Cloud X MesoHello there fellow Traders!

Thanks for stopping by, so today I will be covering everything you need to to know about this TradingView strategy.

Below I will discuss everything you need to know about this strategy so you can get a full grasp of what the strategy is, the features, what it does, how it works, the benefits of how this strategy can help you, and the results.

What is Cloud X Meso?

-Cloud X Meso is a strategy that consists of 7 indicators to all line up for total confluence to take a buy or sell once all 6 indicators conditions are met. This strategy does not repaint and doesn't require any technical analysis to be used. The strategy can be used on any timeframe, and any instrument.

-I have optimized many different variations for different types of trading instruments of this strategy ready to be used. The difference of this strategy is that these variations do not need any reoptimization to keep up with recent market conditions since there are hardly any inputs used, which prevents common overfitting problems. The main goal was for this strategy to be automated, as well as plug and play or you can officially consider this as set and forever forget.

What does this strategy do?

-The main goal for this strategy is to catch long or short term trends by waiting for all 7 indicators to line up as well as using customized trading times to trade certain sessions where there is high amounts of volume in the market. This strategy doesn't always need to have a clear trending market, since it can also catch short term trends in choppy markets as well. Overall, the strategy tell you when it buys, sells, and exits after all conditions are met.

How does the strategy work?

-The way that this strategy works is when all of the indicators confluences are met. Next, a buy or sell label will print and the candles colors will color blue or red to show that the trade is in the buy or sell position followed along with a magenta colored line which is the trailing stop to follow the trade until the trade exits from the trailing stop being hit or if the strategies exit condition is met.

-The strategy does have a set Take Profit target since it relies on the trailing stop to end the trade. This is beneficial so you can catch any size of a trend move when the strategy is in high volume market sessions. You catch these trends by customizing the settings to toggle on or off certain indicators, functions, configuring a customized trading time, and toggling on or off certain trading days to make a specific approach for fine tuning a pair to trade in a certain time window with high amounts of volume to catch trending moves whether it be a long or short term trend.

Below I will explain each functionality of the strategy for you to better understand the different ways you can adjust the settings of this strategy.

Backtest Settings:

-You can use these settings to determine a start / end date of what results you would like to see in the strategy tester.

-You can determine the $ amount you would like to see on strategy testers results to be in terms of net profit and max drawdown.

-You can choose whether you want the strategy to take buys only, sells only, or buys and sells.

Automation:

-Compatible with Pine Connectors to fully automate this strategy for MT4/5

-It uses a % based risk when placing trades so you won't have to calculate a proper lot size or dollar amount.

-You can also put the symbol of what that strategy will be trading on so you know what pair its trading.

Custom Trading Times:

-When you customize a trading time for the strategy to trade in, the background will turn blue for that specific time window, and you can use the "Session Exit" function to have trades close once the time window ends when toggled on, or you can have the existing trades close on their own when "Session Exit" is toggled off.

Dynamic Trailing:

-The algorithm uses a volatility based indicator to determine proper stop loss placement depending on how volatile the market is. This will prevent you from guesstimating if your stop loss is too big or too small.

-When Dynamic trailing is off, then the strategy will use a Risk Reward based stop loss to trail everytime the trades hits a new Risk Reward target.

-You can also toggle on or off for the stop loss to go to break even once the trade hits a 1:1 Risk Reward.

Directional Bias Settings:

-This indicator is the main directional bias that uses a multi timeframe function to determine the directional bias, you can also use the Exponential Moving Average as a form of directional bias instead, or you can use both of them to work together to find the directional bias. You can also toggle each one on or off

Entry / Exit Settings:

-This indicator also uses a multi timeframe function but it determines the entry and exit for a trade when all confluences are met. You can also toggle the entry and exit functions on or off.

1 Candle Rule:

-This feature is inspired by No Nonsense Forex (NNFX) the main function of this is if your entry doesn't meet all the entry conditions, then the strategy will wait 1 more candle to meet all the entry conditions to take a trade.

No Trade Zone:

-This feature will uses a Volume based indicator to filter out low volume markets. The candles will turn grey to indicate the algorithm not to take trades, and you can also customize the sensitivity of how strong this indicator will filter out the low volume in the markets.

Indicator functions

Each indicator plays a certain role and also meets certain conditions when a buy or sell trade is placed. I will reveal 3 out of 7 of the indicators used to preserve the uniqueness of this strategy but overall, the logic of this strategies main goal is to ride long or short terms trends while getting dynamic Risk Reward trades.

-The first indicator that the strategy uses an Exponential Moving Average that is customizable, and is used as a form of a filter for either a long or short term directional bias to filter out false signals to help the algorithm trade with the trend.

-The second indicator that the strategy uses is an Oscillator which is the Wavetrend and this indicators functionality for the algorithm is used for the its buy and sell signals to line up with all the other indicators for confluence. This indicator can also be toggled on or off for you own preference

-The third indicator used is the Volume indicator, and this is used to give the other indicators the green light to enter a trade if there are high amounts of volume in the market.

What are the benefits of using this algorithm?

Stress Free Trading:

-Once automated, you will no longer need to stare at the charts all day, as well as trying to execute the trades on time or worried that you missed a setup. Or you can choose to take trades manually when a buy or sell signal comes up

Stress Free Risk Management:

-All you have to do is provide a risk % and the algorithm will do the rest of the work calculating the stop loss, exiting trades, etc. No more needing to find the right lot size, or dollar amount, all in all the strategy will manage the trades for you.

Psychology:

-when you choose to have a systematic trading approach, it eliminates a lot bad habits from human nature

What are the results like?

-I have multiple different variations of results of this strategy, but I will share one of the results.

Here is a screenshot below of what this strategy can do from just one of the variations.

The backtest below was done with another variation on simulating a 100k account risking 0.50% per trade.

Thank you for taking the time to read through this whole guide, and I hope this helped you better understand the strategy.

Search in scripts for "candle"

Strategy: Range BreakoutWhat?

In the price action, levels have a significant role to play. Based on the price moving above/below the levels - the underlying instrument shows some price-action in the direction of breakout/breakdown.

There are plenty of ways level can be determined. Levels are the decision point to take a trade or not. But if we make the level derivation complex, then the execution may get hamper.

This strategy script, developed in PineScript v5, is our attempt at solving this problem at the core by providing this simple, yet elegant solution to this problem.

It's essentially an attempt to Trade Simple by drawing logical (horizontal) lines in the chart and take actions, after multiple associated parameters confirmation, on the breakout / breakdown of the levels.

How?

Let us explain how we are drawing the levels.

