Easy method to determine next target based on candle closeHey traders today we are going to look in how to determine Daily Bias. Its actually not that complicated how many people thinks.

Please forget about higher highs, and higher lows, channels and moving averages. Yes these can be also used, but we will be looking at the market in terms where is the liquidity and we will be determining the bias based on candle closes which tell us where the liquidity is resting.

We will look at the Daily bias, but as I mentioned this many times in my posts - price is fractal so you can use this at any timeframe. But, If I can give you recommendations look for Higher timeframe bias on Daily and Weekly and H4 / H1 Structure and M15 entries.

This post will be about continuation setups in a trend, I will touch a bit reversal because it's part of setup on LTF in the continuation. Something will be shown on bearish examples something bullish I hope you can use imagination for both sides.

⁉️ Where is the liquidity ? Always follow the Daily / Weekly candle close.

📈 Continuation

If todays daily candle closed above previous days high and its still not reaching the key level, then liquidity is above todays high. Why ? Because people have intentions to sell highs to early, so and price will most likely go there. So we are bullish. Bullish Close 📈 Reversal

If todays candle wicked above previous day high, but closed below , then we can expect liquidity is below Previous days low. Why? Because mostl likely traders entered fake high break out they put SL below days low. It's signs of reversal. Every significant reversal wicked above PDH and closed inside, if not seen on PDH than its on weekly. ‼️ Yes, Its that simple - this is how I predict my bias for the setups.

There is obviously little bit more regarding the market context, because I want to be always selling highs and buying lows. Hence there must but pullback deep enough. I have explained how to buy low and sell highs in this post below. 🔗 Click the picture to learn more 👇 This is not about catching every significant highs and lows, you don't need it to be profitable. We are looking for the high probability trend continuation setups. We can catch highs and lows in the trend. After the stop hunt.

🧪In downtrend you want sell after stop hunt of short term highs 🧪In the uptrend you want be buying after stop hunts of short term lows I have explained more about stop hunts in this post. 🔗 Click the picture to learn more 👇https://www.tradingview.com/chart/XAUUSD/1J6LLshN-The-Art-of-the-Stop-Hunt-Trading/ Now, If we know the bias based on the Daily / Weekly candle close our goal is to position ourself in the right time for the continuation setup which will be during the lower timeframe reversal.

📌 Reversal Setup

first lets have a look to the reversal. We want see a candle high being taken and closed below. In that case draw on liquidity is below the daily low. Sign of reversal. So we can position ourselves in a trade as described on the picture, wick above and close inside is not enough for the signifcant HTF reversal. But its enough for our continuation setup,

📌 Continuation setup

We want to see bullish candle close above previous days high and not liquidity taken above that wick. Then we can assume that liquidity is still resting above and we want to position ourselves during the LTF reversal in the direction of the HTF liquidity. same case will be for this bearish example where we can see how candles closed below the previous days low and last low was not swept hence we can expect price to visit that low again, we have spotted potential reversal by wicking above the candles high and close below and than we can position ourselves to the short and target daily lows. 📌 Continuation LTF reversal timing

same case now you must already see it bullish close above PDH and that high was not swept so liquidity is still above , next day is inside candle once price dips below inside candle low we cans spot reversal setup on LTF and by creation of order block we enter the position during the NY session manipulation 📌 No Stop hunt = No trade

if liquidity was not taken don't enter. Yes you can miss a trade it doesnt happen always, but if it doesnt happen it's not your setup so you didnt miss anything. On this example you can see that we had almost same setup. Bullish daily candle close. High was not swept, and than 2 inside candles. 3 candle manipulated lows and another candle was expansion. Now still focus the the picture above 2nd candle that candle is a range you are entering it after that range was manipulated. Look how price reached 50% of that range , retraced and than it went full range. Its Trading model 1 and Model 2. You mostly get 2 chances to trade it. Trading ranges is in my opinion least subjective approach and unlike diagonal drawings or multiple various pattern it has defined rules. I have described this strategy in details in this post below. 🔗 Click the picture to learn more 👇https://www.tradingview.com/chart/BTCUSDT.P/PkQJvVm4-Complete-system-for-Day-Swing-Traders/ 📌 Final example for today - Schematics

Now try it alone - step by step

1) How are candles closing

2) Was the Liquidity on the low taken ? No - price might go there - Im bearish

3) Lets wait for the LTF reversal - bearish this scheme was actually traded and posted here on Tradingview as a Continuation setup Model 1 & 2 🔗 Click picture below to learn how price action developed 👇 💊 Here are few more examples based on this trading logic

1️⃣ GBPUSD Daily range - Continuation setup Model 1 & 2

🔗 Click picture below to learn how price action developed 👇https://www.tradingview.com/chart/GBPUSD/VSZwqjUj-GBPUSD-Daily-CLS-Range-Key-Level-OB-Distribution-Phase/ 2️⃣ AUDUSD Daily range - Continuation setup Model 1 & 2

🔗 Click picture below to learn how price action developed 👇https://www.tradingview.com/chart/AUDUSD/YzC7vNOf-AUDUSD-I-Daily-CLS-range-I-Manipulation-I-Short/ 3️⃣ DOGE Daily range - Continuation setup Model 1 & 2

🔗 Click picture below to learn how price action developed 👇https://www.tradingview.com/chart/DOGEUSDT.P/t48YbkXb-DOGE-Daily-range-I-Key-Level-FVG-Setup-is-ready/ Final words

Is this holy grail ? Almost.

Why is this approach great ? It's mechanical system for analysis - No subjective guessing.

Does it prevent me from losses ? No, I can make and I sometimes I do mistakes in analysis, Im not perfect.

Dont trust me , Im just a guy from the internet. Verify it by yourself and see if you take some of it to your trading arsenal.

Adapt useful, Reject useless and something specifically your own.

David Perk aka Dave Fx Hunter

Community ideas

Patience - When Calm Feels WrongNOTE – This is a post on mindset and emotion. It is not a trade idea or strategy designed to make you money. My intention is to help you preserve your capital, focus, and composure — so you can trade your own system with calm and confidence.

Markets quiet down.

Price moves slow.

Everything looks still, maybe too still.

Part of you relaxes.

Another part tenses.

It’s that sense that something’s coming.

And sometimes, it is.

But here’s the hard part

Your body doesn’t always know the difference between anticipating danger and feeling unsafe.

For traders, the nervous system reads uncertainty like threat.

Even a normal pause in volatility can trigger the same internal siren:

Something’s wrong. Do something.

You start scanning: news, charts, signals

anything to justify the unease.

But often, the danger isn’t out there.

It’s inside you... a learned association between stillness and not knowing what's going to happen next

Which causes restlessness, uncertainty and a need to fidget and meddle.

The skill isn’t in shutting that instinctive unease down.

It’s in listening without reacting impulsively.

Ask yourself - what is really going on right here, right now?

The point here is:

Patience isn’t passive.

It’s regulated awareness.

It’s being alert, not alarmed.

Ready, but not restless.

Sometimes there is indeed a risk out there.

We are trading the financial markets after all.

However. You have a trading plan.

You know to be risk measured.

All that is needed now is the ability to regulate yourself

Stay calm and patient so you can execute your plan as intended.

the WY of Honeywell's Earnings Report Gap up and Run down It is very important that you understand what is happening in a company that impacts its stock price. HON has had Dark Pool Rotation going on since July of this year. Dark Pools are the most informed of all the Market Participant groups (there are 12 not 2).

The chart of HON has plenty of information that provides an understanding of why the stock ran down this morning. Late retail buyers may push price up if they buy on the dip which is not a dip and it is not profit taking either.

HFTs were the trigger for HON to gap up at open. Smaller funds were the drivers of price upward. HFTs sold quickly. Pro Traders who were in with the HFTs took profits end of day as is their custom. Today is a surprise for many retail day traders as the stock is running down early this morning.

This is smaller funds who want to off load their shares of HON selling into the previous day's speculative trading.

Who controls price today? Smaller funds.

Market Regimes: What they are and why they matterRegimens, what are they and why they matter?

Most traders, especially new ones, don’t understand trading regimens. This is actually normal. Even as a quant based trader with higher education in stats/sciences, I learned of Regimen trading later in my trading career, having successfully navigated trading without it; but insurmountably improving things when I discovered it.

