Energy Fuels (UUUU) — U.S. Uranium + Rare Earths Scale-UpCompany Overview

Leader in U.S. uranium with the White Mesa Mill (only operating conventional mill in the U.S.). 2025 production >1M lbs U₃O₈, riding nuclear demand, SMRs, reactor life extensions, and policy support for domestic supply.

Rare Earths Transformation

NdPr expansion at White Mesa: low-cost ramp, with heavy REE commercialization targeted for 2026, moving toward mine-to-metal integration for EVs, wind, and defense.

ASM acquisition (A$447M): Adds advanced processing/alloying, elevating Energy Fuels to a non-Chinese, global, vertically integrated rare earth supplier. Australian Strategic Materials

Why It Matters

Dual engines: Cash-flow visibility from uranium + margin expansion from rare earths.

Strategic assets: White Mesa enables domestic processing optionality few peers can match.

Policy tailwinds: U.S. energy security + critical minerals initiatives support long-term pricing and offtakes.

Investment View

Bullish above: $18.50–$19.00

Target: $40–$42 — backed by uranium leadership, REE vertical integration, and the ASM scale-up.

📌 AMEX:UUUU — from America’s uranium core to a rare earths champion.

Criticalminerals

Can America Break China's Rare Earth Monopoly?USA Rare Earth (Nasdaq: USAR) stands at the center of America's most ambitious industrial gamble in decades. The company pursues a vertically integrated "mine-to-magnet" strategy designed to break China's stranglehold on rare earth elements, critical materials that power everything from electric vehicles to F-35 fighter jets. With China controlling 70% of global mining and over 90% of refining capacity, the United States faces a strategic vulnerability that threatens both its defense capabilities and its energy transition. Recent Chinese export restrictions on gallium and germanium have accelerated USA Rare Earth's timeline, with commercial production now targeted for late 2028, two years ahead of previous guidance.

The company's success hinges on extraordinary government backing and massive capital infusions. A $1.6 billion letter of intent from the Department of Commerce, combined with a $1.5 billion private investment, provides $3.1 billion in potential funding. The government will take a 10% equity stake, signaling an unprecedented public-private partnership in critical infrastructure. This funding supports the entire value chain: extraction at the Round Top deposit in Texas, chemical separation in Colorado, and advanced magnet manufacturing in Oklahoma. The Round Top deposit itself is geologically unique, a 1-billion-metric-ton laccolith containing 15 of 17 rare earth elements, processable through cost-effective heap leaching rather than traditional roasting.

Beyond minerals, the project represents a test of American industrial resilience. The Trump administration's "Project Vault" initiative establishes a $12 billion strategic mineral reserve modeled after the Strategic Petroleum Reserve. International alliances with Australia, Japan, and the United Kingdom create a network of "friend-shored" supply chains designed to counter Beijing's leverage. USA Rare Earth's acquisition of UK-based Less Common Metals provides critical refining expertise currently unavailable outside China. The company achieved a milestone in January 2026 by producing its first batch of sintered neodymium magnets at its Oklahoma facility, proving its technical capabilities.

The path forward remains treacherous. Critics point to timeline delays, insider selling, and the volatility inherent in pre-revenue mining ventures. Short sellers have claimed a potential 75% downside, questioning equipment age and promotional tactics. Yet the strategic imperative is undeniable: without domestic rare earth capacity, the United States cannot maintain technological superiority in defense or achieve energy independence. USA Rare Earth's 2030 goal of processing 8,000 tons of heavy rare earths and producing 10,000 tons of magnets annually would fundamentally reshape global supply chains. The billion-dollar race for magnet supremacy will determine whether America can reclaim industrial sovereignty or remain dependent on geopolitical rivals for the minerals of the future.

USAR — Building America’s Rare Earth-to-Magnet Supply ChainCompany Overview

USA Rare Earth NASDAQ:USAR is developing a fully domestic, vertically integrated rare earths + permanent magnet supply chain—anchored by the Round Top (TX) resource and the Stillwater, OK magnet facility slated for commercial production in early 2026. The model spans mine → refine → finished magnets for EVs, wind, and defense—directly aligned with U.S. supply-chain security.

