QuantBuilder | FractalystWhat's the strategy's purpose and functionality?

QuantBuilder is designed for both traders and investors who want to utilize mathematical techniques to develop profitable strategies through backtesting on historical data.

The primary goal is to develop profitable quantitive strategies that not only outperform the underlying asset in terms of returns but also minimize drawdown.

For instance, consider Bitcoin (BTC), which has experienced significant volatility, averaging an estimated 200% annual return over the past decade, with maximum drawdowns exceeding -80%. By employing this strategy with diverse entry and exit techniques, users can potentially seek to enhance their Compound Annual Growth Rate (CAGR) while managing risk to maintain a lower maximum drawdown.

While this strategy employs quantitative techniques, including mathematical methods such as probabilities and positive expected values, it demonstrates exceptional efficacy across all markets. It particularly excels in futures, indices, stocks, cryptocurrencies, and commodities, leveraging their inherent trending behaviors for optimized performance.

In both trending and consolidating market conditions, QuantBuilder employs a combination of multi-timeframe probabilities, expected values, directional biases, moving averages and diverse entry models to identify and capitalize on bullish market movements.

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

1. Trading:

- Designed for traders looking to capitalize on bullish markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for both swing and intraday trading with a focus on probabilities and risk per trade approach.

2. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully/partially investing in the asset during bullish conditions.

How does the strategy identify market structure? What are the underlying calculations?

The strategy utilizes an efficient logic with for loops to pinpoint the first swing candle featuring a pivot of 2, establishing the point at which the break of structure begins.

What entry criteria are used in this script? What are the underlying calculations?

The script utilizes two entry models: BreakOut and fractal.

Underlying Calculations:

Breakout: The script assigns the most recent swing high to a variable. When the price closes above this level and all other conditions are met, the script executes a breakout entry (conservative approach).

Fractal: The script identifies a swing low with a period of 2. Once this condition is met, the script executes the trade (aggressive approach).

How does the script calculate probabilities? What are the underlying calculations?

The script calculates probabilities by monitoring price interactions with liquidity levels. Here’s how the underlying calculations work:

Tracking Price Hits: The script counts the number of times the price taps into each liquidity side after the EQM level is activated. This data is stored in an array for further analysis.

Sample Size Consideration: The total number of price interactions serves as the sample size for calculating probabilities.

Probability Calculation: For each liquidity side, the script calculates the probability by taking the average of the recorded hits. This allows for a dynamic assessment of the likelihood that a particular side will be hit next, based on historical performance.

Dynamic Adjustment: As new price data comes in, the probabilities are recalculated, providing real-time aduptive insights into market behavior.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

How does the script calculate expected values? What are the underlying calculations?

The script calculates expected values by leveraging the probabilities of winning and losing trades, along with their respective returns. The process involves the following steps:

This quantitative methodology provides a robust framework for assessing the expected performance of trading strategies based on historical data and backtesting results.

How is the contextual bias calculated? What are the underlying calculations?

The contextual bias in the QuantBuilder script is calculated through a structured approach that assesses market structure based on swing highs and lows. Here’s how it works:

Identification of Swing Points: The script identifies significant swing points using a defined pivot logic, focusing on the first swing high and swing low. This helps establish critical levels for determining market structure.

Break of Structure (BOS) Assessment:

Bullish BOS: The script recognizes a bullish break of structure when a candle closes above the first swing high, followed by at least one swing low.

Bearish BOS: Conversely, a bearish break of structure is identified when a candle closes below the first swing low, followed by at least one swing high.

Bias Assignment: Based on the identified break of structure, the script assigns directional biases:

A bullish bias is assigned if a bullish BOS is confirmed.

A bearish bias is assigned if a bearish BOS is confirmed.

Quantitative Evaluation: Each identified bias is quantitatively evaluated, allowing the script to assign numerical values representing the strength of each bias. This quantification aids in assessing the reliability of market sentiment across multiple timeframes.

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

- Initial Stop-loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14)

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

- Trailing Stop-Loss:

One of the key elements of this strategy is its ability to detect structural liquidity and structural invalidation levels across multiple timeframes to trail the stop-loss once the trade is in running profits.

By utilizing this approach, the strategy allows enough room for price to run.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

To facilitate studying historical data, all conditions and filters can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

How to Use This Quantitive Strategy Builder to Create a Profitable Edge and System?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What makes this strategy original?

QuantBuilder stands out due to its unique combination of quantitative techniques and innovative algorithms that leverage historical data for real-time trading decisions. Unlike most algorithmic strategies that work based on predefined rules, this strategy adapts to real-time market probabilities and expected values, enhancing its reliability. Key features include:

Mathematical Framework: The strategy integrates advanced mathematical concepts, such as probabilities and expected values, to assess trade viability and optimize decision-making.

Multi-Timeframe Analysis: By utilizing multi-timeframe probabilities, QuantBuilder provides a comprehensive view of market conditions, enhancing the accuracy of entry and exit points.

Dynamic Market Structure Identification: The script employs a systematic approach to identify market structure changes, utilizing a blend of swing highs and lows to detect contextual/direction bias of the market.

Built-in Trailing Stop Loss: The strategy features a dynamic trailing stop loss based on multi-timeframe analysis of market structure. This allows traders to lock in profits while adapting to changing market conditions, ensuring that exits are executed at optimal levels without prematurely closing positions.

Robust Performance Metrics: With detailed performance tables and visualizations, users can easily evaluate strategy effectiveness and adjust parameters based on historical performance.

Adaptability: The strategy is designed to work across various markets and timeframes, making it versatile for different trading styles and objectives.

Suitability for Investors and Traders: QuantBuilder is ideal for both investors and traders looking to rely on mathematically proven data to create profitable strategies, ensuring that decisions are grounded in quantitative analysis.

