BABAWith monthly - weekly - daily momentum all in oversold territory, BABA is currently sitting just above a crucial support on the weekly chart.

I will be expecting a bounce and spending some time in the highlighted area for a while..

I'm on the long side as it has more probability in my point of view and last weeks close was a gravestone doji. I think we are finding the bottom finally to neutralize the trend.

Peace..

Alibabalong

BABA - Are we there yet? - FIB Retracement to 0.786 (big picture).

- Confluence @ key support - 2014 & 2016 highs.

- Completed 5th Elliotte wave.

- Bullish Inside week candle formed at support.

- Daily MACD just crossed.

- Weekly and Daily RSI divergence.

- MOMO indicator triggered (78min).

Simple play BABA

"The chart speaketh for itselfth" ~ Sir Michaele Tython the great derithative thrader

You can see we touched trendline, presuming a nice bounce, Alibaba is a behemoth in China, CCP won't let it fail, Fundamentally sound and strong. Watched a Video on VIES structure featuring Chamath, it's pretty funny and good but this would also be a good swing trade play. Of course we'll never know the company inside out but it's at x2 it's BV, so a good chance it will find very strong buyers if it drops to 100$.

RSI oversold, notice the 2 year cycle? It's gonna be an interesting 2 years that's for sure. Taking a long position, and by long I mean schlong.

Worst case scenario it gets delisted but that is highly irrational, given the amount of US investors like Munger who love this.

(Disclaimer, not financial advice, just a bit of fundamentals mixed with technicals)

NYSE:BABA

Dont MISS this Buy ALIBABA AliBaba is greatly Undervalued, a historic chance to enter these levels, if you fall lower add seriously

Significantly Below Fair Value: BABA is trading below fair value by more than 45% .

I will reiterate my long-term bullish call on BABA

BABA UPTREND SOONAlibaba dipped so much this year, I think we will see a very big uptrend this upcoming year.

if you have any feedback about the chart pls feel free to tell me:)

MY IDEA ONLY NOT A FINANCIAL ADVICE!!!

Love Yall :)

BABA Amazing Long OpportunityBABA has retraced from its all time high a lot

This is ok, as it has provided a lovely buy opportunity (buy the dip)

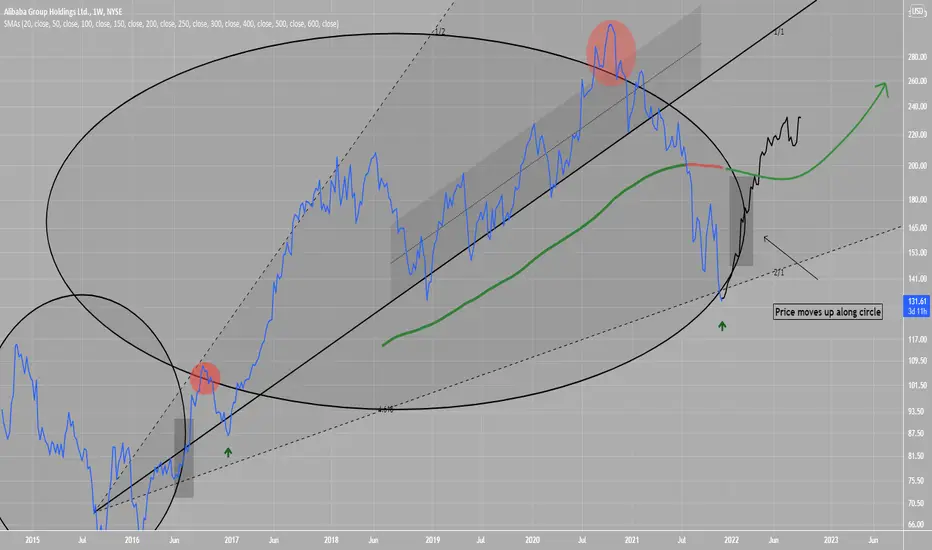

I expect price to move up along the 4.618 circle, and make a recovery

Attaching my thoughts about how price tends to move up along the circle.

BABA - STOCKS - 18. OCT. 2021Welcome to our Weekly V2-Trade Setup ( BABA ) !

-

4 HOUR

Alibaba group undervalued currently.

