FUBO US LongFuboTV (FUBO) has shown significant growth recently, and there are several reasons for this.

In Q2 2025, FuboTV reported

EPS of $0.05, which exceeded analysts' forecasts (-$0.05)

Revenue of $371.3 million, also above expectations ($353.72 million)

The company achieved positive adjusted EBITDA for the first time at $20.7 million

Net loss narrowed to $8 million compared to $25.8 million a year ago

Recent partnerships with DAZN (NFL and UEFA Champions League broadcast rights)

Debt reduction is slow

The number of shares outstanding is increasing

multipliers are low due to the described disadvantages

OCF and FCF entered the positive area. This will limit further additional share issues.

All this has led to improvements in investor sentiment in this issuer.

We will join the long

A3minvestments

IVAT RU ( IVA Technologies) Long#Invest #Russia #IVAT

IVA Technologies offers a wide range of products united in a single ecosystem:

IVA Connect: Corporate messenger for fast communication between teams.

IVA MCU: Video conferencing platform, which is the leader among Russian solutions for the corporate sector

VKurse: Cloud platform for video conferencing.

IVA GPT: AI assistant for business, providing automation of tasks and analytics.

IVA CS: Corporate telephony server.

IVA Room and IVA Largo: Video terminals for negotiations.

VA SBC: Session Controller for Secure Communications

Other Products: IP Phones, Management and Monitoring Systems

IVA Technologies is the leader in the Russian video conferencing market with a 33% share in the corporate segment

The company plans to increase its market share to 91% in 2028

In July 2025, IVA Technologies announced a partnership with the Physicotechnical Institute, which acquired a minority stake (about 1%) from existing shareholders

The news caused a stir in the market, and the shares rose by 75% in four days

IVA Technologies actively invests in the development of new products and technologies. In the first half of 2025, capital expenditures (CAPEX) increased by 75% to 973 million rubles

The company created an artificial intelligence laboratory that focuses on the development of video analytics systems, business process automation and AI tools for developers

Partnership with the Physics and Technology Institute can help IVA Technologies enter international markets

The fund has the resources and expertise to support international expansion

Although revenue for the first half of 2025 remained at the same level as last year (1.07 billion rubles), EBITDA increased by 11% to 2.3 billion rubles, and cash flow from operating activities increased by more than 3.5 times

The company has a small debt

net debt/EBITDA 0.2

The downside is low NAV with high capitalization, i.e. high P/B.

The market believes in the success of the company, its further expansion and growth of financial indicators

SIL ETF US- Silver Miners Mid Term ideaFollow us and don't miss a next idea on global markets

According to Mining Visuals Silver deficit is expected of 118 million ounces. At the same time strong industrial demand - driven by solar, electronics and green technologies.

Historically, mining stocks outperform the growth rates of the metals themselves. This hypothesis is confirmed by the fact that, starting in 2024, ETF SIL (silver miners) has outperform the metal itself.

From a technical point of view, ETF SIL has emerged from a long-term consolidation and there is a high probability of growth to the $80.

USDRUB upside potential 20%Almost 2 years later, the government completely abolishes the mandatory sale of foreign currency earnings for exporters.

The Central Bank of the Russian Federation has begun a cycle of rate cuts.

The budget deficit continues to worsen. The budget needs a higher exchange rate

Today, the Central Bank of the Russian Federation is very tightly clamping down on the money Supply and historically this has led to a sharp jump in the exchange rate

We expect the usdrub to be around 95 rubles per dollar

Stock Market is in Risk OnSubscribe and don't miss next ideas

The US market, as well as some assets, is in a risk-on mode.

Most assets have their own seasonality.

The chart above shows one of them:

In recent years, in the period July-September, a correction began on the US market.

A number of macro indicators also speak in favor of a correction and that it is overdue.

