AppLovin’s Turning PointFew listed companies have moved from relative obscurity to the centre of a global industry as quickly as AppLovin. A decade ago it was known mainly in mobile gaming circles. Today, it sits at the core of how thousands of mobile applications acquire users and make money, powered by an increasingly influential advertising platform built on artificial-intelligence techniques.

That transformation is now colliding with two powerful forces: exceptional financial momentum on one side and rising regulatory scrutiny on the other. Understanding the current state of AppLovin means looking at both stories at once.

What AppLovin Actually Does

At its core, AppLovin is an infrastructure company for the mobile application economy. It provides a technology platform that helps:

Developers of mobile applications show advertising inside their apps and get paid for those impressions.

Advertisers reach the right users at the right moment inside those apps, and measure whether those campaigns are actually profitable.

The company positions itself as an “outcome-driven” marketing platform: instead of simply maximising the number of ad impressions, its tools try to maximise the advertiser’s return on each unit of advertising spend. Its products help clients:

acquire new users for their apps

monetise those users through in-app advertising

track and analyse the performance of campaigns across different ad networks and channels.

In practical terms, a mobile game studio, a shopping application or a streaming service can plug into AppLovin to outsource much of the heavy lifting of advertising technology.

From Game Publisher to Advertising Infrastructure

AppLovin began with deep roots in mobile gaming, including publishing and operating its own titles. Over time, however, the strategic emphasis shifted decisively from being a game studio to becoming the “picks and shovels” provider powering many studios at once.

That shift is now largely complete. In 2025, AppLovin sold its mobile game studio to Tripledot Studios in a transaction worth around eight hundred million dollars, a clear signal that management wants a cleaner, asset-light profile focused on software and data rather than content ownership.

The long-term bet is simple: there are far more economics to be captured in running the rails of mobile advertising than in betting on individual game hits.

The Axon Engine: AppLovin’s “Brain”

The centre of AppLovin’s current strategy is its proprietary engine known as Axon. Axon is a large-scale decision system that evaluates every potential advertisement impression in real time. It decides:

which advertisement should be shown to which user

how much to bid for that impression on behalf of an advertiser

how to balance short-term revenue with longer-term campaign objectives such as retention or in-app purchases.

The latest generation, often referred to as Axon 2, is described by the company and external analysts as a powerful recommendation engine that learns from billions of data points to optimise campaigns. It sits inside a closed ecosystem that combines both “supply” (the apps showing advertising) and “demand” (the advertisers buying it), allowing continuous feedback loops and optimisation.

In 2025 AppLovin rebranded the platform as “Axon by AppLovin” and introduced Axon Ads Manager, a self-service interface that lets advertisers manage campaigns directly through a dashboard. Initially, access is by referral only, emphasising a controlled ramp-up with selected partners. The goal is explicit: to position Axon as a high-return alternative to the advertising ecosystems of very large technology platforms such as Meta and Google.

Financial Momentum: Growth With Extraordinary Margins

The numbers behind this strategy help explain why AppLovin has attracted so much attention in public markets.

For the full year 2024, the company generated approximately 4.71 billion dollars in revenue and about 1.58 billion dollars in net income, implying a net profit margin in the mid-thirties. That is already a highly attractive profile for an advertising technology business.

The acceleration continued into 2025. In the third quarter of 2025:

revenue reached about 1.4 billion dollars, an increase of roughly sixty-eight percent compared with the same period a year earlier

net income rose to around 836 million dollars, up more than ninety percent year on year

Analysts highlight an adjusted operating profit margin above eighty percent in the latest quarter, an extremely high figure even by software standards and far above the typical advertising technology peer.

Management has guided for roughly 1.59 billion dollars in revenue in the fourth quarter (mid-point of guidance), ahead of the average analyst expectation of about 1.55 billion dollars.

The stock market has responded accordingly. Over the past year, AppLovin’s share price has more than quadrupled and it has been added to the main large-capitalisation equity index in the United States. In calendar year 2025 alone, the shares have more than doubled. At the time of writing, AppLovin’s shares trade around five hundred and twenty dollars, giving the company a market value in the region of two hundred billion dollars.