These original elements combine to create a powerful tool that can help both traders and investors to build and refine profitable strategies based on algorithmic quantitative analysis.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Search in scripts for "bear"

ICT Indicator with Paper TradingThe strategy implemented in the provided Pine Script is based on **ICT (Inner Circle Trader)** concepts, particularly focusing on **order blocks** to identify key levels for potential reversals or continuations in the market. Below is a detailed description of the strategy:

### 1. **Order Block Concept**

- **Order blocks** are price levels where large institutional orders accumulate, often leading to a reversal or continuation of price movement.

- In this strategy, **order blocks** are identified when:

- The high of the current bar crosses above the high of the previous bar (for bullish order blocks).

- The low of the current bar crosses below the low of the previous bar (for bearish order blocks).

### 2. **Buy and Sell Signal Generation**

The core of the strategy revolves around identifying the **breakout** of order blocks, which is interpreted as a signal to either enter or exit trades:

- **Buy Signal**:

- Generated when the closing price crosses **above** the last identified bullish order block (i.e., the highest point during the last upward crossover of highs).

- This signals a potential upward trend, and the strategy enters a long position.

- **Sell Signal**:

- Generated when the closing price crosses **below** the last identified bearish order block (i.e., the lowest point during the last downward crossover of lows).

- This signals a potential downward trend, and the strategy exits any open long positions.

### 3. **Strategy Execution**

The strategy is executed using the `strategy.entry()` and `strategy.close()` functions:

- **Enter Long Positions**: When a buy signal is generated, the strategy opens a long position (buying).

- **Exit Positions**: When a sell signal is generated, the strategy closes the long position.

### 4. **Visual Indicators on the Chart**

To make the strategy easier to follow visually, buy and sell signals are marked directly on the chart:

- **Buy signals** are indicated with a green upward-facing triangle above the bar where the signal occurred.

- **Sell signals** are indicated with a red downward-facing triangle below the bar where the signal occurred.

### 5. **Key Elements of the Strategy**

- **Trend Continuation and Reversals**: This strategy is attempting to capture trends based on the breakout of important price levels (order blocks). When the price breaks above or below a significant order block, it is expected that the market will continue in that direction.

- **Order Block Strength**: Order blocks are considered strong areas where price action could reverse or accelerate, based on how institutional investors place large orders.

### 6. **Paper Trading**

This script uses **paper trading** to simulate trades without actual money being involved. This allows users to backtest the strategy, seeing how it would have performed in historical market conditions.

### 7. **Basic Strategy Flow**

1. **Order Block Identification**: The script constantly monitors price movements to detect bullish and bearish order blocks.

2. **Buy Signal**: If the closing price crosses above the last order block high, the strategy interprets it as a sign of bullish momentum and enters a long position.

3. **Sell Signal**: If the closing price crosses below the last order block low, it signals a bearish momentum, and the strategy closes the long position.

4. **Visual Representation**: Buy and sell signals are displayed on the chart for easy identification.

### **Advantages of the Strategy:**

- **Simple and Clear Rules**: The strategy is based on clearly defined rules for identifying order blocks and trade signals.

- **Effective for Trend Following**: By focusing on breakouts of order blocks, this strategy attempts to capture strong trends in the market.

- **Visual Aids**: The plot of buy/sell signals helps traders to quickly see where trades would have been placed.

### **Limitations:**

- **No Shorting**: This strategy only enters long positions (buying). It does not account for shorting opportunities.

- **No Risk Management**: There are no built-in stop losses, trailing stops, or profit targets, which could expose the strategy to large losses during adverse market conditions.

- **Whipsaws in Range Markets**: The strategy could produce false signals in sideways or choppy markets, where breakouts are short-lived and prices quickly reverse.

### **Overall Strategy Objective:**

The goal of the strategy is to enter into long positions when the price breaks above a significant order block, and exit when it breaks below. The strategy is designed for trend-following, with the assumption that price will continue in the direction of the breakout.

Let me know if you'd like to enhance or modify this strategy further!

Larry Conners Vix Reversal II Strategy (approx.)This Pine Script™ strategy is a modified version of the original Larry Connors VIX Reversal II Strategy, designed for short-term trading in market indices like the S&P 500. The strategy utilizes the Relative Strength Index (RSI) of the VIX (Volatility Index) to identify potential overbought or oversold market conditions. The logic is based on the assumption that extreme levels of market volatility often precede reversals in price.

How the Strategy Works

The strategy calculates the RSI of the VIX using a 25-period lookback window. The RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is often used to identify overbought and oversold conditions in assets.

Overbought Signal: When the RSI of the VIX rises above 61, it signals a potential overbought condition in the market. The strategy looks for a RSI downtick (i.e., when RSI starts to fall after reaching this level) as a trigger to enter a long position.

Oversold Signal: Conversely, when the RSI of the VIX drops below 42, the market is considered oversold. A RSI uptick (i.e., when RSI starts to rise after hitting this level) serves as a signal to enter a short position.

The strategy holds the position for a minimum of 7 days and a maximum of 12 days, after which it exits automatically.

Larry Connors: Background

Larry Connors is a prominent figure in quantitative trading, specializing in short-term market strategies. He is the co-author of several influential books on trading, such as Street Smarts (1995), co-written with Linda Raschke, and How Markets Really Work. Connors' work focuses on developing rules-based systems using volatility indicators like the VIX and oscillators such as RSI to exploit mean-reversion patterns in financial markets.

Risks of the Strategy

While the Larry Connors VIX Reversal II Strategy can capture reversals in volatile market environments, it also carries significant risks:

Over-Optimization: This modified version adjusts RSI levels and holding periods to fit recent market data. If market conditions change, the strategy might no longer be effective, leading to false signals.

Drawdowns in Trending Markets: This is a mean-reversion strategy, designed to profit when markets return to a previous mean. However, in strongly trending markets, especially during extended bull or bear phases, the strategy might generate losses due to early entries or exits.

Volatility Risk: Since this strategy is linked to the VIX, an instrument that reflects market volatility, large spikes in volatility can lead to unexpected, fast-moving market conditions, potentially leading to larger-than-expected losses.

