EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

Search in scripts for "alert"

Volumemetrix Variance StrategyThe “Volumemetrix Variance Strategy” is an advanced Pine Script strategy designed to identify trade entries and exits using a combination of volume profile analysis, candle structure, and volatility filters. It constructs a dynamic volume profile over a specified lookback period to identify critical price levels such as the Point of Control (PoC), Value Area High (VAH), and Value Area Low (VAL). These levels represent zones of high trading activity that often act as support and resistance. The script smooths and adjusts these levels across different timeframes to align short-term market structure with higher-timeframe trends. It incorporates a variety of filters to exclude doji candles, detect continuation or rejection patterns, and confirm alignment with higher timeframe candle direction (e.g., 4-hour bullish or bearish bias).

Trade logic is built around detecting crossovers and breakouts relative to the PoC and value areas. The system can trigger entries based on several configurable behaviors: breakout, retake, bounce, reversal, or rejection near key volume zones. It supports flexible entry conditions for long, short, or both sides of the market, as well as a range of customizable settings for time-based trading restrictions, end-of-day position closures, and alert-based data capture. For execution, the script includes integrated risk management—users can specify take-profit and stop-loss levels, enable moving (trailing) stops, and even apply a “power curve” model to dynamically adjust trailing stops using exponential decay logic that adapts to price progress.

Overall, the Volumemetrix Variance Strategy is a hybrid between a quantitative volume-based strategy and a volatility-adaptive trade manager. It combines fixed range volume profiling with multi-timeframe confirmation, candle pattern validation, and adaptive exit logic. Its architecture allows for detailed trade automation, alert generation for external systems, and real-time control over parameters such as ATR scaling, entry delay, or bar confirmation. The result is a high-granularity framework for both backtesting and live execution that seeks to capture statistically favorable setups around liquidity concentration zones.

MoneyPlant-Auto Support Resistance V2.0

🧭 Overview

MoneyPlant – Auto Support Resistance is a professional-grade indicator designed to automatically detect dynamic Support and Resistance levels using real-time market structure.

It combines trend confirmation, structure analysis, and momentum logic to identify high-probability trading zones in all market conditions.

⚙️ Core Concept

This indicator uses a unique combination of classic and proprietary logic to filter only the most relevant S/R levels:

• Dynamic Support/Resistance Mapping: Detects strong reaction levels based on price structure, candle rejection points, and breakout validation.

• EMA & WMA Trend Filter: Uses a triple-moving-average model (default EMA 18, EMA 25, and WMA 7) to confirm current market bias.

• MACD Momentum Filter: Confirms trend strength and helps avoid false breakouts.

• Smart Alignment Logic: Generates signals only when structure, trend, and momentum all align in the same direction.

🧠 How It Works

1. Buy Setup:

When price breaks above a resistance level with bullish EMA/WMA alignment and positive MACD momentum → Buy Signal triggers.

2. Sell Setup:

When price breaks below a support level with bearish EMA/WMA alignment and negative MACD momentum → Sell Signal triggers.

3. Auto-Refreshing Zones:

Support and Resistance zones update dynamically as market structure evolves.

🎯 Best Use Cases

• Works effectively on Stocks, Indices, Forex, and Commodities (e.g., XAUUSD, NIFTY, BANKNIFTY ).

• Ideal for Intraday & Swing Trading (15 min – 1 hour timeframes).

• Fully compatible with TradingView alerts and automation tools.

💡 Key Features

✅ Automatic Support/Resistance detection

✅ Adaptive EMA + WMA + MACD trend logic

✅ Real-time Buy/Sell alerts

✅ Multi-timeframe compatibility

✅ Optimized for clean chart visuals

⚖️ Recommended Settings

• EMA Fast: 18

• EMA Slow: 25

• WMA Filter: 7

• MACD: Default parameters

(Users may adjust EMA/WMA settings according to their own trading style.)

🔒 How to Get Access

To get access to this invite-only script, please send me a private message on TradingView or use the link in my profile.

Once your username is added via Manage Access, you’ll be able to use the indicator.

🧾 Notes for Traders

This tool does not repaint, and it’s meant for educational and analytical purposes only.

Each license is valid for one TradingView username — no resale or redistribution is permitted.

Developed by MoneyPlant

Smart Automation for Professional Traders

DayFlow VWAP Relay Forex Majors StrategySummary in one paragraph

DayFlow VWAP Relay is a day-trading strategy for major FX pairs on intraday timeframes, demonstrated on EURUSD 15 minutes. It waits for alignment between a daily anchored VWAP regime check, residual percentiles, and lower-timeframe micro flow before suggesting trades. The originality is the fusion of daily VWAP residual percentiles with a live micro-flow score from 1 minute data to switch between fade and breakout behavior inside the same session. Add it to a clean chart and use the markers and alerts.

Scope and intent

• Markets: Major FX pairs such as EURUSD, GBPUSD, USDJPY, AUDUSD, USDCHF, USDCAD

• Timeframes: One minute to one hour

• Default demo in this publication: EURUSD on 15 minutes

• Purpose: Reduce false starts by acting only when context, location and micro flow agree

• Limits: This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Core novelty: Residual percentiles to daily anchored VWAP decide “balanced versus expanding day”. A separate 1 minute micro-flow score confirms direction, so the same model fades extremes in balance and rides range breaks in expansion

• Failure modes addressed: Chop fakeouts and unconfirmed breakouts are filtered by the expansion gate and micro-flow threshold

• Testability: Every input is exposed. Bands, background regime color, and markers show why a suggestion appears

• Portable yardstick: Stops and targets are ATR multiples converted to ticks, which transfer across symbols

• Open source status: No reused third-party code that requires attribution

Method overview in plain language

The day is anchored with a VWAP that updates from the daily session start. Price minus VWAP is the residual. Percentiles of that residual measured over a rolling window define location extremes for the current day. A regime score compares residual volatility to price volatility. When expansion is low, the day is treated as balanced and the model fades residual extremes if 1 minute micro flow points back to VWAP. When expansion is high, the model trades breakouts outside the VWAP bands if slope and micro flow agree with the move.

