Multi Indicators v1 - 20 50 200 EMA/SMA, Bollinger Bands, VWAPMulti Indicators v1

20 50 200 EMA/SMA, Bollinger Bands, VWAP

These can be turned on and off

I'll be adding to this multi indicator in future updates

Search in scripts for "indicators"

Multi Indicators- MA, EMA, MA Cross, Parabolic SarMulti Indicators

- 3 Simple Moving Average

- 3 Exp Moving Average

- Cross of Moving Averages

- Parabolic SAR

All indicators in one!All indicators in one!

Hull MA (2 colors) + Bollinger Bands + 6 EMA + 50 SMA + 200 SMA + Parabolic SAR + SUPER TREND (2 colors) + Doji signals (yellow)

EMA Indicators with BUY sell SignalCombine 3 EMA indicators into 1. Buy and Sell signal is based on

- Buy signal based on 20 Days Highest High resistance

- Sell signal based on 10 Days Lowest Low support

Input :-

1 - Short EMA (20), Mid EMA (50) and Long EMA (200)

2 - Resistance (20) = 20 Days Highest High line

3 - Support (10) = 10 Days Lowest Low line

Volume Flow Indicator [LazyBear]VFI,introduced by Markos Katsanos, is based on the popular On Balance Volume (OBV) but with three very important modifications:

* Unlike the OBV, indicator values are no longer meaningless. Positive readings are bullish and negative bearish.

* The calculation is based on the day's median (typical price) instead of the closing price.

* A volatility threshold takes into account minimal price changes and another threshold eliminates excessive volume.

A simplified interpretation of the VFI is:

* Values above zero indicate a bullish state and the crossing of the zero line is the trigger or buy signal.

* The strongest signal with all money flow indicators is of course divergence.

I have exposed options to plot a signal EMA. All parameters are configurable.

Markos suggests using 0.2 coeff for day trading and 0.1 for intra-day.

More info:

www.precisiontradingsystems.com

Indicator: Relative Volume Indicator & Freedom Of MovementRelative Volume Indicator

------------------------------

RVI is a support-resistance technical indicator developed by Melvin E. Dickover. Unlike many conventional support and resistance indicators, the Relative Volume Indicator takes into account price-volume behavior in order to detect the supply and demand pools. These pools are marked by "Defended Price Lines" (DPLs), also introduced by the author.

RVI is usually plotted as a histogram; its bars are highlighted (black, by default) when the volume is unusually large. According to the author, this happens if the indicator value exceeds 2.0, thus signifying that a possible DPL is present.

DPLs are horizontal lines that run across the chart at levels defined by following conditions:

* Overlapping bars: If the indicator spike (i.e., indicator is above 2.0 or a custom value)

corresponds to a price bar overlapping the previous one, the previous close can be used as the

DPL value.

* Very large bars: If the indicator spike corresponds to a price bar of a large size, use its

close price as the DPL value.

* Gapping bars: If the indicator spike corresponds to a price bar gapping from the previous bar,

the DPL value will depend on the gap size. Small gaps can be ignored: the author suggests using

the previous close as the DPL value. When the gap is big, the close of the latter bar is used

instead.

* Clustering spikes: If the indicator spikes come in clusters, use the extreme close or open

price of the bar corresponding to the last or next to last spike in cluster.

DPLs can be used as support and resistance levels. In order confirm and refine them, RVI is used along with the FreedomOfMovement indicator discussed next.

Freedom of Movement Indicator

------------------------------

FOM is a support-resistance technical indicator, also by Melvin E. Dickover. FOM is the ratio of relative effect (relative price change) to the relative effort (normalized volume), expressed in standard deviations. This value is plotted as a histogram; its bars are highlighted (black, by default( when this ratio is unusually high. These highlighted bars, or "spikes", define the positioning of the DPLs.

Suggestions for placing DPLs are the same as for the Relative Volume Indicator discussed above.

Note that clustering spikes provide the strongest DPLs while isolated spikes can be used to confirm and refine those provided by the Relative Volume Indicator. Coincidence of spikes of the two indicator can be considered a sign of greater strength of the DPL.

More info:

S&C magazine, April 2014.

