ANDREW «LEFT» GOES ANDREW «UP» AS PALANTIR CELEBRATES 5YRS ANNIVAndrew Left from "Citron Research" made his name writing shrewd short-seller reports on companies he deemed troublesome. In mid-August, Left called high-flying Palantir "overvalued".

Since that the stock turned down nearly 17% but resistently printed "Double Top" technical figure after. Now Left is excited about the bullish perspectives.

Palantir shares have jumped more than 1,700% since the data analytics company opened on the New York Stock Exchange 5 (five) years ago on Spetember 30, 2020.

During that time, revenue has roughly quadrupled as the company inked more deals with the U.S. government and benefitted from advancements in artificial intelligence.

Palantir’s steep valuation and reliance on government contracts have raised concerns.

The stock price has surged more than 1,700%, closing on Monday nearly at $180 for a market cap of over $430 billion. That puts it among the 20 most-valuable U.S. companies, and above tech stalwarts like Cisco and IBM.

Last year, Palantir joined the S&P 500, replacing American Airlines NASDAQ:AAL .

Quarterly revenue surpassed $1 billion for the first time last quarter, and is expected to reach $4.2 billion this year, according to analysts surveyed by LSEG, up almost sixfold from 2019. The company’s roster of customers grew from 125 in the first half of 2020 to 849 at the end of June. During that time, Palantir has added 1,500 full-time employees.

CEO Alex Karp, who founded the company in 2003 alongside notable investors like Peter Thiel and Joe Lonsdale, was exerting optimism on day one of Palantir’s life on the public market.

“We’ve reached a base where our company is very significant,” Karp, who holds a law degree from Stanford and PhD in neoclassical social theory from Goethe University in Frankfurt, Germany, told in an interview on listing day.

“Being in the public space will help us with our clients and help us grow.”

In a report in August 2025, Citron Research’s Andrew Left, a noted above ex-short-seller, called Palantir “detached from fundamentals and analysis.” When compared to OpenAI’s recent $500 billion valuation, he said Palantir should be priced at $40, or less than one-quarter of its current price, if it was assessed the same revenue multiple as the artificial intelligence startup.

“Karp and his team should be proud. But for investors, that’s where discipline kicks in,” Left wrote. “Comparison is the enemy of happiness, and when measured against true AI leaders, Palantir’s price already reflects success beyond its fundamentals.”

Karp, who doesn’t shy away from a dispute, recently told detractors to “exit” if they “don’t like the price.”

“We are going to be the most important software company in the world, and people will figure out what that’s valued over a long period of time,” Karp said on the day of the company’s NYSE debut.

For now, i.e. over the past 5 years since IPO debut, Palantir is among Top 3 S&P500 index performers, alltogether with Supermicro NASDAQ:SMCI (#1 rank) and Nvidia shares NVDA (#3 rank).

Over the past twelve months, Palantir stock has added nearly +350 %, and this is the 2nd return over all components, just after new kid on the block, Robinhood Markets NASDAQ:HOOD stock that entered S&P500 index earlier this year.

--

Best wishes,

@PandorraResearch Team

Trade ideas

Is Palantir (PLTR) Entering a Consolidation Phase? A Technical aTechnical Analysis: Palantir Technologies (PLTR) Amid Overbought Signals and Valuation Gaps

Palantir Technologies Inc. (NASDAQ: PLTR) has experienced significant volatility in recent sessions, reflecting growing uncertainty among investors regarding its valuation and technical positioning. The stock closed at $173.07, down by 7.47%, after testing its resistance area near $186. Both daily and weekly technical indicators are now suggesting that a potential short-term correction could be underway.

Weekly Chart Outlook: Approaching Resistance After a Prolonged Rally

From the weekly timeframe, NASDAQ:PLTR has been trending upward since early April, supported by consistent higher lows and strong momentum in the technology sector. The recent breakout above the $160–$165 zone confirmed bullish sentiment, but the latest candlestick formation shows rejection near $186, indicating profit-taking pressure.

The Stochastic RSI on the weekly chart is hovering in the overbought zone, signaling that the rally may be losing strength. While this does not necessarily imply an immediate reversal, it often precedes a consolidation phase or a short-term pullback. Volume patterns also show a slight decline compared to the early phase of the uptrend, reinforcing the possibility of slowing momentum.

