Why the Reaction Matters More Than the Level!!!Most traders spend their time hunting for the perfect level.✖️

Support. Resistance. Demand. Supply.

They draw the zone… and assume price must react.

But professionals know something crucial:

The level itself is not the edge.

The reaction is.

Here’s why.

1️⃣ Levels Are Common Knowledge

Everyone sees the same support.

Everyone sees the same resistance.

If levels alone were enough, everyone would be profitable.

A level is just a location.📍

It doesn’t tell you who is in control.

2️⃣The Reaction Reveals Intent

What matters is how price behaves at the level.

Ask yourself:

- Does price reject immediately or hesitate?

- Are candles impulsive or overlapping?

- Does price leave the level with strength or drift away slowly?

A strong reaction tells you:

➡️ One side stepped in aggressively.

A weak reaction tells you:

➡️ The level exists… but conviction doesn’t.

3️⃣ Clean Rejections Beat Perfect Levels

A slightly imperfect level with a violent reaction

is far more valuable than a textbook level with no follow-through.

Professionals wait for:

- sharp rejections

- momentum expansion

- structure confirmation

They don’t assume... they observe.

4️⃣ Failed Reactions Are Warnings

When price reaches a level and does nothing…

that silence is information.

Failed reactions often lead to:

- level breaks

- deeper moves

- trend continuation

The market is telling you:

➡️ “This level no longer matters.”

📚The Big Lesson

Levels tell you where to look.

Reactions tell you what to do.

If you shift your focus from drawing levels to reading behavior at levels,

your trading instantly becomes clearer and more objective.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Community ideas

The Retail Trend-Following MythThe Illusion of Simple Profits: A Quantitative Analysis of Moving Average Trend Following Strategies and the Gap Between Retail Mythology and Institutional Reality

The proliferation of retail trading education has created a widespread belief that trend following through moving average crossover systems represents a reliable path to consistent profits. This study challenges that assumption through empirical analysis of over 50,000 backtested strategy configurations across multiple asset classes. Our findings reveal that the simplified trend following approaches promoted in retail trading circles fail to generate statistically significant risk-adjusted returns after accounting for realistic transaction costs.

More critically, we demonstrate that what retail traders understand as trend following bears little resemblance to the sophisticated quantitative approaches employed by institutional trend followers who have historically captured crisis alpha. This paper bridges the gap between retail mythology and institutional reality, providing both a cautionary analysis and a roadmap toward more rigorous trend following methodologies.

1. Introduction

Every year, millions of aspiring traders encounter some variation of the same promise: draw two lines on a chart, wait for them to cross, and watch the profits roll in. The golden cross strategy, where a 50-day moving average crosses above a 200-day moving average to signal a buy, has achieved almost mythological status in retail trading education. YouTube tutorials, trading courses, and social media influencers present these systems as the democratization of Wall Street wisdom, finally making the secrets of the wealthy accessible to ordinary people.

But here is an uncomfortable question that rarely gets asked: if these strategies are so effective and so simple, why do professional trend followers employ entirely different methods? Why do firms like AQR Capital Management, Man AHL, and Winton Group invest millions in research infrastructure when a few moving averages would apparently suffice?

This study was designed to answer that question empirically. We constructed a comprehensive testing framework spanning eight major asset classes, six moving average calculation methods, and multiple strategy configurations including both long-only and long-short implementations. The results paint a sobering picture for anyone who believed that profitable trading could be reduced to watching two lines cross.

Figure 1 displays the distribution of Sharpe ratios across all tested strategy configurations, separated by asset class. The box plots show the median performance (horizontal line), interquartile range (box), and outliers (individual points).

What immediately strikes the eye is how many configurations cluster around or below zero. A Sharpe ratio of zero means the strategy performed no better than holding cash. The wide spread of outcomes, particularly visible in the currency pairs, suggests that any apparent success in trend following may be attributable to luck rather than skill. Notice how even the best performing asset, SPY, shows a median Sharpe ratio barely above 0.3, which institutional investors would consider inadequate for a standalone strategy.

2. Methodology and Data

Our analysis employed daily price data from 2010 through 2024 for the following instruments: SPY representing US equities, GLD for gold, USO for crude oil, SLV for silver, and currency ETFs FXE, FXB, FXY, and FXA representing EUR/USD, GBP/USD, USD/JPY, and AUD/USD respectively. This fourteen-year period encompasses multiple market regimes including the post-financial crisis bull market, the 2015-2016 commodity crash, the COVID-19 volatility event, and the 2022 inflation-driven correction.

We tested six moving average types: Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), Double Exponential Moving Average (DEMA), and Triple Exponential Moving Average (TEMA). Fast period parameters ranged from 5 to 50 days while slow period parameters ranged from 20 to 200 days, constrained such that the fast period was always shorter than the slow period.

Critically, each configuration was tested in two modes. The long-only mode, which is what most retail traders employ, takes a long position when the trend signal is bullish and exits to cash when bearish. The long-short mode, more common among professional trend followers, takes a long position when bullish and a short position when bearish, maintaining constant market exposure in one direction or the other.

Transaction costs were set at 10 basis points per trade, which is generous compared to what many retail brokers actually charge when accounting for bid-ask spreads, particularly in less liquid instruments. Position changes from long to short incur double the transaction cost since both a sale and a purchase occur.

Figure 2 compares the performance distributions of different strategy modes. Each box represents thousands of backtested configurations. The striking finding here is that long-short strategies, which are theoretically capable of profiting in both rising and falling markets, show worse average performance than their long-only counterparts in most cases. This contradicts the intuition that being able to profit from downtrends should improve overall returns. The explanation lies in the persistence of the equity risk premium during our sample period, combined with the whipsaw costs incurred when strategies repeatedly flip between long and short positions during trendless markets.

3. The Retail Trader Illusion

Before presenting our quantitative findings in detail, it is worth examining what retail traders typically believe about trend following and why those beliefs are so persistent despite limited evidence.

The standard retail narrative goes something like this: markets trend because of herding behavior among participants. Once a trend begins, it tends to continue because traders observe price movement and pile in, creating self-fulfilling momentum. Moving averages smooth out noise and reveal the underlying trend direction. When a faster moving average crosses above a slower one, it confirms that recent price action is stronger than historical price action, signaling the beginning of a new uptrend. The reverse signals a downtrend.

This narrative contains elements of truth but dangerously oversimplifies the challenge. What it omits is far more important than what it includes.

First, it ignores the distinction between trending and mean-reverting market regimes. Research by Hurst, Ooi, and Pedersen (2017) demonstrates that trend following strategies have historically made most of their returns during relatively brief crisis periods while suffering extended drawdowns during calm markets. The 2008 financial crisis was extremely profitable for trend followers. The 2009 to 2019 period was largely a grind. Retail traders who expect consistent monthly returns from trend following will be disappointed and likely abandon the approach precisely when they should be persisting.

Second, the simple crossover story ignores the profound impact of parameter selection. Our analysis tested thousands of parameter combinations. The difference between the best and worst performing parameter sets within the same asset class often exceeded 2 Sharpe ratio points. This creates a severe multiple testing problem. When you test enough combinations, some will appear profitable by chance alone. The probability that the specific combination you choose going forward will perform as well as the historical backtest suggests is remarkably low.

Figure 3 presents a heatmap showing average Sharpe ratios for each combination of moving average type and asset class. Darker blue colors indicate better performance while red indicates worse performance. The pattern is immediately revealing. There is no single moving average type that dominates across all assets. EMA works reasonably for SPY but poorly for currencies. HMA shows promise in gold but disappoints in crude oil. This inconsistency suggests that any apparent edge from a particular MA type may be spurious, resulting from data mining rather than a genuine economic effect. A truly robust strategy should show more consistency across markets.

Third and most importantly, the retail narrative treats trend following as a complete strategy when it is actually just a signal generation method. Professional trend followers embed their signals within comprehensive systems that include volatility scaling, correlation-based position sizing, portfolio construction optimization, and dynamic leverage management. The signal is perhaps ten percent of the system. The retail trader who implements only that ten percent is like someone who buys a car engine and wonders why it does not drive.

