Can a Former Penny Stock Become a Defense Tech Powerhouse?Ondas Holdings Inc. (NASDAQ: ONDS) has executed a remarkable 30% surge, climbing from early-year lows of $0.57 to near its 52-week high of $11.70. This dramatic recovery reflects more than market momentum; it signals a fundamental transformation from a collection of disparate assets into a unified defense technology platform. The company's rebranding to "Ondas Inc." in Q1 2026, along with its strategic relocation to West Palm Beach, Florida, underscores management's commitment to establishing a cohesive identity within the aerospace and defense sector.

The company's growth trajectory is anchored by substantial contract wins and an expanding product ecosystem. Ondas secured a landmark government tender to deploy thousands of autonomous drones for border protection, while recording $16.4 million in counter-UAS orders from major European airports. With revenue targets of at least $110 million for 2026, representing 200% growth over 2025's $36 million, the company is positioning itself for a transition from small-cap to mid-cap visibility. This forecast is supported by a record $23.3 million backlog and a strengthened balance sheet featuring $68.6 million in cash reserves.

Ondas has built competitive advantages through strategic acquisitions and proprietary technology. The acquisition of Sentrycs brought advanced "Cyber-over-RF" capabilities that enable non-jamming drone mitigation—critical for operations in dense urban environments. Combined with its FullMAX platform for mission-critical IoT and precision optics IP from SPO, Ondas offers end-to-end multi-domain autonomy solutions. The company's recent AI-powered humanitarian demining pilot in the Middle East, which identified nearly 150 hazardous items across 22 acres, demonstrates the versatility of its technology beyond traditional defense applications. As global demand for autonomous security solutions intensifies, Ondas appears positioned to capture significant market share across border security, infrastructure protection, and humanitarian operations.

Defensetechnology

Can One Shipbuilder Anchor America's Naval Supremacy?Huntington Ingalls Industries (HII) stands at the nexus of America's resurgent naval strategy, positioning itself not as a legacy shipbuilder but as a cutting-edge technology integrator. With exclusive control of the Arleigh Burke Flight III destroyer program featuring the revolutionary SPY-6 radar, 30 times more sensitive than its predecessor, HII has secured a decades-long revenue fortress. The recent Navy decision to pivot from the failed Constellation-class frigate to HII's proven Legend-class design validates the company's execution-first philosophy and opens a massive second growth engine alongside its destroyer franchise.

Beyond traditional shipbuilding, HII is aggressively capturing the unmanned maritime systems market, projected to grow at 14% annually through 2030. Its Romulus family of autonomous surface vessels, powered by the proprietary Odyssey control system with over 6,000 operational hours, positions the company to dominate the Navy's "Project 33" initiative for cost-effective robotic platforms. Strategic partnerships with Thales for AI-powered mine detection sonar and innovative distributed shipbuilding across 23 manufacturing partners demonstrate HII's adaptation to labor shortages and technological transformation.

Despite industry-leading growth estimates of 11.19% outpacing General Dynamics (7.55%) and Northrop Grumman (5.22%), HII trades at a P/E of 24.2x versus the defense sector average of 37.6x. This valuation disconnect, combined with a multi-decade backlog spanning Flight III destroyers, the new frigate program, and emerging autonomous systems, presents a compelling asymmetry. As geopolitical tensions with China intensify and the Navy pursues its 355-ship fleet goal, HII's monopoly on critical naval capabilities positions it as an indispensable national asset whose market value has yet to reflect its strategic importance.

Is Red Cat the Drone King America Has Been Waiting For?Red Cat Holdings (RCAT) stands at the epicenter of a transformative moment in defense technology. The December 2025 FCC ban on Chinese drone manufacturers DJI and Autel has effectively eliminated Red Cat's primary competition, creating a protected market for domestic producers. With Q3 fiscal 2025 revenue surging 646% year-over-year and a balance sheet fortified with over $212 million in cash, Red Cat has positioned itself as the primary beneficiary of America's pivot toward sovereign defense supply chains. The company's "Blue UAS" certification and inclusion on NATO's procurement catalog provide immediate access to both domestic and allied defense markets at a critical moment of global rearmament.

The company's technological architecture differentiates it from competitors through integrated systems spanning air, land, and sea domains. The "Arachnid" family, including the Black Widow quadcopter, Edge 130 hybrid VTOL, and FANG strike drone, creates a closed-loop ecosystem enhanced by partnerships with Palantir for GPS-denied navigation and Doodle Labs for anti-jamming communications. Red Cat's Visual SLAM technology enables autonomous operation in contested electromagnetic environments, directly addressing Pentagon requirements under the Replicator initiative for "attritable mass" autonomous systems. The recent partnership with Apium Swarm Robotics advances one-to-many drone control, multiplying the combat effectiveness of individual operators.

Strategic acquisitions of FlightWave and Teal Drones have rapidly expanded Red Cat's capabilities while maintaining strict supply chain sovereignty. The company's selection as a finalist for the Army's Short Range Reconnaissance Tranche 2 program validates its tactical systems for infantry deployment. With NATO allies ramping up defense spending and the Ukraine conflict demonstrating voracious demand for small unmanned systems, Red Cat faces a multi-year secular tailwind. The convergence of regulatory protection, technological differentiation, financial strength, and geopolitical necessity positions Red Cat not merely as a defense contractor but as a cornerstone of America's robotic warfare infrastructure for the coming decade.

