIC APPLICATIONS

Mean Reversion Strategy (Range-Bound Markets):

Identify ranging market conditions using price action or Bollinger Bands

Wait for Stochastic to reach extreme zones (above 80 for overbought, below 20 for oversold)

Enter counter-trend position when %K crosses %D in extreme zone (sell on bearish cross above 80, buy on bullish cross below 20)

Set profit targets near opposite extreme or midline (50 level)

Use tight stop-loss above recent swing high/low to protect against breakout scenarios

Exit when Stochastic reaches opposite extreme or %K crosses %D in opposite direction

Trend Following with Momentum Confirmation:

Identify primary trend direction using higher timeframe analysis or moving averages

Wait for Stochastic pullback to oversold zone (<20) in uptrend or overbought zone (>80) in downtrend

Enter in trend direction when %K crosses %D confirming momentum shift (bullish cross in uptrend, bearish cross in downtrend)

Use wider stops to accommodate normal trend volatility

Add to position on subsequent pullbacks showing similar Stochastic pattern

Exit when Stochastic shows opposite extreme with failed cross or bearish/bullish divergence

Divergence-Based Reversal Strategy:

Scan for divergence between price and Stochastic at swing highs/lows

Confirm divergence with at least two price pivots showing divergent Stochastic readings

Wait for %K to cross %D in direction of anticipated reversal as entry trigger

Enter position in divergence direction with stop beyond recent swing extreme

Target profit at key support/resistance levels or Fibonacci retracements

Scale out as Stochastic reaches opposite extreme zone

Multi-Timeframe Momentum Alignment:

Analyze Stochastic on higher timeframe (4H or Daily) for primary trend bias

Switch to lower timeframe (1H or 15M) for precise entry timing

Only take trades where lower timeframe Stochastic signal aligns with higher timeframe momentum direction

Higher timeframe Stochastic in bullish zone (>50) = only take long entries on lower timeframe

Higher timeframe Stochastic in bearish zone (<50) = only take short entries on lower timeframe

Exit when lower timeframe shows counter-signal or higher timeframe momentum reverses

Zone Transition Strategy:

Monitor Stochastic for transitions between zones (oversold to neutral, neutral to overbought, etc.)

Enter long when Stochastic crosses above 20 (exiting oversold), signaling momentum shift from bearish to neutral/bullish

Enter short when Stochastic crosses below 80 (exiting overbought), signaling momentum shift from bullish to neutral/bearish

Use zone midpoint (50) as dynamic support/resistance for position management

Trail stops as Stochastic advances through favorable zones

Exit when Stochastic fails to maintain momentum and reverses back into prior zone

📋 DETAILED PARAMETER CONFIGURATION

%K Length (Default: 14):

Lower Values (5-9): Highly sensitive to price changes, generates more frequent signals, increased false signals in choppy markets, suitable for very short-term trading and scalping

Standard Values (10-14): Balanced sensitivity and reliability, traditional default (14) widely used,适合 swing trading and intraday strategies

Higher Values (15-21): Reduced sensitivity, smoother oscillations, fewer but potentially more reliable signals, better for position trading and lower timeframe noise reduction

Very High Values (21+): Slow response, long-term momentum measurement, fewer trading signals, suitable for weekly or monthly analysis

%K Smoothing (Default: 3):

Value 1: Fast Stochastic, uses raw %K calculation without additional smoothing, most responsive to price changes, generates earliest signals with higher noise

Value 3: Slow Stochastic (default), traditional smoothing level, reduces false signals while maintaining good responsiveness, widely accepted standard

Values 5-7: Very slow response, extremely smooth oscillations, significantly reduced whipsaws but delayed entry/exit timing

Recommendation: Default value 3 suits most trading scenarios, active short-term traders may use 1, conservative long-term positions use 5+

%D Smoothing (Default: 3):

Lower Values (1-2): Signal line closely follows %K, frequent crossover signals, useful for active trading but requires strict filtering

Standard Value (3): Traditional setting providing balanced signal line behavior, optimal for most trading applications

Higher Values (4-7): Smoother signal line, fewer crossover signals, reduced whipsaws but slower confirmation, better for trend trading

Very High Values (8+): Signal line becomes slow-moving reference, crossovers rare and highly significant, suitable for long-term position changes only

Smoothing Type Algorithm Selection:

For Trending Markets:

ZLEMA, DEMA, TEMA: Reduced lag for faster trend entry, quick response to momentum shifts, suitable for strong directional moves

HMA, ALMA: Good balance of smoothness and responsiveness, effective for clean trend following without excessive noise

EMA: Classic choice for trending markets, faster than SMA while maintaining reasonable stability

For Ranging/Choppy Markets:

Kalman Filter, Super Smoother: Superior noise filtering, reduces false signals in sideways action, helps identify genuine reversal points

