Options Blueprint Series [Intermediate]: Breakout With A Buffer1. Market Context: Strength at the Surface, Fragility Underneath

The NASDAQ-100 futures market currently occupies a rare and structurally important zone. Price is trading above a prior all-time high, yet remains below the most recent all-time high, with only a relatively modest distance separating current price from historical extremes.

From a purely technical standpoint, this positioning can be interpreted as constructive. Markets that hold above former highs often retain the potential to transition into renewed expansion and price discovery. However, context matters. This strength exists alongside broader signals of vulnerability across U.S. equity markets—signals that have been explored in prior work and that suggest upside continuation is not guaranteed.

This creates a dual-risk environment:

Upside risk: missing participation if the NASDAQ resumes trending higher.

Downside risk: absorbing full exposure if price fails near historical extremes.

In such conditions, directional certainty is low, but volatility risk is high. This is where outright futures exposure may be less efficient, and where options structures can offer a more robust framework.

2. The Problem With Linear Exposure at Elevated Levels

Holding NASDAQ-100 futures outright implies linear exposure:

Every point higher benefits the position.

Every point lower damages it.

Near historical highs, that symmetry becomes problematic. A trader must be correct not only on direction, but also on timing. Even a structurally bullish thesis can fail if volatility expands or if price retraces before resuming higher.

Linear exposure forces a binary outcome:

Be early and absorb drawdowns.

Be late and miss opportunity.

The goal of this blueprint is to avoid that binary trap by reshaping exposure, not eliminating it.

3. Why Options Are Better Suited for This Environment

Options allow traders to separate direction from risk. Rather than committing capital to a single path, options structures can be designed to:

Define maximum loss in advance

Shift break-even points away from current price

Allow time and volatility to work in favor of the position

Importantly, this blueprint does not rely on forecasting. It assumes uncertainty and builds around it.

The objective is not to predict whether the NASDAQ will break higher or fail lower. The objective is to remain functional across multiple outcomes.

4. Instruments Used: NQ and MNQ Options

This structure applies to:

NASDAQ-100 E-mini futures options (NQ)

NASDAQ-100 Micro E-mini futures options (MNQ)

The logic is identical across both contracts. The difference lies in scale:

NQ offers larger notional exposure and fewer contracts.

MNQ allows finer position sizing, particularly useful when structuring multi-leg options strategies.

Both instruments support the same conceptual framework.

5. Introducing the “Breakout With A Buffer” Concept

The core idea behind this blueprint is simple:

Do not chase price near highs

Do not stand aside entirely

Create a buffer below price while retaining upside access

This is achieved by combining:

A bull put spread placed well below current price

A long call positioned above current price

Together, these components transform uncertainty into a structured payoff.

6. Strategy Construction: Step by Step

The structure consists of three legs:

Short put at approximately 22,000

Long put at approximately 21,000

Long call at approximately 28,750

The bull put spread generates a net credit. That credit is then used to fund the long call.

This matters. Rather than paying outright for upside exposure, the structure monetizes downside stability to finance it.

7. Why a Bull Put Spread and Not a Naked Put

Selling naked puts would introduce undefined downside risk, which contradicts the purpose of this blueprint.

The long put:

Caps downside exposure

Converts the position into a defined-risk structure

Clarifies the maximum loss from the outset

This is not about maximizing credit. It is about controlling tail risk.

8. Strike Selection: Structural, Not Arbitrary

The selected put strikes align with:

The prior all-time high region

A visible concentration of UFOs (UnFilled Orders) acting as structural support

UnFilled Orders represent areas where institutional activity previously absorbed selling pressure. Positioning the put spread near such zones introduces a structural buffer, rather than relying on random distance.

The call strike, by contrast, is intentionally placed far above current price. This avoids overpaying for near-term momentum and instead positions for a regime where price transitions into sustained expansion.

9. Why This Is Not a Collar or a Covered Strategy

It is important to distinguish this blueprint from more common approaches:

Collars require long underlying exposure.

Covered calls cap upside and remain fully exposed to downside.

Outright calls depend heavily on timing and volatility expansion.

This structure does none of those things. It:

Does not require owning futures

Does not cap upside

Does not rely on immediate directional movement

Instead, it converts time and uncertainty into functional components of the trade.

10. Risk Profile: Defined, Asymmetric, Intentional

The resulting payoff has several key characteristics:

Maximum risk is limited to the width of the put spread (approximately 1,000 NASDAQ points), adjusted for net credit.

Break-even is pushed far below current price, near the 22,000 area.

Moderate upside benefits from both time decay on the put spread and directional exposure through the call.