Can a $89M Company Execute on a $151B Defense Contract?Sidus Space (NASDAQ: SIDU) experienced a dramatic 97% stock surge following its selection for the Missile Defense Agency's SHIELD program, an Indefinite-Delivery/Indefinite-Quantity (IDIQ) contract with a staggering $151 billion ceiling. This represents an extraordinary valuation asymmetry—the contract ceiling is 1,696 times the company's current market capitalization of approximately $89 million. The SHIELD award validates Sidus's AI-enabled satellite technology as critical to America's "Golden Dome" missile defense strategy, positioning the micro-cap company alongside defense giants like Parsons Corporation to compete for task orders over the next decade.

The company's LizzieSat platform and FeatherEdge AI system address urgent national security needs, particularly the hypersonic missile threat from near-peer adversaries. By processing data at the edge in orbit rather than relaying it to ground stations, Sidus reduces the "kill chain" latency from minutes to milliseconds—a capability essential for tracking maneuvering hypersonic glide vehicles. The company's 3D-printed satellite manufacturing approach enables rapid 45-day production cycles, supporting the Pentagon's "Tactically Responsive Space" doctrine for quickly reconstituting destroyed assets in contested environments.

However, significant execution risks remain. Sidus currently generates under $5 million in annual revenue while burning approximately $6 million per quarter, with only $12.7 million in cash reserves as of Q3 2025. The company operates at negative gross margins and survives through dilutive equity raises. The SHIELD contract is not guaranteed revenue but rather a "hunting license" requiring successful competitive bidding on individual task orders. The path to profitability depends on winning sufficient task orders to achieve the scale needed to cover high fixed costs and transition to the high-margin Data-as-a-Service model. For investors, this represents a high-risk, asymmetric bet on whether a micro-cap can successfully navigate the "Valley of Death" to become a defense prime contractor.

Will Quantum Computing Rewrite the Rules of Global Power?D-Wave Quantum Inc. (QBTS) stands at the intersection of three transformative forces reshaping the investment landscape: the intensifying U.S.-China technology race, the shift toward energy-efficient computing, and the militarization of optimization technology. The company has achieved what few quantum computing firms can claim: actual commercial revenue with over 200% year-over-year growth and software-like gross margins approaching 78%. With a fortified balance sheet of $836 million in cash, D-Wave has eliminated the existential funding risk that plagues most deep-tech ventures, providing a multi-year runway to execute its dual-track strategy of commercializing quantum annealing while developing next-generation gate-model systems.

The strategic deployment of D-Wave's Advantage2 quantum computer at Davidson Technologies in Huntsville, Alabama, the heart of U.S. missile defense, marks a watershed moment. This isn't cloud access; it's physical hardware embedded in secure defense infrastructure, optimizing interceptor assignments and radar scheduling for national security applications. As the U.S.-China Economic and Security Review Commission warns of "Q-Day" threats and recommends $2.5 billion in quantum funding through 2030, D-Wave's transition from research curiosity to critical defense asset positions it to capture significant government procurement contracts. The company's quantum annealing technology solves combinatorial optimization problems that classical supercomputers struggle with, issues that underpin modern warfare logistics, supply chain resilience, and industrial competitiveness.

Beyond defense, D-Wave addresses a critical bottleneck in the AI revolution: energy consumption. As data centers strain against power grid limits, D-Wave's quantum annealers offer energy-efficient solutions for optimization problems, from pharmaceutical drug discovery to financial portfolio management. The company's "Proof of Quantum Work" blockchain mechanism demonstrates potential applications in secure financial infrastructure, while partnerships with Fortune 500 companies, such as BASF and Ford, show immediate operational value. Scientific validation has proven D-Wave's annealers vastly outperform both gate-model quantum competitors and classical supercomputers on specific problem sets. With institutional investors like Citadel increasing their stakes and macroeconomic conditions favoring a 2026 rotation toward high-growth tech as interest rates decline, D-Wave represents an asymmetric opportunity, a company priced for skepticism but delivering results that demand conviction.

LHX Analysis: $1B Space Deal Signals GrowthThe Strategic Pivot

L3Harris Technologies (NYSE: LHX) is redefining the defense landscape. While the stock has climbed 38.6% year-to-date, recent developments suggest the rally is just beginning. The catalyst is a massive $843 million contract with the Space Development Agency (SDA). This deal confirms L3Harris as a primary player in modern warfare infrastructure. With projected revenues hitting $22 billion and free cash flow nearing $2.7 billion, the fundamentals are robust. This analysis dissects the strategic drivers behind this growth.

Geopolitics & Geostrategy: The High Ground

Modern conflict has shifted to orbit. Major powers are actively militarizing space to secure communications and surveillance advantages. The SDA contract for infrared satellites places L3Harris at the center of this geopolitical contest. Governments demand persistent missile warning capabilities to counter hypersonic threats from rivals. L3Harris provides the "eyes in the sky" necessary for national survival. This geostrategic necessity ensures long-term demand for their orbital assets.

Industry Trends: From Armor to Dat

The defense industry is moving away from heavy manufacturing toward intelligence and connectivity. Tanks and ships are vulnerable without secure data links. L3Harris specializes in this exact niche: avionics, electronic warfare, and sensing. They are not building the metal shell; they are building the brain. This trend favors agile tech integrators over traditional heavy metal defense contractors. The market values high-margin electronics over low-margin hardware.