Key Catalysts

Round Top Acceleration: One of North America’s largest heavy REE deposits; PFS targeted for late 2026 brings forward project value and funding optionality.

Magnet Plant Ramp: U.S.-based NdFeB capacity addresses a critical domestic gap, enabling offtakes with auto, energy, and defense OEMs.

Policy Tailwinds: U.S. industrial policy and defense priorities support onshore materials, permitting, and potential grant/loan access.

Vertical Integration Advantage: Internalized processing + magnet making can improve margins, quality control, and supply assurance vs. import dependence.

Investment Outlook

Bullish above: $16.50–$17.00

Target: $42–$44 — supported by magnet plant commercialization (2026), Round Top de-risking, and strong geopolitical/DOE-DoD tailwinds.

📌 USAR — from ore to magnet, a strategic U.S. cornerstone for EVs, wind, and defense.

Ivanhoe Electric (IE) — Typhoon-Powered U.S. Copper DiscoveryCompany Overview

Ivanhoe Electric AMEX:IE is a technology-driven copper explorer focused on the U.S., leveraging its proprietary Typhoon™ geophysical system and advanced analytics to uncover high-quality, electrification-ready copper assets. The Santa Cruz Copper Project (AZ) anchors the story amid growing U.S. policy support for domestic critical minerals.

Key Catalysts

De-Risked Path at Santa Cruz: Recent land acquisitions plus a $200M credit facility strengthen development readiness and optionality.

Tech Edge = Faster Discoveries: Typhoon™ + data analytics accelerating targets at Tintic (UT) and other districts, improving hit-rates and timelines.

Strategic Partnerships: Collaboration with Ma’aden (Saudi Arabia) adds international upside while maintaining a secure U.S. asset base.

Structural Demand Tailwind: Electrification, grid build-out, EVs, and defense keep copper front-and-center in long-cycle capex.

Investment Outlook

Bullish above: $15–$16

Target: $27–$28 — supported by Typhoon™-enabled discovery efficiency, funding de-risk, and policy-backed U.S. copper supply.

📌 IE — marrying proprietary geophysics with tier-one U.S. copper optionality.

Can Robots Win America's Deep-Sea Mineral Race?Nauticus Robotics (NASDAQ: KITT) has pivoted from a speculative energy services company into a strategic asset positioned at the intersection of national security and resource independence. The company's transformation centers on autonomous underwater robotics designed to extract critical minerals from the deep seabed, a response to China's near-monopoly (80%+ control) over rare earth elements essential for defense systems and the green energy transition. Following President Trump's April 2025 Executive Order declaring seabed minerals a "core national security interest," Nauticus secured a $250 million equity facility. They announced its entry into deep-sea mineral exploration, positioning itself as the technological enabler for U.S. interests in what the report terms the "Blue Cold War."

The company's technological moat rests on its proprietary Aquanaut platform. This transformer-style autonomous underwater vehicle transitions from streamlined cruising to a hoverable work configuration paired with the electric Olympic Arm manipulator and ToolKITT software operating system. This technology stack offers 30-40% cost reductions over traditional crewed operations by eliminating expensive support vessels and replacing human labor with autonomous systems. Nauticus recently achieved critical milestones, including successful testing at 2,300-meter depths, NASDAQ compliance restoration (December 2025), and integration of its software into third-party ROVs, validating both technical capability and commercial viability. The licensing of ToolKITT to retrofit existing underwater vehicles represents a high-margin revenue opportunity across thousands of legacy assets.

However, significant execution risks temper this strategic positioning. The company burned $134.9 million in 2024 and posted only $2 million in Q3 2025 revenue, relying heavily on dilutive equity financing through its $250M facility (capped at 19.99% of shares). The pivot to deep-sea mining remains unproven at commercial scale. Surveying nodules differs vastly from extraction, and regulatory frameworks continue to evolve amid environmental controversies. Nauticus faces competition from well-capitalized Chinese state-owned enterprises and traditional dredging giants while navigating cybersecurity requirements (CMMC compliance) for defense contracts. The company remains under NASDAQ "Panel Monitor" status through December 2026, with any future violation triggering immediate delisting. Success depends on synchronized execution across technology scaling, government contract acquisition, and favorable policy momentum, making Nauticus a high-variance bet on whether autonomous robotics can indeed break China's stranglehold on critical minerals while surviving the precarious journey to profitability.