Scientific Literature and Supporting Research

The use of RSI and VIX in trading strategies has been widely discussed in academic research. RSI is one of the most studied momentum oscillators, and numerous studies show that it can capture mean-reversion effects in various markets, including equities and derivatives.

Wong et al. (2003) investigated the effectiveness of technical trading rules such as RSI, finding that it has predictive power in certain market conditions, particularly in mean-reverting markets .

The VIX, often referred to as the “fear index,” reflects market expectations of volatility and has been a focal point in research exploring volatility-based strategies. Whaley (2000) extensively reviewed the predictive power of VIX, noting that extreme VIX readings often correlate with turning points in the stock market .

Modified Version of Original Strategy

This script is a modified version of Larry Connors' original VIX Reversal II strategy. The key differences include:

Adjusted RSI period to 25 (instead of 2 or 4 commonly used in Connors’ other work).

Overbought and oversold levels modified to 61 and 42, respectively.

Specific holding period (7 to 12 days) is predefined to reduce holding risk.

These modifications aim to adapt the strategy to different market environments, potentially enhancing performance under specific volatility conditions. However, as with any system, constant evaluation and testing in live markets are crucial.

References

Wong, W. K., Manzur, M., & Chew, B. K. (2003). How rewarding is technical analysis? Evidence from Singapore stock market. Applied Financial Economics, 13(7), 543-551.

Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

Averaging Down Strategy1. Averaging Down:

Definition: "Averaging Down" is a strategy in which an investor buys more shares of a declining asset, thus lowering the average purchase price. The main idea is that, by averaging down, the investor can recover faster when the price eventually rebounds.

Risk Considerations: This strategy assumes that the asset will recover in value. If the price continues to decline, however, the investor may suffer larger losses. Academic research highlights the psychological bias of loss aversion that often leads investors to engage in averaging down, despite the increased risk (Barberis & Huang, 2001).

2. RSI (Relative Strength Index):

Definition: The RSI is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is commonly used to identify overbought or oversold conditions. A reading below 30 (or in this case, 35) typically indicates an oversold condition, which might suggest a potential buying opportunity (Wilder, 1978).

Risk Considerations: RSI-based strategies can produce many false signals in range-bound or choppy markets, where prices do not exhibit strong trends. This can lead to multiple losing trades and an overall negative performance (Gencay, 1998).

3. Combination of RSI and Price Movement:

Approach: The combination of RSI for entry signals and price movement (previous day's high) for exit signals aims to capture short-term market reversals. This hybrid approach attempts to balance momentum with price confirmation.

Risk Considerations: While this combination can work well in trending markets, it may struggle in volatile or sideways markets. Additionally, a significant risk of averaging down is that the trader may continue adding to a losing position, which can exacerbate losses if the price keeps falling.

Risk Warnings:

Increased Losses Through Averaging Down:

Averaging down involves buying more of a falling asset, which can increase exposure to downside risk. Studies have shown that this approach can lead to larger losses when markets continue to decline, especially during prolonged bear markets (Statman, 2004).

A key risk is that this strategy may lead to significant capital drawdowns if the price of the asset does not recover as expected. In the worst-case scenario, this can result in a total loss of the invested capital.

False Signals with RSI:

RSI-based strategies are prone to generating false signals, particularly in markets that do not exhibit strong trends. For example, Gencay (1998) found that while RSI can be effective in certain conditions, it often fails in choppy or range-bound markets, leading to frequent stop-outs and drawdowns.

Psychological Bias:

Behavioral finance research suggests that the "Averaging Down" strategy may be influenced by loss aversion, a bias where investors prefer to avoid losses rather than achieve gains (Kahneman & Tversky, 1979). This can lead to poor decision-making, as investors continue to add to losing positions in the hope of a recovery.

Empirical Studies:

Gencay (1998): The study "The Predictability of Security Returns with Simple Technical Trading Rules" found that technical indicators like RSI can provide predictive value in certain markets, particularly in volatile environments. However, they are less reliable in markets that lack clear trends.

Barberis & Huang (2001): Their research on behavioral biases, including loss aversion, explains why investors are often tempted to average down despite the risks, as they attempt to avoid realizing losses.

Statman (2004): In "The Diversification Puzzle," Statman discusses how strategies like averaging down can increase risk exposure without necessarily improving long-term returns, especially if the underlying asset continues to perform poorly.

Conclusion:

The "Averaging Down Strategy with RSI" combines elements of technical analysis with a psychologically-driven averaging down approach. While the strategy may offer opportunities in trending or oversold markets, it carries significant risks, particularly in volatile or declining markets. Traders should be cautious when using this strategy, ensuring they manage risk effectively and avoid overexposure to a losing position.

Fibonacci-Only StrategyFibonacci-Only Strategy

This script is a custom trading strategy designed for traders who leverage Fibonacci retracement levels to identify potential trade entries and exits. The strategy is versatile, allowing users to trade across multiple timeframes, with built-in options for dynamic stop loss, trailing stops, and take profit levels.

Key Features:

Custom Fibonacci Levels:

This strategy calculates three specific Fibonacci retracement levels: 19%, 82.56%, and the reverse 19% level. These levels are used to identify potential areas of support and resistance where price reversals or breaks might occur.

The Fibonacci levels are calculated based on the highest and lowest prices within a 100-bar period, making them dynamic and responsive to recent market conditions.

Dynamic Entry Conditions:

Touch Entry: The script enters long or short positions when the price touches specific Fibonacci levels and confirms the move with a bullish (for long) or bearish (for short) candle.

Break Entry (Optional): If the "Use Break Strategy" option is enabled, the script can also enter positions when the price breaks through Fibonacci levels, providing more aggressive entry opportunities.

Stop Loss Management:

The script offers flexible stop loss settings. Users can choose between a fixed percentage stop loss or an ATR-based stop loss, which adjusts based on market volatility.