This combination of rapid top-line growth, very high margins and a strong stock-market performance has led some commentators to describe AppLovin as a rising leader in artificial-intelligence-driven advertising platforms.

The Shadow on the Story: Data and Regulation

Against this backdrop of financial success, however, the company faces a serious challenge: growing regulatory scrutiny over how it collects and uses data.

In October 2025, reports emerged that the United States Securities and Exchange Commission had opened an investigation into AppLovin’s data-collection practices, following a whistle-blower complaint and several reports by short-selling firms. These critics allege that AppLovin may have violated service agreements with large platforms in order to gather data for advertising purposes, and that certain products enabled more intrusive tracking than disclosed.

Further reporting has suggested that multiple state attorneys general are also examining whether AppLovin’s practices might have breached privacy rules, including regulations designed to protect children online. One controversial product, known as Array, has already been shut down after accusations that it enabled unauthorised application downloads and tracking behaviour.

AppLovin strongly denies wrongdoing. The company says that its systems require user consent and comply with industry standards, and it has hired the law firm Quinn Emanuel to conduct an independent review of the allegations. At this stage, the Securities and Exchange Commission has not formally accused AppLovin of any violation, but the overhang is real: the initial news of the investigation triggered a double-digit percentage fall in the share price in a single session.

For investors and industry observers, the key question is whether the company’s growth has relied on practices that may not be acceptable under tightening privacy rules, or whether it can demonstrate that its edge comes primarily from better modelling and integration, not from cutting corners on compliance.

Strategic Ambition at Global Scale

Regulatory questions aside, AppLovin is clearly playing for very high stakes.

The company has already paused and then reopened access to its flagship Axon platform in order to manage growth and product quality. It is investing heavily in new formats such as dynamic product advertisements that automatically generate image-based creatives for commerce clients, and it is expanding well beyond gaming into sectors such as online retail and services.

Its ambitions extend into deal-making as well. Reports indicate that AppLovin has made a bid for the non-China assets of TikTok, underlining management’s willingness to contemplate very large acquisitions that could reshape the digital advertising landscape.

If Axon Ads Manager gains traction as a self-service tool, AppLovin could increasingly look like a third major “walled garden” in performance advertising, alongside the largest social and search platforms. That would strengthen its bargaining power with advertisers and partners but might also invite closer attention from regulators and competitors.

How to Think About the Current Situation

For readers who are new to the story, AppLovin today can be summarised in three points:

It has become critical mobile infrastructure. Its tools help a large portion of the mobile application ecosystem to acquire users and monetise attention. This gives it scale advantages and a rich data environment that are hard to replicate.

Its financial profile is unusually strong. Revenue is growing rapidly, profitability is very high and cash generation is robust. The market has rewarded this with a very high valuation.

It is operating under an intensifying regulatory cloud. Allegations around data privacy and user tracking, plus formal investigations by regulators, introduce non-trivial legal and reputational risk.

The balance between those three forces will determine the next chapter. If AppLovin can demonstrate that its competitive edge is sustainable within stricter privacy norms, continue to roll out Axon successfully and avoid major legal penalties, it could consolidate its position as a long-term winner in performance advertising. If, however, investigations uncover serious issues or lead to restrictive settlements, the current profitability and valuation could prove difficult to justify.

For now, AppLovin is both one of the most impressive growth stories in digital advertising and one of the most closely watched from a regulatory perspective. Anyone following the mobile economy over the next few years will need to keep an eye on this company, its Axon platform and the evolving rulebook that governs how personal data can be used in the pursuit of advertising performance.

This article is for information purposes only and does not constitute investment advice or a recommendation to buy or sell any security.

Trade ideas

APPAPP has proven strong and a major player in the game of growth. Based on my analysis, I believe it to give us 100$ to the upside in the next 78 hours

APP SwingReasoning:

Strong Industry/Sector

50MA Pullback

Long-Term Investors (3-12 Month Holds)

Entry: Full position on breakout

Profit Taking: Sell 1/4 to 1/5 at Goal 1

Exit Signal: Close below 20-day EMA (your trend guide) or 50EMA

Why: Strong moves are hard to time at the top, but the 20EMA acts as a reliable trend filter

Note:

Remember: Every long-term investment alert can also be played as a swing trade.