DAILY

Most investors panic selling.

WEEKLY

Overall great technical setup!

-

STOCK SETUP

BUY BABA

ENTRY LEVEL @ 168.02

SL @ 151.47

TP @ Open

Max Risk: 0.5% - 1%!

(Remember to add a few pips to all levels - different Brokers!)

Leave us a comment or like to keep our content for free and alive.

Have a great week everyone!

ALAN

My perception of Alibaba's weekly stock chartMy perception of Alibaba's weekly stock chart as follows !

After a five-wave with three continuous shares, it enters a correction in the form of a second wave. This is formed as a flat with a big b wave. maybe just it want to make triangle to ready for powerful third wave .. so buying and maintaining it at prices from $ 140 to $ 150 is extremely attractive

Considering the time of the second wave, , it noted that the third wave is the main continuous wave and has very high goals .. maybe above $ 1500 😁 .. so the long holding stock may not be bad .. though it does bother you a little over time

BABA: Alibaba's future looking goodBABA trying to break the resistance line! Looking to crate a higher low, so that we change the down trend! If it breaks the resistance line it will have a great upside move! Also waiting for the results coming out on the 18th which will decide its future! Positive results, will lead BABA faster to the upside move! Big investors and hedge funds are already in, its a matter of time for it to go up

ALIBABA BREAKOUT?Going to long BABA here with a tight sl and great r/r. The reason im having this tight of an sl is because im not really fan of the whole evergrande situation happening right now. Tps are the black lines. DYOR ;)

Alibaba | Fundamental Analysis + Next target 🔔Chinese e-commerce behemoth Alibaba Group Holding has become one of the top investment trends of 2021. Over the past year, the company's stock has dropped more than 50% of its value, almost inaudible for a company of this size and status.

The stock recently rebounded 15% from its 52-week lows, and investors are curious if the drama is over. And today's review will tell you just why you should be cautious about returning to the Alibaba rollercoaster.

The most interesting thing about Alibaba's troubled year is that it has scarcely anything to do with real business. It is the powerful e-commerce business in China's vast economy, and nearly 1.2 billion people worldwide have used its services in the past year. BABA posted revenues of $31.8 billion in its most recent quarter ended June 30, up 34% from the pandemic peak in mid-2020. The business is undoubtedly effective and brings a lot of free cash flow: $3.2 billion per quarter, or 10% of revenue.

Over the past year, the Chinese government has taken a decisive stance and has become more active in intervening in large Chinese technology companies. Chinese President Xi Jinping has stressed the need to distribute wealth from large corporations to the Chinese population through social programs, infrastructure, etc.

He is putting pressure on dominant Chinese technology companies because China has the regulatory authority to advance them with antitrust lawsuits. Chinese regulators have already fined Alibaba $2.5 billion in antitrust investigations. Perhaps, as a result of this pressure, Alibaba has agreed to donate 100 billion yuan ($15.5 billion) over the next five years to social needs. Given the company's free cash flow of $3.2 billion last quarter, this is a meaningful figure. That's less cash to invest in business development and less money for the company's shareholders.

In late 2020, Chinese regulators blocked an initial public offering by Chinese fintech company Ant Group, which would have valued the company at about $300 billion. Like Alibaba, Ant Group is another business headed by Jack Ma and owns China's largest digital payments platform. Regulators have forced Ant Group to restructure its business to comply with Chinese regulations, separating its Alipay platform from its lending business and sharing ownership of its newly created customer data business with the Chinese government. This definitely turns Ant Group into a bank and gives the Chinese state access to Ant Group's consumer data, the "secret sauce" of the business. Alibaba owns a third of Ant Group, and the halt of its IPO is a value-destroying event that probably played a role in Alibaba's stock decline.

China creates political problems for Alibaba and similar technology companies that are hard for investors to predict. What happens if the Chinese government decides to take more funds from tech companies? What if regulations become even stricter? Investors have little ability to assess these risks.

As a result, Alibaba's stock is selling off as investors try to factor in these risks. Analysts forecast revenues of $140 billion for the entire fiscal year 2022 (the calendar year 2021), resulting in a stock price-to-sales (P/S) ratio of just over 3.

