CHYM: From IPO Laggard to 2026 Leadership?Chime Financial is currently at a critical technical and fundamental inflection point, moving from a high-growth "disruptor" to a potentially profitable "mainstream" financial partner for millions of Americans. A

fter raising its 2025 revenue guidance to a range of $2.16B to $2.17B, the company has demonstrated resilient 29% year-over-year growth fuelled by its expanding Chime Card credit product and high "attach" rates among its 9.1 million active members.

The bullish narrative is further bolstered by a $200 million share repurchase program and a proprietary processing platform, ChimeCore, which has helped expand adjusted EBITDA margins to 5% as of late 2025.

Technically, as the stock clears its 200-day moving average of $25.23, it is breaking out of a textbook consolidation "Handle". With top-tier analysts like Goldman Sachs and B. Riley recently raising price targets to $30 and $35 respectively, the "Dragon's Tail" for this setup appears aimed at a return to the $40–$45 zone, representing the stock's post-IPO high-water mark.

Fintech

USD/ZAR: The Rand’s Strategic Pivot in 2026The South African rand recently surged to 16.33 against the US dollar. This move signals a significant shift in emerging market sentiment. Investors now pivot away from safe-haven assets. They embrace the rand as a primary recovery play for 2026.

Macroeconomic Anchors and Monetary Easing

The South African Reserve Bank (SARB) recently implemented a 3% inflation target . This bold framework provides a new anchor for price stability. Analysts expect this move to foster long-term fiscal credibility. Lower inflation expectations allow the SARB to maintain an accommodative stance.

Parallel to this, US Federal Reserve officials signaled dovish leanings. Markets now price in multiple rate cuts for the 2026 cycle. This interest rate differential heavily favors the rand. Yield-seeking investors find South African government bonds increasingly attractive.

Geopolitics and the G20 Transition

South Africa recently handed the G20 presidency to the United States. This transition marks a critical geostrategy juncture for Pretoria. Diplomatic relations with the Trump administration remain a key variable for trade. Exporters closely watch potential adjustments to the AGOA agreement .

Strategic autonomy remains a priority for South African leadership. The nation continues to balance relations with the BRICS+ bloc and Western partners. This "non-aligned" approach secures diverse investment flows. It also hedges against global supply chain disruptions.

High-Tech Innovation and Patent Trends

The local high-tech sector is evolving from experimentation to execution. "Agentic AI" now drives efficiency in deep-level mining operations. South Africa is filing record patents in AI-driven mineral processing and green hydrogen. These innovations attract significant venture capital from global tech hubs.

The country is also becoming a critical hub for data annotation. Local startups provide high-quality training data for global LLMs. This creates a new "silicon-based" workforce. It leverages the country's demographic dividend to power the global AI revolution.

Industry Trends: Energy and Logistics

Energy reliability has improved significantly following aggressive private-sector participation. Businesses no longer fear the debilitating effects of "loadshedding." Enhanced logistics infrastructure at major ports facilitates smoother trade flows. These reforms reduce the cost of doing business across the SADC region.

Cybersecurity has become a non-negotiable component of business continuity. Companies are adopting zero-trust architectures to combat rising regional cyber threats. This investment in digital resilience bolsters investor confidence in the local financial ecosystem.

Management, Culture, and the New Business Model

Management styles are shifting toward AI-native operating models . Leaders now orchestrate teams where humans and AI agents collaborate seamlessly. This cultural transformation prioritizes agility over traditional hierarchy. It allows South African firms to compete globally on efficiency and innovation.

Hybrid work remains the standard for the urban middle belt. This model reduces overhead costs and improves employee retention. Companies that embrace this flexibility report higher productivity and better mental health outcomes. This shift redefined the corporate landscape in Johannesburg and Cape Town.

Robinhood (HOOD) – Consolidation After Strong Run🔍 Fundamental Highlights:

Cathie Wood’s ARK Invest recently bought 124,427 shares of Robinhood NASDAQ:HOOD , valued at approx. $15.4M, reinforcing her bullish stance despite recent market volatility. This move aligns with ARK's broader rotation into crypto-adjacent and disruptive finance plays — including names like Coinbase, BitMine, and Circle. This kind of conviction buying often precedes major inflection points.

