DWMY Opens (for aggr. charts) by Koenigsegg🟣 DWMY Opens (for Aggregated Charts) by Koenigsegg

Revolutionary compatibility with aggregated charts – This indicator represents a significant breakthrough in displaying Daily, Weekly, Monthly, and Yearly opening levels on aggregated chart types where traditional DWMY indicators have historically failed to function properly.

Complete aggregated chart support – Unlike previous Daily Weekly Monthly Yearly Opens indicators that experienced severe limitations when pulling data from non-standard chart types, this version is specifically engineered to work flawlessly with aggregated charts, range bars, Renko charts, Point & Figure charts, and all other non-time-based chart constructions.

Persistent horizontal reference lines – The indicator draws four distinct horizontal lines representing the opening prices of the current Daily, Weekly, Monthly, and Yearly periods, extending these levels forward into future bars to provide clear reference points for key support and resistance analysis.

Advanced customization capabilities – Features comprehensive user controls including custom label naming for each timeframe, adjustable line colors with independent color selection for Daily, Weekly, Monthly, and Yearly levels, configurable line width settings, and variable label font sizes ranging from tiny to huge.

Dynamic label positioning system – Implements a sophisticated label placement mechanism with configurable tick offset positioning and fixed end-bars-ahead projection, ensuring labels remain visible and properly positioned regardless of chart zoom level or timeframe.

Intelligent period detection logic – Utilizes advanced Pine Script time change detection algorithms specifically optimized for aggregated charts, accurately identifying new Daily, Weekly, Monthly, and Yearly periods even when traditional time-based functions fail on non-standard chart types.

Performance-optimized architecture – Built with efficient persistent variable storage using the var keyword, minimizing computational overhead while maintaining real-time updates across all timeframe levels simultaneously.

Professional visual presentation – Delivers clean, uncluttered chart visualization with strategically positioned labels that clearly identify each timeframe level without interfering with price action analysis.

Universal market compatibility – Functions seamlessly across all asset classes including stocks, forex, cryptocurrencies, commodities, and indices, adapting automatically to different tick sizes and price scales through syminfo.mintick integration.

Pine Script v6 foundation – Leverages the latest Pine Script version 6 capabilities, ensuring optimal performance, stability, and compatibility with current and future TradingView platform updates.

This indicator solves a critical limitation that has long plagued traders using aggregated chart types, finally enabling reliable access to essential Daily, Weekly, Monthly, and Yearly opening levels that serve as fundamental support and resistance zones in technical analysis. The breakthrough lies in its ability to maintain accurate period detection and level plotting regardless of the underlying chart construction methodology.

🟣 How It Works

Automatic period detection – The indicator continuously monitors for time changes across four distinct timeframes using ta.change(time()) functions for Daily and Weekly periods, month transitions for Monthly levels, and year changes for Yearly opens, ensuring precise identification of new period beginnings.

Real-time level updates – When a new period is detected, the indicator captures the opening price at that exact moment and immediately establishes a horizontal line from that bar extending forward to a configurable number of bars ahead, creating persistent reference levels.

Dynamic line management – Each timeframe maintains its own dedicated line object and label, with the indicator continuously updating the endpoint coordinates and label positions as new bars form, ensuring the levels always project the specified distance into the future.

Intelligent label placement – Labels are positioned at the end of each line with automatic vertical offset based on the symbol’s minimum tick size, preventing overlap with price action while maintaining clear identification of each timeframe level.

🟣 Pro Tips for Optimal Usage

Multi-timeframe confluence – Look for areas where multiple DWMY levels converge within close proximity, as these zones typically act as stronger support or resistance levels due to increased market participant attention at these psychological price points.

Breakout confirmation strategy – When price breaks above or below a significant DWMY level with strong volume, the broken level often transforms into support (if broken upward) or resistance (if broken downward), providing excellent entry and exit reference points.

Range trading opportunities – On ranging markets, use Daily and Weekly opens as potential reversal zones, especially when price approaches these levels during low-volume periods or near session opens when institutional activity increases.

Timeframe alignment technique – For swing trading, prioritize trades that align with the direction of the break from Weekly or Monthly opens, while using Daily opens for precise entry timing and position management.

Chart type optimization – This indicator excels on Renko, Range, and Point & Figure charts where traditional time-based DWMY indicators fail, making it invaluable for traders who prefer these aggregated chart types for cleaner price action analysis.

Important Disclaimer:

This indicator is provided for educational and informational purposes only. It is not financial advice, investment advice, or a recommendation to buy or sell any financial instrument. All trading involves risk, and past performance does not guarantee future results. Please conduct your own research and consult with a qualified financial advisor before making any trading decisions. The author is not responsible for any losses incurred from using this indicator.

Search in scripts for "renko"

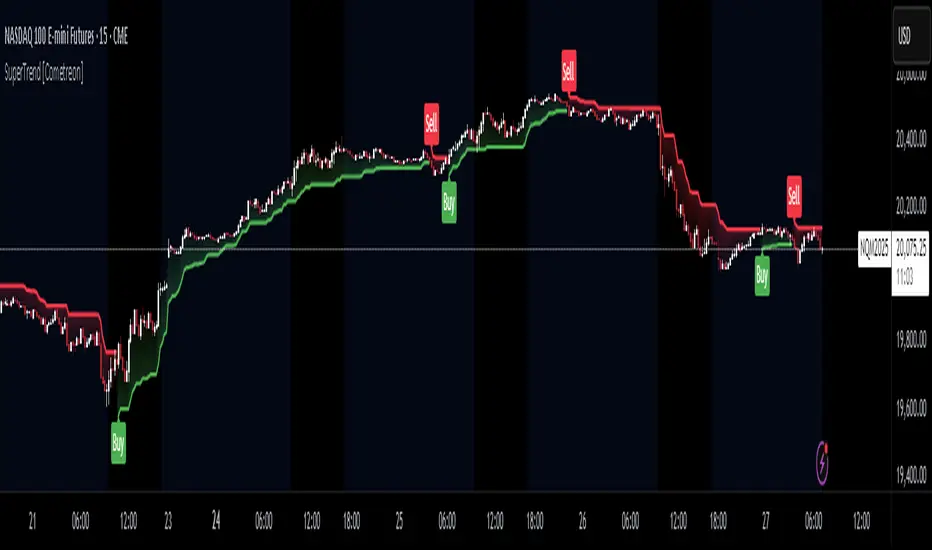

SuperTrend MTF Pro [Cometreon]The SuperTrend MTF Pro takes the classic SuperTrend to a whole new level of customization and accuracy. Unlike the standard version, this indicator allows you to select different moving averages, apply it to various chart types, and fine-tune every key parameter.

If you're looking for an advanced, non-repainting, and highly configurable SuperTrend, this is the right choice for you.

🔷 New Features and Improvements

🟩 Multi-MA SuperTrend

Now you can customize the SuperTrend calculation by choosing from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

🟩 Multiple Chart Types

You're no longer limited to candlestick charts! Now you can use SuperTrend with different chart formats, including:

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Customizable Timeframe

Now you can adjust the SuperTrend timeframe without repainting issues, avoiding signal distortions.

🔷 Technical Details and Customizable Inputs

SuperTrend offers multiple customization options to fit any trading strategy:

1️⃣ ATR Period – Defines the ATR length, affecting the indicator’s sensitivity.

2️⃣ Source – Selects the price value used for calculations (Close, HL2, Open, etc.).

3️⃣ ATR Mult – Multiplies the ATR to determine band distance. Higher values reduce false signals, lower values make it more reactive.

4️⃣ Change ATR Calculation Method – When enabled, uses the default ATR method; when disabled, allows selecting another Moving Average with "Use Different Type".

5️⃣ Source Break – Defines the price source for trend changes (Close for more stability, High/Low for more reactivity).

6️⃣ Use Different Type – Allows selecting an alternative Moving Average for ATR calculation if "Change ATR Calculation Method" is disabled.

7️⃣ SuperTrend Type – Advanced options for specific MAs (JMA, ALMA, FRAMA, VIDYA), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

8️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, and ATR length.

9️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

🔟 Wait for Timeframe Closes -

✅ Enabled – Prevents multiple signals, useful for precise alerts.

❌ Disabled – Displays SuperTrend smoothly without interruptions.

🔷 How to Use SuperTrend MTF Pro

🔍 Identifying Trends

SuperTrend follows the ongoing trend and provides clear visual signals:

When the price is above the line, the trend is bullish.