What is a regimen you may ask? Is it what’s going on in North Korea? Or even the USA?

Chances are, most people may think regime is synonymous with something like fascism or some ultra political significance, but the truth is regime can mean a few things, and I think its important, before getting into the real details, to first understand the meaning of regime.

The Meriam-Webster dictionary defines regime as:

regular pattern of occurrence or action (as of seasonal rainfall)

the characteristic behavior or orderly procedure of a natural phenomenon or process

mode of rule or management a government in power

a form of government

a government in power

a period of rule

If you were to do a grad school ‘ concept analysis’ on regime, you would get some interesting findings of regime. Essentially, all of these definitions have a significance/underlying overlap in meaning. The simplified meaning? I would say (without having done an actual concept analysis), a regime is a “pattern of behaviour / rules / government that forms repeating characteristics that can be measured and predicted against its previous characteristics”.

Still too complex? Let’s simplify with both political and scientific examples.

Political

In the current presidency in the U.S., the Republican party was swift to implement sweeping tariffs against international trade partners, blanketing entire continents in a matter of days with tariffs. These were then paused, resumed, paused, resumed, lowered, raised, lowered, raised, paused, resumed, revoked, resumed, lowered, raised, etc.

Under the current political regime, we can identify the behaviour of “tariff implementation”. From previous tariff implementation and revocation and adjustment, we have the characteristics of this regime. We can then use these characteristics to predict future outcomes under this regime, i.e. we would hypothesize “Tariffs will be paused within the coming 2 months”. We can say this because this is a characteristic of the current regime. In fact, the term TACO is a perfect example of repeating regime characteristics!

What about a scientific example?

Well we can draw on Meriam-Webster making reference to seasonal rainfall. In climatology, a " rainfall regime " refers to the characteristic pattern of precipitation over a region during the year—especially its timing, intensity, and variability across seasons. Identifying these regimes are pivotal to forecasting future meteorological and climatological events!

What about my field? Epidemiology and Biostatistics?

In Epi, we have multiple different regimes, such as:

Treatment Regime: A prescribed course of medical therapy, such as a drug regimen for tuberculosis or chemotherapy for cancer. It includes dosage, timing, and duration.

Vaccination Regime: A schedule of immunizations designed to prevent disease outbreaks—e.g., two-dose mRNA COVID-19 vaccine regime followed by boosters.

Control Regime: A set of public health policies or containment strategies—like quarantine protocols, mask mandates, or vector control in malaria-endemic areas.

Surveillance Regime: The systematic collection and analysis of health data to monitor disease trends—e.g., wastewater surveillance for poliovirus or syndromic surveillance for flu-like illness.

These all matter because these regimes dictate future characteristics/outcomes.

Great! Now that you have an idea of what a regime means, let’s talk about regimes in trading.

If you haven’t already guessed, there obviously exists “ market regime s”. These are, more or less, defined as “a distinct period characterized by specific patterns in market behavior—such as trends, volatility, and macroeconomic conditions—that influence investment strategies and risk management. ”

If you look back to our examples, you can begin to imagine why regimes matter. Remember, TACO! Previous behaviour dictates future characteristics. Once you understand the way or median in which some phenomena operates, you can use these characteristics to predict future characteristics.

If you wanted to dissect market regimes, it could get relatively involved and complex. For example, things such as:

Seasonality,

Momentum,

Mean Reversion,

Financial / economic stability

Geopolitical stability

These can all influence market regimes in their own way and can, in fact, be standalone market regimes. If you trade seasonality, you are trading “ seasonal regimes ”.

Momentum and Mean reversion are independent regimes of themselves (more on that shortly).

If you trade fundamentals, you will be trading economic and geopolitical regimes.

But which is correct? Not all regimes can exist at the same time, correct?

Yes and no! Regimes can momentarily shift and flip into a different one. Take, for example, the U.S. implementation of Tariff’s at the beginning of 2025. The initial blanket tariffs caused a mean reversion regime fueled by financial/economic and geopolitical stability. We had 3 regimes working together for the result, which was ultimately a mean reversion. This quickly shifted from a mean reversion regime to a momentum based regime (more on this shortly).

So, yes, we can, theoretically, have more than one regime simultaneously. However, when it comes to markets, and this is where you are in luck, its actually pretty easy! Markets tend to be either:

Mean reverting; or

Momentum based.

And that’s really that. Those are the only 2 regimes you will ever truly need to pay attention to, which will give you a better edge at trading. Seasonality, financial and geopolitical stability will either augment mean reversion or momentum, but generally are not independent regimes in and of themselves.

In the end, markets either go up, down or sideways. It can be driven by broader contexts, but in the end the up/down/sideways is driven by a predominate regimen;

Down markets: usually mean reverting.

Up markets: usually momentum.

Sideways markets: usually mean reverting with occasional momentum deviations.

If you want to learn more about the evolution of the market, you can check out my post about how the market has evolved into its current regime here:

Now, let the real fun begin and let’s talk about how to correctly trade based on the current regime!

There are some steps, first one must:

Identify the current regime concretely.

Apply the correct strategies that are compatible with the current regime.

Understand the momentum, mean reversion paradox

I will walk you through how to do this step by step.

Identifying the Current Regime Concretely

The easiest way to identify the current regime is by using Hurst Exponent.

The Hurst exponent is a number between 0 and 1 that tells you how predictable a time series is—like stock prices or rainfall.

If it's close to 0, the data is very random and tends to switch directions often.

If it's around 0.5, the data behaves like a random walk—no clear trend.

If it's close to 1, the data shows strong trends and tends to keep moving in the same direction.

So, it helps you measure persistence vs. randomness in patterns over time. The closer to 1 the more “persistent” the market is said to be. Persistence is basically the math equivalent of momentum. If a market is persistent, it will tend to trend with momentum.

The closer to 0 the more random the market is said to be . Randomness usually favours “mean reversion”

For simplicity, if you get a Hurst Exponent > 0.5, you are likely in a momentum regime. If < 0.5, you are likely in a mean reversion regime.

Let’s take a look at some examples using QuantNomad’s Hurt Exponent indicator ( available here ):

This is just before the crash in February 2025. We can see that up here, the Hurst Exponent was < 0.5, indicating a mean reversion preference. And indeed, the market ended up mean

reverting back to its quadratic mean (481) with the crash.

Then let’s see what happened:

After the crash, we can see that the Hurst Exponent was consistently > 0.5, indicating persistence in the market, i.e. trendy and momentum based.

Remember, as a rule of thumb, momentum markets generally faour upside and mean reverting tend to be downside favouring. If we narrow the regime to smaller timeframe regimes, you can see this phenomenon quite easily. Let’s look at SPY on a bearish day and bullish day against the Hurst Exponent:

We can see that on this bull trend day, Momentum and persistence reigned dominate. Hurst did not drop below 0.5, at least not for long, which indicated a persistent trend that was momentum driven.

Now a bearish day:

You can see on this bear trend day that Hurst stayed below 0.5 persistently, indicating mean reverting behaviour.

This also highlights how lower timeframes can have independent and day to day regimes, but its always important and critical to pay attention to the major regime a market is in on the larger timeframe.

Applying Correct Strategies

Depending on the regime, you MUST tailor your strategy to match the regime. If you are trading a mean reverting regime, oscillators like RSI and Stochastics aren’t going to work well. If you are trading a momentum regime with high persistence, mean reverting strategies like Bollinger Bands and Z-Score are not going to work.

As a rule of thumb, when Hurst is > 0.5, you want oscillator based strategies such as RSI, Stochastics, etc.

One indicator that I would recommend in momentum based regimes is my own, Momentum Probability Oscillator indicator ( available here ). This indicator operationalizes probability/sentiment through momentum metrics instead of mean reversion metrics. Let’s take a look at some examples:

In this example on the hourly timeframe for SPY, you can see that momentum is lost (signified by the oscillator falling below the yellow line) indicating that the likely outcome will be selling, this is shown by the pink arrows.

In this next example, we can see where momentum is reclaimed and the bias shifts to upside.

Because this indicator quantifies momentum probabilistically, it does well in momentum based, persistent regimes to identify strong trends and pullback of trends.