Can Silver Become the Most Critical Metal of the Decade?The iShares Silver Trust (SLV) stands at the convergence of three unprecedented market forces that are fundamentally transforming silver from a monetary hedge into a strategic industrial imperative. The November 2025 designation of silver as a "Critical Mineral" by the USGS marks a historic regulatory shift, activating federal support mechanisms including nearly $1 billion in DOE funding and 10% production tax credits. This designation positions silver alongside materials essential for national security, triggering potential government stockpiling that would compete directly with industrial and investor demand for the same physical bars held by SLV.

The supply-demand equation reveals a structural crisis. With 75-80% of global silver production coming as a byproduct of other mining operations, supply remains dangerously inelastic and concentrated in volatile Latin American regions. Mexico and Peru account for 40% of global output, while China is aggressively securing direct supply lines in early 2025. Peru's silver exports surged 97.5%, with 98% flowing to China. This geopolitical repositioning leaves Western vaults increasingly depleted, threatening SLV's creation-redemption mechanism. Meanwhile, chronic deficits persist, with the market balance projected to worsen from -184 million ounces in 2023 to -250 million ounces by 2026.

Three technological revolutions are creating inelastic industrial demand that could consume entire supply chains. Samsung's silver-carbon composite solid-state battery technology, planned for mass production by 2027, requires approximately 1 kilogram of silver per 100 kWh EV battery pack. If just 20% of the 16 million annual EVs adopt this technology, it would consume 62% of the global silver supply. Simultaneously, AI data centres require silver's unmatched electrical and thermal conductivity for reliability, while the solar industry's shift to TOPCon and HJT cells uses 50% more silver than previous technologies, with photovoltaic demand projected to exceed 150 million ounces by 2026. These converging super-cycles represent a technological lock-in where manufacturers cannot substitute silver without sacrificing critical performance, forcing a historic repricing as the market transitions silver from a discretionary asset to a strategic necessity.

Is the World Sleepwalking Into a Platinum Catastrophe?The global economy is currently entering a precarious era defined by resource nationalism, where the BRICS+ alliance has effectively consolidated control over critical minerals, including the vast majority of primary platinum production. As geopolitical fragmentation deepens, the West faces a severe strategic vulnerability, as it relies heavily on adversaries like Russia and China for the metals essential to its green transition. This dependency is compounded by the weaponization of trade, with export controls on other strategic minerals already signaling that platinum—a metal critical for hydrogen fuel cells and electrolysis—could be the next target in a looming "commodities cartel" strategy.

Simultaneously, the market is grappling with a severe and structural supply deficit, projected to reach a critical 850,000 ounces by 2025. This shortfall is driven by the collapse of primary production in South Africa, where a crumbling energy infrastructure, labor instability, and logistical failures are strangling output. The situation is exacerbated by a "recycling cliff," as economic pressures reduce the scrapping of old vehicles, drying up secondary supply lines just as above-ground inventories are being rapidly depleted.

Despite these supply shocks, demand is poised for a tsunami driven by the hydrogen economy, where platinum is the indispensable catalyst for Proton Exchange Membrane (PEM) electrolyzers and heavy-duty fuel cell vehicles. While investors historically viewed platinum through the narrowing lens of internal combustion engines, resilient demand from hybrid vehicles and strict Euro 7 emissions regulations ensures that automotive usage remains robust. Furthermore, the hydrogen sector is projected to grow at a staggering 32% CAGR through 2030, creating entirely new structural demand that the current supply chain cannot meet.

Ultimately, the article argues that platinum is drastically mispriced, trading at a deep discount despite its strategic imperative and monetary value as a hard asset. The convergence of supply destruction, geopolitical leverage, and exponential green demand signals the arrival of a "Platinum Supercycle". With cyber warfare posing an additional invisible risk to mining infrastructure and China aggressively securing patent dominance in hydrogen technology, the window to acquire this undervalued asset is closing, positioning platinum as the potential "apex trade" of the coming decade.