When the price is below the line, the trend is bearish.

📈 Interpreting Signals

Line color and position change → Possible trend reversal

Bounce off the line → Potential trend continuation

Strong breakout of the line → Possible reversal

🛠 Integration with Other Tools

RSI or MACD to filter false signals

Moving Averages to confirm trend direction

Support and Resistance to improve entry points

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

Volatility Percentile (H-LINES)A simple script that adjusts the Volatility Percentile Indicator visibly in order to better accommodate entries/exits and certain trading setups/strategies.

--------------------------------------------------------------------------------------------------------------------------------------------------------

TL;DR - Remember after a full reset, we are looking for initial crosses UP on the UpperSwingline and crosses DOWN on the LowerSwingline for primary and secondary signal derivation.

Vice versa also works great but the prior method mentioned is a little more consistent in my experience, but you should mess around and optimise this for your own setups and strategies anyway.

--------------------------------------------------------------------------------------------------------------------------------------------------------

ORIGINAL SCRIPT HERE:

^Click image for a redirect to that script.

ALL CREDIT GOES TO: www.tradingview.com

He wrote everything so give credit where it's due, good bit of kit this here script is.

--------------------------------------------------------------------------------------------------------------------------------------------------------

HOW I USE MY VISUALLY ALTERED VERSION OF THIS SCRIPT

First of all, the alterations I've made seem only to be consistently viable with renko charts though if you can get the sought after results using candles or any other chart type then perfect, but be wary. All my back-testing done only with LinReg, HMA and SWMA - ATR type settings exclusively on renko charts. The changes I've made to the original script essentially just turns it visibly into an oscillator and uses a couple horizontal lines to generate signals, very simple - absolutely nothing has changed in the actual code of calculating this indicator.

What I believe my adjustments have achieved is quite simple. A full reset/oscillation on the indicator tries to map the strongest parts of a move or at least the part of the move where volume and the rate of transactions is at its peak to even facilitate said move. *take this statement with a pinch of salt though I do believe it's interacting with accumulation/distribution patterns, which is expected of volatility*

For ease of communication let's refer to the area between the the first UpperSwingline cross to the subsequent LowerSwingline cross, as the primary move. Then afterwards when it crosses the UpperSwingline again to make the full reset, the area in between those two points referred to as the secondary move.

Though more interestingly/practically the indicator ends up giving you two signals. In order for this to work we have to first decide that a spike up in volatility which crosses the UpperSwingline implies a significant level of interest at that price level. Usually that means a reversal is brewing, if price has already moved, trended and is approaching a certain area of value; which causes a spike of new positions to be taken, then you know that this is a level where contrarians are looking to enter. Now here's the tricky part, when volatility crosses the LowerSwingline price action becomes a little more open for interpretation, the way I personally like to look at this secondary signal is the potential for an exhaustion period to prolong itself a little longer. I know that's not the perfect analysis for what's going on, a more in-depth look into what's going on would best be described using Elliott Wave Theory, if a cross on the UpperSwingline near a significant area of value gives us a reversal trade lets just assume for the sake of argument that a new Elliott Wave can begin forming here. Making the move from that initial UpperSwngline cross to the cross on the LowerSwingline, the area that encompasses those two points: the impulse wave. After this point my analogy kind of falls apart and sadly my knowledge just isn't what it needs to be in order for me to properly analyse what's going on here but I must digress. Price after crossing the LowerSwingline up until the point where it makes a full reset by crossing the UpperSwingline again, within this area price seems to do either one of two things:

Situation 1 - Most likely occurs after a major trend reversal from major support/resistance or area of value (price has trended to new territory, maybe spent time a little time consolidating but hasn't broken the key level, momentum shifts, price action breaks current structure and you get the signal that primary move is a reversal) = Exhaustion Period, price will continue in direction of primary move during the secondary move. This here is for our trend-followers, you wanna take a continuation trade? Just wait for the pullback/rally to hit a FiB retracement level and enter - or any other means to find a decent support/resistance to enter.

Situation 2 - Most likely occurs when market enters a range or consolidation (price was previously seen as being at either a discount or premium so Situation 1 could have already played out and now you're looking at a full reset after that, imagine this spot to be the centre line of a linear regression channel or bang in the middle of your range, could even occur if price breaks a key moving average and decides it ought to consolidate around it for a while. Basically at any point where a somewhat prolonged consolidation is expected and not a quick reversal) = Corrective Wave, price will move against the direction of primary move during the secondary move. Now you might be expecting me to say this ones for you reversal traders but not really, if this is occurring then there probably isn't a definitive direction the market has chosen so you can use this opportunity to take range trades in the direction or against the direction of whatever the current trend or latest trend was depending on whatever slight bias you may have. <--- Situation 2 is very useful for finding cleaner entries if you do have a trend bias, say price underwent Situation 1, is now at key moving average but your bias is that it will break and continue up, so you wait and allow the secondary move of Situation 2 to take your entry to a much better R:R before entering a position.

--------------------------------------------------------------------------------------------------------------------------------------------------------

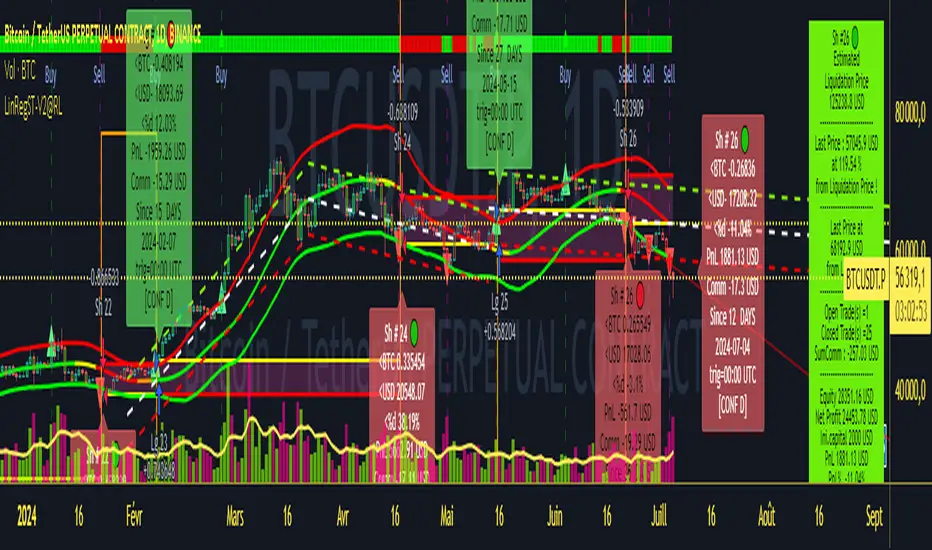

Strategy LinReg ST@RLStrategy LinReg ST@RL

Strategy LinReg ST@RL is a visual trend following indicator.

It is compiled in PINE Script Version V5 language.

This indicator/strategy, based on Linear Regression Calculation, is intended to help beginners (and also the more experienced ones) to trade in the right direction of the market trend and test strategy. It allows you to avoid the mistakes of always trading against the trend.

Strategy based on an original idea of @KivancOzbilgic (SuperTrend) and DevLucem (@LucemAnb) (Lin Reg ++)

A special credit goes to - KivancOzbilgic and @LucemAnb which inspired me a lot to improve this indicator/Strategy.

This indicator can be configured to your liking,according to your needs or your tastes.

The indicator/Strategy works in multi time frame.

The settings (length, offset, deviation, smoothing) are identical for all time frames if “Conf Auto” is not checked.

In this case the default settings (time frame=H1 settings) apply for all time frames.

The choice of source setting is common for all time frames.

If “Auto Conf” is checked,

then the settings will be optimized for each selected time frame (1m-3m H2 H3 H1 H4 & Daily). Time frames, other than 1m-3m H2 H3 H1 H4 & Daily will be affected with the default settings corresponding to the H1 time frame and will therefore not be optimized! The default setting values of each time frame (1m-3m H2 H3 H1 H4 & Daily) can be configured differently and optimized by you.

REVERSAL mode: Signal Buy=Sell and Signal Sell=Buy.

This option may be better than the regular strategy. Default mode is Reversal option.

Note that only for 1m (1 minute) Time frame, the option REVERSAL is opposite as default choice in configuration. (If reversal option is checked, then option for time frame 1m is not reversal!)

Trend indications (potential sell or buy areas) are displayed as a background color (bullish: green or bearish: red), assume that the market is moving in one direction.

