Dianthus — Precision Complement Medicine for gMG & CIDPCompany Overview

Dianthus Therapeutics NASDAQ:DNTH is a clinical-stage biotech developing next-generation monoclonal antibodies that modulate the complement system for severe autoimmune and neuromuscular diseases. Lead asset DNTH103 uses convenient subcutaneous dosing every two weeks, aiming to disrupt the gMG and CIDP markets projected to exceed $10B by 2030.

Key Catalysts

Phase 2 Momentum in gMG: The MaGic trial showed meaningful symptom improvement, supporting advancement toward Phase 3 and reinforcing a best-in-class profile.

CIDP Expansion: Planning a potentially registrational CIDP trial, extending the neuromuscular franchise and adding a second, sizable indication.

Platform Validation: Positive data backs DNTH’s precision immunology approach; q2w SC dosing directly addresses patients’ convenience and adherence needs.

Diversified Pipeline: Additional programs in rare inflammatory disorders create a multi-catalyst path through 2026, broadening the complement footprint.

Why It Matters

✅ High-value indications with unmet needs

✅ Differentiated dosing + mechanism

✅ Clear clinical path with near/medium-term readouts

Investment Outlook

Bullish above: $35.00–$36.00

Target: $80.00–$82.00 — driven by Phase 3 readiness in gMG, CIDP registrational potential, and complement-medicine leadership.

Clinicaltrials

Can a Medical Giant Transform Into a Growth Story?Medtronic has demonstrated significant momentum entering 2026, with its recent 23% share price appreciation reflecting fundamental improvements rather than speculative enthusiasm. The company delivered strong fiscal Q2 2026 results with revenue reaching approximately $9 billion, up 6.6% year-over-year, while adjusted earnings per share rose 8% to $1.36, surpassing both internal projections and analyst expectations. Most notably, cardiovascular revenue surged 10.8% to roughly $3.4 billion, marking the strongest growth in over a decade outside pandemic periods and suggesting sustainable acceleration across its core business.

The company's pulsed-field ablation technology has emerged as a transformative growth driver, with the PulseSelect system achieving FDA clearance as the first PFA platform for treating atrial fibrillation. This innovation propelled a 71% revenue surge in Cardiac Ablation Solutions during Q2, including 128% growth in the United States. Beyond cardiology, Medtronic's Hugo robotic-assisted surgery system represents a strategic initiative to penetrate the underdeveloped surgical robotics market. The system has recently been submitted for FDA clearance following successful urologic trials, achieving a 98.5% success rate. These technological advances position Medtronic across multiple high-growth segments, including neuromodulation, renal denervation, and diabetes management.

From an investment perspective, Medtronic offers a compelling combination of quality, income, and growth potential. The company has raised its dividend for 48 consecutive years, maintaining Dividend Aristocrat status with a current yield in the low-3% range above the S&P 500 average while preserving capital for R&D investment and strategic acquisitions. Management has demonstrated improved execution with consistent guidance raises, and balanced capital allocation between shareholder returns and innovation funding. While risks remain around robotics execution, diabetes strategy decisions, and payer negotiations, the fundamental thesis appears intact for long-term investors seeking defensive growth with rising cash flows and exposure to structural healthcare trends driven by aging demographics and minimally invasive procedure adoption.

Can One Shot Silence a Disease Forever?Benitec Biopharma has emerged from clinical obscurity to platform validation with unprecedented Phase 1b/2a trial results showing a 100% response rate across all six patients treated with BB-301, their gene therapy for Oculopharyngeal Muscular Dystrophy (OPMD). This rare genetic disorder, characterized by progressive swallowing difficulties that can lead to fatal aspiration pneumonia, has no approved pharmaceutical treatments. Benitec's proprietary "Silence and Replace" approach uses DNA-directed RNA interference to simultaneously shut down production of the toxic mutant protein while delivering a functional replacement, a sophisticated dual-action mechanism delivered via a single AAV9 vector injection. The clinical data revealed dramatic improvements, with one patient experiencing an 89% reduction in swallowing burden, essentially normalizing their eating experience. The FDA's subsequent Fast Track Designation for BB-301 underscores the regulatory conviction in this approach.

