Nuclear Renaissance: Why $NNE is Primed for a 2026 MoonshotCan NASDAQ:NNE find the momentum to return to the upper trend-line?

Technically, we are looking for a continuation of the bounce off the lower boundary to validate the next leg up.

While these lines are extrapolated, the historical respect for this channel suggests a significant 'reversion to the mean' or a push toward the upper standard deviation if the current news cycle continues to favour small modular reactors (SMRs).

The AI Power Crunch: By 2026, the demand for "always-on" carbon-free power for AI data centres has moved from theory to urgent necessity.

Tech giants like #Meta and #Amazon are actively signing nuclear deals, and NASDAQ:NNE ’s portable micro-reactors (KRONOS and ZEUS) are positioned as the "plug-and-play" solution for these power-hungry hubs.

What do you think? Are we heading back to the top of the channel, or is a breakdown imminent?"

Artificialintelligence

$AES: Powering the AI Revolution with a Cup & Handle BreakoutThe Bull Case Description

Technical Setup: The Cup and Handle Breakout AES has spent the last several months building a large, rounded "Cup" base, followed by a tight, downward-sloping "Handle" that has successfully stayed in the upper half of the pattern.

Fundamental Bull Case: The "AI Power" Catalyst

Data Center Dominance: AES is the #1 global seller of renewable energy to corporations. It currently has 8.2 GW in signed power purchase agreements (PPAs), specifically targeting the exponential power needs of AI hyperscalers.

Clean Energy Pivot: The company is on track to triple its renewables capacity by 2027 and exit the majority of its coal generation by the end of 2025. This makes it a primary beneficiary of the "Clean, Firm, and Fast" power demand shift.

Financial Stability: Despite a higher debt-to-equity ratio, AES offers a strong 4.9% dividend yield and is projected to see an 8.4% EPS increase in 2026.

Institutional Support: High-tier analysts like Argus and Morgan Stanley have recently upgraded the stock to "Buy," citing its leadership in battery storage and energy transition.

The Verdict: AES represents a rare combination of Deep Value (P/E of ~9.0) and High Growth (AI energy demand). When the technical "Handle" breaks, the institutional rotation into "Energy for AI" should provide the fuel for a multi-month rally.

APLD growing bullishness. Not ready to run to ATHs yet!Cycles analysis is as follows: more range-bound conditions expected on 4 hr tf. I'm looking for retest of 21.6-22$ range for sell-side liquidity run into end of Jan 2026.

After that, the buy-side primary target will be 38$ as we head into March 2026. Looking for another retest of 18.5-19$ one final time in April/early May before we finally complete the consolidation phase on wkly tf & then push higher to ATHs.

NVIDIA’s $20B Groq Move: A Masterclass in AI DominanceNVIDIA recently shocked the tech world with a massive strategic play. The company announced a $20 billion cash deal to license Groq’s technology. This "acqui-hire" secures elite engineering talent, including Groq founder Jonathan Ross. NVIDIA is aggressively reinvesting its massive cash pile to secure total future dominance. The market responded instantly, pushing NVIDIA’s valuation past the $4.6 trillion milestone.

Industry Trends: Navigating the Inference Flip

The AI market shifted fundamentally in late 2025. For years, the industry focused on training massive models. NVIDIA’s Blackwell and Hopper GPUs led that charge. However, revenue from AI Inference (running models) has now surpassed training revenue. This shift, known as the "Inference Flip," demands a new hardware approach.

Training is a one-time event, but inference is a 24/7 utility. Every chatbot response or robotic movement requires high-speed inference. NVIDIA’s move ensures it leads this continuous, high-volume segment of the global economy.

Technology & Science: GPUs vs. LPUs

NVIDIA’s GPUs are powerful "freight trains" built for massive data volume. They excel at throughput but often face latency issues. Conversely, Groq’s Language Processing Units (LPUs) function like Formula 1 cars. They prioritize instant acceleration and real-time speed.

Groq’s chips process up to 500 tokens per second. Standard GPU setups often struggle to reach 100 tokens. By absorbing this technology, NVIDIA bridges its only significant performance gap. This integration provides the low-latency infrastructure required for future agentic AI.

Business Models & Regulatory Strategy

The Federal Trade Commission (FTC) remains a major hurdle for big tech. A traditional merger would likely face a direct block from regulators. NVIDIA’s management navigated this risk with an innovative "reverse acqui-hire" model.

NVIDIA pays for intellectual property and hires core staff. However, the Groq corporate entity technically remains independent. This structure avoids the mandatory waiting periods of the Hart-Scott-Rodino Act. NVIDIA gains the technology today without years of litigation or regulatory delays.

Management & Leadership: Neutralizing the Competition

Human capital is the most valuable asset in this transaction. Jonathan Ross, the creator of Google’s TPU, now joins NVIDIA. This move effectively strips Google of a key architectural visionary.

NVIDIA is not just buying chips; it is absorbing the brains behind them. This leadership transition neutralizes a potent rival. It also deprives competitors of the talent needed to build custom silicon alternatives.

Macroeconomics & Financial Power

NVIDIA’s financials are essentially flawless. The company generated $22.1 billion in free cash flow in just one quarter. Effectively, NVIDIA paid for this expansion with only three months of profit.

The stock trades at a forward P/E of 23x, suggesting strong growth. High interest rates often pressure tech companies, but NVIDIA remains immune. Its cash reserves allow for aggressive expansion while still rewarding shareholders with dividends.