You can tune the input, style and visibility settings to match your own preferences or habits.

Label Info (Simple or Full) gives trend info for each Exit (or current trade)

The choice of indicator colors is suitable for a graph with a "dark" theme, which you will probably need to modify for visual comfort, if you are using a "Light" mode or a custom mode.

This script is an indicator that you can run on standard chart types. It also works on non-standard chart types but the results will be skewed and different.

Non-standard charts are:

• Heikin Ashi (HA)

• Renko

• Kagi

• Point & Figure

• Range

As a reminder: No indicator is capable of providing accurate signals 100% of the time. Every now and then, even the best will fail, leaving you with a losing deal. Whichever indicator you base yourself on, remember to follow the basic rules of risk management and capital allocation.

BINANCE:BTCUSDT

! Français !

Strategy LinReg ST@RL

Stratégie LinReg ST@RL est un indicateur visuel de suivi de tendance.

Il est compilé en langage PINE Script Version V5.

Stratégie basée sur une idée originale de @KivancOzbilgic (SuperTrend) et DevLucem (@LucemAnb) (Lin Reg ++) Un crédit spécial va à - KivancOzbilgic et @LucemAnb qui m'ont beaucoup inspiré pour améliorer cet indicateur/stratégie.

Cet indicateur/strategie, basé sur le calcul de régression linéaire, est destiné à aider les débutants (et aussi les plus expérimentés) à trader dans le bon sens de la tendance du marché et à tester la stratégie. Cela vous permet d'éviter les erreurs de toujours négocier à contre-courant.

Cet indicateur peut être configuré à votre guise, selon vos besoins ou vos goûts.

L'indicateur/Stratégie fonctionne sur plusieurs bases de temps.

Les réglages (longueur, décalage, déviation, lissage) sont identiques pour toutes les bases de temps si

« Conf Auto » n'est pas coché. Dans ce cas, les paramètres par défaut (intervalle de temps=paramètres H1) s'appliquent à toutes les bases de temps.

Le choix du réglage de la source est commun à toutes les bases de temps.

Si "Auto Conf" est coché, alors les paramètres seront optimisés pour chaque base de temps sélectionnée (1m-3m H2 H3 H1 H4 & Daily). Les bases de temps, autres que 1m-3m H2 H3 H1 H4 & Daily seront affectées par les paramètres par défaut correspondant à la base de temps H1 et ne seront donc pas optimisées ! Les valeurs de réglage par défaut de chaque période (1m-3m H2 H3 H1 H4 & Daily) peuvent être configurées différemment et optimisées par vous.

Mode REVERSAL : Signal Achat=Vente et Signal Vente=Achat. Cette option peut être meilleure que la stratégie habituelle. Le mode par défaut est l'option REVERSAL.

Notez que seulement pour la base de temps de 1m (1 minute), l'option REVERSAL est l’opposée du choix par défaut dans la configuration. (Si l'option REVERSAL est cochée, alors l'option pour la base de temps 1 m n'est pas REVERSAL !)

Les indications de tendance (zones potentielles de vente ou d'achat) sont affichées en couleur de fond (haussier : vert ou baissier : rouge), supposons que le marché évolue dans une direction. Vous pouvez ajuster les paramètres d'entrée, de style et de visibilité en fonction de vos propres préférences ou habitudes.

Les informations sur l'étiquette (simples ou complètes) donnent des informations sur de chaque clôture (ou position en cours)

Le choix des couleurs des indicateurs est adapté à un graphique avec un thème "sombre", qu'il vous faudra probablement modifier pour le confort visuel, si vous utilisez un mode "Clair" ou un mode personnalisé.

Ce script est un indicateur que vous pouvez exécuter sur des types de graphiques standard. Cela fonctionne également sur les types de graphiques non standard, mais les résultats seront faussés et différents.

Les graphiques non standard sont :

• Heikin Ashi (HA)

• Renko

• Kagi

• Point & Figure

• Range

Pour rappel : Aucun indicateur n'est capable de fournir des signaux précis 100% du temps. De temps en temps, même les meilleurs échoueront, vous laissant avec une affaire perdante. Quel que soit l'indicateur sur lequel vous vous basez, rappelez-vous de suivre les règles de base de la gestion des risques et de l'allocation du capital.

Combo 4+ KDJ STO RSI EMA3 Visual Trend Pine V5@RL! English !

Combo 4+ KDJ STO RSI EMA3 Visual Trend Pine V5 @ RL

Combo 4+ KDJ STO RSI EMA3 Visual Trend Pine V5 @ RL is a visual trend following indicator that groups and combines four trend following indicators. It is compiled in PINE Script Version V5 language.

• STOCH: Stochastic oscillator.

• RSI Divergence: Relative Strength Index Divergence. RSI Divergence is a difference between a fast and a slow RSI.

• KDJ: KDJ Indicator. (trend following indicator).

• EMA Triple: 3 exponential moving averages (Default display).

This indicator is intended to help beginners (and also the more experienced ones) to trade in the right direction of the market trend. It allows you to avoid the mistakes of always trading against the trend.

The calculation codes of the different indicators used are standard public codes used in the usual TradingView coding for these indicators.

The STO indicator calculation script is taken from TradingView's standard STOCH calculation.

The RSI indicator calculation script is a replica of the one created by @Shizaru.

The KDJ indicator calculation script is a replica of the one created by @iamaltcoin.

The Triple EMA indicator calculation script is a replica of the one created by @jwilcharts.

This indicator can be configured to your liking. It can even be used several times on the same graph (multi-instance), with different configurations or display of another indicator among the four that compose it, according to your needs or your tastes.

A single plot, among the 4 indicators that make it up, can be displayed at a time, but either with its own trend or with the trend of the 4 (3 by default) combined indicators (sell=green or buy=red, background color).

Trend indications (potential sell or buy areas) are displayed as a background color (bullish: green or bearish: red) when at least three of the four indicators (3 by default and configurable from 1 to 4) assume that the market is moving in the same direction. These trend indications can be configured and displayed, either only for the signal of the selected indicator and displayed, or for the signals of the four indicators together and combined (logical AND).

You can tune the input, style and visibility settings of each indicator to match your own preferences or habits.

A 'buy stop' or 'sell stop' signal is displayed (layouts) in the form of a colored square (green for 'stop buy' and red for 'stop sell'. These 'stop' signals can be configured and displayed, either only for the indicator chosen, or for the four indicators together and combined (logical OR).

Note that the presence of a Stop Long signal cancels the background color of the Long trend (green).

Likewise, the presence of a Stop Short signal cancels out the background color of the Short trend (red).

It is also made up of 3 labels:

• Trend Label

• signal Stop Label (signals Stop buy or sell )

• Info Label (Names of Long / Short / Stop Long / Stop Short indicators, and / Open / Close / High / Low ).

Each label is configurable (visibility and position on the graph).

• Trend label: indicates the number of indicators suggesting the same trend (Long or Short) as well as a strength index (PWR) of this trend: For example: 3 indicators in Short trend, 1 indicator in Long trend and 1 indicator in neutral trend will give: PWR SHORT = 2/4. (3 Short indicators - 1 Long indicator = 2 Pwr Short). And if PWR = 0 then the display is "Wait and See". It also indicates which current indicator is displayed and the display mode used (combined 1 to 4 indicators or not combined ).

• Signal Stop Label: Indicates a possible stop of the current trend.

• Label Info (Simple or Full) gives trend info for each of the 4 indicators and OHLC info for the chart (in “Full” mode).

It is possible to display this indicator several times on a chart (up to 3 indicators max with the Basic TradingView Plan and more with the paid plans), with different configurations: For example:

• 1-Stochastic - 2/4 Combined Signals - no Label displayed

• 1-RSI - Combined Signals 3/4 - Stop Label only displayed

• 1-KDJ - Combined Signals 4/4 - the 3 Labels displayed

• 1-EMA'3 - Non-combined signals (EMA only) - Trend Label displayed

Some indicators have filters / thresholds that can be configured according to your convenience and experience!

The choice of indicator colors is suitable for a graph with a "dark" theme, which you will probably need to modify for visual comfort, if you are using a "Light" mode or a custom mode.

This script is an indicator that you can run on standard chart types. It also works on non-standard chart types but the results will be skewed and different.