APP - UPTREND STILL INTACT!APP - CURRENT PRICE : 670.00 - 674.00

APP is showing strong bullish momentum as the price trades above the 50-day EMA and ICHIMOKU CLOUD , indicating a sustained uptrend. The RSI is in bullish territory but not yet overbought, indicating room for further upside. With the current setup, the stock has potential to retest its all-time high area if momentum continues.

ENTRY PRICE : 670.00 - 674.00

FIRST TARGET : 727.00

SECOND TARGET : 770.00

SUPPORT : 50-day EMA

APP: at risk of deeper correctionAs long as price stays below today’s high and the 700 level, I’m watching for a deeper pullback toward 515–480 or a potential re-test of the June 2025 highs.

Alternatively, a sustained breakout above 700 would open the door for a continuation move toward the next macro resistance zone at 900–1100.

Chart:

Macro view:

AppI think it will resolve to the upside Macd shows bears losing momentum No one is selling . showing strength against the market when olmost everything is red . Stop loss below support

BearishAPP (Applovin) – Bearish Trade Plan

Setup: Price rejected from ~$725 resistance after a strong run. Momentum shows signs of exhaustion with potential for a corrective move lower.

Entry:

Short around $695–705 on weakness (confirmation with daily close below $700 preferred).

Stop Loss:

Above $730 (recent high and failed breakout).

Targets:

Target 1: $625 (prior breakout level / strong support).

Target 2: $537 (deeper support zone, aligns with May/June consolidation).

Risk/Reward:

Target 1: ~3.0R

Target 2: ~6.0R

Trade Management:

Scale out 50% at $625.

Move stop to breakeven after first target hit.

Let remaining position run toward $537 if bearish momentum persists.

APP eyes on $652.99: Golden Genesis fib support should BOUNCEAPP is finally pulling back after a big surge.

Now approaching a Golden Genesis fib at $652.99

Look for a clean bounce or drop to next fib for entry.

.

See "Related Publications" for previous plots, including this PERFECT BOTTOM call:

Hit BOOST and FOILLOW for more such PRECISE and TIMELY charts.

=========================================================

.

Short Trade Rationale for APP (AppLovin Corp)While the overall technical picture for AppLovin Corp. (APP) is overwhelmingly bullish, a short case can be built on the following technical and fundamental cautionary signs, suggesting a potential near-term pullback or a high-risk long-term outlook.

The stock's current price is trading significantly above certain valuation models, which may suggest a frothy or unsustainable valuation based on fundamentals.

Significant Insider Selling: The stock has seen "significant insider selling over the past 3 months," which can be interpreted as a lack of confidence in the current valuation or future prospects by those who know the company best.

High Debt Load: AppLovin is noted to have a "high level of debt", which increases financial risk, especially in a higher interest rate environment.

Regulatory & Competition Risk: The business model, heavily reliant on mobile advertising, faces threats from increasing data privacy regulations and widespread consumer use of ad-blockers, which could undermine the effectiveness of AppLovin's ad-targeting platform and limit revenue and margin growth. Furthermore, rising competition from larger tech companies could lead to market share erosion.

Trade Idea:

Short Entry (Red Arrow Target): The proposed short entry is at the price level of $735.32. On the 4-hour chart, the red arrow points to a price area near the upper boundary of the defined uptrend channel (pink lines) and potentially a price rejection point from the overall sharp upward movement. This level represents a technical area of resistance where selling pressure is expected to overcome buying pressure, leading to a downward reversal.

Exit (Green Arrow Target/Take Profit): The proposed exit is at the price level of $641.87. The green arrow on the 4-hour chart points to an area around the lower trendline of the defined short-term uptrend (pink lines). This level could act as a significant level of support. Taking profits here assumes a move down to the lower boundary of the current upward channel before a potential bounce or consolidation.