I am still trying these on various instruments to understand the workings more. Don't forget to share what you learn -- any use cases / ideal scenarios / gotchas, would love to hear them all.

3 new Indicators - PGO / RAVI / TIIMy "to-publish" list is getting too big, so decided to push out 3 indicators in the same chart

Feel free to "make mine" and use :) Leave a comment on what you think.

Pretty Good Oscillator

----------------------------------------

This indicator, by Mark Johnson, measures the distance of the current close from its N-day simple moving average, expressed in terms of an average true range (see Average True Range) over a similar period. So for instance a PGO value of +2.5 would mean the current close is 2.5 average days' range above the SMA.

Johnson's approach was to use it as a breakout system for longer term trades. If the PGO rises above 3.0 then go long, or below -3.0 then go short, and in both cases exit on returning to zero (which is a close back at the SMA). Indicator marks all these areas (3/-3/0)

Rapid Adaptive Variance Indicator

---------------------------------------------------------

RAVI is a simple indicator, by Tushar Chande, to show whether a stock is trending or not. Unlike ADX, RAVI measures only the trend intensity, it doesn't distinguish which way the trend is going. Rising RAVI shows the beginning of a trend or an increase in trend intensity, a decreasing slope signifies decreasing intensity. Also, RAVI often reacts more quickly and exhibits a more pronounced curve than ADX.

The standard values for daily charts are 7 and 65. For hourly charts, the most common averaging periods are 12 and 72 or 24 and 120.

The signal lines suggested are from +/- 0.3% to +/-1%. I haven't added any markings as these signals are instrument-specific. I suggest doing some back testing and adding these accordingly.

Trend Intensity Index

--------------------------------------

TII, by M. H. Pee, measures the strength of a trend, by looking at what proportion of the past "n" days prices have been above or below the level of today's "x"-day simple moving average. You can configure "n" via options page. "x" is calculated as "2 times n".

TII moves between 0 and 100. A strong uptrend is indicated when TII is above 80. A strong downtrend is indicated when TII is below 20.

Pee recommended entering trades when levels of 80 on the upside or 20 on the downside are reached. Indicator marks these lines for easy reference.

[2022]Volume Flow v3 with alertsIndicators are an essential part of technical analysis of cryptocurrency. Their main function is to predict market direction based on historic price, cryptocurrency volume and other information. There are several types of crypto indicators illustrating various parameters (trend, volatility, volume, momentum, etc.) but in this article we will look at volume indicators.

Volume indicators demonstrate changing of trading volume over time. This information is very useful as crypto trading volume displays how strong the current trend is. For example, if the price goes up and the volume is high then the trend is strong and will more likely last longer. There are various volume indicators, but we’ll talk about the most popular ones, such as:

On Balance Volume

Accumulation/Distribution Line

Money Flow Index

Chaikin Oscillator

Chaikin Money Flow

Ease of Movement

Gold Option Signals with EMA and RSIIndicators:

Exponential Moving Averages (EMAs): Faster to respond to recent price changes compared to simple moving averages.

RSI: Measures the magnitude of recent price changes to evaluate overbought or oversold conditions.

Signal Generation:

Buy Call Signal: Generated when the short EMA crosses above the long EMA and the RSI is not overbought (below 70).

Buy Put Signal: Generated when the short EMA crosses below the long EMA and the RSI is not oversold (above 30).

Plotting:

EMAs: Plotted on the chart to visualize trend directions.

Signals: Plotted as shapes on the chart where conditions are met.

RSI Background Color: Changes to red for overbought and green for oversold conditions.

Steps to Use:

Add the Script to TradingView:

Open TradingView, go to the Pine Script editor, paste the script, save it, and add it to your chart.

Interpret the Signals:

Buy Call Signal: Look for green labels below the price bars.

Buy Put Signal: Look for red labels above the price bars.

Customize Parameters:

Adjust the input parameters (e.g., lengths of EMAs, RSI levels) to better fit your trading strategy and market conditions.

Testing and Validation

To ensure that the script works as expected, you can test it on historical data and validate the signals against known price movements. Adjust the parameters if necessary to improve the accuracy of the signals.