Laguerre Filters: Smooth oscillations with adjustable lag, excellent for mean reversion strategies in ranges

T3, TMA: Very smooth output, filters out market noise effectively, clearer extreme zone identification

For Adaptive Market Conditions:

KAMA: Automatically adjusts to market efficiency, fast in trends and slow in congestion, reduces whipsaws during transitions

FRAMA: Adapts to fractal market structure, responsive during directional moves, conservative during uncertainty

McGinley Dynamic: Self-adjusting smoothing, follows price naturally, minimizes lag in trending markets while filtering noise in ranges

For Conservative Long-Term Analysis:

SMA: Traditional choice, predictable behavior, widely understood characteristics

RMA (Wilder's): Smooth oscillations, reduced sensitivity to outliers, consistent behavior across market conditions

Laguerre Binomial Filter: Extremely smooth output, ideal for weekly/monthly timeframe analysis, eliminates short-term noise completely

Source Selection:

Close (Default): Standard choice using closing prices, most common and widely tested

HLC3 or OHLC4: Incorporates more price information, reduces impact of sudden spikes or gaps, smoother oscillator behavior

HL2: Midpoint of high-low range, emphasizes intrabar volatility, useful for markets with wide intraday ranges

Custom Source: Can use other indicators as input (e.g., Heikin Ashi close, smoothed price), creates derivative momentum indicators

📈 PERFORMANCE ANALYSIS & COMPETITIVE ADVANTAGES

Responsiveness Characteristics:

Traditional SMA-Based Stochastic:

Fixed lag regardless of market conditions, consistent delay of approximately (K Smoothing + D Smoothing) / 2 periods

Equal treatment of trending and ranging markets, no adaptation to volatility changes

Predictable behavior but suboptimal in varying market regimes

Enhanced Version with Adaptive Algorithms:

KAMA and FRAMA reduce lag by up to 40-60% in strong trends compared to SMA while maintaining similar smoothness in ranges

ZLEMA and T3 provide near-zero lag characteristics for early entry signals with acceptable noise levels

Kalman Filter and Super Smoother offer superior noise rejection, reducing false signals in choppy conditions by estimations of 30-50% compared to SMA

Performance improvements vary by algorithm selection and market conditions

Signal Quality Improvements:

Adaptive algorithms help reduce whipsaw trades in ranging markets by adjusting sensitivity dynamically

Advanced filters (Kalman, Laguerre, Super Smoother) provide clearer extreme zone readings for mean reversion strategies

Zero-lag methods (ZLEMA, DEMA, TEMA) generate earlier crossover signals in trending markets for improved entry timing

Smoother algorithms (T3, Laguerre Binomial) reduce false extreme zone touches for more reliable overbought/oversold signals

Comparison with Standard Implementations:

Versus Basic Stochastic: Enhanced version offers 21 smoothing options versus single SMA, allowing optimization for specific market characteristics and trading styles

Versus RSI: Stochastic provides range-bound measurement (0-100) with clear extreme zones, RSI measures momentum speed, Stochastic offers clearer visual overbought/oversold identification

Versus MACD: Stochastic bounded oscillator suitable for mean reversion, MACD unbounded indicator better for trend strength, Stochastic excels in range-bound and oscillating markets

Versus CCI: Stochastic has fixed bounds (0-100) for consistent interpretation, CCI unbounded with variable extremes, Stochastic provides more standardized extreme readings across different instruments

Flexibility Advantages:

Single indicator adaptable to multiple strategies through algorithm selection rather than requiring different indicator variants

Ability to optimize smoothing characteristics for specific instruments (e.g., smoother for crypto volatility, faster for forex trends)

Multi-timeframe analysis with consistent algorithm across timeframes for coherent momentum picture

Backtesting capability with algorithm as optimization parameter for strategy development

Limitations and Considerations:

Increased complexity from multiple algorithm choices may lead to over-optimization if parameters are curve-fitted to historical data

Adaptive algorithms (KAMA, FRAMA) have adjustment periods during market regime changes where signals may be less reliable

Zero-lag algorithms sacrifice some smoothness for responsiveness, potentially increasing noise sensitivity in very choppy conditions

Performance characteristics vary significantly across algorithms, requiring understanding and testing before live implementation

Like all oscillators, Stochastic can remain in extreme zones for extended periods during strong trends, generating premature reversal signals

USAGE NOTES

This indicator is designed for technical analysis and educational purposes to provide traders with enhanced flexibility in momentum analysis. The Stochastic Oscillator has limitations and should not be used as the sole basis for trading decisions.