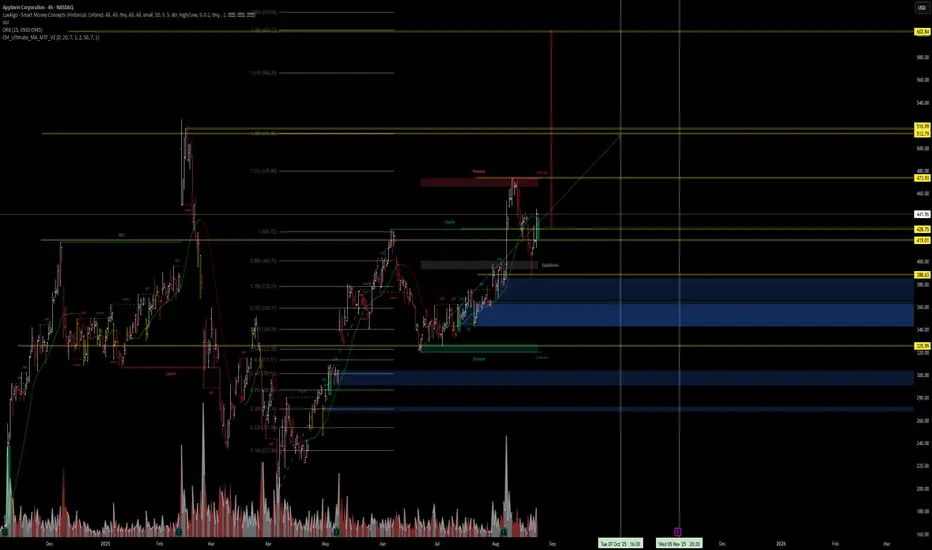

APP | The Dealer Price Pull is Real for Applovin => $800Dealers have been on the right side of APP's recent run. Current analysis shows collective bullish forecast and $800 price target. Small current pivot could be a nice entry point if not in already.

AppLovin the Rocket Ship40% revenue growth quarter after quarter, these guys are the real deal. The stock price reflects the aggressive growth made by AppLovin. Unless there is some serious accounting fraud going on, this is the type of stock you buy on the dip for the next leg up. I entered a swing trade at the confluence of 200 Day moving average and the golden pocket fibonacci level around $237.

The bounce was strong and my stop loss has been moved up to break even . If they have another strong quarter showing 40% growth the 5th Wave could be in play.

Not financial advice, do what's best for you.

APP BUY IDEABroke out of a bullish triangle pattern, with fundamentals backing the move.

AppLovin will be added to the S&P 500 on Sept 22, 2025, while strong earnings and positive analyst ratings reinforce bullish momentum.

Applovin Corp. Trading Idea. 2H. We are seeing how good the first impulse was. It's marked with a green arrow on the Chart.

The second destination is our TP... We hope the second one will be just as good.

Hit Your Take Profits. That's my wish for you.

AppLovin: Undervalued AI Ad Tech Powerhouse or Volatility Trap? AppLovin: Undervalued AI Ad Tech Powerhouse or Volatility Trap? $615 Target Incoming?

AppLovin (APP) shares are trading at $567.12 today, up 1.60% amid a fresh 52-week high and S&P 500 inclusion set for September 22, fueling a 75% YTD rally driven by its AI-powered marketing platform.

With Q2 2025 earnings crushing expectations—revenue surging 44% YoY to $1.44B and EPS at $0.89—analysts are bullish, hiking targets to $615 amid 53% projected EPS growth over 3-5 years. But at a trailing P/E of 78x, is APP the undervalued gem poised to go viral in the $500B mobile ad market, or will high beta (3.85) and market jitters trigger a pullback? Let's unpack the fundamentals, SWOT, charts, and setups for September 11, 2025.

Fundamental Analysis

AppLovin's dominance in mobile app advertising and gaming, bolstered by its AXON AI engine, has propelled explosive growth, with free cash flow hitting $1.2B TTM and margins expanding to 35%. Analysts forecast 2025 EPS of $13.49 on $5.74B revenue, up 40% YoY, as AI optimizations drive advertiser ROI in a post-cookie world. Recent S&P 500 addition could attract $10B+ in passive inflows, underscoring its undervalued status at 1.8% below fair value per DCF models. However, premium valuations reflect growth bets, with risks from ad spending slowdowns if the economy softens.