Strong upside allows the long call to dominate the payoff.

This asymmetry is intentional. The structure sacrifices linear gains in exchange for survivability.

11. Scenario Analysis

At the time of constructing this case study, NASDAQ-100 futures trade near 25,900.

Possible outcomes:

Gradual advance: The put spread decays, the call gains sensitivity.

Strong breakout: The call drives returns.

Sideways consolidation: Time decay works in favor of the structure.

Moderate decline: The buffer absorbs volatility.

Deep decline below support: The defined maximum loss is realized.

Every outcome is known in advance. That clarity is the edge.

12. Volatility Considerations

This structure is volatility-aware:

Short puts benefit from volatility contraction.

Long calls benefit from volatility expansion during upside moves.

Rather than betting on volatility direction, the structure balances exposure across regimes.

13. NQ vs MNQ Implementation

For NQ:

Fewer contracts

Larger notional exposure

Greater margin efficiency per leg

For MNQ:

More granular sizing

Easier scaling

Reduced psychological pressure per contract

The strategy logic remains unchanged.

14. Contract Specifications

NQ Tick size: 0.25 points = $5

MNQ Tick size: 0.25 points = $0.50

Options multipliers mirror the futures contracts. Margin requirements vary by broker and volatility regime, currently:

NQ margin requirement = $33,500 per contract

MNQ margin requirement = $3,350 per contract

15. Risk Management Is the Strategy

Defined risk does not remove responsibility. This blueprint requires:

Proper sizing

Acceptance of worst-case outcomes

Discipline in structure selection

Options do not eliminate uncertainty. They make it visible.

16. Key Takeaways

Elevated markets demand adaptive exposure.

Options allow participation without blind commitment.

The Breakout With A Buffer blueprint prioritizes risk clarity first, opportunity second.

This framework is reusable whenever markets hover near historical extremes amid conflicting signals.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Definedrisk

Options Blueprint Series [Basic]: Risk-Defined Bull Spread on CLIntroduction

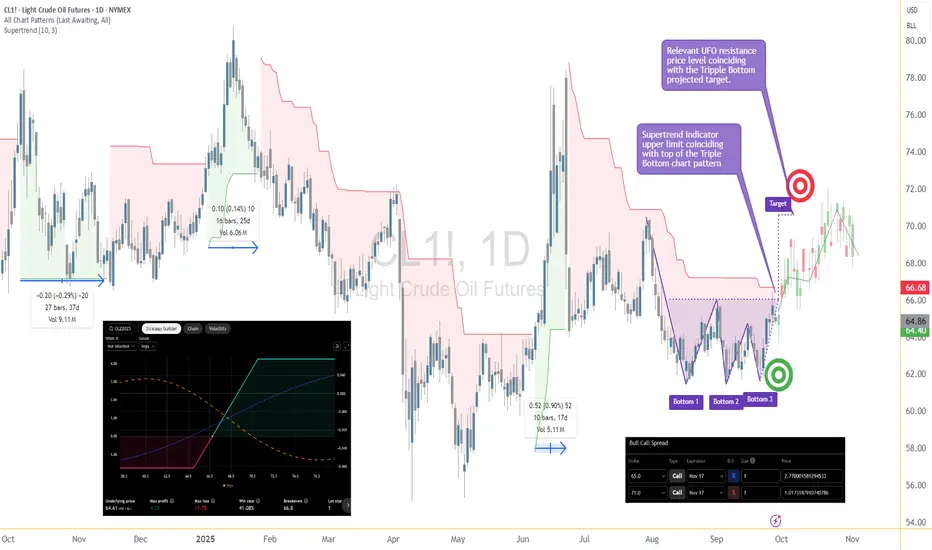

Crude Oil has been carving out a compelling structure on the daily timeframe. The chart has formed a Triple Bottom pattern, a classic base-building formation that often precedes significant directional moves. As prices approach a critical resistance area, traders are watching closely for confirmation of a breakout.

Options provide a unique way to participate in such setups. Instead of buying futures outright — which exposes the trader to potentially unlimited downside — a Bull Call Spread allows participation with limited and predefined risk. Today, we’ll explore how this strategy can be structured on WTI Crude Oil (CL) Options on Futures to target a move higher while keeping risk controlled.

Market Setup

Chart pattern: Triple Bottom on the daily timeframe.

Entry trigger: Breakout above 66.68, where the top line of the Triple Bottom coincides with the upper band of the Supertrend indicator.

Target: ~70.63, which aligns with both the Triple Bottom projected objective and a relevant UFO (UnFilled Orders) resistance area.

