Bollinger Band Wick and SRSI Signals [MW]Introduction

This indicator uses a novel combination of Bollinger Bands, candle wicks crossing the upper and lower Bollinger Bands and baseline, and combines them with the Stochastic SRSI oscillator to provide early BUY and SELL signals in uptrends, downtrends, and in ranging price conditions.

How it’s unique

People generally understand Bollinger Bands and Keltner Channels. Buy at the bottom band, sell at the top band. However, because the bands themselves are not static, impulsive moves can render them useless. People also generally understand wicks. Candles with large wicks can represent a change in pattern, or volatile price movement. Combining those two to determine if price is reaching a pivot point is relatively novel. When Stochastic RSI (SRSI) filtering is also added, it becomes a genuinely unique combination that can be used to determine trade entries and exits.

What’s the benefit

The benefit of the indicator is that it can help potentially identify pivots WHEN THEY HAPPEN, and with potentially minimal retracement, depending on the trader’s time window. Many indicators wait for a trend to be established, or wait for a breakout to occur, or have to wait for some form of confirmation. In the interpretation used by this indicator, bands, wicks, and SRSI cycles provide both the signal and confirmation.

It takes into account 3 elements:

Price approaching the upper or lower band or the baseline - MEANING: Price is becoming extended based on calculations that use the candle trading range.

A candle wick of a defined proportion (e.g. wick is 1/2 the size of a full candle OR candle body) crosses a band or baseline, but the body does not cross the band or baseline - MEANING: Buyers and sellers are both very active.

The Stochastic RSI reading is above 80 for SELL signals and below 20 for BUY signals - MEANING: Additional confirmation that price is becoming extended based on the current cyclic price pattern.

How to Use

SIGNALS

Buy Signals - Green(ish):

B Signal - Potential pivot up from the lower band when using the preferred multiplier

B1 Signal - Potential pivot up from baseline

Sell Signals - Red(ish):

S Signal - Potential pivot down from the upper band when using the preferred multiplier

S1 Signal - Potential pivot down from the baseline

DISCUSSION

During an uptrend or downtrend, signals from the baseline can help traders identify areas where they may enter the trending move with the least amount of drawdown. In both cases, entry points can occur with baseline signals in the direction of the trend.

For example, in an uptrend (when the price is forming higher highs and higher lows, or when the baseline is rising), price tends to oscillate between the upper band and baseline. In this case, the baseline BUY signal (B3) can show an entry point.

In a downtrend (when the price is forming lower highs and lower lows, or when the baseline is falling), price tends to oscillate between the baseline and the lower band. In this case, the baseline SELL signal (S3) can show an entry point.

During consolidation, when price is ranging, price tends to oscillate between the upper and lower bands, while crossing through the baseline unperturbed. Here, entry points can occur at the upper and lower bands.

When all conditions are met at the lower band during consolidation, a BUY signal (B), can occur. This signal may also occur prior to a break out of consolidation to the upside.

When all conditions are met at the upper band during consolidation, a SELL signal (S), can occur. This signal may also occur prior to a break out of consolidation to the downside.

Additional, B1 and S1 signals can be displayed that use the baseline as the pivot level.

Settings

SIGNALS

Show Bollinger Band Signals (Default: True): Allows signal labels to be shown.

Hide Baseline Signals (Default: False): Baseline signals are on by default. This will turn them off.

Show Wick Signals (Defau

lt: True): Displays signals when wicking occurs.

BOLLINGER BAND SETTINGS

Period length for Bollinger Band Basis (Default: 21): Length of the Bollinger Band (BB) moving average basis line.

Basis MA Type (Default: SMA): The moving average type for the BB Basis line.

Source (Default: “close”): The source of time series data.

Standard Deviation Multiplier (Default: 2.5: The deviation multiplier used to calculate the band distance from the basis line.

WICK SETTINGS FOR BOLLINGER BANDS

Wick Ratio for Bands (Default: 0.3): The ratio of wick size to total candle size for use at upper and lower bands.

Wick Ratio for Baseline (Default: 0.3): The ratio of wick size to total candle size for use at baseline.

WICK SETTINGS FOR CANDLE SIGNALS

Upper Wick Threshold (Default: 50): The percent of upper wick compared to the full candle size or candle body size.

Lower Wick Threshold (Default: 50): The percent of lower wick compared to the full candle size or candle body size.

Use Candle Body (Default: false): Toggles the use of the full candle size versus the candle body size when calculating the wick signal.

VISUAL PREFERENCES

Fill Bands (Default: true): Use a background color inside the Bollinger Bands.

Show Signals (Default: true): Toggle the Bollinger Band upper band, lower band, and baseline signals.

Show Bollinger Bands (Default: true): Show the Bollinger Bands.

STOCHASTIC SETTINGS

Use Stochastic RSI Filtering (Default: False): This will only trigger some SELL signals when the stochastic RSI is above 80, and BUY signals when below 20.

K (Default: 3): The smoothing level for the Stochastic RSI.

RSI Length (Default: 14): The period length for the RSI calculation.

Stochastic Length (Default: 8): The period length over which the stochastic calculation is performed.

Calculations

Bollinger Bands are a technical analysis tool that are used to measure market volatility and identify overbought or oversold conditions in the trading of financial instruments, such as stocks, bonds, commodities, and currencies. Bollinger Bands consist of three lines plotted on a price chart:

Middle Band, Basis, or Baseline: This is typically a simple moving average (SMA) of the closing prices over a certain period. It represents the intermediate-term trend of the asset's price.

Upper Band: This is calculated by adding a certain number of standard deviations to the middle band (SMA). The upper band adjusts itself with the increase in volatility.

Lower Band: This is calculated by subtracting the same number of standard deviations from the middle band (SMA). Like the upper band, the lower band adjusts to changes in volatility.

The candle wick signals occur if the wick is at the specified ratio compared to either the entire candle or the candle body. The upper band, lower band, and baseline signals happen if the wick is the specified ratio of the total candle size. For the major signals for upper and lower bands, these occur when the wick extends outside of the bands while closing a candle inside of the bands. For the baseline signals, they occur if a wick crosses a baseline but closes on the other side.

Other Usage Notes and Limitations

To understand future price movement, this indicator assumes that 3 things must be known:

Evidence of a change of market structure. This can be demonstrated by increased volatility, consolidation, volume spikes (which can be tracked with the MW Volume Impulse Indicator) or, in the case of this indicator, candle wicks.

The potential cause of the change. It could be a VWAP line (which can be tracked with the Multi VWAP , and Multi VWAP from Gaps indicators), an event, an important support or resistance level, a key moving average, or many other things. This indicator assumes the ATR bands can be a cause.

The current position in the price cycle. Oscillators like the RSI, and MACD, are typical measures of price oscillation (other oscillators like the Price and Volume Stochastic Divergence indicator can also be useful). This indicator uses the Stochastic RSI oscillator to determine overbought and oversold conditions.

When evidence of the change appears, and the potential cause of the change is identified, and the price oscillation is at a favorable position for the desired trading direction, this indicator will generate a signal.

ATR Bands (or Keltner Channels) are used to determine when price might “revert to the mean”. Crossing, or being near the upper or lower band, can indicate an overbought or oversold condition, which could lead to a price reversal. By tracking the behavior of candle wicks during these events, we can see how active the battle is between buyers and sellers.

If the top of a wick is large, it may indicate that sellers are aggressively attempting to bring the price down. Conversely, if the bottom wick is large, it can indicate that buyers are actively trying to counter the price action caused by selling pressure.

When this wicking action occurs at times when price is not near the upper band, lower band, or baseline, it could indicate the presence of an important level. That could mean a nearby VWAP line, a supply or demand zone, a round price number, or a number of other factors. In any case, this wick may be the first indication of a price reversal.

Shorter baseline periods may be better for short period trading like scalping or day trading, while longer period baselines can show signals that are better suited to swing trading, or longer term investing.

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

The TradingView platform allows a maximum of 500 labels per chart. This means that if your settings allow for a lot of signals, labels for earlier ones may not appear if the total number of labels exceeds 500 for the chart.

Search in scripts for "美股标普500"

Market Internals & InfoThis script provides various information on Market Internals and other related info. It was a part of the Daily Levels script but that script was getting very large so I decided to separate this piece of it into its own indicator. I plan on adding some additional features in the near future so stay tuned for those!

The script provides customizability to show certain market internals, tickers, and even Market Profile TPO periods.

Here is a summary of each setting:

NASDAQ and NYSE Breadth Ratio

- Ratio between Up Volume and Down Volume for NASDAQ and NYSE markets. This can help inform about the type of volume flowing in and out of these exchanges.

