PLTR eyes on $212.12: Golden Genesis fib could mark a TOP PLTR has been slowing its ascent before earnings.

About to test a Golden Genesis fib at $212.12

Reaction here will give clues about its strength.

It is PROBABLE that we orbit this fib a few times.

It is POSSIBLE a Break-n-Retest continues uptrend.

It is PLAUSIBLE that we have topped for a while.

.

See "Related Publications" for previous plots such as this BOTTOM CALL:

Hit BOOST and FOLLOW for more such PRECISE and TIMELY charts.

========================================================

Trade ideas

PLTR Charging Into a Breakout — Key Levels for Nov. 3–7 🚀Weekly Structure (Macro Bias)

Market Structure:

PLTR continues to print clean BOS pushes on the weekly. The trend has respected a rising channel for over a year, and we just saw another rotation from discount back into premium. Smart money is clearly comfortable accumulating on pullbacks into the mid-trend grey zone you marked. The last CHoCH failed to meaningfully break trend — buyers defended instantly.

Liquidity:

You can see them running liquidity above prior weekly highs, then stabilizing rather than rejecting — bullish tell. Until that pattern changes, continuation is favored.

Trend Direction:

Strong bullish trend, higher highs and higher lows, no weekly displacement against structure.

Supply & Demand:

* Demand: 170–188 zone (previous consolidation, order block stack)

* Deeper Demand: 142–150 (weekly value)

* Supply: 204–210 is the next magnet zone; any wick here needs to be watched for absorption.

This week, bulls will try to hold price above 190–188 to maintain momentum.

Indicator Confluence:

* 9EMA > 21EMA and widening — momentum is accelerating, not fading.

* MACD histogram expanding positive again; slope is curling up.

* Stoch RSI rising, supporting continuation.

* Volume uptick on expansion candles — institutions weren’t shy adding.

Daily Structure (Swing Bias)

Market Structure:

The daily trendline shows a clean breakout retest behavior. Last week’s hesitation was simply liquidity engineering around 190. Friday’s candle took initiative — that’s conviction.

Key Levels:

* Support: 190 → 188

* Deeper support: 177

* Resistance: 200.50 → 204.20 next

As long as we stay above that trendline retest zone, the structure remains dominantly bullish.

Order Blocks & Liquidity:

There’s a clear bullish order block around 185–188. Expect bids there if any dip happens.

Smart money loves to nudge price back into OB, shake mid-leveraged longs, then rotate upward.

Indicators:

* 9/21 EMA steepening — strong continuation behavior.

* MACD reversing from a shallow pullback, histogram turning positive.

* Stoch RSI loaded near top, but PLTR is known for grinding in overbought conditions.

* Volume printed healthy displacement candles — confidence, not exhaustion.

15-Minute Structure (Intraday Rotation)

Market Structure:

You saw BOS early, followed by a modest CHoCH reclaim. That bounce back into the 200 level and lateral consolidation is bullish digestion, not a breakdown.

We’re holding a small intraday order block below price around 198 — that’s your first buffer.

Liquidity:

There’s still clean liquidity at 204 waiting to be tapped. If the open sees a minor dip and reclaim, scalp longs become high-probability.

Indicators:

* MACD curling positive, histogram building accumulation.

* Stoch RSI cycling from reset, ready for another push.

Intraday momentum is bullish unless 197 breaks decisively.

1-Hour GEX Map (Options Sentiment & Dealer Behavior)

Gamma Walls (Call-Side Barriers):

* 205

* 207.50

* 212 zone

* 220–225 (extension targets)

Dealers hedge long gamma by pinning price between these walls if flows slow — but if net call momentum increases, it ignites upside squeezes.

Put Support:

* Heavy support at 182.50–180

* A secondary support zone at 175

Below 180, volatility would expand hard — but flow doesn’t support that path yet.

Max Pain Behavior:

Gamma map suggests upward bias with magnets sitting above current price. Dealers are not incentivized to trend PLTR downward this week.

Trade Scenarios

Bullish Setup

Condition: Hold above 197–198 on any morning pullback

Entry: Reclaim of 200.50

Targets: 204 → 207.50 → 212

Stop: 196.50

Invalidation: Full candle close below trendline (approx 188 on daily)

Notes: Liquidity grab at 198 then push is classic.

Bearish Setup (Counter-Trend Only)

Condition: Strong rejection w/ heavy selling wick at 204–207

Entry: Breakdown of 197

Targets: 193 → 188

Stop: 199.25

Invalidation: Reclaim of 200

Only take this if SPY/NQ also roll over.

What to Watch This Week

* Look for false breakouts above 204 — that wick behavior matters.

* If 200 holds as support on retest, bulls gain serious fuel.

* Liquidity above 207.50 could spark a Friday squeeze.

If bulls defend 198 with confidence, I’m leaning toward continuation into mid-premium pricing.

Closing Outlook

This week favors continuation, but PLTR may dance sideways early to burn premium. Watch volume footprint — if buyers show initiative at 200, momentum traders will pile in.

Personal Note:

If the market gives us a clean reclaim at 200.50 and volume confirms, that’s the kind of setup institutions love to run into key gamma walls. I’m watching liquidity traps around 204 — that’s where the real game is.

Disclaimer

This analysis is for educational purposes only and not financial advice. Always manage risk and trade your plan.

Palantir is nowhere NEAR DONE - I see $255 soon. "AI's Exponential Dawn: Why Burry's Bears Are -ERRONEOUSLY- Shorting the Future of 7.8 Billion Lives"

November 5, 2025

AI's Exponential Dawn: Why Bears Like Burry Are Betting Against the Future of 7.8 Billion Civilization.