Important Considerations:

Algorithm performance varies with market conditions - no single smoothing method is optimal for all scenarios

Extreme zone signals (overbought/oversold) indicate potential reversal areas but not guaranteed turning points, especially in strong trends

Crossover signals may generate false entries during sideways choppy markets regardless of smoothing algorithm

Divergence patterns require confirmation from price action or additional indicators before trading

Past indicator characteristics and backtested results do not guarantee future performance

Always combine Stochastic analysis with proper risk management, position sizing, and multi-indicator confirmation

Test selected algorithm on historical data of specific instrument and timeframe before live trading

Market regime changes may require algorithm adjustment for optimal performance

The enhanced smoothing options are intended to provide tools for optimizing the indicator's behavior to match individual trading styles and market characteristics, not to create a perfect predictive tool. Responsible usage includes understanding the mathematical properties of selected algorithms and their appropriate application contexts.

TA█ TA Library

📊 OVERVIEW

TA is a Pine Script technical analysis library. This library provides 25+ moving averages and smoothing filters , from classic SMA/EMA to Kalman Filters and adaptive algorithms, implemented based on academic research.

🎯 Core Features

Academic Based - Algorithms follow original papers and formulas

Performance Optimized - Pre-calculated constants for faster response

Unified Interface - Consistent function design

Research Based - Integrates technical analysis research

🎯 CONCEPTS

Library Design Philosophy

This technical analysis library focuses on providing:

Academic Foundation

Algorithms based on published research papers and academic standards

Implementations that follow original mathematical formulations

Clear documentation with research references

Developer Experience

Unified interface design for consistent usage patterns

Pre-calculated constants for optimal performance

Comprehensive function collection to reduce development time

Single import statement for immediate access to all functions

Each indicator encapsulated as a simple function call - one line of code simplifies complexity

Technical Excellence

25+ carefully implemented moving averages and filters

Support for advanced algorithms like Kalman Filter and MAMA/FAMA

Optimized code structure for maintainability and reliability

Regular updates incorporating latest research developments

🚀 USING THIS LIBRARY

Import Library

//@version=6

import DCAUT/TA/1 as dta

indicator("Advanced Technical Analysis", overlay=true)

Basic Usage Example

// Classic moving average combination

ema20 = ta.ema(close, 20)

kama20 = dta.kama(close, 20)

plot(ema20, "EMA20", color.red, 2)

plot(kama20, "KAMA20", color.green, 2)

Advanced Trading System

// Adaptive moving average system

kama = dta.kama(close, 20, 2, 30)

= dta.mamaFama(close, 0.5, 0.05)

// Trend confirmation and entry signals

bullTrend = kama > kama and mamaValue > famaValue

bearTrend = kama < kama and mamaValue < famaValue

longSignal = ta.crossover(close, kama) and bullTrend

shortSignal = ta.crossunder(close, kama) and bearTrend

plot(kama, "KAMA", color.blue, 3)

plot(mamaValue, "MAMA", color.orange, 2)

plot(famaValue, "FAMA", color.purple, 2)

plotshape(longSignal, "Buy", shape.triangleup, location.belowbar, color.green)

plotshape(shortSignal, "Sell", shape.triangledown, location.abovebar, color.red)

📋 FUNCTIONS REFERENCE

ewma(source, alpha)

Calculates the Exponentially Weighted Moving Average with dynamic alpha parameter.

Parameters:

source (series float) : Series of values to process.

alpha (series float) : The smoothing parameter of the filter.

Returns: (float) The exponentially weighted moving average value.

dema(source, length)

Calculates the Double Exponential Moving Average (DEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Double Exponential Moving Average value.

tema(source, length)

Calculates the Triple Exponential Moving Average (TEMA) of a given data series.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triple Exponential Moving Average value.

zlema(source, length)

Calculates the Zero-Lag Exponential Moving Average (ZLEMA) of a given data series. This indicator attempts to eliminate the lag inherent in all moving averages.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Zero-Lag Exponential Moving Average value.

tma(source, length)

Calculates the Triangular Moving Average (TMA) of a given data series. TMA is a double-smoothed simple moving average that reduces noise.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Triangular Moving Average value.

frama(source, length)

Calculates the Fractal Adaptive Moving Average (FRAMA) of a given data series. FRAMA adapts its smoothing factor based on fractal geometry to reduce lag. Developed by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: (float) The calculated Fractal Adaptive Moving Average value.

kama(source, length, fastLength, slowLength)

Calculates Kaufman's Adaptive Moving Average (KAMA) of a given data series. KAMA adjusts its smoothing based on market efficiency ratio. Developed by Perry J. Kaufman.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the efficiency calculation.

fastLength (simple int) : Fast EMA length for smoothing calculation. Optional. Default is 2.

slowLength (simple int) : Slow EMA length for smoothing calculation. Optional. Default is 30.

Returns: (float) The calculated Kaufman's Adaptive Moving Average value.

t3(source, length, volumeFactor)

Calculates the Tilson Moving Average (T3) of a given data series. T3 is a triple-smoothed exponential moving average with improved lag characteristics. Developed by Tim Tillson.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

volumeFactor (simple float) : Volume factor affecting responsiveness. Optional. Default is 0.7.