CCI-RSI MR Indicators:

Bollinger Bands (20 period, 2σ)

RSI (14 period) and Simple moving average of RSI (5 period)

CCI (20 period)

SMA (5 period)

Entry Conditions:

Buy when:

Swing low (5) should be lower than the highest of lower BB (3 periods)

Both RSI crossover RSI_5 and CCI crossover -100 should have happened within last 3 candles (including the current candle)

Once all the above conditions are met, the close should be higher than SMA (5) within the next 3 candles

After condition 3 is satisfied, we enter the trade at next candle’s open

Stop loss will be at 1 tick lower than previous swing low

Sell when:

Swing high (5) should be higher than the lowest of upper BB (3 periods)

Both RSI crossunder RSI_5 and CCI crossunder 100 should have happened within last 3 candles (including the current candle)

Once all the above conditions are met, the close should be lower than SMA (5) within the next 3 candles

After condition 3 is satisfied, we enter the trade at next candle’s open

Stop loss will be at 1 tick higher than previous swing high

Exit Conditions:

Since it’s mean reversion strategy we’ll be having only 2 target exits with a trailing stop loss after target price 1 is achieved.

Target exit price 1 & 2 are decided based on the risk ‘R’ for each trade

Depending on the instrument and time frame a trailing stop loss of 0.5R or 1R has opted.

A stop limit is placed @Entry_price +- 2*ATR(20) to offset the risk of losing significantly more than 1xR in a trade

Gaussian Acceleration ArrayIndicators play a role in analyzing price action, trends, and potential reversals. Among many of these, velocity and acceleration have held a significant place due to their ability to provide insight into momentum and rate of change. This indicator takes the old calculation and tweaks it with gaussian smoothing and logarithmic function to ensure proper scaling.

A Brief on Velocity and Acceleration: The concept of velocity in trading refers to the speed at which price changes over time, while acceleration is the rate of change(ROC) of velocity. Early momentum indicators like the RSI and MACD laid foundation for understanding price velocity. However, as markets evolve so do we as technical analysts, we seek the most advanced tools.

The Acceleration/Deceleration Oscillator, introduced by Bill Williams, was one of the early attempts to measure acceleration. It helped gauge whether the market was gaining or losing momentum. Over time more specific tools like the "Awesome Oscillator"(AO) emerged, which has a set length on the datasets measured.

Gaussian Functions: Named after the mathematician Carl Friedrich Gauss, the Gaussian function describes a bell-shaped curve, often referred to as the "normal distribution." In trading these functions are applied to smooth data and reduce noise, focusing on underlying patterns.

The Gaussian Acceleration Array leverages this function to create a smoothed representation of market acceleration.

How does it work?

This indicator calculates acceleration based the highs and lows of each dataset

Once the weighted average for velocity is determined, its rate of change essentially becomes the acceleration

It then plots multiple lines with customizable variance from the primary selected length

Practical Tips:

The Gaussian Acceleration Array offers various customizable parameters, including the sample period, smoothing function, and array variance. Experiment with these settings to tailor it to preferred timeframes and styles.

The color-coded lines and background zones make it easier to interpret the indicator at a glance. The backgrounds indicate increasing or decreasing momentum simply as a visual aid while the lines state how the velocity average is performing. Combining this with other tools can signal shifts in market dynamics.

Parabolic Scalp Take Profit[ChartPrime]Indicators can be a great way to signal when the optimal time is for taking profits. However, many indicators are lagging in nature and will get market participants out of their trades at less than optimal price points. This take profit indicator uses the concept of slope and exponential gain to calculate when the optimal time is to take profits on your trades, thus making this a leading indicator.

Usage:

In essence the indicator will draw a parabolic line that starts from the market participants entry point and exponentially grows the slope of the line eventually intersecting with the price action. When price intersects with the parabolic line a take profit signal will appear in the form of an x. We have found that this take profit indicator is especially useful for scalp trades on lower timeframes.

How To Use:

Add the indicator to the chart. Click on the candle which the trade is on. Click on either the price which the trade will be at, or at the bottom of the candle in a long, or the top of a candle in a short. Select long or short. Open the settings of the indicator and adjust the aggressiveness to the desired value.

Settings:

- Start Time -- This is the bar in which your entry will be at, or occured at and the script will ask you to click on the bar with your mouse upon first adding the script.