Trend context: A successful breakout here would not only complete the Triple Bottom pattern but also suggest a broader trend reversal on the daily chart.

This confluence of technical signals makes 66.68 a price level worth paying attention to.

The Strategy: Bull Call Spread

A Bull Call Spread involves buying one call option with a lower strike and simultaneously selling another call option with a higher strike, both with the same expiration.

Buy: CL Nov-17 65 Call (cost ≈ 2.77)

Sell: CL Nov-17 71 Call (credit ≈ 1.02)

Net debit (cost): ≈ 1.75 points

Since each CL options contract represents 1,000 barrels of oil, the cost of this spread is about $1,750 per spread (subject to commissions).

Why November 17?

The timing matches the behavior of prior Supertrend cycles. The longest green cycle shown on the chart lasted about 37 trading days. By selecting Nov-17 expiration, the position allows sufficient time for a breakout and follow-through, while not overpaying for excess time value.

Risk/Reward Profile

From the risk graph:

Maximum Profit: ≈ 4.25 points, or $4,250 per spread.

Maximum Loss: ≈ 1.75 points, or $1,750 per spread.

Reward-to-Risk Ratio: ~2.4:1.

Breakeven: ~66.8 (very close to breakout level).

The breakeven location is important: it aligns almost exactly with the breakout trigger on the chart. This means that if the technical pattern validates, the option structure begins to work immediately.

The reward-to-risk ratio above reflects the pricing available at the time of building the spread. If a trader waits for confirmation of the breakout before entering, option premiums may rise, making the Bull Call Spread slightly more expensive. In that case, the risk-to-reward ratio would be somewhat less favorable, though the trade-off is higher confirmation of the technical signal.

Trade Application

Entry trigger: Now, or confirmed breakout above 66.68 depending on trader style.

Target: ~70.63, aligning with the Triple Bottom projection and UFO resistance.

Stop-loss consideration: If prices fall back below the Triple Bottom lows, the breakout thesis would be invalidated.

Here, the options spread itself already caps the maximum loss at $1,750 per spread. Still, traders may choose to exit earlier if the chart setup fails, avoiding full risk.

The defined-risk nature of the spread helps enforce discipline, as the worst-case scenario is known from the outset.

Contract Specs & Margin Considerations

WTI Crude Oil contracts at CME come in two main forms:

Standard CL Contract: Represents 1,000 barrels of crude oil. A single point move = $1,000 P&L impact.

Micro CL Contract (MCL): Represents 100 barrels of crude oil. A single point move = $100 P&L impact.

Both contracts offer powerful ways to trade Crude Oil, and traders also have access to options on the Micro CL contract. This means the same Bull Call Spread structure can be applied with much smaller capital outlay. Instead of ~$1,750 risk per spread with the standard CL options, the risk would be about $175 per spread using MCL options.

The availability of Micro contracts and options provides traders with greater flexibility to tailor exposure to account size and risk tolerance, while still benefiting from the same strategic advantages.

Margin requirements vary depending on the broker and clearing firm, but options spreads like this one are far more capital-efficient compared to holding outright futures. The premium paid becomes the required margin ($1,750 or $175 in this case) as it defines the total risk, without margin calls tied to daily fluctuations.

Risk Management

The hallmark of this Bull Call Spread is defined risk. Unlike a naked long call, where premium decay can erode value quickly, the short 71 Call helps reduce the upfront cost and lowers time decay exposure.

Key considerations:

Position sizing: Limit risk per trade to a fraction of total trading capital.

Time decay management: If the move happens quickly, consider taking profits early instead of holding until expiration.

Adjustment potential: If CL approaches 70 quickly, traders may roll the short call higher to extend potential gains.

Risk management is not just about setting stops; it’s also about designing positions where the worst-case scenario is tolerable before the trade is entered. This Bull Call Spread embodies that principle.

Conclusion

The WTI Crude Oil market is at a pivotal point. With a Triple Bottom base, a breakout above 66.68 could carry prices toward the 70.63 region, where unfilled orders and technical projections converge.

A Bull Call Spread on the Nov-17 expiration offers a structured way to engage with this potential move. It balances opportunity with defined risk, aligning the technical chart setup with the capital efficiency of options on futures.

As always, this is an educational case study designed to highlight how options can be used to structure trades around market scenarios.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Options Blueprint Series: Perfecting the Butterfly SpreadIntroduction to the Butterfly Spread Strategy

A Butterfly Spread is an options strategy combining bull and bear spreads (calls or puts), with a fixed risk and capped profit potential. This strategy involves three strike prices, typically employed when little market movement is expected. It's an excellent fit for the highly liquid energy sector, particularly CL WTI Crude Oil Futures Options, where traders seek to capitalize on stability or minor price fluctuations.