Returns: (float) The calculated Tilson Moving Average value.

ultimateSmoother(source, length)

Calculates the Ultimate Smoother of a given data series. Uses advanced filtering techniques to reduce noise while maintaining responsiveness. Based on digital signal processing principles by John Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the smoothing calculation.

Returns: (float) The calculated Ultimate Smoother value.

kalmanFilter(source, processNoise, measurementNoise)

Calculates the Kalman Filter of a given data series. Optimal estimation algorithm that estimates true value from noisy observations. Based on the Kalman Filter algorithm developed by Rudolf Kalman (1960).

Parameters:

source (series float) : Series of values to process.

processNoise (simple float) : Process noise variance (Q). Controls adaptation speed. Optional. Default is 0.05.

measurementNoise (simple float) : Measurement noise variance (R). Controls smoothing. Optional. Default is 1.0.

Returns: (float) The calculated Kalman Filter value.

mcginleyDynamic(source, length)

Calculates the McGinley Dynamic of a given data series. McGinley Dynamic is an adaptive moving average that adjusts to market speed changes. Developed by John R. McGinley Jr.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the dynamic calculation.

Returns: (float) The calculated McGinley Dynamic value.

mama(source, fastLimit, slowLimit)

Calculates the Mesa Adaptive Moving Average (MAMA) of a given data series. MAMA uses Hilbert Transform Discriminator to adapt to market cycles dynamically. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Mesa Adaptive Moving Average value.

fama(source, fastLimit, slowLimit)

Calculates the Following Adaptive Moving Average (FAMA) of a given data series. FAMA follows MAMA with reduced responsiveness for crossover signals. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: (float) The calculated Following Adaptive Moving Average value.

mamaFama(source, fastLimit, slowLimit)

Calculates Mesa Adaptive Moving Average (MAMA) and Following Adaptive Moving Average (FAMA).

Parameters:

source (series float) : Series of values to process.

fastLimit (simple float) : Maximum alpha (responsiveness). Optional. Default is 0.5.

slowLimit (simple float) : Minimum alpha (smoothing). Optional. Default is 0.05.

Returns: ( ) Tuple containing values.

laguerreFilter(source, length, gamma, order)

Calculates the standard N-order Laguerre Filter of a given data series. Standard Laguerre Filter uses uniform weighting across all polynomial terms. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.8.

order (simple int) : The order of the Laguerre filter (1-10). Higher order increases lag. Optional. Default is 8.

Returns: (float) The calculated standard Laguerre Filter value.

laguerreBinomialFilter(source, length, gamma)

Calculates the Laguerre Binomial Filter of a given data series. Uses 6-pole feedback with binomial weighting coefficients. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Length for UltimateSmoother preprocessing.

gamma (simple float) : Feedback coefficient (0-1). Lower values reduce lag. Optional. Default is 0.5.

Returns: (float) The calculated Laguerre Binomial Filter value.

superSmoother(source, length)

Calculates the Super Smoother of a given data series. SuperSmoother is a second-order Butterworth filter from aerospace technology. Developed by John F. Ehlers.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Period for the filter calculation.

Returns: (float) The calculated Super Smoother value.

rangeFilter(source, length, multiplier)

Calculates the Range Filter of a given data series. Range Filter reduces noise by filtering price movements within a dynamic range.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the average range calculation.

multiplier (simple float) : Multiplier for the smooth range. Higher values increase filtering. Optional. Default is 2.618.

Returns: ( ) Tuple containing filtered value, trend direction, upper band, and lower band.

qqe(source, rsiLength, rsiSmooth, qqeFactor)

Calculates the Quantitative Qualitative Estimation (QQE) of a given data series. QQE is an improved RSI that reduces noise and provides smoother signals. Developed by Igor Livshin.

Parameters:

source (series float) : Series of values to process.

rsiLength (simple int) : Number of bars for the RSI calculation. Optional. Default is 14.

rsiSmooth (simple int) : Number of bars for smoothing the RSI. Optional. Default is 5.

qqeFactor (simple float) : QQE factor for volatility band width. Optional. Default is 4.236.

Returns: ( ) Tuple containing smoothed RSI and QQE trend line.

sslChannel(source, length)

Calculates the Semaphore Signal Level (SSL) Channel of a given data series. SSL Channel provides clear trend signals using moving averages of high and low prices.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

Returns: ( ) Tuple containing SSL Up and SSL Down lines.

ma(source, length, maType)

Calculates a Moving Average based on the specified type. Universal interface supporting all moving average algorithms.

Parameters:

source (series float) : Series of values to process.

length (simple int) : Number of bars for the moving average calculation.

maType (simple MaType) : Type of moving average to calculate. Optional. Default is SMA.