Amid growing concerns of a market peak, skeptics are increasingly targeting the cornerstone of tomorrow's economic expansion: artificial intelligence. Yet, as I've emphasized, AI stands as the unassailable pillar driving a profound transformation in infrastructure capacity and construction—much of it already financed and underway. This restructuring of industrial organization is not merely national or regional; it is profoundly global, dwarfing any prior industrial cycle in scope and ambition. For the first time in world history, this cycle will encompass 7.8 billion people across more than 150 countries, weaving AI into the fabric of economies from Silicon Valley to Shenzhen and beyond.

It would be both short sighted and unconscionable to permit a cadre of short-sellers to undermine this momentum.I view figures like Michael Burry and his cohort as mere irritants—a fly in the ointment—against the backdrop of the Trump administration's vested interest, with trillions upon trillions at stake. Their resources dwarf anything Burry could marshal, ensuring AI's inexorable advance.Take Palantir (PLTR): Its elevated forward P/E ratio belies the unparalleled optimization efficiencies its platform will deliver, a factor markets have yet to fully price in. To illuminate this, let's quantify the sector's explosive growth and reverse-engineer future revenues for PLTR, NVIDIA (NVDA), and the broader AI ecosystem. What emerges is not speculation, but a structural imperative.Quantifying the Global Scale: 7.8 Billion People, 150+ Countries, and Trillion-Dollar Trade FlowsTo dissect this unprecedented engagement, consider the AI ecosystem's projected footprint: By 2030, the global AI market will swell to $4.8 trillion (a 25-fold surge from $189 billion in 2023, per UNCTAD), directly fueling $19.9 trillion in cumulative economic value (IDC).

This isn't siloed innovation—it's a trade engine reorienting supply chains, semiconductors, and software exports across borders, with AI-related goods and services comprising up to 10% of global merchandise trade by decade's end (WTO World Trade Report 2025).

Engagement spans demographics and geographies: AI tools will reach 729 million direct users by 2030 (up from 116 million in 2020, Bureau Works), but indirect touchpoints—via productivity boosts, job transformations, and embedded applications—will permeate 40-50% of the global workforce, affecting over 3 billion people (IMF estimates). In 150+ countries (spanning Anthropic's Claude. ai adoption data), legislative AI mentions have surged ninefold since 2016 (Stanford AI Index 2025), signaling policy alignment from G7 hubs to emerging BRICS economies. Here's a regional breakdown of projected 2030 impacts, highlighting GDP uplift, population exposure, and AI-driven trade activity (synthesized from McKinsey, PwC, and UNCTAD models; assumes 29% CAGR for AI market):

North America: Population Covered: 0.6B (% of Global Pop.: 8%); Projected GDP Uplift: $3.5T; AI Trade Volume Est.: $1,200B; Key Drivers: Innovation hubs; 14.5% GDP boost (ETA); chip exports dominate.

Europe: Population Covered: 0.7B (% of Global Pop.: 9%); Projected GDP Uplift: $2.8T; AI Trade Volume Est.: $900B; Key Drivers: Regulatory frameworks; software/services trade surges 20% YoY.

Asia-Pacific: Population Covered: 4.7B (% of Global Pop.: 60%); Projected GDP Uplift: $7.2T; AI Trade Volume Est.: $1,800B; Key Drivers: Manufacturing scale (China/India); 50% of global AI hardware trade.

Latin America & Africa: Population Covered: 1.8B (% of Global Pop.: 23%); Projected GDP Uplift: $3.0T; AI Trade Volume Est.: $600B; Key Drivers: Leapfrog adoption; emerging data center investments double trade flows.

Middle East & Others: Population Covered: 0.0B (residual, % of Global Pop.: <1%); Projected GDP Uplift: $0.4T; AI Trade Volume Est.: $300B; Key Drivers: Energy-AI nexus; sovereign funds fuel cross-border deals.

Global Total: Population Covered: 7.8B (% of Global Pop.: 100%); Projected GDP Uplift: $16.9T; AI Trade Volume Est.: $4,800B; Key Drivers: $15.7T cumulative GDP add (PwC); $4.60 ROI per $1 AI spend (IDC).

This matrix underscores the trade multiplier: Every $1 billion in AI infrastructure spend generates $4-5 billion in downstream commerce—semiconductors from Taiwan to hyperscalers in the U.S., optimization platforms like PLTR streamlining ops in 100+ countries, and NVDA's GPUs powering clusters from São Paulo to Seoul. Developing nations risk commoditization without adoption (World Bank), but with $670 billion in annual data center capex by 2025 scaling to $1.67 trillion (McKinsey), the flywheel accelerates inclusive growth.

In sum, this isn't a cycle—it's a paradigm, with AI trade volumes rivaling oil today and touching every citizen through enhanced efficiencies. Markets undervalue this universality; forward thinkers will capitalize.