The company's strategic positioning extends well beyond a single asset. November 2025 marked a transformative capital event with a $100 million raise at $13.50 per share, nearly triple the $4.80 pricing from just 18 months prior, anchored by a $20 million direct investment from Suvretta Capital, which now controls approximately 44% of outstanding shares. This institutional validation, coupled with a fortress balance sheet providing runway into 2028-2029, has fundamentally de-risked the investment thesis. The manufacturing partnership with Lonza ensures scalable, GMP-compliant production while avoiding geopolitical supply chain risks that plague competitors reliant on Chinese CDMOs. With robust IP protection extending into the 2040s and Orphan Drug Designation providing additional market exclusivity, Benitec operates in a competitive vacuum, as no other clinical-stage programs target OPMD.

The broader implications position Benitec as a platform leader rather than a single-product company. The "Silence and Replace" architecture addresses a fundamental limitation of traditional gene therapy: it can treat autosomal dominant disorders where toxic mutant proteins render simple gene replacement ineffective. This unlocks an entire class of previously undruggable genetic diseases. The company's leadership, including CEO Dr. Jerel Banks (who brings both M.D./Ph.D. credentials and biotechnology equity research experience) and board member Dr. Sharon Mates (who guided Intra-Cellular Therapies to a $14.6 billion acquisition by J&J), suggests preparation for either commercial scale-up or strategic acquisition. With potential pricing power in the $2-3 million range per treatment based on comparable gene therapies, and an enterprise value of approximately $250 million against a multi-billion dollar revenue opportunity, Benitec represents a compelling asymmetric risk-reward profile at the vanguard of curative genetic medicine.

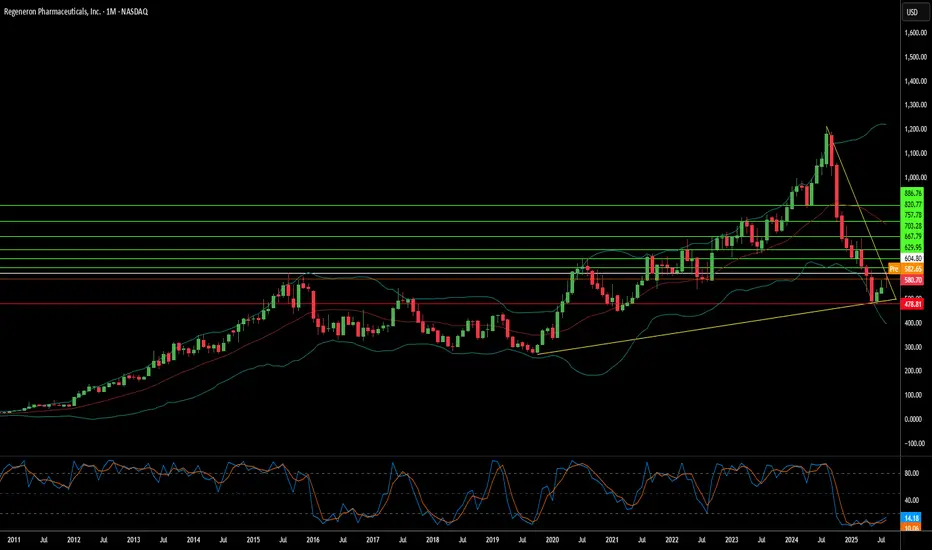

Can Innovation Survive Manufacturing Chaos?Regeneron Pharmaceuticals stands at a fascinating crossroads, embodying the paradox of modern biotechnology: extraordinary scientific achievement shadowed by operational vulnerability. The company has successfully transformed from a blockbuster-dependent enterprise into a diversified biopharmaceutical powerhouse, driven by two key engines. Dupixent continues its remarkable ascent, achieving 22% growth and reaching $4.34 billion in Q2 2025. Meanwhile, the strategic transition from legacy Eylea to the superior Eylea HD demonstrates forward-thinking market positioning, despite apparent revenue declines.

The company's innovation engine supports its aggressive R&D strategy, investing 36.1% of revenue, nearly double the industry average, into discovery and development. This approach has yielded tangible results, with Lynozyfic's FDA approval marking Regeneron's first breakthrough in blood cancer, achieving a competitive 70% response rate in multiple myeloma. The proprietary VelociSuite technology platform, particularly VelocImmune and Veloci-Bi, creates a sustainable competitive moat that competitors cannot easily replicate, enabling the consistent generation of fully human antibodies and differentiated bispecific therapies.

