Can Vertical Integration Ground a Flying Dream?Joby Aviation faces a critical convergence of structural vulnerabilities that threaten its ambitious air taxi vision. The company pursues an all-in vertical integration strategy, controlling everything from manufacturing to operations, which demands extraordinary capital expenditure. With quarterly losses exceeding $324 million and cash reserves depleting rapidly, Joby must continually raise equity financing, perpetually diluting shareholders. This high-burn model collides with a punishing macroeconomic environment where elevated interest rates dramatically increase the cost of capital for pre-revenue ventures, multiplying financial pressure at precisely the wrong moment.

Regulatory friction compounds these economic headwinds. The FAA has requested additional safety documentation, pushing U.S. commercial deployment potentially beyond 2027 and severely undermining financial projections. While Joby has achieved technical milestones like preparing for Type Inspection Authorization flight testing, the market correctly recognizes that hardware readiness cannot overcome bureaucratic inertia. The company's $125 million Blade acquisition, intended to fast-track market entry, now sits idle as an expensive, non-performing asset awaiting regulatory clearance. Meanwhile, Joby faces over $100 million in potential liabilities from Aerosonic's trade secret lawsuit regarding critical air data probes, with the court already denying Joby's motion to dismiss.

The confluence of these challenges creates a severe risk-adjusted valuation problem. Analysts project an average 30% downside from current trading levels, with bearish targets suggesting potential declines exceeding 65%. Joby's international pivot to Dubai and Japan represents a geopolitical hedge against FAA delays but introduces regulatory complexity by reversing the preferred certification sequence. The company's acquisitions of autonomous flight technology (Xwing) and hybrid power systems (H2Fly) may diffuse engineering focus away from core certification objectives. With profitability unlikely before 2027-2028 and existential threats spanning legal, regulatory, and financial domains, the market is rationally discounting Joby's prospects despite its technical achievements.

Evtol

Archer (ACHR) Bullish Pennant Breakout?I love this chart setup so wanted to share. It has a little bit of everything from market structure, fib levels, pattern recognition, falling wedges.. a bullish backdrop for tech, speculative plays, and the air transportation sector in particular.

Archer's top competitor is $JOBY. They have been performing amazing as of late, experiencing all time highs, even. During the last few months though I have watched NYSE:ACHR closely looking for an opportunity to diversify and buy up some real estate. Now is looking like a decent time to start accumulating for a swing trade in my humble opinion.

Reversal At New ATH Points To Next Potential Takeoff For JOBYNYSE:JOBY has been making impressive steps lately with reports coming out Friday, August 15th that the company has achieved a great milestone in being the first to fly a piloted electric vertical takeoff and landing air taxi or eVTOL from one public airport being Marina (OAR) to Monterey (MRY).

www.tradingview.com

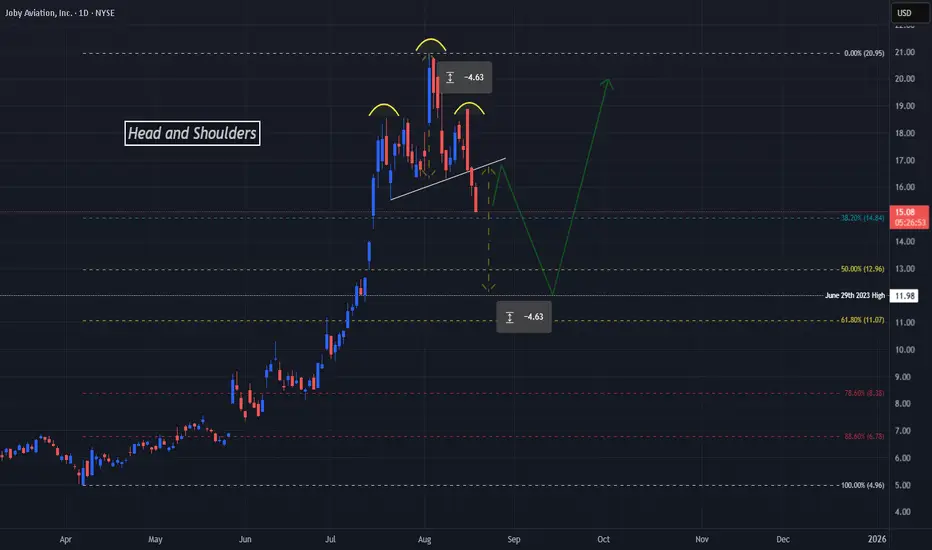

To end last week and start this week we see price on NYSE:JOBY plummeting and this decline has confirmed a very strong reversal pattern, the Head and Shoulders!

Now, Price has made a solid breakout of the Neckline or Support of the Pattern so we can suspect a potential pullback to the Neckline for a Retest before moving down further in the coming days.