Advance/Decline Line (ADL)

The ADL focuses specifically on the number of advancing and declining stocks within an index, without considering their trading volume.

Here's how the ADL works:

It tracks the daily difference between the number of stocks that are up in price (advancing) and the number of stocks that are down in price (declining) within a particular index.

The ADL is a cumulative measure, meaning each day's difference is added to the previous day's total.

If there are more advancing stocks, the ADL goes up.

If there are more declining stocks, the ADL goes down.

By analyzing the ADL, investors can get a sense of how many stocks are participating in a market move.

Here's what the ADL can tell you:

Confirmation of Trends: When the ADL moves in the same direction as the underlying index (e.g., ADL rising with a rising index), it suggests broad participation in the trend and potentially stronger momentum.

Divergence: If the ADL diverges from the index (e.g., ADL falling while the index is rising), it can be a warning sign. This suggests that fewer stocks are participating in the rally, which could indicate a weakening trend.

Keep in mind:

The ADL is a backward-looking indicator, reflecting past market activity.

It's often used in conjunction with other technical indicators for a more complete picture.

TRIN Arms Index

The TRIN index, also called the Arms Index or Short-Term Trading Index, is a technical analysis tool used in the stock market to gauge market breadth and sentiment. It essentially compares the number of advancing stocks (gaining in price) to declining stocks (losing price) along with their trading volume.

Here's how to interpret the TRIN:

High TRIN (above 1.0): This indicates a weak market where declining stocks and their volume are dominating the market. It can be a sign of a potential downward trend.

Low TRIN (below 1.0): This suggests a strong market where advancing stocks and their volume are in control. It can be a sign of a potential upward trend.

TRIN around 1.0: This represents a more balanced market, where it's difficult to say which direction the market might be headed.

Important points to remember about TRIN:

It's a short-term indicator, primarily used for intraday trading decisions.

It should be used in conjunction with other technical indicators for a more comprehensive market analysis. High or low TRIN readings don't guarantee future price movements.

VIX/VXN

VIX and VXN are both indexes created by the Chicago Board Options Exchange (CBOE) to measure market volatility. They differ based on the underlying index they track:

VIX (Cboe Volatility Index): This is the more well-known index and is considered the "fear gauge" of the stock market. It reflects the market's expectation of volatility in the S&P 500 index over the next 30 days.

VXN (Cboe Nasdaq Volatility Index): This is a counterpart to the VIX, but instead gauges volatility expectations for the Nasdaq 100 index over the coming 30 days. The tech-heavy Nasdaq can sometimes diverge from the broader market represented by the S&P 500, hence the need for a separate volatility measure.

Both VIX and VXN are calculated based on the implied volatilities of options contracts listed on their respective indexes. Here's a general interpretation:

High VIX/VXN: Indicates a high level of fear or uncertainty in the market, suggesting investors expect significant price fluctuations in the near future.

Low VIX/VXN: Suggests a more complacent market with lower expectations of volatility.

Important points to remember about VIX and VXN:

They are forward-looking indicators, reflecting market sentiment about future volatility, not necessarily current market conditions.

High VIX/VXN readings don't guarantee a market crash, and low readings don't guarantee smooth sailing.

These indexes are often used by investors to make decisions about portfolio allocation and hedging strategies.

Inside/Outside Day

This provides a quick indication of it we are still trading inside or outside of yesterdays range and will show "Inside Day" or "Outside Day" based upon todays range vs. yesterday's range.

Custom Ticker Choices

Ability to add up to 5 other tickers that can be tracked within the table

Show Market Profile TPO

This only shows on timeframes less than 30m. It will show both the current TPO period and the remaining time within that period.

Table Customization

Provided drop downs to change the text size and also the location of the table.

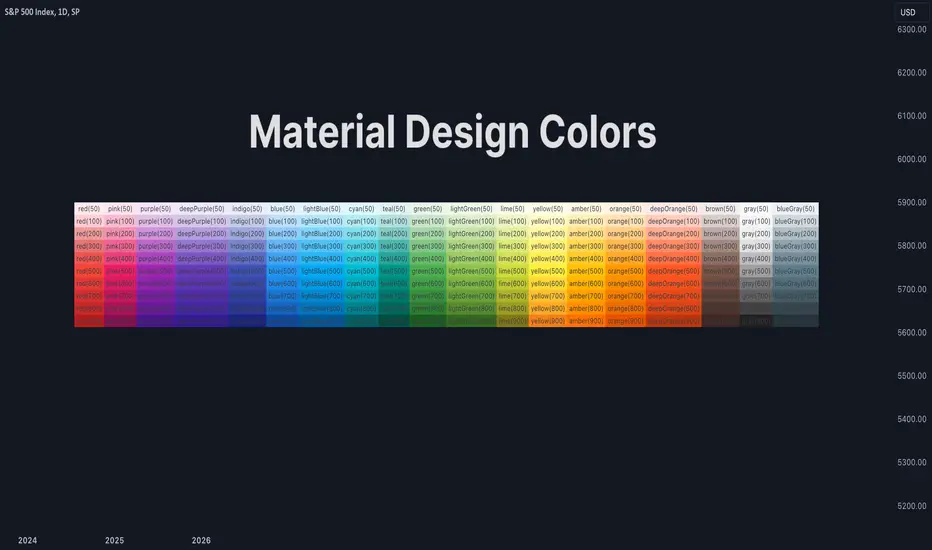

Material Design ColorsThis library provides a standard set of colors defined in Material Design 2.0.

🔵 API

Step 1: Import this library.

import algotraderdev/material/1

// remember to check the latest version of this library and replace the 1 above.

Step 2: Get the color you like. Check the source code or the screenshot above to see all the supported colors.

material.red()

Each color function (except for `black()` and `white()`) accepts an optional `variant` parameter. You can choose any of 50, 100, 200, 300, 400, 500, 600, 700, 800, and 900. By default, 500 is chosen if this parameter is not provided.

Normalized Market IndicatorsExplanation of the Code:

Data Retrieval: The script retrieves the closing prices of the S&P 500 (sp500) and VIX (vix).

Normalization: The script normalizes these values using a simple z-score normalization (subtracting the 50-period simple moving average and dividing by the 50-period standard deviation). This makes the scales of the two datasets more comparable.

Plotting with Secondary Axis: The normalized values of the S&P 500 and VIX are plotted on the same chart. They will share the same y-axis scale as the main chart (e.g. Netflix, GOLD, Forex).

Points to Note:

Normalization Method: The method of normalization (z-score in this case) is a choice and can be adjusted based on your needs. The idea is to bring the data to a comparable scale.

Timeframe and Symbol Codes: Ensure the timeframe and symbol codes are appropriate for your data source and trading strategy.

Overlaying on Price Chart: Since these values are normalized and plotted on a seperate chart, they won't directly correspond to the price levels of the main chart (e.g. Netflix, GOLD, Forex).

ottlibLibrary "ottlib"

█ OVERVIEW

This library contains functions for the calculation of the OTT (Optimized Trend Tracker) and its variants, originally created by Anıl Özekşi (Anil_Ozeksi). Special thanks to him for the concept and to Kıvanç Özbilgiç (KivancOzbilgic) and dg_factor (dg_factor) for adapting them to Pine Script.

█ WHAT IS "OTT"

The OTT (Optimized Trend Tracker) is a highly customizable and very effective trend-following indicator that relies on moving averages and a trailing stop at its core. Moving averages help reduce noise by smoothing out sudden price movements in the markets, while trailing stops assist in detecting trend reversals with precision. Initially developed as a noise-free trailing stop, the current variants of OTT range from rapid trend reversal detection to long-term trend confirmation, thanks to its extensive customizability.

It's well-known variants are:

OTT (Optimized Trend Tracker).

TOTT (Twin OTT).

OTT Channels.

RISOTTO (RSI OTT).

SOTT (Stochastic OTT).

HOTT & LOTT (Highest & Lowest OTT)

ROTT (Relative OTT)

FT (Original name is Fırsatçı Trend in Turkish which translates to Opportunist Trend)

█ LIBRARY FEATURES

This library has been prepared in accordance with the style, coding, and annotation standards of Pine Script version 5. As a result, explanations and examples will appear when users hover over functions or enter function parameters in the editor.

█ USAGE

Usage of this library is very simple. Just import it to your script with the code below and use its functions.

import ismailcarlik/ottlib/1 as ottlib

█ FUNCTIONS

• f_vidya(source, length, cmoLength)

Short Definition: Chande's Variable Index Dynamic Average (VIDYA).