In reality, you can use any oscillator in a momentum based, persistent regime, but obviously I am biased to my own creations.

What about a mean reverting regimen?

If we are in a mean reverting regime, your best indicators to use are Bollinger Bands or, my favourite, the Z-Score probability indicator (by yours truly) available here .

Let’s use $NYSE:IRDM as our mean reverting example

In this image, the red arrow marks the transition to a mean reverting regime. So what do we use here? Well let’s take a look at the Z-Score probability indicator:

The red lines mark the transition to a mean reversion based regime. At the time of this transition, IRDM was oversold based on the Z-Score probability. We can see it in fact rallied back up to a z-score of 0 (mean reversion) before rejecting back down from the 0.

This is incredibly powerful, as the Hurst Exponent tells you that you can trust a reversion back to a mean!

Let’s try a smaller, intraday example, going back to SPY:

This day, SPY looked pretty bullish; however, the Hurst Exponent was consistently below 0.5 indicating mean reversion.

If we applied the Z-Score probability indicator:

I flipped the indicator to use Candles so you can more easily see the mean reversion behaviour. SPY goes to either extremes and always mean reverts back to 0, at times even consolidating in the mean reversion range.

And Bollinger bands:

If we look at a momentum driven day:

We can see that there is a skew or bias to one side of the average. The z-score is all over the map with no real expansion within the average range and infrequent and sporadic reversions that come more from extensive consolidation rather than actual mean reversion.

The indicator isn’t unusable in momentum based trading, but its not ideal. If we flip this same chart to the momentum probability oscillator we can see a stark difference in utility:

You can see the trend is using the full range of the oscillator and there is clear bounces at lower range and rejections at higher range with frequent “mean reversion” of the oscillator momentum based mean.

Now finally, the last section:

The Momentum Mean Reversion Paradox

This is, obviously, a self made up term. However, this is a phenomenon that will happen in corrective environments, where a mean reversion is so substantial, it becomes augmented by momentum itself.

What does this mean? It means that, despite the market actually mean reverting, the Hurst exponent flips to > 0.5, as the market is “persistently bearish”.

We can see this if we flip back to our $NYSE:IRDM example:

Here, we can see despite IRDM selling, the Hurst Exponent is incredibly trendy, with a really high value of > 0.55. Yet, despite this, the ticker continues down. This is the hallmark of a correction.

This is incredibly important and I really would advise you to mark this down and remember this. You can actually tell that something is “correcting” using this exact approach. When Hurst > 0.5 and the trend is down, this is the hallmark of a TRUE correction. No speculation needed!

Statistics is the best, I’m telling you.

Let’s look at the SPY crash of 2025:

During the SPY crash of 2025, the Hurst flipped to > 0.5, with a max of 0.57 indicating a hugely persistent trend. This means that this was a strong correction for SPY, flipping from a Hurst of < 0.5 to a Hurst of > 0.5 with a strong downtrend.

Crashes tend to happen abruptly without such transitions. For example, if we look at the COVID crash:

Theoretically Hurst warned us in advance that SPY was entering mean reversion territory, but when it actually happened, it happened so fast, Hurst never truly converted from mean reversion to trending. It was just a jumbled mess. This is the hallmark of a crash.

Concluding Remarks

And now, my friends, you know all there is to know about how to identify market regimes! Understanding these concepts will put your eons ahead of the average trader and allow you to select the correct tools and actually understand what the market is doing and when its gearing up for some corrections/mean reversions.

This is a long post, I will leave it there, but I really hope you learned something from this and will take some of the key points away!

Thanks for reading and as always, safe trades!

How Key Fundamentals Can Play A Key Role In Your InvestmentsAs popular as Technical Analysis is with the ease of plotting indicators and tools to exhibit trend changes, Fundamental Analysis also plays a role not as simply demonstrated but equally as important!

Now when it comes to Fundamentals, there are a few key financial items that feed investors all the hints they need to potentially make fairly profitable investments and avoid devastatingly horrible mistakes and these are:

1) Income Statement

2) Balance Sheet

3) Cash Flow

The Income Statement retains the most mentioned fundamental metrics like Revenue which is how much money a company makes by selling their goods and services, Operating Expenses like Marketing and Research and Development.

Here I use NYSE:ACHR Income Statement for the example

www.tradingview.com

Even though Archer Aviation still has yet to post any Revenue, news for the company that's come out lately show a strong demand for NYSE:ACHR product and services:

- Signing a partnership with Korean Air to commercialize its electric air taxis in South Korea, with a potential purchase of up to 100 aircraft.

www.tradingview.com

- Named exclusive Air Taxi partner for the Los Angeles Sports & Entertainment Commission who will be hosting the 2026 World Cup.

www.tradingview.com

And with Archer Aviation acquiring Lilium's Patent Portfolio this month adding 300 Patent assets, pushing Archers total patents to exceed 1,000 assets globally, shows rapid expansion potential for the company against competitors!

www.tradingview.com

Now for the Balance Sheet

www.tradingview.com

The Balance Sheet can determine how healthy a company is and produces 3 important factors that basically determine a company's Net Worth and they are:

1) Assets - What the company owns

2) Liabilities - What the company owes

3) Equity - Whats left of the Assets once Liabilities are accounted for

We can see that NYSE:ACHR has maintained a stunning balance between their Assets and Liabilities with Assets just about doubling in Q'2 of 2025 from Q'4 2024 and Liabilities all the while staying relatively the same and low!

Meaning less hurdles to jump and obstacles to pay off that could slow the progress of growth in the long-term with great Equity!

Finally, the Cash Flow

www.tradingview.com

Cash Flow is a companies true way of transparency with showing the flow of cash in and out of the company and shows what's actually generated by the company from doing business and is separated in 3 sections:

1) Operating Activities

2) Investing Activities

3) Financing Activities

Now we can see Operating and Investing activities may not be NYSE:ACHR strong suit yet, but as Financing goes, numbers have continued to rise exponentially since Q'2 of 2024!

This suggests there is a lot of interest in the company from outside lenders and investors!

Like the saying goes, "Sometimes it takes belief in others belief in you before you gain belief in yourself." - Financial Activities could help carry NYSE:ACHR further!

** Remember, nothing in trading no matter how Technical or Fundamental is ever 100% right every time. It takes a combined effort of both Technical and Fundamentals to paint a vivid picture of what a company or asset may be worth or doing. So do your due diligence in research!

Don't Ask What To Invest In, Ask Why Invest In It!!

5 Essentials of Trading Success

Trading is the greatest roller coaster you’ll ever ride.

Trading has its thrills, challenges, and endless potential for growth.

But, before you hit “Buy” or “Sell,” it’s crucial to lay down a solid foundation.

Too many traders jump in without preparation, and without knowing the real life variables.

When things go great, they feel normal and you feel in charge.

When things go bad, you feel it’s the end of the world.

So you need to learn to harness each of the 5 essentials to trading success.

Essential #1: Build a Solid Foundation of Knowledge

You wouldn’t drive a car without knowing the rules of the road, right?

Trading is no different.

Before placing your first trade, you’ll need to understand the key concepts and market basics that will serve as your roadmap.

Key areas to cover include:

Market types:

Know the difference between stocks, forex, commodities, and cryptocurrencies. Know which is the best stock screener. Also you need to know which markets will work for you and your trading personality.

Trading terminology:

Terms like “bearish,” “bullish,” “short-selling,” “leverage,” and “margin” might sound like jargon now, but they’ll soon become your everyday vocabulary.