Technology & Science: Infrared Precision

The science behind the new SDA contract is critical. These satellites utilize advanced infrared sensors to track heat signatures from missile launches. Developing these sensors requires elite engineering and physics capabilities. L3Harris has mastered the suppression of "background noise" in space to detect small targets. This scientific edge creates a high barrier to entry for competitors. Few companies possess the technical heritage to execute this level of precision engineering.

Business Models & Economics: Cash Flow Efficiency

L3Harris operates on a highly efficient financial model. The company generated nearly $2.7 billion in free cash flow (FCF) recently. This liquidity allows them to fund internal Research and Development (R&D) without relying on expensive debt. In a high-interest-rate macroeconomic environment, cash is king. Their ability to self-fund innovation while paying dividends makes them attractive to institutional investors. The economic engine here is stability combined with growth.

Cyber & High-Tech: Hardened Systems

Space assets are prime targets for cyberattacks. L3Harris integrates "cyber-resilience" directly into its satellite architecture. They do not just build communication radios; they build encrypted networks that withstand jamming and spoofing. This convergence of hardware and cybersecurity is a key selling point. Defense clients pay a premium for systems that operate reliably in contested electronic environments.

Management & Leadership: Organic Discipline

The leadership team at L3Harris is executing a disciplined strategy. Instead of relying solely on expensive acquisitions, they are driving "organic growth." The recent financial report highlights this internal efficiency. Management focuses on operational excellence and clearing supply chain bottlenecks. This focus has improved margins and delivery times. Investors trust leadership that delivers on promises without overleveraging the balance sheet.

Patent Analysis: Protecting Intellectual Property

A review of the sector suggests L3Harris holds a "moat" of intellectual property. Their patent portfolio likely covers proprietary sensor integration and waveform technologies. These patents legally protect their market share in tactical communications. Competitors cannot easily replicate their avionics suites without infringing on protected tech. This IP fortress secures future revenue streams and keeps margins high.

Forecast: The Trajectory

L3Harris is currently undervalued relative to its potential. The $843 million contract is a signal, not an anomaly. As global tensions rise, the premium on space-based intelligence will increase. The company’s focus on high-tech sensors, strong cash flow, and strategic positioning makes it a formidable stock. Traders should view the current price as an entry point before the full value of these space contracts materializes in 2026 earnings.

Can One Company Own the Ocean Floor?Kraken Robotics has emerged as a dominant force in subsea intelligence, riding three converging megatrends: the weaponization of seabed infrastructure, the global energy transition to offshore wind, and the technological obsolescence of legacy sonar systems. The company's Synthetic Aperture Sonar (SAS) technology delivers range-independent 3cm resolution, 15 times superior to conventional systems. At the same time, its pressure-tolerant SeaPower batteries solve the endurance bottleneck that has plagued autonomous underwater vehicles for decades. This technological moat, protected by 31 granted patents across 19 families, has transformed Kraken from a niche sensor manufacturer into a vertically integrated subsea intelligence platform.

The financial metamorphosis validates this strategic positioning. Q3 2025 revenue surged 60% Year-Over-Year to $31.3 million, with gross margins expanding to 59% and adjusted EBITDA growing 92% to $8.0 million. The balance sheet fortress of $126.6 million in cash, up 750% from the prior year, provides the capital to pursue a dual strategy: organic growth through NATO's Critical Undersea Infrastructure initiative and strategic acquisitions, such as the $17 million purchase of 3D at Depth, which added subsea LiDAR capabilities. The market's 1,000% re-rating since 2023 reflects not speculative excess but a fundamental recognition that Kraken controls critical infrastructure for the emerging blue economy.

Geopolitical tensions have accelerated demand, with the Nord Stream sabotage serving as an inflection point for defense procurement. NATO's Baltic Sentry mission and the alliance-wide focus on protecting 97% of internet traffic carried by undersea cables create sustained tailwinds. Kraken's technology participated in seven naval teams at REPMUS 2025, demonstrating platform-agnostic interoperability that positions it as the universal standard. Combined with exposure to the offshore wind supercycle (250 GW by 2030) and potential deep-sea mining operations valued at $177 trillion in resources, Kraken has positioned itself as the indispensable "picks and shovels" provider for multiple secular growth vectors simultaneously.

Can Software Win Wars and Transform Commerce?Palantir Technologies has emerged as a dominant force in artificial intelligence, achieving explosive growth through its unique positioning at the intersection of national security and enterprise transformation. The company reported its first billion-dollar quarter with 48% year-over-year sales growth, driven by an unprecedented 93% surge in U.S. commercial revenue. This performance stems from Palantir's proprietary Ontology architecture, which solves the critical challenge of unifying disparate data sources across organizations, and its Artificial Intelligence Platform (AIP) that accelerates deployment through intensive bootcamp sessions. The company's technological moat is reinforced by strategic patent protections and a remarkable 94% Rule of 40 score, signaling exceptional operational efficiency.

Palantir's defense entrenchment provides a formidable competitive advantage and guaranteed revenue streams. The company secured a $618.9 million Army Vantage contract and deployed the Maven Smart System for the Marine Corps, positioning itself as essential infrastructure for the Pentagon's Combined Joint All-Domain Command and Control strategy. These systems enhance battlefield decision-making, with targeting officers processing 80 targets per hour versus 30 without the platform. Beyond U.S. forces, Palantir supports NATO operations, assists Ukraine, and partners with the UK Ministry of Defence, creating a global network of high-margin, long-term government contracts across democratic allies.