📉 Technical Setup:

After a strong rally, HOOD is now consolidating. Price action is tightening, volume is cooling, and a pullback into the $95–$98 zone offers a compelling risk-reward opportunity. This range has previously acted as demand, and a bounce here could trigger the next leg higher.

📌 Trade Plan (Illustrative Only):

Entry Zone: $95 – $98

Take Profit Targets: $117, then $153

Stop Loss: $85 (invalidates support zone)

Adyen 1W: The trend broke twice, the market is just catching upOn the weekly chart, Adyen has broken the long term downtrend twice, and price is now performing a controlled pullback retest. The current consolidation holds above the $15.5–16.0 demand zone, where MA100, 0.786 Fibonacci and strong volume profile support align. Selling pressure is fading, volumes on the pullback are declining, and bullish divergence remains intact. This structure favors confirmation of the breakout rather than a return to a bearish trend. As long as price stays above this zone, upside remains the priority. First target stands at $19.94, followed by $23.23.

Fundamentally, Adyen continues to deliver consistent growth. H1 2025 revenue reached $1.28B, up from $1.13B in H2 2024. H2 2025 revenue is projected at $1.49B, with forecasts extending toward $1.53–1.88B in 2026–2027. EPS came in at $0.18 for H1 2025, with $0.21 expected in H2, rising toward $0.25–0.26 by 2027. Analyst sentiment leans bullish as digital payment volumes continue to expand globally.

When a trend breaks twice, patience usually gets paid.

The Big Short’s Longest Bet: Can Freddie Mac Break Free?Michael Burry, the legendary bear of 2008, has flipped the script. The man who famously shorted the housing market now bets on its bedrock: Freddie Mac (FMCC). Shares rallied 10% Tuesday after Burry revealed a "personal" stake in the government-sponsored enterprise (GSE). He argues the mortgage giant stands on the precipice of a historic transformation. Yet, he warns of a "steep, windy, and rocky climb" ahead. Is this the ultimate contrarian play, or a value trap waiting to snap?

Geopolitics & Macroeconomics: The Housing Anchor

The global financial system rests heavily on the stability of US housing. Freddie Mac does not just fund American homes; it securitizes debt that underpins global bond markets. A successful privatization would send a powerful signal of US financial resilience to foreign creditors. Conversely, continued conservatorship limits US economic agility. The Trump administration’s push for privatization aims to unleash capital, reducing the government's balance sheet exposure while revitalizing the secondary mortgage market.

Business Models: The IPO Pivot

Freddie Mac’s business model is shifting from government ward to private competitor. For 17 years, it surrendered profits to the Treasury. Burry predicts a re-listing could unlock immense value, potentially pricing shares at 1.5 to 2 times book value. The core strategy involves shedding the "net worth sweep" shackles to rebuild capital. This transition requires a fundamental restructuring of how the enterprise prices risk and retains earnings, moving from a utility-like mandate to a growth-oriented equity story.

Technology & Cyber: AI in the Engine Room

Behind the ticker, Freddie Mac is quietly becoming a fintech juggernaut. The company now deploys advanced Artificial Intelligence (AI) and Machine Learning (ML) to modernize credit risk modeling. Innovations like "Automated Collateral Evaluation" (ACE) reduce the need for physical appraisals, streamlining the loan cycle. Furthermore, their deployment of "Early Warning Indicator" (EWI) models uses Natural Language Processing to predict operational bottlenecks. This tech-forward approach reduces defect rates and fortifies their cyber-defense posture against data breaches.

Science & High-Tech: Algorithmic Rigor

The science of risk is evolving. Traditional linear regression models often fail when economic conditions shift abruptly. Freddie Mac’s data scientists are exploring "Hamiltonian-constrained" neural networks to maintain ranking stability in volatile markets. By integrating physics-based optimization into financial modeling, they aim to solve the "concept drift" problem where models degrade over time. This high-tech rigorousness ensures that their multi-trillion-dollar portfolio remains robust against unforeseen economic shocks.

Management & Leadership: Steering Through the Storm

Leadership at Freddie Mac focuses on operational leanness. The management culture has pivoted from crisis survival to efficiency and digital transformation. They prioritize "mission-driven" business while preparing for the scrutiny of public markets. Burry suggests that even Warren Buffett could endorse this leadership by acquiring a stake. This vote of confidence would validate the management’s strategy of balancing affordable housing mandates with shareholder returns.