Base measures

• Range basis: True Range smoothed by ATR for stops and targets, length 14

• Return basis: Not required for signals; residuals are absolute price distance to VWAP

Components

• Daily Anchor VWAP Bands. VWAP with standard-deviation bands. Slope sign is used for trend confirmation on breakouts

• Residual Percentiles. Rolling percentiles of close minus VWAP over Signal length. Identify location extremes inside the day

• Expansion Ratio. Standard deviation of residuals divided by standard deviation of price over Signal length. Classifies balanced versus expanding day

• Micro Flow. Net up minus down closes from 1 minute data across a short span, normalized to −1..+1. Confirms direction and avoids fades against pressure

• Session Window optional. Restricts trading to your configured hours to avoid thin periods

• Cooldown optional. Bars to wait after a position closes to prevent immediate re-entry

Fusion rule

Gating rather than weighting. First choose regime by Expansion Ratio versus the Expansion gate. Inside each regime all listed conditions must be true: location test plus micro-flow threshold plus session window plus cooldown. Breakouts also require VWAP slope alignment.

Signal rule

• Long suggestion on balanced day: residual at or below the lower percentile and micro flow positive above the gate while inside session and cooldown is satisfied

• Short suggestion on balanced day: residual at or above the upper percentile and micro flow negative below the gate while inside session and cooldown is satisfied

• Long suggestion on expanding day: close above the upper VWAP band, VWAP slope positive, micro flow positive, session and cooldown satisfied

• Short suggestion on expanding day: close below the lower VWAP band, VWAP slope negative, micro flow negative, session and cooldown satisfied

• Positions flip on opposite suggestions or exit by brackets

What you will see on the chart

• Markers on suggestion bars: L for long, S for short

• Exit occurs on reverse signal or when a bracket order is filled

• Reference lines: daily anchored VWAP with upper and lower bands

• Optional background: teal for balanced day, orange for expanding day

Inputs with guidance

Setup

• Signal length. Residual and regime window. Typical 40 to 100. Higher smooths, lower reacts faster

Micro Flow

• Micro TF. Lower timeframe used for micro flow, default 1 minute

• Micro span bars. Count of lower-TF bars. Typical 5 to 20

• Micro flow gate 0..1. Minimum absolute flow. Raising it demands stronger confirmation and reduces trade count

VWAP Bands

• VWAP stdev multiplier. Band width. Typical 0.8 to 1.6. Wider bands reduce breakout frequency and increase fade distance

• Expansion gate 0..3. Threshold to switch from fades to breakouts. Raising it favors fades, lowering it favors breakouts

Sessions

• Use session filter. Enable to trade only inside your window

• Trade window UTC. Default 07:00 to 17:00

Risk

• ATR length. Stop and target basis. Typical 10 to 21

• Stop ATR x. Initial stop distance in ATR multiples

• Target ATR x. Profit target distance in ATR multiples

• Cooldown bars after close. Wait bars before a new entry

• Side. Both, long only, or short only

View

• Show VWAP and bands

• Color bars by residual regime

Properties visible in this publication

• Initial capital 10000

• Base currency Default

• request.security uses lookahead off everywhere

• Strategy: Percent of equity with value 3. Pyramiding 0. Commission cash per order 0.0001 USD. Slippage 3 ticks. Process orders on close ON. Bar magnifier ON. Recalculate after order is filled OFF. Calc on every tick OFF. Using standard OHLC fills ON.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategies must run on standard candles for signals and orders.

Honest limitations and failure modes

High impact news, session opens, and thin liquidity can invalidate assumptions. Very quiet days can reduce contrast between residuals and price volatility. Session windows use the chart exchange time. If both stop and target are touched within a single bar, TradingView’s standard OHLC price-movement model decides the outcome.

Expect different behavior on illiquid pairs or during holidays. The model is sensitive to session definitions and feed time. Past results never guarantee future outcomes.

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Fury by Tetrad Fury by Tetrad

What it is:

A rules-based Bollinger+RSI strategy that fades extremes: it looks for price stretching beyond Bollinger Bands while RSI confirms exhaustion, enters countertrend, then exits at predefined profit multipliers or optional stoploss. “Ultra Glow” visuals are purely cosmetic.

How it works — logic at a glance

Framework: Classic Bollinger Bands (SMA basis; configurable length & multiplier) + RSI (configurable length).

Long entries:

Price closes below the lower band and RSI < Long RSI threshold (default 28.3) → open LONG (subject to your “Market Direction” setting).

Short entries:

Price closes above the upper band and RSI > Short RSI threshold (default 88.4) → open SHORT.

Profit exits (price targets):

Uses simple multipliers of the strategy’s average entry price:

Long exit = `entry × Long Exit Multiplier` (default 1.14).

Short exit = `entry × Short Exit Multiplier` (default 0.915).

Risk controls:

Optional pricebased stoploss (disabled by default) via:

Long stop = `entry × Long Stop Factor` (default 0.73).

Short stop = `entry × Short Stop Factor` (default 1.05).

Directional filter:

“Market Direction” input lets you constrain entries to Market Neutral, Long Only, or Short Only.

Visuals:

“Ultra Glow” draws thin layered bands around upper/basis/lower; these do not affect signals.

> Note: Inputs exist for a timebased stop tracker in code, but this version exits via targets and (optional) price stop only.

Why it’s different / original

Explicit extreme + momentum pairing: Entries require simultaneous band breach and RSI exhaustion, aiming to avoid entries on gardenvariety volatility pokes.

Deterministic exits: Multiplier-based targets keep results auditable and reproducible across datasets and assets.

Minimal, unobtrusive visuals: Thin, layered glow preserves chart readability while communicating regime around the Bollinger structure.

Inputs you can tune

Bollinger: Length (default 205), Multiplier (default 2.2).

RSI: Length (default 23), Long/Short thresholds (28.3 / 88.4).

Targets: Long Exit Mult (1.14), Short Exit Mult (0.915).

Stops (optional): Enable/disable; Long/Short Stop Factors (0.73 / 1.05).

Market Direction: Market Neutral / Long Only / Short Only.

Visuals: Ultra Glow on/off, light bar tint, trade labels on/off.

How to use it

1. Timeframe & assets: Works on any symbol/timeframe; start with liquid majors and 60m–1D to establish baseline behavior, then adapt.