Additionally, the price is now slightly extended from its key moving averages, suggesting that any correction toward the $160–$165 support zone would still maintain the longer-term bullish structure.

Daily Chart Confirmation: Stochastic RSI and MACD Turning Cautious

Read full analysis on my website :

darrismanresearch com

Palantir Money Heist – Breakout vs Pullback, Which Side Wins?💎🔫 PLTR Money Heist Plan – Thief Trader Edition 🚀

🎯 Asset: Palantir Technologies Inc. (PLTR)

🏦 Plan Type: Swing / Day Trade

⚡ Bias: Bullish (Pending Order Strategy)

🗺️ Thief Trader Heist Plan

Entry Zone (Breakout): 🔓 $162.00 ⚡

Pullback Entry: 🎯 $132.00 & above any price

🔔 Set TradingView alarms to catch the breakout easily — no excuses thieves!

Stop Loss (Breakout Entry): 🛑 $148.00

Stop Loss (Pullback Entry): 🛑 $120.00

📝 Stops are my thief levels — adjust based on your own strategy & risk.

Target: 💰 Escape vault before $184.00 – $188.00 resistance (Overbought + Trap Zone)

❓ Why This Plan? (Thief Logic)

Bullish Bias: Strong momentum around AI contracts & government adoption = upside fuel.

Breakout @162: Key resistance level tested multiple times → if broken, doors open for rapid move higher.

Pullback @132: Golden reload zone where buyers previously defended → sniper entry for risk/reward thieves.

Fear & Greed (75/100): Market greed creates volatility → perfect environment for quick thefts.

Macro Boost: AI sector tailwinds + gov contracts = solid catalysts.

Thief Rule: We don’t chase blindly — we wait for breakout confirmation or reload on pullback to maximize stolen pips.

📊 Palantir Stock Data Report (As of Sept 7, 2025)

Prev Close: $156.14

Day Change: -$3.03 (-1.94%)

After-Hours: $152.30 (-0.53%)

52-Week Range: $32.47 – $190.00 🎯

Market Cap: $363.23B 🏦

😱 Fear & Greed Sentiment

Retail Traders: 🟢 Bullish (70% optimism, AI hype + contracts)

Institutions: 🟡 Neutral (Valuation caution + competition risks)

Fear & Greed Score: 🔥 75/100 (Greed = volatility fuel)

💰 Fundamental Breakdown

Revenue (TTM): $3.44B

Net Income (TTM): $763.29M

Profit Margin: 22.18% ✅

P/E Ratio: 493.90 ⚠️ (Ultra high)

P/S Ratio: 112.41 (Overvalued vs peers)

Growth Drivers:

U.S. Commercial Rev ↑93% YoY 🚀

Gov Rev ↑49% YoY 🏛️

🌍 Macro & Market Drivers

🧠 AI Tailwinds: Massive global demand

🏛️ Gov Contracts: Potential expansion

⚔️ Competition: OpenAI + enterprise challengers

📊 Overall Market Score: 60/100 → Mildly Bullish 🐂

🔮 Key Takeaways (Thief Edition)

Short-Term: Expect heavy volatility (perfect for a thief’s quick grab).

Long-Term: Growth path strong but valuation = danger zone.

Watchlist: Q3 earnings (Nov 2025) + Gov contract headlines.

🔎 Related Assets to Watch

NASDAQ:META (AI sector peer)

NASDAQ:MSFT (Gov + AI contracts)

NASDAQ:NVDA (AI chip leader)

NASDAQ:TSLA (Speculative momentum)

AMEX:SPY (Macro market sentiment)

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

#PLTR #Palantir #AIStocks #SwingTrade #DayTrade #ThiefTrader #MoneyHeistPlan #StockMarket #TradingViewAnalysis

$PLTR Double top with Bearish Key ReversalPalantir has been in the news a lot recently, for a variety of reasons. However any trader/analyst has been happy following them for a good while.

Are we now about to take a pause? Is all that media attention having an impact on market sentiment?

Certainly last week we printed a bearish Key Reversal pattern, which was also the 2nd leg of a double top. Is price reflecting the sentiment?

PLTR at a Crossroad: $162 Breakout or $144 Retest?