Projecting Revenue Gains from AI Adopters:

Real-World Transformations in Logistics, Fraud Detection, and Autonomous MobilityBuilding on our exploration of AI's global paradigm shift, let's zoom in on tangible revenue uplift for early adopters. These aren't hypotheticals—AI delivers measurable efficiencies that cascade into bottom-line gains, often 20-50%+ in targeted verticals. We'll dissect three pillars: logistics optimization, fraud detection (spotlighting American Express's playbook), and electric autonomous mobility (with Tesla Semi as the benchmark). Projections draw from industry benchmarks, assuming 2025-2030 adoption ramps at 20-40% CAGR, turning cost savings into revenue via pricing power, volume growth, and margin expansion.1. Logistics Efficiency: Unlocking $1T+ in Global Supply Chain ValueAI streamlines routing, inventory, and predictive maintenance, slashing operational costs by 15-25% while boosting delivery speeds 20-30%—translating to 8-15% revenue gains through customer retention and premium services. For a mid-tier logistics firm (e.g., $10B annual revenue like DHL subsets), this means:

2025 Projection: $800M-$1.2B uplift from AI-driven demand forecasting (reducing stockouts by 40%) and autonomous robots cutting warehouse labor 30%.

2030 Cumulative: $5-7B per adopter, as the $306B AI logistics market (42% CAGR) fuels ecosystem trade—e.g., PLTR's AIP optimizing routes for 121% U.S. commercial growth. Net: Adopters like UPS could see EBITDA margins swell 5-7 pts, compounding to 50%+ revenue equivalence over five years.

2. Fraud Detection: American Express's Margin-Doubling MasterclassAI's real-time anomaly detection has revolutionized payments, with false positives down 45-60% and fraud losses curbed 20-38%—directly inflating margins without headcount hikes. Amex exemplifies: Their ML models (deployed since 2014) boosted fraud resolution 100%, maintaining industry-lowest rates for 14 years and enabling 60% fraud reduction—effectively doubling profit margins (ex-expansion) via reclaimed revenue and lower provisions ($1-2B annual savings on $60B+ charge volume).

2025 Projection: For a $50B fintech (e.g., Visa peers), 50% fraud drop yields $500M-$1B margin boost, equating to 10-20% revenue proxy via trust-driven card spend.

2030 Cumulative: $10-15B per major player, as AI fraud tools scale to $50B market subset—PLTR's ontology-driven detection could amplify this 2x for enterprise clients. This isn't cost-cutting; it's revenue alchemy—fraud savings recycle into growth investments.

3. Electric Autonomous Mobility: Tesla Semi's $200K+/Truck Savings FlywheelAutonomous electric semis (e.g., Tesla's) merge 70-84% fuel savings with 90%+ labor reductions, retrofitting special lanes for driverless ops unlocking 20-30% fleet utilization gains. Baseline: Diesel semis cost $0.45/mile (fuel + driver ~$0.20 each); Tesla Semi drops to $0.13/mile electric + scaled labor.

Fuel (10% Base + Efficiency): 70% cut yields $0.03/mile savings (conservative; real 84% = $0.04+). For 100k miles/year/truck: $3k-$4k annual gain.

Driver (1 per 10 Trucks): $50k avg. U.S. salary = $5k/truck/year savings; full autonomous (lanes retrofitted) = $50k/truck elimination.

2025 Projection: Per fleet of 100 Teslas: $800k fuel + $500k labor = $1.3M total (~$13k/truck), or 20% revenue uplift via lower rates/higher loads—$200k/truck over 3 years per Tesla claims.

2030 Cumulative: $50-70M for 500-truck operator (18% fuel cut industry-wide for AVs), scaling to $500B global trucking savings as NVDA-powered autonomy proliferates. Special lanes (e.g., U.S. interstate pilots) could double this by enabling 24/7 driverless runs, turning capex into 40%+ margin expansion.

Across these, adopters capture 15-30% revenue equivalence from AI efficiencies, compounding the $16.9T global GDP uplift we charted. PLTR and NVDA aren't just enablers—they're the multipliers. Skeptics, take note: This is adoption economics at warp speed.

In Closing:

Exponential Revenues Unfolding Now, Fueling Enterprise Transformation

Article content

These projected revenues are not distant mirages but colossal forces accruing in real time—AI's software essence ensures exponential compounding, with adoption accelerating across enterprises, governments, and infrastructures today. From Palantir's AIP platform already powering 500+ deals in Q3 2025 to NVIDIA's Blackwell GPUs shipping at scale amid $670B data center capex this year, the flywheel spins at warp speed. Markets may undervalue the immediacy, but for corporate leaders, this signals a profound operational shift:

Software like Palantir's isn't just a tool—it's the accelerator for your own revenue trajectories, embedding intelligence into every workflow for immediate, scalable gains.Consider Palantir as a prime example of this software-driven momentum. As a pure-play AI optimization platform, its revenue trajectory exemplifies the rapid mushrooming potential available to adopters.

Drawing from the last three quarters (Q1 FY2025: $880M; Q2: $1,004M; Q3: $1,180M), we've seen sequential growth accelerating from 14% to 17.5%—a clear sign of exponential uptake in commercial and government segments. Projecting forward at an averaged 15.8% quarter-over-quarter growth (conservative, given the upward trend and software's low marginal costs), here's the quarter-by-quarter outlook for the next five:

Q4 FY2025 (Oct-Dec 2025): $1,366M (+16% QoQ) – Early signs of tripling annualized run-rate from Q1 levels, as AIP bootcamps convert pilots to full deployments overnight.

Q1 FY2026 (Jan-Mar 2026): $1,582M (+16% QoQ) – U.S. commercial surges could push this 80%+ YoY, mirroring the 121% Q3 clip.

Q2 FY2026 (Apr-Jun 2026): $1,832M (+16% QoQ) – Global enterprise wins stack, with software scalability enabling 50%+ margins on new logos.

