MAG8 Breadth RSI This indicator is for my personal monitoring breadth of MAG 8 , including AVGO for use to trade spy/es and qqq/nq.

A green bar over 6 translates to 6 out of the 8 stocks have RSI's<30. Conversely a red indicator at 6 would indicate 6 out of 8 are overbought, RSI >70.

Extreme 6-8 of 8 either overbought (red) or oversold (green)

Moderate 4-5 of 8 either overbought (red) or oversold (green)

No Signal 0-3 of 8 either overbought (red) or oversold (green)

Not trading advice but thought I would share.

Search in scripts for "spy"

NEW PRICE ACTION ALGO (v2)Updated price action indicator for day trading QQQ,SPY & IWM on the 5-6min chart

BC_Monthly Strength Armor [xAI] - v32.2 MTF LOCKED + SCORE FIXED🛡️ **Monthly Strength Armor - v32.2**

**Multi-Timeframe Institutional Edge Indicator**

🔥 **Detects smart money moves** using:

- **Monthly Range Position (Score 0–100)**

- **Higher High/Low Trend Structure (Daily/Weekly/Monthly)**

- **OBV Trend Lock (100% consistent)**

- **Larry Williams OHLC Institutional Patterns (Daily)**

📊 **MTF Table (locked values — no flicker)**

| Daily | Weekly | Monthly |

|-------|--------|---------|

| OBV | Trend | Score |

| ATR% | Larry | PMH/PML |

🎯 **Confluence Alerts**

- **3-TF Bullish / Bearish**

- **ULTRA BUY/SELL** (all TFs aligned)

- **Larry Institutional Buying/Selling**

✅ **No repaint | No warnings | Live-ready**

Built for **NVDA, MSFT, URA, QQQ, SPY**

*By @TedPrime x Grok @ xAI*

VWAP + Volume Spikes See Where Smart Money ExhaustsVolume tells the truth. VWAP tells the bias. This script shows both — live.

If you trade intraday momentum, reversals, or liquidity sweeps, this indicator is built for you.

It shows where volume spikes hit extreme levels, anchored around VWAP and its dynamic bands, so you can instantly spot capitulation or hidden absorption.

🎯 What This Indicator Does

✅ Plots VWAP — session-anchored, updates automatically

✅ Adds dynamic VWAP bands — standard deviation envelopes showing volatility context

✅ Highlights volume spikes — colored candles + background for abnormal prints

✅ Includes alerts — “Volume Spike”, “VWAP Cross”, or a combined alert with direction

✅ Clean visual design — instantly readable in fast markets

It’s your visual orderflow radar — whether you’re trading gold, indices, or small caps.

🔍 Why It Works

Institutions build and unwind positions around VWAP.

Retail often chases volume… this script shows you when that volume becomes too extreme.

A spike above VWAP near resistance? → Likely distribution.

A spike below VWAP near support? → Likely capitulation.

Combine volume exhaustion + VWAP context, and you’ll see market turning points form before most indicators react.

⚙️ Inputs You Can Tune

Bands lookback: adjusts how reactive the VWAP bands are

Band width (σ): set how tight or wide your deviation envelope is

Volume baseline length: controls how “abnormal” a spike must be

Spike threshold: multiplier vs. average volume

Toggle color-coding, bands, and labels

Default settings work well across 1m–15m intraday charts and 1h–4h swing frames.

💡 How Traders Use It

1️⃣ Fade Parabolics:

When a green spike candle pierces upper VWAP band on high volume → smart money unloading.

Look for rejection and short into VWAP.

2️⃣ Catch Capitulations:

When a red spike candle dumps below lower VWAP band → panic selling.

Watch for stabilization and long back to VWAP.

3️⃣ VWAP Rotation Plays:

Alerts for price crossing VWAP help you spot shift in intraday control.

Above VWAP = buyers in charge.

Below VWAP = sellers in charge.

🧠 Best Practices

Pair it with Volume Profile or Delta/Flow tools to confirm exhaustion.

Don’t chase — wait for spike confirmation + reversal candle.

Use it on liquid tickers (NASDAQ, SPY, GOLD, BTC, etc.).

Great for Dux-style small-cap shorts or index pullbacks.

🔔 Alerts Ready

Choose from:

Volume Spike (single-bar explosion)

VWAP Cross Up/Down (trend shift confirmation)

One Combined Alert (any signal, includes ticker, price, and volume)

Set once — get real-time push notifications, Telegram, or webhook signals.

📊 My Favorite Setups

US100 / NASDAQ: fade rallies above VWAP + spike

Gold / Silver: trade reversals from VWAP bands

Small caps: short back-side after volume climax

ES, DAX, Oil: scalp VWAP rotation with confluence

❤️ Support This Work

I release free and premium scripts weekly — combining smart money concepts, VWAP tools, and volume analytics.

👉 Follow me on TradingView for more indicators and setups.

👉 Comment “🔥” if you want me to post the multi-timeframe VWAP + Volume Pressure version next.

👉 Share this with your team — it helps the community grow.

Hellenic EMA Matrix - PremiumHellenic EMA Matrix - Alpha Omega Premium

Complete User Guide

Table of Contents

Introduction

Indicator Philosophy

Mathematical Constants

EMA Types

Settings

Trading Signals

Visualization

Usage Strategies

FAQ

Introduction

Hellenic EMA Matrix is a premium indicator based on mathematical constants of nature: Phi (Phi - Golden Ratio), Pi (Pi), e (Euler's number). The indicator uses these universal constants to create dynamic EMAs that adapt to the natural rhythms of the market.

Key Features:

6 EMA types based on mathematical constants

Premium visualization with Neon Glow and Gradient Clouds

Automatic Fast/Mid/Slow EMA sorting

STRONG signals for powerful trends

Pulsing Ribbon Bar for instant trend assessment

Works on all timeframes (M1 - MN)

Indicator Philosophy

Why Mathematical Constants?

Traditional EMAs use arbitrary periods (9, 21, 50, 200). Hellenic Matrix goes further, using universal mathematical constants found in nature:

Phi (1.618) - Golden Ratio: galaxy spirals, seashells, human body proportions

Pi (3.14159) - Pi: circles, waves, cycles

e (2.71828) - Natural logarithm base: exponential growth, radioactive decay

Markets are also a natural system composed of millions of participants. Using mathematical constants allows tuning into the natural rhythms of market cycles.

Mathematical Constants

Phi (Phi) - Golden Ratio

Phi = 1.618033988749895

Properties:

Phi² = Phi + 1 = 2.618

Phi³ = 4.236

Phi⁴ = 6.854

Application: Ideal for trending movements and Fibonacci corrections

Pi (Pi) - Pi Number

Pi = 3.141592653589793

Properties:

2Pi = 6.283 (full circle)

3Pi = 9.425

4Pi = 12.566

Application: Excellent for cyclical markets and wave structures

e (Euler) - Euler's Number

e = 2.718281828459045

Properties:

e² = 7.389

e³ = 20.085

e⁴ = 54.598

Application: Suitable for exponential movements and volatile markets

EMA Types

1. Phi (Phi) - Golden Ratio EMA

Description: EMA based on the golden ratio

Period Formula:

Period = Phi^n × Base Multiplier

Parameters:

Phi Power Level (1-8): Power of Phi

Phi¹ = 1.618 → ~16 period (with Base=10)

Phi² = 2.618 → ~26 period

Phi³ = 4.236 → ~42 period (recommended)

Phi⁴ = 6.854 → ~69 period

Recommendations:

Phi² or Phi³ for day trading

Phi⁴ or Phi⁵ for swing trading

Works excellently as Fast EMA

2. Pi (Pi) - Circular EMA

Description: EMA based on Pi for cyclical movements

Period Formula:

Period = Pi × Multiple × Base Multiplier

Parameters:

Pi Multiple (1-10): Pi multiplier

1Pi = 3.14 → ~31 period (with Base=10)

2Pi = 6.28 → ~63 period (recommended)

3Pi = 9.42 → ~94 period

Recommendations:

2Pi ideal as Mid or Slow EMA

Excellently identifies cycles and waves

Use on volatile markets (crypto, forex)

3. e (Euler) - Natural EMA

Description: EMA based on natural logarithm

Period Formula:

Period = e^n × Base Multiplier

Parameters:

e Power Level (1-6): Power of e

e¹ = 2.718 → ~27 period (with Base=10)

e² = 7.389 → ~74 period (recommended)

e³ = 20.085 → ~201 period

Recommendations:

e² works excellently as Slow EMA

Ideal for stocks and indices

Filters noise well on lower timeframes

4. Delta (Delta) - Adaptive EMA

Description: Adaptive EMA that changes period based on volatility

Period Formula:

Period = Base Period × (1 + (Volatility - 1) × Factor)

Parameters:

Delta Base Period (5-200): Base period (default 20)

Delta Volatility Sensitivity (0.5-5.0): Volatility sensitivity (default 2.0)

How it works:

During low volatility → period decreases → EMA reacts faster

During high volatility → period increases → EMA smooths noise

Recommendations:

Works excellently on news and sharp movements

Use as Fast EMA for quick adaptation

Sensitivity 2.0-3.0 for crypto, 1.0-2.0 for stocks

5. Sigma (Sigma) - Composite EMA

Description: Composite EMA combining multiple active EMAs

Composition Methods:

Weighted Average (default):

Sigma = (Phi + Pi + e + Delta) / 4

Simple average of all active EMAs

Geometric Mean:

Sigma = fourth_root(Phi × Pi × e × Delta)

Geometric mean (more conservative)

Harmonic Mean:

Sigma = 4 / (1/Phi + 1/Pi + 1/e + 1/Delta)

Harmonic mean (more weight to smaller values)

Recommendations:

Enable for additional confirmation

Use as Mid EMA

Weighted Average - most universal method

6. Lambda (Lambda) - Wave EMA

Description: Wave EMA with sinusoidal period modulation

Period Formula:

Period = Base Period × (1 + Amplitude × sin(2Pi × bar / Frequency))

Parameters:

Lambda Base Period (10-200): Base period

Lambda Wave Amplitude (0.1-2.0): Wave amplitude

Lambda Wave Frequency (10-200): Wave frequency in bars

How it works:

Period pulsates sinusoidally

Creates wave effect following market cycles

Recommendations:

Experimental EMA for advanced users

Works well on cyclical markets

Frequency = 50 for day trading, 100+ for swing

Settings

Matrix Core Settings

Base Multiplier (1-100)

Multiplies all EMA periods

Base = 1: Very fast EMAs (Phi³ = 4, 2Pi = 6, e² = 7)

Base = 10: Standard (Phi³ = 42, 2Pi = 63, e² = 74)

Base = 20: Slow EMAs (Phi³ = 85, 2Pi = 126, e² = 148)

Recommendations by timeframe:

M1-M5: Base = 5-10

M15-H1: Base = 10-15 (recommended)

H4-D1: Base = 15-25

W1-MN: Base = 25-50

Matrix Source

Data source selection for EMA calculation:

close - closing price (standard)

open - opening price

high - high

low - low

hl2 - (high + low) / 2

hlc3 - (high + low + close) / 3

ohlc4 - (open + high + low + close) / 4

When to change:

hlc3 or ohlc4 for smoother signals

high for aggressive longs

low for aggressive shorts

Manual EMA Selection

Critically important setting! Determines which EMAs are used for signal generation.

Use Manual Fast/Slow/Mid Selection

Enabled (default): You select EMAs manually

Disabled: Automatic selection by periods

Fast EMA

Fast EMA - reacts first to price changes

Recommendations:

Phi Golden (recommended) - universal choice

Delta Adaptive - for volatile markets

Must be fastest (smallest period)

Slow EMA

Slow EMA - determines main trend

Recommendations:

Pi Circular (recommended) - excellent trend filter

e Natural - for smoother trend

Must be slowest (largest period)

Mid EMA

Mid EMA - additional signal filter

Recommendations:

e Natural (recommended) - excellent middle level

Pi Circular - alternative

None - for more frequent signals (only 2 EMAs)

IMPORTANT: The indicator automatically sorts selected EMAs by their actual periods:

Fast = EMA with smallest period

Mid = EMA with middle period

Slow = EMA with largest period

Therefore, you can select any combination - the indicator will arrange them correctly!

Premium Visualization

Neon Glow

Enable Neon Glow for EMAs - adds glowing effect around EMA lines

Glow Strength:

Light - subtle glow

Medium (recommended) - optimal balance

Strong - bright glow (may be too bright)

Effect: 2 glow layers around each EMA for 3D effect

Gradient Clouds

Enable Gradient Clouds - fills space between EMAs with gradient

Parameters:

Cloud Transparency (85-98): Cloud transparency

95-97 (recommended)

Higher = more transparent

Dynamic Cloud Intensity - automatically changes transparency based on EMA distance

Cloud Colors:

Phi-Pi Cloud:

Blue - when Pi above Phi (bullish)

Gold - when Phi above Pi (bearish)

Pi-e Cloud:

Green - when e above Pi (bullish)

Blue - when Pi above e (bearish)

2 layers for volumetric effect

Pulsing Ribbon Bar

Enable Pulsing Indicator Bar - pulsing strip at bottom/top of chart

Parameters:

Ribbon Position: Top / Bottom (recommended)

Pulse Speed: Slow / Medium (recommended) / Fast

Symbols and colors:

Green filled square - STRONG BULLISH

Pink filled square - STRONG BEARISH

Blue hollow square - Bullish (regular)

Red hollow square - Bearish (regular)

Purple rectangle - Neutral

Effect: Pulsation with sinusoid for living market feel

Signal Bar Highlights

Enable Signal Bar Highlights - highlights bars with signals

Parameters:

Highlight Transparency (88-96): Highlight transparency

Highlight Style:

Light Fill (recommended) - bar background fill

Thin Line - bar outline only

Highlights:

Golden Cross - green

Death Cross - pink

STRONG BUY - green

STRONG SELL - pink

Show Greek Labels

Shows Greek alphabet letters on last bar:

Phi - Phi EMA (gold)

Pi - Pi EMA (blue)

e - Euler EMA (green)

Delta - Delta EMA (purple)

Sigma - Sigma EMA (pink)

When to use: For education or presentations

Show Old Background

Old background style (not recommended):

Green background - STRONG BULLISH

Pink background - STRONG BEARISH

Blue background - Bullish

Red background - Bearish

Not recommended - use new Gradient Clouds and Pulsing Bar

Info Table

Show Info Table - table with indicator information

Parameters:

Position: Top Left / Top Right (recommended) / Bottom Left / Bottom Right

Size: Tiny / Small (recommended) / Normal / Large

Table contents:

EMA list - periods and current values of all active EMAs

Effects - active visual effects

TREND - current trend state:

STRONG UP - strong bullish

STRONG DOWN - strong bearish

Bullish - regular bullish

Bearish - regular bearish

Neutral - neutral

Momentum % - percentage deviation of price from Fast EMA

Setup - current Fast/Slow/Mid configuration

Trading Signals

Show Golden/Death Cross

Golden Cross - Fast EMA crosses Slow EMA from below (bullish signal) Death Cross - Fast EMA crosses Slow EMA from above (bearish signal)

Symbols:

Yellow dot "GC" below - Golden Cross

Dark red dot "DC" above - Death Cross

Show STRONG Signals

STRONG BUY and STRONG SELL - the most powerful indicator signals

Conditions for STRONG BULLISH:

EMA Alignment: Fast > Mid > Slow (all EMAs aligned)

Trend: Fast > Slow (clear uptrend)

Distance: EMAs separated by minimum 0.15%

Price Position: Price above Fast EMA

Fast Slope: Fast EMA rising

Slow Slope: Slow EMA rising

Mid Trending: Mid EMA also rising (if enabled)

Conditions for STRONG BEARISH:

Same but in reverse

Visual display:

Green label "STRONG BUY" below bar

Pink label "STRONG SELL" above bar

Difference from Golden/Death Cross:

Golden/Death Cross = crossing moment (1 bar)

STRONG signal = sustained trend (lasts several bars)

IMPORTANT: After fixes, STRONG signals now:

Work on all timeframes (M1 to MN)

Don't break on small retracements

Work with any Fast/Mid/Slow combination

Automatically adapt thanks to EMA sorting

Show Stop Loss/Take Profit

Automatic SL/TP level calculation on STRONG signal

Parameters:

Stop Loss (ATR) (0.5-5.0): ATR multiplier for stop loss

1.5 (recommended) - standard

1.0 - tight stop

2.0-3.0 - wide stop

Take Profit R:R (1.0-5.0): Risk/reward ratio

2.0 (recommended) - standard (risk 1.5 ATR, profit 3.0 ATR)

1.5 - conservative

3.0-5.0 - aggressive

Formulas:

LONG:

Stop Loss = Entry - (ATR × Stop Loss ATR)

Take Profit = Entry + (ATR × Stop Loss ATR × Take Profit R:R)

SHORT:

Stop Loss = Entry + (ATR × Stop Loss ATR)

Take Profit = Entry - (ATR × Stop Loss ATR × Take Profit R:R)

Visualization:

Red X - Stop Loss

Green X - Take Profit

Levels remain active while STRONG signal persists

Trading Signals

Signal Types

1. Golden Cross

Description: Fast EMA crosses Slow EMA from below

Signal: Beginning of bullish trend

How to trade:

ENTRY: On bar close with Golden Cross

STOP: Below local low or below Slow EMA

TARGET: Next resistance level or 2:1 R:R

Strengths:

Simple and clear

Works well on trending markets

Clear entry point

Weaknesses:

Lags (signal after movement starts)

Many false signals in ranging markets

May be late on fast moves

Optimal timeframes: H1, H4, D1

2. Death Cross

Description: Fast EMA crosses Slow EMA from above

Signal: Beginning of bearish trend

How to trade:

ENTRY: On bar close with Death Cross

STOP: Above local high or above Slow EMA

TARGET: Next support level or 2:1 R:R

Application: Mirror of Golden Cross

3. STRONG BUY

Description: All EMAs aligned + trend + all EMAs rising

Signal: Powerful bullish trend

How to trade:

ENTRY: On bar close with STRONG BUY or on pullback to Fast EMA

STOP: Below Fast EMA or automatic SL (if enabled)

TARGET: Automatic TP (if enabled) or by levels

TRAILING: Follow Fast EMA

Entry strategies:

Aggressive: Enter immediately on signal

Conservative: Wait for pullback to Fast EMA, then enter on bounce

Pyramiding: Add positions on pullbacks to Mid EMA

Position management:

Hold while STRONG signal active

Exit on STRONG SELL or Death Cross appearance

Move stop behind Fast EMA

Strengths:

Most reliable indicator signal

Doesn't break on pullbacks

Catches large moves

Works on all timeframes

Weaknesses:

Appears less frequently than other signals

Requires confirmation (multiple conditions)

Optimal timeframes: All (M5 - D1)

4. STRONG SELL

Description: All EMAs aligned down + downtrend + all EMAs falling

Signal: Powerful bearish trend

How to trade: Mirror of STRONG BUY

Visual Signals

Pulsing Ribbon Bar

Quick market assessment at a glance:

Symbol Color State

Filled square Green STRONG BULLISH

Filled square Pink STRONG BEARISH

Hollow square Blue Bullish

Hollow square Red Bearish

Rectangle Purple Neutral

Pulsation: Sinusoidal, creates living effect

Signal Bar Highlights

Bars with signals are highlighted:

Green highlight: STRONG BUY or Golden Cross

Pink highlight: STRONG SELL or Death Cross

Gradient Clouds

Colored space between EMAs shows trend strength:

Wide clouds - strong trend

Narrow clouds - weak trend or consolidation

Color change - trend change

Info Table

Quick reference in corner:

TREND: Current state (STRONG UP, Bullish, Neutral, Bearish, STRONG DOWN)

Momentum %: Movement strength

Effects: Active visual effects

Setup: Fast/Slow/Mid configuration

Usage Strategies

Strategy 1: "Golden Trailing"

Idea: Follow STRONG signals using Fast EMA as trailing stop

Settings:

Fast: Phi Golden (Phi³)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base Multiplier: 10

Timeframe: H1, H4

Entry rules:

Wait for STRONG BUY

Enter on bar close or on pullback to Fast EMA

Stop below Fast EMA

Management:

Hold position while STRONG signal active

Move stop behind Fast EMA daily

Exit on STRONG SELL or Death Cross

Take Profit:

Partially close at +2R

Trail remainder until exit signal

For whom: Swing traders, trend followers

Pros:

Catches large moves

Simple rules

Emotionally comfortable

Cons:

Requires patience

Possible extended drawdowns on pullbacks

Strategy 2: "Scalping Bounces"

Idea: Scalp bounces from Fast EMA during STRONG trend

Settings:

Fast: Delta Adaptive (Base 15, Sensitivity 2.0)

Mid: Phi Golden (Phi²)

Slow: Pi Circular (2Pi)

Base Multiplier: 5

Timeframe: M5, M15

Entry rules:

STRONG signal must be active

Wait for price pullback to Fast EMA

Enter on bounce (candle closes above/below Fast EMA)

Stop behind local extreme (15-20 pips)

Take Profit:

+1.5R or to Mid EMA

Or to next level

For whom: Active day traders

Pros:

Many signals

Clear entry point

Quick profits

Cons:

Requires constant monitoring

Not all bounces work

Requires discipline for frequent trading

Strategy 3: "Triple Filter"

Idea: Enter only when all 3 EMAs and price perfectly aligned

Settings:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (3Pi)

Base Multiplier: 15

Timeframe: H4, D1

Entry rules (LONG):

STRONG BUY active

Price above all three EMAs

Fast > Mid > Slow (all aligned)

All EMAs rising (slope up)

Gradient Clouds wide and bright

Entry:

On bar close meeting all conditions

Or on next pullback to Fast EMA

Stop:

Below Mid EMA or -1.5 ATR

Take Profit:

First target: +3R

Second target: next major level

Trailing: Mid EMA

For whom: Conservative swing traders, investors

Pros:

Very reliable signals

Minimum false entries

Large profit potential

Cons:

Rare signals (2-5 per month)

Requires patience

Strategy 4: "Adaptive Scalper"

Idea: Use only Delta Adaptive EMA for quick volatility reaction

Settings:

Fast: Delta Adaptive (Base 10, Sensitivity 3.0)

Mid: None

Slow: Delta Adaptive (Base 30, Sensitivity 2.0)

Base Multiplier: 3

Timeframe: M1, M5

Feature: Two different Delta EMAs with different settings

Entry rules:

Golden Cross between two Delta EMAs

Both Delta EMAs must be rising/falling

Enter on next bar

Stop:

10-15 pips or below Slow Delta EMA

Take Profit:

+1R to +2R

Or Death Cross

For whom: Scalpers on cryptocurrencies and forex

Pros:

Instant volatility adaptation

Many signals on volatile markets

Quick results

Cons:

Much noise on calm markets

Requires fast execution

High commissions may eat profits

Strategy 5: "Cyclical Trader"

Idea: Use Pi and Lambda for trading cyclical markets

Settings:

Fast: Pi Circular (1Pi)

Mid: Lambda Wave (Base 30, Amplitude 0.5, Frequency 50)

Slow: Pi Circular (3Pi)

Base Multiplier: 10

Timeframe: H1, H4

Entry rules:

STRONG signal active

Lambda Wave EMA synchronized with trend

Enter on bounce from Lambda Wave

For whom: Traders of cyclical assets (some altcoins, commodities)

Pros:

Catches cyclical movements

Lambda Wave provides additional entry points

Cons:

More complex to configure

Not for all markets

Lambda Wave may give false signals

Strategy 6: "Multi-Timeframe Confirmation"

Idea: Use multiple timeframes for confirmation

Scheme:

Higher TF (D1): Determine trend direction (STRONG signal)

Middle TF (H4): Wait for STRONG signal in same direction

Lower TF (M15): Look for entry point (Golden Cross or bounce from Fast EMA)

Settings for all TFs:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base Multiplier: 10

Rules:

All 3 TFs must show one trend

Entry on lower TF

Stop by lower TF

Target by higher TF

For whom: Serious traders and investors

Pros:

Maximum reliability

Large profit targets

Minimum false signals

Cons:

Rare setups

Requires analysis of multiple charts

Experience needed

Practical Tips

DOs

Use STRONG signals as primary - they're most reliable

Let signals develop - don't exit on first pullback

Use trailing stop - follow Fast EMA

Combine with levels - S/R, Fibonacci, volumes

Test on demo before real

Adjust Base Multiplier for your timeframe

Enable visual effects - they help see the picture

Use Info Table - quick situation assessment

Watch Pulsing Bar - instant state indicator

Trust auto-sorting of Fast/Mid/Slow

DON'Ts

Don't trade against STRONG signal - trend is your friend

Don't ignore Mid EMA - it adds reliability

Don't use too small Base Multiplier on higher TFs

Don't enter on Golden Cross in range - check for trend

Don't change settings during open position

Don't forget risk management - 1-2% per trade

Don't trade all signals in row - choose best ones

Don't use indicator in isolation - combine with Price Action

Don't set too tight stops - let trade breathe

Don't over-optimize - simplicity = reliability

Optimal Settings by Asset

US Stocks (SPY, AAPL, TSLA)

Recommendation:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base: 10-15

Timeframe: H4, D1

Features:

Use on daily for swing

STRONG signals very reliable

Works well on trending stocks

Forex (EUR/USD, GBP/USD)

Recommendation:

Fast: Delta Adaptive (Base 15, Sens 2.0)

Mid: Phi Golden (Phi²)

Slow: Pi Circular (2Pi)

Base: 8-12

Timeframe: M15, H1, H4

Features:

Delta Adaptive works excellently on news

Many signals on M15-H1

Consider spreads

Cryptocurrencies (BTC, ETH, altcoins)

Recommendation:

Fast: Delta Adaptive (Base 10, Sens 3.0)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base: 5-10

Timeframe: M5, M15, H1

Features:

High volatility - adaptation needed

STRONG signals can last days

Be careful with scalping on M1-M5

Commodities (Gold, Oil)

Recommendation:

Fast: Pi Circular (1Pi)

Mid: Phi Golden (Phi³)

Slow: Pi Circular (3Pi)

Base: 12-18

Timeframe: H4, D1

Features:

Pi works excellently on cyclical commodities

Gold responds especially well to Phi

Oil volatile - use wide stops

Indices (S&P500, Nasdaq, DAX)

Recommendation:

Fast: Phi Golden (Phi³)

Mid: e Natural (e²)

Slow: Pi Circular (2Pi)

Base: 15-20

Timeframe: H4, D1, W1

Features:

Very trending instruments

STRONG signals last weeks

Good for position trading

Alerts

The indicator supports 6 alert types:

1. Golden Cross

Message: "Hellenic Matrix: GOLDEN CROSS - Fast EMA crossed above Slow EMA - Bullish trend starting!"

When: Fast EMA crosses Slow EMA from below

2. Death Cross

Message: "Hellenic Matrix: DEATH CROSS - Fast EMA crossed below Slow EMA - Bearish trend starting!"

When: Fast EMA crosses Slow EMA from above

3. STRONG BULLISH

Message: "Hellenic Matrix: STRONG BULLISH SIGNAL - All EMAs aligned for powerful uptrend!"

When: All conditions for STRONG BUY met (first bar)

4. STRONG BEARISH

Message: "Hellenic Matrix: STRONG BEARISH SIGNAL - All EMAs aligned for powerful downtrend!"