We are depending on some of the parameters as described below:

Open Range : During intraday movement, often if prices move beyond a particular level, it exibits more movement in the same swing in same direction. We found out, through our back testing for Indian Indices like NSE:NIFTY , NSE:BANKNIFTY or NSE:CNXFINANCE the first 15m (i.e 09:15 AM to 09:30 AM, IST) is one of such range. For Indian stocks, it is 9:15 to 9:45. And for MCX MCX:CRUDEOIL1! it's 5:00 pm to 6:00 pm. There are our first levels.

PDHCL : Previous Day High, Close, Low. This is our next level

VWAP : The rolling VWAP (volume weighted average price)

In the breakout/breakdown of the Open Range and Previous Day High/Low, we are taking the trade decisions as follows using CEST principle:

C onditions :

If current bar's (say you are in 5m timeframe) closing is broken out the Open Range High or Previous Day High, taken a Buy/Long decision (let's say buying a Call Option CE or selling a Put Option PE or buying the future or cash).

If current bar's (say you are in 5m timeframe) closing is broken down the Open Range Low or Previous Day Low, taken a Sell/Short decision (let's say buying a Put Option CE or selling a Call Option PE or selling the future or cash).

Additionally, and optionally (default ON, one can turn off): we are checking various other associated multiple confirmations as follows:

1. Momentum : Checking 14-period RSI value is more than 50 or less than 50 (all parameters like period, OB, OS ranges are configurable through settings)

2. Current bar's volume is more than the last 20 bars volume average. How much more - that multiplier is also configurable. (default is 1)

3. The breakout candle is bullish (green) or bearish (red).

E ntry :

All of these happens only on the closing of the candle . Means: Non Repainting! .

Clearly in the chart we are showing as green up arrow BO (breakout for buy) and red down arrow BD (breakdown for sell) to take your decision process smooth.

So, on the closing of the decision BO/BD candle we are entering the trade (with a thumping heart and nail biting ...)

S top Loss :

We are relying on the time tasted (last 40 years) mechanism of Average True Range (ATR) of default 14 period. This default period is also configurable.

So for Long trades: the 14 period ATR low band is the SL.

For Short trades: the 14 period ATR high band is the SL.

T arget :

We are depending on the thump rule of 1:2 Risk Reward. It's simple and effective. No fancy thing. We are closing the trade on double the favorable price movement compared to the SL placed. Of course, this RR ratio is confiurable from the settings, as usual.

What's Unqiue in it?

The utter simplicity of this trading mechanism. No fancy things like complex chart pattern, OI data, multiple candlestick patterns, Order flow analysis etc.

Simple level determination,

Marking clearly in the chart.

Making each parameter configurable in Settings and showing tooltip adjacent to the parameter to make you understand it better for your customization,

Wait for the candle close, thus eliminating the chances of repainting menace (as much as possible)

Additional momentum and volume check to trade entry confirmation.

Works with normal candlestick (nothing special ones like HA ...)

Showing everything as a Summary Table (which, again can be turned off optionally) overlaying at the bottom-right corner of the chart,

Optionally the Summary Table can be configured to alert you back (say you get it notified in your email or SMS).

That way, a single, simple, effective trade setup will ease your journey as smooth sail as possible.

Mentions

There are plenty of friends from whom time to time we borrowed some of the ideas while working closely together over last one year.

From tradingview community, we took the spirit of @zzzcrypto123 awesome work done long back (in 2020) as the indicator "ORB - Opening Range Breakout". (We tried to reach him for his explicit consent, unable to catch hold of him).

Some other publicly available materials we have consulted to get the additional checks (like RSI, volume).

Lat word

Use it please and thank you for your constant patronage in following us in this awesome platform. Let's keep growing together.

Disclaimer :

This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

Bull Trend Filtered StochRSI (BTFS)Ride Bull Trends Via Stochastic with Special Rules for Heavy Bullish Bias

TLDR: Long Only Trend Indicator Where you are always entered Long if the stochastic is over the lower band line and the price is above the Donchian Chanel high. Exit when Stochastic RSI is below the lower band.

Indicators:

Filter = Trend/Bullish indicator is Donchian of ema(high) this is set as the highest ema(high, 6) in the last 30 candles. this can be adjusted to fit the market as desired.

**indicator prints green background when the filter condition is satisfied***

Entry Exit = enter when the Stoch RSI is above the given lower trend band. This value is set at 35 but can be adjusted according to risk tolerance and market conditions.

Logic:

this indicator allows a trader to be present during bullish/parabolic trends by only triggering if the close is > than the highest 6 candle average high over the last 30 candles. This filter requires the market to be in a generally bullish posture. If the market is in this condition the stochastic RSI indicator value offers a good gauge of price action and only goes significantly down if price trends below the average range of the rsi period. This filters out noise and keeps a trader from over trading on inconsequential corrections while responding fairly quickly to changes in general trend direction. the response is fast enough to produce an unprofitable amount of false signals if the bull market filter is not implemented. However when used in combination the signals return desirable results in bull trending markets.

Hope this Helps. Happy Trades.

-Snarky Puppy

EMA RSI Strategy

Simple strategy

=============

If the last two closes are in ascending order, the rsi is below 50 and ascending, and the current candle is above 200 ema, then LONG. If the last two closes are in descending order, the rsi is above 50 and descending, and the current candle is below 200 ema, then SHORT.

LONG Exit strategy:

ATR: Last 14 day

Lowest: The lowest value of the last 14 candles

Limit points = (Trade Price - Lowest + ATR) * 100000

trail_points : Limit/2

trail_offset = Limit/2

SHORT Exit strategy:

ATR: Last 14 day

Highest: The higher value of the last 14 candles

Limit points = (Trade Price - Highest + ATR) * 100000

trail_points : Limit/2

trail_offset = Limit/2

Backtest results for the AUDUSD pair gave positive results over the last three months.

I am testing this strategy using a python bot in a real environment this week and will update the results at the end of the week.

Disclaimer

This is not financial advice. You should seek independent advice to check how the strategy information relates to your unique circumstances.

We are not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly by this strategy.

Channels Strategy [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on Bollinger Bands / Keltner Channel price "rebounds" (the idea of price bouncing from one band to another).

The strategy has several customizable options, which allows you to refine the strategy for your asset and timeframe.

You can customize settings for ALL indicators, Bollinger Bands (period and standard deviation), Keltner Channel (period and ATR multiplier) and ATR (period).

- AVAILABLE INDICATORS:

You can pick Bollinger Bands or Keltner Channels for the strategy, the chosen indicator will be plotted as well.

- CUSTOM CONDITIONS TO ENTER A POSITION:

1. Price breaks the band (low below lower band for LONG or high above higher band for SHORT).

2. Same as 1 but THEN (next candle) price closes INSIDE the bands.

3. Price breaks the band AND CLOSES OUT of the band (lower band for LONG and higher band for SHORT).

4. Same as 3 but THEN (next candle) price closes INSIDE the bands.

- STOP LOSS OPTIONS:

1. Previous wick (low of previous candle if LONG and high or previous candle if SHORT).

2. Extended band, you can customize settings for a second indicator with larger values to use it as STOP LOSS, for example, Bollinger Bands with 2 standard deviations to open positions and 3 for STOP LOSS.