Innovation & Patent Analysis

Intellectual property is the bedrock of NVIDIA’s long-term moat. The company will integrate Groq’s low-latency IP into its upcoming Rubin architecture . This ensures its "AI Factory" platform remains the industry standard.

NVIDIA is evolving from a hardware vendor into a comprehensive AI Operating System . Every patent and strategic hire reinforces this ecosystem. Competitors find it increasingly difficult to offer a viable alternative to the NVIDIA stack.

SUPER MICRO SEMI #SMCI Can bounce hard to $60This stock has been hit hard on prior forecast cuts and underwhelming results.

So after a big derating, a "less bad than feared" can be a classic bullish catalyst.

So after sentiment washed out but secular #AI demand still intact, can encourage dip buying and short covering in this name.

We also have the #ASML rumour of IP leaking and SMCI speeding up their own fabrication technology.

Palantir - H&S - ShortExpecting something like this to play out coming weeks for Palantir. Went short on the top of the right shoulder (It is still in process of being a shoulder).

Gartner | IT | Long at $240.25Technical Analysis

The stock price for Gartner NYSE:IT recently fell below my selected "crash" simple moving average zone (green lines) and touched off the "major crash" area in August 2025. It's been consolidating since. This could signal a near-term bottom. However, if the next earnings aren't up to expectations, I foresee a tumble into the $180s. At a current P/E of 20x, a tumble that low (if long-term guidance remains high vs a near-term outlook is weak) would signal another personal entry.

Insider Trading

December 10, 2025, a Director purchased $9.9 million at $229.57.

In the last 6 months, more buying than selling.

openinsider.com

Growth

Annual EPS is expected to rise from $12.80 in 2025 to $15.03 by 2027 (+19.53%)

Revenue is expected to grown from $6.5 billion in 2025 to $7.2 billion is 2027 (+10.8%)

www.tradingview.com

Action

While there are near-term risks of further decline into the $180's, the recent $9.9 million insider purchase (plus the technical analysis and continued growth) makes me bullish for the longer-term. Thus, at $240.25, NYSE:IT is in a personal buy-zone with further entries possible if there is a drop (but long-term outlook is bullish).

Targets into 2028

$300 (+24.9%)

$329 (+36.9%)

SOFTBANK can drop another 50%Softbank Group shares took a nosedive on Thursday, dragging down Japanese markets as mixed earnings and guidance from cloud giant Oracle raised fresh worries about excessive spending on artificial intelligence.

#Softbank (TYO:9984) dropped 7.7% to a one-week low of 17,210.0 yen by 22:34 ET (03:34 GMT), making it the biggest loser on the Nikkei 225 index, which fell by over 1%.

The decline in Softbank followed a more than 10% drop in Oracle (NYSE:ORCL), which plummeted after its fiscal second-quarter earnings report. Although the company exceeded market expectations for its net income, it fell short on revenue and provided a weaker-than-anticipated outlook for the upcoming quarter.

#Oracle also raised its fiscal 2026 capital expenditure forecast to $50 billion from $35 billion. The mixed earnings, along with expectations of increased capex, reignited concerns about how Oracle intends to profit from its substantial AI data center spending plans. There are also worries about the company’s debt load, following billions in issuances this year, and its significant exposure to OpenAI, which negatively impacted sentiment towards the stock.

BMO analysts pointed out that Oracle’s ties to OpenAI pose some long-term risks, considering the scale of the startup’s spending commitments and uncertainties about how it plans to fulfill those promises.

These worries spilled over to Softbank, which has a heavy investment in OpenAI. Softbank CFO Yoshimitsu Goto recently mentioned to Nikkei that the tech conglomerate is firmly focused on OpenAI and has no interest in funding its rivals.

Confluent Inc | CFLT | Long at $20.55 Technical Analysis

Confluent's NASDAQ:CFLT stock went through a wild decline after its IPO, dropping 84.5% from its high to the recent low. It is currently in a consolidation / "share accumulation" phase (i.e. trading sideways, overall), and the price is riding just below its historical simple moving average. Often, the price will bounce along this area until momentum picks up and then it's off to the races to fill all the open price gaps above on the daily chart. Given the niche this company has in the AI market, I suspect this is the eventual direction the stock price will move. Time will tell, though, and more major downside isn't a non-possibility.

Market Niche

The explosive growth of AI, particularly agentic and generative models, demands real-time data streaming at scale. NASDAQ:CFLT 's Kafka platform addresses this indispensable AI infrastructure demand - accounting for an estimated 35% of market share in the platform segment as of 2025. While AWS and Azure challenge it in their ecosystems, NASDAQ:CFLT is growing and leading the space, overall.

Revenue and Earnings Growth into 2028

122.2% earnings-per-share growth expected between 2025 ($0.36) and 2028 ($0.80).

53.9% revenue growth expected between 2025 ($1.15 billion) and 2028 ($1.77 billion).

www.tradingview.com

Health

Debt-to-Equity: 1x (good)

Altman's Z-Score/Bankruptcy Risk: 2.6 (very low risk, but over 3 is best)

Insiders

Warning: A LOT of selling and no buying.

openinsider.com

Action

The projected growth of NASDAQ:CFLT as the world moves toward agentic AI makes sense. I think the drop in price after the IPO was calculated and there may be a lot of room to run in the next 1-3 years. Insiders selling and the competitive landscape are red flags, but from the technical analysis to the fundamentals, this looks like a promising growth stock. Thus, at $20.55, NASDAQ:CFLT is in a personal buy zone.