Details: This function computes Chande's Variable Index Dynamic Average (VIDYA), which serves as the original moving average for OTT. The 'length' parameter determines the number of bars used to calculate the average of the given source. Lower values result in less smoothing of prices, while higher values lead to greater smoothing. While primarily used internally in this library, it has been made available for users who wish to utilize it as a moving average or use in custom OTT implementations.

Parameters:

source (float) : (series float) Series of values to process.

length (simple int) : (simple int) Number of bars to lookback.

cmoLength (simple int) : (simple int) Number of bars to lookback for calculating CMO. Default value is `9`.

Returns: (float) Calculated average of `source` for `length` bars back.

Example:

vidyaValue = ottlib.f_vidya(source = close, length = 20)

plot(vidyaValue, color = color.blue)

• f_mostTrail(source, multiplier)

Short Definition: Calculates trailing stop value.

Details: This function calculates the trailing stop value for a given source and the percentage. The 'multiplier' parameter defines the percentage of the trailing stop. Lower values are beneficial for catching short-term reversals, while higher values aid in identifying long-term trends. Although only used once internally in this library, it has been made available for users who wish to utilize it as a traditional trailing stop or use in custom OTT implementations.

Parameters:

source (float) : (series int/float) Series of values to process.

multiplier (simple float) : (simple float) Percent of trailing stop.

Returns: (float) Calculated value of trailing stop.

Example:

emaValue = ta.ema(source = close, length = 14)

mostValue = ottlib.f_mostTrail(source = emaValue, multiplier = 2.0)

plot(mostValue, color = emaValue >= mostValue ? color.green : color.red)

• f_ottTrail(source, multiplier)

Short Definition: Calculates OTT-specific trailing stop value.

Details: This function calculates the trailing stop value for a given source in the manner used in OTT. Unlike a traditional trailing stop, this function modifies the traditional trailing stop value from two bars prior by adjusting it further with half the specified percentage. The 'multiplier' parameter defines the percentage of the trailing stop. Lower values are beneficial for catching short-term reversals, while higher values aid in identifying long-term trends. Although primarily used internally in this library, it has been made available for users who wish to utilize it as a trailing stop or use in custom OTT implementations.

Parameters:

source (float) : (series int/float) Series of values to process.

multiplier (simple float) : (simple float) Percent of trailing stop.

Returns: (float) Calculated value of OTT-specific trailing stop.

Example:

vidyaValue = ottlib.f_vidya(source = close, length = 20)

ottValue = ottlib.f_ottTrail(source = vidyaValue, multiplier = 1.5)

plot(ottValue, color = vidyaValue >= ottValue ? color.green : color.red)

• ott(source, length, multiplier)

Short Definition: Calculates OTT (Optimized Trend Tracker).

Details: The OTT consists of two lines. The first, known as the "Support Line", is the VIDYA of the given source. The second, called the "OTT Line", is the trailing stop based on the Support Line. The market is considered to be in an uptrend when the Support Line is above the OTT Line, and in a downtrend when it is below.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

length (simple int) : (simple int) Number of bars to lookback. Default value is `2`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `1.4`.

Returns: ( [ float, float ]) Tuple of `supportLine` and `ottLine`.

Example:

= ottlib.ott(source = close, length = 2, multiplier = 1.4)

longCondition = ta.crossover(supportLine, ottLine)

shortCondition = ta.crossunder(supportLine, ottLine)

• tott(source, length, multiplier, bandsMultiplier)

Short Definition: Calculates TOTT (Twin OTT).

Details: TOTT consists of three lines: the "Support Line," which is the VIDYA of the given source; the "Upper Line," a trailing stop of the Support Line adjusted with an added multiplier; and the "Lower Line," another trailing stop of the Support Line, adjusted with a reduced multiplier. The market is considered in an uptrend if the Support Line is above the Upper Line and in a downtrend if it is below the Lower Line.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

length (simple int) : (simple int) Number of bars to lookback. Default value is `40`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `0.6`.

bandsMultiplier (simple float) : Multiplier for bands. Default value is `0.0006`.

Returns: ( [ float, float, float ]) Tuple of `supportLine`, `upperLine` and `lowerLine`.

Example:

= ottlib.tott(source = close, length = 40, multiplier = 0.6, bandsMultiplier = 0.0006)

longCondition = ta.crossover(supportLine, upperLine)

shortCondition = ta.crossunder(supportLine, lowerLine)

• ott_channel(source, length, multiplier, ulMultiplier, llMultiplier)

Short Definition: Calculates OTT Channels.

Details: OTT Channels comprise nine lines. The central line, known as the "Mid Line," is the OTT of the given source's VIDYA. The remaining lines are positioned above and below the Mid Line, shifted by specified multipliers.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`

length (simple int) : (simple int) Number of bars to lookback. Default value is `2`

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `1.4`

ulMultiplier (simple float) : (simple float) Multiplier for upper line. Default value is `0.01`

llMultiplier (simple float) : (simple float) Multiplier for lower line. Default value is `0.01`

Returns: ( [ float, float, float, float, float, float, float, float, float ]) Tuple of `ul4`, `ul3`, `ul2`, `ul1`, `midLine`, `ll1`, `ll2`, `ll3`, `ll4`.

Example:

= ottlib.ott_channel(source = close, length = 2, multiplier = 1.4, ulMultiplier = 0.01, llMultiplier = 0.01)

• risotto(source, length, rsiLength, multiplier)

Short Definition: Calculates RISOTTO (RSI OTT).

Details: RISOTTO comprised of two lines: the "Support Line," which is the VIDYA of the given source's RSI value, calculated based on the length parameter, and the "RISOTTO Line," a trailing stop of the Support Line. The market is considered in an uptrend when the Support Line is above the RISOTTO Line, and in a downtrend if it is below.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

length (simple int) : (simple int) Number of bars to lookback. Default value is `50`.

rsiLength (simple int) : (simple int) Number of bars used for RSI calculation. Default value is `100`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `0.2`.

Returns: ( [ float, float ]) Tuple of `supportLine` and `risottoLine`.

Example:

= ottlib.risotto(source = close, length = 50, rsiLength = 100, multiplier = 0.2)

longCondition = ta.crossover(supportLine, risottoLine)

shortCondition = ta.crossunder(supportLine, risottoLine)

• sott(source, kLength, dLength, multiplier)

Short Definition: Calculates SOTT (Stochastic OTT).

Details: SOTT is comprised of two lines: the "Support Line," which is the VIDYA of the given source's Stochastic value, based on the %K and %D lengths, and the "SOTT Line," serving as the trailing stop of the Support Line. The market is considered in an uptrend when the Support Line is above the SOTT Line, and in a downtrend when it is below.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

kLength (simple int) : (simple int) Stochastic %K length. Default value is `500`.

dLength (simple int) : (simple int) Stochastic %D length. Default value is `200`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `0.5`.

Returns: ( [ float, float ]) Tuple of `supportLine` and `sottLine`.

Example:

= ottlib.sott(source = close, kLength = 500, dLength = 200, multiplier = 0.5)

longCondition = ta.crossover(supportLine, sottLine)

shortCondition = ta.crossunder(supportLine, sottLine)

• hottlott(length, multiplier)

Short Definition: Calculates HOTT & LOTT (Highest & Lowest OTT).

Details: HOTT & LOTT are composed of two lines: the "HOTT Line", which is the OTT of the highest price's VIDYA, and the "LOTT Line", the OTT of the lowest price's VIDYA. A high price surpassing the HOTT Line can be considered a long signal, while a low price dropping below the LOTT Line may indicate a short signal.

Parameters:

length (simple int) : (simple int) Number of bars to lookback. Default value is `20`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `0.6`.

Returns: ( [ float, float ]) Tuple of `hottLine` and `lottLine`.

Example:

= ottlib.hottlott(length = 20, multiplier = 0.6)

longCondition = ta.crossover(high, hottLine)

shortCondition = ta.crossunder(low, lottLine)

• rott(source, length, multiplier)

Short Definition: Calculates ROTT (Relative OTT).

Details: ROTT comprises two lines: the "Support Line", which is the VIDYA of the given source, and the "ROTT Line", the OTT of the Support Line's VIDYA. The market is considered in an uptrend if the Support Line is above the ROTT Line, and in a downtrend if it is below. ROTT is similar to OTT, but the key difference is that the ROTT Line is derived from the VIDYA of two bars of Support Line, not directly from it.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

length (simple int) : (simple int) Number of bars to lookback. Default value is `200`.

multiplier (simple float) : (simple float) Percent of trailing stop. Default value is `0.1`.