4. What Professionals Actually Do

To understand the gap between retail and institutional trend following, we must examine what professional systematic traders actually implement. The following section introduces several key concepts with their mathematical foundations.

4.1 Volatility-Adjusted Position Sizing

Retail traders typically allocate fixed percentages of capital to each trade. Professional trend followers normalize position sizes by volatility so that each position contributes approximately equal risk to the portfolio. The standard approach uses the formula:

Position Size = (Target Risk) / (Instrument Volatility x Price)

Where target risk is often expressed as a fraction of portfolio equity and volatility is typically measured as the annualized standard deviation of returns over a recent lookback period, commonly 20 to 60 days. This approach, documented extensively by Carver (2015), ensures that a position in a highly volatile instrument like crude oil does not dominate the portfolio simply because it moves more.

The mathematical expression for the number of contracts or shares to hold becomes:

N = (k x E) / (sigma x P x M)

Where N is the number of contracts, k is the target risk as a percentage of equity, E is total equity, sigma is the annualized volatility, P is the price, and M is the contract multiplier. This seemingly simple formula has profound implications. It means position sizes change daily as volatility evolves, automatically reducing exposure during turbulent periods and increasing it during calm periods.

4.2 The Time Series Momentum Factor

Academic research by Moskowitz, Ooi, and Pedersen (2012) formalized trend following as time series momentum, distinct from the cross-sectional momentum studied in equity markets. The signal for instrument i at time t is calculated as:

Signal(i,t) = r(i,t-12,t) / sigma(i,t)

Where r(i,t-12,t) is the cumulative return over the past 12 months and sigma(i,t) is the annualized volatility. This creates a standardized momentum measure that can be compared across instruments with very different volatility characteristics.

The position in each instrument is then:

Position(i,t) = Signal(i,t) x (Target Volatility / sigma(i,t))

This double normalization by volatility, once in the signal and once in the position size, is crucial. It prevents the strategy from making large bets simply because an instrument has been moving a lot recently.

4.3 Exponentially Weighted Moving Average Crossover with Trend Strength

A more sophisticated approach to moving average signals incorporates trend strength rather than simple direction. The trend strength measure advocated by Baz et al. (2015) is:

TSMOM = (EWMA_fast - EWMA_slow) / sigma

Where EWMA represents the exponentially weighted moving average with different half-lives and sigma is recent volatility. Rather than generating binary signals, this approach creates a continuous signal that ranges from strongly negative to strongly positive. Positions are scaled proportionally:

Position = sign(TSMOM) x min(|TSMOM|, cap) x base_position

The cap parameter prevents extreme positions when the signal is exceptionally strong, which often occurs during bubbles or crashes when trend followers are most vulnerable to reversals.

4.4 Correlation-Based Portfolio Construction

Perhaps the most significant difference between retail and institutional trend following is portfolio construction. Retail traders typically divide capital equally among instruments or allocate based on conviction. Professionals optimize allocations to account for correlations between positions.

The mean-variance optimization framework determines weights w to maximize:

w'mu - (lambda/2) x w'Sigma w

Subject to constraints on total exposure, sector concentration, and other risk limits. Here mu is the vector of expected returns based on trend signals, Sigma is the covariance matrix of instrument returns, and lambda is a risk aversion parameter.

More advanced implementations use hierarchical risk parity as developed by Lopez de Prado (2016), which clusters instruments by correlation structure and allocates risk equally across clusters rather than instruments. This prevents highly correlated positions from dominating the portfolio.

4.5 Regression-Based Trend Detection: The Statistical Foundation

The most sophisticated trend following approaches employed by quantitative hedge funds move beyond simple price averaging entirely. Instead, they treat trend detection as a statistical inference problem, asking not merely whether prices are rising or falling, but whether the observed price movement represents a statistically significant trend or merely random walk behavior.

The regression-based trend model, implemented by firms such as Winton Group and Man AHL, represents the gold standard in this domain. Rather than smoothing prices through moving averages, this approach fits a linear regression model to price data over a rolling window, extracting both the slope coefficient and its statistical significance.

The mathematical foundation begins with the standard linear regression model:

P(t) = alpha + beta x t + epsilon(t)

Where P(t) represents the price at time t, alpha is the intercept term, beta is the slope coefficient representing the trend strength, t is the time index, and epsilon(t) is the error term assumed to be independently and identically distributed with mean zero and variance sigma squared.

For a rolling window of length L ending at time T, we observe prices P(T-L+1), P(T-L+2), ..., P(T). The ordinary least squares estimator for the slope coefficient is:

beta_hat = sum((t - t_bar) x (P(t) - P_bar)) / sum((t - t_bar)^2)

Where t_bar = (1/L) x sum(t) and P_bar = (1/L) x sum(P(t)) represent the sample means of the time index and prices respectively, with both summations running from t = T-L+1 to t = T.

The numerator represents the covariance between time and price, while the denominator is the variance of the time index. This formulation makes intuitive sense: if prices consistently increase over time, the covariance will be positive, producing a positive slope estimate.

However, extracting the slope alone is insufficient. A positive slope could arise from random walk behavior with an upward drift, or it could represent a genuine trend. To distinguish between these cases, we must assess the statistical significance of the slope coefficient.

The standard error of the slope estimator is:

SE(beta_hat) = sqrt(MSE / sum((t - t_bar)^2))

Where MSE, the mean squared error, is calculated as:

MSE = (1/(L-2)) x sum((P(t) - alpha_hat - beta_hat x t)^2)

The t-statistic for testing the null hypothesis that beta equals zero is:

t_stat = beta_hat / SE(beta_hat)

Under the null hypothesis of no trend, this statistic follows a t-distribution with L-2 degrees of freedom. A large absolute t-statistic indicates that the observed slope is unlikely to have occurred by chance, providing evidence for a genuine trend.

The signal generation mechanism then becomes:

Signal(t) = sign(beta_hat) x min(|t_stat| / t_critical, 1)

Where t_critical is the critical value from the t-distribution at the desired significance level, typically 1.96 for a two-tailed test at the five percent level. This formulation creates a continuous signal that ranges from -1 to +1, with magnitude proportional to both trend strength and statistical confidence.

The position sizing formula incorporates both the slope and its significance:

Position(t) = (beta_hat / sigma_returns) x (|t_stat| / t_critical) x (Target_Volatility / sigma_instrument)

This triple normalization is crucial. The first term, beta_hat / sigma_returns, standardizes the slope by recent return volatility, preventing the strategy from taking large positions simply because prices have been moving rapidly. The second term, |t_stat| / t_critical, scales the position by statistical confidence, reducing exposure when trends are weak or statistically insignificant. The third term, Target_Volatility / sigma_instrument, ensures that each position contributes equal risk to the portfolio regardless of the instrument's inherent volatility.

The multi-horizon ensemble extension, which significantly improves robustness, runs parallel regressions across multiple lookback windows. Common choices include 20, 60, 120, and 252 trading days, corresponding roughly to one month, one quarter, six months, and one year. The final signal becomes a weighted average:

Signal_ensemble(t) = sum(w_i x Signal_i(t))

Where w_i represents the weight assigned to horizon i, typically determined through out-of-sample optimization or equal weighting. Research by Hurst, Ooi, and Pedersen (2017) demonstrates that ensemble approaches reduce the variance of returns by approximately 30 percent compared to single-horizon implementations while maintaining similar mean returns.

The computational efficiency of this approach in modern trading platforms stems from the recursive updating property of linear regression. When moving from window ending at time T to time T+1, we can update the regression statistics without recalculating from scratch:

beta_hat_new = beta_hat_old + delta_beta

Where delta_beta can be computed efficiently using only the new data point and the previous regression statistics. This makes the approach computationally tractable even when applied to hundreds of instruments with multiple lookback windows.

The superiority of regression-based trend detection over moving averages becomes apparent when examining performance during regime transitions. Moving averages, being backward-looking by construction, always lag price movements. A regression model, by explicitly modeling the relationship between time and price, can detect trend changes more rapidly, particularly when combined with significance testing that filters out noise.