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate STOP LOSS.

- TAKE PROFIT OPTIONS:

1. Opposite band (top band for LONGs, bottom band for SHORTs).

2. Moving average: Bollinger Bands simple moving average or Keltner Channel exponential moving average .

3. ATR: you can pick average true ratio from a source (like closing price) with a multiplier to calculate TAKE PROFIT.

- OTHER OPTIONS:

You can pick to trade only LONGs, only SHORTs, both or none (just indicator).

You can enable DYNAMIC TAKE PROFIT, which updates TAKE PROFIT on each candle, for example, if you pick "opposite band" as TAKE PROFIT, it'll update the TAKE PROFIT based on that, on every single new candle.

- Visual:

Bands shown will depend on the chosen indicator and it's settings.

ATR is only printed if used as STOP LOSS and/or TAKE PROFIT.

- Recommendations:

Recommended on DAILY timeframe , it works better with Keltner Channels rather than Bollinger Bands .

- Customization:

As you can see, almost everything is customizable, for colors and plotting styles check the "Style" tab.

Enjoy!

============

ESPAÑOL

============

- Descripción:

Esta estrategia se basa en los "rebotes" de precios en las Bandas de Bollinger / Canal de Keltner (la idea de que el precio rebote de una banda a otra).

La estrategia tiene varias opciones personalizables, lo que le permite refinar la estrategia para su activo y temporalidad favoritas.

Puedes personalizar la configuración de TODOS los indicadores, Bandas de Bollinger (periodo y desviación estándar), Canal de Keltner (periodo y multiplicador ATR) y ATR (periodo).

- INDICADORES DISPONIBLES:

Puedes elegir las Bandas de Bollinger o los Canales de Keltner para la estrategia, el indicador elegido será mostrado en pantalla.

- CONDICIONES PERSONALIZADAS PARA ENTRAR EN UNA POSICIÓN:

1. El precio rompe la banda (mínimo por debajo de la banda inferior para LONG o máximo por encima de la banda superior para SHORT).

2. Lo mismo que en el punto 1 pero ADEMÁS (en la siguiente vela) el precio cierra DENTRO de las bandas.

3. El precio rompe la banda Y CIERRA FUERA de la banda (banda inferior para LONG y banda superior para SHORT).

4. Igual que el 3 pero ADEMÁS (siguiente vela) el precio cierra DENTRO de las bandas.

- OPCIONES DE STOP LOSS:

1. Mecha anterior (mínimo de la vela anterior si es LONGy máximo de la vela anterior si es SHORT).

2. Banda extendida, puedes personalizar la configuración de un segundo indicador con valores más extensos para utilizarlo como STOP LOSS, por ejemplo, Bandas de Bollinger con 2 desviaciones estándar para abrir posiciones y 3 para STOP LOSS.

3. ATR: puedes elegir el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el STOP LOSS.

- OPCIONES DE TAKE PROFIT:

1. Banda opuesta (banda superior para LONGs, banda inferior para SHORTs).

2. Media móvil: media móvil simple de las Bandas de Bollinger o media móvil exponencial del Canal de Keltner .

3. ATR: se puede escoger el average true ratio de una fuente (como el precio de cierre) con un multiplicador para calcular el TAKE PROFIT.

- OTRAS OPCIONES:

Puedes elegir operar sólo con LONGs, sólo con SHORTs, ambos o ninguno (sólo el indicador).

Puedes activar el TAKE PROFIT DINÁMICO, que actualiza el TAKE PROFIT en cada vela, por ejemplo, si eliges "banda opuesta" como TAKE PROFIT, actualizará el TAKE PROFIT basado en eso, en cada nueva vela.

- Visual:

Las bandas mostradas dependerán del indicador elegido y de su configuración.

El ATR sólo se muestra si se utiliza como STOP LOSS y/o TAKE PROFIT.

- Recomendaciones:

Recomendada para temporalidad de DIARIO, funciona mejor con los Canales de Keltner que con las Bandas de Bollinger .

- Personalización:

Como puedes ver, casi todo es personalizable, para los colores y estilos de dibujo comprueba la pestaña "Estilo".

¡Que lo disfrutes!

Crypto BTC Correlation Scalper Gaps StrategyThis strategy is based on the gaps theory.

In this case we have the BTC futures from CME, which acts in a way similar to stocks, and we can have gaps present between close/open session, and also sometimes between same candle due to huge movements intra candle.

At the same time I have combined this with a daily moving average, to help out a bit with the trend, since we are looking at small timeframe like 1-15/30min .

On top of that we have a reverse option, where long = short and viceversa, which can be used with against BTC pairs .

Rule are simple:

For long, we have a long gap and the close of the correlated candle is above daily sma

For short, we have a short gap and the close of the correlated candle is below daily sma

For exit:

For exit, we take the highest highest values for short entry TP, meaning we get the different from the HH and rest the current open candle distance, and use that distance as a TP.

At the same time for long entry, we take the lowest low value and rest current close of the candle to that value, and we get the TP.

Can also be applied this logic for SL aswell but from the test I have found out that exiting based on a reverse condition(when tp is not being hit), gives better results/dd overall.

If you have any questions, please let me know !

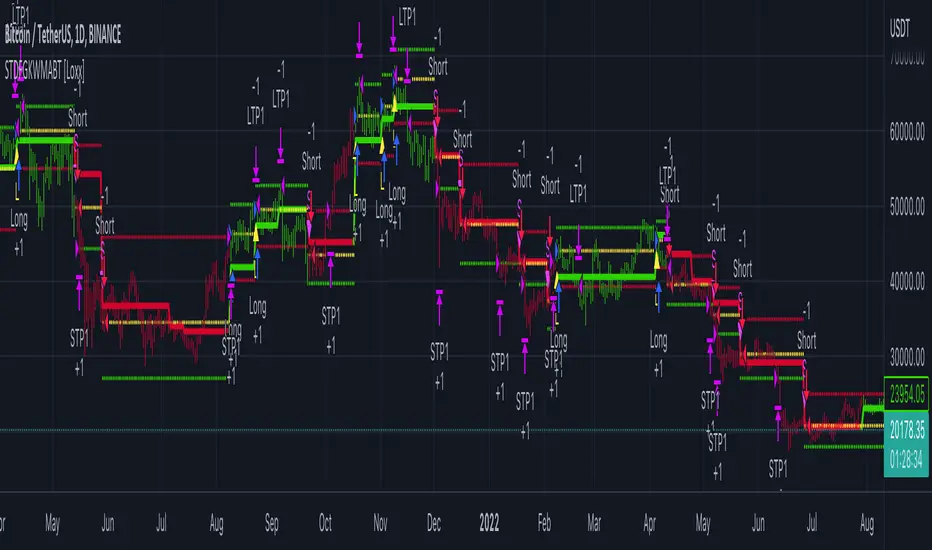

STD-Filtered, Gaussian-Kernel-Weighted Moving Average BT [Loxx]STD-Filtered, Gaussian-Kernel-Weighted Moving Average BT is the backtest for the following indicator

Included:

This backtest uses a special implementation of ATR and ATR smoothing called "True Range Double" which is a range calculation that accounts for volatility skew.