Despite achieving profitability with 26.8% operating margins and maintaining $6 billion in cash with virtually no debt, Palantir trades at extreme valuations of 100 times revenue and 224 times forward earnings. With 84% of analysts recommending Hold or Sell ratings, the market remains divided on whether the premium is justified. Bulls argue the valuation reflects Palantir's transformation from niche government contractor to critical AI infrastructure provider, with analysts projecting potential revenue growth from $4.2 billion to $21 billion. The company's success across nine strategic domains—from military modernization to healthcare analytics—suggests it has built an "institutionally required platform" that could justify sustained premium pricing.

The investment thesis ultimately hinges on whether Palantir's structural advantages—its proprietary data integration technology, defense entrenchment, and accelerating commercial adoption—can sustain the growth trajectory demanded by its valuation. While the platform's complexity requires heavy customization and limits immediate scalability compared to simpler competitors, the 93% commercial growth rate validates enterprise demand. Investors must balance the company's undeniable technological and strategic positioning against valuation risk, with any growth deceleration likely triggering significant multiple compression. For long-term investors willing to weather volatility, Palantir represents a bet on AI infrastructure dominance across both military and commercial domains.

Data Patterns – Absorption Phase Near Trendline ResistanceData Patterns (India) Ltd – Absorption Phase Near Trendline Resistance

NSE:DATAPATTNS

📈 Pattern & Setup:

Data Patterns is floating right below a crucial descending trendline resistance, showing classic signs of absorption after two consecutive shakeouts. Each shakeout was followed by a recovery with narrowing volatility, suggesting strong hands quietly building positions beneath the surface.

The stock has also formed a “Bull Snort” setup — a rare occurrence where the price absorbs supply near resistance instead of rejecting it. This indicates institutional accumulation and prepares the ground for a clean breakout move.

A close above 2,850–2,860 with strong volume could confirm the breakout, unlocking a potential move toward 3,800+.

📝 Trade Plan:

✍Entry: Above 2,860 (breakout confirmation)

🚩Stop-Loss: 2,700 (below the absorption low)

🎯Targets:

Target 1 → 3,250

Target 2 → 3,800 (38% potential move)

💡 Pyramiding Strategy:

1. Enter 60% above 2,860 on breakout confirmation

2. Add remaining 40% above 2,900 with volume follow-through

3. Trail stop-loss to 2,780 once price crosses 3,100

🧠 Logic Behind Selecting this Trade:

The combination of back-to-back shakeouts, higher lows, and visible absorption reflects smart money activity. The stock’s ability to hold near resistance instead of falling back confirms strength. This kind of coiling price action just below a trendline often leads to a powerful breakout rally once supply is fully absorbed.

Keep Learning. Keep Earning.

Let’s grow together 📚🎯

🔴Disclaimer:

This analysis is for educational purposes only. Not a buy/sell recommendation. Please do your own research or consult your financial advisor before trading.

KOPN: trend structure NASDAQ:KOPN price is already quite extended after multiple upside legs, but the mid-term trend structure still presents decent upside potential as long as price holds above the 2.75–2.25 support zone. The next important resistance level is around 6.30.

Chart:

Can China Weaponize the Elements We Need Most?China's dominance over rare earth element (REE) processing has transformed these strategic materials into a geopolitical weapon. While China controls approximately 69% of global mining, its true leverage lies in processing, where it commands over 90% of Global capacity and 92% of permanent magnet manufacturing. Beijing's 2025 export controls exploit this chokehold, requiring licenses for REE technologies used even outside China, effectively extending regulatory control over global supply chains. This "long-arm jurisdiction" threatens critical industries from semiconductor manufacturing to defense systems, with immediate impacts on companies like ASML facing shipment delays and US chipmakers scrambling to audit their supply chains.

The strategic vulnerability runs deep through Western industrial capacity. A single F-35 fighter jet requires over 900 pounds of REEs, while Virginia-class submarines need 9,200 pounds. The discovery of Chinese-made components in US defense systems illustrates the security risk. Simultaneously, the electric vehicle revolution guarantees exponential demand growth. EV motor demand alone is projected to reach 43 kilotons in 2025, driven by the prevalence of permanent magnet synchronous motors that lock the global economy into persistent REE dependency.

Western responses through the EU Critical Raw Materials Act and US strategic financing establish ambitious diversification targets, yet industry analysis reveals a harsh reality: concentration risk will persist through 2035. The EU aims for 40% domestic processing by 2030, but projections show the top three suppliers will maintain their stranglehold, effectively returning to 2020 concentration levels. This gap between political ambition and physical execution stems from formidable barriers environmental permitting challenges, massive capital requirements, and China's strategic shift from exporting raw materials to manufacturing high-value downstream products that capture maximum economic value.

For investors, the VanEck Rare Earth/Strategic Metals ETF (REMX) operates as a direct proxy for geopolitical risk rather than traditional commodity exposure. Neodymium oxide prices, which plummeted from $209.30 per kilogram in January 2023 to $113.20 in January 2024, are projected to surge to $150.10 by October 2025 volatility driven not by physical scarcity but by regulatory announcements and supply chain weaponization. The investment thesis hinges on three pillars: China's processing monopoly converted into political leverage, exponential green technology demand establishing a robust price floor, and Western industrial policy guaranteeing long-term financing for diversification. Success will favor companies establishing verifiable, resilient supply chains in downstream processing and magnet manufacturing outside China, though the high costs of secure supply, including mandatory cybersecurity auditing and environmental compliance, ensure elevated prices for the foreseeable future.