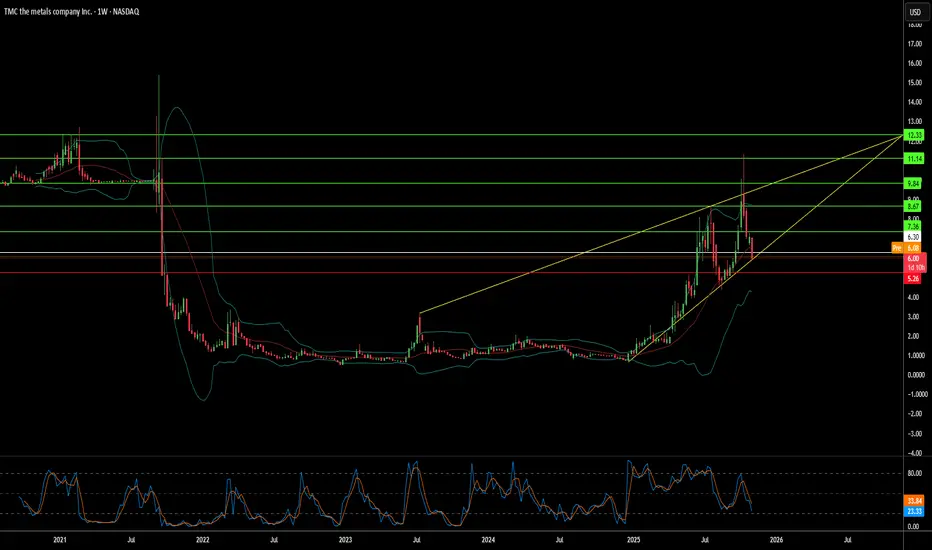

Can Geopolitics Justify a 53x Premium?The Metals Company (TMC) has experienced an extraordinary 790% surge year-to-date, achieving a Price-to-Book ratio of 53.1x, more than twenty times the industry average of 2.4x. This remarkable valuation for a pre-revenue company reflects not conventional profitability metrics, but rather a strategic bet on geopolitical leverage and resource scarcity. The catalyst driving this premium is the April 2025 reactivation of the Deep Seabed Hard Mineral Resources Act (DSHMRA), which enables TMC's U.S. subsidiary to pursue commercial deep-sea mining licenses independent of the United Nations' International Seabed Authority. This unilateral policy shift positions TMC as the primary instrument for U.S. critical mineral independence, bypassing years of international regulatory uncertainty.

The investment thesis centers on converging macroeconomic tailwinds and technological readiness. TMC controls massive polymetallic nodule reserves in the Clarion-Clipperton Zone containing an estimated 340 million tonnes of nickel and 275 million tonnes of copper—critical materials for electric vehicle batteries and renewable energy systems. Global demand for these minerals is projected to triple by 2030 under current policies and potentially quadruple by 2040 if net-zero goals are pursued. The company has successfully demonstrated technical feasibility through 2022 deep-sea collection trials that retrieved over 3,000 tonnes of nodules from depths of 4,000-6,000 meters, establishing a high-tech operational moat. An $85.2 million strategic investment from Korea Zinc at a premium price further validates both the technical viability of processing these nodules and the strategic importance of the resource base.

However, significant risks temper this optimistic narrative. TMC operates with zero revenue and persistent net losses, facing substantial dilution risk through warrants and a $214.4 million shelf registration signaling future equity raises. The company's DSHMRA strategy creates direct conflict with international law, as the ISA rejects any commercial exploitation outside its authorization as a violation of UNCLOS. The market is essentially engaging in regulatory arbitrage, betting that U.S. domestic legal frameworks will prove sufficiently robust despite potential enforcement actions from UNCLOS member states. Additionally, environmental concerns persist regarding the largely unknown deep-sea ecosystems, though TMC's Life Cycle Assessments position nodule collection as environmentally superior to terrestrial mining. The extreme valuation ultimately represents a calculated wager that U.S. strategic policy and the imperative for independent mineral supply will overcome both international legal challenges and scientific uncertainty surrounding deep-sea environmental impacts.

