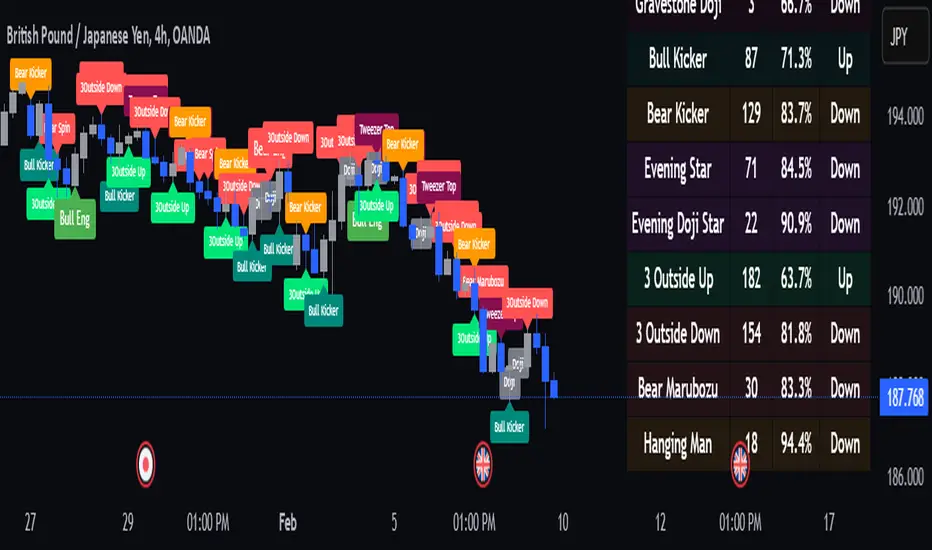

Profit Hunter @DaviddTechProfit Hunter @DaviddTech is an advanced multi-strategy indicator designed to give traders a significant edge in identifying high-probability trading opportunities across all market conditions. By combining the power of T3 adaptive moving averages, ADX-based trend strength analysis, SuperTrend trailing stops, and dynamic support/resistance detection, this indicator delivers a complete trading system in one powerful package.

## 📊 Recommended Usage

Timeframes: Most effective on 1H, 4H, and Daily charts for swing trading; 5M and 15M for day trading

Markets: Works across all markets including Forex, Crypto, Indices, and Stocks

Setup Guidelines: Look for T3 crossovers with strong ADX readings (>25) coinciding with breakout signals (yellow dots/red crosses) near key support/resistance levels for highest probability entries

## 🔥 Key Features:

### T3 Adaptive Trend Detection:

Utilizes premium T3 adaptive indicators instead of standard EMAs for superior smoothing and accuracy

Dynamic color-shifting cloud formation between fast and slow T3 lines reveals immediate trend direction

Proprietary transparency algorithm intensifies cloud colors during strong trends based on real-time ADX readings

### Advanced Support & Resistance Mapping:

Automatically identifies and marks key market structure levels during T3 crossovers

Dynamic horizontal level plotting with optional extension for monitoring future price interactions

Intelligent level validation - converts to dotted lines when price breaks through, maintaining visual clarity

### SuperTrend Trailing Stoploss System:

Professional-grade white trailing stop indicator adapts to market volatility using ATR calculations

Generates precise entry and exit signals with optional buy/sell labels at critical reversal points

Visual trend state highlighting for immediate assessment of current market position

### Breakout Detection & Confirmation:

Sophisticated dual-algorithm breakout system combining Bollinger Bands and Keltner Channels

Visual breakout alerts with yellow dots (bullish) and red crosses (bearish) for instant pattern recognition

Validates breakouts against T3 trend direction to minimize false signals

### Alpha Edge Color System:

Utilizes DaviddTech's signature color scheme with bullish green and bearish pink

Revolutionary transparency algorithm translates ADX readings into precise visual intensity

Higher ADX values produce more vivid colors, instantly communicating trend strength without additional indicators

## 💰 Trading Applications:

Alpha Discovery: Identify emerging trends before the majority of market participants

Precision Entry/Exit: Use SuperTrend signals combined with support/resistance levels for optimal trade execution

Risk Management: Set stops based on the white trailing stoploss line for mathematically-optimized protection

Trend Confirmation: Validate setups using the T3 cloud direction and ADX-based intensity

Breakout Trading: Capture explosive moves with confirmed Bollinger/Keltner breakout signals

Swing Position Management: Monitor extended support/resistance levels for multi-day positioning

## ✨ Strategy Example

As shown in the chart image, ideal entries occur when:

The T3 cloud turns bullish (green) or bearish (pink) with strong color intensity

A yellow dot (bullish) or red cross (bearish) breakout signal appears

Price respects the white SuperTrend line as support/resistance

The trade aligns with key horizontal support/resistance levels identified by the indicator

## 📝 Attribution

This indicator builds upon and enhances concepts from:

Market Trend Levels Detector by BigBeluga (support/resistance detection framework)

T3 indicator implementation by DaviddTech (adaptive moving average system)

Average Directional Index (ADX) methodology for trend strength measurement

Profit Hunter @DaviddTech represents the culmination of advanced technical analysis methodologies in one seamless system.

Pine Script® indicator