The ATR (Average True Range) stop loss is multiplied by a user-defined factor, allowing for tailored risk management based on market conditions.

Trailing Stop Mechanism:

The script includes an optional trailing stop feature, which adjusts the stop loss level as the market moves in favor of the trade. This helps lock in profits while allowing the trade to run if the trend continues.

The trailing stop is calculated as a percentage of the difference between the entry price and the current market price.

Multiple Take Profit Levels:

The strategy calculates seven take profit levels, each at incremental percentages above (for long trades) or below (for short trades) the entry price. This allows for gradual profit-taking as the market moves in the trade's favor.

Each take profit level can be customized in terms of the percentage of the position to be closed, providing precise control over exit strategies.

Strategy Backtesting and Results:

Realistic Backtesting:

The script has been backtested with realistic account sizes, commission rates, and slippage settings to ensure that the results are applicable to actual trading scenarios.

The backtesting covers various timeframes and markets to ensure the strategy's robustness across different trading environments.

Default Settings:

The script is published with default settings that have been optimized for general use. These settings include a 15-minute timeframe, a 1.0% stop loss, a 2.0 ATR multiplier for stop loss, and a 1.5% trailing stop.

Users can adjust these settings to better fit their specific trading style or the market they are trading.

How It Works:

Long Entry Conditions:

The strategy enters a long position when the price touches the 19% Fibonacci level (from high to low) or the reverse 19% level (from low to high) and confirms the move with a bullish candle.

If the "Use Break Strategy" option is enabled, the script will also enter a long position when the price breaks below the 19% Fibonacci level and then moves back up, confirming the break with a bullish candle.

Short Entry Conditions:

The strategy enters a short position when the price touches the 82.56% Fibonacci level and confirms the move with a bearish candle.

If the "Use Break Strategy" option is enabled, the script will also enter a short position when the price breaks above the 82.56% Fibonacci level and then moves back down, confirming the break with a bearish candle.

Stop Loss and Take Profit Logic:

The stop loss for each trade is calculated based on the selected method (fixed percentage or ATR-based). The strategy then manages the trade by either trailing the stop or taking profit at predefined levels.

The take profit levels are set at increments of 0.5% above or below the entry price, depending on whether the position is long or short. The script gradually exits the trade as these levels are hit, securing profits while minimizing risk.

Usage:

For Fibonacci Traders:

This script is ideal for traders who rely on Fibonacci retracement levels to find potential trade entries and exits. The script automates the process, allowing traders to focus on market analysis and decision-making.

For Trend and Swing Traders:

The strategy's flexibility in handling both touch and break entries makes it suitable for trend-following and swing trading strategies. The multiple take profit levels allow traders to capture profits in trending markets while managing risk.

Important Notes:

Originality: This script uniquely combines Fibonacci retracement levels with dynamic stop loss management and multiple take profit levels. It is not just a combination of existing indicators but a thoughtful integration designed to enhance trading performance.

Disclaimer: Trading involves risk, and it is crucial to test this script in a demo account or through backtesting before applying it to live trading. Users should ensure that the settings align with their individual risk tolerance and trading strategy.

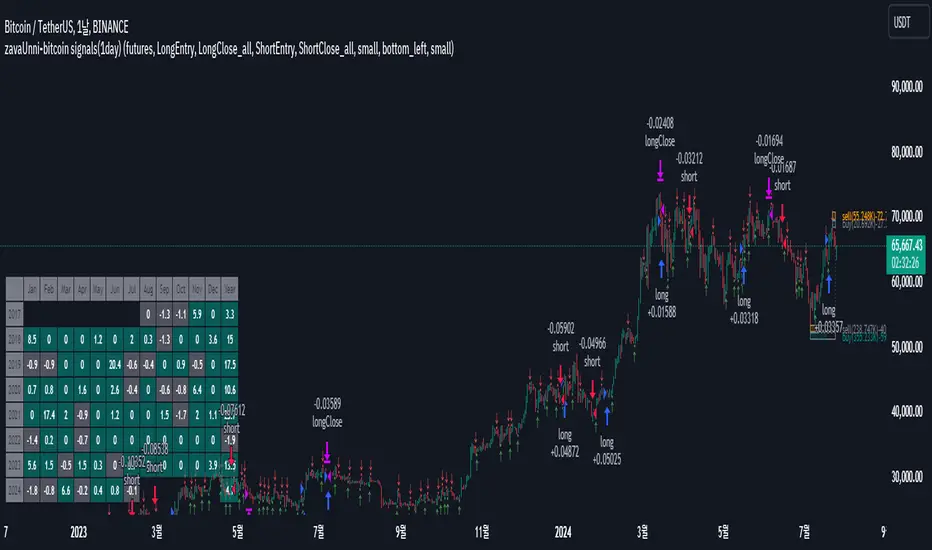

zavaUnni-bitcoin signals(1day)

📌 This strategy predicts price movements based on trading volume and enters positions accordingly. It calculates the expected price increase based on bullish volume and the expected price decrease based on bearish volume to determine the direction of the position.

Top predicted price based on declining bullish volume: top_ifpricebull

Bottom predicted price based on declining bearish volume: top_ifpricebear

Top predicted price based on increasing bullish volume: bot_ifpricebull

Bottom predicted price based on increasing bearish volume: bot_ifpricebear

Using these four values, the strategy calculates the final maxprice and minprice based on volume. If the price settles above the max value, it indicates an upward trend; if it settles below the min value, it indicates a downward trend.

📌 The indicator does not solely rely on the maxprice and minprice conditions. It incorporates complex and sophisticated analysis by considering average volume and candle size.

During a decline, if the average volume and spread of bullish candles exceed those of bearish candles and the price settles above the max value, a long position is entered.

During a rise, if the average volume and spread of bearish candles exceed those of bullish candles and the price settles below the min value, a short position is entered.

Even if the above conditions are met, if the buying pressure significantly outweighs the selling pressure, the position will be closed, but a reverse position will not be entered.