When: All conditions for STRONG SELL met (first bar)

5. Bullish Ribbon

Message: "Hellenic Matrix: BULLISH RIBBON - EMAs aligned for uptrend"

When: EMAs aligned bullish + price above Fast EMA (less strict condition)

6. Bearish Ribbon

Message: "Hellenic Matrix: BEARISH RIBBON - EMAs aligned for downtrend"

When: EMAs aligned bearish + price below Fast EMA (less strict condition)

How to Set Up Alerts:

Open indicator on chart

Click on three dots next to indicator name

Select "Create Alert"

In "Condition" field select needed alert:

Golden Cross

Death Cross

STRONG BULLISH

STRONG BEARISH

Bullish Ribbon

Bearish Ribbon

Configure notification method:

Pop-up in browser

Email

SMS (in Premium accounts)

Push notifications in mobile app

Webhook (for automation)

Select frequency:

Once Per Bar Close (recommended) - once on bar close

Once Per Bar - during bar formation

Only Once - only first time

Click "Create"

Tip: Create separate alerts for different timeframes and instruments

FAQ

1. Why don't STRONG signals appear?

Possible reasons:

Incorrect Fast/Mid/Slow order

Solution: Indicator automatically sorts EMAs by periods, but ensure selected EMAs have different periods

Base Multiplier too large

Solution: Reduce Base to 5-10 on lower timeframes

Market in range

Solution: STRONG signals appear only in trends - this is normal

Too strict EMA settings

Solution: Try classic combination: Phi³ / Pi×2 / e² with Base=10

Mid EMA too close to Fast or Slow

Solution: Select Mid EMA with period between Fast and Slow

2. How often should STRONG signals appear?

Normal frequency:

M1-M5: 5-15 signals per day (very active markets)

M15-H1: 2-8 signals per day

H4: 3-10 signals per week

D1: 2-5 signals per month

W1: 2-6 signals per year

If too many signals - market very volatile or Base too small

If too few signals - market in range or Base too large

4. What are the best settings for beginners?

Universal "out of the box" settings:

Matrix Core:

Base Multiplier: 10

Source: close

Phi Golden: Enabled, Power = 3

Pi Circular: Enabled, Multiple = 2

e Natural: Enabled, Power = 2

Delta Adaptive: Enabled, Base = 20, Sensitivity = 2.0

Manual Selection:

Fast: Phi Golden

Mid: e Natural

Slow: Pi Circular

Visualization:

Gradient Clouds: ON

Neon Glow: ON (Medium)

Pulsing Bar: ON (Medium)

Signal Highlights: ON (Light Fill)

Table: ON (Top Right, Small)

Signals:

Golden/Death Cross: ON

STRONG Signals: ON

Stop Loss: OFF (while learning)

Timeframe for learning: H1 or H4

5. Can I use only one EMA?

No, minimum 2 EMAs (Fast and Slow) for signal generation.

Mid EMA is optional:

With Mid EMA = more reliable but rarer signals

Without Mid EMA = more signals but less strict filtering

Recommendation: Start with 3 EMAs (Fast/Mid/Slow), then experiment

6. Does the indicator work on cryptocurrencies?

Yes, works excellently! Especially good on:

Bitcoin (BTC)

Ethereum (ETH)

Major altcoins (SOL, BNB, XRP)

Recommended settings for crypto:

Fast: Delta Adaptive (Base 10-15, Sensitivity 2.5-3.0)

Mid: Pi Circular (2Pi)

Slow: e Natural (e²)

Base: 5-10

Timeframe: M15, H1, H4

Crypto market features:

High volatility → use Delta Adaptive

24/7 trading → set alerts

Sharp movements → wide stops

7. Can I trade only with this indicator?

Technically yes, but NOT recommended.

Best approach - combine with:

Price Action - support/resistance levels, candle patterns

Volume - movement strength confirmation

Fibonacci - retracement and extension levels

RSI/MACD - divergences and overbought/oversold

Fundamental analysis - news, company reports

Hellenic Matrix:

Excellently determines trend and its strength

Provides clear entry/exit points

Doesn't consider fundamentals

Doesn't see major levels

8. Why do Gradient Clouds change color?

Color depends on EMA order:

Phi-Pi Cloud:

Blue - Pi EMA above Phi EMA (bullish alignment)

Gold - Phi EMA above Pi EMA (bearish alignment)

Pi-e Cloud:

Green - e EMA above Pi EMA (bullish alignment)

Blue - Pi EMA above e EMA (bearish alignment)

Color change = EMA order change = possible trend change

9. What is Momentum % in the table?

Momentum % = percentage deviation of price from Fast EMA

Formula:

Momentum = ((Close - Fast EMA) / Fast EMA) × 100

Interpretation:

+0.5% to +2% - normal bullish momentum

+2% to +5% - strong bullish momentum

+5% and above - overheating (correction possible)

-0.5% to -2% - normal bearish momentum

-2% to -5% - strong bearish momentum

-5% and below - oversold (bounce possible)

Usage:

Monitor momentum during STRONG signals

Large momentum = don't enter (wait for pullback)

Small momentum = good entry point

10. How to configure for scalping?

Settings for scalping (M1-M5):

Base Multiplier: 3-5

Source: close or hlc3 (smoother)

Fast: Delta Adaptive (Base 8-12, Sensitivity 3.0)

Mid: None (for more signals)

Slow: Phi Golden (Phi²) or Pi Circular (1Pi)

Visualization:

- Gradient Clouds: ON (helps see strength)

- Neon Glow: OFF (doesn't clutter chart)

- Pulsing Bar: ON (quick assessment)

- Signal Highlights: ON

Signals:

- Golden/Death Cross: ON

- STRONG Signals: ON

- Stop Loss: ON (1.0-1.5 ATR, R:R 1.5-2.0)

Scalping rules:

Trade only STRONG signals

Enter on bounce from Fast EMA

Tight stops (10-20 pips)

Quick take profit (+1R to +2R)

Don't hold through news

11. How to configure for long-term investing?

Settings for investing (D1-W1):

Base Multiplier: 20-30

Source: close

Fast: Phi Golden (Phi³ or Phi⁴)

Mid: e Natural (e²)

Slow: Pi Circular (3Pi or 4Pi)

Visualization:

- Gradient Clouds: ON

- Neon Glow: ON (Medium)

- Everything else - to taste

Signals:

- Golden/Death Cross: ON

- STRONG Signals: ON

- Stop Loss: OFF (use percentage stop)

Investing rules:

Enter only on STRONG signals

Hold while STRONG active (weeks/months)

Stop below Slow EMA or -10%

Take profit: by company targets or +50-100%

Ignore short-term pullbacks

12. What if indicator slows down chart?

Indicator is optimized, but if it slows:

Disable unnecessary visual effects:

Neon Glow: OFF (saves 8 plots)

Gradient Clouds: ON but low quality

Lambda Wave EMA: OFF (if not using)

Reduce number of active EMAs:

Sigma Composite: OFF

Lambda Wave: OFF

Leave only Phi, Pi, e, Delta

Simplify settings:

Pulsing Bar: OFF

Greek Labels: OFF

Info Table: smaller size

13. Can I use on different timeframes simultaneously?

Yes! Multi-timeframe analysis is very powerful:

Classic scheme:

Higher TF (D1, W1) - determine global trend

Wait for STRONG signal

This is our trading direction

Middle TF (H4, H1) - look for confirmation

STRONG signal in same direction

Precise entry zone

Lower TF (M15, M5) - entry point

Golden Cross or bounce from Fast EMA

Precise stop loss

Example:

W1: STRONG BUY active (global uptrend)

H4: STRONG BUY appeared (confirmation)

M15: Wait for Golden Cross or bounce from Fast EMA → ENTRY

Advantages:

Maximum reliability

Clear timeframe hierarchy

Large targets

14. How does indicator work on news?

Delta Adaptive EMA adapts excellently to news:

Before news:

Low volatility → Delta EMA becomes fast → pulls to price

During news:

Sharp volatility spike → Delta EMA slows → filters noise

After news:

Volatility normalizes → Delta EMA returns to normal

Recommendations:

Don't trade at news release moment (spreads widen)

Wait for STRONG signal after news (2-5 bars)

Use Delta Adaptive as Fast EMA for quick reaction

Widen stops by 50-100% during important news

Advanced Techniques

Technique 1: "Divergences with EMA"

Idea: Look for discrepancies between price and Fast EMA

Bullish divergence:

Price makes lower low

Fast EMA makes higher low

= Possible reversal up

Bearish divergence:

Price makes higher high

Fast EMA makes lower high

= Possible reversal down

How to trade:

Find divergence

Wait for STRONG signal in divergence direction

Enter on confirmation

Technique 2: "EMA Tunnel"

Idea: Use space between Fast and Slow EMA as "tunnel"

Rules:

Wide tunnel - strong trend, hold position

Narrow tunnel - weak trend or consolidation, caution

Tunnel narrowing - trend weakening, prepare to exit

Tunnel widening - trend strengthening, can add

Visually: Gradient Clouds show this automatically!