Targets into 2028

$28.00 (+36.3%)

$41.75 (+103.2%)

GlobalFoundaries | GFS | Long $33.62GlobalFoundaries NASDAQ:GFS

Technical Analysis:

The price is currently trading below the historical mean (see lines on chart). Given the "newness" of this stock on the market (IPO in 2021), I would often avoid an entry here until more data are gathered to better understand if the downside trend is reversing. However, in an era where AI integration is the future of tech, the growth prospects of NASDAQ:GFS make it undervalued in the semiconductor space. The current fair value is near $20. The price may get there in the near-term. But sometimes future fundamentals outweigh technical analysis... sometimes... Time will tell.

Earnings and Revenue Growth

Forecasted revenue growth between 2025 ($6.75 billion) and 2028 ($8.88 billion): 31.6%

Forecasted earnings-per-share growth between 2025 ($1.62) and 2028 ($3.12): 92.6%

www.tradingview.com

Health

Debt-to-Equity: 0.15x (low, healthy)

Altman's Z-Score/Bankruptcy Risk: 2.48 (low risk)

Insiders

Silent...

openinsider.com

Action

Due to the growth prospects and likely high demand of semiconductors, NASDAQ:GFS is in a personal buy zone at $33.62. This entry goes against some technical analysis guidance (more downside may be inevitable this year), but the *long-term* upside is more than likely there *if* earnings and revenue growth projections are accurate beyond 2025.

Targets in 2028

$39.00 (+16.0%)

$50.00 (+48.7%)

Is Cisco Building the Internet of Tomorrow or Something Else?Cisco Systems has undergone a dramatic transformation in 2025, evolving from a traditional hardware vendor into what the company positions as the architect of secure, AI-driven global infrastructure. With fiscal year 2025 revenue reaching $56.7 billion and a remarkable 30% surge in operating cash flow, Cisco's financial performance tells only part of the story. The company has strategically positioned itself at the intersection of three critical technological timelines: the immediate AI infrastructure boom, the ongoing geopolitical supply chain realignment, and the long-term quantum computing development.

The company's geopolitical strategy has been particularly aggressive. In response to escalating US-China trade tensions and tariffs reaching up to 145% on certain components, Cisco has pivoted its manufacturing operations to India, establishing it as a new global export hub. Simultaneously, the company launched its Sovereign Critical Infrastructure portfolio in Europe, offering air-gapped solutions that address European concerns about digital sovereignty and US extraterritorial reach. These moves position Cisco as the "trusted vendor" for Western alliance infrastructure while monetizing the fragmentation of the global internet.

On the technology front, Cisco has made bold bets on the future. A landmark partnership with IBM aims to build the world's first large-scale quantum network by the early 2030s, with Cisco developing the optical infrastructure to connect quantum processors. The company has also integrated SpaceX's Starlink into its SD-WAN portfolio and participated in NASA's Artemis program. Meanwhile, its AI-native Hypershield security platform, protected by the company's 25,000th patent, and the integration of the Splunk acquisition demonstrate Cisco's push into AI-era cybersecurity.

The convergence of these initiatives reveals a company no longer simply selling networking equipment, but rather positioning itself as essential infrastructure for Western technological sovereignty. With explosive demand from hyperscaler customers generating over $2 billion in AI infrastructure orders and analysts raising price targets amid a 25% stock rally, Cisco appears to have successfully weaponized the geopolitical moment to reinforce its market position for the next generation of computing.

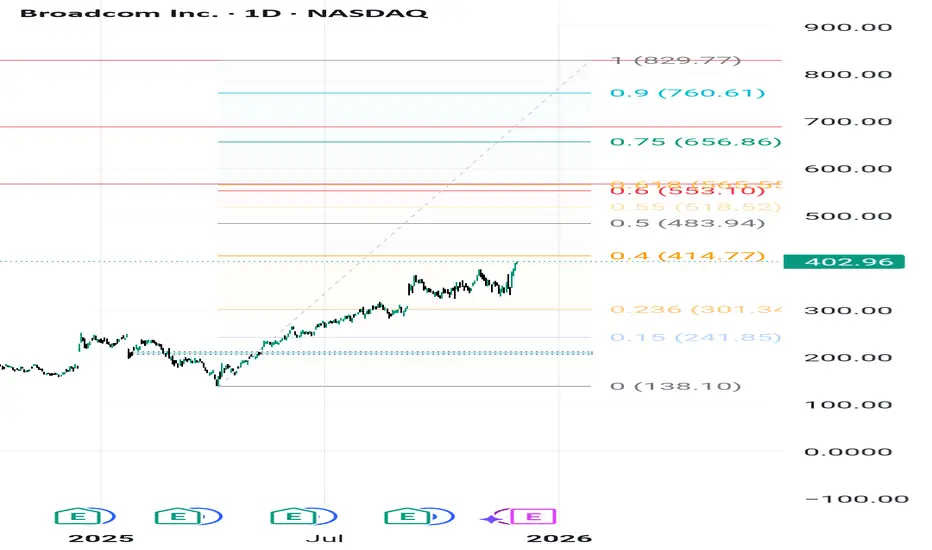

AVGO: Path to $829.77 – Navigating Critical Fibonacci Zones1. Overall Thesis and Price Structure

Broadcom Inc. (AVGO) exhibits a strong underlying bullish trend, fundamentally driven by demand for its AI chips and the successful integration of VMware. The technical objective targets a final high of $829.77. However, the path requires breaking through significant resistance levels defined by the Fibonacci structure. The current price is \mathbf{\$402.96}, maintaining the bullish momentum.