Risk appetite according to Morgan Stanley research has reached a historical maximum

Although seasonality does not guarantee a correction right here and now, but at least it gives reason to think about reducing long positions

SOUN US ( SoundHound AI) LongLong

Exit from triangle upward

Retest of the level

SoundHound AI Reports Record Q2 2025 Revenue of $42.7M, Up 217% YoY

The company raised its full-year 2025 revenue guidance to a range of $160M-$178M (midpoint of $169M), above analysts’ previous expectations of $159.6M

Management expects to achieve positive adjusted EBITDA by the end of 2025

SoundHound is aggressively expanding its voice AI solutions into new industries, including automotive, quick-service restaurants (QSR), healthcare, IoT, and financial services

The company has added computer vision capabilities to its voice platform

The company has a unique technology called Houndify that allows brands to build their own voice assistants with customization, analytics, and real-world data integration

SoundHound had $230M in cash reserves and no debt at the end of Q2 2025

Gold. Expect entry into the fifth waveThe current decline looks like the 4th wave

Before it, 3 in 3 is visible

There is an alternative probability of the marking, that the marking will lengthen and we will get a stronger upward impulse.

But in both scenarios there is another increase in quotes with a target of 3600-3650

In general, the growth of gold is due to a reduction in central bank investments from American treasuries.

Just today we described how investments of India and other non-Western countries in American debt are decreasing.

All this spurred the growth of gold quotes

VRSN US ( VeriSign) LongVeriSign is a key player in the management of .com and .net domain names, processing over 132 billion DNS queries per day

VeriSign has a near-monopoly position in the management of .com and .net domains (146.4 million registered addresses)

Domain renewal rates have increased to 75.5%

EPS was $2.21 in the last quarter, compared to the forecast of $2.20

Revenue has been growing steadily: in the last quarter it reached $410 million, which is 5.9% higher compared to the same period last year

🐻The recent sale of 4.3 million shares of Berkshire Hathaway caused a short-term correction, but it was due more to regulatory reasons (share decline below 10%) than fundamental problems

The board of directors approved a significant share buyback program

The correction is over.

The stock has left the channel upwards.⚡️

We are waiting for a test of the open gap level from above🚀

We are not positive about TeslaFollow us and don't miss a next idea on Global Markets

The impact of tariffs and expiring EV credits is expected to pressure future US deliveries and regulatory credit revenue in the near term

Elon Musk: Well, we're in this weird transition period where we will lose a lot of incentives in the US. Slab incentives actually in many other parts of the world. But we'll lose them in the US. Across all of it at the relatively early stages of autonomy. On the other hand, autonomy is most advanced and most available from a regulatory standpoint in the US. Does that mean we could have a few rough quarters? Yeah. We probably could have a few rough quarters. I'm not saying that we will, but we could. Q4, Q1, maybe Q2.

Revenue -12% y/y ( decline for the first time in 10 years)!!!

EPS 0,27 $ agj vs 0,39 $ estimated

FCF -89% y/y but still positive ( just 146 M$)

CAPEX for 2025 increased

EBITDA dropped by 7.8%.

Price to Sales 12,7

P/B 14

Expensive

We expect declining of the stock price to 210 $

And, yes, many still regard Tesla as a car manufacturer, but this is not a correct view of the company. Later in our blog we will touch on the question of how to correctly look at the brainchild of Elon Musk.

The report is good, but there is no stock dynamicsMSFT gapped up at around $555 on the report and reached a market cap of $4.1 trillion

This happened because the report significantly exceeded expectations on key metrics

The latest quarterly report showed record results.

Revenue for the quarter was $76.4 billion (up 18% y/y)

Net income was $27.2 billion (up 24% y/y).

EPS was $3.65, exceeding analysts' expectations

However, the shares are falling and are already below the level they were before the report.

Capex was increased to $24.2 billion (up 27% YoY)

For fiscal 2026, management forecasts further Capex growth (over $30 billion in Q1 alone)

Operating expenses increased 6% YoY due to investments in AI and engineering

The company recorded $1.71 billion in other expenses in the quarter, partly related to losses on equity investments (likely in OpenAI)

In the call with investors, the company's management warned market participants about further margin compression in the short term and higher-than-expected capital expenditures on AI infrastructure.