- **Positive:**

- AI platform fueling 53% EPS growth forecast; Q2 beat with 44% revenue jump and net income flipping to $236M from prior losses.

- S&P 500 entry sparks institutional demand; market cap at $191.8B undervalues its 700%+ stock surge since 2023 lows.

- Broader trends in digital ads and gaming (e.g., partnerships with Unity) position APP for 20%+ annual gains amid AI boom.

- **Negative:**

- High beta (3.85) amplifies volatility; recent 24% monthly gain risks overextension if Fed delays cuts.

- Competition from Meta and Google could pressure market share if ad budgets shift.

SWOT Analysis

**Strengths:** Leading AI-driven ad tech with 2B+ daily users; strong cash generation ($1.2B FCF) enables buybacks and acquisitions; proven turnaround from gaming to profitable software focus.

**Weaknesses:** Elevated P/E (78x TTM) signals growth dependency; high volatility with beta 3.85 exposes to market swings; reliance on mobile ecosystem vulnerable to app store policy changes.

**Opportunities:** S&P 500 inclusion for passive inflows; expansion into e-commerce and CTV ads via AI; undervalued growth at 42x forward P/E amid 53% EPS CAGR.

**Threats:** Economic downturn crimping ad spend; intensifying competition from Big Tech; regulatory scrutiny on data privacy impacting AI models.

Technical Analysis

On the daily chart, APP is in a strong uptrend, breaking to new 52-week highs at $576 after consolidating above $500 support, with volume spiking on S&P news. The weekly shows a multi-year bull flag breakout from 2023 lows, now extending with higher highs. Current price: $567.12, with VWAP near $560 as intraday pivot.

Key indicators:

- **RSI (14-day):** At 68, bullish but approaching overbought—room for extension if momentum holds. 📈

- **MACD:** Positive crossover with expanding histogram, confirming upside acceleration; watch for divergence on overbought signals. ⚠️

- **Moving Averages:** Price well above 21-day EMA ($520) and 50-day SMA ($480), with golden cross intact; 200-day EMA at $350 trails far below.

Support/Resistance: Key support at $500 (recent breakout level and 50-day SMA), resistance at $576 (all-time high) and $615 (analyst target). Patterns/Momentum: Bull flag extension targets $650; strong buy rating for 1-week horizon. 🟢 Bullish signals: Volume surge and S&P catalyst. 🔴 Bearish risks: Overbought RSI could prompt 10% pullback on profit-taking.

Scenarios and Risk Management

- **Bullish Scenario:** Break above $576 on S&P inflows or soft CPI data targets $615 short-term, then $650 by year-end. Buy pullbacks to $500 for high-conviction entries.

- **Bearish Scenario:** Drop below $500 eyes $450 (200-day EMA); broader tech selloff could retrace 15-20% if growth slows.

- **Neutral/Goldilocks:** Range-bound $500–$576 if data mixed, ideal for options plays or waiting for Q3 earnings.

Risk Tips: Set stops 3% below support ($485) to manage volatility. Risk 1-2% per trade. Diversify with META or GOOGL to hedge ad sector correlations—avoid overexposure in high-beta names.

Conclusion/Outlook

Overall, a bullish bias if APP sustains above $500, highlighting its undervalued growth with 50%+ upside amid AI ad dominance and S&P buzz—perfect for viral momentum in retail circles. But monitor Fed decisions and Q3 guidance for confirmation; this fits September's small-cap rotation into high-growth tech. What’s your take? Loading up on APP's rally or waiting for a dip? Share in the comments!

APP eyes on $407.08: Golden Genesis fib may end the CorrectionAPP has been pulling back with the general market.

Currently testing a Golden Genesis fib at $407.08.

Look for a clean bounce to maybe end correction.

It is UNLIKELY to be "the" bottom.

It is PROBABLE to be "a" bottom.

It is PLAUSIBLE to break and fall.

.

Previous Analysis that caught a PERFECT BREAKOUT

Hit BOOST and FOLLOW for more such PRECISE and TIMELY charts.