Reviewing historical data shows that while there are instances where the position switches from long to short immediately, there are also cases where the position is closed and re-entered after a few candles.

📌 Trading volume is one of the most traditional yet essential indicators, accurately reflecting price direction. This strategy, which simultaneously predicts fundamental trading volume and price changes, consistently achieves a profit factor above 3.

Characteristics and Historical Data of the Strategy

🔴 Short position entry: April 11, 2022

🟢 Long position entry after closing short: January 11, 2023

⚫ Short position holding period: 270 days

🟢 Long position entry: October 9, 2020

🔵 Long position exit: November 30, 2019

⚫ Long position holding period: 52 days

🟢 Long position entry: November 30, 2019

🔵 Long position exit: February 22, 2021

⚫ Long position holding period: 84 days

Settings Explanation

🛠️ In the input, you can choose between spot and futures. Buy and sell signals are generated in spot trading, while long and short signals are generated in futures trading.

🌈 You can configure the screen view.

Fibonacci Trend

Falling Fibonacci levels from the top: 382 and 618 levels (Red lines)

Rising Fibonacci levels from the bottom: 382 and 618 levels (Green lines)

When the price stays within the 382 and 618 levels of the falling Fibonacci, the background turns red; when it stays within the 382 and 618 levels of the rising Fibonacci, the background turns green.

Real-time Volume Strength of Bullish and Bearish Candles

Red arrow: Appears when the strength of bearish candles increases

Green arrow: Appears when the strength of bullish candles increases

Cumulative Volume of Bullish and Bearish Candles during the Trend

Cumulative data of falling bullish and bearish candles from the top

Cumulative data of rising bullish and bearish candles from the bottom

Profit Table

Provides annual and monthly profit tables.

Setting Options

You can change the options in the attributes to test different configurations.

📌 Trading Data

Although Binance data starts from 2017, limiting the number of trades to 60 as of July 2024, this does not undermine the validity of the strategy. Binance provides reliable volume data, which is crucial for evaluating the strategy's performance. In contrast, exchanges like Bitstamp may have longer trading histories but insufficient volume to properly assess the strategy's actual performance. A volume-based strategy cannot be reliably tested on an exchange with low trading volume. Therefore, despite the limited number of trades on Binance, its reliable volume data justifies its use for this strategy.

► Backtesting Details:

Timeframe: 1D / Bitcoin / TetherUS

Initial Balance: $50,000 (Enter the initial capital you will invest)

Order Size: 10% (Enter the percentage of your account balance you will trade)

Commission: 0.04% (Enter the trading commission)

Slippage: 10 ticks (Enter the slippage you want to test)

When using the strategy:

📢 Timeframe: While the strategy performs well on timeframes lower than daily, it is particularly profitable on the daily timeframe.

📢 Exchange: It is recommended to use Binance due to its reliable volume data.

📢 This strategy is suitable for traders who have the patience to hold positions for extended periods, as it calculates the size of bullish and bearish candles carefully and does not change positions easily.

📢 Spot trading is recommended over futures, and if using futures, leverage should be limited to a maximum of 2x.

Chandelier Exit Strategy with 200 EMA FilterStrategy Name and Purpose

Chandelier Exit Strategy with 200EMA Filter

This strategy uses the Chandelier Exit indicator in combination with a 200-period Exponential Moving Average (EMA) to generate trend-based trading signals. The main purpose of this strategy is to help traders identify high-probability entry points by leveraging the Chandelier Exit for stop loss levels and the EMA for trend confirmation. This strategy aims to provide clear rules for entries and exits, improving overall trading discipline and performance.

Originality and Usefulness

This script integrates two powerful indicators to create a cohesive and effective trading strategy:

Chandelier Exit : This indicator is based on the Average True Range (ATR) and identifies potential stop loss levels. The Chandelier Exit helps manage risk by setting stop loss levels at a distance from the highest high or lowest low over a specified period, multiplied by the ATR. This ensures that the stop loss adapts to market volatility.

200-period Exponential Moving Average (EMA) : The EMA acts as a trend filter. By ensuring trades are only taken in the direction of the overall trend, the strategy improves the probability of success. For long entries, the close price must be above the 200 EMA, indicating a bullish trend. For short entries, the close price must be below the 200 EMA, indicating a bearish trend.

Combining these indicators adds layers of confirmation and risk management, enhancing the strategy's effectiveness. The Chandelier Exit provides dynamic stop loss levels based on market volatility, while the EMA ensures trades align with the prevailing trend.

Entry Conditions

Long Entry

A buy signal is generated by the Chandelier Exit.

The close price is above the 200 EMA, indicating a strong bullish trend.

Short Entry

A sell signal is generated by the Chandelier Exit.

The close price is below the 200 EMA, indicating a strong bearish trend.

Exit Conditions

For long positions: The position is closed when a sell signal is generated by the Chandelier Exit.

For short positions: The position is closed when a buy signal is generated by the Chandelier Exit.

Risk Management

Account Size: 1,000,00 yen

Commission and Slippage: 17 pips commission and 1 pip slippage per trade

Risk per Trade: 10% of account equity

Stop Loss: For long trades, the stop loss is placed slightly below the candle that generated the buy signal. For short trades, the stop loss is placed slightly above the candle that generated the sell signal. The stop loss levels are dynamically adjusted based on the ATR.

Settings Options

ATR Period: Set the period for calculating the ATR to determine the Chandelier Exit levels.

ATR Multiplier: Set the multiplier for ATR to define the distance of stop loss levels from the highest high or lowest low.

Use Close Price for Extremums: Choose whether to use the close price for calculating the extremums.

EMA Period: Set the period for the EMA to adjust the trend filter sensitivity.

Show Buy/Sell Labels: Choose whether to display buy and sell labels on the chart for visual confirmation.

Highlight State: Choose whether to highlight the bullish or bearish state on the chart.