GRSE buy at cmp 2625 tgt 3764 for positionalGRSE buy at cmp 2625 tgt 3764 for positional , tgt will done in next 90+ trading days perfect buying range 2500 to 2541

Can Kraken Robotics Dominate the Undersea Battlefield?Kraken Robotics stands at the forefront of the rapidly expanding unmanned underwater systems sector, merging technological innovation with strategic positioning. The Canadian company has built a robust competitive moat through two core technologies: its high-resolution Synthetic Aperture Sonar (SAS) and pressure-tolerant SeaPower batteries. These innovations enable superior imaging and endurance capabilities, giving Kraken a decisive edge in both defense and commercial subsea markets. By vertically integrating its components, platforms, and services, Kraken captures value across the full maritime technology spectrum, turning each innovation into a multiplier for the next.

The company's partnership with Anduril Industries, a disruptive force in modern defense technology, has become a potential game-changer. Kraken provides key sonar and energy systems for Anduril’s Dive-LD and Ghost Shark autonomous underwater vehicles, positioning itself as a strategic enabler in the race toward naval autonomy. This alliance could multiply Kraken’s revenue base several times over if Anduril scales production as planned. Yet, this same dependence also presents significant concentration risk; any delay or contract change at Anduril could sharply impact Kraken’s trajectory.

Financially, Kraken is at a critical juncture. Recent years have seen consistent double-digit revenue growth and expanding EBITDA margins, supported by strong demand for its subsea technologies. A C$115 million capital raise in 2025 strengthened its balance sheet and positioned the company for large-scale production expansion. Forward-looking models forecast revenue growth from C$128 million in 2025 to over C$850 million by 2030 in the base case, with substantial margin expansion as economies of scale take hold.

Despite its risks, operational, financial, and technological, Kraken Robotics embodies a rare pure-play exposure to the multi-decade transformation of underwater defense and exploration. For investors with the patience and tolerance for volatility, it represents a high-risk, high-reward opportunity. If the company executes on its Anduril partnership and leverages its subsea dominance effectively, it may not just participate in the next defense revolution - it could define it.

How Does a Silent Giant Dominate Critical Technologies?Teledyne Technologies has quietly established itself as a formidable force across defense, aerospace, marine, and space markets through a disciplined strategy of strategic positioning and technological integration. The company recently reported record Q2 2025 results with net sales of $1.51 billion (10.2% increase) and demonstrated exceptional organic growth across all business segments. This performance reflects not market timing but the culmination of deliberate long-term positioning at the intersection of mission-critical, high-barrier-to-entry markets where geopolitical factors create natural competitive advantages.

The company's strategic acumen is exemplified by products like the Black Hornet Nano micro-UAV, which has proven its tactical value in conflicts from Afghanistan to Ukraine, and the emerging Black Recon autonomous drone system for armored vehicles. Teledyne has strengthened its market position through geopolitically aligned partnerships, such as its collaboration with Japan's ACSL for NDAA-compliant drone solutions, effectively turning regulatory compliance into a competitive moat against non-allied competitors. The 2021 acquisition of FLIR Systems for $8.2 billion demonstrated horizontal integration mastery, with thermal imaging technology now deployed across multiple product lines and market segments.

Teledyne's competitive advantage extends beyond products to intellectual property dominance, holding 5,131 patents globally with an exceptional 85.6% USPTO grant rate. These patents span imaging and photonics (38%), defense and aerospace electronics (33%), and scientific instrumentation (29%), with frequent citations by industry giants like Boeing and Samsung indicating their foundational nature. The company's $474 million annual R&D investment, supported by 4,700 engineers with advanced degrees, ensures continuous innovation while building legal barriers against competitors.

The company has proactively positioned itself to meet emerging regulatory requirements, particularly the Department of Defense's new Cybersecurity Maturity Model Certification (CMMC) mandate, which takes effect in October 2025. Teledyne's existing cybersecurity infrastructure and certifications provide a crucial advantage in meeting these standards, creating an additional "compliance moat" that will likely enable the company to capture increased defense contract opportunities as competitors struggle with new requirements.