Non-standard charts are:

• Heikin Ashi (HA)

• Renko

• Kagi

• Point & Figure

• Range

As a reminder: No indicator is capable of providing accurate signals 100% of the time. Every now and then, even the best will fail, leaving you with a losing deal. Whichever indicator you base yourself on, remember to follow the basic rules of risk management and capital allocation.

BINANCE:BTCUSDT

**********************************************************************************************************************************************************************************************************************************************************************************

! Français !

Combo 4+ KDJ STO RSI EMA3 Visual Trend Pine V5@RL

Combo 4+ KDJ STO RSI EMA3 Visual Trend Pine V5@RL est un indicateur visuel de suivi de tendance qui regroupe et combine quatre indicateurs de suivi de tendance. Il est compilé en langage PINE Script Version V5.

• STOCH : Stochastique.

• RSI Divergence : Relative Strength Index Divergence. La Divergence RSI est une différence entre un RSI rapide et un RSI lent.

• KDJ : KDJ Indicateur. (indicateur de suivi de tendance).

• EMA Triple : 3 moyennes mobiles exponentielles (Affichage par défaut).

Cet indicateur est destiné à aider les débutants (et aussi les plus confirmé) à trader à dans le bon sens de la tendance du marché. Il permet d'éviter les erreurs qui consistent à toujours trader à contre tendance.

Les codes de calcul des différents indicateurs utilisés sont des codes publics standards utilisés dans le codage habituel de TradingView pour ces indicateurs !

Le script de calcul de l’indicateur STO est issu du calcul standard du STOCH de TradingView.

Le script de calcul de l’indicateur RSI Div est une réplique de celui créé par @Shizaru.

Le script de calcul de l’indicateur KDJ est une réplique de celui créé par @iamaltcoin.

Le script de calcul de l’indicateur Triple EMA est une réplique de celui créé par @jwilcharts

Cet indicateur peut être configuré à votre convenance. Il peut même être utilisé plusieurs fois sur le même graphique (multi-instance), avec des configurations différentes ou affichage d’un autre indicateur parmi les quatre qui le composent, selon vos besoins ou vos goûts.

Un seul tracé, parmi les 4 indicateurs qui le composent, peut être affiché à la fois mais, soit avec sa propre tendance soit avec la tendance des 4 (3 par défaut) indicateurs combinés (couleur de fond vente=vert ou achat=rouge).

Les indications de tendance (zones de vente ou d’achat potentielles) sont affichés sous la forme de couleur de fond (Haussier : vert ou baissier : rouge) lorsque au moins trois des quatre indicateurs (3 par défaut et configurable de 1 à 4) supposent que le marché évolue dans la même direction. Ces indications de tendance peuvent être configuré et affichés, soit uniquement pour le signal de l’indicateur choisi et affiché, soit pour les signaux des quatre indicateurs ensemble et combinés (ET logique).

Vous pouvez accorder les paramètres d’entrée, de style et de visibilité de chacun des indicateurs pour correspondre à vos propres préférences ou habitudes.

Un signal ‘stop achat’ ou ‘stop vente’ est affiché (layouts) sous la forme d’un carré de couleur (vert pour ‘stop achat’ et rouge pour ‘stop vente’. Ces signaux ‘stop’ peuvent être configuré et affichés, soit uniquement pour l’indicateur choisi, soit pour les quatre indicateurs ensemble et combinés (OU logique).

A noter que la présence d’un signal Stop Long annule la couleur de fond de la tendance Long (vert).

De même, la présence d’un signal Stop Short annule la couleur de fond de la tendance Short (rouge).

Il est aussi composé de 3 étiquettes (Labels) :

• Trend Label (infos de tendance)

• Signal Stop Label (signaux « Stop » achat ou vente)

• Infos Label (Noms des indicateurs Long/Short/Stop Long/Stop Short,

et /Open/Close/High/Low )

Chaque label est configurable (visibilité et position sur le graphique).

• Label Trend : indique le nombre d’indicateurs suggérant une même tendance (Long ou Short) ainsi qu’un indice de force (PWR) de cette tendance :

Par exemple : 3 indicateurs en tendance Short, 1 indicateur en tendance Long et 1 indicateur en tendance neutre donnera :

PWR SHORT = 2/4. (3 indicateurs Short – 1 indicateur Long=2 Pwr Short).

Et si PWR=0 alors l’affichage est « Wait and See » (Attendre et Observer).

Il indique aussi quel indicateur actuel est affiché et le mode d’affichage utilisé (combiné 1 à 4 indicateurs ou non combiné ).

• Signal Stop Label : Indique un possible arrêt de la tendance en cours.

• Infos Label (Simple ou complet) donne les infos de tendance de chacun des 4 indicateurs et les infos OHLC du graphique (en mode « Complet »).

Il est possible d’afficher ce même indicateur plusieurs fois sur un graphique (jusqu’à 3 indicateurs max avec le Plan Basic TradingView et plus avec les plans payants), avec des configurations différentes :

Par exemple :

• 1-Stochastique – Signaux Combinés 2/4 – aucun Label affiché

• 1-RSI – Signaux Combinés 3/4 – Label Stop uniquement affiché

• 1-KDJ – Signaux Combinés 4/4 – les 3 Labels affichés

• 1-EMA’3 - Signaux Non combinés (EMA seuls) – Trend Label affiché

Certains indicateurs ont des filtres/seuils (Thresholds) configurables selon votre convenance et votre expérience !

Le choix des couleurs de l’indicateur est adapté pour un graphique avec thème « sombre », qu’il vous faudra probablement modifier pour le confort visuel, si vous utilisez un mode « Clair » ou un mode personnalisé.

Ce script est un indicateur que vous pouvez exécuter sur des types de graphiques standard. Il fonctionne aussi sur des types de graphiques non-standard mais les résultats seront faussés et différents.

Les graphiques Non-standard sont :

• Heikin Ashi (HA)

• Renko

• Kagi

• Point & Figure

• Range

Pour rappel : Aucun indicateur n’est capable de fournir des signaux précis 100% du temps. De temps en temps, même les meilleurs échoueront, vous laissant avec une affaire perdante. Quel que soit l’indicateur sur lequel vous vous basez, n’oubliez pas de suivre les règles de base de gestion des risques et de répartition du capital.

BINANCE:BTCUSDT

R-Candlesjust a modify type of renko candles

it not renko but it use some of it princeples

red is bearish

lime is bullish

the ATR length control how this candles behave

[RESEARCH] Point-and-Figure (P&F) Chart Identifier(Republishing of the hidden script)

A heuristic approach to identify P&F chart type. Catches all variations.

Works correctly with other chart types:

Classic Candles

Heikin-Ashi

Line Break

Kagi

ATR Renko

Traditional Renko

Range Bars

[RESEARCH] Heikin-Ashi Chart IdentifierA deterministic approach to identify Heikin-Ashi chart type.

The script checks the next statements about HA:

HA chart does not have any gaps in a classic sense

Every new HA open price is calculated using a specific recurrence formula. This fact also means that initial HA open price is used to calculate all the next and so on (a construction of Infinite Impulse Response filters)

The script works correctly being applied to other chart types:

Classic Candlestick

Range Bars

Line Break

Traditional Renko

ATR Renko

Traditional Point-and-Figure

ATR Point-and-Figure

Kagi

For special ones: this code allows you to check whether your script is being executed with Heikin-Ashi candles or not inside your script.

Ev sistr 'ta Laou!

[RESEARCH] Kagi Chart IdentifierA heuristic approach to identify Kagi chart type.

This tool allows to identify:

ATR Kagi charts (see ^)

Traditional Kagi charts

Works correctly with other chart types:

Classic Candles

Heikin-Ashi

Line Break

PnF

ATR Renko

Traditional Renko

Range Bars

Do not forget @everget

TradersVenue_Renko_Strategy 5MTradersVenue Renko strategy for intraday and positional trading. It generates buy/sell signals basis Renko ATR and 5M timeframe.

Simple LinesIntroduction

Making lines is great in technical analysis since it can highlights principal movements and make the analysis of the price easier when using certain methodologies (Elliott Waves, patterns).

However most of the indicators making lines (Zig-Zag, simple linear regression) are non causal (repaint), this is the challenge i tried to overcome, making an indicator capable of making lines in a smart way (able to follow price without loosing a linear approach) and with the least lag possible, i inspired myself from the behaviour of the renko when using a small brick size. This indicator does not repaint .

The code is short and i hope, understandable for all of you, making lines is not a difficult task and its important to know that when a problem appear complex it does not mean that the code used to solve this problem must be complex. Lets see the indicator in details.