2. Calibrate thresholds:

Narrow/meanreverting markets often tolerate tighter RSI thresholds.

Fast/volatile markets may need wider RSI thresholds and stronger stop factors.

3. Pick realistic targets: The default multipliers are illustrative; tune them to reflect typical mean reversion distance for your instrument/timeframe (e.g., ATRinformed profiling).

4. Risk: If enabling stops, size positions so risk per trade ≤ 1–2% of equity (max 5–10% is a commonly cited upper bound).

5. Mode: Use Long Only or Short Only when your discretionary bias or higher timeframe model favors one side; otherwise Market Neutral.

Recommended publication properties (for backtests that don’t mislead)

When you publish, set your strategy’s Properties to realistic values and keep them consistent with this description:

Initial capital: 10,000 (typical retail baseline).

Commission: ≥ 0.05% (adjust for your venue).

Slippage: ≥ 2–3 ticks (or a conservative pertrade value).

Position sizing: Avoid risking > 5–10% equity per trade; fixedfractional sizing ≤ 10% or fixedcash sizing is recommended.

Dataset / sample size: Prefer symbols/timeframes yielding 100+ trades over the tested period for statistical relevance. If you deviate, say why.

> If you choose different defaults (e.g., capital, commission, slippage, sizing), explain and justify them here, and use the same settings in your publication.

Interpreting results & limitations

This is a countertrend approach; it can struggle in strong trends where band breaches compound.

Parameter sensitivity is real: thresholds and multipliers materially change trade frequency and expectancy.

No predictive claims: Past performance is not indicative of future results. The future is unknowable; treat outputs as decision support, not guarantees.

Suggested validation workflow

Try different assets. (TSLA, AAPL, BTC, SOL, XRP)

Run a walkforward across multiple years and market regimes.

Test several timeframes and multiple instruments. (30m Suggested)

Compare different commission/slippage assumptions.

Inspect distribution of returns, max drawdown, win/loss expectancy, and exposure.

Confirm behavior during trend vs. range segments.

Alerts & automation

This release focuses on chart execution and visualization. If you plan to automate, create alerts at your entry/exit conditions and ensure your broker/venue fills reflect your slippage/fees assumptions.

Disclaimer

This script is provided for educational and research purposes. It is not investment advice. Trading involves risk, including the possible loss of principal. © Tetrad Protocol.

Camarilla Pivots + 20 EMA StrategyThis is an intraday volatility and trend-following system for commodities like Natural Gas, combining dynamic pivot levels (Camarilla) with a trend filter (20-period EMA) to improve risk-reward and reduce false breakouts.

Core Components

1. Camarilla Pivots:

These are special support and resistance levels (H3, H4, L3, L4) calculated each day based on the previous day's high, low, and close.

The pivots adapt to daily volatility, giving more relevant breakout and bounce zones than static lines.

H4: Aggressive resistance (used for breakout LONG entry)

H3: Moderate resistance/support (used for bounce or stoploss)

L4: Aggressive support (used for breakout SHORT entry)

L3: Moderate support/resistance (used for bounce or stoploss)

2. 20 EMA (Exponential Moving Average):

Plotted on the 30-minute chart, this acts as a trend filter.

If the price is above 20 EMA: Only look for long trades (bullish bias).

If below 20 EMA: Only look for short trades (bearish bias).

How the Strategy Works

Setup (30-Min Chart):

Camarilla pivots for the day are drawn on the chart.

20 EMA is also plotted.

Trade Filter:

Bullish: Trade ONLY if price is above 20 EMA.

Bearish: Trade ONLY if price is below 20 EMA.

Entry:

LONG: Enter when price breaks and closes above the H4 pivot AND is above 20 EMA.

SHORT: Enter when price breaks and closes below the L4 pivot AND is below 20 EMA.

Stop Loss:

LONG: Place stoploss at H3 (the next lower Camarilla resistance).

SHORT: Place stoploss at L3 (the next higher Camarilla support).

Target:

Always set a profit target at 2x the distance (risk) between entry and stoploss (strict R:R 2).

For example, if your entry is at H4 and stoploss at H3, your target is entry + 2*(entry - stoploss).

Alerts & Visuals:

The strategy plots entry arrows, stoploss and target lines for immediate visual reference.

Alerts trigger on breakout signals so you never miss a trade.

Why This Works Well for Natural Gas

Adapts to volatility: The pivots change daily, handling wide-ranging and choppy price moves better than fixed breakouts.

Trend filter: EMA prevents counter-trend whipsaws, only trades with market momentum.

Risk control: Every trade must meet strict risk-reward criteria, so losses are contained and winners can outweigh losers.

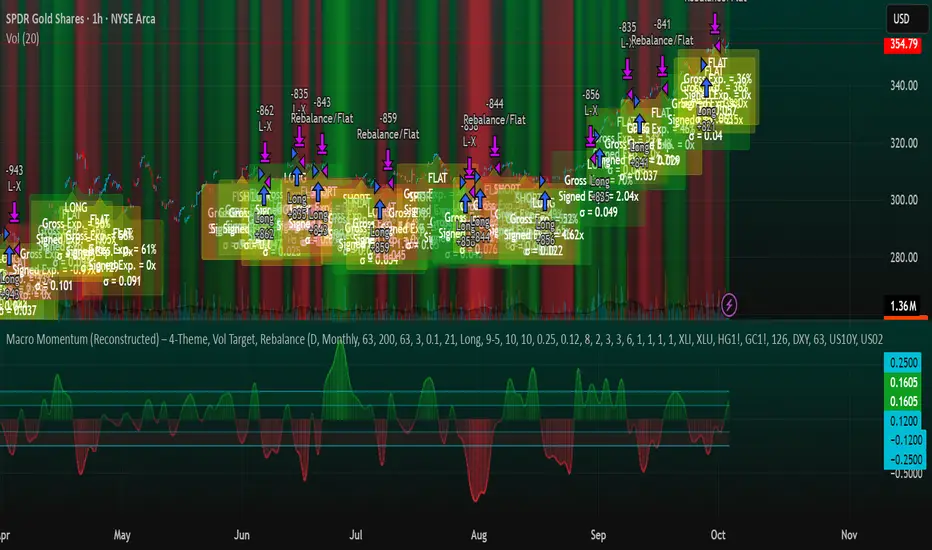

Macro Momentum – 4-Theme, Vol Target, RebalanceMacro Momentum — 4-Theme, Vol Target, Rebalance

Purpose. A macro-aware strategy that blends four economic “themes”—Business Cycle, Trade/USD, Monetary Policy, and Risk Sentiment—into a single, smoothed Composite signal. It then:

gates entries/exits with hysteresis bands,

enforces optional regime filters (200-day bias), and

sizes the position via volatility targeting with caps for long/short exposure.

