TOST looks to breakoutTOST earings are coming around the corner and the company is JUST becoming profitable. This reminds me of SOFI and HOOD and how they picked up steam so heavily as the negative EPS dropped. The stock saw a nice 50% fib pullback and is now contracting right into earnings. These wedges have a habit of breaking down after an upward pump. This is where you want to look at short interest, this amount isnt tremendously high but could cause a false wedge breakout.

My plan: My target for the year is 56$

As I sell out of TSLL I might be adding this as a new play alongside NBIS

The premium is high so I would likely buy 1-200 shares and then start selling CSP here

Trade ideas

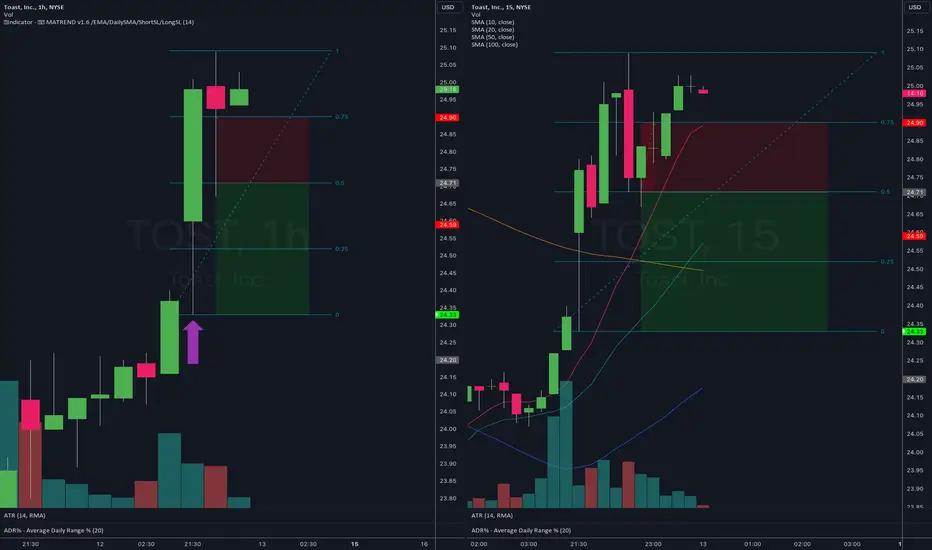

TOST long on Monday if it holds above the trend line supportlong TOST as long as it holds the 1hr support line. The breakout Friday was a show of strength after breaking down.

TOST breakout signals: Bullish trend with $65 targetTOST stock has recently broken out of its base pattern, signaling a continuation of the upward trend with potential for further gains toward $65 or higher. As long as the stock remains above the key support zone of $35/$36, the long-term outlook remains bullish.

TOST weekly chart breakoutTOST weekly chart breakout

NYSE:TOST gave a breakout on a weekly chart.

The base is quite big so the potential upside move could be large as well.

Also we are in a slow rate cut phase, which will help the tech/growth companies.

My stop loss level will be at 27.

Swing trade (my technicals are horrible, but you get the idea)The financials are strong, and I think the technicals show opportunity for a breakout after some price consolidation. I think with the increase in restraurants when interest rates fall, the software will be used more. We'll see!

TOSTMy second attempt to build a position. Starting with a smaller size, after a flat and the continued strength. Expect it to break the base channel. Nice upside potential

Trade safe

TOST - JULY 24 MATrend Unsustainable Momentum- D1 larger trend is aligned to our bearish direction

MATrend Unsustainable Momentum (Systematic) ⏪

The strategy identifies stocks (Tech sector ) that follows the larger market regime's momentum of the day and because they are unable to maintain it price breaks down quickly

Tight stops aligned to the price behaviour we are trying to capture. Which is a rapid break of the momentum.

TOST - JUNE 24 MATrend Unsustainable MomentumBAD Trade

I made a snap decision to enter this price even though it was below 0.5. With the idea that I could tweak the entry rule to be between 0.5 and 0.25.