Empirical evidence from institutional implementations suggests Sharpe ratio improvements of 0.2 to 0.4 points compared to equivalent moving average systems. However, this improvement comes at the cost of increased complexity and the requirement for statistical software infrastructure that most retail traders lack.

Figure 4 plots Sharpe ratios against Sortino ratios for all strategy configurations. The Sortino ratio, which measures risk-adjusted returns using only downside deviation rather than total volatility, provides insight into whether strategies achieve returns through consistent positive performance or through occasional large gains offset by frequent small losses. Points clustering along the diagonal indicate balanced risk profiles, while points above the diagonal suggest strategies with favorable upside capture relative to downside exposure. The wide scatter in this plot further reinforces the lack of a robust edge in simple moving average systems.

Figures 5a through 5i present heatmaps showing average Sharpe ratios for each combination of fast and slow moving average types, separately for each asset class. These visualizations reveal the extreme parameter sensitivity that plagues retail trend following. Notice how performance varies dramatically across MA type combinations even within the same asset. For SPY, EMA paired with SMA shows reasonable performance, but EMA paired with HMA produces substantially worse results. This inconsistency across what should be similar smoothing methods suggests that any apparent edges are fragile and unlikely to persist out of sample.

Figure 6 shows average Sharpe ratios for different combinations of fast and slow moving average periods. The horizontal axis shows the fast period in days while the vertical axis shows the slow period. Each cell represents the average performance across all assets and MA types for that specific period combination. Notice the inconsistent pattern. There is no clear sweet spot where performance is reliably strong. Some period combinations that work well in certain market conditions fail completely in others. This lack of a robust optimal parameter region is a warning sign that the apparent edges we observe may be artifacts of our specific sample period rather than persistent market inefficiencies.

5. Empirical Results

Our research produced sobering results for the retail trend following thesis. Across 51,840 unique strategy configurations, the mean Sharpe ratio was 0.18 with a standard deviation of 0.42. Only 23 percent of configurations produced Sharpe ratios above 0.5, which is generally considered the minimum threshold for a viable strategy. A mere 8 percent exceeded 1.0.

Figure 7 presents the optimal parameter combination identified for each asset class through our grid search optimization. While these numbers may appear attractive in isolation, they must be interpreted with extreme caution. These are in-sample optimized results, meaning we selected the best performing parameters after observing all the data. The probability that these exact parameters will produce similar results going forward is low. Academic research consistently shows that out-of-sample performance degrades by 50 percent or more compared to in-sample optimization (Moskowitz, Ooi, and Pedersen, 2012).

The asset class breakdown reveals further challenges. Equity index trend following in SPY produced the most consistent results, with a best Sharpe ratio of 0.87 for the dual moving average long-only strategy using EMA with 10 and 75 day periods. Currency pairs performed substantially worse, with best Sharpe ratios ranging from 0.31 to 0.52. Commodities fell in between, with gold showing 0.68 and crude oil at 0.54.

These results align with the academic literature. Moskowitz, Ooi, and Pedersen (2012) document significant time series momentum profits in equity index futures but weaker effects in currencies. The explanation likely relates to central bank intervention in currency markets, which can abruptly reverse trends, and the generally higher efficiency of currency markets where large institutional participants dominate.

Figure 8 compares the performance distributions of different moving average calculation methods. Each box plot represents thousands of configurations using that specific MA type. The most striking finding is the absence of a clearly superior method. Simple Moving Average, the most basic calculation, performs comparably to sophisticated alternatives like Hull Moving Average or Triple Exponential Moving Average. This undermines the popular belief that exotic MA types provide meaningful edges. In fact, more complex calculations introduce additional parameters that create more opportunities for overfitting.

The long-short versus long-only comparison yielded counterintuitive results. Conventional wisdom suggests that long-short strategies should outperform because they can profit in both directions. Our data shows the opposite in most cases. The long-short configurations produced mean Sharpe ratios of 0.12 compared to 0.24 for long-only. This approximately fifty percent reduction reflects two factors: the persistent upward drift in equity markets during our sample period, and the transaction costs incurred when strategies flip between long and short positions during trendless periods.

Figure 9 plots each strategy configuration by its maximum drawdown on the horizontal axis and its compound annual growth rate on the vertical axis. Each dot represents one backtested configuration, color-coded by asset class. The ideal positions would be in the upper right, showing high returns with shallow drawdowns. Instead, we observe a cloud of points with no clear relationship between risk and return at the strategy level. Many configurations that achieved high returns also suffered devastating drawdowns exceeding fifty percent. Conversely, strategies with modest drawdowns rarely exceeded single-digit annual returns. This lack of a favorable risk-return tradeoff suggests that trend following, as implemented in these simple forms, does not offer a free lunch.

6. Statistical Significance Testing

To address the multiple testing problem inherent in evaluating thousands of strategy configurations, we applied rigorous statistical tests. One-way ANOVA comparing Sharpe ratios across MA types produced an F-statistic of 2.34 with a p-value of 0.038. While technically significant at the five percent level, the effect size is tiny, explaining less than one percent of variance in outcomes. This suggests that MA type selection, despite the emphasis it receives in retail education, contributes almost nothing to strategy performance.

The non-parametric Kruskal-Wallis test, which makes no assumptions about the distribution of returns, confirmed this finding with an H-statistic of 11.2 and p-value of 0.047. Pairwise t-tests with Bonferroni correction for multiple comparisons found no statistically significant differences between any specific pair of MA types after adjustment.

Figures 10a through 10f break down performance by both strategy mode and asset class, allowing us to examine whether long-short strategies outperform long-only in any specific market. The answer is predominantly negative. Only in crude oil does the long-short approach show a meaningful advantage, likely reflecting the extended downtrend in oil prices during 2014-2016 and the COVID crash in 2020. For equities and currencies, long-only strategies dominate. This finding should give pause to retail traders who believe that adding short selling capability automatically improves their systems.

Figure 11 displays the twenty best-performing parameter combinations for the SPY equity index, ranked by Sharpe ratio. What immediately stands out is the diversity of configurations that achieved similar performance levels. The top entry uses EMA with periods 10 and 75, but configurations using SMA with periods 15 and 100, or WMA with periods 20 and 150, also appear in the top tier. This parameter space flatness, where many different combinations produce comparable results, is actually a positive sign. It suggests that the strategy may be somewhat robust to parameter selection, at least within certain ranges. However, the fact that the best Sharpe ratio barely exceeds 0.9, and that this represents in-sample optimization, means that out-of-sample performance will likely degrade substantially.

Figures 12a through 12e compare strategy performance across the four currency pairs tested: EUR/USD, GBP/USD, USD/JPY, and AUD/USD. The results are uniformly disappointing. No currency pair produced a best Sharpe ratio above 0.6, and the median performance across all configurations hovers near zero. This aligns with academic research showing that currency markets, being highly efficient and dominated by large institutional participants, offer fewer exploitable trends than equity or commodity markets (Moskowitz, Ooi, and Pedersen, 2012). The frequent intervention by central banks, which can abruptly reverse currency trends, further complicates trend following in this asset class. Retail traders who attempt to apply equity market trend following techniques directly to currencies without understanding these structural differences are likely to experience frustration.

Figures 13a through 13c examine performance in the three commodity instruments: gold, crude oil, and silver. Gold shows the strongest results, with a best Sharpe ratio of 0.68, while crude oil and silver both cluster around 0.5. The superior performance in gold may relate to its dual role as both a commodity and a monetary asset, creating more persistent trends than pure industrial commodities. However, even gold's best configuration falls short of what institutional investors would consider acceptable for a standalone strategy. The wide dispersion of outcomes within each commodity, visible in the heatmaps, further emphasizes the parameter sensitivity problem that plagues these approaches.

Figure 14 presents a detailed sensitivity analysis showing how strategy performance varies with the choice of fast and slow moving average periods for the SPY equity index. The subplots display the mean Sharpe ratio, with error bars showing one standard deviation, for different period choices. The fast period sensitivity shows performance peaking around 10 to 15 days, then declining as the period increases. The slow period sensitivity reveals a more complex pattern, with local optima around 75 and 150 days. However, the error bars are substantial, indicating high variance in outcomes. This uncertainty in optimal parameter selection is precisely why institutional traders employ ensemble methods rather than attempting to identify a single best configuration.