You can set the backtest to 1-2 take profits with stop-loss

Signals can't exit on the same candle as the entry, this is coded in a way for 1-candle delay post entry

This should be coupled with the INDICATOR version linked above for the alerts and signals. Strategies won't paint the signal "L" or "S" until the entry actually happens, but indicators allow this, which is repainting on current candle, but this is an FYI if you want to get serious with Pinescript algorithmic botting

You can restrict the backtest by dates

It is advised that you understand what Heikin-Ashi candles do to strategies, the default settings for this backtest is NON Heikin-Ashi candles but you have the ability to change that in the source selection

This is a mathematically heavy, heavy-lifting strategy. Make sure you do your own research so you understand what is happening here.

STD-Filtered, Gaussian-Kernel-Weighted Moving Average is a moving average that weights price by using a Gaussian kernel function to calculate data points. This indicator also allows for filtering both source input price and output signal using a standard deviation filter.

Purpose

This purpose of this indicator is to take the concept of Kernel estimation and apply it in a way where instead of predicting past values, the weighted function predicts the current bar value at each bar to create a moving average that is suitable for trading. Normally this method is used to create an array of past estimators to model past data but this method is not useful for trading as the past values will repaint. This moving average does NOT repaint, however you much allow signals to close on the current bar before taking the signal. You can compare this to Nadaraya-Watson Estimator wherein they use Nadaraya-Watson estimator method with normalized kernel weighted function to model price.

What are Kernel Functions?

A kernel function is used as a weighing function to develop non-parametric regression model is discussed. In the beginning of the article, a brief discussion about properties of kernel functions and steps to build kernels around data points are presented.

Kernel Function

In non-parametric statistics, a kernel is a weighting function which satisfies the following properties.

A kernel function must be symmetrical. Mathematically this property can be expressed as K (-u) = K (+u). The symmetric property of kernel function enables its maximum value (max(K(u)) to lie in the middle of the curve.

The area under the curve of the function must be equal to one. Mathematically, this property is expressed as: integral −∞ + ∞ ∫ K(u)d(u) = 1

Value of kernel function can not be negative i.e. K(u) ≥ 0 for all −∞ < u < ∞.

Kernel Estimation

In this article, Gaussian kernel function is used to calculate kernels for the data points. The equation for Gaussian kernel is:

K(u) = (1 / sqrt(2pi)) * e^(-0.5 *(j / bw )^2)

Where xi is the observed data point. j is the value where kernel function is computed and bw is called the bandwidth. Bandwidth in kernel regression is called the smoothing parameter because it controls variance and bias in the output.

tvbot Trend Following with Mean Reversion algoDefault settings are for the ETHUSDT 5 min Binance Chart regular candles.

Back test Default settings are 10,000 usd to start, Commission 0.075%, capital deployment per position is 10%, slippage value of 1.

This algo uses the EMA to set the trend line . You are also able to turn the trend line into a range instead of just a static line. The algo uses the VWMA to set the base entry parameters. When a candle closes above or below the VWMA it will record that price and then wait for the VWMA to meet the candle close price. When that happens the Base entry condition is met. (it causes the vwma to create a hook like structure. essentially tell you that the momentum has changed directions.)

The algo will always check to see if the trend line has either breached or has been tested and held. If this condition has been met it will then go to the base entry condition to check to see if the momentum has changed.

There is a mean reversion component in this algo as well. When the price has moved away from the mean(set by user) by a certain amount the algo will start to look for a top or bottom. Once that condition has been met it will then use the base entry condition to look for a change in momentum, but the mean reversion base entry condition uses the HMA to check for a change in momentum.

This algo effectively looks like a hamburger. Mean reversion being the tops and bottoms(bun) and the trend following(beef patty)

STD-Filterd, R-squared Adaptive T3 w/ Dynamic Zones BT [Loxx]STD-Filterd, R-squared Adaptive T3 w/ Dynamic Zones BT is the backtest strategy for "STD-Filterd, R-squared Adaptive T3 w/ Dynamic Zones " seen below:

Included:

This backtest uses a special implementation of ATR and ATR smoothing called "True Range Double" which is a range calculation that accounts for volatility skew.

You can set the backtest to 1-2 take profits with stop-loss

Signals can't exit on the same candle as the entry, this is coded in a way for 1-candle delay post entry

This should be coupled with the INDICATOR version linked above for the alerts and signals. Strategies won't paint the signal "L" or "S" until the entry actually happens, but indicators allow this, which is repainting on current candle, but this is an FYI if you want to get serious with Pinescript algorithmic botting

You can restrict the backtest by dates

It is advised that you understand what Heikin-Ashi candles do to strategies, the default settings for this backtest is NON Heikin-Ashi candles but you have the ability to change that in the source selection

This is a mathematically heavy, heavy-lifting strategy with multi-layered adaptivity. Make sure you do your own research so you understand what is happening here. This can be used as its own trading system without any other oscillators, moving average baselines, or volatility/momentum confirmation indicators.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

What is R-squared Adaptive?

One tool available in forecasting the trendiness of the breakout is the coefficient of determination ( R-squared ), a statistical measurement.

The R-squared indicates linear strength between the security's price (the Y - axis) and time (the X - axis). The R-squared is the percentage of squared error that the linear regression can eliminate if it were used as the predictor instead of the mean value. If the R-squared were 0.99, then the linear regression would eliminate 99% of the error for prediction versus predicting closing prices using a simple moving average .

R-squared is used here to derive a T3 factor used to modify price before passing price through a six-pole non-linear Kalman filter.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included:

Bar coloring

Signals

Alerts

Loxx's Expanded Source Types

Estrategia Larry Connors [JoseMetal]============

ENGLISH

============

- Description:

This strategy is based on the original Larry Connors strategy, using 2 SMAs and RSI.

The strategy has been optimized for better total profit and works better on 4H (tested on BTCUSDT).

LONG:

Price must be ABOVE the slow SMA.

When a candle closes in RSI oversold area, the next candle closes out of the oversold area and the closing price is BELOW the fast SMA = open LONG.