========================================================

.

AppLovin (APP) – Momentum Building for a Breakout?Hey traders!

Let’s take a closer look at AppLovin Corp (NASDAQ: APP), which is showing some serious strength on the weekly chart.

Current Price: $466

Entry Zone: $450 – This level has acted as a solid support and could offer a great risk-reward setup.

Target 1: $540 – A key resistance level and potential short-term profit zone.

Target 2: $700 – If bullish momentum continues, this could be the next major upside target.

Catalyst to Watch:

AppLovin is rumored to be a strong candidate for S&P 500 inclusion. Such a move could trigger institutional buying, increase visibility, and act as a powerful tailwind for the stock.

Technical Setup Highlights:

Recent buy signals triggered

Momentum Ghost Machine shows increasing bullish pressure

BBSR extreme close values support a continuation of the uptrend

Add it to your watchlist and let’s see how this plays out!

How to identify a Buy Side Dark Pool Platform Trend.Contrary to popular opinion. Dark Pools do rarely move price in huge runs up or down. The Giant Buy Side Institutions use ATS Venues called "Dark Pools of Liquidity" to ensure that they can control their price to the penny or half penny spread. You need to learn how to read the a stock chart as easily as reading a book. Buy Side Institutions price on daily charts will usually be very small candles. Some candles will be white, some will be doji's and some will be black. A black candle in a platform is not a sell short signal.

Platforms are a narrow price range that has consistent highs and lows that you can draw a rectangle around. Typically a Platform has a very stable price action but the candles are very small and compact. This is the Buy Zone that Dark Pools create that can last 1 -3 months depending on the reason for the Buy Side Institutions accumulation. IF it is for an ETF development, then the accumulation will be faster a month or less. If the accumulation is due to the expectation that the company is going to have a strong earnings report, then the platform will tend to be 3 months in duration before HFTs gap and run the stock up on earnings news. Platforms are an important sideways trend that you need to be able to easily identify so that you can enter the stock before the earnings release and HFT gap up.

The Platform is a trend that takes some study to be able to see but the time is worth it because often the gaps out of a platform can be huge OR there is a strong momentum run or velocity run that nets high profits with low risk.

APP (4H) | Runway to $500+ if AI & Flow HoldAPP (AppLovin) — AI & Smart Money Bust Open Path to $500–$517

Body Text:

AppLovin appears primed for another leg higher—AI models, technical structure, and institutional flow all aligning bullish:

⮕ AI Forecast targets $497.93 (30-day) — logical first major resistance zone. Thru there, $512–$517 opens up as next supply/pumping zone.

⮕ Call sweeps at $462–$470 (Aug 29) show serious bullish wagers in motion.

⮕ Chart Structure: Reclaiming $428–$430 pivot (former supply now support). Cleanup through $473–$480 resistance could clear the way to $500+.

⮕ Fundamentals & Sentiment: Stellar Q2 beat and guidance raise; IBD comp rating now elite at 98; continued analyst upgrades and S&P inclusion talk add fuel.

Probabilistic Targets:

Base Case (~40%): Target zone $490–$500 — aligns with AI and near-term supply breakout.

Extended (~20%): Run to $512–$517 if momentum sustains and broader market holds.

Failure (~40%): Rejection below $428 pivot could re-test $400–$405 demand.

Trade Setup

Entry: $442

Stop-Loss: Ideally $430–$435 (under pivot)

Convert into scale-out or trailing above $497–$500

This is AI + Flow + Structure convergence — textbook and high-probability asymmetric setup.