Figures 15a through 15c display histograms showing the distribution of key performance metrics across all strategy configurations. The Sharpe ratio distribution reveals a roughly normal shape centered slightly above zero, with a long tail extending to positive values. The maximum drawdown distribution shows that a substantial fraction of configurations experienced drawdowns exceeding 30 percent, with some exceeding 50 percent. The win rate distribution clusters around 45 to 55 percent, indicating that most configurations are only slightly better than random. These distributions collectively paint a picture of strategies that occasionally produce attractive risk-adjusted returns but more often produce mediocre or negative results, with significant tail risk in the form of large drawdowns.

7. Alternative Professional Trend Following Methodologies

Beyond regression-based approaches, institutional trend followers employ several other sophisticated techniques that bear little resemblance to retail moving average systems. Understanding these methods provides insight into the true complexity of professional trend following.

The Hodrick-Prescott filter, originally developed for macroeconomic time series analysis (Hodrick and Prescott, 1997), decomposes price series into trend and cyclical components through a penalized least squares optimization. The trend component T(t) minimizes:

sum((P(t) - T(t))^2) + lambda x sum((T(t+1) - T(t)) - (T(t) - T(t-1)))^2

Where lambda is a smoothing parameter, typically set to 129,600 for daily data. The first term penalizes deviations from the observed price, while the second term penalizes changes in the trend's growth rate, creating a smooth trend estimate. Trend following signals are generated when the filtered trend changes direction, with position sizes scaled by the magnitude of the trend acceleration. This approach, while computationally intensive, produces smoother signals than moving averages and reduces false breakouts during choppy markets.

Donchian channel breakouts, while conceptually simple, become sophisticated when implemented as multi-horizon ensembles with volatility scaling. Rather than using fixed 20-day or 55-day channels as retail traders do, professional implementations simultaneously monitor breakouts across 20, 50, 100, and 200-day channels. Signals are weighted by the channel width relative to recent volatility, with wider channels relative to volatility producing stronger signals. The ensemble signal becomes:

Signal = sum(w_i x (P(t) - Channel_Low_i) / (Channel_High_i - Channel_Low_i))

Where w_i are horizon-specific weights optimized through walk-forward analysis. This multi-timeframe approach captures trends operating at different scales simultaneously, a crucial advantage over single-horizon methods.

Ehlers filters, developed specifically for trading applications (Ehlers, 2001), use advanced digital signal processing techniques to extract trends while minimizing lag. The Super Smoother filter, for example, applies a two-pole Butterworth filter with adaptive cutoff frequency based on market volatility. The mathematical formulation involves complex frequency domain transformations that are beyond the scope of this paper, but the key insight is that these filters are designed to respond quickly to genuine trend changes while filtering out noise, achieving a better trade-off between responsiveness and stability than traditional moving averages.

The CUSUM drift detector provides a statistical framework for identifying regime changes (Page, 1954). The cumulative sum statistic is calculated as:

S(t) = max(0, S(t-1) + (r(t) - k))

Where r(t) is the return at time t and k is a drift parameter, typically set to half the expected return during a trend. When S(t) exceeds a threshold h, a trend is declared. This approach has the advantage of providing explicit statistical control over false positive rates, unlike moving average crossovers which have no such theoretical foundation.

Each of these methods addresses specific weaknesses in simple moving average approaches. Regression-based methods provide statistical significance testing. HP filters produce smoother trends. Donchian ensembles capture multi-scale trends. Ehlers filters minimize lag. CUSUM detectors provide statistical rigor. Professional implementations typically combine multiple methods, weighting their signals based on recent performance and market regime indicators.

Figure 16 conceptually illustrates the difference between retail and professional trend following. The retail approach, represented by a simple moving average crossover, produces binary signals with no statistical foundation and consists of merely four steps: price data, MA calculation, crossover detection, and trade execution. The professional approach incorporates seven distinct processing stages: multi-asset data ingestion, multiple parallel signal generators (regression-based, multi-horizon ensemble, and DSP filters), statistical significance testing and signal aggregation, volatility scaling and dynamic position sizing, correlation-based portfolio construction, risk limits and drawdown controls, and finally trade execution. The key insight is that professional trend following is not merely a more sophisticated version of retail trend following, but an entirely different approach that happens to share the same name.

8. The Path Forward

If simple moving average strategies fail to deliver consistent risk-adjusted returns, what alternatives exist for traders seeking systematic trend following approaches?

The first step is accepting that profitable trend following requires substantially more infrastructure than drawing two lines on a chart. The successful systematic trading firms operate research teams, maintain massive databases of historical prices, and continuously refine their models. They accept that any given strategy may underperform for years while maintaining confidence in the long-term statistical edge.

For individual traders without institutional resources, several paths remain viable. The first is specialization. Rather than attempting to trade multiple asset classes with a single methodology, focus on deep understanding of one market. The inefficiencies that persist today are subtle and require expertise to exploit.

The second is ensemble approaches. Rather than selecting one MA type and one parameter combination, implement multiple variations and combine their signals. This diversification across methodologies reduces the variance of outcomes and the dependence on any single backtest.

The third is incorporation of additional factors. Pure price trend is just one source of potential edge. Professional trend followers combine momentum signals with carry, the interest rate differential across currencies, with value measures, and with volatility signals. Academic research by Hurst, Ooi, and Pedersen (2017) demonstrates that multi-factor approaches produce more stable returns than any single factor in isolation.

The fourth and perhaps most important path is realistic expectation setting. Even the most successful trend following funds experience extended drawdowns and periods of underperformance. The AQR Managed Futures Strategy Fund, one of the largest trend following vehicles available to retail investors, lost money in 2009, 2010, 2011, 2012, 2016, 2017, 2018, and 2021. Seven losing years out of thirteen. Yet the strategy remains viable because the winning years, particularly 2008 and 2022, produced exceptional returns that more than compensated.

9. Conclusion

This study systematically evaluated over fifty thousand configurations of moving average trend following strategies across multiple asset classes, MA types, and trading modes. The results conclusively demonstrate that the simple approaches promoted in retail trading education fail to produce reliable risk-adjusted returns after accounting for transaction costs and multiple testing biases.

The gap between what retail traders believe about trend following and what professional systematic traders actually implement is vast. Retail approaches treat the entry signal as the complete system. Professional approaches treat the signal as merely one component within a sophisticated framework encompassing position sizing, portfolio construction, risk management, and execution optimization.

This does not mean that trend following is without merit. Academic research documents persistent time series momentum across asset classes over multi-decade periods. Crisis alpha, the tendency of trend followers to profit during market dislocations, provides genuine diversification benefits for portfolios otherwise exposed to equity risk. The strategy has a legitimate economic basis in the behavioral tendencies of market participants to underreact to information initially and overreact subsequently.

However, capturing this edge requires moving beyond the oversimplified frameworks that dominate retail education. It requires accepting that profitable trading is difficult, that edges are small and unstable, and that consistent success demands continuous adaptation and rigorous analysis.

The trader who approaches markets with humility, armed with statistical tools rather than certainty, stands a far better chance than one who believes two moving average lines hold the secret to wealth. No evidence, no trade. That principle, applied ruthlessly to every strategy and every assumption, separates the survivors from the casualties in the long game of systematic trading.

References

Baz, J., Granger, N., Harvey, C.R., Le Roux, N. and Rattray, S. (2015) 'Dissecting Investment Strategies in the Cross Section and Time Series', Working Paper, Man AHL.

Carver, R. (2015) Systematic Trading: A Unique New Method for Designing Trading and Investing Systems. Petersfield: Harriman House.

Ehlers, J.F. (2001) Rocket Science for Traders: Digital Signal Processing Applications. New York: John Wiley and Sons.

