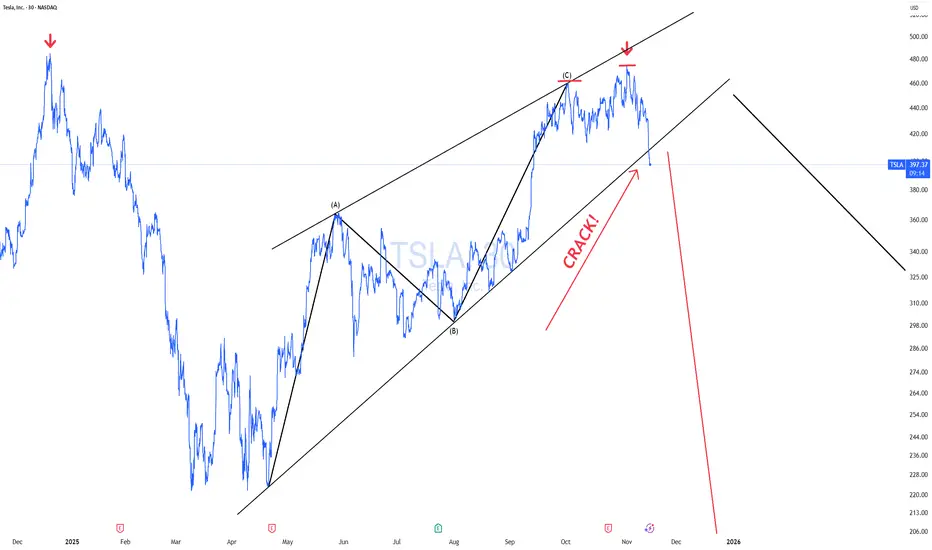

TSLA In Trouble! WARNING!🚫 Why No One Should Be Holding TSLA Right Now

Charting:

Triple Top! Rising wedge fully formed 3-wave rising wedge structure that has hooked and broken! mini double top.

I’ve been saying this for a while — no one should be long TSLA. The stock has done nothing since 2021, yet the hype machine for the boy band keeps spinning.

Ask yourself honestly: Where does Tesla actually lead anymore?

Not in EVs

Not in autonomy

Not in robots

Not in AI

Not in tech innovation

It’s become a stock story with no story left.

And when leadership is built on hype, not execution, it always ends the same way.

Never invest in toxic leadership or cult narratives.

TSLA is a real company, sure — but in fundamental terms, it’s an $8 stock wearing a $450 costume.

If you agree and sell, and it's wrong. Guess what? You will have a bunch of cash waiting to buy it. If you disagree, you won't have a bunch of cash waiting to buy lower BC YOU NEVER SOLD! You can't "BUY THE DIP" Ubless you first SELL THE RIP! It's 2nd-grade math that the boy band who will come in here hating on my call again cannot do. They will give me colorful charts, tell me about cup and handles while riding it all the way down!

They are always buying but NEVER selling. That's the trick with paper money, you can never run out of it. hahah!

Click boost, follow, comment nicely for more authentic, no BS, raw analysis. Let's get to 6,000 followers. ))