NASDAQ:PLTR The stock is consolidating around $158 after pulling back from the $188 high. Key zones and possible scenarios are highlighted:

Support levels:

$156–152 → nearest support

$144 → strong support

$126 → deeper support zone

Resistance levels:

$162–163 → breakout level to watch

$180–188 → upside target if momentum continues

Indicators:

Bollinger Bands are tightening → signaling a potential breakout.

MACD is curling upward after a bearish phase → early sign of a possible reversal.

Scenarios:

• 🟢 Bullish: breakout above $162 could open the way to $180–188.

• 🔴 Bearish: drop below $156 could push price towards $144.

Short-term moves may be strongly influenced by upcoming U.S. macro data (CPI & Fed expectations).

PLTR Testing the Breakout Zone – Big Gamma Cluster Ahead for OctIntraday Technical Outlook (15m Chart)

Palantir (PLTR) closed at $186.75, consolidating under a descending trendline after a strong run earlier this week. On the 15-minute chart, price is tightening into a wedge formation:

* MACD: Flattening near neutral after recent downside momentum, showing signs of a potential shift.

* Stoch RSI: Just bounced from mid-zone toward overbought, suggesting near-term strength if momentum holds.

* Key Levels: Resistance sits at $187.4–188.2, followed by $189.4. Support is at $185, with deeper downside near $183–182.9.

Intraday takeaway: PLTR needs to break above $188.2 for a clean breakout; otherwise, the wedge could force a pullback to $185.

Options Sentiment & GEX Outlook (1H Chart)

The GEX map highlights where institutional positioning could steer price action:

* Gamma Walls:

* $188–192.5: Heavy call wall cluster and highest positive GEX — major resistance zone.

* $185–182.5: Key support layers where dealer hedging may slow selling.

* $175 / $170: Large put walls that would act as magnets if downside momentum accelerates.

* Implications:

* Sustaining above $186.5–187 keeps price pinned toward the $188–190 gamma resistance zone.

* A rejection below $185 increases the risk of a pullback toward $182.5–180 before buyers reload.

* Volatility Context: IVR at 26 vs IVx avg 59.2 means premiums are slightly underpriced. With GEX tightly packed, directional breakouts could deliver outsized option moves.

My Thoughts & Recommendation

For Oct 3 trading, PLTR is sitting right at the breakout test:

* Intraday (scalping/trading): Bullish above $187.4 with targets at $188.2–189.5. Failure to break $188 risks fading back toward $185–183.

* Options trading (swing/0DTE): Calls make sense on confirmed breakout above $188, chasing toward $190–192. Puts become favorable if PLTR rejects $188 and slips back under $185, with $182.5 as the first magnet.

Bias heading into Oct 3: Bullish leaning, but only if $188 breaks cleanly.

Disclaimer:

This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk before trading.

It will simply bounce off and go further up. Pltr super bullish.Lorenztian classification line. Bounces off at 60-80. Goes up again. Simply clear pattern.

Pltr super bullish.

Magic word - AI . Dont go against AI , especialy gov AI.

PLTR Breaking Into Supply – $186 Key Gamma Pivot (Oct 2) Intraday (15-Min Chart)

Palantir surged early but then stalled near the $185–$186 zone, where price is now consolidating. On the 15-min chart, price is moving along a rising trendline but momentum looks extended. MACD is still positive but fading, and Stoch RSI shows overbought conditions that may force short-term cooling.

* Immediate resistance: $186.2–$186.5 (intraday ceiling).

* Support zones: $183.3 (near-term pivot) and deeper at $178.5.

* Upside trigger: Breakout above $186.5 could squeeze toward 188.5–190 intraday.

* Downside risk: Rejection here sends price back to $183, with a deeper flush possible into $178.

Bias intraday: cautiously bullish above 183.3, but stretched oscillators suggest choppy consolidation unless bulls decisively break 186.5.

Options / GEX (1-Hour Chart)

Gamma structure gives a clear roadmap for PLTR’s next move:

* Call walls: Heavy levels sit at 187.5–192.5, with $192.5 marked as the 2nd call wall.

* Put walls: Support zones show up around 177.5 and further at 172.5, defining downside boundaries.

* Sentiment: Options flow is more balanced (≈40% calls), unlike TSLA/MSFT, suggesting less aggressive bullish pressure.