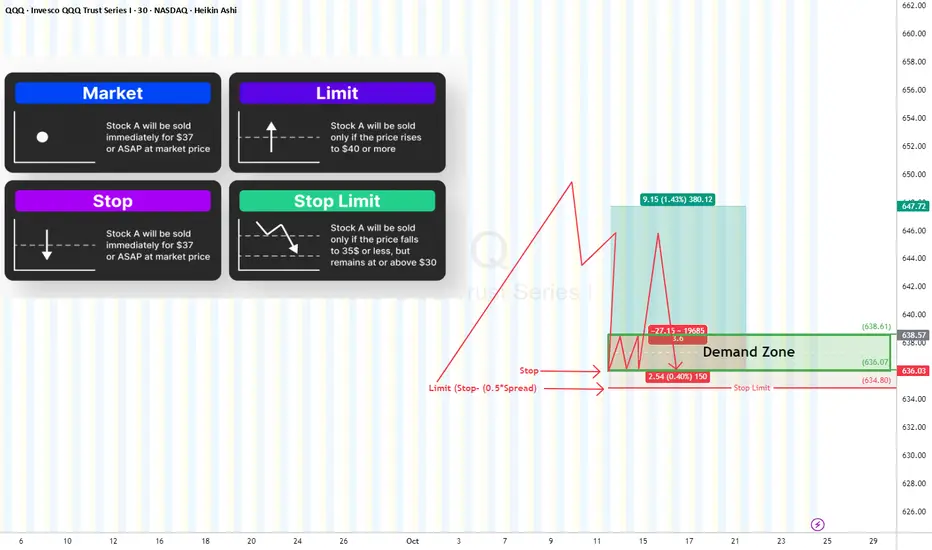

Order types:

Limit orders, market orders, stop-loss, take-profit. Each of these orders serves a specific purpose. Mastering them is essential for making controlled and effective trades.

Essential #2: Select what you want to trade first: The Art of Asset Allocation

Trading is thrilling, but let’s face it.

No one knows what the market will do tomorrow.

That’s why choosing the right mix of assets—and learning the art of asset allocation—is crucial for long-term success.

What does asset allocation mean in practice?

Diversify your portfolio: Don’t put all your eggs in one basket. Invest and trade across different asset classes to spread out risk.

It’s better to trade different portfolios with stocks, Forex, indices and even commodities.

Successful trading isn’t about picking one “winning” asset.

It’s about managing risk and creating a balanced portfolio that can weather market storms.

Diversification is KEY!

Essential #3: Risk Management: Strategies to Protect Your Capital

If you only remember one thing from this article, let it be this:

Risk management is your best friend in trading.

Not only do you learn how to be a trader, but also a risk portfolio manager.

A smart trader doesn’t only think about potential gains—they think about how to protect their capital when things don’t go as planned.

Simple, powerful ways to manage risk include:

Set stop-loss orders: Automatically sell a position when it drops to a certain price to minimize losses.

Use position sizing: Avoid putting too much of your capital into a single trade. Limit each trade to a small percentage of your total funds—usually no more than 0.5%-2%.

Apply the “2% rule”: Never risk more than 2% of your capital on a single trade. This can help prevent one loss from wiping out your progress.

Remember, every trader has losses; it’s part of the game.

But with a solid risk management strategy, those losses won’t be catastrophic.

Essential #4: Charting the Path: Introduction to Technical Analysis

Charts are a trader’s treasure map. Learn to interpret them, and you’ll have insights into market trends, price movements, and potential buy/sell signals. Technical analysis allows traders to make data-driven decisions rather than relying on gut feelings.

Key tools for technical analysis:

Candlestick patterns: These can show trends, reversals, and market sentiment. Patterns like “doji,” “hammer,” and “engulfing” candles can offer powerful insights.

Indicators: Tools like moving averages, RSI (Relative Strength Index), and MACD (Moving Average Convergence Divergence) help you assess price momentum and potential reversal points.

As you might know by now. I like to stick to three indicators: Breakout patterns, 2 Moving Averages and Trend lines.

We need to learn to simplify our strategy because we will be following it over our entire trading career.

Trendlines: Drawn on charts, trendlines reveal price direction and potential breakout or breakdown levels.

Essential #5: The Psychology of Success: Developing a Trader’s Mindset

Trading isn’t just about strategies and technical skills; it’s also a mental game.

Emotions—fear, greed, EGO, frustration — can interfere with sound decision-making.

If you can’t manage your mind, you can’t manage your portfolio.

And that’s why it’s essential to develop a mechanical, professional and calm mind when trading.

Developing a disciplined mindset is what separates successful traders from those who burn out.

Conclusion

Let’s sum up the 5 ESSENTIALS to trading success.

Essential #1: Knowledge First: Understand trading terminology, market types, and order types.

Essential #2: Asset Allocation: Diversify your portfolio based on your risk profile.

Essential #3: Risk Management: Protect your capital with stop-losses, position sizing, and the 2% rule.

Essential #4: Technical Analysis: Learn chart patterns, indicators, and trendlines to guide decisions.

Essential #5: Trader’s Mindset: Control emotions, maintain discipline, and focus on long-term success.

Trading isn’t just a skill—it’s an adventure that rewards preparation, patience, and resilience.

Keep learning, stay focused, and remember: your success is built one trade at a time.

Time to buy or time to panic on crypto!?Is this the moment to run away, or the one to stay calm?

Isn’t the collective fear itself the signal we’ve seen before every comeback?

In a market ruled by emotions, sometimes you just need to take one step away from fear.

Hello✌️

Spend 2 minutes ⏰ reading this educational material.

🎯 Analytical Insight on Dogecoin:

BINANCE:DOGEUSDT has breached all key Fibonacci supports and now rests on a critical daily support level. If this holds, a potential 30% upside toward 0.25 becomes likely. 📊🛡️

Now , let's dive into the educational section,

💭 The psychology of fear in the market

When charts turn red, traders’ minds fill with panic. But markets are places where some people’s fear becomes others’ opportunity. Emotions are the biggest enemy of logic. Every downtrend is a redistribution of emotions, not necessarily the end of a trend.

📈 The cycle of greed and fear

The market constantly swings between greed and fear. When greed rises, prices grow beyond value; when fear dominates, assets fall below it. These extremes are where smart money buys, while newcomers sell.

🔍 Signs of a possible reversal

Rising volume near support zones, reversal candles on higher timeframes, and positive RSI divergence are key indicators of potential trend change. When prices stop falling but sentiment remains negative, that’s often when smart capital quietly starts moving in.

🧠 The mindset of a successful trader

A strong trader looks for opportunity when fear dominates. They enter with a plan, not emotion. The market rewards the patient, not the impulsive. They always have a scenario, rely on data over rumors, and let logic guide their trades.

⚙️ Entry and risk control strategy

During any bearish phase, the first step is to identify confirmed support levels. Then use staged entries to reduce exposure to volatility. Set your stop loss below recent structure and keep targets realistic. You can’t control the market, but you can always control your risk.

💡 Why now looks like a buying zone

Sentiment is dark, yet technicals reveal weakness in sellers’ momentum. The ratio of selling to buying volume is shrinking, and reversal candles are forming on key levels. The market is quietly building a new base. When everyone talks about collapse, smart money prepares for the next leg up.

🧭 TradingView tools that help confirm the move

The TradingView platform offers multiple indicators that give traders a practical edge.

• RSI (Relative Strength Index): Helps identify oversold and overbought zones clearly.

• Volume Profile: Reveals where the most trades occurred, highlighting real buyer–seller strength.

• Moving Average Cross: A simple but powerful signal for trend reversals.

• Fear and Greed Gauge: Tracks overall market sentiment in real time and shows when emotions are overreacting.

Using these tools together provides a complete perspective. Traders who analyze them in combination often spot reversals earlier than the crowd.

🔔conclusion

The crypto market is deep in a fear phase, and that’s usually where the best setups form. Fear creates the base for opportunity always has, always will.

💬 Three golden pieces of advice

1. Enter the market with a plan, never with emotion; every unplanned trade is a costly one.

2. Master patience the market always rewards those who wait for clarity.

3. Ignore collective fear; trust your data, your structure, and your logic.

✨ Need a little love!

We pour love into every post your support keeps us inspired! 💛 Don’t be shy, we’d love to hear from you on comments. Big thanks, Mad Whale 🐋

📜Please make sure to do your own research before investing, and review the disclaimer provided at the end of each post.

Doji Candlestick: A Key to Market ReversalsAlright, let’s break down the Doji candlestick pattern.

If you're trading crypto, you've probably bumped into this little guy at some point. It’s not a wild trendsetter on its own, but it definitely has something to say about the market’s mood 🤔. The Doji is one of those candlestick patterns you’ll want to pay attention to if you're trying to catch reversals or just understand what's going on in the market.

What is the Doji Candlestick Pattern?