Sufficient Sample Size

The strategy has been backtested with a sufficient sample size to evaluate its performance accurately. This ensures that the strategy's results are statistically significant and reliable.

Notes

This strategy is based on historical data and does not guarantee future results.

Thoroughly backtest and validate results before using in live trading.

Market volatility and other external factors can affect performance and may not yield expected results.

Acknowledgment

This strategy uses the Chandelier Exit indicator. Special thanks to the original contributors for their work on the Chandelier Exit concept.

Clean Chart Explanation

The script is published with a clean chart to ensure that its output is readily identifiable and easy to understand. No other scripts are included on the chart, and any drawings or images used are specifically to illustrate how the script works.

AlgoBuilder [Mean-Reversion] | FractalystWhat's the strategy's purpose and functionality?

This strategy is designed for both traders and investors looking to rely and trade based on historical and backtested data using automation.

The main goal is to build profitable mean-reversion strategies that outperform the underlying asset in terms of returns while minimizing drawdown.

For example, as for a benchmark, if the S&P 500 (SPX) has achieved an estimated 10% annual return with a maximum drawdown of -57% over the past 20 years, using this strategy with different entry and exit techniques, users can potentially seek ways to achieve a higher Compound Annual Growth Rate (CAGR) while maintaining a lower maximum drawdown.

Although the strategy can be applied to all markets and timeframes, it is most effective on stocks, indices, future markets, cryptocurrencies, and commodities and JPY currency pairs given their trending behaviors.

In trending market conditions, the strategy employs a combination of moving averages and diverse entry models to identify and capitalize on upward market movements. It integrates market structure-based moving averages and bands mechanisms across different timeframes and provides exit techniques, including percentage-based and risk-reward (RR) based take profit levels.

Additionally, the strategy has also a feature that includes a built-in probability function for traders who want to implement probabilities right into their trading strategies.

Performance summary, weekly, and monthly tables enable quick visualization of performance metrics like net profit, maximum drawdown, profit factor, average trade, average risk-reward ratio (RR), and more.

This aids optimization to meet specific goals and risk tolerance levels effectively.

-----

How does the strategy perform for both investors and traders?

The strategy has two main modes, tailored for different market participants: Traders and Investors.

Trading:

1. Trading:

- Designed for traders looking to capitalize on bullish trending markets.

- Utilizes a percentage risk per trade to manage risk and optimize returns.

- Suitable for active trading with a focus on mean-reversion and risk per trade approach.

◓: Mode | %: Risk percentage per trade

3. Investing:

- Geared towards investors who aim to capitalize on bullish trending markets without using leverage while mitigating the asset's maximum drawdown.

- Utilizes pre-define percentage of the equity to buy, hold, and manage the asset.

- Focuses on long-term growth and capital appreciation by fully investing in the asset during bullish conditions.

- ◓: Mode | %: Risk not applied (In investing mode, the strategy uses 10% of equity to buy the asset)

-----

What's is FRMA? How does the triple bands work? What are the underlying calculations?

Middle Band (FRMA):

The middle band is the core of the FRMA system. It represents the Fractalyst Moving Average, calculated by identifying the most recent external swing highs and lows in the market structure.

By determining these external swing pivot points, which act as significant highs and lows within the market range, the FRMA provides a unique moving average that adapts to market structure changes.

Upper Band:

The upper band shows the average price of the most recent external swing highs.

External swing highs are identified as the highest points between pivot points in the market structure.

This band helps traders identify potential overbought conditions when prices approach or exceed this upper band.

Lower Band:

The lower band shows the average price of the most recent external swing lows.

External swing lows are identified as the lowest points between pivot points in the market structure.

The script utilizes this band to identify potential oversold conditions, triggering entry signals as prices approach or drop below the lower band.

Adjustments Based on User Inputs:

Users can adjust how the upper and lower bands are calculated based on their preferences:

Upper/Lower: This method calculates the average bands using the prices of external swing highs and lows identified in the market.

Percentage Deviation from FRMA: Alternatively, users can opt to calculate the bands based on a percentage deviation from the middle FRMA. This approach provides flexibility to adjust the width of the bands relative to market conditions and volatility.

-----

What's the purpose of using moving averages in this strategy? What are the underlying calculations?

Using moving averages is a widely-used technique to trade with the trend.

The main purpose of using moving averages in this strategy is to filter out bearish price action and to only take trades when the price is trading ABOVE specified moving averages.

The script uses different types of moving averages with user-adjustable timeframes and periods/lengths, allowing traders to try out different variations to maximize strategy performance and minimize drawdowns.

By applying these calculations, the strategy effectively identifies bullish trends and avoids market conditions that are not conducive to profitable trades.

The MA filter allows traders to choose whether they want a specific moving average above or below another one as their entry condition.

This comparison filter can be turned on (>) or off.

For example, you can set the filter so that MA#1 > MA#2, meaning the first moving average must be above the second one before the script looks for entry conditions. This adds an extra layer of trend confirmation, ensuring that trades are only taken in more favorable market conditions.

⍺: MA Period | Σ: MA Timeframe

-----

What entry modes are used in this strategy? What are the underlying calculations?

The strategy by default uses two different techniques for the entry criteria with user-adjustable left and right bars: Breakout and Fractal.

1. Breakout Entries :

- The strategy looks for pivot high points with a default period of 3.

- It stores the most recent high level in a variable.

- When the price crosses above this most recent level, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot high left bars period | ◨: Pivot high right bars period

2. Fractal Entries :

- The strategy looks for pivot low points with a default period of 3.

- When a pivot low is detected, the strategy checks if all conditions are met and the bar is closed before taking the buy entry.

◧: Pivot low left bars period | ◨: Pivot low right bars period

2. Hunt Entries :

- The strategy identifies a candle that wicks through the lower FRMA band.

- It waits for the next candle to close above the low of the wick candle.

- When this condition is met and the bar is closed, the strategy takes the buy entry.

By utilizing these entry modes, the strategy aims to capitalize on bullish price movements while ensuring that the necessary conditions are met to validate the entry points.