Accordingly, this raises questions about the future profitability of both the investments themselves and the future results of the company as a whole, which will be released in future reports.

Professional investors have begun to change their DCF models in accordance with the new data.

From a “tech” perspective, we are seeing weaker dynamics in the broad market.

It is clear how the company's comments have broken the up trend that has been observed in recent months.

We expect further cooling of sentiment in the stock, the closing of another gap from below and a slide in the price to the $400-420.

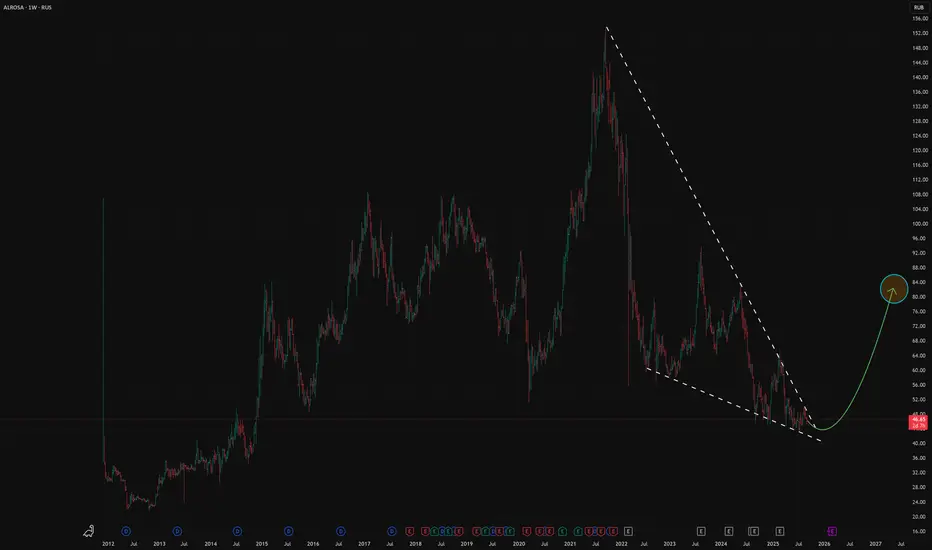

Alrosa is the Most Efficient Diamond Mining Company in the WorldWe have already made a note about the diamond mining industry in the World.

We will add information to this post and present it as an investment idea for subscribers from Russia

There are two main companies in the World diamond mining market: Alrosa (Russia. World market share ~28%) and De Beers (US. World market share ~22%)

Even with the dollar below 90 rubles and with sanctions obstacles, it remains profitable

At the same time, American De Beers reduced production by 36% in the second quarter of 2025 compared to the data of a year ago

EBITDA will be negative for the second half of the year in a row

If EBITDA is negative, then operating profit is deeply negative.

Another company from this sector, Petra Diamonds, is trying to survive in 2025, although only 3 years ago it underwent restructuring and zeroed out its net debt.

The rest of the sector is doing even worse

Judging by the state of affairs at De Beers, a significant share of the world's capacity is unprofitable at current diamond prices.

The main thing is that ALROSA is operationally profitable in the most difficult conditions, unlike its competitors.

ALROSA has a very large working capital

The basis of working capital is ready-to-sell diamonds

ALROSA has already incurred production costs to extract these diamonds from the ground, but has not yet received revenue.

ALROSA can get about 25% of its capitalization from working capital in the future by selling off stocks.

We indicated earlier in the post why demand for diamonds will return

Russia's Stock Market On The Brink Of a Major RallyIn this world, everything is subject to change. Not so long ago, we all observed colossal pressure on Russia. And last month, in Alaska, for the first time in many years, the presidents of Russia and the United States met.

This is the first step in big geopolitics, and also opens up great opportunities for the Russian stock market.

Earlier, we wrote in a note about USDRUB that we expect a further reduction in the Central Bank of the Russian Federation's key rate. This will not only cause USDRUB to grow, but will also lead to a revaluation of companies in Russia.