Returns: ( [ float, float ]) Tuple of `supportLine` and `rottLine`.

Example:

= ottlib.rott(source = close, length = 200, multiplier = 0.1)

isUpTrend = supportLine > rottLine

isDownTrend = supportLine < rottLine

• ft(source, length, majorMultiplier, minorMultiplier)

Short Definition: Calculates Fırsatçı Trend (Opportunist Trend).

Details: FT is comprised of two lines: the "Support Line", which is the VIDYA of the given source, and the "FT Line", a trailing stop of the Support Line calculated using both minor and major trend values. The market is considered in an uptrend when the Support Line is above the FT Line, and in a downtrend when it is below.

Parameters:

source (float) : (series float) Series of values to process. Default value is `close`.

length (simple int) : (simple int) Number of bars to lookback. Default value is `30`.

majorMultiplier (simple float) : (simple float) Percent of major trend. Default value is `3.6`.

minorMultiplier (simple float) : (simple float) Percent of minor trend. Default value is `1.8`.

Returns: ( [ float, float ]) Tuple of `supportLine` and `ftLine`.

Example:

= ottlib.ft(source = close, length = 30, majorMultiplier = 3.6, minorMultiplier = 1.8)

longCondition = ta.crossover(supportLine, ftLine)

shortCondition = ta.crossunder(supportLine, ftLine)

█ CUSTOM OTT CREATION

Users can create custom OTT implementations using f_ottTrail function in this library. The example code which uses EMA of 7 period as moving average and calculates OTT based of it is below.

Source Code:

//@version=5

indicator("Custom OTT", shorttitle = "COTT", overlay = true)

import ismailcarlik/ottlib/1 as ottlib

src = input.source(close, title = "Source")

length = input.int(7, title = "Length", minval = 1)

multiplier = input.float(2.0, title = "Multiplier", minval = 0.1)

support = ta.ema(source = src, length = length)

ott = ottlib.f_ottTrail(source = support, multiplier = multiplier)

pSupport = plot(support, title = "Moving Average Line (Support)", color = color.blue)

pOtt = plot(ott, title = "Custom OTT Line", color = color.orange)

fillColor = support >= ott ? color.new(color.green, 60) : color.new(color.red, 60)

fill(pSupport, pOtt, color = fillColor, title = "Direction")

Result:

█ DISCLAIMER

Trading is risky and most of the day traders lose money eventually. This library and its functions are only for educational purposes and should not be construed as financial advice. Past performances does not guarantee future results.

forex_factory_events_id_BLibrary "forex_factory_events_id_B"

Supporting Utility Library for the Live Economic Calendar by toodegrees Indicator; database with the second 500 Forex Factory News Event types.

ff_titleB(ID)

Converts a number to Forex Factory News title (second 500).

Parameters:

ID (string) : Identifier of the Forex Factory News Event. Please see the library for more information.

Returns: Returns the title of the Forex Factory News Event.

forex_factory_events_id_ALibrary "forex_factory_events_id_A"

Supporting Utility Library for the Live Economic Calendar by toodegrees Indicator; database with the first 500 Forex Factory News Event types.

ff_titleA(ID)

Converts a number to Forex Factory News title (first 500).

Parameters:

ID (string) : Identifier of the Forex Factory News Event. Please see the library for more information.

Returns: Returns the title of the Forex Factory News Event.

S&P500 Investment AverageThis script lets you choose the best time to invest in the S&P 500, thanks to a line showing an average growth of 8.32% over 50 years, starting from the price of $86.84 on January 1, 1974.

Thanks to this line indicating the price of the S&P 500 based on the average growth of the index. You'll be able to tell when the index is overvalued or undervalued.

When the price is below 20% of the line, it's a good time to invest your cash for the crash. And when it's back in the black, it's time to reduce your DCA.

You can also specify a specific date in the settings to watch the percentage whenever you like.

COT MCIThe COT MCI script is a market indicator based on the data from the Commitment of Traders Reports.

Integration of COT Report Data:

The script sources COT data from futures contracts, including:

Treasury Bonds (ZB), Dollar Index (DX), 10-Year Treasury Notes (ZN)

Commodities like Soybeans (ZS), Soy Meal (ZM), Soy Oil (ZL), Corn (ZC), Wheat (ZW), Kansas City Wheat (KE), Pork (HE), Cattle (LE)

Precious Metals such as Gold (GC), Silver (SI), Palladium (PA), Platinum (PL)

Industrial Metals like Copper (HG), Aluminum (AUP), Steel (HRC)

Energy Products like Crude Oil (CL), Heating Oil (HO), Gasoline (RB), Natural Gas (NG), Brent Crude (BB)

Currencies such as AUD (6A), GBP (6B), CAD (6C), EUR (6E), JPY (6J), CHF (6S), NZD (6N), BRL (6L), MXN (6M), RUB (6R), ZAR (6Z)

Others: Sugar (SB), Coffee (KC), Cocoa (CC), Cotton (CT), Ethanol (EH), Rice (ZR), Oats (ZO), Whey (DC), Orange Juice (OJ), Lumber (LBS), Livestock (GF), E-mini S&P 500 (ES), E-mini Russell 2000 (RTY), E-mini Dow Jones (YM), E-mini NASDAQ-100 (NQ), VIX Futures (VX), S&P 500 (SP), DJIA (DJIA)

Cryptocurrencies such as Bitcoin (BTC) and Ethereum (ETH)

Functions and Logic of the Script:

COT Calculation: Determines the net positions for commercial actors and large speculators. Also Available are short and long positions of commercials or large speculators.

Position Change Analysis: Analyzes the percentage changes in net positions and open interest data over a period of 6 weeks (Weekly Chart).

Average Value Calculation: Determines short-term and long-term trend averages.

Trend Analysis: Buy and sell signals (represented in colors) are based on linear regressions and average calculations.

Usage and Application Examples:

Ideal for traders looking for a detailed analysis of market dynamics and position changes in the futures market. Suitable for decision-making in transaction timing and assessing market sentiment.

Usage Notes:

Users should be familiar with the interpretation of COT data and basic concepts of futures trading. Particularly suitable for medium to long-term trading strategies.

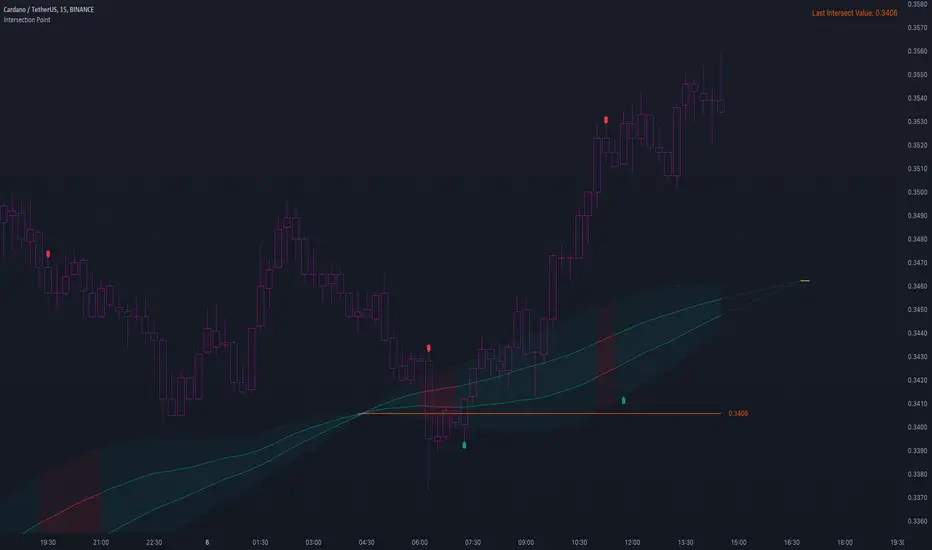

Intersection PointThis publication focusses at the intersection of 2 lines, and a trend estimation derived from a comparison of Intersection Point value against current price value.

The formula to calculate the Intersection Point (IP) is:

change1 = ta.change (valueLine1)

change2 = ta.change (valueLine2)

sf = (valueLine2 - valueLine1 ) / (change1 - change2)

I = valueLine1 + change1 * sf

🔶 USAGE

🔹 Future / Past Intersection

The position where 2 lines would intersect in the future is shown here by extending both lines and a yellow small line to indicate its location:

Of course this can change easily when price changes.

If "Back" is enabled, the IP in history can be seen:

The yellow line which indicates the IP is only visible when it is not further located then +/- 500 bars from current bar.

If this point is further away, lines towards the IP still will be visible (max 500 bars further) without the IP.