Understanding CL WTI Crude Oil Futures Options

WTI (West Texas Intermediate) Crude Oil Futures are one of the world's most traded energy products. These futures are traded on the NYMEX and are highly regarded for their liquidity and transparency. The introduction of Micro WTI Crude Oil Futures has further democratized access to oil markets, allowing for more granular position management and lower capital requirements.

Key Contract Specifications for Crude Oil Futures:

Standard Crude Oil Futures (CL)

Contract Size: Each contract represents 1,000 barrels of crude oil.

Price Quotation: Dollars and cents per barrel.

Trading Hours: 24 hours a day, Sunday-Friday, with a 60-minute break each day.

Tick Size: $0.01 per barrel, equivalent to a $10.00 move per contract.

Product Code: CL

Micro Crude Oil Futures (MCL):

Contract Size: Each contract represents 100 barrels of crude oil, 1/10th the size of the standard contract.

Price Quotation: Dollars and cents per barrel.

Trading Hours: Mirrors the standard CL futures for seamless market access.

Tick Size: $0.01 per barrel, equivalent to a $1.00 move per contract.

Product Code: MCL

Options on Crude Oil Futures : Options on WTI Crude Oil Futures offer traders the ability to hedge price risk or speculate on the price movements. These options provide the flexibility of exercising into futures positions upon expiration.

Constructing a Butterfly Spread

The essence of a Butterfly Spread lies in its construction: It involves buying one in-the-money (ITM) option, selling two at-the-money (ATM) options, and buying one out-of-the-money (OTM) option. For CL WTI Crude Oil Futures Options, this could translate into buying an ITM call or put, selling two ATM calls or puts, and buying an OTM call or put, all with the same expiration date. The goal is to profit from the premium decay of the ATM options faster than the ITM and OTM options, especially as the futures price gravitates towards the middle strike price.

Using call options would typically generate positive delta making the strategy slightly bullish. Using put options would typically generate negative delta making the strategy slightly bearish.

Selection of Strike Prices: Identify suitable ITM, ATM, and OTM strike prices based on current crude oil futures prices and expected market movement. (The below chart example uses Support and Resistance UFO price levels to determine the optimal Strike Selection.)

Determine Expiration: Choose an expiration date that balances time decay with your market outlook.

Manage Premiums: The premiums paid and received for these options should result in a net debit, establishing your maximum risk.

Advantages and Risks

Advantages:

Defined Risk: The maximum potential loss is known at the trade's outset, limited to the net debit of establishing the spread.

Profit Potential: Profits are maximized if the futures price is at the middle strike at expiration.

Flexibility: Suitable for various market conditions, especially in a range-bound market.

Risks:

Limited Profit: The strategy caps the maximum profit, which is achieved under very specific conditions.

Commission Costs: Multiple legs mean higher transaction costs, which can erode profits.

Complexity: Requires careful planning and monitoring, making it less suitable for novice traders.

The construction of a Butterfly Spread in the context of CL WTI Crude Oil Futures Options highlights the strategic depth required to navigate the volatile energy market. Meanwhile, understanding its advantages and inherent risks equips traders with the knowledge to apply this strategy effectively, balancing the potential for profit against the complexity and costs involved.

Market Scenarios and Butterfly Spread Performance

The performance of a Butterfly Spread in CL WTI Crude Oil Futures Options is highly contingent on market stability and slight fluctuations. Given crude oil's propensity for volatility, identifying periods of consolidation or mild trend is crucial for this strategy's success.

Neutral Market Conditions: Ideal for a Butterfly Spread, where prices oscillate within a narrow range around the ATM strike price.

Volatility Impact: Sudden spikes or drops in crude oil prices can move the market away from the strategy's profitable zone, reducing its effectiveness.

Understanding these scenarios helps in planning entry and exit strategies, aligning them with expected market movements and historical price behavior within the crude oil market.

Executing the Strategy

Executing a Butterfly Spread involves precise timing and adherence to a pre-defined risk management plan. The entry point is critical, often timed with expected market stagnation or minor fluctuations.

Entry Criteria: Initiate the spread when volatility is expected to decrease, or ahead of market events predicted to have a muted impact.

Adjustments: If the market moves unfavorably, adjustments can be made, such as rolling out the spread to a further expiration or adjusting strike prices.

Exit Strategy: The ideal exit is at expiration, with the futures price at the ATM option's strike. However, taking early profits or cutting losses based on predefined criteria can optimize outcomes.