Conclusion: The Verdict

Freddie Mac is no longer just a distressed asset; it is a technology-empowered financial fortress awaiting liberation. Michael Burry’s entry signals that the risk-reward ratio has finally tipped. While the path to an IPO remains fraught with political hurdles, the fundamental drivers—innovation, leadership, and market necessity—are aligning. Investors willing to endure the volatility may find themselves holding the keys to the next decade’s most significant financial turnaround.

FINX - FinTech back on the cards?This fund is making up some previously lost ground...is it ready to seek new all-time highs?

About FINX:

This ETF is focused on companies with significant exposure to mobile payments, market-place lending, crowd-funding, enterprise solutions, blockchain & alternative currencies, personal finance software and automated wealth-management services.

Is this sector set to deliver results beyond expectations over the coming year? The market seems to be anticipating so, but time will tell...

Our current reading sees current momentum rated as 'Bullish', however note the following point as a point of potential interest & volatility NASDAQ:FINX

If price can hold above $27.00 ... Significant Bullish potential may be unlocked.

If however price falls below $27.00 ... Significant Bearish risk may come into play.

We're inspired to bring you the latest developments across worldwide markets, helping you look in the right place, at the right time.

Stay tuned for further updates, and we look forward to being of service along your trading & investing journey...

Disclaimer: Please note all information contained within this post and all other Bullfinder-official Tradingview content is strictly for informational purposes only and is not intended to be investment advice. Please DYOR & Consult your licensed financial advisors before acting on any information contained within this post, or any other Bullfinder-official TV content.

Is South Korea Financing Its Own Currency Collapse?The South Korean Won (KRW) is unraveling. Trading at 1,465.5 against the US Dollar (USD), the currency has shed over 7% of its value in the second half of 2025. While Finance Minister Koo Yun-cheol publicly vowed stability this Wednesday, his "bland" delivery and lack of concrete policy measures sent a chilling signal to global investors: Seoul is out of ammunition. The forces driving the USD/KRW pair higher are no longer just macroeconomic—they are structural, geopolitical, and deeply rooted in the technology sector.

Macroeconomics & Policy: The "Bland" Defense

Minister Koo’s refusal to implement tax benefits for repatriating exporter earnings exposes a critical policy gap. Koo admitted that the market reacts hypersensitively to global uncertainty, yet his proposed solution—a consultative body with the National Pension Service (NPS)—lacks immediate bite. The NPS, the world's third-largest pension fund, is ostensibly a stabilizing force. However, its mandate to maximize returns drives it to aggressively accumulate dollar-denominated assets, exacerbating the very weakness the government seeks to curb. The Bank of Korea’s expected decision to hold interest rates on Thursday further cements the paralysis, trapped between a volatile currency and an overheating housing market.

Geopolitics & Geostrategy: The Cost of Alliances

The Won’s depreciation is the collateral damage of South Korea’s geostrategic pivot. A looming trade deal with the United States includes a massive investment package requiring Korean conglomerates to deploy capital into American soil. This structural capital outflow creates persistent demand for dollars that no short-term intervention can offset. Simultaneously, regional tensions with North Korea and trade disputes involving China have eroded the Won’s status as a stable proxy for Asian growth. Investors are pricing in the risk of South Korea becoming an economic frontline state.

Industry Trends & Business Models: The Export Paradox

South Korean industry is decoupling its success from its currency. The traditional model—weak currency boosts exports—is failing. While orders for transport equipment and machinery have risen, the value is captured in rising manufacturing costs driven by tariffs on imported raw materials. Major conglomerates (Chaebols) are shifting from "Made in Korea" to "Made by Korea in the USA." This business model evolution means record corporate profits no longer translate into domestic currency demand, as earnings are increasingly retained offshore to fund global operations.

Technology & Science: The Innovation Deficit

Despite South Korea’s reputation as a high-tech powerhouse, the underlying mechanics of its innovation sector hurt the currency.

High-Tech Arbitrage: Korean firms are aggressively acquiring US-based AI and biotech startups to bypass domestic regulatory hurdles. This M&A activity requires selling Won to buy Dollars.