LONG is closed when a candle closes ABOVE the fast SMA.

SHORT:

Price must be BELOW the slow SMA.

When a candle closes in RSI overbought area, the next candle closes out of the overbought area and the closing price is ABOVE the fast SMA = open SHORT.

SHORT is closed when a candle closes BELOW the fast SMA.

*Larry Connor's strategy does NOT use a fixed Stop Loss or Take Profit, as he said, that reduces performance significantly.

- Visual:

Both SMAs (fast and slow) are shown in the chart.

By default, the fast SMA is aqua color, the slow changes between green and red depending on the "trend" (price over slow SMA = bullish, below = bearish).

RSI can't be shown because TradingView doesn't allow to show both overlay and panel indicators, so candles get a RED color when RSI is in OVERBOUGHT area and GREEN when they're on OVERSOLD area to help with that.

Background is colored when conditions are met and a position is going to be open, green for LONGs red for SHORTs.

- Usage and recommendations:

As this is a coded strategy, you don't even have to check for indicators, just open and close trades as the strategy shows.

The original strategy uses a 5 period SMA instead of the 10, and 10/90 for oversold/overbought levels, this has been optimized after the testings and results but feel free to change settings and test by yourself.

Also, the original strategy was developed for daily, but seems to work better en 4H.

- Customization:

As usual I like to make as many aspects of my indicators/strategies customizable, indicators, colors etc., feel free to ask if you feel that something that should be configurable is missing or if you have any ideas to optimize the strategy.

============

ESPAÑOL

============

- Descripción:

Esta estrategia está basada en la estrategia original de Larry Connors, utilizando 2 SMAs y RSI.

La estrategia ha sido optimizada para un mejor beneficio total y funciona mejor en 4H (probado en BTCUSDT).

LONG:

El precio debe estar por encima de la SMA lenta.

Cuando una vela cierra en la zona de sobreventa del RSI, la siguiente vela cierra fuera de la zona de sobreventa y el precio de cierre está POR DEBAJO de la SMA rápida = abre LONG.

Se cierra cuando una vela cierra POR ENCIMA de la SMA rápida.

SHORT:

El precio debe estar POR DEBAJO de la SMA lenta.

Cuando una vela cierra en la zona de sobrecompra del RSI, la siguiente vela cierra fuera de la zona de sobrecompra y el precio de cierre está POR ENCIMA de la SMA rápida = abre SHORT.

Se cierra cuando una vela cierra POR DEBAJO de la SMA rápida.

*La estrategia de Larry Connor NO utiliza un Stop Loss o Take Profit fijo, como él dijo, eso reduce el rendimiento significativamente.

- Visual:

Ambas SMAs (rápida y lenta) se muestran en el gráfico.

Por defecto, la SMA rápida es de color aqua, la lenta cambia entre verde y rojo dependiendo de la "tendencia" (precio por encima de la SMA lenta = alcista, por debajo = bajista).

El RSI no puede mostrarse porque TradingView no permite mostrar tanto los indicadores superpuestos como los del panel, así que las velas obtienen un color ROJO cuando el RSI está en el área de SOBRECOMPRA y VERDE cuando están en el área de VENTA para ayudar a ello.

El fondo se colorea cuando se cumplen las condiciones y se va a abrir una posición, verde para LONGs rojo para SHORTs.

- Uso y recomendaciones:

Como se trata de una estrategia ya programada, ni siquiera hay que comprobar los indicadores, sólo hay que abrir y cerrar las operaciones tal y como muestra la estrategia en el gráfico.

La estrategia original utiliza una SMA de 5 periodos en lugar de 10, y 10/90 para los niveles de sobreventa/sobrecompra, esto ha sido optimizado después de las pruebas y los resultados, pero sé libre de cambiar la configuración y probarla por sí mismo.

Además, la estrategia original fue desarrollada para diario, pero parece funcionar mejor en 4H.

- Personalización:

Como siempre me gusta hacer personalizables todos los aspectos de mis indicadores/estrategias, indicadores, colores, etc., preguntar si notas que falta algo que debería ser configurable o si tienes alguna idea para optimizar la estrategia.

MACD Strategy [Trading Nerd]This Strategy uses a EMA as a trend filter and MACD for entries. The stoploss can be calculated by the last highs/lows or by the ATR.

Entry Conditions

Long:

close price must be above the EMA

MACD-Line crossover MACD-Signal-Line

MACD-Signal- Line mus be below 0

Short:

close price must be below the EMA

MACD-Line crossunder MACD-Signal-Line

MACD-Signal- Line mus be above 0

Exit Conditions

The Stoploss can be set in two different ways:

1. By the calculated ATR value of the entry Candle. This Value can be multiplied with the ATR multiplier for SL .

For Longs: SL = entry Price - ATR * ATR-multiplier

For Shorts: SL = entry Price + ATR * ATR-multiplier

2. By the previous highest high or lowest low (also called Donchain Channels). The lookback length can be changed in the at Lookback length for HH/LL SL .

For Longs: SL = LL of the last X candles

For Shorts: SL = HH of the last X candles

Take Profit

The TP is calculated by the Risk * Risk Reward Ratio . The Risk Reward Ratio can be changed in the Settings. The Risk is the difference of entry price and stoploss price: Risk = absolute(entry price - stoploss price)

For Longs: TP = entry Price + Risk * Risk Reward Ratio.

For Shorts: TP = entry Price - Risk * Risk Reward Ratio.

Risk Management

You can set the Risk % per Trade in the settings. A Value of 2 means that the position size is calculated in a way that at a loosing trade the strategy will only loose 2% of the current capital (initial capital + net profit).

E.g.: The current capital is $1000 and a trade hits the SL. The strategy will only loose $20.

Info for Alerts: Alert message conversion of JSON Strings. You don't need to add any \n or \" to the alert String.

When you create the Alert the Message must be: {{strategy.order.alert_message}}

Swing Trades Validator - The One TraderThis swing trading strategy validator is built on the original strategy taught in my bootcamp for swing traders.

The strategy is simple and follows a trend trading pattern on prices reacting to Exponential Moving Averages over a multiple time-frame analysis.

The details of the strategy are as follows:

- Holding Period : Upto a couple of months

- Time-frames to be analysed : Month - Week - Day

- Trade Execution : Daily Time-frame

Analysis Details:

Step 1 : On the Monthly time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the month.

Step 2 : The price needs to be above the 8ema on the Monthly time-frame.

Step 3 : The 8ema must be above the 20ema on the Monthly time-frame.

The above steps indicate a bullish strength in the instrument on the Monthly time-frame.

Step 4 : On the Weekly time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the week.

Step 5 : The price needs to be above the 8ema on the Weekly time-frame.