2. Crucial Resistance and Volatility Points

The analysis identifies two critical intermediate targets. The first and most significant hurdle is at $567.10, which aligns closely with the \mathbf{0.618} Fibonacci Golden Ratio. This zone is expected to trigger major volatility, profit-taking, and consolidation. The price action at $567.10 is the key test for trend continuity. Should the price break this level decisively, the next primary resistance target is $688.63, paving the way for the ultimate goal.

3. Key Support and Trend Invalidation

The long-term structural support, or the "Invalidation Point" for the bullish scenario, is the Key Zone at \mathbf{\$206.00}. As long as AVGO trades above this level, the multi-year uptrend remains valid. In the short term, the stock needs to overcome immediate resistance near $414.77 to gather momentum and continue its push towards the intermediate Fibonacci targets.

Is the Age of the Human Warehouse Over?Symbotic is no longer just a vendor; it is becoming the operating system of the industrial economy. The robotics leader saw its shares surge nearly 40% Tuesday following a fiscal fourth-quarter report that shattered expectations. With revenue hitting $618 million and system deployments doubling, Wall Street is finally waking up to a new reality. Symbotic’s entry into the $93 billion healthcare logistics market signals a structural shift. The company is transitioning from a retail solution to a critical infrastructure provider, insulating the supply chain from human volatility.

Geopolitics & Geostrategy: The Automation of Sovereignty

Symbotic’s rise is a direct play on "supply chain sovereignty." As global trade routes fracture, nations are aggressively prioritizing domestic logistics resilience. Symbotic’s technology allows the U.S. economy to maintain high-velocity distribution without relying on a fragile, shrinking labor pool. By automating the "middle mile," the company reduces exposure to demographic decline and migration policy shifts. Logistics capacity is no longer just a business metric; it is now a national security asset.

Industry Trends: The Healthcare Alpha

The partnership with Medline Industries marks a pivotal diversification moment. Healthcare logistics demands a level of precision with zero tolerance for error that general retail does not. Winning a contract with a medical supply giant validates Symbotic’s AI as "clinical grade." This move aligns with the broader "Intelligent Supply Chain" trend of 2025. Resilience and redundancy now outweigh pure just-in-time efficiency. Symbotic is positioning itself as the backbone for mission-critical distribution.

Technology & Science: Density as a Deflationary Force

Symbotic’s "Next-Generation" storage architecture is a feat of spatial physics. By reducing warehouse footprints by nearly 40%, the technology acts as a deflationary force against rising industrial real estate costs.

High-Tech Engineering: The system uses proprietary mobile bots that operate independently of specific racking, a radical departure from legacy automation.

Physics of Density: The proprietary design maximizes cubic density, allowing companies to store more inventory in smaller, cheaper spaces close to urban centers.

Macroeconomics & Economics: The Inflation Hedge

The macroeconomic thesis for Symbotic is the spread between the cost of capital and the cost of labor. Even with interest rates elevated, the long-term cost of human labor is rising faster than the cost of robot depreciation. Symbotic’s systems provide a hedge against wage inflation, offering a fixed-cost structure in an inflationary world. This creates a predictable operational expenditure model that CFOs crave in volatile economic climates.

Business Models: The "GreenBox" Evolution

Symbotic is evolving its business model from pure hardware sales to "Warehouse-as-a-Service." The company is democratizing automation, allowing diverse sectors to access enterprise-grade logistics without massive upfront complexity. This recurring revenue model creates a stickier, more predictable cash flow profile. It commands a higher valuation multiple from investors who now view the company as a software platform rather than a hardware manufacturer.

Management & Leadership: The Owner-Operator Edge

CEO Rick Cohen leads with a "three-comma" operator mindset. As the third-generation leader of C&S Wholesale Grocers, Cohen built Symbotic to solve his own problems, not just to sell a product. This "owner-operator" culture permeates the company. Their disciplined refusal to chase growth at the expense of functionality sets them apart. His focus on "monitoring speculative trading" reflects a management team focused on long-term industrial value rather than quarterly stock jukes.

Cyber & Patent Analysis: The Digital Moat

With a massive portfolio of issued and pending patents, Symbotic has built a formidable legal moat around its "structure-independent" bot technology.

Intellectual Property: The patent wall prevents competitors from easily replicating their high-density architecture.

Cyber-Physical Security: As logistics centers become digital nodes, they become targets. Symbotic’s centralized AI "brain" offers a consolidated defense point, crucial for protecting the physical flow of goods from cyber threats.

Conclusion: The Industrial Prime

Symbotic has proven it can scale beyond its largest retail patrons. The Medline deal is the "proof of concept" the market demanded. Investors are no longer buying a grocery logistics company; they are buying the premier industrial automation platform of the decade. The stock’s surge is a delayed recognition of a simple truth: in a world of labor scarcity, the robot is not a luxury; it is a necessity.

Plug Power's AI Pivot: A Strategic RechargePlug Power is executing a high-stakes pivot from government-backed green hydrogen to the booming AI infrastructure market. We analyze the strategic, industrial, and technological drivers behind this potential turnaround.