Can One Company Break China's Rare Earth Stranglehold?Lynas Rare Earths Limited (OTCPK: LYSCF / ASX: LYC) has emerged as the Western world's strategic counterweight to Chinese dominance in rare earth minerals, positioning itself as critical infrastructure rather than merely a mining company. As the only significant producer of separated rare earths outside Chinese control, Lynas supplies materials essential for advanced defense systems, electric vehicles, and clean energy technologies. The company's transformation reflects an urgent geopolitical imperative: Western nations can no longer tolerate dependence on China, which controls nearly 90% of global rare earth refining capacity and previously held 99% of heavy rare earth processing. This monopoly has enabled Beijing to weaponize critical minerals as diplomatic leverage, prompting the U.S., Japan, and Australia to intervene with unprecedented financial backing and strategic partnerships.

The confluence of government support validates Lynas's indispensable role in allied supply chain security. The U.S. Department of Defense awarded a $120 million contract for domestic heavy rare earth separation capability in Texas, while Japan's government provided A$200 million in financing to secure priority NdPr supply through 2038. Australia committed A$1.2 billion to a Critical Minerals Reserve, and U.S. officials are exploring equity stakes in strategic projects. This state-backed capital fundamentally alters Lynas's risk profile, stabilizing revenue through defense contracts and sovereign agreements that transcend traditional commodity market volatility. The company's recent A$750 million equity placement demonstrates investor confidence that geopolitical alignment overrides cyclical price concerns.

Lynas's technical achievements cement its strategic moat. The company successfully achieved the first production of separated heavy rare earth oxides—dysprosium and terbium—outside China, eliminating the West's most critical military supply vulnerability. Its proprietary HREE separation circuit can produce up to 1,500 tonnes annually, while the high-grade Mt Weld deposit provides exceptional cost advantages. The October 2025 partnership with U.S.-based Noveon Magnetics creates a complete mine-to-magnet supply chain using verified non-Chinese materials, addressing downstream bottlenecks where China also dominates magnet manufacturing. Geographic diversification across Australia, Malaysia, and Texas provides operational redundancy, though permitting challenges at the Seadrift facility reveal the friction inherent in forcing rapid industrial development onto allied soil.

The company's strategic significance is perhaps most starkly demonstrated by its targeting in the DRAGONBRIDGE influence operation, a Chinese state-aligned disinformation campaign using thousands of fake social media accounts to spread negative narratives about Lynas facilities. The U.S. Department of Defense publicly acknowledged this threat, confirming Lynas's status as a national defense proxy. This adversarial attention, combined with robust intellectual property protections and government commitments to defend operational stability, suggests that Lynas's valuation must account for factors beyond traditional mining metrics—it represents the West's collective bet on achieving mineral independence from an increasingly assertive China.

Could One Alaskan Mine Reshape Global Power?Nova Minerals Limited has emerged as a strategically critical asset in the escalating U.S.-China resource competition, with its stock surging over 100% to reach a 52-week high. The catalyst is a $43.4 million U.S. Department of War funding award under the Defense Production Act to develop domestic military-grade antimony production in Alaska. Antimony, a Tier 1 critical mineral essential for defense munitions, armor, and advanced electronics, is currently imported by the U.S. in its entirety, with China and Russia controlling the global market. This acute dependency, coupled with China's recent export restrictions on rare earths and antimony, has elevated Nova from mining explorer to national security priority.

The company's dual-asset strategy offers investors exposure to both sovereign-critical antimony and high-grade gold reserves at its Estelle Project. With gold prices exceeding $4,000 per ounce amid geopolitical uncertainty, Nova's fast-payback RPM gold deposit (projected sub-one-year payback) provides crucial cash flow to self-fund the capital-intensive antimony development. The company has secured government backing for a fully integrated Alaskan supply chain from mine to military-grade refinery, bypassing foreign-controlled processing nodes. This vertical integration directly addresses supply chain vulnerabilities that policymakers now treat as wartime-level threats, evidenced by the Department of Defense's renaming to the Department of War.