Step 6 : The 8ema must be above the 20ema on the Weekly time-frame.

The above steps indicate a bullish strength in the instrument on the Weekly time-frame.

Step 7 : On the Daily time-frame, the candle needs to be bullish with the latest close being higher than the opening price of the day.

Step 8 : The price needs to be above the 8ema on the Daily time-frame.

Step 9 : The 8ema must be above the 20ema on the Daily time-frame.

The above steps indicate a bullish strength in the instrument on the Daily time-frame.

Step 10 : While the 8ema is above the 20ema on the Daily time-frame, the price must be allowed to rise before a pullback is seen towards the moving averages, indicating a bearish move trying to change the trend.

Step 11 : These pullback candles need to form a pattern called the Ring Low with the second pullback candle having a lower high and lower low and the low of the last pullback candle being lesser than or equal to the fat ema on the Daily time-frame.

Step 12 : If the stock is still bullish and the trend is displaying a strength in the underlying bullish direction, then there will be a resumption candle that will have a closing price higher than the previous day's high price.

This trend continuation signal is a confirmation that the instrument will continue in the underlying trend direction and we will be able to enter if this condition is satisfied.

The profit and loss percentages are set at a default 10% as this can be a minimum risk : reward for swing trades on average, but the inputs have been made available to the users in order to adjust the risk : reward to find the most optimum breathing room for each individual stock or instrument. This will give the user a highly custom overview of the strategy on individual instruments based on their volatility and price movements.

The strategy tester will auto back-test this strategy historically and find all the trades that were taken based on this strategy and populate a performance summary.

The most important data in V1.0 of this script are as follows:

1. No. of Trades Taken : We want to see many trades being taken on this strategy in that particular instrument. This shows us a healthy report on the number of winning vs. losing trades.

2. Percentage Profitable : We want to see that this strategy has worked out in the past and is giving us a high probability of return. This in no way an indication that the strategy will definitely work out in the future as well, but gives us an idea of whether or not we should enter this trade.

3. No. of Winning Trades vs. Losing Trades : We would like to see a significantly higher number of winning trades.

4. Avg. # of bars in a trade : This gives us an idea of how long on average we might have to wait to see the results of this strategy either in favor of our reward or against our desired direction. Some trades can be completed in around 15-20 bars on average and some trades have shown to take upto 45 days to reach desired reward. This is in line with our planned holding period, but gives the trader a sense of time and increased level of patience.

The future updates will have more utility of the various elements of the strategy tester and the entire exit strategy will be integrated into the script.

This script is not to be used as a standalone method and must be studied well in order to execute trades. I have not hidden visibility on other time-frames, but since order execution is done on the Daily time-frame, the script must run on the Daily time-frame only.

There are many other factors to be taken into consideration before entering a trade and proper risk management and position sizing rules must be followed.

Our bootcamp participants will use this strategy tester in conjunction with the invite-only Trading Toolkit assigned to them.

The development of this script will be ongoing and all comments and feedback are welcome.

Zendog V3 backtest DCA bot 3commasMAJOR UPDATE:

- Update to Pinescript v5

- MAJOR refactor for the logic of how orders are placed. BO order is placed when the condition is first encountered and we are not in a deal.

The extra SO orders (if based on price movement) are all placed on the next candle after BO order, instead of each being placed one after another.

Take profit (if percentage) and Stop loss are placed on the first candle after BO order because if BO and TP are on the same candle TV does not execute properly.

These changes should improve strategy accuracy when multiple prices are hit by the same candle.

- NEW FEATURE: Support to Stop deal using an external indicator (i.e. stop long deal when RSI > 80)

- NEW FEATURE: Support to trigger Safety orders using an external indicator (i.e. trigger each additional SO when RSI < 10, regardless of price movement)

The price movement logic may be implemented in the indicator that plots start / end signals. The SO size is calculated using the configuration of steps.

- NEW FEATURE: Safety order command for 3commas bot. This is implemented using Add funds in the quote currency (for pair BTCUSDT the quote currency is USDT)

The SO size is calculated using the configuration of steps, for exact order size (and price) use the built-in Steps table.

- NEW FEATURE: Addition of extra columns to the steps table: Required price for TP, Required % change for TP, Required % change for BEP (Breakeven point)

- Update to steps table to remove prices when Safety orders are not based on % price change

- The code is opensource. I will not be able to sustain merges for the script, but feel free to use and develop your own version and ping me on discord to review them

and maybe include in the original script

Hull MA TimeFrame CrossOverHello traders,

Although this strategy is configured on BTCUSDT , with a changing of settings, it can be used on any trading instrument.

Here it is seen, on the 2 hour chart. With Trading Fees included in result (adjust to suit your exchange fees).

The candle crossover is set to Daily timeframe.

That means that the Candle crossover is going to see if todays price is higher than yesterdays price.

If user sets this to 4 hour timeframe, the candle crossover would be when price is higher than the the price 4 hours ago...

The rest is simple, a moving average to detect direction, and an ATR StopLoss (if activated).

There is StopLoss and Take Profit settings which work by percentage.

The periods of the moving average and the ATR can be adjusted, as can the TP % and SL %.

The price is taken from the CLOSE or the OPEN or OHLC4 etc... which can be changed in the settings. OPEN is recommended to avoid repainting.

The moving average also has selectable types (ALMA,SMA,EMA,WMA,HMA)

So if the Price is above the Moving average, and the moving average is above the alternate timeframe value, then a buy is activated

if the Price is below the Moving average, and the moving average is below the alternate timeframe value, then a sell is activated

if OPEN is selected as Price source, then the alternate timeframe value would be the OPEN of the alternate timeframes candle.

the values are all plotted on chart so user can see what is happening when what crosses over what, and then what changes when settings are adjusted.

Have FuN!

if this strategy brings you the epik win......

.... dont forget about me

seaside420 ❤️

Profit Maxima: a crypto strategyThis strategy is designed for those who are looking for long-term positions with low risk and high profitability.

How does it work?

In short, the basis of this strategy is the frequent modeling of the price using regression equations and the estimation of the range of price movements.

The price modeling process starts from the first bars and will be repeated on each bar. This process is performed in each candle based on the data available up to that candle, and data for subsequent bars is not used.

There is also no fixed price model, but it will change from one candle to the next; Therefore, the more candles there are, the larger the statistical population and therefore the quality of the price model increases.

I have also used the concept of scarcity. Bitcoin is the first scarce digital object in the world. Once something becomes scarce enough, it can be used as money. This scarcity gradually increases and affects the price. The entire crypto market also follows Bitcoin.

However, always remember that past results in no way guarantee future performance.

Why this strategy generates a small number of trades?

Preston Pysh believed Bitcoin cycles happen in three phases: the Bull Run, the Correction, and the Reversion to the Mean. He estimates there are about 200,000 blocks per cycle and there are about 144 blocks per day.