It’s designed to run on any chart (index, ETF, futures, single stocks) while reading external macro proxies on a chosen Signal Timeframe.

How it works (high level)

Build four theme signals from robust macro proxies:

Business Cycle: XLI/XLU and Copper/Gold momentum, confirmed by the chart’s price vs a long SMA (default 200D).

Trade / USD: DXY momentum (sign-flipped so a rising USD is bearish for risk assets).

Monetary Policy: 10Y–2Y curve slope momentum and 10Y yield trend (steepening & falling 10Y = risk-on; rising 10Y = risk-off).

Risk Sentiment: VIX momentum (bearish if higher) and HYG/IEF momentum (bullish if credit outperforms duration).

Normalize & de-noise.

Optional Winsorization (MAD or stdev) clamps outliers over a lookback window.

Optional Z-score → tanh mapping compresses to ~ for stable weighting.

Theme lines are SMA-smoothed; the final Composite is LSMA-smoothed (linreg).

Decide direction with hysteresis.

Enter/hold long when Composite ≥ Entry Band; enter/hold short when Composite ≤ −Entry Band.

Exit bands are tighter than entry bands to avoid whipsaws.

Apply regime & direction constraints.

Optional Long-only above 200MA (chart symbol) and/or Short-only below 200MA.

Global Direction control (Long / Short / Both) and Invert switch.

Size via volatility targeting.

Realized close-to-close vol is annualized (choose 9-5 or 24/7 market profile).

Target exposure = TargetVol / RealizedVol, capped by Max Long/Max Short multipliers.

Quantity is computed from equity; futures are rounded to whole contracts.

Rebalance cadence & execution.

Trades are placed on Weekly / Monthly / Quarterly rebalance bars or when the sign of exposure flips.

Optional ATR stop/TP for single-stock style risk management.

Inputs you’ll actually tweak

General

Signal Timeframe: Where macro is sampled (e.g., D/W).

Rebalance Frequency: Weekly / Monthly / Quarterly.

ROC & SMA lengths: Defaults for theme momentum and the 200D regime filter.

Normalization: Z-score (tanh) on/off.

Winsorization

Toggle, lookback, multiplier, MAD vs Stdev.

Risk / Sizing

Target Annualized Vol & Realized Vol Lookback.

Direction (Long/Short/Both) and Invert.

Max long/short exposure caps.

Advanced Thresholds

Theme/Composite smoothing lengths.

Entry/Exit bands (hysteresis).

Regime / Execution

Long-only above 200MA, Short-only below 200MA.

Stops/TP (optional)

ATR length and SL/TP multiples.

Theme Weights

Per-theme scalars so you can push/pull emphasis (e.g., overweight Policy during rate cycles).

Macro Proxies

Symbols for each theme (XLI, XLU, HG1!, GC1!, DXY, US10Y, US02Y, VIX, HYG, IEF). Swap to alternatives as needed (e.g., UUP for DXY).

Signals & logic (under the hood)

Business Cycle = ½ ROC(XLI/XLU) + ½ ROC(Copper/Gold), then confirmed by (price > 200SMA ? +1 : −1).

Trade / USD = −ROC(DXY).

Monetary Policy = 0.6·ROC(10Y–2Y) − 0.4·ROC(10Y).

Risk Sentiment = −0.6·ROC(VIX) + 0.4·ROC(HYG/IEF).

Each theme → (optional Winsor) → (robust z or scaled ROC) → tanh → SMA smoothing.

Composite = weighted average → LSMA smoothing → compare to bands → dir ∈ {−1,0,+1}.

Rebalance & flips. Orders fire on your chosen cadence or when the sign of exposure changes.

Position size. exposure = clamp(TargetVol / realizedVol, maxLong/Short) × dir.

Note: The script also exposes Gross Exposure (% equity) and Signed Exposure (× equity) as diagnostics. These can help you audit how vol-targeting and caps translate into sizing over time.

Visuals & alerts

Composite line + columns (color/intensity reflect direction & strength).

Entry/Exit bands with green/red fills for quick polarity reads.

Hidden plots for each Theme if you want to show them.

Optional rebalance labels (direction, gross & signed exposure, σ).

Background heatmap keyed to Composite.

Alerts

Enter/Inc LONG when Composite crosses up (and on rebalance bars).

Enter/Inc SHORT when Composite crosses down (and on rebalance bars).

Exit to FLAT when Composite returns toward neutral (and on rebalance bars).

Practical tips

Start higher timeframes. Daily signals with Monthly rebalance are a good baseline; weekly signals with quarterly rebalances are even cleaner.

Tune Entry/Exit bands before anything else. Wider bands = fewer trades and less noise.

Weights reflect regime. If policy dominates markets, raise Monetary Policy weight; if credit stress drives moves, raise Risk Sentiment.

Proxies are swappable. Use UUP for USD, or futures-continuous symbols that match your data plan.

Futures vs ETFs. Quantity auto-rounds for futures; ETFs accept fractional shares. Check contract multipliers when interpreting exposure.

Caveats

Macro proxies can repaint at the selected signal timeframe as higher-TF bars form; that’s intentional for macro sampling, but test live.

Vol targeting assumes reasonably stationary realized vol over the lookback; if markets regime-shift, revisit volLook and targetVol.

If you disable normalization/winsorization, themes can become spikier; expect more hysteresis band crossings.

What to change first (quick start)

Set Signal Timeframe = D, Rebalance = Monthly, Z-score on, Winsor on (MAD).

Entry/Exit bands: 0.25 / 0.12 (defaults), then nudge until trade count and turnover feel right.

TargetVol: try 10% for diversified indices; lower for single stocks, higher for vol-sell strategies.