- Start Price -- This is the price in which the entry will be at, or was at and the script will ask you to click on the price with your mouse upon first adding the script.

- Long/Short -- This is a setting which lets the script know if it is a long or a short trade, and the script will ask you to confirm this upon first adding it to the chart.

- Aggressiveness -- This directly affects how aggressive the exponential curve is. A value of 101 is the lowest possible setting, indicating a very non-aggressive exponential buildup. A value of 200 is the highest and most aggressive setting, indicating a doubling effect per bar on the slope.

Pre-Market PillarsIndicators that displays where to enter and exit on pre market and low cap stocks.

Inspired by Ross Cameron strategy.

Alson Chew PAM EXE and Mother BarIndicators for strategies taught by Alson Chew's Price Action Manipulation (PAM) course

Two functions.

First it identifies EXE bars (Pin, Mark, Icecream bars).

Second it identifies Mother bars and draws an extension line for 6 bars.

Applicable to all time frames and can customise how many signals to show.

To be used in conjunction with trading strategies like

- 20 SMA, 50 SMA, 200 SMA FS formation

- Force Bottom, Force Top FS formation

- UR1 and DR1 using EXE Bar

Indicators OverviewThis Indicator help you to see whether the price is above or below vwap, supertrend. Also you can see realtime RSI value.

You can add upto 15 stock of your choice.

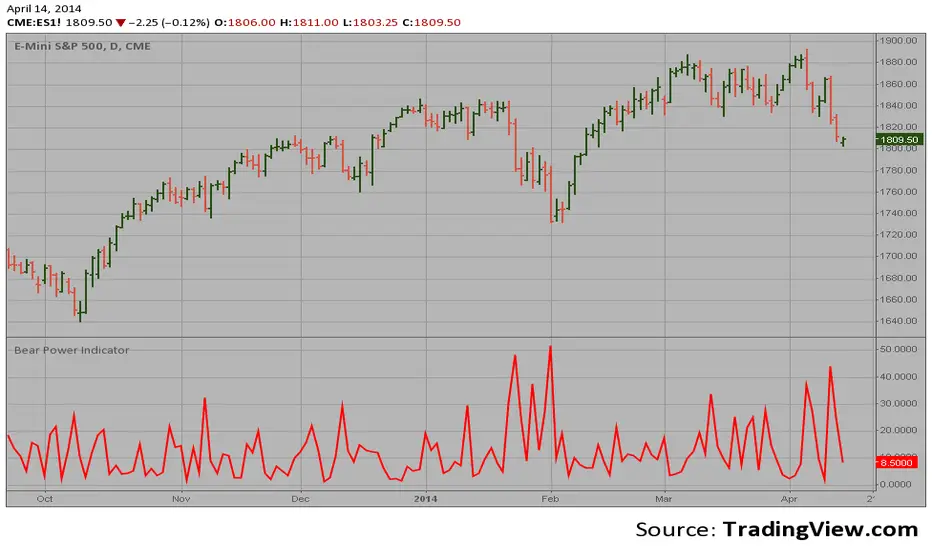

Bear Power Indicator Hi

Let me introduce my Bear Power Indicator script.

To get more information please see "Bull And Bear Balance Indicator"

by Vadim Gimelfarb.

Gei-IndicatorFor trading and for fundaTradingView, combining three critical layers of market data into a single, high-level summary.

Key Features:

Fundamental Analysis: It pulls real-time financial data (P/E Ratio, Free Cash Flow, Revenue, EBIT, and Dividend Yield) to evaluate the company's health. It even includes a "Tech Mode" toggle to adjust valuation expectations for growth stocks.

Technical Indicators: It monitors price momentum and trend direction using the RSI (14) and a Moving Average crossover (MA20/MA50).

Market Benchmarking: It calculates and displays the Year-To-Date (YTD) performance of the SPY (S&P 500 ETF), allowing you to see at a glance if the current stock is outperforming the broader market.