The indicator

The indicator have 4 parameters, the length parameter who control the length of lines, the emphasis parameter who control the stability and also the ability to make lines closer to the price (thus minimizing the sum of squares) , the mult parameter which is similar to emphasis and a point option that we will discuss later.

When emphasis and mult are both equal to 1 the indicator will sometimes draw a perfect line, however this line will try to follow the price and thus can create a noisy result.

This is where emphasis and mult will correct this behaviour. The emphasis parameter give a more periodic look as well as some control to the lines but can also destroy them.

This should not happen with mult , this parameter also give more predictability to the lines. Overall it correct the drawbacks of the parameters combinations mentioned earlier.

Its also possible to mix both the emphasis and mult parameter, but take into account that when both are equals the result consist of less reactive lengthy lines with low accuracy. Its better to only use one of them and let the other stay to 1.

Point Option

The indicator can sometimes have a weird look, appearing almost flat or just dont appearing at all. When such thing happen use the point option.

XPDUSD without point option.

with point option :

Time Frame Problem and Its Fix

When using higher time-frames the result of the indicator can appear different, in general the higher the time frame the lengthier are the lines. In order to fix this you can use decimals in the length parameter

length and mult both equal to 5.5, emphasis cant use decimals.

Conclusion

I have highlighted a simple way to make use of the small renko box size method in order to return reactive lines without making the indicator repaint. However Its ability to be close to the price as well as being always super reactive is not a guarantee.

For any suggestion/help feel free to pm me, i would be happy to help you :)

Fractal Framer added buy sellThis script was written by Brobear and published. I only modified by adding buy and sell signal when price crossover fractal channel.

buy_breakout=crossover(close,fracLevelHigh) and OsMA >OsMA and emaRSI >emaRSI

sell_breakout=crossunder(close,fracLevelLow) and OsMA

AlphaTrend++ offset labelsAlphaTrend++

Overview

The AlphaTrend++ is an advanced Pine Script indicator designed to help traders identify buy and sell opportunities in trending and volatile markets. Building on trend-following principles, it uses a modified Average True Range (ATR) calculation combined with volume or momentum data to plot a dynamic trend line. The indicator overlays on the price chart, displaying a colored trend line, a filled trend zone, buy/sell signals, and optional stop-loss tick labels, making it ideal for day trading or swing trading, particularly in markets like futures (e.g., MES).

What It Does

This indicator generates buy and sell signals based on the direction and momentum of a custom trend line, filtered by optional time restrictions and signal frequency logic. The trend line adapts to price action and volatility, with a filled zone highlighting trend strength. Buy/sell signals are plotted as labels, and stop-loss distances are displayed in ticks (customizable for instruments like MES). The indicator supports standard chart types for realistic signal generation.

How It Works

The indicator employs the following components:

Trend Line Calculation: A dynamic trend line is calculated using ATR adjusted by a user-defined multiplier, combined with either Money Flow Index (MFI) or Relative Strength Index (RSI) depending on volume availability. The line tracks price movements, adjusting upward or downward based on trend direction and volatility.

Trend Zone: The area between the current trend line and its value two bars prior is filled, colored green for bullish trends (upward movement) or red for bearish trends (downward movement), providing a visual cue of trend strength.

Signal Generation: Buy signals occur when the trend line crosses above its value two bars ago, and sell signals occur when it crosses below, with optional filtering to reduce signal noise (based on bar timing logic). Signals can be restricted to a 9:00–15:00 UTC trading window.

Stop-Loss Ticks: For each signal, the indicator calculates the distance to the trend line (acting as a stop-loss level) in ticks, using a user-defined tick size (default 0.25 for MES). These are displayed as labels below/above the signal.

Time Filter: An optional filter limits signals to 9:00–15:00 UTC, aligning with active trading sessions like the US market open.

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to avoid unrealistic results associated with non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Multiplier: Adjust the ATR multiplier (default 1.0) to control trend line sensitivity. Higher values widen the stop-loss distance.

Common Period: Set the ATR and MFI/RSI period (default 14) for trend calculations.

No Volume Data: Enable if volume data is unavailable (e.g., for certain forex pairs), switching from MFI to RSI.

Tick Size: Set the tick size for stop-loss calculations (default 0.25 for MES futures).

Show Buy/Sell Signals: Toggle signal labels (default enabled).

Show Stop Loss Ticks: Toggle stop-loss tick labels (default enabled).

Use Time Filter: Restrict signals to 9:00–15:00 UTC (default disabled).

Use Filtered Signals: Enable to reduce signal frequency using bar timing logic (default enabled).

Interpret Signals:

Buy Signal: A blue “BUY” label below the bar indicates a potential long entry (trend line crossover, passing filters).

Sell Signal: A red “SELL” label above the bar indicates a potential short entry (trend line crossunder, passing filters).

Trend Zone: Green fill suggests bullish momentum; red fill suggests bearish momentum.

Stop-Loss Ticks: Gray labels show the stop-loss distance in ticks, helping with risk management.

Monitor Context: Use the trend line and filled zone to confirm the market’s direction before acting on signals.

Unique Features

Adaptive Trend Line: Combines ATR with MFI or RSI to create a responsive trend line that adjusts to volatility and market conditions.

Tick-Based Stop-Loss: Displays stop-loss distances in ticks, customizable for specific instruments, aiding precise risk management.

Signal Filtering: Optional bar timing logic reduces false signals, improving reliability in choppy markets.

Trend Zone Visualization: The filled zone between trend line values enhances trend clarity, making it easier to assess momentum.

Time-Restricted Trading: Optional 9:00–15:00 UTC filter aligns signals with high-liquidity sessions.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume spikes) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in highly volatile or low-liquidity markets due to ATR-based calculations.

The 9:00–15:00 UTC time filter may not suit all markets; disable it for 24-hour assets like forex or crypto.

Stop-loss tick calculations assume consistent tick sizes; verify compatibility with your instrument.

This indicator is designed for traders seeking a robust, trend-following tool with customizable risk management and signal filtering, optimized for active trading sessions.

This update enhances label customization, clarity, and signal usability while preserving all existing AlphaTrend++ logic. The goal is to improve readability during live trading and allow traders to personalize the visual footprint of entries and stop-loss levels.

Improvements

• Cleaner Label Placement

Labels now maintain consistent spacing from the candle, regardless of volatility or ATR expansion.

• Enhanced Visual Structure

BUY/SELL signals remain bold and clear, while SL ticks use a more compact and optional sizing scheme.

• Better User Control

New UI inputs:

Entry Label Size

SL Label Size

SL Label Offset (Ticks)nces.

C&B Auto MK5C&B Auto MK5.2ema BullBear

Overview

The C&B Auto MK5.2ema BullBear is a versatile Pine Script indicator designed to help traders identify bullish and bearish market conditions across various timeframes. It combines Exponential Moving Averages (EMAs), Relative Strength Index (RSI), Average True Range (ATR), and customizable time filters to generate actionable signals. The indicator overlays on the price chart, displaying EMAs, a dynamic cloud, scaled RSI levels, bull/bear signals, and market condition labels, making it suitable for swing trading, day trading, or scalping in trending or volatile markets.

What It Does

This indicator generates bull and bear signals based on the interaction of two EMAs, filtered by RSI thresholds, ATR-based volatility, a 50/200 EMA trend filter, and user-defined time windows. It adapts to market volatility by adjusting EMA lengths and RSI thresholds. A dynamic cloud highlights trend direction or neutral zones, with candlestick coloring in neutral conditions. Market condition labels (current and historical) provide real-time trend and volatility context, displayed above the chart.

How It Works

The indicator uses the following components:

EMAs: Two EMAs (short and long) are calculated on a user-selected timeframe (1, 5, 15, 30, or 60 minutes). Their crossover or crossunder triggers potential bull/bear signals. EMA lengths adjust based on volatility (e.g., 10/20 for volatile markets, 5/10 for non-volatile).

Dynamic Cloud: The area between the EMAs forms a cloud, colored green for bullish trends, red for bearish trends, or a user-defined color (default yellow) for neutral zones (when EMAs are close, determined by an ATR-based threshold). Users can widen the cloud for visibility.

RSI Filter: RSI is scaled to price levels and plotted on the chart (optional). Signals are filtered to ensure RSI is within volatility-adjusted bull/bear thresholds and not in overbought/oversold zones.