Returns: (float) The calculated moving average value based on the specified type.

atr(length, maType)

Calculates the Average True Range (ATR) using the specified moving average type. Developed by J. Welles Wilder Jr.

Parameters:

length (simple int) : Number of bars for the ATR calculation.

maType (simple MaType) : Type of moving average to use for smoothing. Optional. Default is RMA.

Returns: (float) The calculated Average True Range value.

macd(source, fastLength, slowLength, signalLength, maType, signalMaType)

Calculates the Moving Average Convergence Divergence (MACD) with customizable MA types. Developed by Gerald Appel.

Parameters:

source (series float) : Series of values to process.

fastLength (simple int) : Period for the fast moving average.

slowLength (simple int) : Period for the slow moving average.

signalLength (simple int) : Period for the signal line moving average.

maType (simple MaType) : Type of moving average for main MACD calculation. Optional. Default is EMA.

signalMaType (simple MaType) : Type of moving average for signal line calculation. Optional. Default is EMA.

Returns: ( ) Tuple containing MACD line, signal line, and histogram values.

dmao(source, fastLength, slowLength, maType)

Calculates the Dual Moving Average Oscillator (DMAO) of a given data series. Uses the same algorithm as the Percentage Price Oscillator (PPO), but can be applied to any data series.

Parameters:

source (series float) : Series of values to process.

fastLength (simple int) : Period for the fast moving average.

slowLength (simple int) : Period for the slow moving average.

maType (simple MaType) : Type of moving average to use for both calculations. Optional. Default is EMA.

Returns: (float) The calculated Dual Moving Average Oscillator value as a percentage.

continuationIndex(source, length, gamma, order)

Calculates the Continuation Index of a given data series. The index represents the Inverse Fisher Transform of the normalized difference between an UltimateSmoother and an N-order Laguerre filter. Developed by John F. Ehlers, published in TASC 2025.09.

Parameters:

source (series float) : Series of values to process.

length (simple int) : The calculation length.

gamma (simple float) : Controls the phase response of the Laguerre filter. Optional. Default is 0.8.

order (simple int) : The order of the Laguerre filter (1-10). Optional. Default is 8.

Returns: (float) The calculated Continuation Index value.

📚 RELEASE NOTES

v1.0 (2025.09.24)

✅ 25+ technical analysis functions

✅ Complete adaptive moving average series (KAMA, FRAMA, MAMA/FAMA)

✅ Advanced signal processing filters (Kalman, Laguerre, SuperSmoother, UltimateSmoother)

✅ Performance optimized with pre-calculated constants and efficient algorithms

✅ Unified function interface design following TradingView best practices

✅ Comprehensive moving average collection (DEMA, TEMA, ZLEMA, T3, etc.)

✅ Volatility and trend detection tools (QQE, SSL Channel, Range Filter)

✅ Continuation Index - Latest research from TASC 2025.09

✅ MACD and ATR calculations supporting multiple moving average types

✅ Dual Moving Average Oscillator (DMAO) for arbitrary data series analysis

Hurst Momentum Oscillator | AlphaNattHurst Momentum Oscillator | AlphaNatt

An adaptive oscillator that combines the Hurst Exponent - which identifies whether markets are trending or mean-reverting - with momentum analysis to create signals that automatically adjust to market regime.

"The Hurst Exponent reveals a hidden truth: markets aren't always trending. This oscillator knows when to ride momentum and when to fade it."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📐 THE MATHEMATICS

Hurst Exponent (H):

Measures the long-term memory of time series:

H > 0.5: Trending (persistent) behavior

H = 0.5: Random walk

H < 0.5: Mean-reverting behavior

Originally developed for analyzing Nile river flooding patterns, now used in:

Fractal market analysis

Network traffic prediction

Climate modeling

Financial markets

The Innovation:

This oscillator multiplies momentum by the Hurst coefficient:

When trending (H > 0.5): Momentum is amplified

When mean-reverting (H < 0.5): Momentum is reduced

Result: Adaptive signals based on market regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 KEY ADVANTAGES

Regime Adaptive: Automatically adjusts to trending vs ranging markets

False Signal Reduction: Reduces momentum signals in mean-reverting markets

Trend Amplification: Stronger signals when trends are persistent

Mathematical Edge: Based on fractal dimension analysis

No Repainting: All calculations on historical data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING SIGNALS

Visual Interpretation:

Cyan zones: Bullish momentum in trending market

Magenta zones: Bearish momentum or mean reversion

Background tint: Blue = trending, Pink = mean-reverting

Gradient intensity: Signal strength

Trading Strategies:

1. Trend Following:

Trade momentum signals when background is blue (trending)

2. Mean Reversion:

Fade extreme readings when background is pink

3. Regime Transition:

Watch for background color changes as early warning

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 OPTIMAL USAGE

Best Conditions:

Strong trending markets (crypto bull runs)

Clear ranging markets (forex sessions)

Regime transitions

Multi-timeframe analysis

Market Applications:

Crypto: Excellent for identifying trend persistence

Forex: Detects when pairs are ranging

Stocks: Identifies momentum stocks

Commodities: Catches persistent trends

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Fractal Market Analysis

Version: 1.0

Classification: Adaptive Regime Oscillator

Not financial advice. Always DYOR.