Dynamic UI: All data is neatly organized in a color-coded table (Green/Orange/Red) at the top-right of your chart, making it easy to perform a "quick health check" without leaving the main price action.mental analysis

[TehThomas] - Order Blocks█ OVERVIEW

This Order Blocks indicator identifies institutional-level support and resistance zones using fractal pattern recognition combined with Fair Value Gap (FVG) filtering. Order blocks represent areas where large institutional orders have been placed, creating significant price reactions when retested. This indicator uses a 5-bar fractal pattern to detect market structure breaks and highlights the last bearish or bullish candle before a strong impulse move.

█ KEY FEATURES

- Fractal-Based Detection: Uses 5-candle fractal patterns to identify key market structure highs and lows

- FVG Filtering: Optional Fair Value Gap confirmation ensures order blocks are followed by true market imbalances

- Automatic Mitigation: Order blocks are automatically removed when price breaks through them

- Overlap Prevention: Prevents cluttered charts by avoiding overlapping order block zones

- Customizable Display: Full control over colors, labels, line heights (body/wick), and maximum blocks shown

- Dual Polarity: Detects both bullish (OB+) and bearish (OB-) order blocks independently

█ HOW IT WORKS

The indicator scans price action for fractal patterns where the middle candle forms a local extreme (highest high or lowest low among 5 bars). When price breaks above a fractal high or below a fractal low, the script identifies the last opposing candle in the impulse move as the order block.

For bearish order blocks, it finds the highest bullish candle before a fractal low is broken, marking institutional selling pressure. For bullish order blocks, it locates the lowest bearish candle before a fractal high is breached, indicating institutional buying.

When FVG filtering is enabled, the indicator confirms that a Fair Value Gap (a 3-candle imbalance where price leaves an unfilled gap) occurred within the specified distance from the order block. This combination increases the probability that institutional traders are present in these zones.

█ SETTINGS

Bullish Order Block Settings

- Show/hide bullish order blocks

- Customize fill color and border color

- Toggle OB+ label display

Bearish Order Block Settings

- Show/hide bearish order blocks

- Customize fill color and border color

- Toggle OB- label display

Label Settings

- Label size: Tiny, Small, Normal, or Large

- Label text color customization

General Settings

- Bars Back to Check (10-200): Lookback period for order block detection

- Filter by FVG: Requires Fair Value Gap confirmation

- Max Bars Between OB and FVG (1-6): Distance tolerance for FVG filtering

- Line Height: Choose between Body or Wick for order block boundaries

- Prevent Overlapping OBs: Avoids drawing overlapping zones

- Max Order Blocks to Display (1-50): Limits active blocks on chart

- Length of Boxes (10-100): Horizontal projection length

█ HOW TO USE

1. Add the indicator to your TradingView chart

2. Configure settings based on your trading timeframe and style

3. Watch for OB+ labels (bullish order blocks) as potential support zones where price may bounce

4. Watch for OB- labels (bearish order blocks) as potential resistance zones where price may reverse

5. Wait for price retracement to the order block zone before taking entries

6. Use confirmation signals like volume spikes or reversal patterns at the order block

7. Place stop loss just outside the order block boundary to manage risk

8. Monitor mitigation: Order blocks disappear when price breaks through them completely

█ TRADING STRATEGY EXAMPLES

Bullish Order Block Strategy

Wait for a market structure shift from bearish to bullish. When price creates a bullish impulse breaking a fractal high, identify the OB+ zone. Enter long positions when price retraces to test the bullish order block, placing stop loss 10-20 pips below the zone's low. Target previous highs or resistance levels.

Bearish Order Block Strategy

Monitor for market structure shift from bullish to bearish. After price creates a bearish impulse breaking a fractal low, locate the OB- zone. Enter short positions when price retraces to test the bearish order block, placing stop loss 10-20 pips above the zone's high. Target previous lows or support levels.

FVG-Confirmed Entries

Enable FVG filtering to only display order blocks validated by Fair Value Gaps. These aligned setups increase probability as they combine institutional order placement with market inefficiencies. Trade retracements to these high-confluence zones for better risk-reward ratios.