Based off the Potential Extension of a Confirmed Breakout and Validated Retest of a Head and Shoulders Pattern, we can suspect that Price will fall the same length as from the Head to the Neckline, being approx. $4.63, which would land Price not only right in the middle of the Fibonacci Golden Ratio Zone but also a Previous High from June of 2023 @ $11.98! --> This will be the next Buy Opportunity!

With NYSE:JOBY expanding by purchasing Blade Air Mobility who operated in lounges and terminals in the US and Europe and plans to deploy commercially in 2026, this could be a great stock to stock up on!

www.tradingview.com

ACHR – 50 SMA Bounce with Sympathy Momentum from JOBYNYSE:ACHR – 50 SMA Pullback + Options Play Into Support

Archer Aviation ( NYSE:ACHR ) is showing signs of life right at the 50 SMA, and with competitor NYSE:JOBY ripping to new highs today on news, this could be the sympathy setup traders are looking for.

🔹 Technical Setup

After a strong run, NYSE:ACHR has pulled back in an orderly fashion, now resting on the 50-day moving average — a key support zone.

The stock is sitting on clean support, showing signs of stabilization.

🔹 Sector Tailwind from NYSE:JOBY

NYSE:JOBY is breaking out today on headlines — and NYSE:ACHR often moves in sympathy.

If momentum spills over, this could be the launchpad for NYSE:ACHR to retest prior highs.

🔹 My Trade Plan:

1️⃣ Position: Buying the August 1st $11 calls around the $0.90 area.

2️⃣ Reasoning: Strong reward-to-risk if NYSE:ACHR bounces from here.

3️⃣ Trigger: Watching for a reclaim of the short-term EMAs and increased volume as confirmation.

Why I Like This Setup:

50 SMA bounce + sympathy play = great combo.

Options are cheap, offering leverage without heavy risk.

If this breaks out again, it could move fast — this name has range.

Archer Aviation: Fact or Fiction in the Skies?Archer Aviation, a prominent player in the burgeoning electric vertical takeoff and landing (eVTOL) industry, recently experienced a significant stock surge, followed by a sharp decline. This volatility was triggered by a report from short-seller Culper Research, which accused Archer of "massive fraud" and systematically misleading investors on key development and testing milestones for its Midnight eVTOL aircraft. Culper's allegations included misrepresentations of assembly timelines, readiness for pilot-controlled flights, and the legitimacy of a "transition flight" to unlock funding. The report also criticized Archer's promotional spending and claimed stalled progress on FAA certification, challenging the company's aggressive commercialization timeline.

Archer Aviation swiftly and forcefully refuted these claims, labeling them "baseless" and questioning Culper Research's credibility, citing its founder's "shorting and distorting" reputation. Archer emphasized its strong first-quarter 2025 earnings, which saw a dramatic narrowing of net losses and a substantial increase in cash reserves to over $1 billion. The company highlighted its operational momentum, including strategic partnerships with Palantir for AI development and Anduril for defense applications, a $142 million U.S. Air Force contract, and significant early customer orders exceeding $6 billion. Archer also pointed to its progress on FAA operational certifications, having secured three of four essential licenses, and its preparation for "for credit" flight testing for Type Certification, a critical step towards commercial passenger operations.

Culper Research's past track record presents a mixed picture, with previous targets like Soundhound AI experiencing initial stock declines followed by strong financial rebounds, though some legal challenges persisted. This nuanced history suggests that while Culper's reports can cause immediate market disruption, they do not consistently predict long-term corporate failure or fully validate the most severe allegations. The eVTOL industry itself faces immense challenges, including stringent regulatory hurdles, high capital requirements, and the need for extensive infrastructure development.

For investors, Archer Aviation remains a high-risk, long-duration investment. The conflicting narratives necessitate a cautious approach, focusing on verifiable milestones such as FAA Type Certification progress, cash burn rate, successful commercialization execution, and Archer's comprehensive response to the allegations. While the "fraud" thesis might be "overblown" given Archer's verifiable progress and strong financial position, ongoing due diligence is crucial. The company's long-term success hinges on its ability to navigate these complexities and meticulously execute its ambitious commercialization plan.

$ACHR ARCHER AVIATION SCORES 300M BOOST BLACKROCK JOINS THE RIDEARCHER AVIATION SCORES $300M BOOST—BLACKROCK JOINS THE RIDE

1/7

🚀 $300M just landed in Archer Aviation’s pocket! Major institutional investors like BlackRock are backing Archer’s quest to dominate the eVTOL game. Ready to see why this funding is a big deal? Let’s go! ⚡️✈️

2/7 – WHAT’S ARCHER BUILDING?

Midnight Aircraft: Designed for short urban flights (~20 miles) with rapid turnarounds.

Targets commercial operations by 2025, battling congestion & pollution. 🌆

Hybrid Approach: Electric + other propulsion to boost range and expedite FAA certification.

3/7 – BLACKROCK’S INVOLVEMENT

Big Vote of Confidence: World’s largest asset manager sees serious potential. 💪

Aligns with green investing—eVTOLs can slash emissions compared to helicopters. ♻️

Could draw more partnerships and capital to Archer’s runway.

4/7 – WHY COMPOSITES & BATTERIES MATTER

Composites: Lighter & stronger materials = extended range & higher efficiency. 🏋️♀️

Batteries: High-energy density is critical for flight duration & payload. 🔋⚡️

Archer’s push here signals they’re tackling the industry’s biggest hurdles head-on.

5/7 – FINANCIAL & STRATEGIC IMPACT

Stronger Balance Sheet: $300M for R&D, testing, manufacturing. 💼

Timing is key: Archer eyes FAA approval soon—this cash could speed up that process. ⏱️

Competing with Joby, Vertical Aerospace, Lilium—the race is on! 🏁

6/7 Are eVTOLs the future of urban travel?

1️⃣ Absolutely—Game-changer for city traffic! 🏙️

2️⃣ Maybe—Need more proof and better tech. 🤔

3️⃣ Nope—I’m still skeptical about costs & safety. ❌

Vote below! 🗳️👇

7/7 – INDUSTRY CONTEXT

Market could hit $1.5T by 2040 (Morgan Stanley). 💰

Key markets: US, UAE, Japan, India—Archer is eyeing them all. 🌏

eVTOLs promise faster, greener commutes, but hurdles remain: regulations, infrastructure, battery tech.

Strengths: Archer’s recent $300 million funding, strategic partnerships, and regulatory progress position it well to compete in the eVTOL market. Its focus on composites and batteries aligns with industry needs.

Weaknesses: High R&D costs, limited manufacturing capacity, and lack of commercial revenue highlight financial and operational challenges.

Opportunities: The growing eVTOL market, international expansion, and defense applications offer significant growth potential.

LILIUM LILM Bullish ideaThis stock is awakening.

After long bear market for this stock, there is apparently an accumulation zone created.

The volatility is getting lower and lower.

To me it looks like the bulls are getting back.

Idea with target on the charts.

NFA,

GL

PONO CAPITAL, the worst performing SPAC in the history of SPACs?Can Aerwins be saved? SO FAR I HAVE BEEN ABSOLUTELY WRONG.

PONO CAPITAL, the worst performing SPAC in the history of SPACs?

Check the chart #AWIN #AWINW

Can the company that did flying hoverbikes and unmanned vehicles live again? Fly again? Or?

OR?

Aerwins - A study of a SPAC - As of the latest data, the stock was trading at around $0.0953, which marks a minor increase of $0.0003 (+0.32%) from its previous close. This level of activity reflects the ongoing fluctuations in the stock's value, which has seen a broad range over the past 52 weeks from as low as $0.076 to as high as $2.92. Based on the latest information available for Aerwins Technologies Inc. (ticker: AWIN)

Financially, Aerwins Technologies has been navigating through challenges, as indicated by its performance metrics and stock trends. The company's market capitalization stands at approximately $5.974 million, with a significant range in its daily trading volume and price points over the past year.

Do your research and due diligence.

AerwinsAt the time of this writing, as of December 26, 2023, Aerwin Technologies Inc.'s stocks and warrants, AWIN and AWINW respectively, exhibit significant trading activity, which is crucial given the looming deadline for compliance and the risk of delisting.

Aerwin's Stock (AWIN): The stock price hit $0.1669, a 38.97% increase from its previous close of $0.1201. The day's range was $0.1420 to $0.2180, with an exceptionally high trading volume of 69,669,435 shares, far exceeding the average volume of 4,996,940 shares.

Aerwin's Warrant (AWINW): The warrant experienced a 30% increase in its price, reaching $0.0130. It opened at $0.0200, with a bid of $0.0090 x 900 and an ask of $0.0100 x 800. The day's range was between $0.0074 and $0.0200, and it recorded a volume of 98,292, though the average volume is not available

The recent surge in both the stock and warrant trading volumes is particularly significant against the backdrop of the company's delisting notice received on June 8 from Nasdaq Aerwins Technologies Says On June 8, Got Notice Of Delisting Or Failure To Satisfy Continued Listing Rule Or Standard From Nasdaq. This increase in trading activity could be a critical factor in determining whether Aerwin can meet Nasdaq's compliance requirements.

However, the company's communication strategy, or lack thereof, adds to the uncertainty. While there was a notable announcement on December 22 about entering into a Letter of Intent with a helicopter technology company. Aerwins Technologies Inc. Enters into Letter of Intent with Helicopter Technology Company, there has been no substantial follow-up or detailed information regarding the company's strategies to address the potential delisting and compliance issues.

In summary, Aerwin Technologies Inc. is at a crucial juncture with its stocks and warrants showing significant trading activity. This activity is crucial for the company's efforts to maintain compliance with market regulations, particularly in light of the potential delisting risk and the absence of detailed communications from the company.