🔹 Trend

The calculated intersection price is compared with the latest close and used for estimating the trend direction.

When close is above the intersection price (I), this is an indication the market is trending up, if close is below I, this would indicate the market is trending down.

The included bands can be useful for entry/SL/TP,...

🔶 DETAILS

🔹 Map.new()

All values are put in a map.new() with the function value()

The latest Intersection is also placed in this map with the function addLastIntersectValue() and retrieved at the last bar (right top)

🔹 Intersection Point Line

The intersection price can be made visible by enabling "Intersection Price" in SETTINGS -> STYLE. To ensure lines aren't drawn all over the place, this value is limited to maximum high + 200 days-ATR and minimum low - 200 days-ATR.

🔶 SETTINGS

🔹 Choose the value for both lines :

Type : choose between

• open, high, low, close,

• SMA, EMA, HullMA, WMA, VWMA, DEMA, TEMA

• The Length setting sets 1 of these Moving Averages when chosen

• src 1 -> You can pick an external source here

🔹 Length Intersection Line : Max length of line:

Intersection Line will update untillthe amount of bars reach the "Length Intersection Line"

💜 PURPLE BARS 😈

• Since TradingView has chosen to give away our precious Purple coloured Wizard Badge, bars are coloured purple 😊😉

Fear & Greed Index (Zeiierman)█ Overview

The Fear & Greed Index is an indicator that provides a comprehensive view of market sentiment. By analyzing various market factors such as market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand, the Index can depict the overall emotions driving market behavior, categorizing them into two main sentiments: Fear and Greed.

Fear: Indicates a market scenario where investors are scared, possibly leading to a sell-off or a stagnant market. In such conditions, the indicator helps in identifying potential buying opportunities as assets may be undervalued.

Greed: Represents a state where investors are overly confident and buying aggressively, which can lead to inflated asset prices. The indicator in such cases can signal overbought conditions, advising caution or potential short opportunities.

█ How It Works

The Fear & Greed Index is an aggregate of seven distinct indicators, each gauging a specific dimension of stock market activity. These indicators include market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The Index assesses the deviation of each individual indicator from its average, in relation to its typical fluctuations. In compiling the final score, which ranges from 0 to 100, the Index assigns equal weight to each indicator. A score of 100 denotes the highest level of Greed, while a score of 0 represents the utmost level of fear.

S&P 500's Momentum: The Index monitors the S&P 500's position relative to its 125-day moving average. Positive momentum (price above the average) signals growing confidence among investors (Greed), while negative momentum (price below the average) indicates rising fear.

Stock Price Strength: By comparing the number of stocks hitting 52-week highs to those at 52-week lows on the NYSE, the Index gauges market breadth. An extreme number of highs indicates Greed, whereas an extreme number of lows suggests Fear.

Stock Price Breadth (Market Volume): Using the McClellan Volume Summation Index, which considers the volume of advancing versus declining stocks, the Index assesses whether the market is broadly participating in a trend, or if a smaller subset of stocks is driving it.

Put and Call Options: The put/call ratio helps gauge investor sentiment. A rising ratio, particularly above 1, indicates increasing fear, as more investors are buying puts to protect against a decline. A falling ratio suggests growing confidence.

Market Volatility (VIX): The VIX measures expected market volatility. Higher values generally indicate Fear, while lower values point to Greed. The Fear & Greed Index compares the VIX to its 50-day moving average to understand its trend.

Safe Haven Demand: The performance of stocks versus bonds over a 20-day period helps understand where investors are putting their money. Bonds outperforming stocks is a sign of Fear, while the opposite suggests Greed.

Junk Bond Demand: By comparing the yields on junk bonds to safer investment-grade bonds, the Index gauges risk appetite. A narrower yield spread suggests Greed (investors are taking more risk), while a wider spread indicates Fear.

The Fear & Greed Index combines these components, scales, and averages them to produce a single value between 0 (Extreme Fear) and 100 (Extreme Greed).

█ How to Use

The Fear & Greed Index serves as a tool to evaluate the prevailing sentiments in the market. Investors, often driven by emotions, can react impulsively, and sentiment indicators like the Fear & Greed Index aim to highlight these emotional states, helping investors recognize personal biases that might impact their investment choices. When integrated with fundamental analysis and additional analytical instruments, the Index becomes a valuable resource for understanding and interpreting market moods and tendencies.

The Fear & Greed Index operates on the principle that excessive fear can result in stocks trading well below their intrinsic values,

while uncontrolled Greed can push prices above what they should be.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Volume Profile with a few polylinesThe base of "Volume Profile with a few polylines" is another script of mine, Volume Profile (Maps) .

The structure of maps is used to gather the data. However, the drawings is done with polylines.

This enables coders to draw an entire volume profile with just a few polylines, while the range is broader.

This results in the benefit to draw more "lines" than with line.new() / box.new() alone.

🔶 CONCEPTS

🔹 Polylines

polyline.new creates a new polyline instance and displays it on the chart, sequentially connecting all of the points in the `points` array with line segments.

The segments in the drawing can be straight or curved depending on the `curved` parameter.

In this script, points are connected, starting from the bottom. The created line moves up until there is a price level where a volume value needs to be displayed,

at which the line goes to the left to the concerning volume value, coming back at the same price level until the line returns to its initial x-axis,

after which the line will continue to rise until all values are displayed.

A polyline can contain maximum 10000 points (10K).

Since the line has to go back and forth, each price/volume line takes 3 points.

In the case that 20K bars all have a different price, we would need 60K points, or just 6 polylines. A maximum of 100 polylines can be displayed.

The 3 highest volume values are displayed with line.new(), each with their own colour.

🔹 Maps

A map object is a collection that consists of key - value pairs

Each key is unique and can only appear once. When adding a new value with a key that the map already contains, that value replaces the old value associated with the key .

You can change the value of a particular key though, for example adding volume (value) at the same price (key), the latter technique is used in this script.

Volume is added to the map, associated with a particular price (default close, can be set at high, low, open,...)

When the map already contains the same price (key), the value (volume) is added to the existing volume at the associated price.

A map can contain maximum 50K values, which is more than enough to hold 20K bars (Basic 5K - Premium plan 20K), so the whole history can be put into a map.

🔹 Rounding function

This publication contains 2 round functions, which can be used to widen the Volume Profile

Round

• "Round" set at zero -> nothing changes to the source number

• "Round" set below zero -> x digit(s) after the decimal point, starting from the right side, and rounded.

• "Round" set above zero -> x digit(s) before the decimal point, starting from the right side, and rounded.

Example: 123456.789

0->123456.789

1->123456.79

2->123456.8

3->123457

-1->123460

-2->123500

Step

Another option is custom steps.

After setting "Round" to "Step", choose the desired steps in price,

Examples

• 2 -> 1234.00, 1236.00, 1238.00, 1240.00

• 5 -> 1230.00, 1235.00, 1240.00, 1245.00

• 100 -> 1200.00, 1300.00, 1400.00, 1500.00

• 0.05 -> 1234.00, 1234.05, 1234.10, 1234.15

•••

🔶 FEATURES

🔹 Volume * currency

Let's take as example BTCUSD, relative to USD, 10 volume at a price of 100 BTCUSD will be very different than 10 volume at a price of 30000 (1K vs. 300K)

If you want volume to be associated with USD, enable Volume * currency . Volume will then be multiplied by the price:

• 10 volume, 1 BTC = 100 -> 1000

• 10 volume, 1 BTC = 30K -> 300K

Polylines has the attributes curved & closed.

When "curved" is enabled the drawing will connect all points from the `points` array using curved line segments.

When "closed" is enabled the drawing will also connect the first point to the last point from the `points` array, resulting in a closed polyline.

They are default disabled, but can be enabled:

🔶 DETAILS

🔹 Put

When the map doesn't contain a price, it will be added, using map.put(id, key, value)

In our code:

map.put(originalMap, price, volume)

or

originalMap.put(price, volume)

A key (price) is now associated with a value (volume) -> key : value

Since all keys are unique, we don't have to know its position to extract the value, we just need to know the key -> map.get(id, key)

We use map.get() when a certain key already exists in the map, and we want to add volume with that value.

if originalMap.contains(price)

originalMap.put(price, originalMap.get(price) + volume)

-> At the last bar, all prices (source) are now associated with volume.

🔶 SETTINGS

Source : Set source of choice; default close , can be set as high , low , open , ...