Trading:

Enter on STRONG signal (tunnel starts widening)

Hold while tunnel wide

Exit when tunnel starts narrowing

Technique 3: "Wave Analysis with Lambda"

Idea: Lambda Wave EMA creates sinusoid matching market cycles

Setup:

Lambda Base Period: 30

Lambda Wave Amplitude: 0.5

Lambda Wave Frequency: 50 (adjusted to asset cycle)

How to find correct Frequency:

Look at historical cycles (distance between local highs)

Average distance = your Frequency

Example: if highs every 40-60 bars, set Frequency = 50

Trading:

Enter when Lambda Wave at bottom of sinusoid (growth potential)

Exit when Lambda Wave at top (fall potential)

Combine with STRONG signals

Technique 4: "Cluster Analysis"

Idea: When all EMAs gather in narrow cluster = powerful breakout soon

Cluster signs:

All EMAs (Phi, Pi, e, Delta) within 0.5-1% of each other

Gradient Clouds almost invisible

Price jumping around all EMAs

Trading:

Identify cluster (all EMAs close)

Determine breakout direction (where more volume, higher TFs direction)

Wait for breakout and STRONG signal

Enter on confirmation

Target = cluster size × 3-5

This is very powerful technique for big moves!

Technique 5: "Sigma as Dynamic Level"

Idea: Sigma Composite EMA = average of all EMAs = magnetic level

Usage:

Enable Sigma Composite (Weighted Average)

Sigma works as dynamic support/resistance

Price often returns to Sigma before trend continuation

Trading:

In trend: Enter on bounces from Sigma

In range: Fade moves from Sigma (trade return to Sigma)

On breakout: Sigma becomes support/resistance

Risk Management

Basic Rules

1. Position Size

Conservative: 1% of capital per trade

Moderate: 2% of capital per trade (recommended)

Aggressive: 3-5% (only for experienced)

Calculation formula:

Lot Size = (Capital × Risk%) / (Stop in pips × Pip value)

2. Risk/Reward Ratio

Minimum: 1:1.5

Standard: 1:2 (recommended)

Optimal: 1:3

Aggressive: 1:5+

3. Maximum Drawdown

Daily: -3% to -5%

Weekly: -7% to -10%

Monthly: -15% to -20%

Upon reaching limit → STOP trading until end of period

Position Management Strategies

1. Fixed Stop

Method:

Stop below/above Fast EMA or local extreme

DON'T move stop against position

Can move to breakeven

For whom: Beginners, conservative traders

2. Trailing by Fast EMA

Method:

Each day (or bar) move stop to Fast EMA level

Position closes when price breaks Fast EMA

Advantages:

Stay in trend as long as possible

Automatically exit on reversal

For whom: Trend followers, swing traders

3. Partial Exit

Method:

50% of position close at +2R

50% hold with trailing by Mid EMA or Slow EMA

Advantages:

Lock profit

Leave position for big move

Psychologically comfortable

For whom: Universal method (recommended)

4. Pyramiding

Method:

First entry on STRONG signal (50% of planned position)

Add 25% on pullback to Fast EMA

Add another 25% on pullback to Mid EMA

Overall stop below Slow EMA

Advantages:

Average entry price

Reduce risk

Increase profit in strong trends

Caution:

Works only in trends

In range leads to losses

For whom: Experienced traders

Trading Psychology

Correct Mindset

1. Indicator is a tool, not holy grail

Indicator shows probability, not guarantee

There will be losing trades - this is normal

Important is series statistics, not one trade

2. Trust the system

If STRONG signal appeared - enter

Don't search for "perfect" moment

Follow trading plan

3. Patience

STRONG signals don't appear every day

Better miss signal than enter against trend

Quality over quantity

4. Discipline

Always set stop loss

Don't move stop against position

Don't increase risk after losses

Beginner Mistakes

1. "I know better than indicator"

Indicator says STRONG BUY, but you think "too high, will wait for pullback"

Result: miss profitable move

Solution: Trust signals or don't use indicator

2. "Will reverse now for sure"

Trading against STRONG trend

Result: stops, stops, stops

Solution: Trend is your friend, trade with trend

3. "Will hold a bit more"

Don't exit when STRONG signal disappears

Greed eats profit

Solution: If signal gone - exit!

4. "I'll recover"

After losses double risk

Result: huge losses

Solution: Fixed % risk ALWAYS

5. "I don't like this signal"

Skip signals because of "feeling"

Result: inconsistency, no statistics

Solution: Trade ALL signals or clearly define filters

Trading Journal

What to Record

For each trade:

1. Entry/exit date and time

2. Instrument and timeframe

3. Signal type

Golden Cross

STRONG BUY

STRONG SELL

Death Cross

4. Indicator settings

Fast/Mid/Slow EMA

Base Multiplier

Other parameters

5. Chart screenshot

Entry moment

Exit moment

6. Trade parameters

Position size

Stop loss

Take Profit

R:R

7. Result

Profit/Loss in $

Profit/Loss in %

Profit/Loss in R

8. Notes

What was right

What was wrong

Emotions during trade

Lessons

Journal Analysis

Analyze weekly:

1. Win Rate

Win Rate = (Profitable trades / All trades) × 100%

Good: 50-60%

Excellent: 60-70%

Exceptional: 70%+

2. Average R

Average R = Sum of all R / Number of trades

Good: +0.5R

Excellent: +1.0R

Exceptional: +1.5R+

3. Profit Factor

Profit Factor = Total profit / Total losses

Good: 1.5+

Excellent: 2.0+

Exceptional: 3.0+

4. Maximum Drawdown

Track consecutive losses

If more than 5 in row - stop, check system

5. Best/Worst Trades

What was common in best trades? (do more)

What was common in worst trades? (avoid)

Pre-Trade Checklist

Technical Analysis

STRONG signal active (BUY or SELL)

All EMAs properly aligned (Fast > Mid > Slow or reverse)

Price on correct side of Fast EMA

Gradient Clouds confirm trend

Pulsing Bar shows STRONG state

Momentum % in normal range (not overheated)

No close strong levels against direction

Higher timeframe doesn't contradict

Risk Management

Position size calculated (1-2% risk)

Stop loss set

Take profit calculated (minimum 1:2)

R:R satisfactory

Daily/weekly risk limit not exceeded

No other open correlated positions

Fundamental Analysis

No important news in coming hours

Market session appropriate (liquidity)

No contradicting fundamentals

Understand why asset is moving

Psychology

Calm and thinking clearly

No emotions from previous trades

Ready to accept loss at stop

Following trading plan

Not revenging market for past losses

If at least one point is NO - think twice before entering!

Learning Roadmap

Week 1: Familiarization

Goals:

Install and configure indicator

Study all EMA types

Understand visualization

Tasks:

Add indicator to chart

Test all Fast/Mid/Slow settings

Play with Base Multiplier on different timeframes

Observe Gradient Clouds and Pulsing Bar

Study Info Table

Result: Comfort with indicator interface

Week 2: Signals

Goals:

Learn to recognize all signal types

Understand difference between Golden Cross and STRONG

Tasks:

Find 10 Golden Cross examples in history

Find 10 STRONG BUY examples in history

Compare their results (which worked better)

Set up alerts

Get 5 real alerts

Result: Understanding signals

Week 3: Demo Trading

Goals:

Start trading signals on demo account

Gather statistics

Tasks:

Open demo account

Trade ONLY STRONG signals

Keep journal (minimum 20 trades)

Don't change indicator settings

Strictly follow stop losses

Result: 20+ documented trades

Week 4: Analysis

Goals:

Analyze demo trading results

Optimize approach

Tasks:

Calculate win rate and average R

Find patterns in profitable trades

Find patterns in losing trades

Adjust approach (not indicator!)

Write trading plan

Result: Trading plan on 1 page

Month 2: Improvement

Goals:

Deepen understanding

Add additional techniques

Tasks:

Study multi-timeframe analysis

Test combinations with Price Action

Try advanced techniques (divergences, tunnels)

Continue demo trading (minimum 50 trades)

Achieve stable profitability on demo

Result: Win rate 55%+ and Profit Factor 1.5+

Month 3: Real Trading

Goals:

Transition to real account

Maintain discipline

Tasks:

Open small real account

Trade minimum lots

Strictly follow trading plan

DON'T increase risk

Focus on process, not profit

Result: Psychological comfort on real

Month 4+: Scaling

Goals:

Increase account

Become consistently profitable

Tasks:

With 60%+ win rate can increase risk to 2%

Upon doubling account can add capital

Continue keeping journal

Periodically review and improve strategy

Share experience with community

Result: Stable profitability month after month

Additional Resources

Recommended Reading

Technical Analysis:

"Technical Analysis of Financial Markets" - John Murphy

"Trading in the Zone" - Mark Douglas (psychology)

"Market Wizards" - Jack Schwager (trader interviews)

EMA and Moving Averages:

"Moving Averages 101" - Steve Burns

Articles on Investopedia about EMA

Risk Management:

"The Mathematics of Money Management" - Ralph Vince

"Trade Your Way to Financial Freedom" - Van K. Tharp

Trading Journals:

Edgewonk (paid, very powerful)

Tradervue (free version + premium)

Excel/Google Sheets (free)

Screeners:

TradingView Stock Screener

Finviz (stocks)

CoinMarketCap (crypto)

Conclusion

Hellenic EMA Matrix is a powerful tool based on universal mathematical constants of nature. The indicator combines:

Mathematical elegance - Phi, Pi, e instead of arbitrary numbers

Premium visualization - Neon Glow, Gradient Clouds, Pulsing Bar

Reliable signals - STRONG BUY/SELL work on all timeframes

Flexibility - 6 EMA types, adaptation to any trading style

Automation - auto-sorting EMAs, SL/TP calculation, alerts

Key Success Principles:

Simplicity - start with basic settings (Phi/Pi/e, Base=10)

Discipline - follow STRONG signals strictly

Patience - wait for quality setups

Risk Management - 1-2% per trade, ALWAYS

Journal - document every trade

Learning - constantly improve skills

Remember:

Indicator shows probability, not guarantee

Important is series statistics, not one trade

Psychology more important than technique

Quality more important than quantity

Process more important than result

Acknowledgments

Thank you for using Hellenic EMA Matrix - Alpha Omega Premium!