Science & R&D: While domestic R&D spending is high, the commercialization of breakthrough science increasingly relies on global supply chains priced in USD.

Patent Analysis & Cyber Landscape

A deep dive into 2025 patent filings reveals a disturbing trend for the Won. While the volume of patents filed by Korean entities remains high, the citation impact—a proxy for value—is highest in software and cybersecurity technologies dominated by US firms.

Intellectual Property: Korean tech giants are paying record licensing fees for American foundational AI models and cybersecurity protocols.

Cyber Defense: Escalating state-sponsored cyber threats have forced Korean financial institutions to upgrade infrastructure using imported, dollar-priced security solutions, further draining foreign reserves.

Management, Leadership & Company Culture

A cultural shift in corporate leadership is accelerating capital flight. A new generation of Chaebol management prioritizes global diversification over national loyalty. Unlike their predecessors, who repatriated earnings to build domestic empires, today’s leaders view the US market as the safest harbor for capital. This "herd-like behavior," which Minister Koo criticized, is a rational response to perceived domestic stagnation. Even retail investors are abandoning local equities for US tech stocks, signaling a total loss of confidence in the domestic market's growth potential.

Conclusion: No Floor in Sight

The USD/KRW increase is not a temporary fluctuation; it is a structural repricing of South Korea's economic future. Without a radical shift in policy that incentivizes capital repatriation or a sudden geopolitical thaw, the path of least resistance is higher. Traders should ignore the rhetoric from Sejong City and focus on the flows: money is leaving the peninsula, and it isn't coming back soon.

Buy the bottom of the PayPal uptrendNASDAQ:PYPL is known to be a high value stock with a depressing valuation.

Investors are under optimistic due to the struggling performance the past several years after a dizzying rally during the pandemic.

Recently the stock rallied on earnings due to a deal with Open-AI. Shares quickly gave the spike back and headed lower along with a broader tech pullback on AI bubble fears.

NASDAQ:PYPL has now undercut a long term upward trend line. Judging by the past few times this has happened, it could be a fantastic setup. It looks like the downtrend was broken in late 2024 when the price bottomed on an RSI divergence. The shares seem to be coiling up for a big move, and have been for almost a year now.

Block (XYZ): Weak Earnings, Bitcoin Exposure, and the Next Move📊 Fundamental Overview

I entered Block (XYZ) about a year ago when the company’s cash flow trends were very strong.

However, right now the picture is becoming more concerning.

EPS growth is not stable.

Previously, EPS was growing rapidly (65%, 38%, 155%), but the last two quarters showed only –10% and +13% growth.

Revenue growth stagnated.

Year-over-year revenue used to grow strongly —

2019: $4M → 2020: $9M → 2021: $17M → 2023: $21M → 2024: $24M — but is now roughly flat (~+1% YoY).

Forward P/E: ~22.7 — not particularly attractive considering the company’s decelerating fundamentals.

Share dilution stopped.

Since 2022, Block has halted share issuance, and total shares outstanding remain stable within ±2%, which is a positive signal compared to other fintech peers.

💥 Q3 Earnings Miss

In the latest earnings report:

Expected EPS: $0.63 → Actual: $0.54

Revenue: $6.11 B (below expectations)

The miss triggered a 15–18% drop after earnings, followed by a partial rebound as dip buyers stepped in.

But fundamentally, the company is clearly losing growth momentum.

₿ Bitcoin Exposure Risk

Block currently holds about 8,700 BTC (~$1 billion) on its balance sheet.

While this gives long-term upside potential, it also adds massive volatility risk.

If Bitcoin enters a –70% correction (which I expect in the next 3–4 months), that could hit Block’s balance sheet hard and accelerate the drawdown.

📈 Technical Structure

Technically, the stock has already corrected about –86% from its all-time high.

We’re currently sitting inside a major accumulation cluster between $50–80 — a very strong volume node.

If this cluster breaks down, the next major support zone is $8–15, which would imply a potential –90%+ drawdown, typically a “pre-bankruptcy” level of decline.

After the latest earnings report, XYZ dropped by nearly 18%, forming a noticeable gap down. However, the volume on this sell-off was relatively low compared to the massive volume spikes seen in July 2025.

Typically, such sharp post-earnings drops come with high capitulation volume, signaling panic selling and potential bottom formation, but this time, that confirmation is missing.