Therefore, each cycle of Bitcoin lasts about four years. The entire crypto market follows bitcoin. On the other hand, cryptocurrency is a new phenomenon. They have a limited price history.

This strategy is designed to open a long position at the lowest possible price. In addition, due to the concept of scarcity and its continued impact on prices, trading in the “short” direction is avoided.

The combination of these factors leads to generate a small number of trades. However, you can test it on several different charts to make sure it works properly.

Default settings

{ default_qty_type } = strategy.percent_of_equity

{ default_qty_value } = 3.3

{ commission_value } = 0.1

{ pyramiding } = 3

{ close_entries_rule } = "ANY"

In a simple word, buy (Entry) and sell (take-profit) orders are each done at three different levels. At each level, 3.3% of equity is used (9.9% in total)

0.1% commission is considered for each transaction.

“close_entries_rule” determines the order in which orders are closed. The default is FIFO (first in, first out), but in this strategy, orders are executed in “first in, last out” order. In this way, the lowest buy (Entry) order corresponds to the lowest sell (take profit) order.

Choose the best chart

Charts have a significant impact on the performance of the strategy. As mentioned, the more historical bars there are, the larger the statistical population and therefore the quality of the price model increases.

You can use the Chart Quality panel to choose the appropriate chart:

The ‘Historical Bars’ field shows the number of candles in the chart. Choose the chart of an exchange that has the most historical bars.

The ‘Recommended Chart’ field shows the suggested chart for some symbols.

The “Predictability” field indicates to what extent price movements can be predicted using the model; the higher the “predictability”, the more credible the results of the strategy. "Predictability" indicates that the results of the strategy are reliable or not.

The image below shows the recommended chart for 20 different symbols:

How to use

You don't need automated trading platforms to use it. It can be used by placing simple buy and sell (take-profit) orders manually.

The green and red lines indicate the 'Entry' and 'Profit' levels respectively. If there is no order (buy / sell) active on one of these levels, it will be displayed in gray. The corresponding values are displayed in the Entry & Profit Limits table.

After choosing the appropriate chart, you can use this table to place your orders manually.

Note that trading in the "short" direction is not recommended at all.

Samples

Scalper Helper System===========================================================================

===========================================================================

Description

===========================================================================

===========================================================================

Scalper Helper System combines a series of trade strategies which have been learned and honed in the Jim of All Trades channel.

Paixy has contributed candlestick combination rules, Jonas has shared his deep understanding of Stochastic.

Jim himself has taught clearly on the merits of RSI.

This system attempts to formulate all the notes and rules I have made over the past months.

The system searches for 10 - 15 rules which are divided into bullets and bombs. Bombs relate to momentum, so these signals may not be pinpoint accurate, but they are more often leading to bigger moves.

This initial version is released mainly only to the JOAT community to help continue the development of the idea and to help find

continued improvements.

Special thanks to FiendishFeather for his strategy work, (check out his work to learn how to apply any trading strategy to his back testing harness), and the date filtering snippet and the tip to show this option at the top.

===========================================================================

===========================================================================

The strategy decisions are based on the following general rules:

===========================================================================

===========================================================================

BULLETs are hint to the idea of firing a small sized position into the market, BOMBs are hints to go all in - however this does not mean proper risk management should be forgotten.

Without risk management this and any strategy will lead to failure.

Without risk management this and any strategy will lead to failure.

Without risk management this and any strategy will lead to failure.

Without risk management this and any strategy will lead to failure.

===========================================================================

Bullet1 uses the value of the stochastic and checks for buy/sell cross over on 5m, 8m and 13m chart.

These values should be calculated on a ratio basis ideally.

Bullet2 measures divergence between the printed Stochastic signals.

Bullet3 has been decommissioned.

Bullet4 is an RSI divergence and value indicator.

Bullet5 has been decommissioned.

Bullet6 uses the history of the stochastic buy and sell signals

Bullet7 uses the Scalper Helper Trends for entries by attempting to see how the overall trend is changing. More refinement is needed here.

Bullet8 uses the Scalper Helper Trends on multiple timeframes for entries.

Bullet9 strict buy/sell signals from Stochastic RSI

Bomb1 relies on the Fast, Medium and Slow MA's being correctly lined up as well as the Stochastic, this hints at a more imminent move and so the strategy suggests a quicker entry.

Bomb2 relies on the Fast, Medium and Slow MA's NOT being correctly lined up as well as the Stochastic, and therefore has the luxury of suggesting Limit orders near the local high/low.

Bomb3 looks for two or more Stochastics signals in the same direction and then performs a divergence calculation.

Bomb4 looks a change in the Stochastics signals direction and then performs a divergence calculation.

===========================================================================

===========================================================================

Configuration settings:

===========================================================================

===========================================================================

Users can chose to show mainly buy and/or sell signals and can select a level of strictness. Enabling strict rules will force a multi timeframe comparison of Stochastic analysis.

Users can try different levels for long and short targets for profit and stop loss. This is important because the market does not behave the same going up as it does going down.

The RSI conditional check makes the strategy more selective. This discernment can be applied to bullets or bombs in order to validate entry and exits.

During the bull run and perhaps even in ranging markets, the RSI overbought levels is usually 70-80, but in the bear market we are seeing in Crypto now, a value of 60 is more useful. Try for yourself to see what works for you and feedback in the comments.

An additional indicator, Scalper Helper Trends is recommended to get a quick view on the trend condition (rally, base, down) by viewing the MACD from multiple time frames. Further research is required to know which larger timeframes work best here.

For the 15min chart, 15m, 30m, 45m, 60m, 120m, 240m, 360m, 960m would work well. Note it is not possible to go higher than 1000 at this time.

Whether you use the Scalper Helper trends or not for your own visual confirmation, it is possible to allow this indicator to attempt to read it for you. More research is required to best model the reading of this. For now, it will simply measure the gradient of the number of up versus down colors.

The system can also find entries off the Scalper Helper Trends - but really this, by design is not the best use of Scalper Helper Trends. Although you may prove me wrong so the option is given for you to find buy/sells with your own testing.

Users can chose to use some engulfing candle arrangements to trigger exits and define the length of the 200MA and decide if this should play a part in the filtering of the signals. Similarly, a check can be made to ensure that the first two candles after a signal are behaving as we would expect with the "Wait for 2 closing in the direction of the signal" option. This has a lot of value on the 1min chart.

When Revenge trade is set to true you may re-enter a trade in the same direction as the last one when the last one was stopped out, otherwise you would only be looking for trades in the other direction. We all should not revenge trade, and indeed I have only seen a few cases when it has increased the profitability, however this option remains for now.