Adaptive Convergence Divergence### Adaptive Convergence Divergence (ACD)

By Gurjit Singh

The Adaptive Convergence Divergence (ACD) reimagines the classic MACD by replacing fixed moving averages with adaptive moving averages. Instead of a static smoothing factor, it dynamically adjusts sensitivity based on price momentum, relative strength, volatility, fractal roughness, or volume pressure. This makes the oscillator more responsive in trending markets while filtering noise in choppy ranges.

#### 📌 Key Features

1. Dual Adaptive Structure: The oscillator uses two adaptive moving averages to form its convergence-divergence line, with EMA/RMA as signal line:

* Primary Adaptive (MA): Fast line, reacts quickly to changes.

* Following Adaptive (FAMA): Slow line, with half-alpha smoothing for confirmation.

2. Adaptive MA Types

* ACMO: Adaptive CMO (momentum)

* ARSI: Adaptive RSI (relative strength)

* FRMA: Fractal Roughness (volatility + fractal dimension)

* VOLA: Volume adaptive (volume pressure)

3. PPO Option: Switch between classic MACD or Percentage Price Oscillator (PPO) style calculation.

4. Signal Smoothing: Choose between EMA or Wilder’s RMA.

5. Visuals: Colored oscillator, signal line, histogram with adaptive transparency.

6. Alerts: Bullish/Bearish crossovers built-in.

#### 🔑 How to Use

1. Add to chart: Works on any timeframe and asset.

2. Choose MA Type: Experiment with ACMO, ARSI, FRMA, or VOLA depending on market regime.

3. Crossovers:

* Bullish (🐂): Oscillator crosses above signal → potential long entry.

* Bearish (🐻): Oscillator crosses below signal → potential short entry.

4. Histogram: expansion = strengthening trend; contraction = weakening trend.

5. Divergences:

* Bullish (hidden strength): Price pushes lower, but ACD turns higher = potential upward reversal.

* Bearish (hidden weakness): Price pushes higher, but ACD turns lower = potential downward reversal.

6. Customize: Adjust lengths, smoothing type, and PPO/MACD mode to match your style.

7. Set Alerts:

* Enable Bullish or Bearish crossover alerts to catch momentum shifts in real time.

#### 💡 Tips

* PPO mode normalizes values across assets, useful for cross-asset analysis.

* Wilder’s smoothing is gentler than EMA, reducing whipsaws in sideways conditions.

* Adaptive smoothing helps reduce false divergence signals by filtering noise in choppy ranges.

Up/Down Volume Delta %this script is based on FractalTrade_'s rendition of the up/down volume bars.

the shortcomings of that chart were that large volume bars caused the auto-scaling to shrink smaller volume bar displays to the point where much of the data was too small to see.

in this chart, the bars are displaying the percent delta out of the total bar volume. this way, large overall volume bars do not cause visual compression to everything else in the chart.

I've used color modulation to indicate relation to a relative volume point, so users can still tell when overall volume is large or small. when volume is under a moving average, the bars will display at a basis transparency. when the volume is over the average, the brightness will increase up to a specific ratio of volume defined by the user.

for example, if basis transparency is at 20, and the full opacity ratio is at 3, and the volume average is at 1M, a volume of 750k will display the delta bar at the basis transparency. a volume of 3M will achieve full brightness. a volume of 2M will display with moderate brightness (about 60%), but still stand out against other bars with basis transparency.

areas of the chart that are either increasing bar sizes or increasing in brightness can indicate directional force. when volume delta direction contradicts the candle direction, this can indicate support / resistance.

Multifractal Forecast [ScorsoneEnterprises]Multifractal Forecast Indicator

The Multifractal Forecast is an indicator designed to model and forecast asset price movements using a multifractal framework. It uses concepts from fractal geometry and stochastic processes, specifically the Multifractal Model of Asset Returns (MMAR) and fractional Brownian motion (fBm), to generate price forecasts based on historical price data. The indicator visualizes potential future price paths as colored lines, providing traders with a probabilistic view of price trends over a specified trading time scale. Below is a detailed breakdown of the indicator’s functionality, inputs, calculations, and visualization.

Overview

Purpose: The indicator forecasts future price movements by simulating multiple price paths based on a multifractal model, which accounts for the complex, non-linear behavior of financial markets.