I will make it a point that critical decisions that impacts system rules rules should only happen after an evaluation when the market closes.

I can then solve it with clarity and without trading pressure. I do not need to take the trade as there will always be new opportunities

MATrend Unsustainable Momentum (Systematic) ⏪

The strategy identifies stocks (Tech sector ) that follows the larger market regime's momentum of the day and because they are unable to maintain it price breaks down quickly

Tight stops aligned to the price behaviour we are trying to capture. Which is a rapid break of the momentum.

TOST Potential Buy SetupReasons for bullish bias:

- Bullish Crab formation

- Entry at HH breakout for trend confirmation

- Dow theory

- Bearish divergence

Entry Level(buy stop): 20.45

Stop Loss Level: 15.97

Take Profit Level 1: 24.93

Take Profit Level 2: open

TOST - Keep an Eye on Ita little checkback on TOST here would set this up nicely around its 50 MA.

Shakeout of its 50 MA few days back and a higher low here ahead of earnings would be ideal.

One to keep on your secondary watchlist.

$TOST 4/26/24 $23 calls speculation flowNYSE:TOST sitting at the ~22.50 zone. This zone has acting as a zone of major support/resistance in the past. NYSE:TOST has been consolidating at this level for the past 3 days.

Broadening Formation and right at important pivotBroadening formation which can lead to volatility. Looks to want to go higher after a lengthy consolidation and downtrend. Not long, but would take a short swing trade after a break of the pivot in the middle of the broadening formation

TOST Back to Breakout LevelToast pulling back to previous breakout base level. 200 MA line just turning back up (turning blue). Could use 2 to 3 more days to see how the stuck gets supported at these levels.

Watch item as we head into next week.

cup and handlecup and handle forming, wait for confirmation of break out and could go up 46 percent move!!!

TOST - Early breakout above value presents nice R/RTOST broke out above value at the end of last week, and is triggering a long as a result with the target being the Monthly VPOC at $35.05.

With a stop just inside of value for the year this represents a risk/reward ratio above 5.

Toast breaking out of 2 year long baseMarket conditons are favorable.

Toast is attempting to break out of a 2 year long base. The 2 year trend is now up.

I will buy with a stop.

Best of luck.

Toast Inc - Long NYSE:TOST has demonstrated considerable momentum, leading us to explore two potentially favorable scenarios for its price trajectory.

Firstly, considering the current landscape of an overextended broader market, driven by the success of NASDAQ:NVDA , the potential for a correction becomes apparent, possibly triggered by the impending NASDAQ:NVDA earnings call. In this scenario, a positive outcome would involve a rebound within the 17-19 dollar range, indicative of a resilient continuation of momentum for $TOST.

In a second scenario, if broader markets hold momentum or NASDAQ:NVDA reports earnings substantially exceeding expectations, leading to a persistent buying frenzy, NYSE:TOST could sustain its momentum and break potentially out of its current range.

Same applies in a scenario when there's zero correlation to the broader market and the momentum holds ground.

In this context, a plausible price target would be within the 30-32 dollar range, supported by the technical broadening channel and historical highs.

Please note that this analysis is for informational purposes only and should not be considered financial advice.

TOST breakout ideaBig Sideway base for TOST over last two years and after a strong earnings report this stock is on watch for a breakout.

Using the MarketWebs system (VolumeAtPrice) the trigger is a break over $22.97

Toast Plans To lay Off 10% of its Workforce, As Growth SlowsToast, ( NYSE:TOST ) maker of restaurant management software, stated on Thursday it will lay off 550 employees, about 10% of its workforce. The company also reported fourth-quarter earnings that beat Wall Street’s expectations.

Several Tech companies have instituted layoffs in 2024. On Wednesday Cisco ( NASDAQ:CSCO ) said it would eliminate 4,000 jobs as sales declined and clients became even more cautious about spending.