Today, the yield on Russian government bonds is 14% with a key rate of 18%. As the key rate decreases, the yield on government bonds will also decrease, which will cause a flow of money from bonds to stocks. At the end of next year, the CBR rate will be about 10%.

The dividend yield on stocks in the Russian Federation is around 10-12%. Investors will be pricing in further rate cuts, which will cause stock revaluations

As the Ukrainian conflict ends, sanctions against Russia by the United States will be partially lifted, which will reduce the geopolitical discount of risky assets in the Russian Federation.

The weakening of the ruble will also help Russian exporters with revenue and profit.

The stock market was under pressure not only due to geopolitical factors, but also due to the actions of the CBR, which, in addition to a strong rate hike, greatly compressed the M2 money supply. This led to historically low stock multiples (P/E, P/B)

From a technical point of view, the market is finishing the last wave E in a triangle and with a further upward exit

Statistical Research. BitcoinToday we will touch upon such type of analysis as seasonal patterns in Bitcoin

Bitcoin seasonality is cyclical patterns in its price dynamics, repeating in certain calendar periods (months, weeks, days). These patterns are formed under the influence of many factors:

1. Halving

Historically, Bitcoin's four-year cycles tied to halvings (halvings of the mining reward) have been a key driver of price highs. Bullish rallies peaked approximately 1060 days after the previous cycle bottom.

At the same time, changes have already begun to occur in these statistics:

According to some Research notes that the impact of halvings on the Bitcoin price has significantly decreased:

- Bitcoin is increasingly responsive to global macroeconomic factors such as inflationary pressure, geopolitical tensions, and monetary policy (especially the US Federal Reserve). This pushes purely internal factors, such as halving, into the background

- Characterizes Bitcoin as a transition from a "speculative reflexive asset" to a more established "reactionary store of value"

2. Macroeconomic events (changes in interest rates, inflation)

It is necessary to remember that Bitcoin is not a defensive asset, as some call it, but belongs to the category of risk-on assets.

Therefore, it, like risk assets, is affected by inflation and interest rates, primarily in the US.

Since the price of risky assets is very strongly influenced by the Fed's policy, very strong fluctuations will occur not even on the fact of changing interest rates from the Central Bank, but on the outgoing macroeconomic indicators, which, in the opinion of market participants, the Central Bank (the Fed, the ECB, etc.) will look at.

3. Institutional activity.

The creation of Bitcoin ETFs is beginning to have a strong impact on the BTC spot market. For example, by the third quarter of 2025, American Bitcoin ETFs attracted $118 billion inflows. BlackRock's IBIT alone manages assets worth $50 billion

Corporations have begun to buy cryptocurrency: MicroStrategy and Tesla.

4. News related exclusively to the cryptocurrency market and transactions with them. For example, network updates.

Now we move on to statistical models:

The strongest months in Bitcoin: March, October

Weak months: August and September

This does not mean that every code the market will grow in March and October, and fall in August. This note can help in combination with other types of analysis.

Best days for Long:

February 1, February 14, March 26, September 22, October 29, November 29

Best days for Short:

February 13, April 17, June 18, July 5, August 2, October 2

Also note that these are average statistics. At the very least, it is necessary to know them.

5. Flow of funds within the cryptocurrency market:

Bitcoin, as the main cryptocurrency, dominates at the beginning of the bull market, then capital moves to altcoins

What we have now:

Analytical companies draws attention to the ongoing outflows from spot BTC ETFs

Also according to these studies, the peak may already be reached in this cycle

We also pointed out in another post about the S&P500 that statistically we are entering a weak period.