The highest positive GEX resistance is currently at $182.5, which PLTR has just cleared. This flip shifts dealer hedging into a supportive dynamic, meaning price could grind toward 187–190 as long as $183 holds.

My Thoughts

For Oct 2, PLTR is pressing into a pivotal resistance zone. If $186.5 breaks with volume, momentum could carry it into 188–190 quickly. If rejected, expect a retest of 183, and possibly a pullback toward $178 if weakness persists.

* Bullish play: $185/190 call spread targeting continuation toward gamma walls.

* Defensive play: Hedge under $183 with short-term puts, eyeing 178.

Bias: PLTR looks constructive above 183, but $186.5 is the true breakout line to watch.

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk before trading.

PLTR Oct. 1 – Testing the Top of the Range! 🚀Intraday View (15-Min Chart)

PLTR surged early but is now pulling back from $183 resistance, consolidating near $181 within an ascending channel. Momentum has cooled, with MACD rolling over and Stoch RSI slipping toward oversold.

* Support Levels: $181.40, $178.86, $177.48

* Resistance Levels: $182.76, $183.00

* Indicators: MACD showing bearish histogram build, Stoch RSI nearing bottom levels.

📌 Intraday Thought (Oct. 1): If $181 holds, PLTR could bounce back to retest $182.7–$183. A breakdown below $181 risks sliding to $178.5–$177.5. Scalpers can lean long near $181 support with stops just below, or fade strength near $183 resistance.

Options & Swing View (1H + GEX)

Gamma levels outline the battlefield:

* Upside: Strong call wall at $182.5–$187.5, with another stacked wall above $190.

* Downside: Key put support near $172.5–$170, with deeper protection at $162.5.

This paints a range between $177.5–$183 short term. A breakout over $183 could fuel a run toward $187.5–$190, while losing $177.5 risks momentum fading back to $172.

* Bullish Play (Oct. 1): Calls or spreads targeting $187.5–$190 if $183 breaks convincingly.

* Bearish Hedge: Short puts toward $177.5 → $172 if $181 support fails.

* Neutral Play: Iron condor between $177–$183 for range capture while PLTR churns sideways.

My Thoughts (Oct. 1)

PLTR is pressing into the upper end of its range again. The $183 level is the line in the sand—above it, we could see quick follow-through toward $187.5+. If it can’t clear $183, expect chop back toward $178. For now, I’d trade this as a range setup, but keep tight risk management if $183 breaks.

Disclaimer: This analysis is for educational purposes only and does not constitute financial advice. Always do your own research and manage risk before trading.

PLTR goes higherPrice just crushed the resistance with big volume slowly coming back in. Watch it make a new ATH

Hello trader, for tomorrow, 9/30/25, PLTR: 178.86If the open is above the closing price, we could enter a quick bullish position up to 182.00. If the movement continues, we could close the position at 184.00, forming a triple top. Our next bullish entry could be above 186.00. The price could also find a rejection zone at 182.00.

On a bearish entry, a rejection zone could be found at 176.00. If this price falls below 176.00, we only enter bearish below 174.00/172.00.

PLTR - Palantir - What i see - Double TopHello Everyone,

Happy evening to all and my followers.

Normally i do not check the charts Weekdays as i am working quite busy and I do not have a power to have a look at charts and write anaylsis.

But today I just wanted to share this, because pattern is so obvious for me.

I see the double Top pattern and second top is lower than first one. This is a signal to Pull-back.

I am expecting to pull-back between 150-156 and if it reach to this level , I can definately invest good amount of money on Palantir.

I see a high possibility to Pull-back and it is worth to watch it.

First support levels are 166 - 166.50, second one 156

Resistance levels are 185 and 190.

If it breaks to 190 and close above this level more than 2 days then there is potential to reach 228 - 230 .

Mainly i could go short for Palantir for short term and wait for between 150 - 156 then decide what to do.

This is just my thinking and it is not invesment suggestion , please do not make any decision with my anaylsis.

Have a lovelly evening to all.

PLTR Weekly Chart – Multiyear Uptrend Intact📊 Technical View

Palantir (PLTR) has been in a powerful multiyear uptrend, consistently building higher lows and respecting its internal long-term trendline. Despite short-term fluctuations, the broader structure remains intact and strongly bullish.