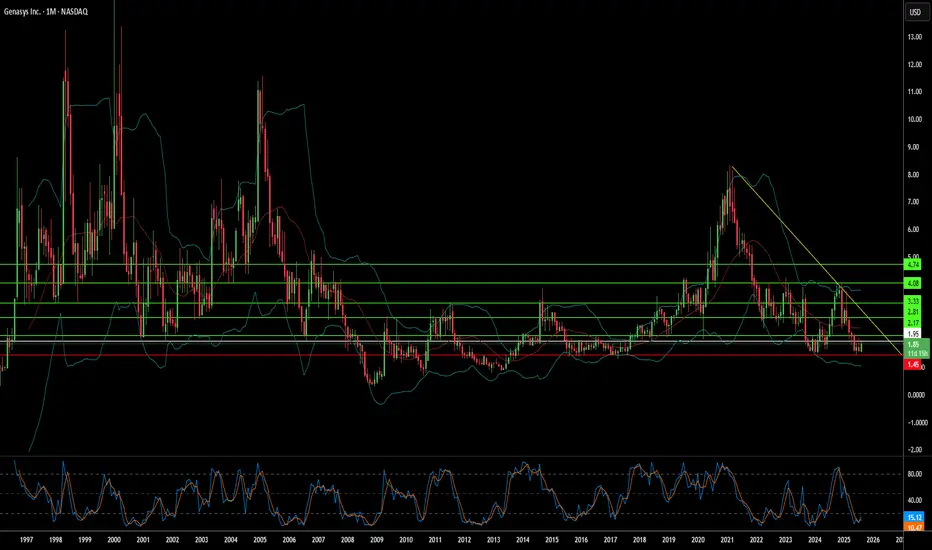

Can Sound Waves Become Tomorrow's Shield Against Global Chaos?Genasys Inc. (NASDAQ: GNSS) operates at the convergence of escalating global instability and technological innovation, positioning itself as a critical player in the protective communications sector. The company's sophisticated portfolio combines its proprietary Long Range Acoustic Device (LRAD) systems with the cloud-first Genasys Protect software platform, serving over 155 million individuals across more than 100 countries. With law enforcement agencies in over 500 U.S. cities utilizing LRAD systems for applications ranging from SWAT operations to crowd control, Genasys has established itself as the global standard in acoustic hailing devices, delivering messages 20-30 decibels louder and with superior intelligibility compared to traditional systems.

The company's growth trajectory aligns with powerful macroeconomic forces driving unprecedented demand for protective communications. Global defense spending surged to $2.718 trillion in 2024—a 9.4% increase representing the steepest rise since 1988—while the critical infrastructure protection market is projected to grow from $148.64 billion in 2024 to $213.94 billion by 2032. Genasys's integrated solutions directly address this expanding market through non-kinetic de-escalation capabilities and cyber-physical threat mitigation, recently securing $1 million in LRAD orders for the Middle East and Africa as geopolitical tensions intensify.

Genasys's competitive advantage rests on a robust foundation of 17 registered patents, particularly in acoustic hailing technology, creating significant barriers to entry while enabling premium pricing. The company's $4.2 million annual R&D investment ensures continued innovation, while strategic partnerships like its collaboration with FloodMapp demonstrate the platform's evolution toward predictive threat mitigation rather than merely reactive response. Despite current profitability challenges—with Q3 2025 net losses of $6.5 million—the company maintains a substantial project backlog exceeding $16 million, plus the transformative $40 million Puerto Rico Early Warning System project expected to generate $15-20 million in fiscal 2025 revenue.

The investment thesis centers on Genasys's unique positioning to capitalize on the global shift toward sophisticated, non-lethal security solutions amid rising geopolitical instability. With percentage-of-completion accounting currently suppressing gross margins to 26.3% but promising significant margin expansion as major projects near completion, the company represents a compelling opportunity for investors seeking exposure to defense, public safety, and critical infrastructure growth markets. The convergence of technological superiority, strategic market positioning, and substantial revenue visibility through confirmed backlog suggests significant long-term potential despite near-term financial complexities.

Is a Spider's Silk the New Steel and Kevlar?Kraig Biocraft Laboratories, Inc. is a leading biotechnology company that has pioneered a scalable method for producing genetically engineered spider silk. By leveraging the domesticated silkworm as a "microfactory," the company has overcome the challenges of traditional spider farming. Its proprietary gene-editing technology inserts specific spider silk protein genes into silkworms, enabling them to spin high-performance fibers like Dragon Silk™ and Monster Silk®. This unique approach provides a cost-effective and efficient manufacturing platform, setting the company apart from competitors who rely on expensive fermentation-based methods.

The resulting material possesses properties that exceed those of conventional high-performance fibers. Genetically engineered spider silk is renowned for its exceptional toughness and tensile strength, a combination that makes it stronger than steel and tougher than Kevlar, while remaining remarkably lightweight. This unique blend of characteristics positions the company to capitalize on the rapidly expanding technical fibers and biomaterials markets, which are valued at billions of dollars annually. The company's production platform offers a significant competitive advantage in creating high-value materials for a wide range of industries.

This groundbreaking material has substantial strategic and geopolitical implications, particularly for defense and security. Its superior strength and energy absorption capabilities make it an ideal candidate for applications such as advanced ballistic protection and lightweight military gear. The company has engaged in collaborative agreements with government agencies, further validating its technology and demonstrating its strategic importance. Beyond defense, the material's potential extends to aerospace, high-end textiles, and advanced medical devices like sutures and implants.

Furthermore, Kraig Biocraft Laboratories’ technology offers a sustainable alternative to petroleum-based synthetics. The spider silk is a protein-based, biodegradable fiber, and its production process is less resource-intensive. This focus on sustainability and scalability aligns with the growing global demand for eco-friendly materials. By combining innovative technology, superior material performance, and a clear path to commercialization, Kraig Biocraft Laboratories is poised to be a pivotal player in the future of advanced materials.

Is BigBear.ai the Next Titan of Defense AI?BigBear.ai (NYSE: BBAI) is emerging as a significant player in the artificial intelligence landscape, particularly within the critical national security and defense sectors. While often compared to industry giant Palantir, BigBear.ai carves its niche by intensely focusing on modern warfare applications, including guiding unmanned vehicles and optimizing missions. The company has recently garnered considerable investor attention, evidenced by its impressive 287% rally over the past year and a notable surge in public interest. This enthusiasm stems from several key factors, including a substantial 2.5x increase in backlog orders to $385 million by March 2025 and a significant ramp-up in research and development spending, signaling robust foundational growth.