Key Concepts:

Multifractal Model of Asset Returns (MMAR): Models price movements as a multifractal process, capturing varying degrees of volatility and self-similarity across different time scales.

Fractional Brownian Motion (fBm): A generalization of Brownian motion that incorporates long-range dependence and self-similarity, controlled by the Hurst exponent.

Binomial Cascade: Used to model trading time, introducing heterogeneity in time scales to reflect market activity bursts.

Hurst Exponent: Measures the degree of long-term memory in the price series (persistence, randomness, or mean-reversion).

Rescaled Range (R/S) Analysis: Estimates the Hurst exponent to quantify the fractal nature of the price series.

Inputs

The indicator allows users to customize its behavior through several input parameters, each influencing the multifractal model and forecast generation:

Maximum Lag (max_lag):

Type: Integer

Default: 50

Minimum: 5

Purpose: Determines the maximum lag used in the rescaled range (R/S) analysis to calculate the Hurst exponent. A higher lag increases the sample size for Hurst estimation but may smooth out short-term dynamics.

2 to the n values in the Multifractal Model (n):

Type: Integer

Default: 4

Purpose: Defines the resolution of the multifractal model by setting the size of arrays used in calculations (N = 2^n). For example, n=4 results in N=16 data points. Larger n increases computational complexity and detail but may exceed Pine Script’s array size limits (capped at 100,000).

Multiplier for Binomial Cascade (m):

Type: Float

Default: 0.8

Purpose: Controls the asymmetry in the binomial cascade, which models trading time. The multiplier m (and its complement 2.0 - m) determines how mass is distributed across time scales. Values closer to 1 create more balanced cascades, while values further from 1 introduce more variability.

Length Scale for fBm (L):

Type: Float

Default: 100,000.0

Purpose: Scales the fractional Brownian motion output, affecting the amplitude of simulated price paths. Larger values increase the magnitude of forecasted price movements.

Cumulative Sum (cum):

Type: Integer (0 or 1)

Default: 1

Purpose: Toggles whether the fBm output is cumulatively summed (1=On, 0=Off). When enabled, the fBm series is accumulated to simulate a price path with memory, resembling a random walk with long-range dependence.

Trading Time Scale (T):

Type: Integer

Default: 5

Purpose: Defines the forecast horizon in bars (20 bars into the future). It also scales the binomial cascade’s output to align with the desired trading time frame.

Number of Simulations (num_simulations):

Type: Integer

Default: 5

Minimum: 1

Purpose: Specifies how many forecast paths are simulated and plotted. More simulations provide a broader range of possible price outcomes but increase computational load.

Core Calculations

The indicator combines several mathematical and statistical techniques to generate price forecasts. Below is a step-by-step explanation of its calculations:

Log Returns (lgr):

The indicator calculates log returns as math.log(close / close ) when both the current and previous close prices are positive. This measures the relative price change in a logarithmic scale, which is standard for financial time series analysis to stabilize variance.

Hurst Exponent Estimation (get_hurst_exponent):

Purpose: Estimates the Hurst exponent (H) to quantify the degree of long-term memory in the price series.

Method: Uses rescaled range (R/S) analysis:

For each lag from 2 to max_lag, the function calc_rescaled_range computes the rescaled range:

Calculate the mean of the log returns over the lag period.

Compute the cumulative deviation from the mean.

Find the range (max - min) of the cumulative deviation.

Divide the range by the standard deviation of the log returns to get the rescaled range.

The log of the rescaled range (log(R/S)) is regressed against the log of the lag (log(lag)) using the polyfit_slope function.

The slope of this regression is the Hurst exponent (H).

Interpretation:

H = 0.5: Random walk (no memory, like standard Brownian motion).

H > 0.5: Persistent behavior (trends tend to continue).

H < 0.5: Mean-reverting behavior (price tends to revert to the mean).

Fractional Brownian Motion (get_fbm):

Purpose: Generates a fractional Brownian motion series to model price movements with long-range dependence.

Inputs: n (array size 2^n), H (Hurst exponent), L (length scale), cum (cumulative sum toggle).

Method:

Computes covariance for fBm using the formula: 0.5 * (|i+1|^(2H) - 2 * |i|^(2H) + |i-1|^(2H)).

Uses Hosking’s method (referenced from Columbia University’s implementation) to generate fBm:

Initializes arrays for covariance (cov), intermediate calculations (phi, psi), and output.

Iteratively computes the fBm series by incorporating a random term scaled by the variance (v) and covariance structure.

Applies scaling based on L / N^H to adjust the amplitude.

Optionally applies cumulative summation if cum = 1 to produce a path with memory.

Output: An array of 2^n values representing the fBm series.

Binomial Cascade (get_binomial_cascade):

Purpose: Models trading time (theta) to account for non-uniform market activity (e.g., bursts of volatility).