Before the pandemic, the stock was trading at a P/S ratio of 10, so it's obvious how much the stock price has declined while the core business keeps expanding. If we go back even further, to three years ago, the P/S of the stock was 15. In other words, the stock's valuation has declined 80% over the past few years. Wow! Right?

Let's compare Alibaba to Amazon, a similar company: an e-commerce giant with additional segments like cloud services. Amazon's P/S has never surpassed 5 in the last five years, meaning that at the peak of the P/S ratio Alibaba was valued at five times the price of Amazon stock. Amazon's P/S is currently 3.4, which is only 10% higher than Alibaba's, which may be fair since they are very similar. Alibaba is smaller and may grow a little faster, but then you have to consider the political risks and the company's huge donations to China's social programs.

So it would be logical to argue that Alibaba should trade at a discount to Amazon, as it does now. But if you want to absolve doubts about Alibaba, it would still be difficult to justify a significant premium over Amazon's price. It may turn out that Alibaba has been expensive for years and that much of the fall was due to the stock coming to a more adequate valuation, rather than the fall being a once-in-a-lifetime buying opportunity, as some investors think. This means that Alibaba does not have as many prospects as it appears at first glance, and so investors might think twice before grasping Alibaba's recent bounce.

ALIBABA weekly Alibaba on the way to 250$, macd looking pretty good! First resistance will be at the 50 day moving averge

BABA stock will be good for long termBABA stock will be good for long term

the target in chart

Regards,

BABA Daily TimeframeSNIPER STRATEGY

This magical strategy works like a clock on almost any charts

Although I have to say it can’t predict pullbacks, so I do not suggest this strategy for leverage trading.

It will not give you the whole wave like any other strategy out there but it will give you huge part of the wave.

The best timeframe for this strategy is Daily, Weekly and Monthly however it can work any timeframe above three minutes.

Start believing in this strategy because it will reward believers with huge profit.

There is a lot more about this strategy.

It can predict and also it can give you almost exact buy or sell time on the spot.

I am developing it even more so stay tuned and start to follow me for more signals and forecasts.

Alibaba 4H - LONGStock Market Trading is dangerous and non profitable for most of you out there. Follow signals, make money. Period.

How to use my signals?

LONG: Buy and hold as long as the price stays above the green zone.

SHORT: Sell and hold as long as the price stays below the red zone.

ALIBABA:FUNDAMENTAL ANALYSIS+PRICE ACTION|NEXT TARGET|LONG🔔🔔Shares of Chinese tech giant Alibaba Group Holding fell 14.4 percent in August, according to S&P Global Market Intelligence. Although Alibaba became the first major Chinese tech company to face fines and regulations late last year, the punishment continued in July, when shares fell 13.9%, and in August, when shares fell another 14.4%.

The culprits behind Alibaba's continued August decline in shares were an earnings report that fell short of expectations for the top line, and continued, escalating regulatory aggression against the Chinese Internet giant.

In early August, Alibaba reported quarterly earnings that beat earnings expectations but fell short of earnings expectations. With such low sentiment, the mixed results were probably enough to worry investors that regulations are starting to affect the company's financial performance.

Previously, Alibaba had used its first-mover advantage to squeeze out competitors, often forcing brands into exclusive contracts to gain access to its market-leading e-commerce platform. But in April, the company was fined $2.8 billion for violating antitrust rules and was ordered to stop the practice. Ending forced exclusivity could strengthen upwardly mobile e-commerce challengers, so the fact that Alibaba's revenues came in slightly below expectations is not a good sign.

The situation didn't get any easier as the month progressed. In mid-August, the State Market Regulation Administration issued a comprehensive list of rules prohibiting tech giants from illegally collecting and using customer data or using technology to deny access to competitors' products. As one of the largest and most powerful "legacy" technology platforms in China,

Alibaba is likely to lose more than its competitors as the rules are designed to level the playing field. The Ministry of Transportation has also begun work on rules to ensure the welfare of delivery drivers, which could affect the cost of food delivery for Alibaba subsidiaries Ele.me and Freshippo.

A series of new rules will undoubtedly hit Alibaba's financial performance. But it doesn't look like the company will disappear anytime soon. After all, last quarter the company's revenue was up 34%, though, minus the effect of Alibaba Sun Art's retail consolidation, it was only 22%.