Toast’s ( NYSE:TOST ) shares were initially up as much as 16%.88 after hours but then gave back much of the gains.

According to the recently published report, the company's earnings per share were a loss of 7 cents per share, which is better than the expected loss of 11 cents per share. The revenue for the quarter was $1.04 billion, which exceeded expectations of $1.02 billion. Toast ( NYSE:TOST ), as per the statement released by the company, saw an increase of nearly 35% in revenue as compared to the previous year. Its net loss of $36 million in the current quarter is an improvement from the $99 million loss in the same quarter last year. The company has allocated $250 million for share buybacks.

The pandemic led many restaurants to adopt Toast’s mobile ordering and payment tools, which helped double the company’s revenue. Shares debuted on the New York Stock Exchange in 2021, amid that uptick. Demand has sublimed since then, down from 37% in the third quarter and about 45% in the second quarter.

Toast ( NYSE:TOST ) faces increasing competition from the likes of Block, Fiserv, and Shift4, Bank of America analysts wrote in a December note as they reduced their rating on the stock from buy to neutral.

Toast’s ( NYSE:TOST ) new layoffs should result in $45 million to $55 million in charges, mostly in the first quarter, and $100 million in annualized savings.

Those cuts come weeks after Aman Narang, Toast’s co-founder and COO, replaced Chris Comparato as CEO. Under Comparato’s leadership last summer, Toast ( NYSE:TOST ) began to charged a fee of 99 cents for each online order that totaled more than $10. Consumers and restaurant owners objected, prompting urging the company to eliminate the surcharge.

TOST, SELL, 17.1% PROFITShorted NYSE:TOST on 11/7/2023 at market close and closed the position on 11/8/2023 at market open. net 17.1% profit.

Toast's (TOST:NYSE) Recent Successes Impressive Financial Milestones: Toast's Recent Successes

Exceeding $1 Billion Annualized Recurring Run-Rate

In a recent announcement, Toast revealed remarkable financial achievements, surpassing the significant milestone of $1 billion in annualized recurring run-rate. This accomplishment underscores the company's robust business model and its capacity to capture recurring revenue streams, indicative of customer loyalty and market demand.

Achieving Adjusted EBITDA Profitability and Positive Free Cash Flow

A noteworthy highlight in Toast's recent financial report is its attainment of Adjusted EBITDA profitability and positive free cash flow, marking a pivotal moment since its initial public offering (IPO). This achievement demonstrates the company's dedication to achieving financial sustainability and efficiency in its operations.

Anticipated Growth Trajectory

Toast remains optimistic about its growth prospects, projecting continued increases in both revenue and Adjusted EBITDA for the third quarter of 2023 and the entirety of the year. This outlook speaks to the company's strategic planning, market positioning, and its ability to adapt to evolving market dynamics effectively.

Comprehensive Platform and Competitive Edge

Toast's success is attributed, in part, to its comprehensive platform that caters to various aspects of the restaurant industry. This all-encompassing approach enables the company to offer end-to-end solutions, enhancing its value proposition to clients. Additionally, Toast benefits from a competitive moat and strong network effects, solidifying its market position and reducing the threat of new entrants.

Compelling Valuation and Limited Risks

Intriguingly, Toast's valuation has become increasingly compelling as its financial performance improves. This presents an opportunity for potential investors to enter the market at an advantageous point. Furthermore, the company's approach to risk management has resulted in limited uncertainties, contributing to the overall appeal of investing in Toast's stock.

Conclusion: A Promising Investment Prospect

In conclusion, Toast's recent financial achievements, coupled with its projected growth, comprehensive platform, competitive advantages, appealing valuation, and prudent risk management, collectively position the company as a compelling investment opportunity. As the company continues to make strides in its industry, investors are likely to view Toast's stock as an attractive addition to their portfolios.

This content is provided for general information purposes only and is not to be taken as investment advice nor as a recommendation for any security, investment strategy or investment account.