Q3 FY2026 (Jul-Sep 2026): $2,121M (+16% QoQ) – Cross-border optimization deals proliferate, potentially doubling from Q3 2025.

Q4 FY2026 (Oct-Dec 2026): $2,456M (+16% QoQ) – Cumulative FY2026 could exceed $9B, a near-tripling from FY2025's $4.4B guide, underscoring software's viral adoption curve.

This isn't linear scaling—it's software at work: Zero-capex marginal revenue from each new user, compounding efficiencies in logistics, fraud prevention, and beyond. Imagine applying similar velocity to your P&L: A 16% QoQ lift in your core ops could mean double-digit revenue mushrooms within a year, all without proportional headcount bloat. Enter Michael Burry: Yet another fool wagering unethically against humanity's most transformative industrial process to date—a global reconfiguration touching 7.8 billion souls. History will judge such shorts not as visionaries, but as footnotes in progress.

The imperative for managers ? Pilot AI software now—before competitors claim the edge.

#AI #DigitalTransformation #EnterpriseTech #Leadership

PLTR No wonder why that man bought puts rsi is over 95 in the monthly . Scam needs a retrace before going higher . Also everything is showing bulls losing momentum I think the market will retrace here for the coming days . Just a thought

PLTR: potential mid-term top formation Price have reached key mid-term resistance zone outlined in May idea:

As long as price remains below the Nov 3 highs, I’ll be operating under the main assumption that the mid-term top is in, anticipating more downside in the coming weeks and months.

A 1–3 day bounce to potentially close the gap could provide a good delayed-reaction short setup.

Chart:

Macro support ideal for this correction: 120–85.

Macro view:

PLTR: Potential for Further Upside in H2 2025Price is showing a constructive, low-volume pullback into rising EMAs - a healthy sign within an ongoing uptrend as long as price is holding above 118-110 support zone.

Daily trend structure:

Macro trend structure (Weekly):

Thank you for your attention and I wish you successful trading decisions!

SHORTS WINNING TODAY (ʘ‿ʘ)Michael Burry is once again betting against the market. For Nvidia, he bought puts covering about 1 million shares worth approximately $187 million. For Palantir the exposure is puts on roughly 5 million shares valued at about $912 million

Palantir, which has gained over 170% this year, but is currently down 8.8% on Tuesday after its latest quarterly results (which were good) were eclipsed by Burry and a general risk-off shift in the market. Palantir CEO, Alex Karp has called Burry out for market manipulation even though most analysts might call Palantir “overvalued”.

In crypto markets, Bitcoin has been hovering near the key $100,000 level, a price it hasn’t dropped below since June 23. If it breaks lower, traders could be watching $98,240 and then $96,975 as the next major support levels.

Ether tumbled as much as 9% on Monday, breaking below the $3,600 support after hackers stole more than $100 million from a major DeFi protocol. The decline leaves Ethereum about 25% below its August peak of $4,885.

$PLTR weekly close above $200 before earnings#PLTR has been on a storming run this year. As I tell students - never fight a strong trend - you just need to find a way to surf it. Nevertheless, I had become concerned the last few weeks that perhaps it was overheating; we'd gone parabolic; followed by creating a double top; which then printed bearish key reversals and rejection candles. I wasn't short (don't fight a good trend), but it was on my watch list. I thought we may drift lower into earnings. Well, I was clearly wrong in my concerns, when price blasted higher last week, and also closed about $200 the week before earnings.

Can we turn $200 in a base before a move higher?

Palantir (NASDAQ: $PLTR) Set For Breakout Amidst Earnings ReportPalantir (NASDAQ: NASDAQ:PLTR ) is set for a bullish spike as earnings reports are slated for tomorrow November 3rd, 2025. With the last trading session ending with NASDAQ:PLTR up 5.93% investors are keen on driving the share price to $250 amidst a positive earnings bead.

Adding to the bullish sentiment, the RSI is at 60, implying that NASDAQ:PLTR is well validated for a bullish move tomorrow before or after earnings beat.

On a different note, should the asset fail to report a favourable news, the 38.2% Fib level is well articulated for a support zone for $PLTR.

About Palantir

Palantir Technologies Inc. builds and deploys software platforms for the intelligence community to assist in counterterrorism investigations and operations in the United States, the United Kingdom, and internationally. It provides Palantir Gotham, a software platform, which enables users to identify patterns hidden deep within datasets, ranging from signals intelligence sources to reports from confidential informants, as well as facilitates the hand-off between analysts and operational users.

Palantir (PLTR) Bulls Preparing for Takeoff — Setup Explained💎 PALANTIR TECHNOLOGIES INC. (PLTR) — Swing Trade Profit Playbook 💎

Exchange: NASDAQ

Style: Swing Trade | Thief Layering Strategy | Bullish Pullback Setup

🧭 PLAN

We’re plotting a bullish pullback setup confirmed by the Hull Moving Average and a Heikin Ashi reversal doji — signaling that buyers are regaining strength and getting ready to dominate again. 💪📊

This setup thrives when the crowd is sleeping — that’s when the thief plans the perfect entry on discount zones! 🕶️💸

🎯 ENTRY STRATEGY — “THIEF LAYERING SYSTEM”

Instead of chasing green candles, this strategy stacks multiple buy limit layers to build position quietly and efficiently. Each layer grabs value from dip zones — just like a thief collecting gold coins on the way down! 🏴☠️💰

Layered Entry Plan:

🔹 1st Layer: $175 — early scout entry, feel the market reaction.

🔹 2nd Layer: $180 — main position loading zone near Hull MA support.