-----

What type of stop-loss identification method are used in this strategy? What are the underlying calculations?

Initial Stop-Loss:

1. ATR Based:

The Average True Range (ATR) is a method used in technical analysis to measure volatility. It is not used to indicate the direction of price but to measure volatility, especially volatility caused by price gaps or limit moves.

Calculation:

- To calculate the ATR, the True Range (TR) first needs to be identified. The TR takes into account the most current period high/low range as well as the previous period close.

The True Range is the largest of the following:

- Current Period High minus Current Period Low

- Absolute Value of Current Period High minus Previous Period Close

- Absolute Value of Current Period Low minus Previous Period Close

- The ATR is then calculated as the moving average of the TR over a specified period. (The default period is 14).

Example - ATR (14) * 2

⍺: ATR period | Σ: ATR Multiplier

2. ADR Based:

The Average Day Range (ADR) is an indicator that measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

Calculation:

- To calculate the ADR for a particular day:

- Calculate the average of the high prices over a specified number of days.

- Calculate the average of the low prices over the same number of days.

- Find the difference between these average values.

- The default period for calculating the ADR is 14 days. A shorter period may introduce more noise, while a longer period may be slower to react to new market movements.

Example - ADR (20) * 2

⍺: ADR period | Σ: ADR Multiplier

3. PL Based:

This method places the stop-loss at the low of the previous candle.

If the current entry is based on the hunt entry strategy, the stop-loss will be placed at the low of the candle that wicks through the lower FRMA band.

Example:

If the previous candle's low is 100, then the stop-loss will be set at 100.

This method ensures the stop-loss is placed just below the most recent significant low, providing a logical and immediate level for risk management.

Application in Strategy (ATR/ADR):

- The strategy calculates the current bar's ADR/ATR with a user-defined period.

- It then multiplies the ADR/ATR by a user-defined multiplier to determine the initial stop-loss level.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance.

-----

What type of break-even and take profit identification methods are used in this strategy? What are the underlying calculations?

For Break-Even:

Percentage (%) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain percentage above the entry.

Calculation:

Break-even level = Entry Price * (1 + Percentage / 100)

Example:

If the entry price is $100 and the break-even percentage is 5%, the break-even level is $100 * 1.05 = $105.

Risk-to-Reward (RR) Based:

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

Example:

If the entry price is $100, the initial risk is $10, and the RR ratio is 2, the break-even level is $100 + ($10 * 2) = $120.

FRMA Based:

Moves the stop-loss to break-even when the price hits the FRMA level at which the entry was taken.

Calculation:

Break-even level = FRMA level at the entry

Example:

If the FRMA level at entry is $102, the break-even level is set to $102 when the price reaches $102.

For TP1 (Take Profit 1):

- You can choose to set a take profit level at which your position gets fully closed or 50% if the TP2 boolean is enabled.

- Similar to break-even, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP1 level as a percentage amount above the entry price or based on RR.

For TP2 (Take Profit 2):

- You can choose to set a take profit level at which your position gets fully closed.

- As with break-even and TP1, you can select either a percentage (%) or risk-to-reward (RR) based take profit level, allowing you to set your TP2 level as a percentage amount above the entry price or based on RR.

When Both Percentage (%) Based and RR Based Take Profit Levels Are Off:

The script will adjust the take profit level to the higher FRMA band set within user inputs.

Calculation:

Take profit level = Higher FRMA band length/timeframe specified by the user.

This ensures that when neither percentage-based nor risk-to-reward-based take profit methods are enabled, the strategy defaults to using the higher FRMA band as the take profit level, providing a consistent and structured approach to profit-taking.

For TP1 and TP2, it's specifying the price levels at which the position is partially or fully closed based on the chosen method (percentage or RR) above the entry price.

These calculations are crucial for managing risk and optimizing profitability in the strategy.

⍺: BE/TP type (%/RR) | Σ: how many RR/% above the current price

-----

What's the ADR filter? What does it do? What are the underlying calculations?

The Average Day Range (ADR) measures the volatility of an asset by showing the average movement of the price between the high and the low over the last several days.

The period of the ADR filter used in this strategy is tied to the same period you've used for your initial stop-loss.

Users can define the minimum ADR they want to be met before the script looks for entry conditions.

ADR Bias Filter:

- Compares the current bar ADR with the ADR (Defined by user):

- If the current ADR is higher, it indicates that volatility has increased compared to ADR (DbU).(⬆)

- If the current ADR is lower, it indicates that volatility has decreased compared to ADR (DbU).(⬇)

Calculations:

1. Calculate ADR:

- Average the high prices over the specified period.

- Average the low prices over the same period.

- Find the difference between these average values in %.

2. Current ADR vs. ADR (DbU):

- Calculate the ADR for the current bar.

- Calculate the ADR (DbU).

- Compare the two values to determine if volatility has increased or decreased.

By using the ADR filter, the strategy ensures that trades are only taken in favorable market conditions where volatility meets the user's defined threshold, thus optimizing entry conditions and potentially improving the overall performance of the strategy.

>: Minimum required ADR for entry | %: Current ADR comparison to ADR of 14 days ago.

-----

What's the probability filter? What are the underlying calculations?

The probability filter is designed to enhance trade entries by using buyside liquidity and probability analysis to filter out unfavorable conditions.

This filter helps in identifying optimal entry points where the likelihood of a profitable trade is higher.

Calculations:

1. Understanding Swing highs and Swing Lows

Swing High: A Swing High is formed when there is a high with 2 lower highs to the left and right.

Swing Low: A Swing Low is formed when there is a low with 2 higher lows to the left and right.