Volume & currency : Enable to multiply volume with price (see Features )

Amount of bars : Set amount of bars which you want to include in the Volume Profile

🔹 Round -> ' Round/Step '

Round -> see Concepts

Step -> see Concepts

🔹 Display Volume Profile

Offset: shifts the Volume Profile (max. 500 bars to the right of last bar, see Features )

Max width Volume Profile: largest volume will be x bars wide, the rest is displayed as a ratio against largest volume (see Features )

Colours

Curved: make lines curved

Closed: connect last with first point

🔶 LIMITATIONS

• Lines won't go further than first bar (coded).

• The Volume Profile can be placed maximum 500 bar to the right of last price.

Machine Learning: Optimal RSI [YinYangAlgorithms]This Indicator, will rate multiple different lengths of RSIs to determine which RSI to RSI MA cross produced the highest profit within the lookback span. This ‘Optimal RSI’ is then passed back, and if toggled will then be thrown into a Machine Learning calculation. You have the option to Filter RSI and RSI MA’s within the Machine Learning calculation. What this does is, only other Optimal RSI’s which are in the same bullish or bearish direction (is the RSI above or below the RSI MA) will be added to the calculation.

You can either (by default) use a Simple Average; which is essentially just a Mean of all the Optimal RSI’s with a length of Machine Learning. Or, you can opt to use a k-Nearest Neighbour (KNN) calculation which takes a Fast and Slow Speed. We essentially turn the Optimal RSI into a MA with different lengths and then compare the distance between the two within our KNN Function.

RSI may very well be one of the most used Indicators for identifying crucial Overbought and Oversold locations. Not only that but when it crosses its Moving Average (MA) line it may also indicate good locations to Buy and Sell. Many traders simply use the RSI with the standard length (14), however, does that mean this is the best length?

By using the length of the top performing RSI and then applying some Machine Learning logic to it, we hope to create what may be a more accurate, smooth, optimal, RSI.

Tutorial:

This is a pretty zoomed out Perspective of what the Indicator looks like with its default settings (except with Bollinger Bands and Signals disabled). If you look at the Tables above, you’ll notice, currently the Top Performing RSI Length is 13 with an Optimal Profit % of: 1.00054973. On its default settings, what it does is Scan X amount of RSI Lengths and checks for when the RSI and RSI MA cross each other. It then records the profitability of each cross to identify which length produced the overall highest crossing profitability. Whichever length produces the highest profit is then the RSI length that is used in the plots, until another length takes its place. This may result in what we deem to be the ‘Optimal RSI’ as it is an adaptive RSI which changes based on performance.

In our next example, we changed the ‘Optimal RSI Type’ from ‘All Crossings’ to ‘Extremity Crossings’. If you compare the last two examples to each other, you’ll notice some similarities, but overall they’re quite different. The reason why is, the Optimal RSI is calculated differently. When using ‘All Crossings’ everytime the RSI and RSI MA cross, we evaluate it for profit (short and long). However, with ‘Extremity Crossings’, we only evaluate it when the RSI crosses over the RSI MA and RSI <= 40 or RSI crosses under the RSI MA and RSI >= 60. We conclude the crossing when it crosses back on its opposite of the extremity, and that is how it finds its Optimal RSI.

The way we determine the Optimal RSI is crucial to calculating which length is currently optimal.

In this next example we have zoomed in a bit, and have the full default settings on. Now we have signals (which you can set alerts for), for when the RSI and RSI MA cross (green is bullish and red is bearish). We also have our Optimal RSI Bollinger Bands enabled here too. These bands allow you to see where there may be Support and Resistance within the RSI at levels that aren’t static; such as 30 and 70. The length the RSI Bollinger Bands use is the Optimal RSI Length, allowing it to likewise change in correlation to the Optimal RSI.

In the example above, we’ve zoomed out as far as the Optimal RSI Bollinger Bands go. You’ll notice, the Bollinger Bands may act as Support and Resistance locations within and outside of the RSI Mid zone (30-70). In the next example we will highlight these areas so they may be easier to see.

Circled above, you may see how many times the Optimal RSI faced Support and Resistance locations on the Bollinger Bands. These Bollinger Bands may give a second location for Support and Resistance. The key Support and Resistance may still be the 30/50/70, however the Bollinger Bands allows us to have a more adaptive, moving form of Support and Resistance. This helps to show where it may ‘bounce’ if it surpasses any of the static levels (30/50/70).

Due to the fact that this Indicator may take a long time to execute and it can throw errors for such, we have added a Setting called: Adjust Optimal RSI Lookback and RSI Count. This settings will automatically modify the Optimal RSI Lookback Length and the RSI Count based on the Time Frame you are on and the Bar Indexes that are within. For instance, if we switch to the 1 Hour Time Frame, it will adjust the length from 200->90 and RSI Count from 30->20. If this wasn’t adjusted, the Indicator would Timeout.

You may however, change the Setting ‘Adjust Optimal RSI Lookback and RSI Count’ to ‘Manual’ from ‘Auto’. This will give you control over the ‘Optimal RSI Lookback Length’ and ‘RSI Count’ within the Settings. Please note, it will likely take some “fine tuning” to find working settings without the Indicator timing out, but there are definitely times you can find better settings than our ‘Auto’ will create; especially on higher Time Frames. The Minimum our ‘Auto’ will create is:

Optimal RSI Lookback Length: 90

RSI Count: 20

The Maximum it will create is:

Optimal RSI Lookback Length: 200

RSI Count: 30

If there isn’t much bar index history, for instance, if you’re on the 1 Day and the pair is BTC/USDT you’ll get < 4000 Bar Indexes worth of data. For this reason it is possible to manually increase the settings to say:

Optimal RSI Lookback Length: 500

RSI Count: 50

But, please note, if you make it too high, it may also lead to inaccuracies.

We will conclude our Tutorial here, hopefully this has given you some insight as to how calculating our Optimal RSI and then using it within Machine Learning may create a more adaptive RSI.

Settings:

Optimal RSI:

Show Crossing Signals: Display signals where the RSI and RSI Cross.

Show Tables: Display Information Tables to show information like, Optimal RSI Length, Best Profit, New Optimal RSI Lookback Length and New RSI Count.

Show Bollinger Bands: Show RSI Bollinger Bands. These bands work like the TDI Indicator, except its length changes as it uses the current RSI Optimal Length.

Optimal RSI Type: This is how we calculate our Optimal RSI. Do we use all RSI and RSI MA Crossings or just when it crosses within the Extremities.

Adjust Optimal RSI Lookback and RSI Count: Auto means the script will automatically adjust the Optimal RSI Lookback Length and RSI Count based on the current Time Frame and Bar Index's on chart. This will attempt to stop the script from 'Taking too long to Execute'. Manual means you have full control of the Optimal RSI Lookback Length and RSI Count.

Optimal RSI Lookback Length: How far back are we looking to see which RSI length is optimal? Please note the more bars the lower this needs to be. For instance with BTC/USDT you can use 500 here on 1D but only 200 for 15 Minutes; otherwise it will timeout.

RSI Count: How many lengths are we checking? For instance, if our 'RSI Minimum Length' is 4 and this is 30, the valid RSI lengths we check is 4-34.

RSI Minimum Length: What is the RSI length we start our scans at? We are capped with RSI Count otherwise it will cause the Indicator to timeout, so we don't want to waste any processing power on irrelevant lengths.

RSI MA Length: What length are we using to calculate the optimal RSI cross' and likewise plot our RSI MA with?

Extremity Crossings RSI Backup Length: When there is no Optimal RSI (if using Extremity Crossings), which RSI should we use instead?

Machine Learning:

Use Rational Quadratics: Rationalizing our Close may be beneficial for usage within ML calculations.

Filter RSI and RSI MA: Should we filter the RSI's before usage in ML calculations? Essentially should we only use RSI data that are of the same type as our Optimal RSI? For instance if our Optimal RSI is Bullish (RSI > RSI MA), should we only use ML RSI's that are likewise bullish?

Machine Learning Type: Are we using a Simple ML Average, KNN Mean Average, KNN Exponential Average or None?

KNN Distance Type: We need to check if distance is within the KNN Min/Max distance, which distance checks are we using.

Machine Learning Length: How far back is our Machine Learning going to keep data for.

k-Nearest Neighbour (KNN) Length: How many k-Nearest Neighbours will we account for?

Fast ML Data Length: What is our Fast ML Length? This is used with our Slow Length to create our KNN Distance.

Slow ML Data Length: What is our Slow ML Length? This is used with our Fast Length to create our KNN Distance.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Z ScoreWhat Is Z-Score?