Leave weights = 1.0 until you’ve inspected the four theme lines; then tilt deliberately.

NQ Opening Range BreakoutOpening Range Breakout script with:

Customizable opening range timeframe selection.

Inputs for Risk to Reward ratio, EMAs, Vwap, and ATR sizing to avoid ranges that are too big or too small.

Features a toggle for reversal trades that when enabled will trade the other direction if the initial ORB gets stopped out.

Default it will use the entire opening range to determine stop loss and take profit and if neither the take profit or stop loss is hit it will end the trade at 16:00. There are toggles to use half the opening range as the stop loss and take profit will then be calculated as risk reward ratio * stop loss or you can select entry candle stop loss and risk reward ratio which places the stop loss at the entry candles opening price. There is also a take profit option that will only exit the trade when price closes below (for longs) or above (for shorts) a customizable ema length.

Note that if you have the opening range, for example, selected as 9:30 - 9:45 and are on a 5 minute chart it will enter on the first 5 min closure outside of that range and if you are on a 15 minute chart it will enter on the first 15 min closure outside of that range and so on.

You can automate the entries and exits by using a webhook service and using the strategy’s alerts.

Weekend Hunter Ultimate v6.2 Weekend Hunter Ultimate v6.2 - Automated Crypto Weekend Trading System

OVERVIEW:

Specialized trading strategy designed for cryptocurrency weekend markets (Saturday-Sunday) when institutional traders are typically offline and market dynamics differ significantly from weekdays. Optimized for 15-minute timeframe execution with multi-timeframe confluence analysis.

KEY FEATURES:

- Weekend-Only Trading: Automatically activates during configurable weekend hours

- Dynamic Leverage: 5-20x leverage adjusted based on market safety and signal confidence

- Multi-Timeframe Analysis: Combines 4H trend, 1H momentum, and 15M execution

- 10 Pre-configured Crypto Pairs: BTC, ETH, LINK, XRP, DOGE, SOL, AVAX, PEPE, TON, POL

- Position & Risk Management: Max 4 concurrent positions, -30% account protection

- Smart Trailing Stops: Protects profits when approaching targets

RISK MANAGEMENT:

- Maximum daily loss: 5% (configurable)

- Maximum weekend loss: 15% (configurable)

- Per-position risk: Capped at 120-156 USDT

- Emergency stops for flash crashes (8% moves)

- Consecutive loss protection (4 losses = pause)

TECHNICAL INDICATORS:

- CVD (Cumulative Volume Delta) divergence detection

- ATR-based dynamic stop loss and take profit

- RSI, MACD, Bollinger Bands confluence

- Volume surge confirmation (1.5x average)

- Weekend liquidity adjustments

INTEGRATION:

- Designed for Bybit Futures (0.075% taker fee)

- WunderTrading webhook compatibility via JSON alerts

- Minimum position size: 120 USDT (Bybit requirement)

- Initial capital: $500 recommended

TARGET METRICS:

- Win rate target: 65%

- Average win: 5.5%

- Average loss: 1.8%

- Risk-reward ratio: ~3:1

IMPORTANT DISCLAIMERS:

- Past performance does not guarantee future results

- Leveraged trading carries substantial risk of loss

- Weekend crypto markets have 13% of normal liquidity

- Not suitable for traders who cannot afford to lose their entire investment

- Requires continuous monitoring and adjustment

USAGE:

1. Apply to 15-minute charts only

2. Configure weekend hours for your timezone

3. Set up webhook alerts for automation

4. Monitor performance table in top-right corner

5. Adjust parameters based on your risk tolerance

This is an experimental strategy for educational purposes. Always test with small amounts first and never invest more than you can afford to lose completely.

Killzones SMT + IFVG detectorKillzones SMT + IFVG Detector

Summary

This strategy implements a specific intraday workflow inspired by ICT-style concepts.

It combines:

Killzone session levels (recording untouched highs/lows)

SMT divergence between NQ and ES (exclusive sweep logic)

IFVG confirmation (3-bar imbalance + width filter + inversion guard)

and an optional smart exit engine

The components are not simply mashed together: they interact in sequence.

A setup only confirms if all conditions line up (time window → untouched level sweep → divergence → valid IFVG → confirmation candle → risk filter).

Workflow

Killzones & session levels

Tracks highs/lows inside default killzones (19:00–23:00, 01:00–04:00, 08:30–10:00, 11:00–12:00, 12:30–15:00, chart timezone).

Stores untouched levels forward; sweeps trigger candidate signals.

SMT divergence (exclusive sweep)

Bullish SMT : one index sweeps its low while the other remains above its session low.

Bearish SMT : one index sweeps its high while the other remains below its session high.

Detection supports “Sweep (Cross)” or “Exact Tick.”

Session IDs are tracked so once a side has fired, later re-touches can’t re-trigger .

IFVG confirmation

Locks the first valid 3-bar IFVG after SMT.

Confirmation requires a candle close beyond the IFVG boundary in the direction of the close.

IFVGs must meet a minimum width filter (default 1.0 point).

Inversion guard: ignores IFVGs already inverted before SMT.

Optional “re-lock” keeps tracking the latest IFVG until confirmation/expiry.

Smart exit engine

Initial stop from opposite wick (+ buffer).

Fixed TP (default 40 points).

Dynamic stop escalation at progress thresholds (BE → 50% → 80% of target).

Safety gates

Weekend lockout (Fri 16:40 → Sun 18:00).

Same-bar sweep of high & low cancels setups.

Max initial stop filter skips oversized setups.

Optional cooldown bars.

Alerts

SMT Bullish/Bearish : divergence detected this bar.

Confirm Long/Short : IFVG confirmation triggered.

Default Strategy Properties (used in screenshots/backtests)

Initial capital: $25,000

Order size: 1 contract

Commission: $1.25 per contract per side

Slippage: 2 ticks

Backtest window: Jun 16, 2025 – Sep 14, 2025

These settings are intentionally conservative. If you change them, your results will differ.

How to use

Apply on an NQ or ES futures chart (1–5 min).

Choose your killzones and detection mode.

Select confirmation symbol (NQ, ES, or “Sweeper”).

Enable/disable IFVG re-lock.

Review signals and use alerts for automation if desired.