Nova's operational advantage stems from implementing advanced X-Ray Transmission ore sorting technology, achieving a 4.33x grade upgrade while rejecting 88.7% of waste material. This innovation reduces capital requirements by 20-40% for water and energy, cuts tailings volume up to 60%, and strengthens environmental compliance critical for navigating Alaska's regulatory framework. The company has already secured land use permits for its Port MacKenzie refinery and is on track for initial production by 2027-2028. However, long-term scalability depends on the proposed $450 million West Susitna Access Road, with environmental approval expected in Winter 2025.

Despite receiving equivalent Department of War validation as peers like Perpetua Resources (market cap ~$2.4 billion) and MP Materials, Nova's current enterprise value of $222 million suggests significant undervaluation. The company has been invited to brief the Australian Government ahead of the October 20 Albanese-Trump summit, where critical minerals supply chain security tops the agenda. This diplomatic elevation, combined with JPMorgan's $1.5 trillion Security and Resiliency Initiative, which targets critical minerals, positions Nova as a cornerstone investment in Western supply chain independence. Success hinges on disciplined execution of technical milestones and securing major strategic partnerships to fund the estimated A$200-300 million full-scale development.

Can China Weaponize the Elements We Need Most?China's dominance over rare earth element (REE) processing has transformed these strategic materials into a geopolitical weapon. While China controls approximately 69% of global mining, its true leverage lies in processing, where it commands over 90% of Global capacity and 92% of permanent magnet manufacturing. Beijing's 2025 export controls exploit this chokehold, requiring licenses for REE technologies used even outside China, effectively extending regulatory control over global supply chains. This "long-arm jurisdiction" threatens critical industries from semiconductor manufacturing to defense systems, with immediate impacts on companies like ASML facing shipment delays and US chipmakers scrambling to audit their supply chains.

The strategic vulnerability runs deep through Western industrial capacity. A single F-35 fighter jet requires over 900 pounds of REEs, while Virginia-class submarines need 9,200 pounds. The discovery of Chinese-made components in US defense systems illustrates the security risk. Simultaneously, the electric vehicle revolution guarantees exponential demand growth. EV motor demand alone is projected to reach 43 kilotons in 2025, driven by the prevalence of permanent magnet synchronous motors that lock the global economy into persistent REE dependency.

Western responses through the EU Critical Raw Materials Act and US strategic financing establish ambitious diversification targets, yet industry analysis reveals a harsh reality: concentration risk will persist through 2035. The EU aims for 40% domestic processing by 2030, but projections show the top three suppliers will maintain their stranglehold, effectively returning to 2020 concentration levels. This gap between political ambition and physical execution stems from formidable barriers environmental permitting challenges, massive capital requirements, and China's strategic shift from exporting raw materials to manufacturing high-value downstream products that capture maximum economic value.

For investors, the VanEck Rare Earth/Strategic Metals ETF (REMX) operates as a direct proxy for geopolitical risk rather than traditional commodity exposure. Neodymium oxide prices, which plummeted from $209.30 per kilogram in January 2023 to $113.20 in January 2024, are projected to surge to $150.10 by October 2025 volatility driven not by physical scarcity but by regulatory announcements and supply chain weaponization. The investment thesis hinges on three pillars: China's processing monopoly converted into political leverage, exponential green technology demand establishing a robust price floor, and Western industrial policy guaranteeing long-term financing for diversification. Success will favor companies establishing verifiable, resilient supply chains in downstream processing and magnet manufacturing outside China, though the high costs of secure supply, including mandatory cybersecurity auditing and environmental compliance, ensure elevated prices for the foreseeable future.

Can One Idaho Mine Break China's Grip on America's Defense?Perpetua Resources Corp. (NASDAQ: PPTA) has emerged as a critical player in America's quest for mineral independence through its Stibnite Gold Project in Idaho. The company has secured substantial backing with $474 million in recent financing, including investments from Paulson & Co. and BlackRock, plus over $80 million in Department of Defense funding. This support reflects the strategic importance of the project, which aims to produce both gold and antimony while restoring legacy mine sites and creating over 550 jobs in rural Idaho.

The geopolitical landscape has dramatically shifted in Perpetua's favor following China's export restrictions on antimony imposed in September 2024. With China controlling 48% of global antimony production and 63% of U.S. imports, Beijing's ban on sales to America has exposed critical supply chain vulnerabilities. The Stibnite Project represents America's only domestic antimony source, positioning Perpetua to potentially supply 35% of U.S. antimony needs and reduce dependence on China, Russia, and Tajikistan, which collectively control 90% of global supply.