█ IDEAL FOR

- ICT Traders: Follows Inner Circle Trader methodology for institutional order flow

- Smart Money Concepts: Tracks where large players place orders

- Swing Traders: Identifies key support/resistance for multi-day holds

- Price Action Traders: Pure chart-based approach without lagging indicators

- Breakout Traders: Confirms structure breaks with fractal patterns

- Forex, Crypto, and Stock Markets: Works on all liquid markets and timeframes

█ TECHNICAL SPECIFICATIONS

- Max Boxes: 500

- Max Labels: 500

- Detection Method: 5-bar fractal pattern recognition

- Mitigation Logic: Automatic removal when price breaks order block boundaries

- Time Projection: Uses time offset calculations for box extension

- Array Management: Dynamic array cleanup to prevent memory issues

█ NOTES & DISCLAIMERS

- Order blocks work best when combined with overall market context and trend analysis

- Not all order blocks result in price reversals; use proper risk management

- FVG filtering may reduce the number of signals but increases quality

- Fractal patterns require 5 bars to form, causing a 2-bar delay in detection

- Works optimally on higher timeframes (4H, Daily) for institutional footprints

- This indicator does not guarantee profitable trades; always use stop losses

- Past performance of order blocks does not predict future results

- Compatible with other ICT concepts like liquidity sweeps and market structure

ST: MA E BB LEVELSThis indicator is designed for intraday traders who need to visualize key Dynamic Support and Resistance levels from higher timeframes (Daily and Weekly) directly on their current chart.

Unlike standard moving average indicators that plot historical lines, this script projects forward-looking target lines extending from the current price action into the future. It is ideal for identifying potential reversal zones or profit targets based on institutional anchors.

Consecutive count backtester / Flowly Indicators- Overview

Consecutive counting is a simple method to mechanically define trending states to the upside and downside. Consecutive counts are calculated by taking reference price level (e.g. close 4 candles ago) and count closes above/below it up to a maximum count that resets the consecutive count back to 1. This tool provides the means to backtest each count by measuring % change in price after each count (e.g. % gain 2 candles after a given count).

Users can define reference source that starts the consecutive count (e.g. close 4 candles ago), maximum count where counter resets (e.g. after 9th count) and backtesting period (e.g. price change 2 candles after count).

Filters add extra conditions that must be met on the consecutive count to qualify as valid, which are also reflected on the backtest metrics. The counts can be refined using the following filters:

- RSI above/below X

- Price above/below/at moving average of choice

- Relative volume above/below X

Average gain corresponding to each count as they occur can be toggled off for less clutter. Average price change can also be visualized using candle color. Colors, gradient and table/label sizes are fully customizable.

- Practical guide

Example #1: Identify reversal potential

Consecutive counting is a simple yet effective method to for detecting reversals, for which 7-9 counts are traditionally used. Whether that holds true or not can now be put through a test with different variations of the method as well as using additional filters to improve the probability of a turn.

Example #2: Identify trend following potential

Consecutive counts can also have utility value for trend following. When historical short term change is to the downside, expect downside, when to the upside, expect upside.

Auto-magnifier / Flowly Indicators- Overview

Auto-magnifier shows a lower timeframe view of candles and volume bars inside any main timeframe candle by zooming into it. Candles and volume bars as they develop are shown chronologically from left to right. By default, magnifier is triggered when less than 3 candles are visible on the chart.

By default, 20 lower timeframe candles are displayed by splitting main timeframe into 20 parts. The amount of candles displayed is a target rate, meaning the script will use a lower timeframe that has the closest match to 20 candles and therefore will vary a bit. Users can override automatic timeframe calculation and opt in to display any specific lower timeframe or adjust amount of candles shown (e.g. 20 -> 30 candles) per each main timeframe candle.

Example

Main timeframe set to 30 minute, candles displayed set to 20 -> Magnifying using 2 minute candles (30 minute/20 candles = 1.5 min, rounded to 2 min)

Main timeframe set to 30 minute, override set to 5 minutes -> Displaying 5 minute candles

Size of volume bars is calculated using relative volume (volume relative to volume SMA20), lowest bar representing relative volume values of under or equal to 1x the moving average and from there onwards progressively growing.

- Limitations and considerations

Amount of candles shown might flow over from the background on smaller screen sizes, in which case you would want to decrease the amount shown. Opposite is true for bigger screens, this value can be increased as more candles fit.