Limitations

Strict filters reduce trade count; extend backtest window for more samples.

Works best on NQ/ES; not validated elsewhere.

Past performance is not indicative of future results.

This is an educational tool ; not financial advice.

Universal Webhook Connector Demo.This strategy demonstrates how to generate JSON alerts from TradingView for multiple trading platforms.

Users can select platform_name (MT5, TradeLocker, DxTrade, cTrader, etc).

Alerts are constructed in JSON format for webhook execution.

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

Mutanabby_AI | Algo Pro Strategy# Mutanabby_AI | Algo Pro Strategy: Advanced Candlestick Pattern Trading System

## Strategy Overview

The Mutanabby_AI Algo Pro Strategy represents a systematic approach to automated trading based on advanced candlestick pattern recognition and multi-layered technical filtering. This strategy transforms traditional engulfing pattern analysis into a comprehensive trading system with sophisticated risk management and flexible position sizing capabilities.

The strategy operates on a long-only basis, entering positions when bullish engulfing patterns meet specific technical criteria and exiting when bearish engulfing patterns indicate potential trend reversals. The system incorporates multiple confirmation layers to enhance signal reliability while providing comprehensive customization options for different trading approaches and risk management preferences.

## Core Algorithm Architecture

The strategy foundation relies on bullish and bearish engulfing candlestick pattern recognition enhanced through technical analysis filtering mechanisms. Entry signals require simultaneous satisfaction of four distinct criteria: confirmed bullish engulfing pattern formation, candle stability analysis indicating decisive price action, RSI momentum confirmation below specified thresholds, and price decline verification over adjustable lookback periods.

The candle stability index measures the ratio between candlestick body size and total range including wicks, ensuring only well-formed patterns with clear directional conviction generate trading signals. This filtering mechanism eliminates indecisive market conditions where pattern reliability diminishes significantly.

RSI integration provides momentum confirmation by requiring oversold conditions before entry signal generation, ensuring alignment between pattern formation and underlying momentum characteristics. The RSI threshold remains fully adjustable to accommodate different market conditions and volatility environments.

Price decline verification examines whether current prices have decreased over a specified period, confirming that bullish engulfing patterns occur after meaningful downward movement rather than during sideways consolidation phases. This requirement enhances the probability of successful reversal pattern completion.

## Advanced Position Management System

The strategy incorporates dual position sizing methodologies to accommodate different account sizes and risk management approaches. Percentage-based position sizing calculates trade quantities as equity percentages, enabling consistent risk exposure across varying account balances and market conditions. This approach proves particularly valuable for systematic trading approaches and portfolio management applications.

Fixed quantity sizing provides precise control over trade sizes independent of account equity fluctuations, offering predictable position management for specific trading strategies or when implementing precise risk allocation models. The system enables seamless switching between sizing methods through simple configuration adjustments.

Position quantity calculations integrate seamlessly with TradingView's strategy testing framework, ensuring accurate backtesting results and realistic performance evaluation across different market conditions and time periods. The implementation maintains consistency between historical testing and live trading applications.

## Comprehensive Risk Management Framework

The strategy features dual stop loss methodologies addressing different risk management philosophies and market analysis approaches. Entry price-based stop losses calculate stop levels as fixed percentages below entry prices, providing predictable risk exposure and consistent risk-reward ratio maintenance across all trades.

The percentage-based stop loss system enables precise risk control by limiting maximum loss per trade to predetermined levels regardless of market volatility or entry timing. This approach proves essential for systematic trading strategies requiring consistent risk parameters and capital preservation during adverse market conditions.

Lowest low-based stop losses identify recent price support levels by analyzing minimum prices over adjustable lookback periods, placing stops below these technical levels with additional buffer percentages. This methodology aligns stop placement with market structure rather than arbitrary percentage calculations, potentially improving stop loss effectiveness during normal market fluctuations.

The lookback period adjustment enables optimization for different timeframes and market characteristics, with shorter periods providing tighter stops for active trading and longer periods offering broader stops suitable for position trading approaches. Buffer percentage additions ensure stops remain below obvious support levels where other market participants might place similar orders.

## Visual Customization and Interface Design

The strategy provides comprehensive visual customization through eight predefined color schemes designed for different chart backgrounds and personal preferences. Color scheme options include Classic bright green and red combinations, Ocean themes featuring blue and orange contrasts, Sunset combinations using gold and crimson, and Neon schemes providing high visibility through bright color selections.

Professional color schemes such as Forest, Royal, and Fire themes offer sophisticated alternatives suitable for business presentations and professional trading environments. The Custom color scheme enables precise color selection through individual color picker controls, maintaining maximum flexibility for specific visual requirements.

Label styling options accommodate different chart analysis preferences through text bubble, triangle, and arrow display formats. Size adjustments range from tiny through huge settings, ensuring appropriate visual scaling across different screen resolutions and chart configurations. Text color customization maintains readability across various chart themes and background selections.

## Signal Quality Enhancement Features

The strategy incorporates signal filtering mechanisms designed to eliminate repetitive signal generation during choppy market conditions. The disable repeating signals option prevents consecutive identical signals until opposing conditions occur, reducing overtrading during consolidation phases and improving overall signal quality.

Signal confirmation requirements ensure all technical criteria align before trade execution, reducing false signal occurrence while maintaining reasonable trading frequency for active strategies. The multi-layered approach balances signal quality against opportunity frequency through adjustable parameter optimization.

Entry and exit visualization provides clear trade identification through customizable labels positioned at relevant price levels. Stop loss visualization displays active risk levels through colored line plots, ensuring complete transparency regarding current risk management parameters during live trading operations.

## Implementation Guidelines and Optimization

The strategy performs effectively across multiple timeframes with optimal results typically occurring on intermediate timeframes ranging from fifteen minutes through four hours. Higher timeframes provide more reliable pattern formation and reduced false signal occurrence, while lower timeframes increase trading frequency at the expense of some signal reliability.

Parameter optimization should focus on RSI threshold adjustments based on market volatility characteristics and candlestick pattern timeframe analysis. Higher RSI thresholds generate fewer but potentially higher quality signals, while lower thresholds increase signal frequency with corresponding reliability considerations.