ATR Volatility Filter: An optional filter ensures signals occur during sufficient volatility (ATR(14) > SMA(ATR, 20)).

50/200 EMA Trend Filter: An optional filter restricts bull signals to bullish trends (50 EMA > 200 EMA) and bear signals to bearish trends (50 EMA < 200 EMA).

Time Filter: Signals are restricted to a user-defined UTC time window (default 9:00–15:00), aligning with active trading sessions.

Market Condition Labels: Labels above the chart display the current trend (Bullish, Bearish, Neutral) and optionally volatility (e.g., “Bullish Volatile”). Up to two historical labels persist for a user-defined number of bars (default 5) to show recent trend changes.

Visual Aids: Bull signals appear as green triangles/labels below the bar, bear signals as red triangles/labels above. Candlesticks in neutral zones are colored (default yellow).

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to produce realistic signals, avoiding non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Timeframe: Choose a timeframe (1, 5, 15, 30, or 60 minutes) to match your trading style.

Filters:

Enable/disable the ATR volatility filter to focus on high-volatility periods.

Enable/disable the 50/200 EMA trend filter to align signals with the broader trend.

Enable the time filter and set custom UTC hours/minutes (default 9:00–15:00).

Cloud Settings: Adjust the cloud width, neutral zone threshold, color, and transparency.

EMA Colors: Use default trend-based colors or set custom colors for short/long EMAs.

RSI Display: Toggle the scaled RSI and its thresholds, with customizable colors.

Signal Settings: Toggle bull/bear labels and set signal colors.

Market Condition Labels: Toggle current/historical labels, include/exclude volatility, and adjust decay period.

Interpret Signals:

Bull Signal: A green triangle or “Bull” label below the bar indicates potential bullish momentum (EMA crossover, RSI above bull threshold, within time window, passing filters).

Bear Signal: A red triangle or “Bear” label above the bar indicates potential bearish momentum (EMA crossunder, RSI below bear threshold, within time window, passing filters).

Neutral Zone: Yellow candlesticks and cloud (if enabled) suggest a lack of clear trend; consider range-bound strategies or avoid trading.

Market Condition Labels: Check labels above the chart for real-time trend (Bullish, Bearish, Neutral) and volatility status to confirm market context.

Monitor Context: Use the cloud, RSI, and labels to assess trend strength and volatility before acting on signals.

Unique Features

Volatility-Adaptive EMAs: Automatically adjusts EMA lengths based on ATR to suit volatile or non-volatile markets, reducing manual configuration.

Neutral Zone Detection: Uses an ATR-based threshold to identify low-trend periods, helping traders avoid choppy markets.

Scaled RSI Visualization: Plots RSI and thresholds directly on the price chart, simplifying momentum analysis relative to price.

Flexible Time Filtering: Supports precise UTC-based trading windows, ideal for day traders targeting specific sessions.

Historical Market Labels: Displays recent trend changes (up to two) with a decay period, providing context for market shifts.

50/200 EMA Trend Filter: Aligns signals with the broader market trend, enhancing signal reliability.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in fast-moving markets due to EMA-based calculations.

Neutral zone detection may vary in extremely volatile or illiquid markets.

Time filters are UTC-based; ensure your platform’s timezone settings align.

This indicator is designed for traders seeking a customizable, trend-following tool that adapts to volatility and provides clear visual cues with robust filtering for bullish and bearish market conditions.

AlphaTrend++AlphaTrend++

Overview

The AlphaTrend++ is an advanced Pine Script indicator designed to help traders identify buy and sell opportunities in trending and volatile markets. Building on trend-following principles, it uses a modified Average True Range (ATR) calculation combined with volume or momentum data to plot a dynamic trend line. The indicator overlays on the price chart, displaying a colored trend line, a filled trend zone, buy/sell signals, and optional stop-loss tick labels, making it ideal for day trading or swing trading, particularly in markets like futures (e.g., MES).

What It Does

This indicator generates buy and sell signals based on the direction and momentum of a custom trend line, filtered by optional time restrictions and signal frequency logic. The trend line adapts to price action and volatility, with a filled zone highlighting trend strength. Buy/sell signals are plotted as labels, and stop-loss distances are displayed in ticks (customizable for instruments like MES). The indicator supports standard chart types for realistic signal generation.

How It Works

The indicator employs the following components:

Trend Line Calculation: A dynamic trend line is calculated using ATR adjusted by a user-defined multiplier, combined with either Money Flow Index (MFI) or Relative Strength Index (RSI) depending on volume availability. The line tracks price movements, adjusting upward or downward based on trend direction and volatility.

Trend Zone: The area between the current trend line and its value two bars prior is filled, colored green for bullish trends (upward movement) or red for bearish trends (downward movement), providing a visual cue of trend strength.

Signal Generation: Buy signals occur when the trend line crosses above its value two bars ago, and sell signals occur when it crosses below, with optional filtering to reduce signal noise (based on bar timing logic). Signals can be restricted to a 9:00–15:00 UTC trading window.

Stop-Loss Ticks: For each signal, the indicator calculates the distance to the trend line (acting as a stop-loss level) in ticks, using a user-defined tick size (default 0.25 for MES). These are displayed as labels below/above the signal.

Time Filter: An optional filter limits signals to 9:00–15:00 UTC, aligning with active trading sessions like the US market open.

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to avoid unrealistic results associated with non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Multiplier: Adjust the ATR multiplier (default 1.0) to control trend line sensitivity. Higher values widen the stop-loss distance.

Common Period: Set the ATR and MFI/RSI period (default 14) for trend calculations.

No Volume Data: Enable if volume data is unavailable (e.g., for certain forex pairs), switching from MFI to RSI.

Tick Size: Set the tick size for stop-loss calculations (default 0.25 for MES futures).

Show Buy/Sell Signals: Toggle signal labels (default enabled).

Show Stop Loss Ticks: Toggle stop-loss tick labels (default enabled).

Use Time Filter: Restrict signals to 9:00–15:00 UTC (default disabled).

Use Filtered Signals: Enable to reduce signal frequency using bar timing logic (default enabled).

Interpret Signals:

Buy Signal: A blue “BUY” label below the bar indicates a potential long entry (trend line crossover, passing filters).

Sell Signal: A red “SELL” label above the bar indicates a potential short entry (trend line crossunder, passing filters).

Trend Zone: Green fill suggests bullish momentum; red fill suggests bearish momentum.

Stop-Loss Ticks: Gray labels show the stop-loss distance in ticks, helping with risk management.

Monitor Context: Use the trend line and filled zone to confirm the market’s direction before acting on signals.

Unique Features

Adaptive Trend Line: Combines ATR with MFI or RSI to create a responsive trend line that adjusts to volatility and market conditions.

Tick-Based Stop-Loss: Displays stop-loss distances in ticks, customizable for specific instruments, aiding precise risk management.

Signal Filtering: Optional bar timing logic reduces false signals, improving reliability in choppy markets.

Trend Zone Visualization: The filled zone between trend line values enhances trend clarity, making it easier to assess momentum.

Time-Restricted Trading: Optional 9:00–15:00 UTC filter aligns signals with high-liquidity sessions.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume spikes) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in highly volatile or low-liquidity markets due to ATR-based calculations.

The 9:00–15:00 UTC time filter may not suit all markets; disable it for 24-hour assets like forex or crypto.

Stop-loss tick calculations assume consistent tick sizes; verify compatibility with your instrument.

This indicator is designed for traders seeking a robust, trend-following tool with customizable risk management and signal filtering, optimized for active trading sessions.

Adaptive Freedom Machine w/labelsAdaptive Freedom Machine w/ Labels

Overview

The Adaptive Freedom Machine w/ Labels is a versatile Pine Script indicator designed to assist traders in identifying buy and sell opportunities across various market conditions (trending, ranging, or volatile). It combines Exponential Moving Averages (EMAs), Relative Strength Index (RSI), Average True Range (ATR), and customizable time filters to generate actionable signals. The indicator overlays on the price chart, displaying EMAs, a dynamic cloud, scaled RSI levels, buy/sell signals, and market condition labels, making it suitable for swing trading, day trading, or scalping.

What It Does

This indicator generates buy and sell signals based on the interaction of two EMAs, filtered by RSI thresholds, ATR-based volatility, and user-defined time windows. It adapts to the selected market condition by adjusting EMA lengths, RSI thresholds, and trading hours. A dynamic cloud highlights trend direction or neutral zones, and candlestick bodies are colored in neutral conditions for clarity. A table displays real-time trend and volatility status.