#APP #TradingView #AITrading #OptionsFlow #BreakoutSetup #AppLovin #TechnicalAnalysis

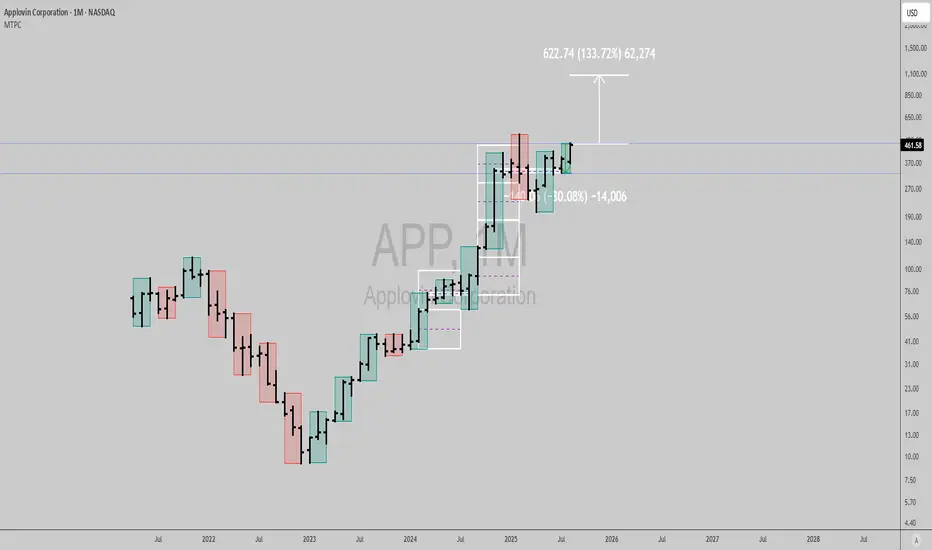

$APP: Strong technical signal with bullish fundamentalsAppLovin ( NASDAQ:APP ) stands out as a compelling growth story driven by its AI-powered AXON platform, which has transformed the company into a high-margin leader in digital advertising technology.

With robust revenue growth of 43% in 2024 and analyst projections of nearly 90% earnings growth in 2025, APP demonstrates the strong quarterly and annual growth that growth investors would find appealing.

The company’s innovation, leadership position in a rapidly expanding market, and strong institutional sponsorship further support the bullish outlook.

Technically, APP has broken out of a favorable Time@mode pattern, the proprietary trend-following system I use (coined by @timwest here), which projects an impressive 133% rally over the next seven months - an upside well above consensus analyst targets.

This blend of fundamental strength, market leadership, positive institutional demand, and confirmed technical momentum creates an attractive setup for significant stock appreciation in the near to medium term.

Best of luck!

Cheers,

Ivan Labrie.

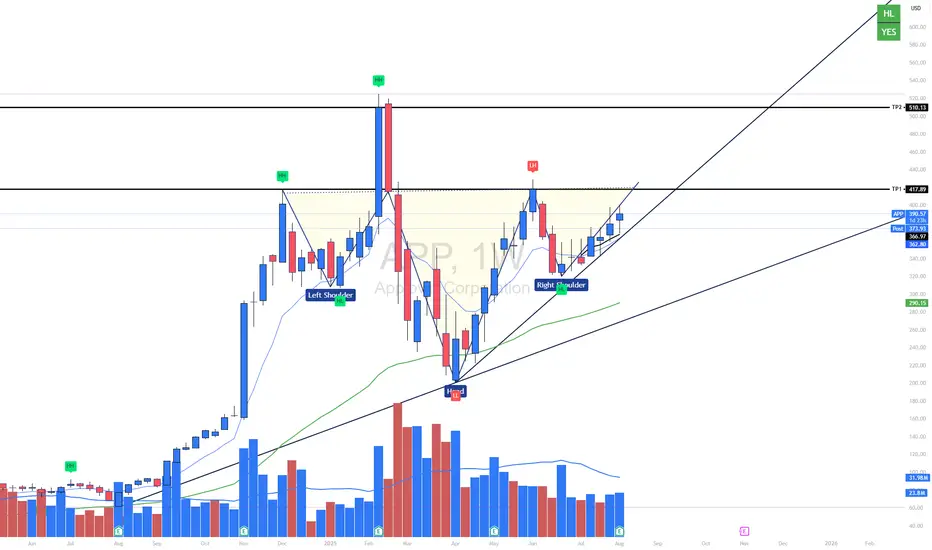

Bullish | APPNASDAQ:APP

Weekly Chart | Swing and Position Setup

APP is forming a textbook inverse head and shoulders pattern, signaling a major bullish reversal on the weekly timeframe.