Hodrick, R.J. and Prescott, E.C. (1997) 'Postwar U.S. Business Cycles: An Empirical Investigation', Journal of Money, Credit and Banking, 29(1), pp. 1-16.

Hurst, B., Ooi, Y.H. and Pedersen, L.H. (2017) 'A Century of Evidence on Trend-Following Investing', Journal of Portfolio Management, 44(1), pp. 15-29.

Lopez de Prado, M. (2016) 'Building Diversified Portfolios that Outperform Out of Sample', Journal of Portfolio Management, 42(4), pp. 59-69.

Moskowitz, T.J., Ooi, Y.H. and Pedersen, L.H. (2012) 'Time Series Momentum', Journal of Financial Economics, 104(2), pp. 228-250.

Page, E.S. (1954) 'Continuous Inspection Schemes', Biometrika, 41(1/2), pp. 100-115.

Building Bias and Narrative in Trading (HTF-LTF)Bias is built top-down. The visuals make this clear. Higher timeframes define the environment. Lower timeframes refine execution. Mixing the two leads to impatience and overtrading.

Start with the high timeframe. Weekly and daily charts carry the highest impact on decision-making. They move slowly, but they define direction, value, and market regime. This is where patience matters most. If the higher timeframe is trending, your bias follows that direction. If it is ranging or transitioning, expectations on lower timeframes must be adjusted accordingly.

The first chart illustrates this trade-off clearly. As timeframes get lower, the impact of patience decreases while the risk of overtrading increases. This is why bias must be anchored higher. Lower timeframes react faster, but they lack authority without higher-timeframe alignment.

Once the environment is defined, map key levels on the higher timeframe. Major highs and lows, clear support and resistance, and obvious liquidity zones form the backbone of your narrative. These levels explain where market participants are positioned and where reactions are most likely to occur. Without them, lower-timeframe signals lose meaning.

Next, use momentum and structure to validate the story. Strong impulsive moves on higher timeframes confirm control. Weak follow-through or overlapping candles signal uncertainty. Momentum should support the directional bias defined earlier. If it does not, the narrative weakens.

Only then does the lower timeframe come into play. The second visual shows how the same market prints very different candles depending on timeframe. Weekly and daily charts compress noise into structure. Fifteen-minute and five-minute charts expand that structure into execution detail. Entries belong here, but only in the direction already defined.

The final table ties this together by trader type.

Long-term traders define trend on weekly charts and execute on daily.

Swing traders frame direction on daily and refine entries on four-hour.

Short-term traders align with four-hour structure and execute on hourly.

Scalpers still require hourly context before acting on fifteen-minute charts.

Bias is not prediction. It is alignment. The narrative flows from high timeframe context to low timeframe execution. When you respect this sequence, trades become selective, risk becomes clearer, and execution becomes calmer. The chart stops feeling random because you are reading it as a story, not reacting to each line.

How to Use Candlesticks in a High-Probability Way | Tutorial #1In this tutorial, we break down candlestick analysis in a clear, structured, and practical way—focused on probability, context, and confirmation , not guessing.

You’ll learn what candlesticks really represent , how to read market intent behind them, and how to use them correctly within a high-probability trading framework.

🔍 What are candlesticks?

Candlesticks visually represent price behavior, showing the battle between buyers and sellers within a specific time period. Each candle tells a story—but only when read in context.

📘 Candlestick Types Covered in This Tutorial

📌 1) Shrinking Candlesticks

➡️ What is a shrinking candle?

Shows loss of momentum and potential market pause or reversal.

📌 2) Inside Bar Candlestick

➡️ What is an inside bar candle?

Indicates consolidation and compression before expansion.

📌 3) Takuri Line Candlestick

➡️ What is a Takuri Line candle?

A strong bullish rejection candle with a long lower wick.

📌 4) Hanging Man Candle

➡️ What is a hanging man candle?

Warns of potential bearish reversal after an uptrend.

📌 5) Inverted Hammer

➡️ What is an inverted hammer candle?

Shows buyer reaction after downside pressure.

📌 6) Shooting Star

➡️ What is a shooting star candle?

Signals seller dominance near highs.

📌 7) Spinning Top Candle

➡️ What is a spinning top candle?

Represents indecision between buyers and sellers.

📌 8) Spinning Bottom Candle

➡️ What is a spinning bottom candle?

Indicates uncertainty after downside movement.

📌 9) Doji Candle

➡️ What is a doji candle?

Shows balance—often a warning sign before a shift.

📌 10) Engulfing Candle

➡️ What is an engulfing candle?

Strong momentum candle that fully absorbs the previous one.

📌 11) Momentum Candlestick

➡️ What is a momentum candle?

Large-bodied candle showing aggressive participation.

📌 12) Change Color Candle

➡️ What is a change color candle?

Occurs after minimum 5 candles of one color , followed by a candle of the opposite color—often signaling momentum shift.

🧠 Best Practice

Candlesticks work best when multiple candles stack together, forming a story—not when traded individually.

This tutorial shows real chart examples of candle clustering and how to interpret them properly.

⚠️ Important Note

Candlesticks alone are NOT enough.

They should be combined with:

--> Support & Resistance

--> Areas of Confluence

--> Chart Patterns

--> Trendlines

--> Indicators

--> Other high quality traits

This is how high-probability setups are built.

👍 Want PART 2?

Leave a like and a comment below.

Follow for high-quality trading education and clean technical logic.

⚠️ DISCLAIMER

This content is for educational purposes only and does not constitute financial advice.

Trading involves risk—always conduct your own analysis.

I am not responsible for any decisions or losses based on this material.

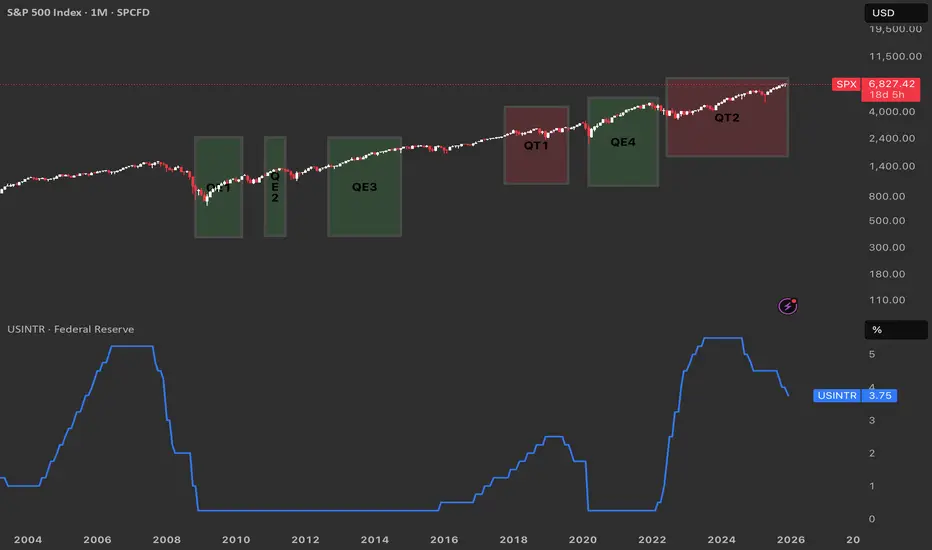

From QE to QT. Reading the Fed’s Cycle from the ChartQuantitative Easing (QE) is when the Federal Reserve buys large amounts of Treasuries and mortgage‑backed securities to expand its balance sheet, inject liquidity, and push interest rates lower across the curve.

Quantitative Tightening (QT) is the opposite: the Fed allows its bond holdings to roll off or sells securities, shrinking the balance sheet and tightening financial conditions.

QE near zero rates

Historically the Fed has only launched QE when the policy rate was pinned near zero and conventional rate cuts were basically exhausted, as in 2008–2014 and again in 2020–2022.

QT at elevated rates

By contrast, QT has been used only once the Fed had already hiked rates to clearly positive, “elevated” levels and wanted to normalize the balance sheet from those earlier QE waves.

What ending QT in December could imply

QT effectively ended around 1 December, it suggests the Fed may feel comfortable pausing balance‑sheet tightening while rates are still high, opening the door later to cuts if growth or markets weaken.