How It Works

The indicator uses the following components:

EMAs: Two EMAs (short and long) are calculated on a user-selected timeframe (1, 5, 15, 30, or 60 minutes). Their crossover or crossunder generates potential buy/sell signals, with lengths adjusted based on the market condition (e.g., longer EMAs for trending markets, shorter for ranging).

Dynamic Cloud: The area between the EMAs forms a cloud, colored green for uptrends, red for downtrends, or a user-defined color (default yellow) for neutral zones (when EMAs are close, determined by an ATR-based threshold). Users can widen the cloud for visibility.

RSI Filter: RSI is scaled to price levels and plotted on the chart (optional). Signals are filtered to ensure RSI is within user-defined buy/sell thresholds and not in overbought/oversold zones, with thresholds tailored to the market condition.

ATR Volatility Filter: An optional filter ensures signals occur during sufficient volatility (ATR(14) > SMA(ATR, 20)).

Time Filter: Signals are restricted to a user-defined or market-specific time window (e.g., 10:00–15:00 UTC for volatile markets), with an option for custom hours.

Visual Aids: Buy/sell signals appear as green triangles (buy) or red triangles (sell). Candlesticks in neutral zones are colored (default yellow). A table in the top-right corner shows the current trend (Uptrend, Downtrend, Neutral) and volatility (High or Low).

The indicator ensures compatibility with standard chart types (e.g., candlestick charts) to produce realistic signals, avoiding non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Timeframe: Choose a timeframe (1, 5, 15, 30, or 60 minutes) to align with your trading style.

Market Condition: Select one market condition (Trending, Ranging, or Volatile). Volatile is the default if none is selected. Only one condition can be active.

Filters:

Enable/disable the ATR volatility filter to trade only in high-volatility periods.

Enable the time filter and choose default hours (specific to the market condition) or set custom UTC hours.

Cloud Settings: Adjust the cloud width, neutral zone threshold, and color. Enable/disable the neutral cloud.

RSI Display: Toggle the scaled RSI and its thresholds on the chart.

Interpret Signals:

Buy Signal: A green triangle below the bar indicates a potential long entry (EMA crossover, RSI above buy threshold, within time window, and passing volatility filter).

Sell Signal: A red triangle above the bar indicates a potential short entry (EMA crossunder, RSI below sell threshold, within time window, and passing volatility filter).

Neutral Zone: Yellow candlesticks and cloud (if enabled) suggest a lack of clear trend; avoid trading or use for range-bound strategies.

Monitor the Table: Check the top-right table for real-time trend (Uptrend, Downtrend, Neutral) and volatility (High or Low) to confirm market context.

Unique Features

Adaptive Parameters: Automatically adjusts EMA lengths, RSI thresholds, and trading hours based on the selected market condition, reducing manual tweaking.

Neutral Zone Detection: Uses an ATR-based threshold to identify low-trend periods, helping traders avoid choppy markets.

Scaled RSI Visualization: Plots RSI and thresholds directly on the price chart, making it easier to assess momentum relative to price action.

Flexible Time Filtering: Supports both default and custom UTC-based trading windows, ideal for day traders targeting specific sessions.

Dynamic Cloud: Enhances trend visualization with customizable width and neutral zone coloring, improving readability.

Notes

Use on standard candlestick or bar charts to ensure realistic signals.

Test the indicator on a demo account to understand its behavior in your chosen market and timeframe.

Adjust settings to match your trading strategy, but avoid over-optimizing for past data.

The indicator is not a standalone system; combine it with other analysis (e.g., support/resistance, news events) for better results.

Limitations

Signals may lag in fast-moving markets due to EMA-based calculations.

Neutral zone detection may vary in extremely volatile or illiquid markets.

Time filters are UTC-based; ensure your platform’s timezone settings align.

This indicator is designed for traders seeking a customizable, trend-following tool that adapts to different market environments while providing clear visual cues and robust filtering.

Alert on Candle CloseAlert on Candle Close is a simple indicator allowing you to set alerts when a candlestick closes.

Instructions for use

From the chart window, click on "Indicators" and search for "Alert on Candle Close".

Click on "Alert on Candle Close" to add the indicator to your chart. Click on the star icon to add it to your favourites to easily access later.

Set your chart timeframe to the timeframe you wish to alert on. For example, to create an alert when a 4h candlestick closes, set your chart to the "4h" timeframe.

Hover over the "Alert on Candle Close" indicator which has been added to your chart and click the ellipsis "..." icon, then click "Add alert on Alert on Candle Close" or use the keyboard shortcut "Alt+A" from the chart.

In the alert pop-up window, make sure "Condition" is set to "Alert on Candle Close" and "Trigger" is set to "Once Per Bar".

Optionally, you can set a custom expiry for the alert, give the alert a name and customise the alert message. You can configure notification settings from the "Notifications" tab.

Click "Create" and your alert is set up!

Each alert is tied to the timeframe and chart it was created on, so you can change the timeframe or asset and create more alerts by repeating the above process.

Note : this indicator is only designed to work with time-based chart types, such as Bars, Candles or Heikin Ashi. It will not work for non-time charts such as Renko.

FAQs

Why do my alerts sometimes not fire as soon as the candle closes?

This is a limitation with Pine Script's execution model. Indicators are calculated whenever a price or volume change occurs i.e. when a new trade happens. For illiquid or slow moving markets, there may be some time between when a candle closes and the next trade, leading to a delay in the alert triggering. The alert will trigger on the next tick of data on the chart.

Why can't I create more alerts?

TradingView has a limit on the number of active technical alerts you can have based on your membership tier. To configure more alerts, consider upgrading your TradingView plan to a higher tier. See a comparison of TradingView plans at www.tradingview.com

My alert only fired once, how can I get it to keep working?

When configuring the alert in the alert pop-up window, make sure you set "Trigger" to "Once Per Bar" and "Expiration" to "Open-ended alert".

Multi-Session Volume Profile Suite [MarkitTick]💡 This indicator provides a sophisticated, institutional-grade Volume Profile analysis suite that renders multiple temporal profiles simultaneously. It is designed for traders utilizing Auction Market Theory who require a holistic view of where value is being established across Daily, Weekly, and Monthly timeframes, alongside custom intraday sessions. By bypassing standard built-in functions in favor of a custom array-based calculation engine, this tool offers granular control over Value Area logic, Point of Control (POC) migration, and multi-timeframe confluence detection.

✨ Originality and Utility

Standard Volume Profile tools often limit traders to a single timeframe or the visible range of the chart. This creates a fragmented view of the market, where a trader might see the daily value but miss the context of the weekly or monthly auction.

This script solves that problem by layering three distinct higher-timeframe profiles (Daily, Weekly, Monthly) plus three customizable intraday session profiles onto a single chart.

● Key Differentiators

Confluence Detection Engine: The script mathematically calculates when the Points of Control (POC) of different timeframes overlap (e.g., Daily POC inside Weekly POC). It explicitly highlights these high-probability zones with specific labels (e.g., "TRIPLE CONFLUENCE"), automating the search for key support/resistance levels.

POC Migration Tracking: Unlike static profiles, this tool tracks the "Shift" of the POC. It visualizes whether value is migrating higher (▲), lower (▼), or remaining neutral (=) compared to the previous period, providing immediate insight into the trend's acceptance.

Synthetic Chart Protection: The script includes logic to detect and prevent usage on non-standard chart types like Heikin Ashi or Renko, ensuring that the volume data processed is accurate and not subject to the repainting often found in synthetic OHLC variations.

🔬 Methodology and Concepts

The core engine relies on a custom implementation of the Volume Profile formula using dynamic arrays. It does not simply pull pre-calculated data but processes the tick volume of the underlying asset relative to price action.

• Volumetric Binning

The script divides the price range of a specific period (e.g., a Day) into a user-defined number of "rows" (bins). As price trades within a specific bin, the corresponding volume is accumulated.

Point of Control (POC): The bin with the highest accumulated volume is identified as the POC. This represents the "Fair Value" or the mode of the distribution for that period.

Value Area (VA): The script calculates the total volume of the profile and then identifies the range surrounding the POC that contains a specific percentage (default 70%) of that volume. It uses a dual-scanning algorithm that expands upwards or downwards from the POC based on which adjacent row has higher volume, mimicking the auction process of testing prices.