The indicator was created with love for mathematics, markets, and beautiful visualization.

Wishing you profitable trading!

Guide Version: 1.0

Date: 2025

Compatibility: Pine Script v6, TradingView

"In the simplicity of mathematical constants lies the complexity of market movements"

Dual TF VWAP + ATR BandsDual TF VWAP + EMA (3×3 Outer Shells)

A precision volatility framework combining institutional VWAP structure with trend-anchored EMA logic.

🔍 Overview

Dual TF VWAP + EMA is a multi-layer trend and volatility system designed for traders who want clean directional context, controlled volatility boundaries, and a reliable method to spot pivots, expansions, compressions, and exhaustion points across any timeframe.

This tool blends:

Higher-Timeframe VWAP (50-period rolling)

Local EMA Midline (configurable)

3×3 ATR Outer Shells

Directional Color Coding

Signal-Ready Interaction Zones

Unlike traditional Bollinger Bands, Keltner channels, or static envelopes, this indicator adapts dynamically with both price and volume, giving deeper insight into how institutions accumulate, distribute, or expand trends.

🎯 What It Shows

1. Higher-Timeframe VWAP Midline

A 50-period Rolling VWAP that reflects where real volume-weighted control sits.

Perfect for reading:

Institutional trend bias

Value area reclaims

High-confidence mean reversions

High-probability trend continuations

2. Local EMA Trendline (Configurable)

A flexible EMA that acts as your local “risk-on/off” trend gauge.

You can use:

12 EMA for aggression

20 EMA for balanced trending

50 EMA for slower institutional rhythm

This EMA + VWAP pairing creates a powerful trend confirmation system.

3. Outer ATR Shells (U1–U3 / L1–L3)

Three upper and three lower ATR-based shells form a volatility map showing:

U1/L1: First reaction zones

U2/L2: Overextension zones

U3/L3: Exhaustion / blow-off tops / panic bottoms

The 3×3 shells tell you instantly whether price is:

Expanding

Compressing

Overextended

Reversing

Trending cleanly

📘 How To Use It — Practical Trading Logic

1. Trend Confirmation

Bullish: Price above VWAP + EMA rising + 12 EMA above U1

Bearish: Price below VWAP + EMA falling + 12 EMA under L1

2. Reversals

U3/L3 taps signal exhaustion

EMA rejection at U1/U2 confirms fading momentum

VWAP reclaim confirms the reversal

Trend resumes once EMA crosses back above/below VWAP

3. Momentum Acceleration

When price floats above the EMA without touching it and rides between:

EMA → U1 → U2

trend acceleration is underway (trip-wire continuation signal).

4. Safe Entries

EMA reclaim

VWAP reclaim after sweep

EMA → VWAP “compression and release”

Price floating above EMA with U1 break

5. Safe Exits

U2/U3 spikes

EMA flattening

EMA cross back under VWAP

Shell compression before trend shift

---Why This Tool Works---

Traditional bands are one-dimensional:

They react to price only.

This tool uses price + volatility + volume, so it shows:

Real trend strength

Institutional control zones

High-probability reversal points

Low-risk entry pockets

It performs exceptionally well across:

SPY / QQQ

Tech momentum

Small caps

Crypto

High-beta growth names

Summary

Dual TF VWAP + EMA (3×3 Outer Shells) is built for traders who want:

Clear trend direction

Accurate expansion/reversal signals

Dynamic institutional value zones

Multi-timeframe confidence

Clean volatility boundaries

A powerful companion for confirmation systems, breakout strategies, and liquidity-based execution.

GEX / Gamma - SPX Indicator Description – GEX / Gamma (SPX)

This indicator allows you to manually plot your daily +GEX, TRANS-GEX, and –GEX levels on SPX and visualize how price reacts around key gamma zones.

You enter the three levels each morning, and the script automatically draws:

+GEX / TRANS / –GEX zones with an adjustable buffer

Clean labels (e.g., “+GEX: 6850”) pinned to the right side of the chart

Today-only candle coloring (green above TRANS-GEX, red below)

Zones extend from yesterday’s session through the current session, helping highlight areas where dealer hedging flows may influence volatility, compression, or acceleration.

How to Use

Add the indicator to any intraday SPX chart.

Open settings and enter your +GEX, TRANS-GEX, and –GEX levels for the day.

Adjust the buffer, colors, and label style as needed.

Watch how price behaves as it moves above or below TRANS-GEX and interacts with +/- GEX zones.

Best For

Intraday SPX / ES / SPY

Options traders

Volatility and gamma-aware strategies

Strategy Behind It (Tight Version)

GEX levels help identify where dealer hedging flows can influence SPX price behavior.

+GEX (Positive Gamma)

Market tends to stabilize here. Dealers hedge against price moves, creating mean-reversion and lower volatility.

TRANS-GEX (Transition Level)

Key pivot where gamma flips. Price crossing this level often signals a shift in volatility or intraday direction.

–GEX (Negative Gamma)

Market becomes more reactive. Dealers hedge with price, increasing volatility, momentum, and trend potential.

How traders use it:

Expect resistance or slowdown into +GEX

Watch for potential bottoming or increased volatility –GEX

Use TRANS-GEX as a bias line or trigger for intraday shifts

A move outside of either the +GEX or -GEX will likely result in some type of high volume move.

TradeUniv.com Expected MovesTradeUniv.com Expected Moves

See where the market expects stocks to move based on options pricing data. This indicator shows you upper and lower price levels that help identify potential support, resistance, and overextended moves.

What Are Expected Moves?

Expected moves are calculated from option prices and show where the market thinks a stock is likely to trade by the end of the day or week. Think of them as probability zones - when price reaches or crosses these levels, it may signal an unusual

move or potential reversal opportunity.

What You'll See on Your Chart:

• Upper Level (Green) - Expected high for the period

• Lower Level (Red) - Expected low for the period• Midpoint (Gray) - Previous day's closing price (your reference point)

• Shaded Area - The expected trading range between levels

How to Use:

1. Visit www.tradeuniv.com

2. Select your favorite tickers

3. Click "Generate Script" and copy the TradingView input

4. Paste it into this indicator's settings

5. The indicator automatically shows the expected moves for whatever chart you're viewing

Perfect For:

• Day traders planning entry and exit zones

• Identifying when price has moved "too far too fast"

• Spotting potential reversal areas

• Understanding daily volatility expectations

• Planning option strategies around expected ranges

Features:

• Automatically detects daily vs weekly expirations (SPY, IWM, QQQ use daily; others use weekly)

• Customizable colors and line styles

• Price crossing alerts (get notified when price breaks above/below expected levels)

• Works on any timeframe

• Clean, minimal chart display

Important:

• Requires TradeUniv.com free account to generate data

• Refresh your data daily for accurate calculations

• Only shows levels for tickers you selected when generating

P1 - Multi-Instrument Weekly Levels - Version 11.9.25.5Levels based on RDGD channels.

// ===========================================================================

// Multi-Instrument Weekly Levels + MSL X + Alerts + ES to SPX Converter

// Version: 11.9.25.5

//

// VERSION TRACKING:

// Format: xx.xx.xx.x (Month.Day.Year.Revision)

// - First number: Month (11 = November)

// - Second number: Day (9 = 9th)

// - Third number: Year (25 = 2025)

// - Fourth number: Revision (5 = updated MSL/NPL values and reorganized settings)

//

// CHANGE LOG:

// 11.9.25.5 - Updated MSL/NPL values and reorganized settings layout

// 11.9.25.4 - Updated NQ Monday and Weekly levels

// 11.9.25.3 - Fixed showSPXLevels variable name (capital L)

// 11.9.25.2 - Updated SPY, QQQ, ES, YM, RTY, GC weekly and daily levels

// 11.9.25.1 - Initial version saved as starting script

// ===========================================================================

X ATM Option Ladder FlowX ATM Option Ladder Flow is a specialized options-market visualization tool designed for intraday tracking of at-the-money (ATM) option volume flow in index ETFs such as QQQ and SPY.

The script dynamically identifies the ATM contract on every bar and plots real-time call-versus-put volume distributions and marker to represent if the volume corresponded with the price of the option going up or down.

By analyzing volume and direction data from multiple strikes within an ±8-point range, the indicator produces a real-time histogram that reflects how order flow evolves relative to the underlying price.

Complementary status tables display the active strike, ladder position, and warnings when the underlying moves outside the monitored range.

Core Features

Dynamic ATM selection – Each bar automatically maps to the option contract closest to the underlying’s price.

Bidirectional volume comparison – Visual separation of call and put volume, with “up” markers highlighting contracts trading above their prior close.

Multi-strike ladder analysis – Samples strikes ±8 points from the defined center to capture flow skew and momentum near the money.

Optimized data calls – Uses tuple requests to minimize request.security() load, enabling a deeper ladder within TradingView limits.

Session awareness – Restricts processing to the 9:30 AM – 4:15 PM ET option-trading window.

Status dashboard – Displays date, active strike, warning flags (“⚠︎ / •outside”), and ladder parameters directly on chart.

Use Case

The indicator is intended for intraday traders and options-flow analysts who want to visualize how short-term liquidity and sentiment migrate across the ATM region as the underlying moves. Typical applications include:

Monitoring real-time call/put volume balance to confirm directional momentum or detect absorption zones.

Identifying volatility clustering near the money—where hedging pressure or gamma concentration can influence underlying price stability.

Detecting when price exits the monitored ladder (⚠︎ / •outside), signaling a potential shift to a new dominant option band or requiring manual recentering.

Integrating option flow into broader futures or ETF bias models (e.g., NQ/ES alignment or QQQ/SPY flow confirmation).

Technical Notes

Static-center architecture ensures historical consistency: prior bars remain fixed even after re-centering.

Ladder depth is hard-coded to ±8, the maximum possible within TradingView’s security-call limits.

auto_nudge is enabled to smoothly align the selected lane with the active ATM without requiring user intervention.

Indicator is optimized for 1-minute to 5-minute charts; use overlay = false to preserve scale clarity.

MACD Volume VWAP Scalping (2min) by Obiii📘 Strategy Description (for TradingView)

MACD Volume VWAP Scalping Strategy (2-Minute Intraday Momentum)

This strategy is designed for scalpers and short-term intraday traders who focus on capturing small, high-probability moves during the most active hours of the trading session — typically between 9:45 AM and 11:30 AM (New York time).

The system combines three key momentum confirmations:

MACD crossovers to detect short-term trend shifts,

Volume spikes to validate real market participation, and

VWAP / EMA alignment to filter trades in the direction of the prevailing intraday trend.

🔹 Entry Logic

Long Entry:

MACD line crosses above the signal line

Both MACD and Signal are above zero

Current volume > average of the last 10 candles

Price is above VWAP and (optionally) above EMA 9 and EMA 20

Short Entry:

MACD line crosses below the signal line

Both MACD and Signal are below zero

Current volume > average of the last 10 candles

Price is below VWAP and (optionally) below EMA 9 and EMA 20

🎯 Exit Logic

Fixed Take Profit: +0.25%

Fixed Stop Loss: -0.15% to -0.20%

Optionally, switch to the 5-minute chart after entry to monitor momentum and manage exits more smoothly.

⚙️ Recommended Settings

Timeframe: 2 minutes (entries), 5 minutes (monitoring)

Market Session: 9:45 AM – 11:30 AM EST

Assets: Highly liquid instruments such as SPY, QQQ, NVDA, TSLA, AAPL, or large-cap momentum stocks.

💡 Notes

This is a momentum-based scalping strategy — precision and discipline are key.

It performs best in high-volume environments where clear direction emerges after the morning volatility settles.

The system can be fine-tuned for different profit targets, MACD settings, or volume thresholds depending on volatility.

A+ Trade Checklist (Bullish + Bearish Mode + Alerts) – Fixed v61. Trend direction (EMA alignment)

2. Relative Strength vs SPY (is your stock stronger than the market?)

3. Volume confirmation

4. RSI strength

5. Candle momentum

Price Action Scanner (v1)Price Action Scanner 1st addition, This indicator is begging developed using many combination and basing signal in price action and market volume. After years of trading I'm trying to make something simple to trade SPY, IWM and QQQ.

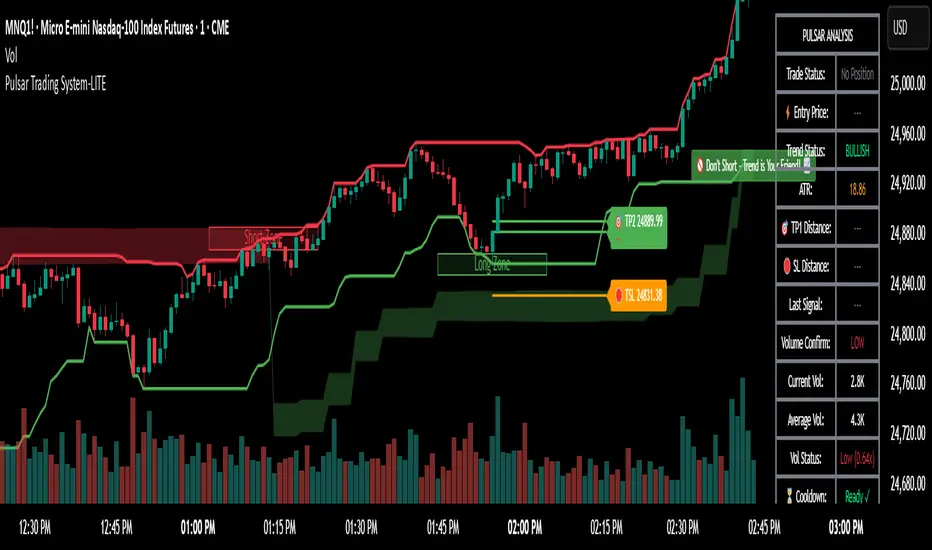

Pulsar Trading System-LITE📡 Pulsar Trading System

OVERVIEW

Pulsar is a comprehensive breakout trading system that combines dynamic support/resistance detection, trend filtering, and volume confirmation to identify high-probability entry opportunities. Unlike simple breakout indicators, Pulsar uses multi-timeframe analysis and adaptive ATR-based calculations to filter false signals and provide complete trade management from entry to exit.

WHAT MAKES THIS ORIGINAL

This indicator is unique in its integration of multiple complementary systems:

-Adaptive ATR Zones: Support and resistance levels are not static—they dynamically adjust based on current market volatility (ATR), creating entry zones that expand and contract with market conditions rather than using fixed price levels.

-Multi-Timeframe SuperTrend Filter: The trend filter operates on a higher timeframe than the chart (e.g., 5-minute SuperTrend on a 1-minute chart) to prevent counter-trend trades while maintaining granular entry precision. The visual ribbon with humorous warning text ("🚫 Don't Short - Trend is Your Friend! 📈") provides immediate trend awareness.

-Intelligent Cooldown System: After any trade exit (stop loss or take profit), the system enters a configurable cooldown period, preventing overtrading during choppy or consolidating market conditions—a critical feature often missing in breakout systems.

-Dynamic Trailing Stops: The trailing stop uses ATR multipliers to lock in profits while adapting to volatility, moving only in the favorable direction and never loosening.

-Comprehensive Dashboard: Real-time analysis displays trade status, entry prices, distances to targets in both points and ATR multiples, volume confirmation status, and cooldown countdown.

HOW IT WORKS

Core Detection Logic:

Pulsar identifies breakout opportunities by monitoring price interaction with dynamically calculated support and resistance levels:

Support/Resistance Calculation: Uses ta.lowest() and ta.highest() over a configurable lookback period to identify key levels, then adds ATR-based buffers (0.5 × ATR) to create entry zones.

Breakout Conditions:

Long Entry: Price closes above support buffer AND recent low touched support AND volume exceeds threshold

Short Entry: Price closes below resistance buffer AND recent high touched resistance AND volume exceeds threshold

SuperTrend Filter: A separate higher-timeframe SuperTrend calculation determines overall trend direction. Entries only trigger when breakout direction aligns with SuperTrend (bullish breakout + bullish trend, or bearish breakout + bearish trend).

Volume Confirmation: Current volume must exceed a configurable multiple of the 14-period SMA (default 1.0×) to confirm genuine interest in the breakout.

Cooldown Mechanism: After exit, the system tracks bars elapsed and blocks new signals until the cooldown period completes, preventing rapid-fire entries in ranging markets.

Trade Management:

Stop Loss: Calculated as entry zone ± (ATR × SL Multiplier)

Take Profit 1: Entry zone ± (ATR × TP1 Multiplier)

Take Profit 2: Entry zone ± (ATR × TP2 Multiplier)

Trailing Stop (optional): Updates every bar, moving the stop closer by maintaining distance of (ATR × Trailing Multiplier) from current price, but only in favorable direction

SuperTrend Calculation:

The SuperTrend uses standard methodology:

Upper Band = (High + Low) / 2 + (Multiplier × ATR)

Lower Band = (High + Low) / 2 - (Multiplier × ATR)

Direction changes when price crosses opposite band

The ribbon visualization adds a width offset (ATR × Ribbon Width) to create a filled zone rather than a single line.

HOW TO USE

Setup:

Add Pulsar to your chart (works best on liquid instruments like NQ, ES, CL)

Configure timeframe-specific settings (see recommendations below)

Enable SuperTrend Filter for trend-following mode, or disable for pure breakout mode

Set up alerts for Entry, TP1, TP2, and Stop Loss events

Recommended Settings by Timeframe:

1-Minute Charts:

Lookback Period: 10-15

SuperTrend Timeframe: 5 min

ATR Timeframe: 5 min (for stability)

Cooldown: 8-12 bars

Trailing Stop: Enabled with 0.8-1.0 multiplier

5-Minute Charts:

Lookback Period: 15-20

SuperTrend Timeframe: 15 min

ATR Timeframe: current chart

Cooldown: 5-8 bars

Trailing Stop: Optional

15-Minute+ Charts:

Lookback Period: 20-30

SuperTrend Timeframe: 1 hour

ATR Timeframe: current chart

Cooldown: 3-5 bars

Trailing Stop: Optional

Interpreting Signals:

Long/Short Zone Box: Green (long) or red (short) box appears when breakout conditions are met

Blue Entry Line: Shows your entry price

Red/Orange SL Line: Red = fixed stop, Orange = trailing stop (moves in real-time)

Green TP Lines: TP1 (closer) and TP2 (further) targets

SuperTrend Ribbon: Green = bullish trend (favor longs), Red = bearish trend (favor shorts)

Dashboard Status: Monitor trade state, distances, volume confirmation, and cooldown

Best Practices:

Use SuperTrend Filter: Significantly reduces false signals by avoiding counter-trend trades

Enable Cooldown on Fast Timeframes: Prevents overtrading on 1-5 minute charts

Volume Confirmation is Critical: Don't lower volume multiplier below 0.9 on futures

Use Higher Timeframe ATR: On 1-minute charts, use 5-minute ATR for stability

Avoid Major News Events: Disable during FOMC, NFP, CPI releases

Scale Out Strategy: Consider taking partial profits at TP1, letting remainder run to TP2

Parameter Optimization:

Start conservative and adjust based on results:

Too many stop-outs: Increase SL multiplier or SuperTrend multiplier

Missing good trades: Decrease volume multiplier or cooldown period

Too many false signals: Increase volume multiplier, lookback period, or cooldown

Profits not protected: Enable trailing stop or reduce trailing multiplier

KEY FEATURES

✅ Dynamic ATR-Based Zones: Entry, stop loss, and take profit levels automatically adjust to market volatility

✅ Multi-Timeframe Trend Filter: Uses higher timeframe SuperTrend to eliminate counter-trend trades

✅ Volume Confirmation: Filters low-volume false breakouts

✅ Intelligent Cooldown: Prevents overtrading with configurable post-trade waiting period

✅ Trailing Stop System: Optional dynamic stops that lock in profits using ATR distance

✅ Real-Time Dashboard: 13-row analysis showing trade status, targets, distances, volume, and cooldown

✅ Visual Ribbon Warnings: Humorous trend-following reminders on SuperTrend ribbon

✅ Complete Alert System: Notifications for entries, TP1, TP2, fixed stops, and trailing stops

✅ Customizable Visuals: Adjustable colors, dashboard position, text size, and line lengths

✅ Non-Repainting: Uses lookahead = barmerge.lookahead_off for all multi-timeframe calculations

SETTINGS EXPLAINED

SuperTrend Filter:

Enable: Toggle trend filtering on/off

Timeframe: Higher timeframe for trend analysis (recommended 3-5x chart timeframe)

ATR Period: Period for ATR calculation in SuperTrend (10-14 standard)

Multiplier: Distance from center band (2.5-3.5 for most markets)

Ribbon Width: Visual thickness of trend ribbon (0.2-0.5)

Core Parameters:

Lookback Period: Bars used to identify support/resistance (lower = more sensitive)

ATR Period: Bars for Average True Range calculation (14 is standard)

ATR Timeframe: Use higher timeframe ATR for smoother calculations on fast charts

Volume Multiplier: Required volume vs average (1.0 = average, 1.5 = 50% above average)

TP/SL:

SL Multiplier: Stop loss distance in ATR units (1.0-2.0 typical)

TP1 Multiplier: First target in ATR units (1.5-2.5 typical)

TP2 Multiplier: Second target in ATR units (2.0-3.5 typical)

Trailing Stop:

Enable: Activate dynamic trailing stop

Multiplier: Distance from current price in ATR units (0.8-1.5 typical)

Cooldown:

Enable: Prevent new signals after trade exit

Bars: Number of bars to wait before allowing next trade (higher on fast timeframes)

IMPORTANT NOTES

⚠️ Not a Holy Grail: No indicator is perfect. Pulsar is a tool that requires proper risk management, position sizing, and trading discipline.

⚠️ Backtest First: Test settings on historical data before live trading. Results vary by instrument, timeframe, and market conditions.

⚠️ Market Conditions Matter: Breakout systems perform best in trending markets. Consider reducing size or disabling during known choppy periods.

⚠️ Stop Loss is Mandatory: Always use the provided stop loss levels. Markets can move against you rapidly.

⚠️ Volume Data Required: This indicator requires volume data to function properly. It will display a warning if volume is unavailable.

⚠️ No Repainting: All multi-timeframe calls use non-repainting settings. What you see in real-time is what will be plotted historically.

TECHNICAL SPECIFICATIONS

Version: Pine Script v6

Type: Indicator (overlay = true)

Max Boxes: 500 (for zone visualization)

Max Lines: 500 (for TP/SL levels)

Max Labels: Unlimited (for annotations)

Repainting: None (uses lookahead = barmerge.lookahead_off)

COMPATIBLE INSTRUMENTS

Works best on liquid instruments with reliable volume data:

✅ Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, GC

✅ Forex: Major pairs (EUR/USD, GBP/USD, etc.)

✅ Stocks: Large-cap stocks with high volume

⚠️ Crypto: Works but requires higher ATR multipliers

❌ Low Volume Stocks: May produce unreliable signals

SUPPORT

For questions, suggestions, or to report issues, please comment below. I actively maintain this indicator and appreciate feedback from the community.

Enjoy trading with Pulsar! 🌟

TrendRebel.pro SMA 🆓Welcome to Trend Rebel!

This 🆓 Indicator will help guide you through boundaries across multiple timeframes.

Seamlessly watch your 4 Hour or any other timeframe while being able to plot aand or just view other important SMA's.

Add this with a FREE subscription to Trend Rebels Bootcamp and you can master the boundaries that SMA"s provide giving you an edge.

SMA's provide you with the boundaries that define how technicals move, while they are based on previous candles, future candles respect them with patterns and institutions use them to guide their trading as well. This of it as a cheat sheet to awareness of whats to come.

This Free version is somewhat limited, so make sure you get a free trial to trend rebel and explore the many Indicators we use to navigate the market with precision.

For instance our Pivot Indicator which is based on charting techniques that Trading View cannot duplicate, therefore we manually update our Pivots DAILY and deliver them to your screen!

For a Paid Subscription to TrendRebel copy paste this link to your browser:

whop.com

For a FREE subscription to Bootcamp copy paste this link to your browser:

whop.com

For more information go to:

www.trendrebel.pro

Dashboard — Vol & PriceDashboard for traders

Indicator Description

1. Prev Day High

What it shows: the previous trading day's high.

Why it shows: a resistance level. Many traders watch to see if the price will hold above or below this level. A breakout can signal buying strength.

2. Prev Day Low

What it shows: the previous day's low.

Why it shows: a support level. If the price breaks downwards, it signals weakness and a possible continuation of the decline.

3. Today

What it shows:

The difference between the current price and yesterday's close (in absolute values and as a percentage).

Color: green for an increase, red for a decrease.

Why it shows: immediately shows how strong a gap or movement is today relative to yesterday. This is an indicator of current momentum.

4. ADR, % (Average Daily Range)

What it shows: Average daily range (High – Low), expressed as a percentage of the closing price, for the selected period (default 7 days).

Why it's useful: To understand the "normal" volatility of an instrument. For example, if the ADR is 3%, then a 1% move is small, while a 6% move is very large.

5. ATR (Average True Range)

What it shows: Average fluctuation range (including gaps), in absolute points, for the specified period (default 7 days).

Why it's useful: A classic volatility indicator. Useful for setting stops, calculating position sizes, and identifying "noise" movements.

6. ATR (Today), %

What it shows: How much the current movement today (from yesterday's close to the current price) represents in % of the average ATR.

Why it shows: Shows whether the instrument has "played out" its average range. If the value is already >100%, there is a high probability that the movement will begin to slow.

7. Vol (Today)

What it shows:

Current trading volume for the day (in millions/billions).

Comparison with yesterday as a percentage (for example: 77.32M (-52.78%)).

Color: green if the volume is higher than yesterday; red if lower.

Why it shows:Quickly shows whether the market is active today. Volume = fuel for price movement.

8. Avg Vol (20d)

What it shows: Average daily volume over the last 20 trading days.

Why it's useful:"normal" activity level. It's a convenient backdrop for assessing today's turnover.

9. Rel. Vol (Today), % (Relative Volume)

What it shows: Deviation of the current volume from the average (20 days).

Formula: `(today / average - 1)` * 100`.

+30% = volume 30% above average, -40% = 40% below average.

Color: green for +, red for –.

Why it's useful:A key indicator for a trader. If RelVol > 100% (green), the market is "charged," and the movement is more significant. If low, activity is weak and movements are less reliable.

10. Normalized RS (Relative Strength)

What it shows: the relative strength of a stock to a selected benchmark (e.g., SPY), normalized by the period (default 7 days).

100 = same result as the market.