A Strategic Pivot Amidst Headwinds

Plug Power (PLUG) has long promised a "green hydrogen revolution," but its stock performance tells a different story—plummeting 99% since its 1999 debut. Facing a cash crunch and a $364 million quarterly loss, management is now steering the company toward a new, voracious customer: Artificial Intelligence data centers .

This move is not merely opportunistic; it is a survival imperative. With the Trump administration recently canceling a vital $1.7 billion Department of Energy (DOE) loan, Plug Power has halted capital-intensive green hydrogen projects. Instead, it is monetizing assets to survive, signaling a shift from government-subsidized dreams to immediate commercial reality.

Geostrategy: Adapting to Policy Shifts

The cancellation of the DOE loan reflects a broader geopolitical shift. The new administration prioritizes immediate energy availability over subsidized decarbonization. By pivoting to the private sector, Plug Power is reducing its exposure to political risk.

This aligns with a "geostrategy of resilience." Data centers are a national critical infrastructure. By offering independent power generation, Plug positions itself as a guarantor of digital sovereignty, insulating tech giants from an increasingly fragile U.S. power grid.

Industry Trends: The AI Energy Crunch

The timing of this pivot addresses a critical market failure. Major analysts project that data center electricity demand will grow 16% in 2025 and double by 2030. AI-optimized servers consume nearly five times the power of standard racks, creating a bottleneck that utility companies cannot resolve quickly.

Plug’s recent letter of intent to sell electricity rights for $275 million confirms this demand. Tech giants are desperate for power *now*. Plug is capitalizing on this by selling its grid interconnection queue spots—effectively selling "time" to power-starved hyperscalers.

Innovation & Tech: PEM Fuel Cells vs. Diesel

Technologically, Plug holds a distinct advantage. Traditional data centers rely on diesel generators for backup, which are dirty, noisy, and maintenance-heavy. Plug’s **Proton Exchange Membrane (PEM) fuel cells** offer a superior alternative:

Instant Response: PEM cells ramp up power in seconds, matching the uptime requirements of mission-critical AI workloads.

Zero Emissions: This allows data centers to operate in urban zones with strict air quality mandates.

Energy Density: Hydrogen offers higher energy density than batteries, essential for facilities with limited real estate.

Business Models: Asset Monetization & Liquidity

Management is restructuring the business model from "build-and-own" to "asset-light." The $275 million liquidity injection from selling electricity rights provides a crucial runway. Rather than burning cash to build massive hydrogen plants, Plug is leveraging its existing technology stack—GenSure and ProGen systems—to generate immediate revenue.

This shift improves the cash conversion cycle. Selling backup power hardware to well-capitalized tech firms offers faster payment terms and lower capital risk than long-term utility projects.

Management & Leadership: A Decisive Course Correction

CEO Andy Marsh’s decision to suspend DOE-related activities demonstrates decisive leadership. A rigid adherence to the original "green hydrogen" roadmap would have been fatal without federal backing. By pivoting to the "AI trade," leadership is aligning the company with the only sector currently enjoying unlimited capital expenditure: Big Tech.

Conclusion: A Speculative Renaissance?

Plug Power remains a high-risk investment, but the investment thesis has fundamentally improved. The company is trading a dependency on government policy for a dependency on AI infrastructure growth—a far more robust driver. If Plug can successfully deploy its fuel cells as the standard for data center backup, it will transition from a speculative energy play to an essential component of the AI economy.

Can One Company Power America's Nuclear Future?BWX Technologies (BWXT) has positioned itself at the critical intersection of national security and energy infrastructure, establishing dominance in the advanced nuclear sector through strategic contracts and technological leadership. The company's Q3 2025 results reveal remarkable momentum, with revenue reaching $866 million (a 29% year-over-year increase) and total backlog surging to $7.4 billion, a 119% increase. With a book-to-bill ratio of 2.6 times, BWXT demonstrates demand substantially exceeding current capacity, driven by converging forces of decarbonization, electrification, and the explosive growth of AI power requirements.

BWXT's competitive moat extends across multiple dimensions. The company secured pivotal defense contracts worth $1.5 billion for domestic uranium enrichment and $1.6 billion for high-purity depleted uranium production, directly addressing America's strategic vulnerability to foreign fuel dependence. Leading Project Pele, the Department of Defense's first transportable microreactor prototype delivering 1-5 MW, BWXT is manufacturing the reactor core for 2027 delivery, aligned with Executive Order 14299's mandate to accelerate advanced nuclear deployment for national security and AI infrastructure. This first-mover advantage positions the company strongly for follow-on programs like Project JANUS, which aims to deploy a military installation reactor by September 2028.

The company's technical superiority centers on mastery of TRISO fuel manufacturing tristructural isotropic particles that cannot melt under reactor conditions and serve as self-contained safety systems. BWXT controls proprietary patents for specialized HALEU fuel element designs and maintains strategic partnerships with Northrop Grumman (control systems) and Rolls-Royce LibertyWorks (power conversion), ensuring compliance with stringent DoD cybersecurity standards. This integrated approach spanning fuel enrichment authorization, patented component design, validated manufacturing capabilities, and defense-grade partnerships creates formidable barriers to competition while capturing the multi-decade tailwind of institutional nuclear adoption mandated by federal policy and geopolitical necessity.