BigBear.ai's technological prowess underpins its rising profile. The company develops sophisticated AI and machine learning models for diverse applications, from facial recognition systems deployed at major international airports like JFK and LAX to AI-augmented shipbuilding software for the U.S. Navy. Its Pangiam® Threat Detection and Decision Support Platform enhances airport security by integrating with advanced CT scanner technology, while its ConductorOS platform facilitates secure communication and coordination for drone swarm operations under the U.S. Army's Project Linchpin. These cutting-edge solutions position BigBear.ai at the forefront of AI-driven advancements crucial for evolving geopolitical landscapes and increasing defense AI investments.

Strategic collaborations and a favorable market environment further fuel BigBear.ai's ascent. The company recently formed a significant partnership in the UAE with Easy Lease and Vigilix Technology Investment to accelerate AI adoption across key industries like mobility and logistics, marking a major step in its international expansion. Additionally, multiple contracts with the U.S. Department of Defense, including those for J-35 fleet management and geopolitical risk assessment, underscore its vital role in government initiatives. While BigBear.ai faces challenges, including revenue stagnation, escalating losses, and stock volatility, its strategic market position, growing backlog, and continuous innovation in mission-critical AI solutions present a compelling high-risk, high-reward investment opportunity in the burgeoning defense AI sector.

Can AI Revolutionize Our World Beyond Data?Palantir Technologies has not merely emerged but soared in the financial markets, with shares rocketing 22% after an earnings report that surprised Wall Street. The company's fourth-quarter results for 2024 were a testament to its strategic placement at the heart of the AI revolution, exceeding expectations with revenue and earnings per share. This performance underscores the potential of AI not only to enhance but potentially redefine operational paradigms across industries, particularly in defense and governmental sectors where Palantir holds significant sway.

The growth trajectory of Palantir is not just a story of numbers; it's a narrative of how AI can be harnessed to transform complex data into actionable insights, thereby driving efficiency and innovation. CEO Alex Karp's vision of Palantir as a software juggernaut at the inception of a long-term revolution invites us to ponder the broader implications of AI. With a 64% growth in U.S. commercial revenue and a 45% increase in U.S. government revenue, Palantir demonstrates the power of AI to bridge the gap between raw data and strategic decision-making in real-world applications.

Yet, this success story also prompts critical reflection. How sustainable is this growth, especially considering Palantir's heavy reliance on government contracts? The company's future might hinge on its ability to diversify its clientele and continue innovating in a rapidly evolving tech landscape. As we stand at what Karp describes as the "beginning of the first act" of AI's influence, one must ask: Can Palantir maintain its momentum, or will it face challenges in a market increasingly crowded with AI contenders? This question challenges investors, technologists, and policymakers alike to consider the long-term trajectory of AI integration in our society.

Can Stealth Redefine Power on the Battlefield?In a strategic leap forward, Northrop Grumman has introduced the Stand-in Attack Weapon (SiAW). This new air-to-ground missile promises to redefine the landscape of modern aerial warfare. This innovation, designed to be deployed from stealth aircraft like the F-35, offers unprecedented capabilities in striking high-value, mobile targets while keeping the launching platform safe from enemy defenses. The SiAW's development highlights a critical evolution in military technology, where speed, precision, and stealth converge to neutralize threats in complex, hostile environments.

The SiAW's design is not merely an incremental improvement but a paradigm shift. It builds upon the foundational technology of the AGM-88G AARGM-ER but goes further by increasing range, speed, and accuracy, all while ensuring compatibility with future stealth platforms. This missile is tailored to engage rapidly relocatable targets like missile launchers and electronic warfare systems, which are pivotal in modern anti-access/area denial (A2/AD) strategies. Its ability to operate autonomously after launch, even under conditions of electronic jamming, challenges military strategists to rethink traditional engagement tactics.

The implications of the SiAW extend beyond mere tactical advantages. With the U.S. Air Force planning to achieve initial operational capability by 2026 and aiming for a significant purchase by 2028, the missile is set to become a cornerstone in air combat strategy. It enhances U.S. military capabilities and signals a shift in international defense dynamics, prompting allies and adversaries to adapt their military doctrines.

Moreover, this development by Northrop Grumman sparks a conversation about the ethics and future of warfare. As technology allows for more precise and less risky engagements, the moral calculus of military operations shifts. This missile could - potentially decrease collateral damage, but it also raises questions about the increasing automation of war and the human element's role in decision-making processes.

Thus, the SiAW does not just push the envelope of what's technologically possible; it invites a deeper contemplation on the nature of conflict, the responsibilities of power, and the path forward in an era where technology can both protect and threaten on unimaginable scales. As we stand on the brink of this new frontier, one must ponder: How will such advancements shape the future of global security and peace?

Can Defense Industry Giants Turn Global Tensions into SustainablIn a fascinating paradox of modern defense economics, RTX Corporation stands at the epicenter of escalating global security demands while grappling with production constraints that challenge its ability to meet them. With a remarkable $90 billion defense backlog and recent approval for a $744 million missile sale to Denmark, RTX exemplifies how geopolitical tensions are reshaping the aerospace and defense industry landscape. Yet this surge in demand raises profound questions about the sustainability of growth in an industry where production capacity faces inherent limitations.