🔹 3rd Layer: $185 — continuation confirmation layer if trend holds.

🔹 4th Layer: $190 — momentum add-on for breakout confirmation.

👉 You can add more layers if volatility gives deeper discounts. Adjust according to your risk profile — precision is key, greed is optional! 🎯

🛑 STOP LOSS

This is the Thief SL at $165 — clean, disciplined, and below the recent structural support.

⚠️ Note to all Thief OG’s: This isn’t a fixed stop for everyone. Manage your own risk — move smart, stay stealthy. Every thief has their own escape route! 🏃♂️💨

💰 TARGET / TAKE PROFIT

Our main target is $220, where the “police force” (strong resistance) is waiting to trap late buyers. That’s our signal to escape with profits while the market gets noisy. 🚨💵

⚠️ Note: Don’t copy-paste my TP — adjust it based on your risk-reward ratio. The thief gets in, takes the bag, and disappears like smoke! 😎💨

🌐 CORRELATIONS & RELATED PAIRS TO WATCH

While executing this PLTR play, keep an eye on related movers:

💡 NYSE:AI (C3.ai): another AI data stock — often mirrors PLTR’s momentum.

⚙️ NASDAQ:NVDA (NVIDIA): strong leader in AI space; when NVDA rallies, PLTR usually follows.

📊 NASDAQ:QQQ (NASDAQ ETF): overall tech sentiment indicator — if QQQ pulls back, expect PLTR sympathy moves.

🧠 NASDAQ:META , NASDAQ:GOOG : big-data and AI-driven plays that set tone for broader sector trends.

Key Insight: When NASDAQ:QQQ or NASDAQ:NVDA show continuation strength, PLTR tends to respond aggressively due to its higher volatility factor. A synchronized move could amplify this setup’s reward potential! 💥📈

⚙️ MARKET CONTEXT

Palantir continues to benefit from the AI and defense analytics boom, showing stronger fundamentals and recurring government contracts. The chart recently cooled off, forming a healthy reaccumulation base, ideal for swing traders planning layered re-entries before the next push to $220+. ⚔️📊

🕶️ DISCLAIMER (READ BEFORE HEISTING)

This is a Thief-Style Trading Strategy — meant for fun and education.

Trade smart, manage your capital, and always protect your loot! 🧠💼

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

#PLTR #Palantir #SwingTrade #ThiefStrategy #StockMarket #AI #BullishSetup #TechnicalAnalysis #HullMA #HeikinAshi #RiskManagement #NASDAQ #ProfitPlaybook

PALANTIR PLUS GOLD. 21 MONTHS OF ULTIMATE SHAG-ALL-BEARS SUCCESSSomewhere far far ago.. in the Faraway Kingdom, or maybe even in the Thirties Land... (in brief - "somewhere in another Galaxy"),

...in late December, 2024 (yet in era of 'altseason-2024' expectations),

..@TradingView has asked somewhat at it awesome Giveaway: Happy Holidays & Merry Christmas.

1️⃣ What was your best trade this year?

2️⃣ What is your trading goal for 2025?

Here's what we answered:

1️⃣ What was your best trade this year?

- Surely Palantir NASDAQ:PLTR 💖

2️⃣ What is your trading goal for 2025?

- Once again, surely Palantir NASDAQ:PLTR 💖

It's gone twelve months or so... (Duh..? Ahah.. 12 months really? 😸).

What's happened since that:

📌 Trump definitely failed to become 'Crypto Tsar';

📌 America failed to become 'Crypto Capital of the World',

📌 America still is not 'Great Again' (but definitely goes 'Nuclear');

📌 Crypto future does not shine bright any further (well, in this given time, over Top-200 crypto tokens nearly 75% are down now in the year 2025).

In the midst of all this crap, we have been focused all the year 2025 on two things only.

- Know what?

- For sure, they both are defensive assets. These are - Palantir and Gold.

Reducing a portfolio to just two assets Palantir and Gold is very reasonable for several strategic and performance-driven reasons.

This streamlined approach offers unique benefits based on recent returns, diversification, and macroeconomic context, especially during periods of high volatility and inflation.

Rationale for a Two-Stock Portfolio

A portfolio concentrated in Palantir and Gold capitalizes on the complementary strengths of both assets.

Palantir, as a rapidly volatility and growing tech company specializing in AI and big data analytics, provides exposure to high-growth technology, while Gold acts as a timeless stability hedge against economic uncertainty, inflation, and market stress.

The reduction to two assets simplifies management, decreases transaction costs, and focuses allocation on assets with contrasting properties, growth technology and defensive commodity.

Volatility plus Stability. Two wise words to explain it all.

Diversification benefits

Although minimal, the combination exploits Gold’s low to negative correlation with equities during turmoil. Gold typically rises in market distress, offsetting potential losses in stocks.

Focused conviction investing. Belief in Palantir’s disruptive business and the ongoing value of gold can justify concentrated exposure, especially if robust research supports the thesis.

Risk management through asset characteristics. Gold’s stability and history as a store of value counterbalance Palantir’s volatility and growth-driven risk.

Optimal drawdown protection and inflation defense. Gold historically has protected investor portfolios during crises, high inflation, and periods where traditional diversification fails.

Ultimate Recent Returns

Recent performance underscores the appeal:

Palantir: As of the end of October 2025, Palantir stock reached an all-time high of $204.16, showing a remarkable climb from a year low of $41.03, an almost fivefold increase within twelve months. Year-to-date, the stock is up over 160%, exemplifying the company’s explosive growth phase powered by surging enterprise adoption of AI.