Can AI See What Bullets Cannot?VisionWave Holdings is transforming from an emerging defense technology provider into a critical AI infrastructure and platform integrator, positioning itself to capitalize on urgent global demand for autonomous military systems. The company's strategic evolution is driven by heightened geopolitical instability in Eastern Europe and the Indo-Pacific, where conflicts, such as the war in Ukraine, have fundamentally shifted battlefield doctrine away from traditional heavy armor toward agile, autonomous platforms. With the military unmanned ground vehicle market projected to reach $2.87 billion by 2030 and a structural shift toward Manned-Unmanned Teaming doctrine adding sustained long-term demand, VisionWave's timing aligns with accelerating procurement cycles across NATO allies.

The company's competitive advantage centers on its Varan UGV platform, which integrates proprietary 4D imaging radar technology and independently actuated suspension to deliver superior mission resilience in extreme environments. Unlike conventional sensors, VisionWave's 4D radar adds elevation data to standard measurements, achieving detection ranges exceeding 300 meters while maintaining reliable operation through fog, rain, and darkness capabilities essential for 24/7 military readiness. This technological foundation is strengthened by the company's partnership with PVML Ltd., which creates a "secure digital backbone" that resolves the critical Security-Speed Paradox by enabling rapid autonomous operations while maintaining strict security protocols through real-time permission enforcement.

VisionWave's recent institutional validation underscores its transition from emerging player to credible defense-AI equity. The company raised $4.64 million through warrant exercises without issuing new equity, demonstrating financial discipline and strong shareholder confidence while minimizing dilution. Strategic appointments of Admiral Eli Marum and Ambassador Ned L. Siegel to its Advisory Board establish crucial operational bridges to complex international defense procurement systems, accelerating the company's path from pilot validations in 2025 to scaled commercialization. Combined with S&P Total Market Index inclusion and a 5/5 technical rating from Nasdaq Dorsey Wright, VisionWave presents a comprehensive value proposition at the intersection of urgent geopolitical demand and next-generation autonomous defense technology.

Can One Company Control Computing's Future?Google has executed a strategic transformation from a digital advertising platform to a full-stack technology infrastructure provider, positioning itself to dominate the next era of computation through proprietary hardware and breakthrough scientific discoveries. The company's vertical integration strategy centers on three pillars: custom Tensor Processing Units (TPUs) for AI workloads, quantum computing breakthroughs with verifiable advantages, and Nobel Prize-winning drug discovery capabilities through AlphaFold. This approach creates formidable competitive barriers by controlling foundational computational infrastructure rather than relying on commodity hardware.

The TPU strategy exemplifies Google's infrastructure lock-in model. By designing specialized chips optimized for machine learning tasks, Google achieved superior energy efficiency and performance scaling compared to general-purpose processors. The company's multibillion-dollar deal with Anthropic, deploying up to one million TPUs, transforms a potential cost center into a profit generator while locking competitors into Google's ecosystem. This technical dependence makes migration to rival platforms financially prohibitive, ensuring Google monetizes a significant portion of the generative AI market through its cloud services regardless of which AI models succeed.

Google's quantum computing achievement represents a paradigm shift from theoretical benchmarks to practical utility. The Willow chip's "Verifiable Quantum Advantage" demonstrates a 13,000-times speedup over classical supercomputers in physics simulations, with immediate applications in molecular structure mapping for drug discovery and materials science. Meanwhile, AlphaFold delivers quantifiable economic impact, reducing Phase I drug development costs by approximately 30% from over $100 million to $70 million per candidate. Isomorphic Labs has secured nearly $3 billion in pharmaceutical partnerships, validating this high-margin revenue stream independent of advertising.

The geopolitical implications are profound. Google holds the second-highest number of quantum technology patents globally, with strategic IP covering essential scaling technologies like chip tiling and error correction. This intellectual property portfolio creates a technical chokepoint, positioning Google as a mandatory licensing partner for nations seeking to deploy quantum technology. Combined with the dual-use nature of quantum computing for both commercial and military applications, Google's dominance extends beyond market competition to national security infrastructure. This convergence of proprietary hardware, scientific breakthroughs, and IP control justifies premium valuations as Google transitions from cyclical advertising dependence to an indispensable deep-tech infrastructure provider.

Meta vs Microsoft – AI Euphoria or ExhaustionThe AI boom that lifted Big Tech to record highs may be entering its most delicate phase yet. Meta and Microsoft, two of the biggest winners of the AI wave, are now testing investors’ patience with a spending spree that’s starting to look excessive even by Silicon Valley standards.

In the last quarter alone, Meta, Microsoft, and Alphabet poured a combined $78 billion into data centers, GPUs, and AI infrastructure — an 89% increase year-over-year. The market’s reaction was telling: Meta and Microsoft both slipped after earnings, as traders began to question whether the growth in AI revenue can keep pace with the ballooning costs.

Microsoft’s $34.9 billion in capex didn’t deliver a higher growth rate for Azure, and Meta warned that next year’s spending will accelerate “significantly.” Google, by contrast, managed to calm investors with solid cloud growth and a more balanced tone — but even it now projects capex as high as $93 billion for 2025.

The common thread is clear: all three are betting the next decade on AI, but the near-term return on that investment remains murky. For Microsoft, capacity constraints still limit revenue growth. For Meta, the challenge is sharper — it’s spending on infrastructure without a clear monetization path, relying mostly on advertising optimization and early-stage hardware bets.