Antimony's strategic significance extends far beyond its typical use as a mining commodity, serving as an essential component in defense technologies, including missiles, night vision equipment, and ammunition. The U.S. currently maintains stockpiles of just 1,100 tons against annual consumption of 23,000 tons, highlighting the critical supply shortage. Global antimony prices surged 228% in 2024 due to these shortages, while conflicts in Ukraine and the Middle East have amplified demand for defense-related materials.

The project combines economic development with environmental restoration, employing advanced technologies for low-carbon operations and partnering with companies like Ambri to develop liquid metal battery storage systems. Analysts have set an average price target of $21.51 for PPTA stock, with recent performance showing a 219% surge reflecting market confidence in the company's strategic positioning. As clean energy transitions drive demand for critical minerals and U.S. policies prioritize domestic production, Perpetua Resources stands at the intersection of national security, economic development, and technological innovation.

Can Strategic Minerals Transform National Security?MP Materials has experienced a significant market revaluation, with its stock surging over 50% following a pivotal public-private partnership with the U.S. Department of Defense (DoD). This multi-billion-dollar agreement, which includes a $400 million equity investment, substantial additional funding, and a $150 million loan, aims to rapidly establish a robust, end-to-end U.S. rare earth magnet supply chain. This strategic collaboration is designed to curtail the nation's reliance on foreign sources for these critical materials, which are indispensable for advanced technology systems across both defense and commercial applications, from F-35 fighter jets to electric vehicles.

The partnership underscores a profound geopolitical imperative: countering China's near-monopoly over the global rare earth supply chain. China dominates rare earth mining, refining, and magnet production, a leverage it has demonstrably used through export restrictions amidst escalating trade tensions with the U.S. These actions highlighted acute U.S. vulnerabilities and the imperative for domestic independence, propelling the DoD's "mine to magnet" strategy aimed at achieving self-sufficiency by 2027. The DoD's substantial investment and its new position as MP Materials' largest shareholder signal a decisive shift in U.S. industrial policy, directly challenging China's influence and asserting economic sovereignty in a vital sector.

Central to the deal's financial attractiveness and long-term stability is a 10-year price floor of $110 per kilogram for key rare earths, significantly higher than historical averages. This guarantee not only ensures MP Materials' profitability, even against potential market manipulation, but also de-risks its ambitious expansion plans, including new magnet manufacturing facilities expected to produce 10,000 metric tons annually. This comprehensive financial and demand certainty transforms MP Materials from a commodity producer vulnerable to market whims into a strategic national asset, attracting further private investment and setting a powerful precedent for securing other critical mineral supply chains in the Western Hemisphere.

Perpetua – Unlocking Strategic Gold & Critical Mineral Value Project Focus:

Perpetua NASDAQ:PPTA is advancing the Stibnite Gold Project—a rare dual-value asset with both economic and national security significance.

Key Catalysts:

Federal Backing Accelerates Permitting 🏛️

Labeled a “Transparency Project” by the White House

Streamlined permitting process → lowers execution risk, expedites timeline

Outstanding Economics 💰

$3.7B after-tax NPV, 27%+ IRR at spot prices

AISC: $435/oz in early years → Tier-one margins + downside protection

Antimony Exposure: Critical Strategic Edge 🇺🇸

One of the few domestic sources of antimony, vital for:

Defense applications

Battery storage technologies

Geopolitical importance enhances long-term value proposition

Environmental Remediation Built-In 🌱

Project includes restoration of a legacy mining site → aligns with ESG frameworks and broadens support base

Investment Outlook:

✅ Bullish Above: $11.50–$12.00

🚀 Target Range: $18.00–$19.00

🔑 Thesis: Tier-1 economics + critical mineral relevance + federal backing = asymmetric upside for long-term investors

📢 PPTA: A gold play with strategic minerals and federal momentum behind it.

#Gold #CriticalMinerals #Antimony #MiningInnovation #EnergySecurity #PPTA