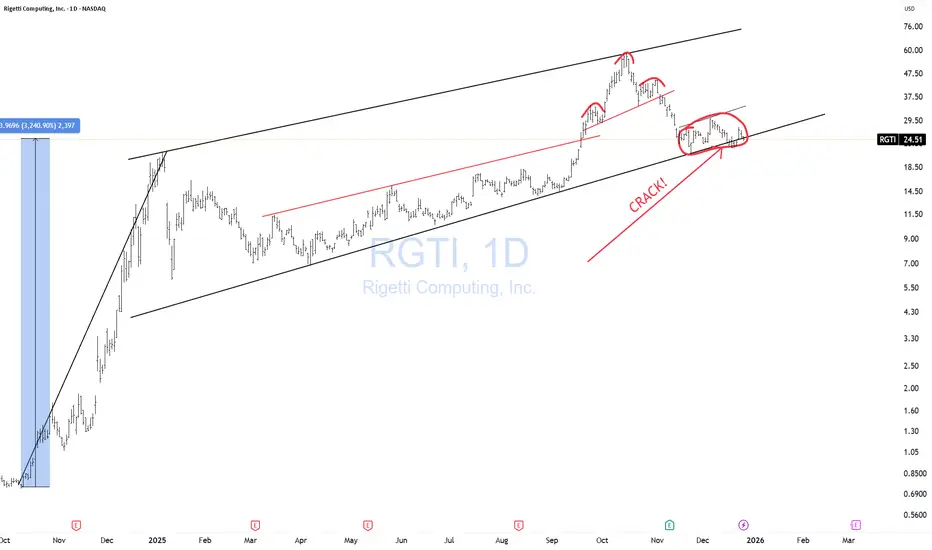

Charting

RGTI CRACK!RGTI is up 3,240% in a bit over a year, with A complete wave 3 up with a hook, Rising F flag that CRACKED, with a broken H&S within it, followed by a low base consolidation flagging out.

RGTI has already lost about -57% of its total value. Don't be surprised if it loses another 50% from here given the run it has had. (And no, I am not doing Trump math. hahah!)

THANK YOU for getting me to 5,000 followers! 🙏🔥

Let’s keep climbing.

If you enjoy the work:

👉 Drop a solid comment

Let’s push it to 6,000 and keep building a community grounded in truth, not hype.

$SPY & $SPX Scenarios — Friday, Dec 26, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Friday, Dec 26, 2025 🔮

🌍 Market-Moving Headlines

• Post-holiday, low-liquidity session: No scheduled macro data — price action driven by flows, positioning, and thin volume.

• Year-end dynamics: Window dressing, tax positioning, and reduced participation can exaggerate moves without real conviction.

📊 Key Data & Events (ET)

• None scheduled

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #markets #trading #holiday #yearend

$SPY & $SPX Scenarios — Wednesday, Dec 24, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Wednesday, Dec 24, 2025 🔮

🌍 Market-Moving Headlines

• Holiday-thinned session: Early close dynamics and reduced liquidity can exaggerate moves.

• Labor check-in only: Jobless claims is the sole macro print before markets wind down for Christmas.

📊 Key Data & Events (ET)

8 30 AM

• Initial Jobless Claims (Dec 20): 225,000

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #JoblessClaims #markets #trading #macro #stocks

$SPY & $SPX Scenarios — Tuesday, Dec 23, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Tuesday, Dec 23, 2025 🔮

🌍 Market-Moving Headlines

• Heavy delayed macro dump: Markets digest a backlog of growth, manufacturing, and production data all at once.

• Growth vs slowdown check: GDP revision and durable goods help frame whether the economy is cooling into year-end.

• Consumer pulse: Confidence print may influence risk appetite heading into the holiday-shortened week.

📊 Key Data & Events (ET)

8 30 AM

• GDP Q3 (delayed): 3.2 percent

• Durable Goods Orders Oct (delayed): -1.1 percent

9 15 AM

• Industrial Production Oct: 0.1 percent

• Capacity Utilization Oct: 75.9 percent

• Industrial Production Nov: 0.1 percent

• Capacity Utilization Nov: 76.0 percent

10 00 AM

• Consumer Confidence Dec: 91.7

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #GDP #DurableGoods #ConsumerConfidence #macro #markets #trading

$SPY & $SPX Scenarios — Week of Dec 22 to Dec 26, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Week of Dec 22 to Dec 26, 2025 🔮

🌍 Market-Moving Headlines

• Holiday week liquidity: Thin volumes amplify moves, especially around Tuesday’s data dump.

• Delayed macro catch-up: GDP and durable goods hit at once, giving markets a late-cycle growth read before year-end positioning.

• Consumer confidence update: One of the few forward-looking signals in a quiet, holiday-shortened week.