From a market perspective, both charts show fatigue setting in. After a year of relentless gains, momentum is flattening and volatility is creeping back in. The market still believes in AI — but it’s starting to question how much belief is already priced in.

If earnings growth doesn’t catch up with capex soon, these charts could be signaling the first cracks in the AI narrative. Whether this is just a pause or the beginning of a revaluation cycle will depend on how quickly these investments translate into tangible profit, not just GPU headlines.

Idea Summary:

NASDAQ:META and NASDAQ:MSFT are spending at record levels to stay ahead in AI, but returns are slowing. The charts hint at exhaustion — investors may be entering the first real “AI reality check.

Can Software Win Wars and Transform Commerce?Palantir Technologies has emerged as a dominant force in artificial intelligence, achieving explosive growth through its unique positioning at the intersection of national security and enterprise transformation. The company reported its first billion-dollar quarter with 48% year-over-year sales growth, driven by an unprecedented 93% surge in U.S. commercial revenue. This performance stems from Palantir's proprietary Ontology architecture, which solves the critical challenge of unifying disparate data sources across organizations, and its Artificial Intelligence Platform (AIP) that accelerates deployment through intensive bootcamp sessions. The company's technological moat is reinforced by strategic patent protections and a remarkable 94% Rule of 40 score, signaling exceptional operational efficiency.

Palantir's defense entrenchment provides a formidable competitive advantage and guaranteed revenue streams. The company secured a $618.9 million Army Vantage contract and deployed the Maven Smart System for the Marine Corps, positioning itself as essential infrastructure for the Pentagon's Combined Joint All-Domain Command and Control strategy. These systems enhance battlefield decision-making, with targeting officers processing 80 targets per hour versus 30 without the platform. Beyond U.S. forces, Palantir supports NATO operations, assists Ukraine, and partners with the UK Ministry of Defence, creating a global network of high-margin, long-term government contracts across democratic allies.

Despite achieving profitability with 26.8% operating margins and maintaining $6 billion in cash with virtually no debt, Palantir trades at extreme valuations of 100 times revenue and 224 times forward earnings. With 84% of analysts recommending Hold or Sell ratings, the market remains divided on whether the premium is justified. Bulls argue the valuation reflects Palantir's transformation from niche government contractor to critical AI infrastructure provider, with analysts projecting potential revenue growth from $4.2 billion to $21 billion. The company's success across nine strategic domains—from military modernization to healthcare analytics—suggests it has built an "institutionally required platform" that could justify sustained premium pricing.

The investment thesis ultimately hinges on whether Palantir's structural advantages—its proprietary data integration technology, defense entrenchment, and accelerating commercial adoption—can sustain the growth trajectory demanded by its valuation. While the platform's complexity requires heavy customization and limits immediate scalability compared to simpler competitors, the 93% commercial growth rate validates enterprise demand. Investors must balance the company's undeniable technological and strategic positioning against valuation risk, with any growth deceleration likely triggering significant multiple compression. For long-term investors willing to weather volatility, Palantir represents a bet on AI infrastructure dominance across both military and commercial domains.

Can a Wristband Read Your Mind Before You Move?Wearable Devices Ltd. (NASDAQ: WLDS) is pioneering a radical shift in human-computer interaction through its proprietary neural input interface technology. Unlike invasive brain-computer interfaces or basic gesture-recognition systems, the company's Mudra Band and Mudra Link decode subtle neuromuscular signals at the wrist, enabling users to control digital devices through intent rather than physical touch. What distinguishes WLDS from competitors like Meta's surface electromyography (sEMG) solutions is its patented capability to measure not just gestures, but quantifiable physical forces, including weight, torque, and applied pressure, opening applications far beyond consumer electronics into industrial quality control, extended reality (XR) environments, and mission-critical defense systems.

The company's strategic value lies not in hardware sales but in its planned evolution into a neural data intelligence platform. WLDS is executing a four-phase roadmap that transitions from consumer adoption (Phases 1-2) to data monetization through its Large Motor-Unit Action Potential Model (LMM), a continuously learning biosignal platform expected to launch by 2026. This proprietary dataset, generated from millions of user interactions, positions WLDS to offer high-margin licensing services to OEMs and enterprise clients, particularly in predictive health monitoring and cognitive analytics. With partnerships including Qualcomm and TCL-RayNeo, the company is building the infrastructure for what it envisions as the industry-standard neural interaction platform.

However, WLDS operates in a market defined by extraordinary potential and substantial execution risk. The global brain-computer interface market is projected to reach $6.2 billion by 2030, yet current wireless neural interface revenues remain modest at an estimated $1.5 billion by 2035, suggesting either a massive untapped opportunity or significant adoption barriers. The company's lean 26-34 person operation, $522,000 in 2024 revenue, and extreme stock volatility (Beta: 3.58, 52-week range: $1.00-$14.67) underscore its early-stage profile. Success hinges entirely on converting consumer adoption into the proprietary biosignal data required to train the LMM platform, which in turn must prove sufficiently valuable to command enterprise licensing agreements at scale.

WLDS represents a calculated bet on the convergence of AI, wearable computing, and neurotechnology, a company that could either establish the foundational infrastructure for touchless interaction across XR, healthcare, and defense sectors or struggle to bridge the gap between technological capability and market validation. Its military contracts and robust IP portfolio covering force-measurement capabilities provide technical credibility, but the path to ubiquitous platform adoption (Phase 4) requires flawless execution across consumer seeding, data accumulation, and B2B conversion, a multiyear journey with no guarantee of arrival.