The company's financial performance tells a compelling story of adaptation and resilience, with its stock attracting increased attention from major analysts and an upward revision of earnings guidance. However, beneath these promising figures lies a more complex narrative: RTX must balance the immediate pressures of global defense requirements against the long-term challenges of production capacity and technological innovation. This delicate equilibrium becomes even more critical as the company serves not just one nation's defense needs, but those of at least 14 allied nations simultaneously.

What emerges is a thought-provoking case study in strategic industrial scaling: How can defense manufacturers like RTX transform short-term geopolitical pressures into sustainable long-term growth? The answer may lie in the company's diversified approach, combining traditional defense contracts with innovative aerospace solutions, while navigating the intricate balance between immediate market demands and long-term strategic planning. This scenario challenges our traditional understanding of defense industry dynamics and forces us to reconsider how global security needs might reshape industrial capacity in the decades to come.

Is the XRQ-73 the ultimate silent killer?The Unseen Predator

Imagine a drone so advanced it can slip past the most sophisticated defenses, a silent hunter in the sky. The XRQ-73, DARPA's latest X-plane, is not just a UAV; it's a harbinger of a new era in warfare.

The XRQ-73, a groundbreaking new drone from DARPA, could revolutionize the way wars are fought. With its advanced stealth technology and hybrid-electric propulsion, this unmanned aerial vehicle (UAV) is capable of performing a wide range of missions, from precision strikes to reconnaissance.

A Technological Marvel

Combining the best of electric and traditional propulsion, the XRQ-73 is a marvel of engineering. Its stealthy design and advanced capabilities make it a formidable asset for military operations. From precision strikes to intelligence gathering, its potential applications are vast.

Beyond the Battlefield

But the XRQ-73's impact extends beyond the battlefield. Its technology could revolutionize civilian sectors, aiding in disaster relief, search and rescue, and environmental monitoring.

The Future of Warfare

The XRQ-73 is a testament to human ingenuity and a glimpse into the future of warfare. As technology continues to evolve, we can expect to see even more groundbreaking advancements in unmanned aerial vehicles.

But what truly sets it apart?

Its ability to remain undetected, combined with its long-range capabilities and versatility, makes the XRQ-73 a formidable weapon. As technology advances, we can only imagine the possibilities that this and other similar drones hold for the future of warfare.

Are you ready for a world where drones rule the skies?

PLTR Has Reached Key Upside Levels: Tighten StopsPrimary Chart : Palantir Technologies Inc. NYSE:PLTR on a daily time frame with key Fibonacci Levels drawn as well as support, resistance, the 21-day EMA, and a critical VWAP from the bear-market lows of December 2022

Palantir Technologies Inc. NYSE:PLTR , once a tech darling of the 2020-2021 bull market in equities, has achieved a substantial retracement now of its vicious 2021-2022 bear-market decline. PLTR has been a popular stock ever since going public via a direct public offering, the same type of registered share offering used by NYSE:SPOT and Slack Technologies, LLC, which is now owned by Salesforce. PLTR provides data-analysis and AI technologies to large government agencies, including defense agencies and branches of the military, as well as large corporations.

Despite periods of consolidation—especially from August 1, 2023, to November 1, 2023, PLTR has been in a primary-degree uptrend since its bear market low on December 27, 2022. The uptrend has been mostly strong and supported by the volume-weighted average price anchored to the bear-market low (green), which is shown on the Primary Chart above.

Price has also run into a major long-term Fibonacci level at $20.74. This level is also shown on the Primary Chart in gold. Using a logarithmic scale, this Fibonacci level at $20.74 is a 61.8% retracement of the all-time high to the December 2022 low. Above this level suggests more upside. Below this level suggests either (i) consolidation, or (ii) resumption of the downtrend (if key long-term support levels break decisively).

When plotted on a linear chart, PLTR has also reached (and stalled at) a critical Fibonacci retracement of its entire bear-market decline. This .382 Fibonacci retracement at $20.85 is often where bull flags or bear flags consolidate within a given trend. Some might view this level as a decisive level for the bbear case given that 38.2% of the bear-market decline has been retraced, and therefore, rising above this level would suggest the uptrend has further to climb (e.g., $25.46 at the 50% retracement shown in green below). So this level at $20.74 / $20.85 (whether viewed as a .618 Fibonacci retracement or a .382 Fibonacci retracement) is crucial to monitor.

Supplementary Chart A

This post argues that the primary uptrend looks as though it has become extended. Does this mean the high has been reached for the this particular uptrend? It's not wise to call the end of a primary trend until technical confirmation has occurred. Picking a long-term high is nearly impossible. The negative divergences on weekly and daily time frames are shown in the following charts:

Supplementary Chart B

Supplementary Chart C

Supplementary Chart D

Supplementary Chart E

Supplementary Chart F

So momentum has definitely slowed in this AI / tech / data-analysis name, and negative (bearish) divergences have arisen. At a minimum, this could signal a period of consolidation lies ahead in the first half (1H) of 2024. The supplementary charts show the divergences one should watch carefully. This may provide a reason for bullish position traders and investors to tighten stops. And if key levels snap decisively, such as the $16.36 level or the August 2023 supports at $13.68 or the VWAP (green) from December 2022, then watch for a retest or break of lows.