A Doji candlestick pattern forms when the opening and closing prices are almost identical. The body of the candle becomes tiny, while the shadows (the lines extending above and below the body) are long. It might look like a cross, plus sign, or even an “✖️.” The key point is that the market is indecisive, which is why this pattern gets so much attention.

🐂Bullish Doji Candlestick Pattern

So, what happens when you spot a Doji after a downtrend? You might be looking at a potential reversal, signaling that the bears are running out of steam. A bullish Doji candlestick pattern forms when the market closes near the opening price but after a steady downtrend. It’s like the bulls are just waiting for the right moment to step in. But don’t jump in too quickly! A single Doji doesn't mean the market's ready to flip. Look for confirmation in the following candles — ideally, a strong bullish candle that closes above the previous high.

🐻Bearish Doji Candlestick Pattern

Now, flip the script. If you see a bearish Doji candlestick pattern after a nice uptrend, it’s time to pay attention. This signals that the bulls might be running out of energy, and the bears could be gearing up for a push. It’s not an instant signal to sell, but it’s a red flag that the market’s strength is weakening. After spotting the Doji, wait for confirmation — usually in the form of a bearish candle that closes below the previous low.

How to Use the Doji Trading Pattern Effectively?

So you’ve spotted a Doji chart pattern. Now what? This pattern is all about context. If it shows up in the middle of a strong trend, it’s probably just a pause in the action — not a reversal. But, if it appears after a big rally or a significant drop, it could indicate that market sentiment is shifting.

Here’s the key: Confirmation is king. The Doji itself doesn’t tell you where the market is going. It only tells you that the market is uncertain. Look for the next few candles to see if they support a reversal — a bullish follow-up candle after a bearish Doji or a bearish candle after a bullish Doji.

🏁Final Thoughts

The Doji candlestick pattern can be a valuable addition to your trading strategy, offering insights into market sentiment when combined with other indicators. While it highlights moments of indecision, it's essential to exercise caution and not rely solely on a single signal. In trading, context, confirmation, and proper risk management are key. Remember, tools like the Doji are meant to inform your decisions, but ultimately, it's your judgment and strategy that will guide your moves. Happy trading!

The Historical Crashes of Gold — What Really Caused Them ?Hello Traders 🐺

Throughout history, every major bear market in gold has been deeply connected to macro factors, monetary policy, and investor psychology.

Here I’ve summarized the key factors behind gold’s biggest crashes since the 1970s 👇

🧩 Key Factors Behind Historical Gold Crashes

1️⃣ Rising Real Interest Rates (↑)

The biggest historical enemy of gold.

Since gold has no yield, when real interest rates (nominal rates – inflation) turn positive, investors prefer bonds or the U.S. dollar.

Example:

In the 1980s, Fed Chair Paul Volcker raised rates above 15% to fight inflation.

Result: gold dropped from $850 (1980) to around $300 by the mid-80s — a 65% crash, marking the longest bear market in gold’s history (1980–1999).

2️⃣ A Stronger Dollar (DXY ↑)

Gold usually moves inversely to the dollar index.

When the dollar strengthens (especially vs EUR and JPY), gold comes under pressure.

Example:

Between 2011–2015, DXY rose from 73 → 100, while gold fell from $1920 → $1050 (≈45% decline).

3️⃣ End of Crises or Return of Market Confidence

When fear fades and confidence returns (e.g., after financial crises or geopolitical tensions ease), investors move away from safe-haven assets like gold.

Example:

After the 2008 crisis, once markets stabilized, gold entered a prolonged bear market (2012–2015).

4️⃣ Central Banks Stopping Gold Purchases

When central banks reduce or halt their gold accumulation, supply pressure builds.

Example:

In the late 1990s, European central banks sold large portions of their reserves (known as the Central Bank Gold Agreement 1999), which accelerated gold’s decline.

5️⃣ Strong Stock Market Returns

When equities deliver strong real returns, capital often rotates out of gold.

Example:

From 1995–2000, the S&P 500 rallied massively, while gold suffered one of its weakest decades.

6️⃣ Low Inflation & Economic Stability

Gold thrives on uncertainty and high inflation.

When inflation is low and stable, investors see little reason to hold gold.

Example:

Between 1985–2000, inflation in the U.S. stayed low — and gold traded sideways between $250–$400 for nearly 20 years.

7️⃣ Technical & Sentiment Breakdown

When key supports break and sentiment turns bearish, fear-driven selling usually accelerates the downtrend.

Example:

In 2013, gold broke below the $1550 support, triggering a rapid 20% selloff within months.

My final thought:

Every time gold enters a euphoric phase, history reminds us that the higher it climbs, the harder it falls.

So what do you think right know ? is GOLD about to fall ? let me know in the comment section down below this idea 😉🤔

So stay disciplined, watch the macro shifts carefully — and as always remember:

🐺 Discipline is rarely enjoyable, but almost always profitable. 🐺

🐺 KIU_COIN 🐺

Understanding the Foundation of Global MarketsFutures contracts are everywhere, from crude oil and stock indices to interest rates and even Bitcoin. They’re essential tools for traders and institutions to manage risk or capitalize on price speculation.

What Are Futures?

A futures contract is a legally binding agreement to buy or sell an asset at a set price on a future date. These contracts can involve commodities, currencies, or financial instruments.

Why Trade Futures?

Futures serve two core purposes

Hedging: Used by businesses to protect against adverse price moves. Example: A Corn farmer locks in $4.00 per bushel using a short futures position. If the price drops, they’re protected by gains in the contract. Conversely, if the price rises, the farmer should theoretically be able to sell the physical product at a higher amount.

Speculation: Speculators are a very important piece to market stability and liquidity. Many traders use futures to attempt to profit from market direction, in other words speculate on market moves. For instance, if a trader buys an E-mini S&P 500 contract at 6500 and it rises to 6550, they profit*. But losses can occur just as quickly if the market moves against the position.

*Always account for fees and commissions when evaluating performance."

Types of Futures Contracts

Commodity Futures — Crude oil, soybeans, gold.

Financial Futures — S&P 500, interest rates, Treasury bonds.

Currency Futures — Euro, Yen, and other FX contracts.

Cryptocurrency Products — Bitcoin, Etherum, Solana.

Key Takeaway

Whether you’re hedging or speculating, futures are dynamic and powerful tools. But they also carry significant risk. The first step is understanding what you're trading and why.

At EdgeClear, we’re here to help you trade with confidence. If you’re new or want to enhance your strategy, follow us on TradingView to learn more about Futures and read our latest Trade Ideas.

CME_MINI:ES1! CME_MINI:NQ1! COMEX:GC1! NYMEX:CL1! CME:BTC1!

Causes of Global CrashesEconomic, Political, and Psychological Factors.

Global financial crashes have been recurring phenomena throughout modern economic history. From the Great Depression of 1929, the Dot-Com Bubble of 2000, the Global Financial Crisis of 2008, to the COVID-19 market crash of 2020, each episode has revealed vulnerabilities in the global financial system. Despite different triggers, all share underlying causes linked to economic imbalances, political decisions, and collective psychological behavior. Understanding these factors is crucial for policymakers, investors, and economists to anticipate and mitigate future crises.

1. Economic Factors: The Foundation of Market Instability

Economic factors form the backbone of most global crashes. They often arise from systemic imbalances, over-leverage, speculative bubbles, and policy missteps that distort market efficiency.

a) Asset Bubbles and Overvaluation

One of the most common precursors to a crash is the formation of asset bubbles—situations where asset prices rise far beyond their intrinsic value due to excessive speculation. Investors, driven by the belief that prices will continue to climb, pour money into overvalued assets. When reality strikes and prices begin to fall, panic selling ensues, leading to a sharp market correction.

Examples include:

The Dot-Com Bubble (2000): Exuberance over internet startups drove technology stocks to irrational valuations, with companies having minimal profits being valued in billions.

U.S. Housing Bubble (2008): Excessive lending and subprime mortgages inflated real estate prices until defaults triggered a collapse, spreading through global financial markets via securitized mortgage products.