ECL US ( Ecolab ) LongLong

Retest from top to bottom of level

strong impulse

Operating margin expanded 170 basis points in Q2 2025

Management forecasts adjusted EPS growth of 12-15% in 2025-2026

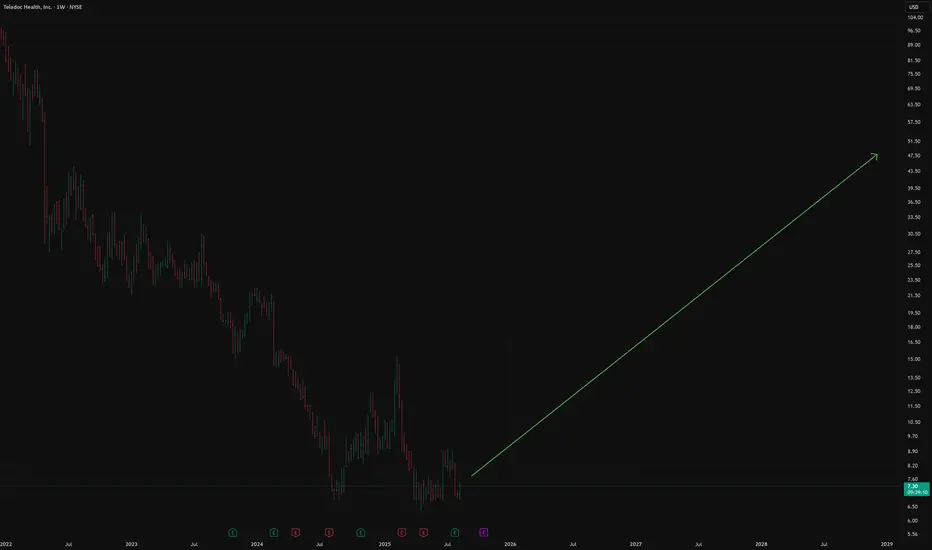

Teladoc Mid-Long term ideaTeladoc Health is a company specializing in telemedicine and virtual healthcare.

The company gained wide popularity during the covid-19 pandemic.

The company has historically expanded its operations through M&A:

In 2013 and 2014, the acquisition of Consult A Doctor, AmeriDoc allowed Teladoc to become one of the largest telemedicine companies in the United States.

Today, the company is valued by the market as value, although a few years ago the valuation was growth. Why did this happen?

As part of its strategy, the company's previous CEO had aggressive M&A deals on credit.

In 2021, TDOC's revenue growth began to slow rapidly. And in Growth companies, growth rates determine, if not everything, then a lot, including market valuation.

Price/Sales 2020 at its peak was over 30, which is very expensive. Before the company's triumph in 2020, the valuation was around 10. Today, P/S is only 0.5

It is necessary to separately touch upon such a parameter as the company's balance sheet and valuation through the prism of the P/B multiplier. The balance sheet grew rapidly in 2020, but it was done through the growth of goodwill, and not through the growth of fixed assets. In general, the growth of goodwill in the balance sheet is an extremely interesting thing and we will discuss this in the following posts. Starting in 2022, the company's balance sheet began to decline sharply, but the write-offs were NON-CASH, and there was a revision of that same goodwill.

On average, the company's P/B was around 4-5 and at its peak it reached 15. Today, the market values companies at 0.9, and this is despite the fact that the main write-offs have already occurred. The company has a debt of 0.99 B$

Cash and cash equivalents 0.67 B$

Which gives us a net debt of 314 M$

The company's revenue has been stagnating since 2023 and is 2.54 B$ TTM

The good thing is that starting from the same 2023, EBITDA began to grow from 0.066 B$ to 0.160 B$

OCF is positive

2022 193.99 M$

OCF today 303 M$ TTM

FCF is positive

2022 16 M$

2025 151 M$ TTM

The company today has a stable financial position with a net debt of 314 M$ and FCF 150 M$

In June 2024, Chuck Divita was appointed as the new CEO of the company, who is trying to put TDOC back on the rails of revenue growth and restart revenue growth while maintaining current margins. The first steps in this direction have already been taken and in February 2025 Teladoc acquired Catapult Health for 70 M$ in order to launch a sales funnel.

Also, in the near future, the Fed will begin to lower rates and since TDOC belongs to the small caps category, this will help in the revaluation of both the sector and Teladoc itself.

Conservative targets can be called 45-55$ , closing the very gap when the company made a large write-off of goodwill in the report.

In general, we make the target 80-100$