📊 Key Data & Events (ET)

Tuesday, Dec 23

8 30 AM

• GDP Q3 (delayed): 3.2 percent

• Durable Goods Orders (Oct, delayed): -1.1 percent

9 15 AM

• Industrial Production (Oct): 0.1 percent

• Capacity Utilization (Oct): 75.9 percent

• Industrial Production (Nov): 0.1 percent

• Capacity Utilization (Nov): 76.0 percent

10 00 AM

• Consumer Confidence (Dec): 91.7

Wednesday, Dec 24

8 30 AM

• Initial Jobless Claims (Dec 20): 225,000

Thursday, Dec 25

• Christmas Holiday — Markets Closed

Friday, Dec 26

• No major data scheduled

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #markets #macro #holidayweek #GDP #durablegoods #consumerconfidence

$SPY & $SPX Scenarios — Friday, Dec 19, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Friday, Dec 19, 2025 🔮

🌍 Market-Moving Headlines

• Housing + sentiment check: Existing home sales and consumer sentiment close out the week, offering a read on demand resilience after a heavy CPI and labor stretch.

• Light macro, positioning matters: With no inflation or labor surprises today, flows, OPEX dynamics, and technical levels take priority.

📊 Key Data & Events (ET)

10 00 AM

• Existing Home Sales (Nov): 4.1 million

• Consumer Sentiment, Final (Dec): 53.5

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #markets #housing #consumer #trading #stocks

$SPY & $SPX Scenarios — Thursday, Dec 18, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Thursday, Dec 18, 2025 🔮

🌍 Market-Moving Headlines

• 🚨 CPI Day — inflation is back in focus with November CPI and Core CPI printing together. This is the primary macro catalyst for rates, equities, and the dollar.

• 📉 Labor cooling check: Jobless claims add confirmation or pushback to the disinflation narrative.

• 🏭 Regional growth signal: Philly Fed survey gives a real-time read on manufacturing momentum into year-end.

📊 Key Data & Events (ET)

8 30 AM — Major Inflation Print

• Consumer Price Index, CPI (Nov): 0.3 percent

• CPI Year over Year: 3.1 percent

• Core CPI (Nov): 0.3 percent

• Core CPI Year over Year: 3.0 percent

• Initial Jobless Claims (Dec 13): 225,000

• Philadelphia Fed Manufacturing Index (Dec): 3.6

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #CPI #inflation #macro #rates #markets #trading #stocks

$SPY & $SPX Scenarios — Wednesday, Dec 17, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Wednesday, Dec 17, 2025 🔮

🌍 Market-Moving Headlines

• Very light macro day: No major inflation, labor, or growth data scheduled.

• Post-data digestion: Markets continue to digest Tuesday’s delayed jobs, retail sales, and PMI releases.

• Fed speakers are secondary: With CPI and employment already out, commentary matters only if tone shifts meaningfully.

📊 Key Data & Events (ET)

• No top-tier economic data scheduled

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #markets #trading #macro #stocks

$SPY & $SPX Scenarios — Tuesday, Dec 16, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Tuesday, Dec 16, 2025 🔮

🌍 Market-Moving Headlines

• Delayed jobs + retail combo: Backlogged payrolls and retail sales hit together, shaping growth and soft-landing narratives.

• Wages in focus: Hourly earnings and YoY wages matter for inflation stickiness after last week’s Fed messaging.

• Flash PMIs: Real-time read on December activity for services and manufacturing.

📊 Key Data & Events (ET)

8 30 AM

• U.S. Employment Report (Nov, delayed): 45,000

• U.S. Unemployment Rate (Nov): 4.5 percent

• U.S. Hourly Wages (Nov): 0.3 percent

• Hourly Wages YoY: 3.6 percent

• U.S. Retail Sales (Oct, delayed): 0.1 percent

• Retail Sales minus autos (Oct): 0.2 percent

9 45 AM

• S and P Flash U.S. Services PMI (Dec): 54.0

• S and P Flash U.S. Manufacturing PMI (Dec): 52.5

10 00 AM

• Business Inventories (Sept): 0.1 percent

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #jobs #retailsales #PMI #macro #markets #trading

$SPY & $SPX Scenarios — Week of Dec 15 to Dec 19, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Week of Dec 15 to Dec 19, 2025 🔮

🌍 Market-Moving Headlines

• 🚩 Delayed macro dump continues: November Jobs, Retail Sales, and CPI all land this week — backlog data finally gives clarity on growth and inflation trends.