2. Understanding the purpose and the underlying calculations behind Buyside, Sellside and Equilibrium levels.

3. Understanding probability calculations

1. Upon the formation of a new range, the script waits for the price to reach and tap into equilibrium or the 50% level. Status: "⏸" - Inactive

2. Once equilibrium is tapped into, the equilibrium status becomes activated and it waits for either liquidity side to be hit. Status: "▶" - Active

3. If the buyside liquidity is hit, the script adds to the count of successful buyside liquidity occurrences. Similarly, if the sellside is tapped, it records successful sellside liquidity occurrences.

5. Finally, the number of successful occurrences for each side is divided by the overall count individually to calculate the range probabilities.

Note: The calculations are performed independently for each directional range. A range is considered bearish if the previous breakout was through a sellside liquidity. Conversely, a range is considered bullish if the most recent breakout was through a buyside liquidity.

Example - BSL > 55%

-----

What's the range length Filter? What are the underlying calculations?

The range length filter identifies the price distance between buyside and sellside liquidity levels in percentage terms. When enabled, the script only looks for entries when the minimum range length is met. This helps ensure that trades are taken in markets with sufficient price movement.

Calculations:

Range Length (%) = ( ( Buyside Level − Sellside Level ) / Current Price ) ×100

Range Bias Identification:

Bullish Bias: The current range price has broken above the previous external swing high.

Bearish Bias: The current range price has broken below the previous external swing low.

Example - Range length filter is enabled | Range must be above 1%

>: Minimum required range length for entry | %: Current range length percentage in a (Bullish/Bearish) range

-----

What's the day filter Filter, what does it do?

The day filter allows users to customize the session time and choose the specific days they want to include in the strategy session. This helps traders tailor their strategies to particular trading sessions or days of the week when they believe the market conditions are more favorable for their trading style.

Customize Session Time:

Users can define the start and end times for the trading session.

This allows the strategy to only consider trades within the specified time window, focusing on periods of higher market activity or preferred trading hours.

Select Days:

Users can select which days of the week to include in the strategy.

This feature is useful for excluding days with historically lower volatility or unfavorable trading conditions (e.g., Mondays or Fridays).

Benefits:

Focus on Optimal Trading Periods:

By customizing session times and days, traders can focus on periods when the market is more likely to present profitable opportunities.

Avoid Unfavorable Conditions:

Excluding specific days or times can help avoid trading during periods of low liquidity or high unpredictability, such as major news events or holidays.

Increased Flexibility: The filter provides increased flexibility, allowing traders to adapt the strategy to their specific needs and preferences.

Example - Day filter | Session Filter

θ: Session time | Exchange time-zone

-----

What tables are available in this script?

Table Type:

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- OFF: Hides the performance table.

Profit Color:

- Allows users to set the color for representing profit in the performance table, helping to quickly distinguish profitable periods.

Loss Color:

- Allows users to set the color for representing loss in the performance table, helping to quickly identify loss-making periods.

These customizable tables provide traders with flexible and detailed performance analysis, aiding in better strategy evaluation and optimization.

-----

User-input styles and customizations:

To facilitate studying historical data, all conditions and rules can be applied to your charts. By plotting background colors on your charts, you'll be able to identify what worked and what didn't in certain market conditions.

Please note that all background colors in the style are disabled by default to enhance visualization.

-----

How to Use This Algobuilder to Create a Profitable Edge and System:

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker or prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 100 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade value is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

Automation:

- Once you’re confident in your strategy, you can use the automation section to connect the algorithm to your broker or prop firm.

- Trade a fully automated and backtested trading strategy, allowing for hands-free execution and management.

-----

What makes this strategy original?

1. Incorporating direct integration of probabilities into the strategy.

2. Utilizing built-in market structure-based moving averages across various timeframes.

4. Offering both investing and trading strategies, facilitating optimization from different perspectives.

5. Automation for efficient execution.

6. Providing a summary table for instant access to key parameters of the strategy.

-----

How to use automation?

For Traders:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Enter your PineConnector License ID in the designated field.

3. Specify the desired risk level.

4. Provide the Metatrader symbol.

5. Check for chart updates to ensure the automation table appears on the top right corner, displaying your License ID, risk, and symbol.

6. Set up an alert with the strategy selected as Condition and the Message as {{strategy.order.alert_message}}.

7. Activate the Webhook URL in the Notifications section, setting it as the official PineConnector webhook address.

8. Double-check all settings on PineConnector to ensure the connection is successful.

9. Create the alert for entry/exit automation.

For Investors:

1. Ensure the strategy parameters are properly set based on your optimized parameters.

2. Choose "Investing" in the user-input settings.

3. Create an alert with a specified name.

4. Customize the notifications tab to receive alerts via email.

5. Buying/selling alerts will be triggered instantly upon entry or exit order execution.

-----

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

FVG Positioning Average with 200EMA Auto Trading [Pakun]Description

Strategy Name and Purpose

FVG Positioning Average with 200EMA Auto Trading

This strategy uses Fair Value Gaps (FVG) combined with a 200-period Exponential Moving Average (EMA) and Average True Range (ATR) to generate trend-based trading signals. It is designed to help traders identify high-probability entry points by leveraging the gaps between fair value prices and current market prices.

Originality and Usefulness

This script combines multiple indicators to create a cohesive trading strategy that is greater than the sum of its parts. While FVG is a powerful tool on its own, combining it with the EMA and ATR adds layers of confirmation and risk management, enhancing its effectiveness. Here’s how the components work together:

Fair Value Gap (FVG): Identifies gaps in the market where price action has not fully filled, indicating potential reversal or continuation points.

200-period Exponential Moving Average (EMA): Acts as a trend filter to ensure trades are taken in the direction of the overall trend, improving the probability of success.

Average True Range (ATR): Used to filter out insignificant gaps and set dynamic stop-loss levels based on market volatility, enhancing risk management.

Entry Conditions

Long Entry

The close price crosses above the downtrend FVG.

The close price, FVG up average, and down average are all above the 200 EMA, indicating a strong bullish trend.

Short Entry

The close price crosses below the uptrend FVG.

The close price, FVG up average, and down average are all below the 200 EMA, indicating a strong bearish trend.