Trendlines:

📈 Multiyear uptrend driving price action since early 2023

📈 Internal long-term trend providing additional confirmation

Price Behavior: Steady accumulation, followed by breakouts aligned with the uptrend channel

📌 Outlook

Bullish Scenario: Continuation of this multiyear structure could lead to further highs as long as trendlines are respected.

Risk Factor: Only a decisive break below the long-term uptrend would shift the market bias.

🌍 Fundamental Insight

Palantir remains at the core of AI, defense, and enterprise data adoption. The company’s role as a leader in government contracts and AI-driven solutions reinforces the technical outlook — a long-term story of growth aligned with its multiyear uptrend.

✅ Conclusion

The weekly chart highlights PLTR’s long-term strength. As long as price action respects the uptrend, the bullish case remains dominant.

✨ If you find this analysis helpful, please don’t forget to like and follow for more insights!

⚠️ Disclaimer

This analysis is for educational purposes only and is not financial advice.

$PLTR - Expensive, Overbought and Valuation Ready to PopI know Palantir NASDAQ:PLTR has earned a cult following as an "AI leader play" aside from $NVDA. I successfully traded this to the upside but right now the stock valuation is detached from reality.

With a trailing P/E near 600× and a forward P/E still above 240×, investors are pricing in decades of flawless execution and hyper-growth. While revenue growth remains steady around 30% YoY, that pace is not extraordinary compared to other enterprise software names trading at a fraction of Palantir’s multiples. Even industry leaders like NASDAQ:MSFT trade at a lower valuations ratios despite broader market reach and deeper moats.

I'm concerned of NASDAQ:PLTR 's reliance on government contracts. Risks such as political shifts, budget tightening and contract delays could quickly hit the growth. The imbalance between valuation and fundamentals makes this stock fragile.

Technically, the chart reflects euphoric buying. Price is extended very well above our major moving averages and momentum is fading as stochastics roll over from overbought territory.

If NASDAQ:PLTR slips below key support levels, momentum traders could unwind positions rapidly, amplifying downside. With fundamentals stretched and technicals overheated, NASDAQ:PLTR looks less like a growth stock and more like a speculative bubble vulnerable to sharp mean reversion.

NASDAQ:PLTR first support right now is at around $166 (50EMA) while the major support lies at around $151. Once that $166 (50EMA) becomes the resistance, I will take a short position here. I will also get a $155 put strike with Oct10 exp. My trade plan for these long puts is if my premium is down by 30% I'll take it out. It means my option play isn't working. Managing the risk is the only way to survive this zero sum game. Good luck and God bless everyone!

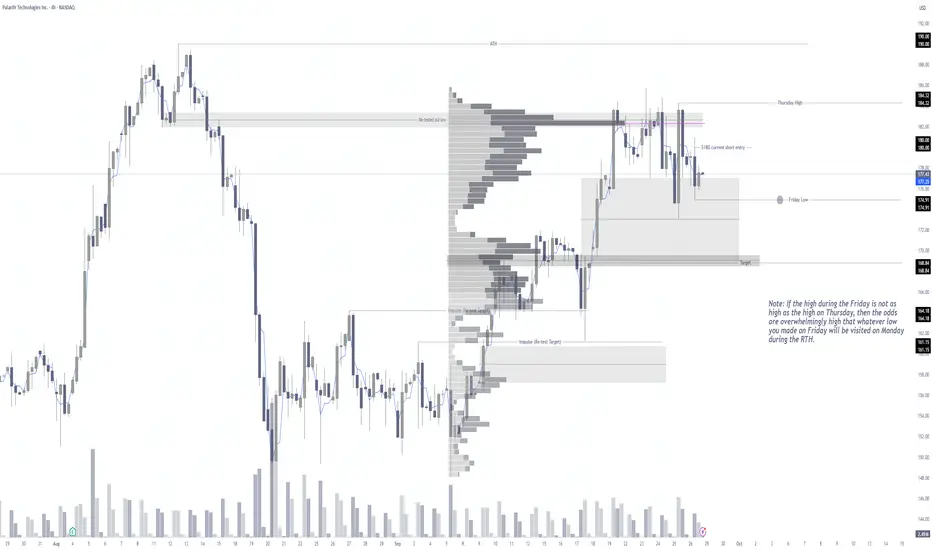

PLTR - Current Short (Idea behind)PLTR 4-hr could not break highs on Thursday. So, Friday pre-market, I took a short position at $180; failing highs indicate weakness. Additionally, Friday could not break Thursday high, so its highly likely that Friday lows will be re-tested on Monday.