These bubbles illustrate how the combination of easy credit, speculative mania, and weak regulation can inflate asset values to unsustainable levels.

b) Excessive Debt and Leverage

High levels of debt—whether by households, corporations, or governments—create systemic vulnerability. When asset prices fall, overleveraged entities struggle to meet obligations, leading to a chain reaction of defaults and bankruptcies. Leverage amplifies both gains and losses; thus, when confidence erodes, deleveraging occurs rapidly, deepening the crisis.

The 2008 Financial Crisis serves as a textbook example, where banks and financial institutions had high exposure to mortgage-backed securities financed through short-term debt. Once the housing market declined, the inability to refinance debt led to liquidity freezes and institutional failures such as Lehman Brothers.

c) Monetary Policy and Interest Rate Mismanagement

Central banks play a crucial role in maintaining economic stability. However, prolonged periods of low interest rates and quantitative easing can encourage speculative behavior and excessive borrowing. Conversely, sudden tightening of monetary policy can burst bubbles and reduce liquidity.

For instance:

The U.S. Federal Reserve’s tightening before the 1929 crash is believed to have reduced liquidity, accelerating the market collapse.

Similarly, the rate hikes of 2022–2023 to combat inflation led to a correction in tech stocks and cryptocurrencies that had benefited from years of cheap money.

d) Global Trade Imbalances

Trade imbalances between major economies—such as the U.S. and China—can lead to distortions in capital flows and currency valuations. Persistent current account deficits or surpluses create dependency and volatility. When these imbalances adjust abruptly, global financial markets experience turbulence, as seen during the Asian Financial Crisis of 1997, when capital flight led to currency collapses and regional recessions.

e) Banking System Fragility

Weak regulation, risky lending practices, and insufficient capital buffers make banking systems vulnerable. The interconnectedness of global finance means that the failure of one major institution can cascade across borders, as seen in 2008 when the collapse of Lehman Brothers triggered a global credit crunch.

2. Political Factors: The Role of Governance and Geopolitics

While economic indicators often signal a crash, political factors can act as both catalysts and amplifiers. Governments influence markets through fiscal policies, regulation, and geopolitical actions.

a) Policy Uncertainty and Mismanagement

Political instability and inconsistent economic policies create uncertainty that undermines investor confidence. Sudden tax reforms, nationalization, or trade restrictions can shock markets. For instance:

The Brexit referendum (2016) caused massive volatility in global markets due to uncertainty about trade and investment flows.

The U.S.-China trade war (2018–2019) disrupted global supply chains, leading to stock market fluctuations and slower growth.

In emerging markets, policy mismanagement, corruption, and lack of transparency can drive capital flight, devalue currencies, and cause inflationary spirals—factors often preceding financial crises.

b) Geopolitical Conflicts and Wars

Wars and geopolitical tensions disrupt trade routes, increase commodity prices, and trigger risk aversion in investors. The Russia-Ukraine war (2022), for instance, caused spikes in energy and food prices, contributing to global inflation and slowing growth. Similarly, the Oil Crisis of 1973—triggered by OPEC’s embargo—plunged Western economies into stagflation, demonstrating how political decisions in one region can create worldwide economic turmoil.

c) Regulatory Failures and Deregulation

Governments and financial regulators are tasked with maintaining market integrity. However, deregulation or lax oversight can allow risky practices to proliferate.

The U.S. financial deregulation in the 1980s and 1990s encouraged complex derivatives and speculative trading, setting the stage for the 2008 crash.

In developing economies, weak regulatory frameworks have allowed unmonitored capital inflows that later reversed abruptly, causing crises.

d) Globalization and Policy Interdependence

Globalization has tightly interlinked economies, but it also means that crises can spread faster. The collapse of one major economy now has ripple effects through trade, finance, and investment channels. When political decisions—like sanctions, tariffs, or capital controls—are implemented by major powers, they can unintentionally trigger market dislocations worldwide.

e) Fiscal Deficits and Unsustainable Public Debt

Governments running persistent fiscal deficits often resort to excessive borrowing. When investors lose confidence in a government’s ability to service its debt, bond yields rise sharply, leading to a debt crisis.

Examples include:

The Eurozone Sovereign Debt Crisis (2010–2012), where Greece, Spain, and Italy faced massive sell-offs in government bonds due to high debt-to-GDP ratios.

Argentina’s repeated debt defaults illustrate how fiscal indiscipline can repeatedly destabilize markets and economies.

3. Psychological Factors: The Human Element in Market Crashes

While economic and political factors lay the groundwork for crashes, psychology drives the timing and intensity of market collapses. Investor sentiment, herd behavior, and cognitive biases play central roles in shaping market dynamics.

a) Herd Behavior and Speculative Mania

Markets are not purely rational systems—they are deeply influenced by crowd psychology. When prices rise, investors fear missing out, leading to herd behavior where everyone buys simply because others are buying. This collective optimism inflates bubbles beyond fundamental values.

Historical examples include:

Tulip Mania (1637) in the Netherlands, where tulip bulbs sold for the price of houses before crashing overnight.

Bitcoin and crypto booms (2017 and 2021), where social media hype and retail participation drove valuations to extreme levels before sharp corrections.

b) Overconfidence and Illusion of Control

Investors often overestimate their ability to predict markets. During bull markets, this overconfidence bias leads to risk-taking and neglect of fundamentals. Financial analysts, fund managers, and even policymakers may believe “this time is different,” ignoring signs of overheating.

Before the 2008 crash, many economists and bankers genuinely believed that new financial innovations had made the system more resilient—an illusion that collapsed once subprime defaults surged.

c) Panic and Loss Aversion

Once asset prices start falling, fear takes over. Loss aversion, the psychological principle that people feel losses more intensely than gains, causes panic selling. The speed of modern digital trading and algorithmic systems amplifies this panic, leading to rapid market declines.

During the COVID-19 crash of March 2020, stock markets fell over 30% within weeks as investors rushed to liquidate positions amid uncertainty, demonstrating how fear can drive faster collapses than fundamentals alone would justify.

d) Media Influence and Narrative Contagion

Media and social networks can accelerate both optimism and fear. Positive stories during bubbles and alarmist headlines during downturns amplify collective emotions. Economist Robert Shiller’s concept of “narrative economics” highlights how viral stories—such as “housing prices never fall” or “AI will revolutionize everything”—fuel speculative behavior detached from reality.

e) Behavioral Finance and Feedback Loops

Modern behavioral finance explains how psychological feedback loops amplify volatility. Rising prices attract attention, which draws more investors, pushing prices even higher—a self-reinforcing cycle. When this reverses, selling pressure creates a downward spiral, often far exceeding what fundamentals justify.

4. Interconnection Between Economic, Political, and Psychological Forces

Global crashes rarely result from a single cause—they emerge from a complex interaction of economic misalignments, political actions, and psychological dynamics.

For instance:

The 2008 crisis combined excessive leverage (economic), weak regulation (political), and investor complacency (psychological).

The COVID-19 crash reflected a sudden geopolitical shock (pandemic response), economic slowdown, and psychological panic selling.

The Asian Financial Crisis (1997) arose from overborrowing (economic), weak policy responses (political), and investor herd behavior (psychological).

This interconnectedness makes prediction and prevention challenging, as policymakers must manage not only economic fundamentals but also public sentiment and political realities.

5. Lessons and Preventive Measures

To prevent or mitigate global crashes, lessons from past crises must be applied systematically:

Stronger Financial Regulation:

Transparent accounting, capital adequacy norms, and limits on leverage can reduce systemic risks.

Balanced Monetary Policy:

Central banks should avoid prolonged ultra-low interest rates that encourage asset bubbles, while managing liquidity during downturns.

International Coordination:

Global financial stability requires coordination among central banks, governments, and institutions like the IMF to manage cross-border capital flows and crises.

Investor Education and Behavioral Awareness:

Educating investors about cognitive biases, speculative risks, and market psychology can foster more rational decision-making.

Crisis Communication and Transparency:

Governments and regulators should maintain clear, transparent communication to prevent misinformation and panic during economic shocks.

Conclusion

Global crashes are inevitable episodes in the cyclical nature of financial markets, driven by a combination of economic imbalances, political misjudgments, and psychological dynamics. While the specific triggers may vary—be it a housing bubble, a war, or a pandemic—the underlying patterns remain strikingly similar. Understanding these causes not only helps explain past collapses but also equips policymakers and investors to build more resilient financial systems. Ultimately, preventing future crashes requires recognizing that markets are not just machines of numbers—they are reflections of human behavior, confidence, and collective decision-making in an ever-interconnected world.