BigBear (BBAI) — Expanding AI Leadership in Defense IntelligenceCompany Overview:

BigBear.ai Holdings, Inc. NYSE:BBAI is a leading provider of AI-powered decision intelligence for defense, supply chain, and digital identity markets—offering investors exposure to the rapidly growing AI and analytics sector focused on mission-critical applications.

Key Catalysts:

Defense expansion: New U.S. Navy partnership for UNITAS 2025 and strategic alliance with Tsecond strengthen BigBear.ai’s role in real-time, edge-based AI processing via ConductorOS and BRYCK platforms.

Long-term contracts: Over $178 million in multi-year defense deals provide strong revenue visibility and recurring income stability.

Strategic momentum: Growing adoption across national security agencies underscores BigBear.ai’s position in U.S. defense modernization efforts.

Investment Outlook:

Bullish above: $6.80–$7.00

Upside target: $17.00–$18.00, supported by defense partnerships, scalable AI deployment, and national security demand.

#BigBearAI #ArtificialIntelligence #DefenseTech #NationalSecurity #EdgeComputing #AIAnalytics #Investing #BBAI

Can Memory Chips Become Geopolitical Weapons?Micron Technology has executed a strategic transformation from commodity memory producer to critical infrastructure provider, positioning itself at the intersection of AI computing demands and U.S. national security interests. The company's fiscal 2025 performance demonstrates this pivot's success, with data center revenue surging 137% year-over-year to comprise 56% of total sales. Gross margins expanded to 45.7% as the company captured pricing power across both its advanced High-Bandwidth Memory (HBM) portfolio and traditional DRAM products. This dual-margin expansion stems from an unusual market dynamic: capacity reallocation toward specialized AI chips has created artificial supply constraints in legacy memory, driving price increases exceeding 30% in some segments. In contrast, HBM3E capacity through 2026 is already sold out.

Micron's technological leadership centers on power efficiency and manufacturing innovation that translate directly into customer economics. The company's HBM3E solutions deliver bandwidth exceeding 1.2 TB/s while consuming 30% less power than competing 8-high configurations—a critical advantage for hyperscale operators managing electricity costs across massive data center footprints. This efficiency edge is reinforced by scientific advances in manufacturing, particularly the mass production deployment of 1γ DRAM using Extreme Ultraviolet lithography. This node transition delivers over 30% more bits per wafer than previous generations while reducing power consumption by 20%, creating structural cost advantages that competitors must match through heavy R&D investment.

The company's unique position as America's sole HBM manufacturer has transformed it from a component supplier to a strategic national asset. Micron's $200 billion U.S. expansion plan, supported by $6.1 billion in CHIPS Act funding, aims to produce 40% of its DRAM capacity domestically within a decade. This geostrategic positioning grants preferential access to U.S. hyperscalers and government projects requiring secure, domestically sourced components, a competitive moat independent of immediate technological specifications. Combined with a robust intellectual property portfolio covering 3D memory stacking and secure boot architectures, Micron has established multiple defensive layers that transcend typical semiconductor industry cycles, validating an investment thesis for sustained high-margin growth through structural rather than cyclical drivers.

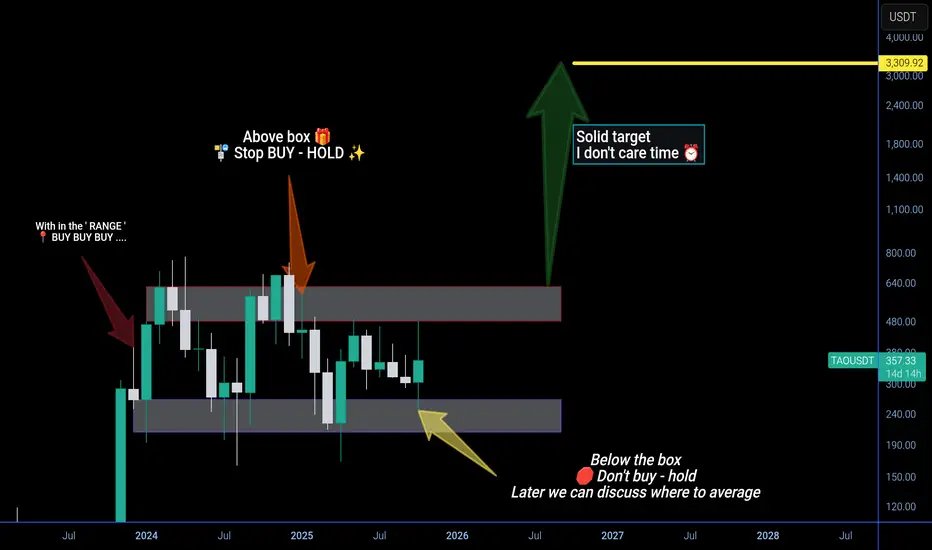

Future is AI - win or lose but I hold and support it upto $3k" DYOR / NFA " ⚠️

i support BINANCE:TAOUSDT for future strong project , i don't care about time but I care only one target $3000 above for one COINBASE:TAOUSD .

Note - time and future price candle change the price forecast ,

so pls be updated by following the post 📯 .

With in range always BUY

‼️ Stop buy above _&_ below the box ☑️

1TAO = $3000+