Structure Highlights:

Left Shoulder – Head – Right Shoulder confirmed

Neckline breakout with change of character (ChoCH)

Price is trending above all key moving averages (EMA 9, EMA 50, VWAP)

Bullish volume behavior: expansion on rallies, contraction on pullbacks

Key Levels:

TP1: 417.89 (neckline resistance)

TP2: 510.13 (measured move target)

Final projection: 600+ if macro conditions align

Invalidation Level: Weekly close below 345

Thesis:

As long as the neckline holds, the bullish momentum remains valid. The structure is clean, technical confluence is strong, and volume confirms accumulation. This setup favors swing traders and position holders looking for high reward-to-risk entries.

APP Earnings Triangle BreakoutWith APP breaking key resistance to the upside. There is a possibility for an aggressive move to the upside. This will NOT be a straight line up, but does show the possibility of the measured move. If I were to enter this, todays candle would be my entry and my stop loss would be an aggressive close back under the trendline.

Let's see what happens.

Buy Idea APP (Applovin Corp)Entry: $371 - 372

Stop: $342.50

Risk per share: $28.80

Earnings Catalyst Setup

• Flat base breakout above $370 zone, strong price structure

• Volume expanding into earnings — ideal for pre-earnings momentum pop

• Holding all major MAs: 21EMA, 50MA, 200MA clustered below

• MACD & Oscillators turning up, showing early momentum shift

• Institutional positioning appears supportive

• Earnings Date: ~9 days (6 Aug 2025 after mkt)

⚠️ Key Notes

• Pre-earnings breakout pattern, keep size light

• Possible re-rating if earnings surprise positively — watch for revenue growth in AI/game ads

• Sell partial above 1R to de-risk, trail rest

DISCLAIMER : The content and materials featured are for your information and education only and are not attended to address your particular personal requirements. The information does not constitute financial advice or recommendation and should not be considered as such. Risk Management is Your Shield! Always prioritise risk management. It’s your best defence against losses.

BofA note: : Excellent setup w/catalysts from mobile gaming & adConfirmation of self-serve launch would put story on track: APP remains top pick under coverage. We see big upside to CY26 EBITDA expectations, with this print potentially prompting upward revisions; the vast majority of investors we spoke with appear to exclude both a continued managed service onboarding ramp, and a major self-serve ramp in CY26. This quarter, management has the opportunity to

(1) confirm the launch timing of APP’s eCommerce self-serve platform for small advertisers,

and

(2) indicate the resumption of onboarding of larger merchants to its managed service. About one third of investors we spoke with expect the self-serve platform to launch this Fall, and ~40% expect a launch during the holiday shopping season. Despite this, expectations of Q3/Q2 growth appear too conservative; APP’s managed service would resume onboarding well before self-serve launches.

Mobile game ads could drive big Q2 expectations beat: Based on client conversations, 2Q25 Advertising Revenue expectations are above guidance of $1.20Bn (+4%-5% Q/Q as usual), but in line with BofA’s $1.26Bn (+9% Q/Q). Few investors we spoke with assumed a performance break-through (eg “model enhancement”) in Q2, but virtually all are above guidance. Mobile game engagement and ad load continued to trend upwards in Q2, giving our model some fundamental support. We assume flattish Q/Q eCommerce revenue, although a first cohort managed service advertisers is known to have tested APP’s new AI dashboard. We removed APP’s 1P games segment from our consolidated model as APP will report it in discontinued operations from Q2 onwards; we estimate an incremental $30mn of Advertising net revenue contribution from

divested 1P studios in Q3 onwards.

Q3 & CY25 expectations likely too conservative: Few investors we spoke with appear to assume a Q3 (1) a model enhancement or (2) an eCommerce managed service ramp, putting BofA’s $1.42bn well above the vast majority of clients. The likelihood of a model enhancement rises with each passing quarter, making upward revisions likely post print. We change CY25 Revenue/EBITDA forecast to $5.8bn/$4.5bn from $6.2bn/$4.6bn to reflect the divestiture of APP’s 1P games segment in Q2.