Global IPO trends and SME listings1. Macro picture: why IPOs dipped and why they’re coming back

From the 2021 frenzy to the 2022–2024 slowdown, three macro forces depressed IPO supply: rising interest rates, equity market volatility, and geopolitical policy shocks (trade/tariff announcements, sanctions, etc.). Those same variables determine the timing and size of any recovery: when volatility eases and public valuations become predictable, IPO windows reopen. By H1–Q3 2025 many markets recorded year-on-year increases in IPO counts and proceeds compared with 2024, signalling a cautious but visible rebound in investor risk appetite and issuer confidence. Major advisory firms reported a stronger pipeline and bigger average deal sizes in 2025 versus the trough.

Key takeaways:

Market sentiment and index performance remain the gating factor. When broader indices are stable or rising, companies and underwriters are more willing to price primary offerings.

Policy shocks (tariffs, regulation) can cause abrupt freezes—as seen in mid-2025 in some reporting—so recovery is patchy and regionally uneven.

2. Regional patterns — Americas, Europe, Asia

Americas (US/Canada): The U.S. market led global deals by proceeds in 2025’s first half, helped by both traditional IPOs and a revival of SPACs. Institutional appetite for high-quality growth names returned gradually; Nasdaq and NYSE regained traction for tech and fintech issuers. PwC and market banks flagged strong H1 2025 proceeds in the Americas, albeit with SPACs making up a significant portion.

Europe: Activity recovered more slowly but steadily. European exchanges and advisors pointed to unused capacity—investor demand exists but issuers and banks are selective about timing and valuation. Several jurisdictions enhanced SME support programs and pre-IPO education to stimulate listings.

Asia-Pacific: The region showed resilience and, in parts, growth—China and Japan saw notable listings and larger offerings. India’s domestic platforms recorded strong SME listing activity (see below). Overall, regulatory facilitation and local investor depth helped Asia outperform other regions in some periods.

3. The SPAC story: back — but different

After the 2020–2021 SPAC boom and the 2022–2024 cooling (regulatory scrutiny and poor post-deSPAC performance), 2025 brought a measured SPAC reappearance. Sponsors and investors are more disciplined: fewer overly ambitious valuations, more sponsor skin in the game, and clearer disclosure/earnout structures. SPACs accounted for a materially higher share of listings in early-to-mid 2025 versus 2024, but they are operating with tighter governance and (in many cases) better alignment with private equity and institutional exit strategies. Analysts expect SPACs to feature as one option among many for sponsor exits rather than the overwhelmingly dominant vehicle they once were.

4. SME listings — scale, purpose and platforms

SME listing platforms have evolved from niche curiosities into mainstream capital-raising mechanisms for smaller growth companies. Exchanges tailor admission rules, disclosure requirements, and investor education for SMEs to balance access to capital with investor protection.

Why SMEs list? Access to growth capital, brand visibility, liquidity for founders, and the ability to use publicly traded equity for M&A and employee incentives.

Popular SME venues: Euronext Growth (continental Europe), London AIM (though AIM’s structure is different), NSE Emerge and BSE SME (India), TSX Venture (Canada) and various regional growth boards. Exchanges increasingly offer pre-IPO programs and index inclusion to attract issuers. Euronext explicitly markets tailored listing journeys and investor pools for SMEs.

India as a case study: India’s SME markets (BSE SME, NSE Emerge) saw large volumes of small listings and notable capital raised historically; BSE’s SME crossing 600 listings and significant funds raised shows the scale and appetite for this route. Local retail and HNI investors play a disproportionate role in IPO allocations on SME boards, and many SMEs use these markets as stepping stones to main exchanges. However, regulators and exchanges warn about uneven due diligence standards and the need for investor education.

5. Structural features and investor behaviour in SME markets

Lower entry thresholds and lighter continuing obligations make SME boards attractive, but they also increase information asymmetry.

Investor mix: Retail and domestic institutional investors dominate many SME markets; that makes them sensitive to local sentiment and sometimes less correlated with global capital flows.

Price volatility & illiquidity: Many SME listings experience high initial pops or post-listing declines; long-term liquidity and governance can be variable. This means SME investing requires more focused research and risk tolerance.

Graduation pathway: Exchanges promote “graduation” from SME boards to the main market—this pathway creates an investment narrative (list, scale, graduate) that attracts some growth companies.

6. Regulatory & policy shifts affecting listing dynamics

Regulators in multiple regions have been balancing two objectives: broaden access to public capital for growth firms while protecting retail and unsophisticated investors. Typical policy moves include:

Strengthening disclosure and minimum corporate governance standards for SME boards.

Running pre-IPO education programs for management teams and investors (exchanges like Euronext emphasize educational support).

Closer monitoring of sponsor and promoter actions (especially after SPAC turbulence).

Incentives—tax or listing cost reductions—to encourage listings or relistings in domestic markets.

7. Challenges and risks (global & SME-specific)

Macro sensitivity: IPO pipelines can re-freeze quickly if interest rates or geopolitical tensions spike. (Mid-2025 tariff headlines illustrated this risk.)

Valuation gap: Private markets still sometimes price growth more richly than public markets will tolerate, delaying exits.

Post-IPO performance: A significant portion of IPO underperformance stems from immature governance, overly optimistic forecasting, or market rotation away from growth.

SME risk profile: SME boards have higher issuer-specific risk (concentration of promoter ownership, limited operating history). Robust disclosure and investor due diligence are essential.

8. Practical implications for stakeholders

For issuers (SMEs & midcaps): A public listing remains a credible route to scale. Plan the listing only when financials and governance can withstand scrutiny; consider whether an SME venue or direct main-board listing better serves long-term strategy. Use pre-IPO education services exchanges provide.

For investors: Diversify between established listed companies and a select set of SMEs—apply active due diligence on SME financials, promoter track record, and liquidity. Treat SME allocations as higher risk/high return.

For exchanges/regulators: Continue improving surveillance, standardise disclosure across SME platforms where possible, and invest in investor education campaigns to reduce information asymmetry.

9. Outlook (near term)

Most major advisory houses and banks saw a cautiously improving pipeline through H1–Q3 2025: more issuers willing to test the market, SPACs returning in a curated way, and regional variability (Americas and parts of Asia leading proceeds while Europe rebuilds). SME listings are likely to remain active where local investor demand and exchange support are strong (e.g., India, parts of Europe). However, a sustained recovery requires macro stability—lower volatility, clearer global trade policy, and accommodative capital markets. If those conditions hold, expect opportunistic pockets of high-quality IPOs and continued maturation of SME listing ecosystems.

10. Short recommendations (one-line each)

Issuers: prepare governance and communications early; choose the listing venue that fits growth stage.

Investors: treat SME allocations as active, research-intensive bets.

Exchanges/regulators: keep improving disclosure, investor education, and mechanisms to promote liquidity.

Advisors/underwriters: price conservatively, stress-test deals against volatility scenarios.

Regional Growth Strategies in the Global MarketIntroduction

In today’s interconnected and competitive global economy, companies no longer limit themselves to their domestic markets. They pursue expansion into multiple regions to tap new consumer bases, access resources, reduce costs, and diversify risk. However, global expansion is not a one-size-fits-all process. Each region presents unique economic conditions, cultural nuances, regulatory systems, and consumer preferences. Hence, the concept of regional growth strategies has become vital — it focuses on tailoring global business operations to fit the specific dynamics of different geographic regions.

Regional growth strategies in the global market are structured plans that multinational corporations (MNCs) and emerging firms employ to achieve sustainable expansion, build competitive advantage, and secure long-term profitability in target regions. These strategies are influenced by several factors such as regional trade blocs, demographic trends, technology adoption, government policies, and local market behavior.

1. Understanding Regional Growth Strategies

A regional growth strategy refers to a business plan that integrates global objectives with localized approaches. It involves identifying and prioritizing high-potential regions, customizing products and marketing to suit local needs, and establishing operations or partnerships to gain a competitive edge. Companies use these strategies to adapt their business model to regional conditions while maintaining global consistency.