• 🚩 Inflation focus shifts to CPI: Thursday’s CPI print is the key risk after PCE and FOMC week.

• 🧭 Labor + consumer health: Jobs, wages, retail sales, and sentiment together shape recession vs soft-landing narratives into year-end.

📊 Key Data & Events (ET)

MONDAY, DEC 15

⏰ 8 30 AM

• Empire State Manufacturing Survey (Dec): 10.0

⏰ 10 00 AM

• Home Builder Confidence Index (Dec): 38

TUESDAY, DEC 16 — 🚩 HEAVY DATA DAY

⏰ 8 30 AM

• U.S. Employment Report (Nov, delayed): 50,000

• Unemployment Rate (Nov): 4.5 percent

• Hourly Wages (Nov): 0.3 percent

• Retail Sales (Oct, delayed): 0.1 percent

• Retail Sales minus Autos (Oct): 0.2 percent

⏰ 9 45 AM

• S&P Flash Services PMI (Dec)

• S&P Flash Manufacturing PMI (Dec)

⏰ 10 00 AM

• Business Inventories (Sept): 0.1 percent

WEDNESDAY, DEC 17

• No major market-moving economic data

THURSDAY, DEC 18 — 🚩 CPI DAY

⏰ 8 30 AM

• Consumer Price Index (Nov)

• Core CPI (Nov)

• CPI YoY: 3.1 percent

• Core CPI YoY: 3.0 percent

• Initial Jobless Claims (Dec 13): 223,000

• Philadelphia Fed Manufacturing Survey (Dec): 3.6

Note: October and November CPI data combined into one release

FRIDAY, DEC 19

⏰ 10 00 AM

• Existing Home Sales (Nov): 4.1 million

• Consumer Sentiment, Final (Dec): 53.8

⚠️ Disclaimer: For informational and educational purposes only — not financial advice.

📌 #SPY #SPX #macro #CPI #jobs #inflation #markets #trading #stocks #economy

SPY SPX Scenarios Friday, Dec 12, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Friday, Dec 12, 2025 🔮

🌍 Market-Moving Headlines

• Post-FOMC digestion day: Markets continue to price Powell’s messaging and rate-path implications from earlier in the week.

• Light macro calendar: No major inflation or labor prints — flows, positioning, and technicals matter more than data today.

📊 Key Data & Events (ET)

10 00 AM

• Wholesale Inventories (Sept): 0.1 percent

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #markets #trading #macro #stocks

$SPY & $SPX Scenarios — Thursday, Dec 11, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Thursday, Dec 11, 2025 🔮

🌍 Market-Moving Headlines

• Jobless Claims remain the only real-time labor gauge while other data is still catching up from delays.

• Trade Deficit offers macro context but usually has limited intraday impact unless the miss is extreme.

📊 Key Data & Events (ET)

8 30 AM

• Initial Jobless Claims (Dec 6): 223,000

• U.S. Trade Deficit (Sept): -62.0B

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #JoblessClaims #Macro #Trading

$SPY & $SPX Scenarios — Wednesday, Dec 10, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Wednesday, Dec 10, 2025 🔮

🌍 Market-Moving Headlines

• Major Fed Day — rate decision and Powell’s presser will dictate all intraday volatility.

• Employment Cost Index (delayed) gives the market another wage-pressure read before Powell speaks.

• Treasury Budget may add context to fiscal trajectory but is secondary today — FOMC dominates everything.

📊 Key Data & Events (ET)

8 30 AM

• Employment Cost Index (Q3, delayed): 0.9 percent

2 00 PM

• FOMC Interest-Rate Decision

• Monthly Federal Budget (Nov): -137.3B

2 30 PM

• Fed Chair Powell Press Conference

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #FOMC #Powell #markets #macro #trading

$SPY & $SPX Scenarios — Tuesday, Dec 9, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Tuesday, Dec 9, 2025 🔮

🌍 Market-Moving Headlines

• Small business sentiment + job openings hit Tuesday morning — both matter for labor tightness and inflation interpretation ahead of Wednesday’s FOMC.