Z-score is a statistical measurement that describes a value's relationship to the mean of a group of values. Z-score is measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. A Z-score of 1.0 would indicate a value that is one standard deviation from the mean. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

CBOE Volatility Index

VIX is the ticker symbol and the popular name for the Chicago Board Options Exchange's CBOE Volatility Index, a popular measure of the stock market's expectation of volatility based on S&P 500 index options. It is calculated and disseminated on a real-time basis by the CBOE, and is often referred to as the fear index or fear gauge. To summarize, VIX is a volatility index derived from S&P 500 options for the 30 days following the measurement date, with the price of each option representing the market's expectation of 30-day forward-looking volatility. The resulting VIX index formulation provides a measure of expected market volatility on which expectations of further stock market volatility in the near future might be based

Z Scores of VIX

When the Z-scored VIX indicator exceeds the +2 standard deviation mark, the system forecasts mean reversion and decreasing volatility and the possibility of an upward trend in S&P500.

When the Z-scored VIX indicator falls below -2 standard deviations, the system predicts future increasing volatility and the possibility of a downward trend in S&P500.

ZWAP (ZigZag Anchored VWAP) [Kioseff Trading]Hello!

Quick script showcasing the new polyline function for Pine Script!

Features

Up to 100 high/low pivot points auto anchored VWAP

Visible range auto anchored VWAP

Curved ZigZag (Adjustable!)

With the new polyline function, auto-anchored VWAP at specific price points is more viable.

When using line.new() only 500 lines can exist on the chart concurrently and, since VWAP is calculated on every update, a "proper" VWAP drawn using line.new() can extend 500 bars at most, to which no additional VWAP lines can be drawn after.

Of course, when using the plot() function a VWAP line will draw on every bar; however, this method isn't highly compatible with auto-anchoring VWAP lines.

However!

A polyline, from beginning to end irrespective of the number of coordinates used, constitutes 1 polyline; 100 can exist simultaneously with 10,000 xy coordinates per line.

The image above shows an attempt to draw the same auto-anchored VWAP lines using the line.new() function. Not an ideal outcome!

The image above shows the same attempt using the polyline.new() function!

Very nice (:

The image above shows the indicator auto anchoring to zig zag turning points.

Subsequent to a new anchoring, VWAP is calculated for the following bars - up to the current bar.

Thank you for checking this out; if you have any ideas to spice it up feel free to comment!

ATR Based EMA Price Targets [SS]As requested...

This is a spinoff of my EMA 9/21 cross indicator with price targets.

A few of you asked for a simple EMA crossover version and that is what this is.

I have, of course, added a bit of extra functionality to it, assuming you would want to transition from another EMA indicator to this one, I tried to leave it somewhat customizable so you can get the same type of functionality as any other EMA based indicator just with the added advantage of having an ATR based assessment added on. So lets get into the details:

What it does:

Same as my EMA 9/21, simply performs a basic ATR range analysis on a ticker, calculating the average move it does on a bullish or bearish cross.

How to use it:

So there are quite a few functions of this indicator. I am going to break them down one by one, from most basic to the more complex.

Plot functions:

EMA is Customizable: The EMA is customizable. If you want the 200, 100, 50, 31, 9, whatever you want, you just have to add the desired EMA timeframe in the settings menu.

Standard Deviation Bands are an option: If you like to have standard deviation bands added to your EMA's, you can select to show the standard deviation band. It will plot the standard deviation for the desired EMA timeframe (so if it is the EMA 200, it will plot the Standard Deviation on the EMA 200).

Plotting Crossovers: You can have the indicator plot green arrows for bullish crosses and red arrows for bearish crosses. I have smoothed out this function slightly by only having it signal a crossover when it breaks and holds. I pulled this over to the alert condition functions as well, so you are not constantly being alerted when it is bouncing over and below an EMA. Only once it chooses a direction, holds and moves up or down, will it alert to a true crossover.

Plotting labels: The indicator will default to plotting the price target labels and the EMA label. You can toggle these on and off in the EMA settings menu.

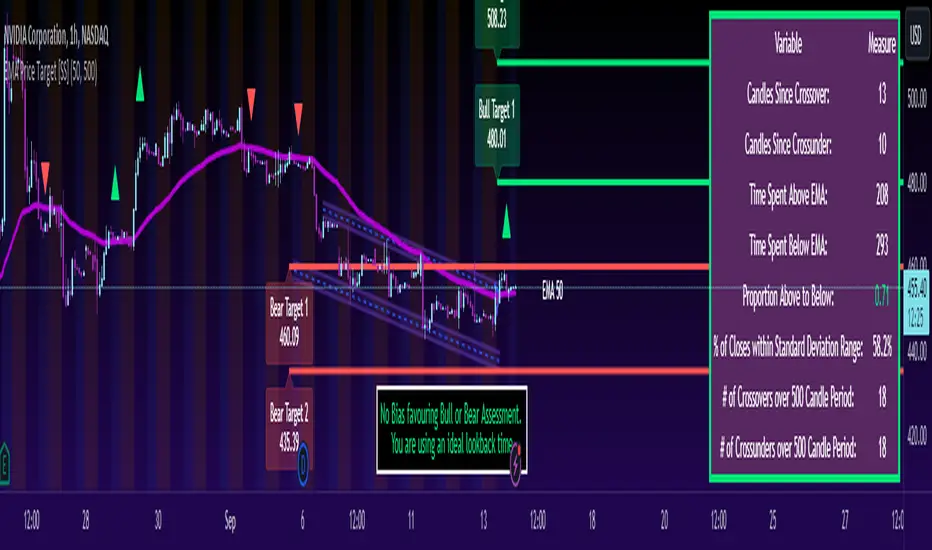

Trend Assessment Settings:

In addition to plotting the EMA itself and signaling the ATR ranges, the EMA will provide you will demographic information about the trend and price action behaviour around the EMA. You can see an example in the image below:

This will provide you with a breakdown of the statistics on the EMA over the designated lookback period, such as the number of crosses, the time above and below the EMA and the amount the EMA has remained within its standard deviation bands.

Where this is important is the proportion assessment. And what the proportion assessment is doing is its measuring the amount of time the ticker is spending either above or below the EMA.

Ideally, you should have relatively equal and uniform durations above and below. This would be a proportion of between 0.5 and 1.5 Above to Below. Now, you don't have to remember this because you can ask the indicator to do the assessment for you. It will be displayed at the bottom of your chart in a table that you can toggle on and off:

Example of a Uniform Assessment:

Example of a biased assessment:

Keep in mind, if you are using those very laggy EMAs (like the 50, 200, 100 etc.) on the daily timeframe, you aren't going to get uniformity in the data. This is because, stocks are technically already biased to the upside over time. Thus, when you are looking at the big picture, the bull bias thesis of the stock market is in play.

But for the smaller and moderate timeframes, owning to the randomness of price action, you can generally get uniformity in data representation by simply adjusting your lookback period.

To adjust your lookback period, you simply need to change the timeframe for the ATR lookback length. I suggest no less than 500 and probably no more than 1,500 candles, and work within this range. But you can use what the indicator indicates is appropriate.

Of course, all of these charts can be turned off and you are left with a clean looking EMA indicator:

And an example with the standard deviation bands toggled on:

And that, my friends, is the indicator.

Hopefully this is what you wanted, let me know if you have any suggestions.

Enjoy and safe trades!

EMA 9/21 with Target Price [SS]Hey everyone,

Coming back with my EMA 9/21 indicator.

My original one was removed a long time ago because I didn't really realize that there were already plenty of similar indicators (my bad!) but this one is my unique, Steversteves edition haha.

About the Indicator:

Essentially, it just combines the 2 only EMA's I ever really use (the 9 and 21) with an ATR based analysis to calculate the average range a ticker undergoes after an EMA 9 / 21 Cross-over and Cross-under.

You can see the major example being in the chart above. I use this for dramatic effect as SPY just happened to have topped at the second expected bull target on the daily. But obviously the intention for this indicator is to be used on the smaller timeframes. Let's take a look at some examples with various tickers.

TSLA:

So let's just use the previous day as example (which was Friday). If we look to the chart below:

TSLA did an EMA 9/21 crossover (bullish) in premarket. This put the immediate TP at 234.59. If we play out the chart:

We shot right to it at open.

We then did a cross under with a TP of 225.93, but that was not realized as the sentiment was too bullish. We then cross back over to the upside, putthing next TP at 238.88 which was realized:

NVDA:

On Friday, NVDA was a bit of a mess, lots of whipsaw off open. But once we finally had a cross under with 3 consecutive closes below the EMA9/21 on the 5 minute chart, it solidified the likelihood of a short:

And this was the result:

We came down to the first target, held it actually as support before finally crossing back over, setting the next TP at 475.05. We got 3 consecutive closes above the EMA 9/21, so let's see what happened:

Nothing really, we closed before we got there, but we did make progress towards it.