For instance:

McDonald’s adjusts its menu to suit local tastes — vegetarian options in India, teriyaki burgers in Japan, and halal-certified meat in Middle Eastern countries.

Apple Inc. tailors pricing and distribution strategies differently in North America, Europe, and Asia-Pacific regions due to varying consumer behavior and income levels.

Regional growth strategies allow global firms to balance global efficiency (standardization for cost savings) with local responsiveness (adaptation to local markets), a key principle in international business theory.

2. Importance of Regional Strategies in the Global Market

Globalization has made regional growth strategies more important than ever. Some key reasons include:

Economic Diversification:

Companies avoid dependence on a single market by spreading their operations across regions. Economic slowdowns in one area can be offset by growth in another.

Access to Emerging Markets:

Emerging economies such as India, Brazil, Indonesia, and Vietnam have become growth hubs. Regional strategies enable firms to target these areas with customized offerings.

Cultural and Consumer Adaptation:

Understanding local culture, traditions, and consumer psychology improves brand acceptance and customer loyalty.

Regulatory Compliance:

Different regions have varying legal frameworks and trade barriers. Regional planning ensures compliance and smooth market entry.

Supply Chain Optimization:

Locating production or sourcing closer to key markets helps reduce costs, manage risks, and improve operational efficiency.

Strategic Alliances and Regional Clusters:

Regional partnerships and innovation clusters (like Silicon Valley in the US or Shenzhen in China) help firms leverage local expertise and networks.

In essence, regional strategies are crucial for aligning business operations with the realities of global diversity.

3. Types of Regional Growth Strategies

Companies use several strategic models depending on their goals, industry, and market maturity. Below are some common types:

a. Market Penetration Strategy

This involves increasing the firm’s share in existing regional markets through aggressive marketing, competitive pricing, or improved distribution. It focuses on strengthening brand visibility and consumer loyalty.

b. Market Development Strategy

Here, firms enter new regional markets with existing products. For instance, a European apparel brand might expand to Latin America, adapting its offerings slightly to suit local preferences.

c. Product Localization Strategy

To succeed regionally, firms often customize products or services for local audiences. This can include language adaptation, design modifications, or even creating region-specific versions of products.

d. Strategic Alliances and Joint Ventures

Collaborating with regional partners provides access to local knowledge, regulatory support, and established customer bases. Toyota’s joint venture with China’s FAW Group is a notable example.

e. Regional Manufacturing and Supply Chain Strategy

Setting up production centers within or near target regions reduces logistical challenges, tariffs, and currency risks. Many technology companies have established hubs in Southeast Asia for this reason.

f. Mergers and Acquisitions (M&A)

Acquiring local firms allows quick entry and immediate access to established operations. For example, Walmart’s acquisition of Flipkart in India provided a strong foothold in the Indian e-commerce market.

g. Digital and E-commerce Expansion

Firms are increasingly using digital channels to reach regional markets cost-effectively. E-commerce platforms enable global brands to operate regionally without physical infrastructure.

4. Key Regional Growth Models Across Continents

1. North America

The North American market, led by the United States, offers advanced infrastructure, high consumer spending, and a stable regulatory environment. Companies focus on innovation-driven growth, brand differentiation, and digital transformation. For example, Tesla’s regional strategy involves expanding production across multiple states and developing localized supply chains for electric vehicles.

2. Europe

Europe is a complex but lucrative region due to the European Union’s single market framework. Regional strategies here emphasize sustainability, compliance with EU standards, and cultural diversity management. Many firms adopt green technologies and ethical business practices to align with European consumer values.

3. Asia-Pacific

Asia-Pacific (APAC) is the fastest-growing region globally. Its diverse economies — China, India, Japan, South Korea, and ASEAN nations — present both opportunities and challenges. Strategies here focus on mass customization, digital-first marketing, and regional production hubs. For instance, Samsung and Huawei leverage regional R&D centers to innovate products tailored for Asian consumers.

4. Latin America

Latin America’s regional strategy revolves around price-sensitive consumers, economic volatility, and political uncertainty. Firms often adopt localized pricing, distribution through regional partners, and community-based marketing to gain traction.

5. Middle East and Africa (MEA)

The MEA region offers vast opportunities due to its growing youth population, digital adoption, and natural resource wealth. However, it also poses regulatory and infrastructural challenges. Successful regional strategies here include partnerships with local conglomerates, adapting to religious and cultural norms, and investing in sustainable infrastructure.

5. Regional Trade Blocs and Their Strategic Impact

Trade agreements and economic blocs shape regional growth strategies significantly. Some key examples include:

European Union (EU): Facilitates tariff-free trade and uniform regulations across member countries, encouraging firms to set up pan-European operations.

North American Free Trade Agreement (NAFTA) (now USMCA): Promotes trade between the US, Canada, and Mexico, encouraging integrated manufacturing and cross-border supply chains.

Association of Southeast Asian Nations (ASEAN): Provides access to a large consumer market with reduced trade barriers.

Mercosur (South America): Enhances trade cooperation among Argentina, Brazil, Paraguay, and Uruguay.

African Continental Free Trade Area (AfCFTA): Aims to create a unified African market, attracting global investors.

Companies strategically align their regional operations to take advantage of these trade frameworks, optimizing cost structures and supply chain efficiency.

6. Challenges in Implementing Regional Growth Strategies

While regional expansion offers significant opportunities, it also presents challenges that businesses must manage carefully:

Regulatory Complexity:

Each region has its own legal requirements, taxation rules, and trade policies. Navigating these can be time-consuming and costly.

Cultural Barriers:

Misunderstanding local customs, values, or communication styles can lead to marketing failures and brand rejection.

Political Instability:

Regions with political volatility or weak governance pose risks to investment and operations.

Economic Inequality:

Income disparities within and across regions affect pricing strategies and product positioning.

Competition from Local Firms:

Domestic companies often understand the market better and can respond faster to changes.

Supply Chain Disruptions:

Global crises (like the COVID-19 pandemic) highlight the vulnerability of extended supply chains and the need for regional diversification.

7. Strategies for Successful Regional Growth

To ensure sustainable success, firms should follow structured approaches:

Market Research and Data Analytics:

Understanding regional demographics, purchasing patterns, and competitor behavior is crucial before entry.

Localization and Cultural Sensitivity:

Customizing marketing, communication, and product offerings to suit local tastes builds trust and engagement.

Strategic Partnerships:

Collaborating with regional firms, distributors, or technology partners enhances market penetration.

Agile Operations:

Adopting flexible supply chains and decentralized decision-making allows quick adaptation to local market shifts.

Talent and Leadership Development:

Hiring local management teams familiar with the regional context improves responsiveness.

Digital Transformation:

Leveraging digital tools, e-commerce, and regional analytics helps firms engage customers efficiently.

Sustainability and CSR Integration:

Consumers increasingly prefer brands that demonstrate responsibility toward regional communities and the environment.

8. Case Studies of Regional Growth Success

Coca-Cola

Coca-Cola’s success lies in its ability to think globally but act locally. The company customizes flavors, packaging, and advertising campaigns to reflect local cultures. For instance, in Japan, Coca-Cola offers unique beverages such as green tea and coffee blends under regional sub-brands.

Unilever

Unilever’s regional strategy combines global brand consistency with local product innovation. It invests heavily in emerging markets like India and Indonesia by offering affordable product sizes suited for lower-income groups while maintaining sustainability goals.

Toyota

Toyota uses a regional production model, setting up manufacturing hubs in key markets to serve local demand efficiently. Its “Kaizen” philosophy of continuous improvement is applied globally but adapted regionally to meet workforce and cultural variations.

Netflix

Netflix’s regional growth strategy focuses on content localization. By producing region-specific shows in local languages (like “Money Heist” in Spain or “Sacred Games” in India), it successfully appeals to diverse audiences worldwide.

9. The Future of Regional Growth Strategies

The future of regional strategies will be shaped by three key trends:

Digital and AI Integration:

Artificial intelligence will help companies analyze regional markets in real-time, personalize offerings, and automate regional operations.

Sustainability Focus:

Green technologies and responsible supply chains will be central to regional competitiveness.

Geopolitical Realignments: