TRADE IDEA/EXAMPLE: A 20/10 DELTA "DYNAMIC" IRON CONDORA creature of habit, I always sell the 20 delta when selling naked puts or setting up strangles/iron condors. Some traders like selling the 16's; some, the 30's; so I'm kind of "in between" ... .

Here, I show an example of a setup where I'm selling the 20 delta call (at whatever strike it lies), the 20 delta put (at whatever strike it lies), and buying the 10 delta put and call (at whatever strikes they lie). As compared to a "static" setup where you are making each wing the exact same width, here I'm letting the options' respective delta values dictate where my strikes, resulting in a skewed setup with the short call vert side of the setup being wider (4 strikes) than the short put side (3 strikes).

In actuality, this is a fairly good high IVR/IV setup, although I generally like to get at least 1/3rd the width of the wings in credit:

POP% 63%

Max Profit: $93/contract

Max Loss: $307/contract

BE's: 30.07/42.93

Notes: The "naked," undefined risk alternative is the body of this setup -- the Feb 31/42 short strangle with a max profit potential of $168/contract.

Dynamicironcondors

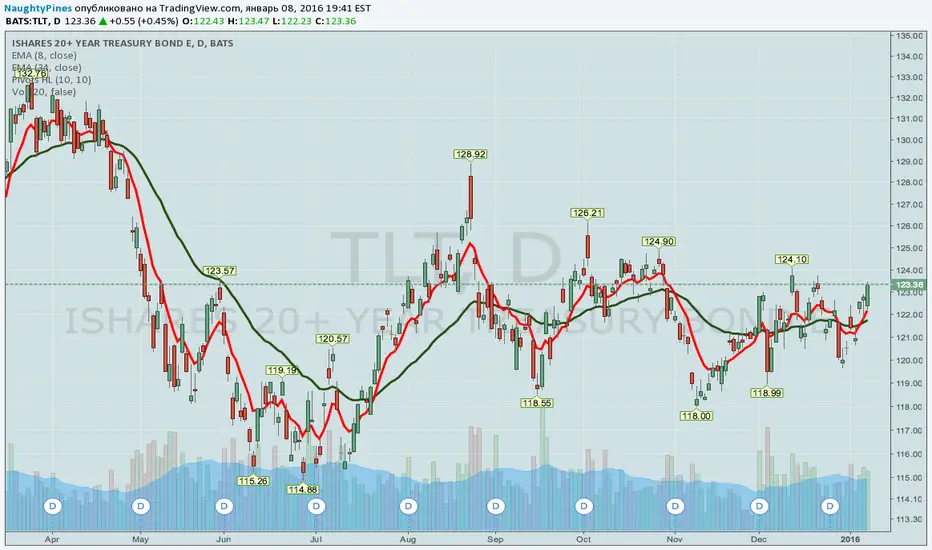

TLT LONG-DATED DYNAMIC IRON CONDORHaving gone somewhat "covered call" crazy last month and being somewhat ball and chained to those for the near future (most are Feb 19th expiry setups), I figured I'd turn my attention to old bread and butter standbys while I work through those particular trades, looking for setups that I can put on fairly cheaply from a buying power perspective. One of these is in TLT, which I haven't worked in a while. Because near term expirations have little volatility (current implied volatility rank is 4), I figured what I would do is go out further in time for my setup, as I did with my SPY setups when there was no volatility in near-term months in that instrument and manage the setup dynamically over time, rolling the call/put sides toward current price as time passed and the short option decayed and/or price moved.

Here's the basic setup:

April 15th 108/111/136/139 iron condor

Probability of Profit: 83%

Max Profit: $36

Buying Power Effect: ~$285

Break Evens: 110.64/136.36

Notes: As with the SPY dynamic iron condor, the notion is to roll the call or put side toward current price when it is profitable to do so to capture additional credit during the life of the setup while at the same time paying close attention to the 1 standard deviation line (basically the 84% out of the money/16% in the money line) for the expiry. The easiest thing to do in the vast majority of cases is to watch the short options price and if it is approaching worthless, check to see whether you can roll the side toward current price while staying clear of the 1 standard deviation line in light of the time remaining ... . My general rule of thumb is don't bother rolling unless you can get at least a .25 credit for doing so.

DYNAMIC IRON CONDOR MANAGEMENTSeveral days ago (before we had this downmove/volatility pop), I set up a long-term SPY iron condor, my intent being to manage it "dynamically" over time, rolling my options intratrade as price moved either toward my short put wing or toward my short call wing.

The original setup was a March 18th 166/169/219/222 SPY iron condor, for which I originally received a fairly paltry .71 in credit. In my earlier post, I discussed various options for managing the setup intratrade: (1) rolling the wings as a unit toward current price; (2) leaving the long options alone and moving only the short options toward current price; and (3) moving both the long options away from current price and the short options toward current price. I pointed out the pluses and minuses of each of these methodologies, with the preference being toward moving the wings as a unit toward current price.

In the interest of experimentation (and also to capture greater credit than that offered by merely rolling the call side wing down three strikes), I'm going to opt to roll the short call toward current price and the long put away from current price at the same time and by the same number of strikes to capture credit generated by this down move (i.e., I am going to roll the 219 short call to the 216 and the 166 long put to 163 and will look to get a fill for an additional .77 credit/contract to do this). I chose the 216 short call strike, since that is currently at the edge of the current expected move for SPY for the March 18th expiration.

Should I get filled, the new iron condor will be a Mar 18 SPY 163/169/216/222 iron condor, so I will be widening the wings to six strikes wide by rolling the short call/long put in this manner. The upside is that I received .77 in credit for the intratrade roll (on top of the .71 I originally received); the downside is that widening the spreads requires some additional margin and could potentially give me a headache if I need to roll one of those 6-wides out for duration on the back end of the trade. Consequently, I naturally want to exercise caution going forward as to how many times I roll intratrade, keeping an eye on the width of the wings, the overall margin used, and whether I am getting too aggressive by bringing in the wings too tightly to current price.

LONG TERM BREAD AND BUTTER -- "DYNAMIC" IRON CONDORSI have frequently described my days 'til expiry (DTE) "sweet spot" as 45 days with nonearnings plays and the same Friday of an earnings announcement or the Friday thereafter as the DTE for earnings plays.

Every so often, however, I like to look farther out in time, particularly where a nearer time setup doesn't provide what I'm looking for, which is usually at least a 1.00 credit/contract in the vast majority of setups. (In low volatility environments, I'm simply not a fan of calendars, debit spreads, diagonals and the like. I prefer to just dry powder out, wait for the next volatility wave, and enjoy the free time that these lulls in volatility provide).

Here's one setup (100 DTE+) that I look to put on as a background trade in SPY, IWM, QQQ, or DIA when volatility isn't that great in the market as a whole, the notion being that -- at least in broad market instruments like SPY -- volatility is a bit more "regular" or "average" farther out than nearer in time:

SPY 166/169/219/222 Iron Condor

POP%: 69%

Max Profit: $69/contract

BPE: ~$231/contract

BE's: 168.31/219.69

On the face of it, that isn't a very enticing setup -- $69 is the max, per contract profit and your theta decay's about .66 a day. But this isn't one of those setups that you just get filled and walk away from. Rather, you manage it intratrade, balancing delta when it's reasonably profitable to do so, rolling the put/call wings toward current price as time elapses and/or there is a pop in volatility such that premium becomes richer.

For example, I think it's a fairly high probability that we're not going to see 169 in SPY by March, so as time goes by and things become more certain, the 169/166 short put vertical side of the setup will decrease substantially in value (that's what you want as a premium seller) such that you can roll it up to higher strikes for an additional credit (ka-ching).

I do know traders who do these on a regular basis, but do one of two variations on intratrade management/delta balancing: (1) Do not roll the wings as a unit. Instead, roll the long options away from price if price moves toward them and the short options toward price if price moves away from them or (2) Don't touch the long options, only the short ones. In other words, roll the short call/put toward price when delta balancing, but leave the long options in place throughout the trade.

Personally, I don't like these particular variations, since you invariably end up with wings of oddball width which could cause problems in the event you have to roll. Moreover, when you widen the width between the short and long options in a spread, greater margin is required.

Even with my setup, however, there are drawbacks. If you enter a premium selling play during a period of low volatility and volatility increases, the premium in the options becomes richer and your setup can consequently go "under water"/in the red until volatility decreases. However, I generally deal with such volatility increases by rolling toward current price to take advantage of the richer premium intratrade -- that is, if I can do so profitably; it's not always possible, so sometimes you just have to wait until volatility recedes.

Another reason why you should always go small on any setup ... .