Case Study: Applying Butterfly Spread to Crude Oil Market

Let's explore a hypothetical scenario where a trader employs a Butterfly Spread in anticipation of a stable WTI Crude Oil market. The futures are trading at $80.63 per barrel. The trader expects the price to move down slowly due to mixed market signals even though key support and resistance (UFOs) price levels would indicate a potential fall.

As seen on the below screenshot, we are using the CME Group Options Calculator in order to generate fair value prices and Greeks for any options on futures contracts.

Underlying Asset: WTI Crude Oil Futures or Micro WTI Crude Oil Futures (Symbol: CL1! or MCL1!)

Strategy Setup:

Buy 1 ITM put option with a strike price of $82.5 (Cost: $3.00 per barrel)

Sell 2 ATM put options with a strike price of $78 (Credit: $0.92 per barrel each)

Buy 1 OTM put option with a strike price of $73.5 (Cost: $0.24 per barrel)

Net Debit: $1.40 per barrel ($3.00 - $0.92 - $0.92 + $0.24)

Maximum Profit: Achieved if crude oil prices are at $78 at expiration.

Maximum Risk: Limited to the net debit of $1.40 per barrel.

Over the following days/weeks, crude oil prices could fluctuate mildly due to competing factors in the market but ultimately close at $78 at the options' expiration. The trader's maximum profit scenario is realized, demonstrating the strategy's effectiveness in a stable market.

Risk Management Considerations

Executing a Butterfly Spread or any options strategy without a robust risk management plan is perilous.

The following considerations are essential for traders:

Use of Stop Loss Orders: To mitigate losses in unexpected market moves.

Hedging: Employing alternative positions to protect against adverse price movements.

Defined Risk Exposure: Always know the maximum potential loss before entering any trade.

Market Analysis: Continuous monitoring and analysis of the crude oil market for signs that may necessitate strategy adjustment.

Conclusion

The Butterfly Spread is a nuanced strategy that, when applied carefully, can offer traders of CL WTI Crude Oil Futures Options a means to capitalize on relatively slow market moves. While the potential for profit is capped, so is the risk, making it an attractive option for those with a precise market outlook. It exemplifies the strategic depth available to options traders, allowing for profit in less volatile market conditions.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

NNDM possible profit strategyBuy shares strategy -

Dip Buy NNDM at $2.98 yellow 8 EMA LINE

RISK 5% -> Stop Loss $2.91

TARGET 1 Reward: 10.4% Sell $3.29

TARGET 2 Reward: 13.4% Sell $3.38

________________________________________________________________________________________________________________

In order for NNDM to make a serious move north, bullish volume needs to kick in. Volume holds the weight of price up, it validates price. Here i am using several variables to justify a possible buy. This is a day chart. I am using the EXTENDED FIBONACCI RETRACEMENT to acquire my target lines.

What I Like -

*The candlestick formations; there is a push to break prior support/now resistance at $3.06. (yellow horizontal line) Notice how many times $3.06 was opened or touched in the past, going back to Jan 24, 2022, Feb 24, mar 8th, 14th 15th, and so forth...VERY IMPORTANT PRICE for NNDM. Now, with the 8ema and the red 34ema, the candles are using those as a springboard to push north. That's why bullish volume is so important to accomplish that.

*RSI is trending somewhat bullish; at a value of 57, the RSI, being a momentum indicator, suggests more room for running north

*8 EMA AND 34 EMA; The 8 ema has just crossed north over the 34 ema, suggesting that this stock price is ready to move bullish. Finding these crosses can be parabolic bullish moves!

What I Don't Like -

*Stochastic indicator is quite Overbought; While some investors suggest using the Stochastic as an overbought/oversold indicator, others suggest using it as a momentum indicator. The ideal stochastic indication would be both the RSI and Stochastic at the bottom of their respected graph moving upwards, suggesting an overall SENTIMENT that the bullish move is underway.

*VOLUME is not ideal; as stated above, we need more volume to come in

*Let's see what happens*

DISCLAIMER - I am not a professional trader. These are merely my thoughts and possible moves; i enjoy watching these stocks validate my process or slap me across the face lol. If you are in need of professional assistance with your trades, don't look here. I am not that guy.

OPENING: FORD OCTOBER/MAY 3/5 LONG CALL DIAGONAL... for a 1.73 debit/contract.

Metrics:

Max Loss: $173/contract

Max Profit/Return on Capital: $27/contract ; 15.6%

Break Even: 4.73/share

Notes: A small, defined risk engagement trade here in Ford. The metrics generally aren't what I'm looking for in one of these setups (25% ROC or greater), but I'm selling the front month shortie at-the-money, so that's to be expected.