Where am I looking to take profit? Once we reach Friday low, I will watch to see how price reacts. Looking at the volume node, if we break Friday low, its possible to have a quick decent down (due to volume gap) to the $170 area; my target is $168ish (bottom of volume node).

PLTR Long Idea: Potential Resistance Flip to SupportHello, traders.

This is an analysis of Palantir (PLTR) on the 15-minute timeframe, highlighting a potential long trading opportunity.

Analysis:

The chart shows a key horizontal level at approximately $177.56. This price level previously acted as strong resistance in mid-September, rejecting upward price movement.

Recently, the price has successfully broken through and established itself above this former resistance. The current price action appears to be a retest of this level, which now has the potential to act as new support. This "resistance-turned-support" is a classic technical pattern that can signal a continuation of the bullish trend.

Trade Plan:

Entry: An entry is considered around the current support level of $177.56.

Stop Loss: To manage risk, a stop loss is placed at $169.67, below the recent swing low. A drop to this level would likely invalidate the bullish thesis.

Take Profit: The target for this long position is set at $198.07, aiming for a higher area of potential resistance.

This setup presents a favorable risk-to-reward ratio based on the levels identified on the chart.

Disclaimer: This is for educational purposes only and reflects a personal market analysis. It is not investment advice. Please conduct your own research and manage your risk appropriately before making any trading decisions.

Good scenario for PalantirDo you want coffee NASDAQ:PLTR ?

Palantir has performed excellently throughout 2025 and looks set to continue doing so.

AI Momentum and investor flowsCurrent update on portfolio

I believe that the main ai push has fizzled out hence have entered into some shorts yesterday.

The main inflows into the market are from retail investors, however when stocks start to drop these are the first to panic sell. A crash/pullback in this market could be amplified.

www.nber.org

Interesting academic paper in my opinion explains price movement in the market. Also can look at Jean-Philippe Bouchaud and his paper on this matter. (Inelastic Market Hypothesis)

arxiv.org

Short

-PLTR

-QUBT

Long

-VKTX (Pipeline etc) this is a longer term hold

Palantir Technologies PLTR STRONG BUY Palantir stands at the forefront of artificial intelligence for both the U.S. government and commercial clients. Its platforms including Gotham, Foundry, Apollo, and the Artificial Intelligence Platform are rapidly reshaping enterprise deployment of AI and big data. PLTR has gained over 145% since April, riding institutional demand as well as retail enthusiasm for generative AI innovation.

Potential H&S on PLTRShort post:

There is a potential H&S on PLTR that might materialize by early to mid October. I am expecting a retreat to 200MA and below in the next months.

double top for $pltrdouble top for NASDAQ:PLTR is coming

- stretched roar at 70-80 degree angle

- reverse divergence of RSI and MACD

- price has 10+X from bottom

PALANTIR PLUS GOLD. VOLATILITY + STABILITY = EXPLOSIVE MIXTUREWere you still dream about super-duper hyped crypto/ AI names, which change each other like TikTok Reels or for example Google Shorts?..

.. but shortening Big portfolios or even tight ones, like Magnificent Seven, to just Palantir and Gold can provide a focused approach with compelling performance and risk management, given how both assets have outperformed tech mega-caps in 2025.

The process involves strategic decision-making, in-depth performance analysis, and clear rebalancing steps.

Magnificent Seven: 2025 Performance Context

The Magnificent Seven - Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, Tesla - have dominated market attention. But in 2025, their stocks saw significant declines. Tesla dropped by around 38%, Apple and Nvidia by 21%, while the others also posted double-digit losses in a few quarters ago. High market concentration and rising tariffs pressured these tech giants, leading investors to reconsider diversification. This environment sets the stage for seeking alternative performers.

Why Focus on Palantir and Gold?

Palantir (PLTR) has surged as one of the top S&P 500 performers, gaining over 138% this year, far surpassing the Magnificent Seven ETF, which (in the best case) print low double-digit numbers in 2025. Palantir's edge lies in its government contracts and leadership in AI platforms, making it a market leader during sector disruptions and economic uncertainty.