Gold: Spot gold is trading at nearly $4020 per ounce, i.e. up by almost 47% compared to this time last year, and up 27% YTD as of July.

Gold has delivered an annualized average return of about 10.9% over the last 25 years, but its resilience during crisis years (like 2025’s inflation surge) makes it especially attractive now.

Economic Context and Defensive Logic

In the current environment, marked by inflation spikes and geopolitical risks, a two-asset allocation underscores defensive logic.

Market stress resistance. Gold provides protection when equities falter and can cushion overall volatility.

Participation in accelerating digital transformation. Palantir leverages global data partnerships and AI innovation, promising outsized returns as enterprises and governments digitize operations.

Drawdown and inflation protection. When stock-bond correlations break down—as witnessed during stagflation and recent crises, Gold’s unique properties shine, ensuring resilience.

This strategic portfolio reduction is still reasonable.

Investors with high conviction in technology and commodities.

Those seeking clarity, simplicity, and rapid decision-making.

Defending against volatility, inflation, and uncertain macro trends.

Portfolio managers less reliant on traditional broad diversification.

Summary

Portfolio restricted to Palantir and gold leverages their respective strengths

21 (Twenty One) consecutive rising months. Months of ultimate shag-all-bears success.

Try to find the same or even something similar... We bet you will not!

High-growth technology with outsized returns and defensive commodity protection.

Recent performance validates this concentrated approach, yielding stellar returns for both and a sensible hedge against future uncertainty.

--

Best wishes,

@PandorraResearch Team

PLTR: Earnings week!My thoughts on PLTR into earnings!

Hope you find it helpful, but as always not advice!

Safe trades everyone and enjoy your weekend!

S(t) = E f_t]

(new pretentious signature ;))

$PLTR The short of the year?Update NASDAQ:PLTR

I am still heavily short.

Palantir has spent all of 2025 inside a bull channel. I see bull channels as bear flags because they behave exactly the same.

Now we’ve broken the channel in the pre market and taken out a 5-touch support level. That’s a major structural failure.

Nothing is guaranteed in trading, but it’s hard to find a cleaner setup than this. Risk/reward is exceptional.

A Risk of Deeper Pullback in PLTRThe trend on daily/time-short frames is weak, momentum is bearish, the chart shows a likely distribution phase entering mark-down.

Its Longer term trend is still positive but fading.

I’d lean bearish to neutral in the near‐term with a risk of deeper pullback .

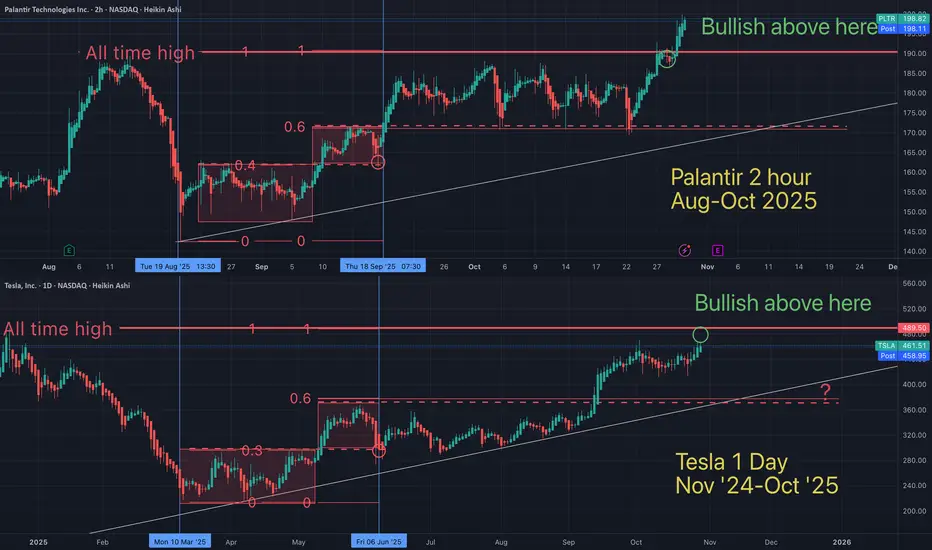

Tesla / Palantir FRACTAL - When will it endTodays 14% Palantir bounce was followed by Tesla...at the same time...in the same ratio.

Learn to spot patterns.

May the trends be with you.

Tesla / Palantir "fractal" - Why do fractals exist?Even when there is a "deviation" from the pattern, the overall agenda prevails. There's no stoping this moving train. Hopefully you're on board...and know when to get off.

May the trends be with you.

FRACTALS are like maps. This one is STILL working.On Oct 7th I suggested the Palantir / Tesla "fractal" would lead them both to an all time high. Fast forward to today (1 month later), Palantir has recently hit a new ATH and Tesla is still following the fractal closely. I believe Tesla is days or weeks away from an ATH.

Here was the 15min chart at that time:

Tesla will move very quickly in 3rd angle fashion, once it breaks ATH & holds support.

If the fractals continues at this pace, how soon do you think Tesla will HOLD SUPPORT above ATH?

$PLTR - $200 break for a move towards $220PLTR - Stock breaking all time as expected. Swing call added in the group. Stock looking strong here. calls above $200 looking good for more upside. Stock has nice pattern breakout on the daily.

A broader look at the Palantir / Tesla Fractal (Tesla ATH Next?)What do you think? Is Tesla primed for an all time high (soon)...and a blow off top?