• Shutdown-delayed JOLTS data finally drops. Market will react to whether openings continue to cool or stay elevated.

📊 Key Data & Events (ET)

6 00 AM

• NFIB Small Business Optimism (Nov): 98.2

10 00 AM

• Job Openings, JOLTS (Oct, delayed): 7.2 million

⚠️ Disclaimer: For informational use only — not financial advice.

📌 #SPY #SPX #trading #macro #JOLTS #NFIB #markets #investing

$SPY & $SPX Scenarios — Week of Dec 8 to Dec 12, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Week of Dec 8 to Dec 12, 2025 🔮

🌍 Market-Moving Headlines

🏦 FOMC week: Wednesday’s rate decision and Powell press conference are the dominant catalysts. Markets will focus on wording around inflation progress, growth risks, and timing of future cuts.

🧾 Shutdown-delayed data continues: Job openings, Employment Cost Index, and several September reports are still rolling in late, creating uneven visibility for traders.

📉 Labor and inflation signals midweek: ECI, jobless claims, and trade balance provide additional color on wage pressures and global demand.

🧺 Quiet Monday — then the calendar heats up fast.

📊 Key Data & Events (ET)

MONDAY, DEC 8

• None scheduled

TUESDAY, DEC 9

⏰ 6 00 AM

• NFIB Small Business Optimism (Nov): 98.3

⏰ 10 00 AM

• Job Openings (Oct, delayed): 7.2 million

Note: From the shutdown backlog

WEDNESDAY, DEC 10 — FOMC DAY

⏰ 8 30 AM

• Employment Cost Index, ECI (Q3, delayed): 0.9 percent

⏰ 2 00 PM

• FOMC Interest Rate Decision

• Monthly United States Federal Budget (Nov): –139.6 billion

⏰ 2 30 PM

• Fed Chair Powell Press Conference

THURSDAY, DEC 11

⏰ 8 30 AM

• Initial Jobless Claims (Dec 6): 220,000

• United States Trade Deficit (Sept): –61.6 billion

FRIDAY, DEC 12

⏰ 10 00 AM

• Wholesale Inventories (Sept): Not released for this cycle

Note: September report was canceled; August was the last available

⚠️ Disclaimer: For educational and informational use only — not financial advice.

📌 #SPY #SPX #trading #macro #FOMC #Powell #inflation #labor #economy #markets #investing

$SPX | COVERAGE INITIATED — Personal Position Update [W49]SPX — WEEK 49 COVERAGE INITIATED | 12/05/2025

Ticker: SP:SPX

Timeframe: W

This is a reactive structural classification of SPX based on the weekly chart as of this timestamp. Price conditions are evaluated as they stand — nothing here is predictive or forward-assumptive.

⸻

Author’s Note — Personal Position Update

I initiated my own position on [ SP:SPX ] during Week , entering at $ . This decision follows my personal criteria: I only participate when my system identifies a verified structural trend shift supported by both a confirmed weekly flag and a qualifying candle state. This note reflects my activity only and is not a suggestion for anyone else.

As of this update, my position is currently up ~ from my entry. My structural exit level is $ on a weekly-close basis. This level will continue to adjust upward automatically as the structure strengthens. If price closes below that threshold, my system classifies the trend as structurally compromised, and that is where I personally exit.

This update exists solely to document my own participation and the structural levels I monitor. It is not predictive and does not imply any future outcome.

⸻

Structural Integrity

1) Current Trend Condition [ Numbers to Watch ]

Current Price @ $

• Trend Duration @ +2 Weeks

( Bullish )

• Trend Reversal Level ( Bearish ) @ $

• Trend Reversal Level ( Bearish Confirmation ) @ $

• Pullback Retracement @ $

• Correction Support @ $

⸻

2) Structure Health

• Retracement Phase:

Uptrend (operating above 78.6%)

• Position Status:

Healthy (price above both structural layers)

⸻

3) Temperature :

Warming Phase

⸻

4) Momentum :

Bullish

⸻

Structural Integrity

UPWARD STRUCTURAL ALIGNMENT

This mark reflects a point where market behavior supported the continuation of the existing upward direction. It does not imply forecasting or targets — it simply notes where strength became observable within the current trend. Its meaning holds only while price continues to respect the broader structural levels that define the trend.