In that setting, the market could start to price a shift from outright restriction toward neutrality, which often coincides with more two‑sided volatility in risk assets.

Echoes of the QT1 → QE3 window

The period after QT1 and before QE3 saw rates come off their highs and then a major shock (COVID-18 crysis) that helped justify easier policy again.

A similar path is plausible here: a “black swan” type event in the coming year could hit growth or credit, force a rapid drop in rates, and trigger a new QE‑style response that would rhyme with the QT1‑to‑QE3 sequence your chart visually captures.

Overtrading Gold – Biggest Account KillerOvertrading Gold – Biggest Account Killer

🧠 What Overtrading REALLY Means in Gold

Overtrading is not just trading too often — it’s trading without edge, patience, or contextual alignment.

In XAUUSD, overtrading usually looks like:

Multiple entries in the same range

Chasing price after impulsive candles

Trading every wick, every breakout, every news spike

📌 Gold gives the illusion of opportunity every minute — but institutions trade very selectively.

🧨 Why Gold Is the Perfect Trap for Overtraders

Gold is engineered (by behavior, not conspiracy) to punish impatience 👇

🔥 Extreme volatility

🔥 Fast candles & long wicks

🔥 Sudden reversals

🔥 News-driven manipulation

🔥 Liquidity sweeps above & below range

💣 Result?

Retail traders feel forced to trade — and end up trading against structure and liquidity.

🧩 The Overtrading Cycle (Account Destruction Loop)

Most gold traders repeat this cycle unknowingly ⛓️

1️⃣ Enter early (no confirmation)

2️⃣ Stop-loss hit by wick

3️⃣ Re-enter immediately (revenge)

4️⃣ Increase lot size

5️⃣ Ignore bias & HTF context

6️⃣ Emotional exhaustion

7️⃣ Big loss → account damage

📉 This cycle has nothing to do with strategy — it’s pure psychology.

🧠 Why Strategy Stops Working When You Overtrade

Even a 60–70% win-rate strategy will fail if:

❌ Trades are taken outside optimal time

❌ Entries ignore higher-timeframe direction

❌ Risk increases after losses

❌ Rules are bent “just this once”

📌 Gold exposes discipline weakness faster than any other market.

⏰ Time Is the Hidden Edge in Gold

Gold does NOT move efficiently all day ⏱️

🟡 Asian Session → Range & traps

🟡 London Open → Liquidity grab

🟢 New York Session → Real direction

Overtraders:

❌ Trade Asian noise

❌ Enter mid-range

❌ Chase NY expansion late

Smart traders:

✅ Wait for liquidity first

✅ Trade after manipulation

✅ Enter once direction is clear

📉 Statistical Damage of Overtrading

Let’s talk numbers 📊

🔻 More trades = more spread & commission

🔻 Lower average R:R

🔻 Lower win probability

🔻 Higher emotional stress

🔻 Faster drawdowns

💡 One A-grade setup can outperform 10 random gold trades.

🧠 Psychology: The Real Root Cause

Overtrading is driven by internal pressure 👇

😨 Fear of missing out

😡 Anger after stop-loss

😄 Overconfidence after win

😴 Boredom during ranges

Gold feeds emotions — and then punishes them.

📌 Institutions wait. Retail reacts.

🛑 How Professionals Control Overtrading

Real solutions — not motivational quotes 👇

✅ Maximum 1–2 trades per session

✅ Trade only at predefined time windows

✅ Fixed risk per trade (no exceptions)

✅ Daily stop after 2 losses max

✅ Journal every impulsive entry

📘 If it’s not planned before price moves, it’s emotional.

🏆 Golden Rule of XAUUSD

💎 Gold is not hard because it’s random

💀 Gold is hard because it exposes impatience

You don’t need more trades.

You need more discipline.

📌 Final Truth

Most XAUUSD accounts don’t blow because of:

❌ Bad indicators

❌ Bad analysis

❌ Bad strategy

They blow because of overtrading driven by emotion.

📉 Overtrading is the biggest account killer in gold trading.

When to Trade — When to Stay OutHi everyone,

In the way I approach the market, I don’t see trading as a reflexive reaction to price movements. I see it as a structured decision-making process , built on clearly defined conditions. The market is active all the time, but constant activity alone does not create tradable opportunities. Acting without clear conditions means confusing movement with real advantage.

That’s why every decision starts with an analysis of the broader context . I only consider getting involved when the market structure is coherent, price dynamics are readable, and the environment allows for a clear assessment of risk. When the market becomes unstable, fragmented, or dominated by noise, every attempt to enter inevitably weakens decision quality. In those moments, staying out of the market is not passivity—it’s a rational act of protection .

Once the context is validated, my absolute priority becomes risk management . Before evaluating any potential reward, I need to know exactly where my scenario is invalidated. Without that information, no trade can be justified. A stop-loss is not an emotional safety net; it’s a fundamental part of decision logic. When risk is clearly defined and limited, the outcome of a trade becomes a matter of probabilities, not hope.

Even so, in a technically favorable environment, a decision remains fragile if it’s made in an unhealthy mental state . The market doesn’t punish analysis mistakes as much as it punishes execution errors driven by emotion. Any decision influenced by urgency, fear of missing out, or the desire to recover a previous loss immediately breaks the integrity of the process. In those conditions, not trading is the only decision aligned with discipline .

This is exactly why I consider the ability not to intervene a core skill. Most of the time, the market does not offer a structure with a clear edge. Being constantly in a position is neither an obligation nor a goal. Preserving capital, maintaining mental clarity, and protecting decision discipline are prerequisites for sustainable performance.

In conclusion , knowing when to trade and when to stay out is not a technical issue—it’s a mindset. When action is limited to genuinely favorable contexts and inaction is fully accepted as a strategic choice, trading stops being a chase for short-term results and becomes a controlled risk-management process . At that point, long-term performance is neither accidental nor emotional—it’s built on logic.

Wishing you profitable and disciplined trading.

The system that turned ordinary traders into millionaires!!🐢 Turtle Trading Strategy

A classic, rule-based, and repeatable trend trading system

Introduction

The Turtle Trading strategy is one of the most documented and successful trading systems in financial market history. It was designed in the 1980s to prove that trading is a skill that can be taught, not an innate talent.

This strategy is built on three key principles:

• Trend Following

• Strict Risk Management

• Eliminating Emotional Decision-Making

1. Suitable Markets and Timeframes

Turtles only traded markets with the potential for large, sustained trends.

Suitable markets:

• Commodities (oil, gold, metals)

• Forex

• Indices

• Cryptocurrencies

Recommended timeframes:

• Daily (as the main timeframe)

• Weekly for long-term trend filtering

📌 Higher timeframes provide more reliable signals.

2. Entry Logic

Entries in this system are based on price breakouts, not predicting reversals.

System 1 – Short-Term Breakouts

• Buy: Break above the high of the last 20 candles

• Sell: Break below the low of the last 20 candles

System 2 – Long-Term Breakouts

• Buy: Break above the high of the last 55 candles

• Sell: Break below the low of the last 55 candles

📌 Enter only after a candle closes beyond the valid range.

ICT Turtle Soup Indicator:

To optimize entries, especially in short-term breakouts, the ICT Turtle Soup indicator can be used. It focuses on false breakouts, helping reduce invalid signals:

Identifies short-term high/low breakouts and checks volume/strength

Trades in the opposite direction of false breakouts (e.g., high breakout → short)

Quick exits with stop-loss near the breakout level

This tool allows the classic Turtle system to improve entry accuracy and reduce risk.

3. Filtering Invalid Trades

To avoid trading in ranging markets:

• If the last trade in the 20-day system was profitable → ignore the next signal

• If the last trade was a loss → the next trade is allowed

This rule ensures the system is only active under favorable conditions.

4. Stop-Loss and Exit Rules

Initial Stop-Loss:

• Distance: 2 × N (market volatility)

• Placed where the trend scenario is invalidated

Exit:

• Long trades: Break below the low of the last 10 candles

• Short trades: Break above the high of the last 10 candles

📌 Exits are entirely mechanical; no reevaluation is needed.