May the trends be with you

Palantir is at dot-com levels of overvaluationTl;dr, Palantir is grossly overpriced against the general market, as well as against its own financial metrics from 4 years ago, and its valuation metrics put it in peak dot-com bubble territory.

Metrics

Palantir's current price puts it at a market cap of $467.35B. With expected $3.5B in annual revenues in 2025, the price/sales (PS) ratio is at ~147 . PS ratios are the financial metric to watch for growth stocks, since growth companies prioritize revenue growth.

A high PS ratio should mean that the market expects high revenue growth. While Palantir's revenue growth is pretty high, it's not as exceptional as the PS ratio would imply. It seems that the market is not only extrapolating the revenues to continue rising, but it's also extrapolating that the growth itself (or first derivative of revenues) is going to keep increasing for years sequentially. Palantir has to generate far higher annual growth than it currently has to come close to justifying this valuation, I'd expect at least 175% annually.

For reference, Nvidia traded at a PS ratio of 43 in mid 2023, and then generated 125% growth 2 years in a row. The PS ratio stayed relatively stable since then, and never went past 43. Important thing to note here is that Nvidia also has higher net profit margins than Palantir, and profit margins play a role in how PS is interpreted (since earnings is what really matters). Palantir's profit margins have been growing consistently, from 10% -> 16% -> 32% annually, but still not close to Nvidia's 50%. Further profit margin growth would help to justify the overvaluation.

Comparisons

As the chart shows, Palantir's annualized revenue growth last quarter is equivalent to its growth in 2021 at ~50%. Revenues since then increased by 170%. Palantir at the time traded at a PS of 37, which is pretty high for 50% growth, but not too crazy.

If the stock traded at the same PS ratio as in 2021, where its growth was the same, the stock would be trading at ~$53 today at a market cap of $120B.

A PS ratio of >100 implies extreme bubble levels. From what I've found, during the very peak of the dot-com bubble:

Yahoo! traded at PS 100

Amazon traded at ~50

Ask Jeeves traded at ~55

CMGI traded at >300

Internet Capital Group traded at >200

Webvan traded at ~150

With Palantir trading at a PS of 147, it's well within the peak dot-com levels of overvaluation. While the entire tech/AI market is currently at very high valuations, Palantir still towers far above them.

Some examples of other high growth stocks today:

Crowdstrike at PS 30

AppLovin at PS 41

ServiceNow at PS 16

Netflix at PS 11

Even with the stock screener I couldn't find a stock that came close to trading Palantir's PS ratio, except for Microstrategy (which has no revenues as a crypto holding company) and for moonshot pharma R&D stocks which also have little to no sales by design.

The point of this idea is to show how grossly and absurdly overpriced this stock is, but it's not a recommendation to take a short position. The stock is so far decoupled from reality that you should consider it as equivalent to a meme coin. The financials don't matter, and it's simply an asset with a limited supply that is in high demand, so the price keeps going up.

Palantir Is +160% YTD. What Its Chart Says Ahead of EarningsPalantir Technologies NASDAQ:PLTR will report Q3 results next week as the security-software firm is enjoying roughly 160% year-to-date gains that have pushed its stock to all-time highs. Let's see what its chart and fundamentals say.

Palantir's Fundamental Analysis

PLTR plans to release earnings after the closing bell on Monday, with the Street currently looking for $0.17 in adjusted earnings per share on about $1.1 billion of revenue. This would represent a 70% year-over-year gain in adjusted EPS, as well as more than 50% in y/y sales growth.

If those numbers prove true, then the sales growth would represent the steepest year-over-year revenue gains that Palantir has ever put to the tape for any quarter. They would also mark the eighth consecutive quarter of accelerating year-over-year sales growth vs. the quarter prior.

In fact, 20 of the 21 sell-side analysts that I can find that cover Palantir have revised their earnings estimates upward since quarter began. (One estimate remains unchanged.)

Palantir's Technical Analysis

Next, let's check out PLTR's chart going back some eight months and running through Monday afternoon:

It looked recently like Palantir was forming a double-top pattern of bearish reversal after the stock found support at a 38.2% Fibonacci retracement of its April-through-August rally (the dark-gray line and shaded area in the chart above).

But as the shares managed to base and consolidate near that second top, this threat might have passed.

However, by stretching out the second top over several weeks, PLTR has instead formed an ascending-triangle pattern of bullish continuation with a $188 indicated pivot. The stock has traded above that at record levels recently ($196.29 as of Tuesday afternoon) as PLTR tries to hold the pivot ahead of earnings.

Meanwhile, the swing crowd appeared over the past few weeks to play both sides of Palantir's 21-day Exponential Moving Average (or "EMA," marked with a green line). That said, portfolio managers appear to have defended PLTR when the stock tested its 50-day Simple Moving Average (or "SMA," marked with a blue line at $172 above).

At the same time, Palantir's Relative Strength Index (the gray line at the chart's top) has rebounded out of neutral territory and is getting more muscular without yet reaching a technically overbought state.

The stock's daily Moving Average Convergence Divergence indication (or "MACD," marked with black and gold lines and blue bars at the chart's bottom) is also notably improving.

For openers, the histogram of the 9-day EMA (the blue bars) has crossed back into positive territory. In addition, the 12-day EMA (the black line) has crossed above the 26-day EMA (the gold line), with both in positive territory. These are all short-to medium-term bullish signals.

An Options Option

Options investors projecting a moderate upside move and seeking to profit using leverage might employ what's known as a "bull-call spread" in this scenario.