Stop loss method selection depends on trading style preferences and market analysis philosophy. Entry price-based stops suit systematic approaches requiring consistent risk parameters, while lowest low-based stops align with technical analysis methodologies emphasizing market structure recognition.

## Performance Considerations and Risk Disclosure

The strategy operates exclusively on long positions, making it unsuitable for bear market conditions or extended downtrend periods. Users should consider market environment analysis and broader trend assessment before implementing the strategy during adverse market conditions.

Candlestick pattern reliability varies significantly across different market conditions, with higher reliability typically occurring during trending markets compared to ranging or volatile conditions. Strategy performance may deteriorate during periods of reduced pattern effectiveness or increased market noise.

Risk management through stop loss implementation remains essential for capital preservation during adverse market movements. The strategy does not guarantee profitable outcomes and requires proper position sizing and risk management to prevent significant capital loss during unfavorable trading periods.

## Technical Specifications

The strategy utilizes standard TradingView Pine Script functions ensuring compatibility across all supported instruments and timeframes. Default configuration employs 14-period RSI calculations, adjustable candle stability thresholds, and customizable price decline verification periods optimized for general market conditions.

Initial capital settings default to $10,000 with percentage-based equity allocation, though users can adjust these parameters based on account size and risk tolerance requirements. The strategy maintains detailed trade logs and performance metrics through TradingView's integrated backtesting framework.

Alert integration enables real-time notification of entry and exit signals, stop loss executions, and other significant trading events. The comprehensive alert system supports automated trading applications and manual trade management approaches through detailed signal information provision.

## Conclusion

The Mutanabby_AI Algo Pro Strategy provides a systematic framework for candlestick pattern trading with comprehensive risk management and position sizing flexibility. The strategy's strength lies in its multi-layered confirmation approach and sophisticated customization options, enabling adaptation to various trading styles and market conditions.

Successful implementation requires understanding of candlestick pattern analysis principles and appropriate parameter optimization for specific market characteristics. The strategy serves traders seeking automated execution of proven technical analysis techniques while maintaining comprehensive control over risk management and position sizing methodologies.

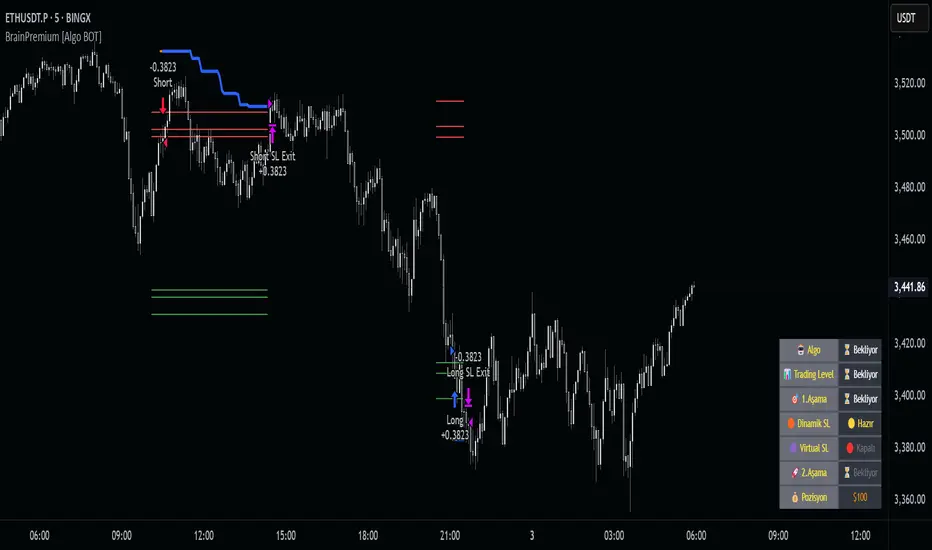

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

Multi-Timeframe MACD/RSI Pro StrategyKey Features: Pine Script v5 Structure:

Multi-Timeframe Analysis: for higher timeframe data

MACD, RSI, and ATR calculated on higher timeframe

EMA50 on current timeframe

Risk Management:

1:2.5 risk-reward ratio enforced

Stop loss based on 1.5x ATR

Position sizing (10% of equity per trade)

Profit Tracking:

Real-time performance metrics

Win rate calculation

ROI percentage display

Alert for 17% profit target

Visualization:

EMA50 plot on chart

Entry markers (triangles)

Performance table in top-right corner

Usage Instructions:

Apply to any TradingView chart

Default settings:

Higher timeframe: 4H

Risk/Reward: 1:2.5

Position size: 10% of equity

Commission: 0.1%

Monitor performance table for:

Total trades

Win rate percentage

Net profit

ROI percentage

To Verify 17% Profit Target:

Run backtest over significant historical data

Check ROI percentage in performance table

The alert will trigger automatically when 17% profit is reached

Note: For accurate backtesting:

Use at least 2 years of historical data

Test across multiple instruments

Adjust timeframe settings to match your trading style

Optimize ATR multiplier and risk/reward ratio for specific markets

Dubic EMA StrategyThe Dubic EMA Strategy is a trend-following and volatility-aware strategy that combines dual EMA filters with intelligent range and noise detection to provide clean, actionable entries. It's designed to avoid choppy markets, enhance trade precision, and adapt to different market conditions.

✅ Key Features:

Dual EMA Filter: Enters long when price is above both EMA High & EMA Low, and short when below both.

Range Filter: Avoids entries during tight consolidations or sideways markets.

Volatility Filter: Prevents trading in low-ATR conditions.

Dynamic Risk Management:

ATR-based or fixed % Stop Loss and Take Profit.

Optional Parabolic SAR trailing stop.

One Trade per Trend: Prevents re-entry until trend direction changes.

Unbroken Range Visualization: Detects and displays consolidation zones that can lead to breakouts.

Alerts & Labels: Clean BUY/SELL signals with alerts and chart labels.

🧩 Customization Options:

Adjustable EMA length

Toggle between ATR or % based SL/TP

Volatility threshold

Range detection sensitivity

Enable/disable SAR trailing stop

This strategy works best on trending assets and timeframes with volatility (e.g., crypto, forex, indices). Suitable for both manual trading and automation.

🛠️ Built for clarity, control, and precision.