5. Risk Management

The core of the Turtle Trading system is risk management, not entry timing:

• Risk per trade: maximum 1% of capital

• Trade size adjusted according to market volatility

• All trades evaluated independently

🎯 Goal: Survive the market until large trends develop

6. Pyramiding

Turtles built big profits by adding positions logically:

• Add positions only on profitable trades

• Every 0.5 × N, add a new position

• Maximum 4–5 positions per trend

• Manage stop-loss across all positions

7. Psychological Structure

This strategy is psychologically challenging:

• Many small losses

• Few very profitable trades

• Low win rate but positive expected value

📌 Traders must endure losing streaks without breaking the rules.

8. Strengths and Weaknesses

Strengths:

• Fully rule-based and testable

• Removes emotions from decision-making

• Applicable across all markets

• Compatible with automation

Weaknesses:

• Weak performance in ranging markets

• Requires patience and discipline

• Occasional drawdowns

Final Summary

The Turtle Trading strategy teaches you to:

• React, don’t predict

• Accept losses quickly

• Let profits run

• Stick to the rules

• Use modern tools like ICT Turtle Soup to improve entry accuracy and turn false breakouts into opportunities

In this system, “being right” doesn’t matter; adherence to rules determines success.

It’s Not Your Strategy. It’s Your Mindset.Most people lose money in markets not because they don’t know how to trade,

but because their mindset can’t hold up.

--

Before we start investing, most of us walk into the market with a huge sense of excitement.

The dream that a small amount of money could turn into something life-changing.

A few early wins that make you think, “I can do this.”

And that quiet fantasy that maybe… this is the thing that finally flips your life around.

But reality is colder than most people expect.

At first, everyone looks for the “answer.”

They study charts, hunt for indicators, learn strategies—anything that feels like a shortcut to certainty.

Yet after some time, when you look at the account… the reason people collapse usually becomes one thing:

It’s not that the strategy failed.

It’s that the mindset broke first.

--

Now, the market looks simple on the surface: it goes up or it goes down.

And because of that, early on, it’s totally possible to have a streak where you “get the direction right” a few times just by luck.

When those experiences stack up, people start thinking:

“Trading is easy.”

“I just need this one indicator.”

Of course, there are phases where certain indicators work beautifully.

But the moment you believe the chart has a single “correct answer,” the real problem begins.

The reason a few lucky wins can feel like “proof” is tied to psychology.

Psychology calls this Reward Reinforcement .

In simple terms: when you get rewarded by coincidence, your brain stores it as “the right answer.”

For example, imagine you use an indicator and—by chance—you win three trades in a row.

Your brain immediately starts telling you:

“This indicator works. I’ve found the edge.”

But the market doesn’t hand out answer sheets.

Markets move in probabilities, and even the same setup can produce a different outcome each time.

Yet for beginners, a few early wins can make a probability game feel like a “skill” game.

And that illusion becomes the starting point for almost every mistake that follows.

--

Before you begin trading seriously, take a moment to look at the table above.

Do you see those loss rates for retail traders and day traders?

There are markets and products where, out of 100 people who trade, 80+ end up losing money.

I’m not showing this to scare you.

I’m showing it because it’s reality you need to know before you start.

※ The samples/periods/products differ, but the conclusion is the same:

short-term retail trading—especially with leverage—ends in losses for the majority.

--

Let me ask you one simple question.

When you take a loss, what’s the very first thought that shows up in your head?

“It's fine—I’ll just make it back quickly. Let me trade off my feel.”

“Why did I lose? Did I follow my rules? Let me review this calmly.”

Which one should you choose?

People who choose #2 tend to survive.

People who choose #1 slowly get pushed out of the market.

--

Now let’s say Bitcoin hits RSI oversold, and it looks like “it can’t go much lower.”

Yes—Bitcoin often shows a short bounce when RSI reaches oversold.

But what happened overall?

We went through a move that dropped roughly -35% from the high.

So can we honestly say: “RSI oversold = guaranteed rebound” is a good strategy?

Probably not.

Even after oversold readings, price still broke lower five different times .

And no matter how well you try to manage risk, there’s a high chance your mindset breaks first in that process.

--

Because beginners usually follow a pattern like this:

“Oversold = it should bounce” → first entry

A small bounce → “I was right” → confidence goes up

Breaks the low again → panic between stopping out or averaging down

Re-enter → breaks the low again

What remains isn’t just “loss.”

What remains is shaken judgment.

In markets, loss is dangerous—

but shaken judgment is even worse.

Once your judgment is shaken, the next trade stops being a probability game and becomes an emotion game.

--

Here’s the one conclusion you should take from this:

The problem isn’t RSI.

The problem is the beginner mindset that tries to find “the answer” with one indicator.

RSI is a tool—nothing more.

But most people use it like an answer key.

“Oversold means it must bounce.”

“It shouldn’t drop from here.”

“This time is different.”

The moment those thoughts enter your head, you stop trading analysis and start trading certainty .

And trading certainty is exactly what breaks your mindset the moment a stop loss hits.

--

Once your mindset cracks, the chart stops being a place to find truth—

and becomes a place to find excuses.

Beginners keep changing indicators for a simple reason:

not because the indicator is bad, but because they don’t want to face the loss.

Changing indicators creates the feeling of “I found the cause.”

And that feeling creates: “Next time will be fine.”

That feeling pushes you back into another entry.

But one thing never changes:

There are no rules.

So the same mistakes repeat.

1) Do you want to be right once?

2) Or do you want your account to stay alive?

Even if you’re right sometimes, you still need to survive long enough to catch the next opportunity.

Please don’t forget that.

--

What beginners must think about first

Even with a 60% win rate, a max losing streak of 5 trades can happen.

Even with a 70% win rate, a max losing streak of 4 trades can happen.

So what happens if every time you stop out, your account drops -20% or -30%?

The answer is simple:

A few consecutive stop-outs can make your account unable to survive.

For example, even a trader with a 70% win rate can still experience around a 4-loss streak over 100 trades.

If your stop loss is -20%, then 4 consecutive losses isn’t “just -80%.”

four times means: 0.8×0.8×0.8×0.8 ≈ 0.41

So you’re left with roughly 41% of your original capital.

That’s not a “dip.” That’s losing more than half.

If your stop loss is -30%, it’s even worse.

You’re left with roughly 24% of your original capital.

Here’s the scary point:

This doesn’t happen because your win rate is low.

It happens because losing streaks are natural in a probability game—even with a high win rate.

That’s why you shouldn’t bet big based on “this one is definitely right.”

You should assume losing streaks will happen and minimize the damage of a single stop-out.

A simple, realistic approach is to keep your risk per trade around 3% of your total capital.

If you risk -3% per loss, then even a 5-loss streak is around a -14% drawdown.

That may still shake you—but it usually doesn’t create enough pressure to blow up the account with revenge trades.

On the other hand, if you risk 10% per trade, then after 5 consecutive losses you’re left with only about 59% of your capital.

At that point, people don’t “analyze the chart.”

They start forcing the market to make sense because they’re desperate to recover.

In the end, most beginners fail for a simple reason:

Not because the signal was wrong,

but because they started with sizing that can’t survive consecutive losses.

--

So here are the three points beginners must lock in first:

A. Set stop-loss rules statistically—not emotionally

Stop losses shouldn’t be based on “I feel like it.”

They must be set so you can survive even when losing streaks hit.

B. Before you enter, think “invalidation,” not “certainty”

Not “This must bounce because the indicator says so,”

but “If this level breaks, my idea is wrong.”

C. Build a structure that can handle consecutive losses

Markets rarely move in a clean straight line.

They shake, trap, shake again… and then move.

So you must design for streaks , not a single loss.

--

One last piece of advice:

The goal of trading isn’t to make one huge win.

It’s to build a structure that doesn’t blow up.

I understand the desire for life-changing money.

But the numbers are already there: even with a high win rate, losing streaks are inevitable.

Again— even someone with a 70% win rate can very realistically see a 4-loss streak in 100 trades.