That's where you buy one call and simultaneously sell another with the same expiration date, but a higher strike price. Here's an example using recent market prices:

-- Long one PLTR $192.50 call with a Nov. 7 expiration date (i.e. after next week's earnings) at $10.30.

-- Short one PLTR Nov. 7 $207.50 call at $5.

Net Debit: $5.30

This trader is risking $5.30 to try to receive up to $9.70 for a maximum profit at expiration of 183%. Meanwhile, the maximum potential loss at expiration is the $5.30 net debit.

An options trader willing to end up owning Palantir might also choose to sell a put in addition to the above strategy, which could provide the person with PLTR shares at a lower cost basis. Example:

-- Sell (write) one PLTR Nov. 7 $177.50 put for $5.50.

New net credit: $0.20

The trader has essentially paid for the bull-call spread above by risking the possibility of having to buy 100 shares of PLTR at $177.50 at expiration even if the shares are trading lower than that price.

This may serve to lower the net basis for the shares by offsetting the cost of the long call, but also adds the risk of significant losses, as the stock could theoretically fall to zero.

(Moomoo Technologies Inc. Markets Commentator Stephen "Sarge" Guilfoyle was long PLTR at the time of writing this column.)

This article discusses technical analysis, other approaches, including fundamental analysis, may offer very different views. The examples provided are for illustrative purposes only and are not intended to be reflective of the results you can expect to achieve. Specific security charts used are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Past investment performance does not indicate or guarantee future success. Returns will vary, and all investments carry risks, including loss of principal. This content is also not a research report and is not intended to serve as the basis for any investment decision. The information contained in this article does not purport to be a complete description of the securities, markets, or developments referred to in this material. Moomoo and its affiliates make no representation or warranty as to the article's adequacy, completeness, accuracy or timeliness for any particular purpose of the above content. Furthermore, there is no guarantee that any statements, estimates, price targets, opinions or forecasts provided herein will prove to be correct.

Options trading is risky and not appropriate for everyone. Read the Options Disclosure Document (j.moomoo.com) before trading. Options are complex and you may quickly lose the entire investment. Supporting docs for any claims will be furnished upon request.

Options trading subject to eligibility requirements. Strategies available will depend on options level approved.

Maximum potential loss and profit for options are calculated based on the single leg or an entire multi-leg trade remaining intact until expiration with no option contracts being exercised or assigned. These figures do not account for a portion of a multi-leg strategy being changed or removed or the trader assuming a short or long position in the underlying stock at or before expiration. Therefore, it is possible to lose more than the theoretical max loss of a strategy.

Moomoo is a financial information and trading app offered by Moomoo Technologies Inc. In the U.S., investment products and services on Moomoo are offered by Moomoo Financial Inc., Member FINRA/SIPC.

TradingView is an independent third party not affiliated with Moomoo Financial Inc., Moomoo Technologies Inc., or its affiliates. Moomoo Financial Inc. and its affiliates do not endorse, represent or warrant the completeness and accuracy of the data and information available on the TradingView platform and are not responsible for any services provided by the third-party platform.

Can Software Win Wars and Transform Commerce?Palantir Technologies has emerged as a dominant force in artificial intelligence, achieving explosive growth through its unique positioning at the intersection of national security and enterprise transformation. The company reported its first billion-dollar quarter with 48% year-over-year sales growth, driven by an unprecedented 93% surge in U.S. commercial revenue. This performance stems from Palantir's proprietary Ontology architecture, which solves the critical challenge of unifying disparate data sources across organizations, and its Artificial Intelligence Platform (AIP) that accelerates deployment through intensive bootcamp sessions. The company's technological moat is reinforced by strategic patent protections and a remarkable 94% Rule of 40 score, signaling exceptional operational efficiency.

Palantir's defense entrenchment provides a formidable competitive advantage and guaranteed revenue streams. The company secured a $618.9 million Army Vantage contract and deployed the Maven Smart System for the Marine Corps, positioning itself as essential infrastructure for the Pentagon's Combined Joint All-Domain Command and Control strategy. These systems enhance battlefield decision-making, with targeting officers processing 80 targets per hour versus 30 without the platform. Beyond U.S. forces, Palantir supports NATO operations, assists Ukraine, and partners with the UK Ministry of Defence, creating a global network of high-margin, long-term government contracts across democratic allies.

Despite achieving profitability with 26.8% operating margins and maintaining $6 billion in cash with virtually no debt, Palantir trades at extreme valuations of 100 times revenue and 224 times forward earnings. With 84% of analysts recommending Hold or Sell ratings, the market remains divided on whether the premium is justified. Bulls argue the valuation reflects Palantir's transformation from niche government contractor to critical AI infrastructure provider, with analysts projecting potential revenue growth from $4.2 billion to $21 billion. The company's success across nine strategic domains—from military modernization to healthcare analytics—suggests it has built an "institutionally required platform" that could justify sustained premium pricing.

The investment thesis ultimately hinges on whether Palantir's structural advantages—its proprietary data integration technology, defense entrenchment, and accelerating commercial adoption—can sustain the growth trajectory demanded by its valuation. While the platform's complexity requires heavy customization and limits immediate scalability compared to simpler competitors, the 93% commercial growth rate validates enterprise demand. Investors must balance the company's undeniable technological and strategic positioning against valuation risk, with any growth deceleration likely triggering significant multiple compression. For long-term investors willing to weather volatility, Palantir represents a bet on AI infrastructure dominance across both military and commercial domains.