This indicator involves a lot of tricks with text elements to make it work automatically by zooming in. Size of wicks, bodies and volume bars are calculated by adding more text elements on big candles and less text elements on smaller candles. This means the displayed candles won't be a 100% match, but a rather a fair representation of the view, e.g. candle is green = lower timeframe candle is green, candle has a big wick = lower timeframe candle has a big wick (but not a 100% match).

Example

Magnified lower timeframe chart vs. Actual lower timeframe chart

Most mismatch will be found on the price levels where lower timeframe candles are shown, which is sacrificed for the sake of getting a better readability on the overall shape of lower timeframe price action. Users can alternatively optimize calculations for more accuracy, giving a better representation of the price levels where candles truly originated. This typically comes with the cost of worse readability however.

Example

Optimized for readability vs. Optimized for accuracy

- Visuals

All visual elements are fully customizable.

Broad market index / Flowly Indicators- Overview

Broad market index is a market breadth based oscillator, depicting broad market trend by analysing ratio between symbols moving up and symbols moving down in a given market. When market breadth is positive, more symbols are going up and when negative, more symbols are going down. As markets tend to correlate, broad market trend dictates likely path for all individual symbols that make up the market.

This tool provides market breadth for US equities (based on NYSE advancers - decliners) and ability to build two custom breadth baskets with up to 39 symbols included in each. Market breadth can be customized with variety of smoothing options, weighting and threshold modes to find most optimal rules for trend following. Performance of the model is reflected on metrics showing percentage of up/down moves during bullish/bearish states.

Example

↑ 63% = 63% of price moves during positive breadth state are to the upside

↓ 59% = 59% of price moves during negative breadth state are to the downside

Breadth state is colorized on line and chart according to its state (negative/positive/equilibrium) and direction (trending up/down). Upper and lower bands depict historical turning points in breadth for identifying extremes in broad market trend. Triangles mark breadth thrusts, in other words abnormally large moves in breadth at either upper or lower extreme. Breadth thrusts can serve as early signs of broad market trend reverting.

- Concept and features

By default, market breadth is calculated based on NYSE advancers - decliners, usable for all major indices that depict broad markets in US equities (SP500, QQQ, IWM). Users can also build 2 custom breadth baskets consisting of up to 39 symbols for defining broad market on other asset classes, such as cryptocurrencies. Custom baskets are suitable for any chart that fairly represents a market as a whole.

Example

Basket consisting of cryptocurrencies = Use on CRYPTOCAP:TOTAL (all cryptocurrencies aggregated)

Basket consisting of healthcare stocks = Use on AMEX:XLV (healthcare sector ETF)

Breadth line can be further refined using various smoothing options (SMA, EMA, HMA, RMA, WMA), threshold method and weights. By default, threshold (dividing line between bullish and bearish states) is set to fixed at 0, depicting an equilibrium where equal amount of symbols are going up and down.

Threshold mode can also be set to Dynamic, switching threshold to a moving average of the breadth line. Fundamental functionality still remains, breadth line above threshold marks bullish state and below threshold marks bearish state. Difference here is that the threshold no longer depicts a point of equilibrium, but simply a smoothed version of the breadth line itself, which can catch turns in broad market trend earlier.

Breadth basket can be adjusted to volatility of the viewed chart, causing an overstating of breadth on high volatility and understating on low volatility. Weighting takes into account magnitude of up/down moves, which can provide better relevance for trend following purposes.

- Practical guide

Example #1 : Broad market trend

The utility of market breadth is based on the idea that markets correlate and individual symbols making up the market will eventually join the broad market trend. With this in mind, going against broad market is like swimming upstream, it's going to be the hard way. A well performing basket with clear skew for upside and downside on respective breadth states can be used to form directional bias for trades and risk on/off regimes for investing.

Example #2 : Broad market reversals

Thrusts signify two things: a historical extreme in breadth and an aggressive move to the opposite direction. Thrusts are valuable clues for exhaustion in broad market trend, potentially leading to a reversal.

Example #3 : Breadth/price divergences

Market breadth and price diverging signify events where most symbols that make up the market are going one way but a few high weight symbols (big tech for SP500) are going the other way. In other words, only a few symbols are moving the market while general interest and intention is to the other direction. Divergences in breadth and price are not ideal for sustainable trend and can be expected to eventually revert to the direction of broad market.