• Exact-Anchor Pivots

Simultaneously, the script tracks "Exact-Anchor" pivots. Unlike standard pivots that settle at the close, these track the absolute High and Low of the period (Daily/Weekly/Monthly) in real-time and extend them until a new period begins.

🎨 Visual Guide

The indicator uses a color-coded hierarchy to distinguish between timeframes. Understanding this visual language is critical for interpreting the data.

● Profile Hierarchy (Default Theme)

Daily Profile (Yellow/Gold): Represents the immediate, short-term auction.

Solid Line: Daily POC.

Dotted Line: Daily Value Area High (VAH) and Low (VAL).

Weekly Profile (Blue): Represents the intermediate auction. A solid Blue line indicates the Weekly POC.

Monthly Profile (Purple): Represents the macro auction. A solid Purple line indicates the Monthly POC.

● Labels and Symbols

Right-Side Labels: At the end of profile lines, text labels display the exact price of the POC.

Shift Arrows (▲ / ▼): Located inside the POC label, these arrows indicate the direction the POC has moved relative to the previous period's POC. An Up arrow (▲) suggests buyers are accepting higher prices.

Confluence Labels: If enabled, a text box appears near price action stating "POC CONFLUENCE" or "TRIPLE CONFLUENCE" when the POCs of different timeframes align within a tight margin.

Block Symbol (⬛): A small block icon may appear above bars to denote the center of a specific session's time window.

● Pivot Lines

Orange Lines: Previous Daily High (PDH) and Low (PDL).

Green Dashed Lines: Previous Weekly High (PWH) and Low (PWL).

Red Dotted Lines: Previous Monthly High (PMH) and Low (PML).

White Dashed Line: New York Midnight Open price (if enabled).

📖 How to Use

This suite is designed for "Contextual Trading." It answers the question: Where are we relative to value?

• Trend Acceptance

Observe the Shift Arrows on the POC labels. In a healthy uptrend, you should see a sequence of Daily and Weekly profiles with (▲) arrows, indicating that the market is validating higher prices as fair value. If price rises but the POC remains lower or shifts down, it may indicate a "weak high" or a potential reversal (divergence between price and value).

• Support and Resistance

The POC lines act as high-probability support and resistance. Price returning to a Weekly (Blue) or Monthly (Purple) POC often results in a reaction, as these are areas of significant historical agreement between buyers and sellers.

• The Confluence Play

Pay special attention when the "Confluence" label appears. When a Daily POC aligns with a Weekly or Monthly POC, that specific price level possesses reinforced structural importance. A rejection from such a level is a strong signal; a breakout through such a level often leads to an explosive move as value transitions rapidly.

⚙️ Inputs and Settings

The script is highly customizable via the settings menu.

● General Settings

Row Resolution: Determines the granularity of the profile. Higher numbers (e.g., 100) create smoother, more detailed profiles but use more calculation resources.

Value Area %: Default is 70.0, representing the standard deviation of value.

Show POC Shift: Toggles the (▲/▼) comparison logic.

● Profile Scope

Show Daily/Weekly/Monthly: Checkboxes to individually enable or disable specific timeframe profiles.

Session Lookback: Controls how many historical days/weeks the profiles are kept on the chart.

● Pivots (PDH/PMH/NYM)

Show Pivots: Enables the High/Low lines for previous periods.

Show NY Midnight: Specifically toggles the opening price of the New York session (00:00 EST).

● Alerts

Approach Distance: Sets the sensitivity (in ticks) for alerts when price nears a key POC level.

🔍 Deconstruction of the Underlying Scientific and Academic Framework

This indicator is grounded in Auction Market Theory (AMT) and statistical distribution analysis.

• The Market as a Mechanism

AMT postulates that the primary purpose of the market is to facilitate trade. Price advertises opportunity, while Time regulates the opportunity. Volume is the validation of that price. When the market spends significant time and transacts significant volume at a specific level, it establishes "Value."

• Gaussian Distribution and Central Limit Theorem

A Volume Profile is essentially a histogram of volume over price, often resembling a Gaussian (Normal) Distribution or "Bell Curve" when the market is balanced.

POC (Mode): The peak of the curve. Mathematically, this is the mode of the dataset—the price occurring with the highest frequency (volume).

Value Area (Standard Deviation): In a normal distribution, approximately 68.2% of data points fall within one standard deviation of the mean. This script defaults to a 70% Value Area to approximate this statistical boundary. Prices outside this area are considered statistically significant anomalies or "imbalanced."

• Confluence and Probability

The "Confluence" feature leverages the intersection of independent datasets. If the mode (POC) of a short-term distribution (Daily) aligns with the mode of a long-term distribution (Weekly), the probability of that price representing "True Value" increases exponentially. This aligns with statistical principles where overlapping data clusters suggest a stronger underlying signal amidst market noise.

⚠️ Disclaimer

All provided scripts and indicators are strictly for educational exploration and must not be interpreted as financial advice or a recommendation to execute trades. I expressly disclaim all liability for any financial losses or damages that may result, directly or indirectly, from the reliance on or application of these tools. Market participation carries inherent risk where past performance never guarantees future returns, leaving all investment decisions and due diligence solely at your own discretion.

Relative Equal Highs/Lows by tncylyvRelative Equal Highs/Lows

Relative Equal Highs/Lows (REH/REL) is a technical analysis utility designed to identify significant liquidity pools based on Smart Money Concepts (SMC). Unlike standard support and resistance tools that look for single touches, this script identifies sequences of swing points that form relatively flat or slightly stepping structures.

These structures typically represent engineered liquidity or inducement levels where stop-losses are clustered. The indicator visualizes these areas and projects the price level that is likely to be targeted by future price action.

Core Concepts

Relative Structure Detection

Markets rarely form perfectly equal double tops or bottoms to the exact tick. This indicator detects "Relative" Equal Highs or Lows by analyzing a sequence of swing points. It looks for a user-defined number of swings (default is 3) that occur within a specific point threshold of each other, forming a trendline liquidity or flat structure.

Validation System (Noise Reduction)

A distinct feature of this script is its validation mechanism. When a potential pattern is detected, it is not drawn immediately. Instead, it enters a "pending" state for a specific number of bars.

• If price immediately breaks the level during this wait period, the pattern is discarded as noise.

• If the level remains unmitigated after the wait period, it is confirmed and drawn on the chart.

This logic helps reduce clutter and false signals caused by immediate volatility.

Standard Data Integrity

The indicator explicitly requests standard ticker data for all calculations. This ensures that even if you are viewing Heikin Ashi, Renko, or other synthetic chart types, the liquidity levels remain accurate to the real market OHLC prices.

Key Features

• Customizable Swing Detection: You can define how many swings are required to form a pattern (e.g., 2 for double tops/bottoms, 3 or more for extended liquidity pools).

• Gap Management: Options to enforce a minimum number of bars between swings to ensure the structure covers a significant timeframe.

• Mitigation Handling: Choose exactly how a level is considered broken (Wick Touch, Candle Close, or Sweep/Rejection).

• Visual Connectors: Optional dotted lines connect the specific pivot points used to derive the level, helping you visualize the structure of the liquidity.

Settings Overview

Pivot Length

Determines the lookback period to define a Swing High or Low. Higher values will identify more significant market structures.

Max Step Difference (Points)

This is the tolerance range allowed between consecutive swing points. Since this calculates based on raw points, this value must be adjusted significantly depending on the asset class (e.g., Forex pairs versus Crypto or Indices) to match the price scale of the instrument.

Required Swings Amount

The number of swing points required to confirm a pattern.

Min Bars Between Swings

Ensures that the detected pivots are distinct and spaced out by a minimum amount of time.

Validation Wait (Bars)

The duration a pattern must survive before being rendered. Increasing this value filters out structures that are immediately swept.

Mitigation Mode

• Wick Touch: The level is mitigated as soon as a wick touches it.

• Close Through: The level is only mitigated if a candle closes beyond it.

• Sweep Reject: The level is mitigated only if price sweeps it but closes back inside the range.

Visualization

Controls the colors, line styles, and line widths for both active and mitigated levels. Connectors can be toggled on or off to show the path of the swing points.

VDUB Bands - MTF WMA+ATR Volatility Lanes (6 Alerts)VDUB Bands draws volatility-scaled “trend lanes” around a Weighted Moving Average (WMA) using ATR (or a WMA of True Range). It can display up to four tiers (L1–L4), with higher tiers sourced from higher timeframes to show local structure → higher-timeframe structure on a single chart.

────────────────────────────────────────