However, Regeneron's scientific triumphs are increasingly threatened by third-party manufacturing dependencies that have created critical vulnerabilities. The FDA's second rejection of odronextamab, despite strong European approval and compelling clinical data, is due to manufacturing issues at an external facility, rather than scientific deficiencies. This same third-party bottleneck has delayed crucial Eylea HD enhancements, potentially allowing competitors to gain market share during a pivotal transition period.

The broader strategic landscape presents both opportunities and risks that extend beyond manufacturing concerns. Although the company's strong victories in intellectual property cases against Amgen and Samsung Bioepis showcase effective legal defenses, the proposed 200% drug tariffs and industry-wide cybersecurity breaches, such as the Cencora incident impacting 27 pharmaceutical companies, highlight significant systemic vulnerabilities. Regeneron's fundamental strengths-its technological platforms, diverse pipeline spanning oncology to rare diseases, and proven ability to commercialize breakthrough therapies-position it for long-term success, provided it can resolve the operational dependencies that threaten to derail its scientific achievements.

Protagonist Therapeutics (PTGX) AnalysisCompany Overview:

Protagonist Therapeutics NASDAQ:PTGX is a clinical-stage biotech developing peptide-based drugs in hematology, inflammatory, and metabolic diseases. Its pipeline spans polycythemia vera, psoriasis, and obesity — addressing multi-billion-dollar markets.

Pipeline & Catalysts:

Rusfertide (Polycythemia Vera) 🩸

Phase 3 VERIFY trial met all primary and secondary endpoints.

Showed reduced phlebotomy needs and improved hematocrit control.

Positions rusfertide as a first-in-class treatment and regulatory catalyst.

Icotrokinra (Psoriasis) 🌐

NDA filed for IL-23 receptor antagonist.

Approval could unlock a major dermatology revenue stream.

PN-477 (Obesity) ⚡

Expands PTGX’s reach into the fast-growing obesity market.

Strategic Advantage:

Global Takeda partnership enhances execution power.

Recent $25M milestone payment post-Phase 3 validates science & provides financial support.

Investment Outlook:

Bullish Case: Above $46–$48, driven by strong clinical data & regulatory progress.

Upside Potential: Target $78–$80, supported by trial success, NDA filings, and Takeda backing.

📢 PTGX—A high-upside biotech story with catalysts across hematology, dermatology, and obesity.

#PTGX #Biotech #ClinicalTrials #Obesity #Psoriasis #Takeda #GrowthStocks

AI in Biotech: The Future of Cancer Therapy?Lantern Pharma Inc. is making waves in the biotech sector, leveraging its proprietary RADR® AI platform to accelerate the development of targeted cancer therapies. The company recently achieved significant milestones, including FDA clearance for a Phase 1b/2 trial of LP-184 in a difficult-to-treat non-small cell lung cancer (NSCLC) subset. This patient population, characterized by specific genetic mutations and poor response to existing treatments, represents a substantial unmet medical need and a multi-billion-dollar market opportunity. LP-184's mechanism, which selectively targets cancer cells overexpressing the PTGR1 enzyme, offers a precision approach aimed at improving efficacy while reducing toxicity.

LP-184's potential extends beyond NSCLC, having received multiple FDA Fast Track Designations for aggressive cancers like Triple-Negative Breast Cancer (TNBC) and Glioblastoma. Preclinical data support its activity in these areas, including synergy with other therapies and favorable properties like brain penetrance for CNS cancers. Furthermore, Lantern Pharma has demonstrated a commitment to rare pediatric cancers, securing Rare Pediatric Disease Designations for LP-184 in MRT, RMS, and hepatoblastoma, which could also yield valuable priority review vouchers.

The company's financial position, marked by strong liquidity according to InvestingPro data, supports its ongoing investment in R&D and its AI-driven pipeline. While reporting a net loss reflecting these investments, Lantern Pharma anticipates key data readouts in 2025 and actively seeks further funding. Analysts view the stock as potentially undervalued, with price targets suggesting future growth. Lantern Pharma's strategy of combining advanced AI with a deep understanding of cancer biology positions it to address high-need patient populations and potentially transform oncology drug development.