📈 Backtest, optimize, and deploy with confidence.

CryptoPulseStoch AICryptoPulseStoch AI Strategy

This strategy combines Bollinger Bands, multi-timeframe EMAs (200 and 50), and Stochastic Oscillator for crypto trading signals on the 1-minute timeframe. Long entries trigger on Stochastic %K/%D crossovers in oversold zones with price breaking the lower Bollinger Band and an upward EMA trend; shorts on crossunders in overbought zones with price breaking the upper Bollinger Band and a downward EMA trend. Includes ATR-based risk management, position sizing, and R:R targets. Overlay on any chart; supports leverage (100% margin). Visual lines/labels for TP/SL/entries; alerts for webhooks.

- **Account Balance (Default: 10000)**: Initial balance for calculating risk and position size; increase for larger accounts.

- **BB Length (Default: 20)**: Periods for Bollinger Bands basis and deviation; shorter for more signals, longer for smoothing.

- **BB Multiplier (Default: 2.0)**: Std dev factor for band width; higher widens bands, reducing false breakouts.

- **Stochastic %K Length (Default: 14)**: Periods for Stochastic Oscillator %K calculation; adjust for sensitivity.

- **Stochastic Smooth K (Default: 1)**: Smoothing period for %K; higher values reduce noise.

- **Stochastic Smooth D (Default: 3)**: Smoothing period for %D; higher values smooth the signal line.

- **Overbought Level (Default: 70)**: Stochastic threshold for bearish signals; lower for more frequent signals.

- **Oversold Level (Default: 30)**: Stochastic threshold for bullish signals; higher for more frequent signals.

- **Risk Per Trade (%) (Default: 2.0)**: Account percentage risked per trade; lower for conservative sizing.

- **Risk:Reward Ratio (Default: 6.0)**: Target profit multiple of risk; higher aims for bigger wins.

- **SL Multiplier (Default: 9.0)**: ATR factor for stop loss distance; adjust based on volatility.

- **TP Multiplier (Default: 6.0)**: ATR factor for take profit distance, scaled by R:R; adjust for target distance.

- **Line Length (bars) (Default: 25)**: Bars to extend TP/SL/entry lines; longer for better visibility.

- **Label Position (Default: left)**: Text placement relative to lines (left/right); choose for chart clarity.

- **ATR Period (Default: 14)**: Periods for ATR volatility measure; affects SL, TP, and position size.

- **EMA Timeframe (Default: 5 min)**: Resolution for EMA 200/50 calculation; use lower TFs for finer trend confirmation.

- **Visuals**: BB plots (blue basis, green upper, red lower); EMA200 (red), EMA50 (green); Stochastic %K (blue), %D (orange); red/green lines/labels for sell/buy entries, SL (red), TP (green).

- **Alerts**: Conditions for buy/sell signals with webhook messages for integration (e.g., Bitget).

CryptoPulse AI### CryptoPulse AI Strategy

This strategy combines Bollinger Bands, multi-timeframe EMAs (200 and 50), and candlestick wick detection for crypto trading signals. Long entries trigger on downward wicks breaking lower BB with upward EMA trend; shorts on upward wicks breaking upper BB with downward EMA trend. Includes ATR-based risk management, position sizing, and R:R targets. Overlay on any chart; supports leverage (100% margin). Visual lines/labels for TP/SL/entries; alerts for webhooks.

- **Account Balance (Default: 10000)**: Initial balance for calculating risk and position size; increase for larger accounts.

- **BB Length (Default: 20)**: Periods for Bollinger Bands basis and deviation; shorter for more signals, longer for smoothing.

- **BB Multiplier (Default: 2.0)**: Std dev factor for band width; higher widens bands, reducing false breakouts.

- **Wick to Body Ratio (Default: 1.1)**: Min wick size vs. body for valid signals (1.1 = 10% larger); higher requires stronger wicks.

- **Risk Per Trade (%) (Default: 2.0)**: Account percentage risked per trade; lower for conservative sizing.

- **Risk:Reward Ratio (Default: 6.0)**: Target profit multiple of risk; higher aims for bigger wins.

- **SL Multiplier (Default: 9.0)**: ATR factor for stop loss distance; adjust based on volatility.

- **Line Length (bars) (Default: 25)**: Bars to extend TP/SL/entry lines; longer for better visibility.

- **Label Position (Default: left)**: Text placement relative to lines (left/right); choose for chart clarity.

- **ATR Period (Default: 14)**: Periods for ATR volatility measure; affects SL and position size.

- **EMA Timeframe (Default: 5 min)**: Resolution for EMA 200/50 calculation; use lower TFs for finer trend confirmation.

- **Visuals**: BB plots (blue basis, green upper, red lower); EMA200 (red), EMA50 (green); red/green lines/labels for sell/buy entries, SL (red), TP (green).

- **Alerts**: Conditions for buy/sell signals with webhook messages for integration (e.g., Bitget).

SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.

Buy Dip Multiple Positions🎯 Objective

This strategy aims to capture aggressive dip-buying opportunities during volume-confirmed price reversals in short term downtrending markets. It is optimized for multi-entry precision, adaptive stop management, and real-time trade monitoring.

It allows traders to execute multiple long entries and dynamically trail stops to maximize gains while capping risk. Designed with modular inputs, this strategy is ideal for intraday momentum scalping and swing trading alike.

🔧 How It Operates

The strategy triggers buy entries when three conditions align:

Reversal Candle: Current close < prior low × 0.998

Volume Confirmation: Current volume exceeds average of prior 2 bars × 1.2

Price Surge Threshold: Current close below user-defined % of close from N bars ago

Once a reversal candle is confirmed, the strategy:

Calculates position size based on user-defined risk parameters

Allows up to a max number of simultaneous trades

Trailing Stop kicks in 2 bars after entry, climbing by a user-defined % each bar

Exit occurs when price hits either the trailing stop or target price

🛠️ Inputs

Users can customize all major aspects of the strategy:

Max Simultaneous Trades: Default 20

Trailing Stop Increase per Bar (%): Default 1%

Initial Stop (% of Reversal Low): Default 85%

Target Price (% Above Reversal Low): Default 60%

Price Surge Threshold (% of Past Close): Default 89%