⸻

Methodology Overview

This classification framework evaluates directional conditions using internal trend-interpretation logic that references price behavior relative to its structural layers. These relationships are used to identify when price movement aligns with the framework’s criteria for directional phases, transition points, or regime shifts. Visual elements or structural labels reflect these internal interpretations, rather than explicit trading signals or preset indicator crossovers. This framework is observational only and does not imply future outcomes.

SPOT - A Ticking Time Bomb!SPOT Earnings Yield of 1.3% according to current data — meaning you’re getting about 1.3 cents of profit per dollar invested. LOL!

Better you give me your hard-earned money and I'll give you 2% instead of 1.3%. I like to splurge! :)

The Structural Constraint

Spotify cannot scale margins the way Netflix did because:

They don’t own the content

They don’t control input costs

They have to pay out ~70% of every dollar to rights holders

Their pricing power is weak and regulated by deals with labels

The labels decide what happens to Spotify’s margins, not Spotify

This is the definition of a business with a hard economic ceiling.

No amount of subscribers fixes the cost structure.

Spotify’s long-run net margin:

1–2% (When they “beat,” the gains evaporate the next quarter.) If Spotify hit 5% margins — a level they’ve never sustained.

And on a positive note —

THANK YOU for helping me hit 5,000 followers! 🙏🔥

Let’s keep going.

If you find value in the work:

👉 Boost

👉 Follow

👉 Leave a comment

Let’s push to 6,000 and keep building a community rooted in facts, not fairy tales.

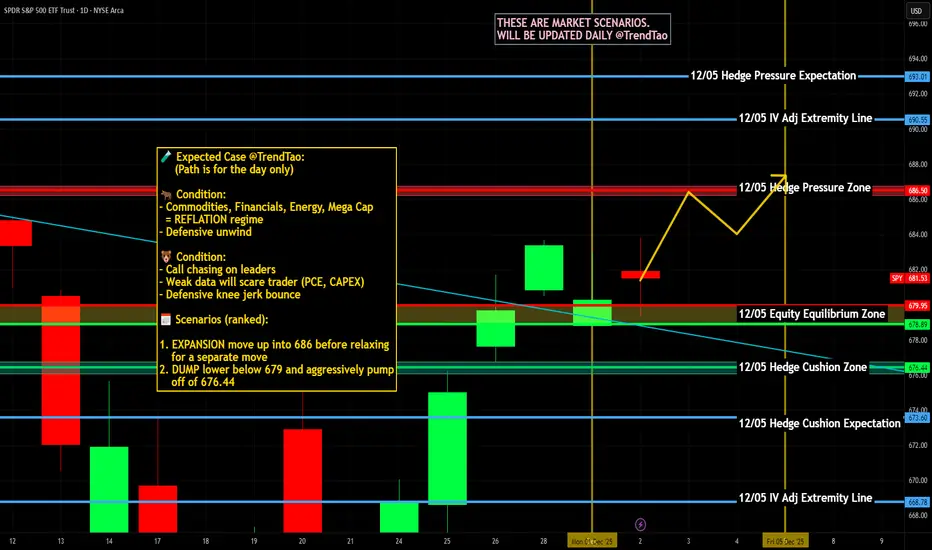

$SPY & $SPX Scenarios — Friday, Dec 5, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Friday, Dec 5, 2025 🔮

🌍 Market-Moving Headlines

🧨 Big inflation catch-up day: A cluster of delayed PCE reports hits at once — this is the Fed’s preferred inflation gauge and will dictate rate-path expectations into year-end.

🧭 Consumer sentiment & credit: Adds read-through on household stress, spending durability, and recession probability.