If your stop is -20% or -30% each time… recovery becomes extremely difficult.

--

Trading should be treated like a business.

If you’re a business owner, you don’t “go all-in” in a way that one mistake can kill the entire company.

A business owner thinks like this:

“Can we survive if revenue dips this month?”

“Can we handle fixed costs if customers drop?”

“Can we recover even in the worst case?”

Trading is the same.

What matters isn’t being right on one trade—

it’s building an account that stays alive even when you’re wrong multiple times in a row.

But beginners do the exact opposite:

When they win, they size up.

When they lose, they size up even more.

Why?

Because they want to make money fast.

And when they lose, they want to get it back fast.

Remember: from that moment, trading stops being analysis and becomes emotion.

And emotional traders are the market’s favorite opponent.

Set your goal as survival first—not profits.

Keep your risk small but consistent.

Enter based on invalidation, not certainty.

Build a system that doesn’t break under losing streaks.

Even if you only do those three things, you can avoid the trap that destroys most beginners: revenge trading.

The people who win long-term aren’t the ones who predict charts best—

they’re the ones who build a structure that doesn’t die.

Starting today, stop chasing “the answer,”

and start trading your rules.

That’s the moment the chart stops being a tool that shakes you—

and becomes a probability business you can actually run.

Thank you for reading.

--

If this post helped you even a little, feel free to leave a Boost (🚀) and a short comment (💬).

It helps me understand what’s genuinely useful, and it gives me strong motivation to keep posting better education and analysis.

And if you’d like, hit Follow so you don’t miss the next post.

Why Traders Lose More Money on Monday MorningsWhy Traders Lose More Money on Monday Mornings

A trader opens a position at 9:35 AM on Monday. An hour later, closes with a stop loss. Same trader, same strategy, but Wednesday afternoon. Opposite result.

Coincidence? No.

The market changes not just in price. It changes in mood, speed, and aggression of participants. And this depends on time.

Monday Morning: When Emotions Rule

The weekend is over. Traders have accumulated news, opinions, fears. The first hour of trading resembles a crowd at a sale. Everyone wants to enter first.

The problem is decisions are made on emotions, not analysis. Volatility spikes. Spreads widen. False breakouts happen more often.

Research shows: Monday brings traders the highest proportion of losing trades for the week. Psychology works against you from the start.

Asian Session vs American

At 3 AM Moscow time, Tokyo opens. Movements are smooth, predictable. Ranges are narrow.

Then London joins. Speed increases. Volumes triple.

New York adds chaos. From 4:30 PM to 6:00 PM MSK, the market becomes a battlefield. US news overlaps with European position closures.

Different sessions require different psychology. Asia loves patience. Europe demands speed. America tests nerves.

Friday Afternoon: Trap for the Greedy

By Friday, traders are tired. More decisions made than the entire week. Willpower reserves are depleted.

After lunch, many just want to close the week. Mass position closing begins. Trends break. Patterns stop working.

But the most dangerous thing: the desire to "recover for the week." A trader sees the last chance to fix results. Enters risky trades. Increases lot size.

Broker statistics confirm: Friday after 3 PM MSK collects more stop losses than any other time.

Ghost Hours

There are periods when the market technically works, but better not to trade.

From 10 PM to 2 AM MSK, America closed, Asia still sleeping. Liquidity drops. One large order can move price 20 pips.

European lunch time (1 PM-2 PM MSK) is also treacherous. Volumes freeze. Price marks time. Then suddenly shoots in any direction without reason.

Trading these hours resembles fishing in an empty pond. You can sit long and catch nothing.

How Time Affects Your Thinking

Fatigue accumulates. In the morning you analyze each trade. By evening you just click on the chart.

Biorhythms dictate concentration. Peak performance for most people falls at 10 AM-12 PM. After lunch comes a decline. By 5 PM, risk assessment ability drops 30%.

Add caffeine, sleep deprivation, personal problems. Your state changes perception of the same situation on the chart.

Wednesday: The Golden Middle

Statistics say: Wednesday gives the most stable results.

Monday emotions passed. Friday fatigue hasn't arrived yet. Market works in normal mode without surprises.

Most professional traders concentrate activity right in the middle of the week. Less noise, more patterns.

Find Your Time

No universal recipe exists. Some trade Asian session excellently. Others catch New York volatility.

Keep a journal not just on trades, but on time. Mark when you make the best decisions. When you make impulsive mistakes.

After a month you'll see a pattern. Perhaps your brain works clearer in the evening. Or Mondays really bring only losses.

Adapt your schedule to biology, not to the desire to trade 24/7.

Time as a Filter

Experienced traders use time as an additional entry filter.

Good setup on Monday morning? Skip it. Same setup on Wednesday? Take it.

Buy signal at 11 PM? Wait for Tokyo opening. No point risking with low liquidity.

Time doesn't cancel strategy. But it adds probability in your favor.

What the Numbers Say

Data from thousands of accounts show clear patterns:

Monday: minus 2-3% to average profitability

Tuesday-Thursday: stable results

Friday: minus 1-2% after 3 PM

Night sessions: unprofitable for 78% of traders

London-New York overlap: maximum profit for scalpers

Numbers don't lie. Psychology is real.

Final Word

You can have the best strategy in the world. But if you trade at the wrong time, results will be average.

The market doesn't change. People trading in it change. Their fatigue, fear, greed, inattention.

Time of day and day of week determine who is in the market now and in what state. And this determines how price will move.

Choose trading time as carefully as you choose entry point. Many traders add time filters to their strategies or use indicators that help track session activity.

How to Use S & R in a High-Probability Way | Tutorial #1❓ What is Support & Resistance?

Support and Resistance are key price levels where the market has previously shown strong reactions, often leading to reversals, pauses, or continuations.

🧩 Key Traits of High-Quality Support & Resistance

✔ Multiple rejections ( minimum 2 , more is better)

✔ Level has acted as both support and resistance

✔ Recently respected by price (close to the left structure)

✔ Recently formed level (fresh in market memory)

✔ Strong and impulsive move away from the level

✔ Very obvious level (can be spotted within seconds)

📌 Note:

Not all traits are required.

The more traits align, the higher the probability.

⚠️ Important

Support & Resistance alone is not enough .

High-probability setups come from combining S&R with:

🕯 Candlestick confirmation

🧠 Area of confluence

📐 Chart patterns

⏱ Multi-timeframe alignment

📊 Other high-quality technical factors

👍 Want PART 2?

Leave a like and a comment below.

📈 Follow for high-quality trading education and clean technical logic.

⚠️ DISCLAIMER

This content is for educational purposes only and does not constitute financial advice.

Trading involves risk—always conduct your own analysis.

I am not responsible for any decisions or losses based on this material.

The Anatomy of an Overextended Market MoveMarket Context: When Momentum Accelerates

Markets periodically enter phases where price accelerates rapidly, often driven by a combination of macro catalysts, positioning imbalances, and behavioral feedback loops. In such environments, momentum can appear self-reinforcing: higher prices attract more participation, which in turn pushes prices even higher. While these phases can feel decisive and convincing, they also introduce an important analytical question — is the move being accepted by the market, or is it simply expanding faster than structure can support?

This distinction matters because strong momentum does not automatically imply durability. In fact, the most aggressive moves often carry the seeds of their own instability, particularly when price begins to disconnect from commonly observed reference points such as volatility envelopes, prior value zones, and resting order clusters.

The recent advance examined in this case study provides a clear example of this dynamic: a structurally bullish resolution followed by a sharp acceleration that raises legitimate questions about sustainability.

Pattern Resolution Versus Move Sustainability

Classical chart patterns are useful because they describe how markets transition from balance to imbalance. A double bottom, for example, reflects a failed attempt by sellers to extend lower prices, followed by renewed demand. Once the neckline is cleared, the pattern is considered resolved.

However, pattern resolution only explains directional bias — it does not guarantee how price will behave after the breakout.

In practice, many pattern completions coincide with:

Early participants reducing exposure

Profit-taking activity near projected objectives

New positioning that is more sensitive to short-term adverse movement