The flip opens a new trade in the reverse direction when a signal is given to close a trade, but does not apply to scenarios where stop losses or take profit closed the trade.

Hi-Lo Channel StrategyHaven't seen a strategy quite like it. Buy when Heikin Ashi candle closes above a moving average that is sourced on highs - Sell when Heikin Ashi candle closes above a moving average that is sourced on lows. Moving average length should be between 5 and 20 ideally.

NOTE: the Heikin Ashi close values are calculated when the box is checkmarked. You do not need to view the chart with Heikin Ashi candles enabled on the chart. The buy and sell points of the strategy do not change whether or not you are viewing Heikin Ashi candles on the chart as long as the Heikin Ashi setting is enabled.

[BTCUSD] DinhChienFX [2 orders]* Historical statistics from 2018:

* Strategy will enter 2 orders, Order 2 will appear only when there is Order 1:

- Percent profitable of 1st order: 64.76%.

- Percent profitable of 2nd order: 49.86%.

- Average percent profitable: 57.31%.

- 14 consecutive wins.

- 4 consecutive losses.

Order 1: risk / reward ratio 1/1 used to determine if this rule is effective or not?

Order 2: Appears when there is order 1, Use take-profit and take-loss level of order 1 at Fibonacci 75%.

. * 1st Order conditions:

- Buy: When the ADX index cuts up to 45, check earlier if the closing price has cut up and is above the Upper 2 line, enter the Buy order.

- Sell: when the ADX indicator cuts up to 45, check before that if the closing price has cut down and is above Lower 2 then enter a Sell order.

* How to enter Order 2: When order 1 appears, there are always Stoploss and Takeprofit levels. Draw Fibonacci from take-profit and take-loss prices, Fibonacci retracement level = 75%

----------------

1. Trend identification:

- Channel Keltner:

... Uptrend: when the closing candlestick cuts up and is above the Keltner channel, the Upper Line 2

... Down trend: when the candle closes and falls above the Keltner Line Lower 2

2. Rules of entry:

- Channel Keltner:

... Buy: Candlestick closing price cuts up and above the Keltner Upper 2.

... Sell: The closing price of the candle cuts down and is lower than the Keltner Below 2.

ADX indicator:

... Buy: The ADX value crossed to 45 and the close of the candle was higher than Keltner Upper 2.

... Sell: ADX value cuts to 45 and the close of the candle is lower than Keltner Below 2.

3. Stoploss and Profit = atr (20) * 2.

NIKI MSS BANKNIFTYThis is the strategy version of my old indicator NIKI BANKIFTY. It is more suitable for day trading with a 5 min chart. It is more profitable in BANKNIFTY future. It is based on multiple Supertrend, moving average, Donchain channel, and linear regression. The background color indicates the main trend and the color of the candle represents a short-term trend. The label with TA and SL represents more profitable entry positions. The label RE: LE and RE: SE stands for re-entry positions or signals with less accuracy. Consider the direction of the linear regression line to take trades on re-entry positions. The yellow candle indicates the entry and the blue candle represents the target or stop-loss.

The backtest results are based on BANKNIFTY last year's data. It has an initial capital of 100000 and the size of the lot is 1. The target is 0.3% and stop-loss is 1.5%. It exactly not following the stop loss, the trade will exit based on the Donchain channel breakout. It appears on the chart as a blue candle. The commission paid is 20 cash per trade and the slippage is 5 ticks per trade. Some of the Indian broker's commission is only 10 cash per trade. Adjust the commission as per your broker. Trades are conducted based on the intraday time in India set from 9.20 am to 2.25 pm. All positions will get square off at 3.00 pm. It will execute a maximum of 4 trades per day. All other parameters are suitable for Robo trading with Indian stock brokers.

Contact us using the link given below to obtain access to this indicator.

London Breakout/Session GBP/USD Forex DaytradeThis is a forex strategy suited for day traders, specialized in the london breakout session

The key elements for this strategy are the specific london time session, together with an exit time(before asian trade/at the end of new york session).

At the same time, as logic elements we only use price action inside like :

For long we have 3 ascending candles, and for short we have 3 descending candles.

For exit we have both TP/SL based on price percentage movement, or we exit if we reach the end of the day.

If you have any questions message me in private !

CRYPTO HA Strategy money maker long termToday I bring you another amazing strategy.

Its made of 2 EMA in this case 50 and 100.

At the same time, internaly for candles we calculate the candles using the HA system ( while still using in live the normal candles). This way we can assure that even if we use HA candles, we avoid repainting, and its legit.

We first calculate the HA candles based on the EMA 50 values, and after that , we use that candle properties to apply to EMA 100.

Once we have that, for entries we have the next conditions :

sell = o2 > c2 and o2 < c2 and time_cond

buy = o2 < c2 and o2 > c2 and time_cond

For sell : Our open from HA 100 is bigger than Close from ha 100, and the previous open is smaller than previous close

For long : Our open from ha 100 is smaller than close from ha 100 and the previous open is bigger than previous close.

Then we have 2 options :

If we wnat to go only long , which is my prefered version ,or the original one where we go both long and short.

I found that the best results are in general around bigger timeframes, 1h+ , 3h works the best so far on my tests.

For exit we have 2 versions :

1 lets say we had a long signal, as soon as we have a short signal we close the trade. Viceversa for short.

2. Is based on price % movement. In this case I use 7.5% price movement of asset.

We have no TP in use for this system.

For the purpose of this test I use 10.000 $ account. For test I use 100% of it, without any leverage.

I use the SL based on price movement , which is a very risky tool, since it can fluctuate even at 20-30% of our capital.

For comission I used 0.1% for each deal, and a slippage of 5 points.

Be cautious with this system !

If you have any questions , message me.

Parabolic SAR Swing strategy GBP JPY Daily timeframeToday I bring you a new strategy thats made of parabolic sar. It has optmized values for GBPJPY Daily timeframe chart.

It also has a time period selection, in order to see how it behave between selected years.

The strategy behind it is simple :

We have an uptrend , (the psar is below our candles) we go long. We exit when our candle crosses the psar value.

The same applies for downtrend(the psar is above our candles), where we go short. We exit when our candle cross the psar value.

Among the basic indicators, it looks like PSAR is one of the best canditates for swing trading.

If you have any questions, please let me know.

2HLA very simple, almost naive strategy, in which you buy on the lowest of the two previous candles and sell at the highest of the two previous candles. You can configure these highest and lowest lenght, in some assets two is too small of a number to make profit. You can also configure to exit the position after X, and I found that 7 (which is a week of working days) is a good number for that.

This is strategy is intended to be used as a swing trade. Your capital needs to be high enough so that it can pay the operaitonal costs, and reach it's target with a reasonable profit.

Since this is a volatility based strategy, assets that are more liquid won't work properly.