📊 Key Data and Events (ET)

⏰ 8 30 AM — Heavy Macro Drop

• Personal Income (Sept, delayed): 0.3% vs 0.4%

• Personal Spending (Sept, delayed): 0.4% vs 0.3%

• PCE Index (Sept, delayed): 0.3% vs 0.3%

• PCE YoY: 2.9% vs 2.9%

• Core PCE Index (Sept, delayed): 0.2% vs 0.2%

• Core PCE YoY: 2.8% vs 2.7%

⏰ 10 00 AM

• Consumer Sentiment (prelim, Dec): 52.0 vs 51.0

⏰ 3 00 PM

• Consumer Credit (Oct): $10.5B vs $13.1B

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #PCE #inflation #macro #fed #consumer #markets #stocks #trading #investing

$SPY & $SPX Scenarios — Thursday, Dec 4, 2025🔮 AMEX:SPY & SP:SPX Scenarios — Thursday, Dec 4, 2025 🔮

🌍 Market-Moving Headlines

🧱 Labor pulse before the weekend: Weekly claims remain a key gauge of cooling versus resilience in the labor market — especially with jobs data still disrupted from prior shutdown delays.

🎤 Bowman speaks at noon: Moderate-impact event, but tone on regulation, credit conditions, and inflation watch may move yields slightly in a light-data session.

📊 Key Data and Events (ET)

⏰ 8 30 AM

• Initial Jobless Claims (Nov 29): 220,000 vs 216,000

⏰ 12 00 PM

• Fed Vice Chair for Supervision Michelle Bowman — Remarks

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #macro #labor #joblessclaims #fed #markets #stocks #trading #investing

$SPY & $SPX Scenarios — Wednesday, Dec 3, 2025 🔮 AMEX:SPY & SP:SPX Scenarios — Wednesday, Dec 3, 2025 🔮

🌍 Market-Moving Headlines

💼 Labor + services-heavy morning: ADP, import prices, services PMIs, and ISM all land before 10 AM — a full macro pulse on jobs, inflation pressure, and service-sector strength.

🧾 Shutdown-delayed September reports continue: Import Prices, Industrial Production, and Capacity Utilization still come from the backlog but remain relevant for inflation and growth trend review.

📈 ISM Services is the star: With manufacturing soft, services remain the market’s key gauge of economic momentum into year end.

📊 Key Data and Events (ET)

⏰ 8 15 AM

• ADP Employment (Nov): 40,000 vs 42,000

⏰ 8 30 AM

• Import Price Index (Sept, delayed): 0.1 percent vs 0.3

• Import Prices ex Fuel (Sept, delayed): 0.4 percent

⏰ 9 15 AM

• Industrial Production (Sept, delayed): 0.1 percent

• Capacity Utilization (Sept): 77.3 percent

⏰ 9 45 AM

• S and P Final United States Services PMI (Nov): 55.0

⏰ 10 00 AM

• ISM Services (Nov): 52.5 percent

⚠️ Disclaimer: Educational and informational only — not financial advice.

📌 #SPY #SPX #trading #macro #ADP #services #ISM #inflation #imports #markets #investing

$SPY & $SPX Scenarios — Tuesday, Dec 2, 2025 🔮 AMEX:SPY & SP:SPX Scenarios — Tuesday, Dec 2, 2025 🔮

🌍 Market-Moving Headlines

🎤 Bowman testimony hits at 10 AM — this is the only fixed macro event of the day, and her tone on regulation and economic conditions can nudge yields.

🚗 Auto Sales (Nov) TBA — release time unclear, but this report can move cyclicals if it prints far from expectations. Previous level was 16.4 million annualized.

📊 Key Data and Events (ET)

10 00 AM

• Fed Vice Chair for Supervision Michelle Bowman — Testimony

TBA

• Auto Sales (Nov)

Previous: 16.4 million

Note: Release time is not announced

⚠️ Disclaimer: For educational use only, not financial advice.

📌 #SPY #SPX #stocks #macro #fed #autosales #markets #trading #investing