Gold has soared nearly 44% year-to-date, reaching record highs as the most crowded trade on Wall Street. As tech stocks falter, gold's appeal as a safe haven has intensified amid tariffs, a weakening dollar, and economic uncertainty. Major fund managers now see gold as the top-performing asset for 2025.

Portfolio Construction: Reducing to Two Securities

Capital Allocation. Split proceeds between Palantir (growth/innovation) and gold (risk-off hedge). A typical split could be 50/50 for simplicity or tailored to risk tolerance - higher gold allocation for defensive profiles, higher Palantir for aggressive growth.

Risk Management: Hedge Palantir’s volatility plus gold’s stability. Stability.... plus volatility. Two words to explain it all.

Rationale and Benefits

Concentrating on two uncorrelated assets amplifies both upside (Palantir) and defensive resilience (gold). Diversification outside tech mega-caps mitigates regulatory and single-sector risks, as seen in the recent performance divergence. Enhanced returns: Palantir’s growth-oriented rally and gold’s safe-haven gains both outperformed not only the S&P 500 but the tech elite.

By systematically selling underperforming Magnificent Seven stocks and reallocating into Palantir and gold, the portfolio tilts toward assets with strong 2025 track records and complementary risk profiles, aligning with current market realities and future outlook.

Have you seen the similar before or not yet, Palantir plus Gold move together... in one-way direction.. for TWENTY straight months in a row.

--

Best wishes,

@PandorraResearch Team

PALANTIR - STOCK REPORT1) Executive summary

Palantir (PLTR) showed very strong revenue growth in 2023–2025 driven by commercial expansion and adoption of its platforms (Gotham, Foundry) across government and private sectors. As of September 2025 the company is clearly profitable on a TTM basis with positive operating margins, strong cash generation (high FCF) and a sizable net cash position. However, relative valuation is extremely high (P/S, EV/Rev, P/E multiples well above peers), reflecting aggressive growth expectations and strong speculative interest.

Main risks: high sensitivity to AI sentiment, reliance on large government contracts and a concentrated commercial customer base, potential regulatory pressure and share-price volatility.

Short recommendation: Hold.

Rationale: financial strength and growth justify exposure, but valuation requires the company to deliver continued high growth and margins; new purchases should wait for a pullback or operational confirmations (stabilized growth rate and guidance). Risk-seeking/high-return investors may consider a partial position.

2) Key data and company overview

Name: Palantir Technologies Inc.

Sector: Software — Data analytics / Enterprise AI

Primary market: NYSE/NASDAQ (Class A) — Ticker: PLTR

Business brief: Software platforms for data integration, analytics and decision‑making (Gotham for governments, Foundry for enterprises, Apollo for deployment). Revenue model: software licenses, SaaS/cloud subscriptions, implementation services and multi‑year government contracts. Main geographies: USA (largest weight, both government and commercial), Europe, expanding APAC.

Market & key metrics (sources: StockAnalysis / MarketBeat / Macrotrends; close price 22‑Sep‑2025):

- Market cap: ~425–433B USD

- Shares outstanding: ~2.365B

- Float: ~2.19B

- P/E (TTM): ~560–595

- EV/EBITDA (TTM): ~700

- Last close (22‑Sep‑2025) used: 179.33 USD

- Price change: 1Y ≈ +398%

3) Financial results summary (last 3 years + last 4 quarters)

Sources: Annual reports 2022–2024, 2025 10‑Q/earnings, StockAnalysis.

TTM / annual rounded (USD millions):

- Revenue (TTM): 2.87B

- Net income (TTM): 462.19 M USD

- Operating income (TTM): 569.55 M

- Diluted EPS (TTM): 0.30

- Free cash flow (TTM): ~1,710

- Operating margin (TTM): 26.83%

- Net margin (TTM): 32.55%

YoY trends: revenue growth ~40–48% in portions of 2025 (company reported strong quarter-over-quarter acceleration); net income materially higher as company turned profitable.

Last 3 years (rounded):

- 2022 Revenue: ~1,801M

- 2023 Revenue: ~2,319M (+29% YoY)

- 2024 Revenue: ~2,866M (+24% YoY)

- 2025 TTM: ~3,440M (+20% vs 2024 TTM; mid‑2025 quarters show acceleration)

Recent quarterly pattern (indicative): Q3‑2024 ~640M; Q4‑2024 ~700M; Q1‑2025 ~780–800M; Q2‑2025 ~1,000M.