Inputs: n (array size 2^n), m (multiplier), T (trading time scale).

Method:

Initializes an array of size 2^n with values of 1.0.

Iteratively applies a binomial cascade:

For each block (from 0 to n-1), splits the array into segments.

Randomly assigns a multiplier (m or 2.0 - m) to each segment, redistributing mass.

Normalizes the array by dividing by its sum and scales by T.

Checks for array size limits to prevent Pine Script errors.

Output: An array (theta) representing the trading time, which warps the fBm to reflect market activity.

Interpolation (interpolate_fbm):

Purpose: Maps the fBm series to the trading time scale to produce a forecast.

Method:

Computes the cumulative sum of theta and normalizes it to .

Interpolates the fBm series linearly based on the normalized trading time.

Ensures the output aligns with the trading time scale (T).

Output: An array of interpolated fBm values representing log returns over the forecast horizon.

Price Path Generation:

For each simulation (up to num_simulations):

Generates an fBm series using get_fbm.

Interpolates it with the trading time (theta) using interpolate_fbm.

Converts log returns to price levels:

Starts with the current close price.

For each step i in the forecast horizon (T), computes the price as prev_price * exp(log_return).

Output: An array of price levels for each simulation.

Visualization:

Trigger: Updates every T bars when the bar state is confirmed (barstate.isconfirmed).

Process:

Clears previous lines from line_array.

For each simulation, plots a line from the current bar’s close price to the forecasted price at bar_index + T.

Colors the line using a gradient (color.from_gradient) based on the final forecasted price relative to the minimum and maximum forecasted prices across all simulations (red for lower prices, teal for higher prices).

Output: Multiple colored lines on the chart, each representing a possible price path over the next T bars.

How It Works on the Chart

Initialization: On each bar, the indicator calculates the Hurst exponent (H) using historical log returns and prepares the trading time (theta) using the binomial cascade.

Forecast Generation: Every T bars, it generates num_simulations price paths:

Each path starts at the current close price.

Uses fBm to model log returns, warped by the trading time.

Converts log returns to price levels.

Plotting: Draws lines from the current bar to the forecasted price T bars ahead, with colors indicating relative price levels.

Dynamic Updates: The forecast updates every T bars, replacing old lines with new ones based on the latest price data and calculations.

Key Features

Multifractal Modeling: Captures complex market dynamics by combining fBm (long-range dependence) with a binomial cascade (non-uniform time).

Customizable Parameters: Allows users to adjust the forecast horizon, model resolution, scaling, and number of simulations.

Probabilistic Forecast: Multiple simulations provide a range of possible price outcomes, helping traders assess uncertainty.

Visual Clarity: Gradient-colored lines make it easy to distinguish bullish (teal) and bearish (red) forecasts.

Potential Use Cases

Trend Analysis: Identify potential price trends or reversals based on the direction and spread of forecast lines.

Risk Assessment: Evaluate the range of possible price outcomes to gauge market uncertainty.

Volatility Analysis: The Hurst exponent and binomial cascade provide insights into market persistence and volatility clustering.

Limitations

Computational Intensity: Large values of n or num_simulations may slow down execution or hit Pine Script’s array size limits.

Randomness: The binomial cascade and fBm rely on random terms (math.random), which may lead to variability between runs.

Assumptions: The model assumes log-normal price movements and fractal behavior, which may not always hold in extreme market conditions.

Adjusting Inputs:

Set max_lag based on the desired depth of historical analysis.

Adjust n for model resolution (start with 4–6 to avoid performance issues).

Tune m to control trading time variability (0.5–1.5 is typical).

Set L to scale the forecast amplitude (experiment with values like 10,000–1,000,000).

Choose T based on your trading horizon (20 for short-term, 50 for longer-term for example).

Select num_simulations for the number of forecast paths (5–10 is reasonable for visualization).

Interpret Output:

Teal lines suggest bullish scenarios, red lines suggest bearish scenarios.

A wide spread of lines indicates high uncertainty; convergence suggests a stronger trend.

Monitor Updates: Forecasts update every T bars, so check the chart periodically for new projections.

Chart Examples

This is a daily AMEX:SPY chart with default settings. We see the simulations being done every T bars and they provide a range for us to analyze with a few simulations still in the range.

On this intraday PEPPERSTONE:COCOA chart I modified the Length Scale for fBm, L, parameter to be 1000 from 100000. Adjusting the parameter as you switch between timeframes can give you more contextual simulations.

On BITSTAMP:ETHUSD I modified the L to be 1000000 to have a more contextual set of simulations with crypto's volatile nature.

With L at 100000 we see the range for NASDAQ:TLT is correctly simulated. The recent pop stays within the bounds of the highest simulation. Note this is a cherry picked example to show the power and potential of these simulations.

Technical Notes