And last but not least SPY:

We opened the day with a bullish crossover and 3 consecutive closes above the EMA9/21, making our TP 441.38 (chart above). Let's see what happened:

We came just shy of it after the fed release volatility slammed it down, where we got a crossunder (bearish) to a TP of 436.21:

This ended up playing out, we did get a bullish crossover later in the day and so let's see what happened then:

So those are the real examples, most recent examples of trading using this. They are not all perfect, which is intentional because you need to use a bit of your own analysis, of course, when you are using this type of strategy or indicator. The EMA 9/21 is not sufficient generally on its own, but it is very helpful to gauge the immediate PA and whether the expected move aligns with your overall thesis on the day in terms of realistic target prices.

Customizability:

In terms of the customizability, this is a very basic indicator aside from the assessment of ranges. So there really is not a lot to customize.

You can toggle off and on the labels if you do not want them, you can also adjust the lookback length for the ATR assessment. The lookback length is defaulted to 500, I do really highly suggest you leave it at 500 because this has worked well for me and in back-testing, it has performed above my own expectations.

But, that said, you can take this and back-test as you wish with whatever parameters you feel are most appropriate. I haven't back-tested this on every stock known to man, my go to's are SPY, QQQ, sometimes MSFT and so it works well on those. But perhaps some others will have differing results.

Final Thoughts:

That is the indicator in a nutshell! It is really self explanatory and its likely a strategy most of you already know. This just helps to add realistic price targets and context to those cross-overs and cross-unders.

It also works fine on larger timeframes. We can see it on the 1 hour with MSFT:

On the 2 hour hour with QQQ:

And I am sure you can find other examples!

That's it everyone, safe trades!

RedK Relative Strength Ribbon: RS Ribbon and RS ChartsRedK Relative Strength Ribbon (RedK RS_Ribbon) is TA tool that plots the Relative Strength of the current chart symbol against another symbol, or an index of choice. It enables us to see when a stock is gaining strength (or weakness) relative to (an index that represents) the market, and when it hits new highs or lows of that relative strength, which may lead to better trading decisions.

I searched TV for existing RS indicators but didn't find what I really wanted, so I put this together and added some additional features for my own use. It started as a simple RS line with new x-weeks Hi/Lo markers, then evolved into what you see here in v1.0 with the ability to plot a full RS chart in regular or HA candle types. Hope this will be useful to some other growth traders here on TV.

What is Relative Strength (RS)

------------------------------------

(RS is a comprehensive concept in TA, below is a quick summary - please research further if it's not already a familiar topic)

Relative Strength (RS) is a technical concept / indicator used mainly by growth / swing / momentum traders to compare the performance of one security or asset against another. RS measures the price performance of a specific security relative to a benchmark, such as an index or another asset. It's not to be confused with the famous Relative Strength Index (RSI) technical indicator

For example, In the context of comparing a stock's relative strength to the SPY (S&P 500) index, the relative strength calculation involves dividing the stock's price or price-related value (e.g., close price) by the corresponding value of the SPY index. The resulting ratio (and its trend over time) indicates the relative performance of the stock compared to the index.

Traders and investors use relative strength analysis to identify securities that have been showing relative strength or weakness compared to a benchmark, which can help in making investment decisions or identifying the "market leaders" and potential trading opportunities.

There are so many books and documentation about the RS concept and its importance to identify market leaders, especially when recovering from a bear market - if you're interested in the concept, please search more about it and review some of that literature. There's also a more detailed definition of Relative Strength in this article on Invstopedia

RedK RS_Ribbon features and options

---------------------------------------------------

The indicator settings provide many options and features - see the settings box below

- Change / choose base symbol

The default is to use SPY as the base symbol - so we're comparing the chart's symbol to a proxy of the S&P 500 - Some traders may prefer to use the QQQ - or other index or ETF that acts as a proxy for the industry / sector / market they are trading

- RS Calculation / RS line

we use the simple form of the RS calculation,

RS = closing price of current chart symbol / closing price of the base symbol (default is SPY) * 100

some RS documentation will use the Rate of Change (RoC) - but that's not what we're using here.

- The RS_Ribbon

* Once the RS line is plotted, it made sense to add couple of moving averages to it, to make it easier to observe the trend of the RS and the changes in that trend as you can see in the sample chart on top.

* The RS_Ribbon is made up of a fast and slow moving averages and will change color (green / red) based on detected trend RS direction - the 2 MA types and lengths can be changed until you get the setup that provides the best view for you of the RS trend over time. My preferred settings are used as defaults here.

- Identifying New (x)Week Hi/Lo RS Values

* Most traders would be interested when the calculated RS hits a new 52-week high or low value.

* There are cases where we may want to see when a new RS Hi/Lo has been hit for a different period - for example, a quarter (13 weeks)

* the number of weeks can be changed as well as adjusting the numbers of trading days per week (if needed for certain symbols/exchanges)

- Working with Different Timeframes

* Now these "markers" will only be available in the daily and weekly timeframes and there is a good reason for that, it's not the fact that i'm lazy :) and that enabling this in timeframes lower than 1D would have been some heavy lifting, but the reality is that with RS, we're really interested if a "day's close" hits a new RS high or low value against the moving window of x weeks (and the weeks close also) - if you think of this more, at lower TF, RS can hit a lower value that never end up registering on the daily closing and that causes a lot of visual confusion. So i took the "cleaner way out" of that issue.

* note that you can choose a different timeframe for the RS_Ribbon than the chart - if you do, please make sure the chart is at a lower timeframe than the indicator's - (and in that case remember to hide the candles because they won't make much sense)

i wanted to leverage TV's built-in multi-Timeframe (MTF) support with the caveat that using the indicator at lower TF with a chart at a higher TF (example chart at 1Wk and indicator at 1D) will show inaccurate results. If this sounds confusing, keep the indicator TF same as the chart.

the example here shows a 2-Hr chart against 1D RS_Ribbon

- Using RS Charts and RS Candles

* Beside the ability to plot the RS "closing" value with the RS line, the indicator provides the ability to show a "full" RS Chart with candles that represent the relative values of open, high, low. and close against the base symbol.

* the RS Charts can be used for regular chart analysis, for example, we can identify common chart patterns like Cup & Handle, VCP, Head & Shoulder..etc using these charts .. which can provide some edge over the price charts

* for the Heikin Ashi fans, I added the ability to choose classic or HA candles for the chart. note you have to enable the option to show the RS candles first before you choose the option to switch to HA.

The chart below shows a side-by-side comparison on the 2 RS chart types

Closing remarks

-----------------------

* RS is a good way to identify market/sector leaders (who will usually recover from a bear market before others) - and enable us to see the strength that comes from the broader makrket versus the one that comes from the stock's own performance and identify good trading opportunities

* I'll continue to update this work and alerts will come in next version - but wanted to check initial reaction and value

* as usual, if you decide to use this in your chart analysis, it's necessary to combine with other momentum, trend, ...etc indicators and do not make trading decision only based on the signales from a single indicator

Trend Correlation HeatmapHello everyone!

I am excited to release my trend correlation heatmap, or trend heatmap for short.

Per usual, I think its important to explain the theory before we get into the use of the indicator, so let's get into the theory!

The theory:

So what is a correlation?

Correlation is the relationship one variable has to another. Correlations are the basis of everything I do as a quantitative trader. From the correlation between the same variables (i.e. autocorrelation), the correlation between other variables (i.e. VIX and SPY, SPY High and SPY Low, DXY and ES1! close, etc.) and, as well, the correlation between price and time (time series correlation).

This may sound very familiar to you, especially if you are a user, observer or follower of my ideas and/or indicators. Ninety-five percent of my indicators are a function of one of those three things. Whether it be a time series based indicator (i.e.my time series indicator), whether it be autocorrelation (my autoregressive cloud indicator or my autocorrelation oscillator) or whether it be regressive in nature (i.e. my SPY Volume weighted close, or even my expected move which uses averages in lieu of regressive approaches but is foundational in regression principles. Or even my VIX oscillator which relies on the premise of correlations between tickers.) So correlation is extremely important to me and while its true I am more of a regression trader than anything, I would argue that I am more of a correlation trader, because correlations are the backbone of how I develop math models of stocks.

What I am trying to stress here is the importance of correlations. They really truly are foundational to any type of quantitative analysis for stocks. And as such, understanding the current relationship a stock has to time is pivotal for any meaningful analysis to be conducted.

So what is correlation to time and what does it tell us?