After such a brutal collapse, the company's stock looks cheap: it's trading at about 17.9 times this year's projected earnings -- and that's with a significant net cash position and tens of billions in minority investments in other companies. Alibaba stock had already attracted prominent value investors Charlie Munger and Bill Miller earlier this year, and now its value has dropped significantly.

Thus, Alibaba could be a good deal for patient investors if they can pay attention to the key factors. And here are three factors supporting Alibaba.

1. Dominating business in China

According to Goldman Sachs, Alibaba dominates the e-commerce market with a 69% share by 2020, making it the Chinese Amazon. Alibaba has 912 million active customers in China and 1.17 billion worldwide. In 2020, the company will have a gross market size of $1.2 trillion, representing the value of all transactions flowing through Alibaba's business.

Alibaba also owns a 33% stake in Ant Group, a major payment company in China that operates Alipay, which handles more than half of third-party payments in China. In other words, Alibaba is relevant to many aspects of the Chinese consumer and their economic activity.

2. Fantastic financial performance

In 2020, Alibaba's revenue grew 41% to $109 billion, aided by consumers using online services during the pandemic. In the first quarter of 2021 (ending in June), the company saw rapid revenue growth of nearly $32 billion, 34% more than in 2020. Alibaba is expected to generate $143 billion in revenue by the end of the year, a 30% increase.

The company is also very profitable. It converted $3.2 billion of first-quarter revenue into free cash flow and now has $72 billion in cash, cash equivalents, and short-term investments on its balance sheet. This gives Alibaba tremendous financial flexibility to create/develop new business segments or acquire emerging competitors.

3. It's a bargain buy

Even though the company's stock price is falling, Alibaba's continued growth is driving the stock down. Last fall, the stock was trading at a price-to-sales ratio of nearly 8, and today it is less than 4 when using the expected full-year earnings for 2021.

In terms of earnings, we can use the price-to-earnings ratio to take another look at Alibaba's valuation. The company is expected to earn $9.70 per share in 2021, resulting in a price-to-earnings (P/E) ratio of 20, which is about a third less than Amazon's current P/E ratio if we use its expected 2021 earnings per share.

Alibaba stock seems very inexpensive given its dominant position in China and its ability to grow its huge revenue by 30% - and remain profitable.

Alibaba is a unique company that offers investors growth, strong fundamentals, and an attractive valuation, but despite all these positive factors, it is risky. The company may continue to trade at a lower valuation than companies such as Amazon for a long time to come because investors can never be completely sure that political risks will not emerge in the future.

Nevertheless, Alibaba stock is like a "coil spring," which could unleash strong gains if investor sentiment becomes more favorable. This upside potential makes Alibaba an interesting idea for savvy investors.

BABA Long Term Weekly Chart Weekly Chart for ALl BABA holders

Be strong we will see all target

HOOOOLD

Regards NYSE:BABA

ALIBABA, SPECULATION MODE ON!Alibaba Group Holding Limited, also known as Alibaba Group and Alibaba.com, is a Chinese multinational technology company specializing in e-commerce, retail, Internet, and technology.

Strong divergence on the monthly. The price level at which Alibaba now stands has always been characterized by high volatility in the past. The market has always reacted with a reabsorption over 60% of the time in the past at this level. This opens the scenario to an interesting short-term speculative operation which, in the event of a positive outcome, could turn into a medium-term operation on an asset which, ignoring short-term problems, creates several points of GDP for the Chinese economy.

High risk transaction, the investor should consider the volatility of the underlying and the riskiness of the transaction in managing this asset.

$BABA | Model Identifies Buy OpportunityHello Traders,

The targets on this chart are produced by a proprietary model. Data is fed into the model, the output is the targets you see on the chart.

In light of recent fundamentals $BABA and a slew of Chinese Stocks have taken a nose dive. My proprietary model is pointing in the opposite direction.

This will be a test for the model.

Alibaba Group Holding $BABA - Bullish idea 💡 This is based on 10D timeframe, the stock in the middle of the demand zone. Selected the best entries. Technical indicators still bearish except on entra day.

✅BABA / ALIBABA 💥+65%RSI at it lowest usually means a buy opportunity.

Warren Buffett use to say “be fearful when others are greedy, and greedy when others are fearful.”