Comment: strong commercial acceleration in 2024–H1 2025, especially U.S. commercial; profitable on TTM with high FCF, though EPS/margins affected by stock‑based comp and non‑cash items.

4) Balance sheet and liquidity

Key (TTM / latest quarter, USD millions):

- Cash & equivalents: ~6,000

- Total debt: ~238

- Net cash: ~5,760

- Working capital: ~5,800; Current ratio ~6.3; Quick ratio ~6.19

- Debt/Equity: ~0.04

Comment: very strong liquidity and low leverage; primary risks are customer concentration and capital needs for major AI/cloud investments or M&A.

5) Cash flows

TTM (USD millions):

- Operating cash flow: ~1,730

- CapEx: ~21

- Free cash flow: ~1,710

Comment: high operating cash conversion and very low capex yield an elevated FCF margin. Increased investment in cloud/AI or acquisitions could raise capex and cash use.

6) Valuation

Peers: Snowflake (SNOW), CrowdStrike (CRWD), Splunk (SPLK).

Comparable multiples (TTM, vendor ranges):

- PLTR: P/S ~122–183, P/E ~565, EV/EBITDA ~700

- SNOW: P/S ~20–80 (varies), P/E N/A (historical losses)

- CRWD: P/S ~25–40, P/E >100 (varies)

- SPLK: P/S ~10–20, P/E variable

Observation: Palantir trades at revenue and earnings multiples far above peers, reflecting high growth expectations and speculative demand.

Simple DCF (assumptions stated):

Base revenue TTM = 3,440M.

Growth assumptions: 2026 +30%, Yr2 +15%, Yr3 +10%, Yr4 +6%, Yr5 +5%; terminal growth 3.5%.

EBIT margin converging to 18%; tax 18%; CapEx = 1% of revenue; WACC = 9%. Result: implied fair value per share roughly in the range ~8–25 USD (highly sensitive to assumptions).

Sensitivity: lower WACC / higher terminal growth materially raises value; higher WACC or lower growth materially lowers it.

Detailed year‑by‑year DCF is available on request.

7) SWOT

Strengths:

- Integrated platforms (Gotham/Foundry) with data advantages.

- Strong net cash position and high FCF.

- Rapid commercial AI adoption and high customer retention.

- Strategic government contracts with entry barriers.

Weaknesses:

- Revenue concentration in a few large clients/government.

- High share‑price volatility and valuation disconnect vs peers.

- Dependence on costly AI/R&D talent.

- Historical share dilution.

Opportunities:

- International commercial expansion and Foundry cross‑sell.

- Monetization of advanced AI/cloud offerings.

- Partnerships with hyperscalers.

- Upsell within regulated enterprises.

Threats:

- Regulatory pressure on data/AI use.

- Intensifying competition (Snowflake, Databricks, cloud vendors, AI startups).

- Reputational risks tied to government contracts.

- AI sentiment correction reducing valuation.

8) Key risks and catalysts + timeline

Key risks : regulation on data/AI, customer concentration and loss of large contracts, slowdown in commercial demand or IT spend, valuation sensitivity to market sentiment.

Catalysts / timeline:

- Q3 2025 earnings — estimated Nov 3, 2025 (after market) — primary near‑term catalyst.

- Major government contract announcements or large ARR renewals (timing variable).

- Product/feature releases and cloud partnerships (ongoing).

9) Final recommendation and risk positioning

Operational recommendation: Hold .

Time horizon: medium term (12–24 months) to monitor growth consolidation and margin confirmations.

Risk/return profile: High risk / potentially high reward — elevated valuation creates meaningful downside if growth slows; upside depends on sustaining high growth and margins. Risk‑tolerant investors who believe in Palantir’s AI/commercial momentum may hold or take a partial position with risk controls; risk‑averse investors should avoid new purchases until valuation normalizes.

10) Sources and data date

Main sources: Palantir Investor Relations (SEC 10‑K / 10‑Q / earnings releases), TradingView, public research notes. Data date: 22 September 2025. Assumptions: market cap ~428B; close price 22‑Sep‑2025 = 179.33 USD; shares outstanding = 2.365B.