This raises the risk that the current decline might not yet be over, and that smart money may still be waiting lower, around the next demand zone.

From a wave-structure perspective, it looks like wave 1 is complete, followed by a sharp corrective move that has already exceeded the typical 38–62% retracement range, falling by about 86%, an unusually deep correction, but not impossible within a prolonged cycle.

The ongoing consolidation phase has lasted significantly longer than previous ones, which increases the probability of a final downward push, forming a classic zigzag pattern (A–B–C), a drop, consolidation, and one more leg down to complete seller capitulation.

Volume patterns in such structures usually peak in the middle of the formation, aligning with current price behavior.

Technically, both outcomes remain open,

we could see a short-term bounce from this zone or a double zigzag (dZ) structure unfolding lower before the true bottom forms.

Upside momentum currently lacks fuel, fundamentals don’t support a strong rally yet.

If price breaks above $100, the next upside target sits around $280, offering roughly 4× potential from current levels.

So the setup remains binary, either accumulation continues before reversal, or we break down further in sync with BTC weakness.

⚠️ Risk View

Fundamental growth has stalled.

Earnings miss raises red flags.

Bitcoin exposure magnifies downside risk.

If price breaks below $32–30, that would confirm a breakdown, potential free-fall to $8–15.

On the positive side, the company stopped share dilution, maintains good liquidity, and still has strong brand power in fintech.

🧩 My Position

I currently hold a protected position (protective puts) till march 2026, limited downside, but I’m considering a full exit.

There’s no visible fuel for strong upside, and with BTC risk rising, the short-term picture remains shaky.

If we see capitulation into the $30–40 range with BTC bottoming, that could be a smart-money accumulation zone again.

🔑 Key Levels

$100 → breakout confirmation, opens path to $280

$50–80 → main accumulation cluster

$32–30 → invalidation / stop-loss zone

$8–15 → next major demand zone if breakdown continues

🧭 Summary

Block’s fundamentals are slowing, its Bitcoin exposure is a double-edged sword, and technically we’re at a critical level.

If BTC corrects sharply, Block could retest the $30–40 area or even lower, but if it holds and reverses above $100, the next bull wave could be massive.

At this stage, risk management and patience are key.

BKKT — Streamlined, Debt-Free, and Aiming at Stablecoin + AICompany Overview:

Bakkt NYSE:BKKT is a regulated digital asset platform offering crypto trading, custody, and financial services to both institutions and retail—positioning itself as a pure-play crypto infrastructure provider in the $2.7T digital asset market.

Key Catalysts:

Bitcoin Treasury + Institutional Tailwind: Leveraging the BTC rally and a treasury strategy to align with accelerating institutional adoption.

Portfolio Simplification: Sale of the loyalty business and Up-C reorganization streamline ops, upgrade governance, and boost investor appeal.

Balance Sheet Strength: Now debt-free after redeeming all convertible notes—greater optionality for growth initiatives.

New Verticals: Well-capitalized to expand into stablecoin infrastructure and AI-driven finance, widening recurring-revenue opportunities.

Investment Outlook:

Bullish above: $21.00–$22.50

Target: $68.00–$70.00, supported by clean capital structure, regulatory footing, and expansion into stablecoins + AI finance.

#BKKT #DigitalAssets #CryptoCustody #Stablecoins #AIFinance #FinTech 🚀

Up from here towards 140?Today might be the last big drawdown. Hopefully it should recover towards 140 in next 6-9 months. All the best.

Not a financial advice.

Thanks

Fiserv | FI | Long at $69.91For the first time since its IPO in 1986, a "major stock" crash has happened to Fiserv NYSE:FI . Previously, the stock "crashed" and followed the trajectory of ups and downs of the S&P 500, but this one is different. And, perhaps, a major opportunity for savy investors.

I won't say much about the financials since after today's earnings call the stock plummeted and earnings/revenue projections will get revised serval times, but this was a high-growth opportunity in the past. What I see today is a huge overreaction to a company going through a growth transition, but by all means, not dead... yet www.tradingview.com

I think we'll see leadership shakeups, layoffs, and system adaptions into 2026. This drop, and where it landed near my major crash simple moving average, hints this price cut was planned (at least algorithmically) and I won't be surprised if the near-term bottom is in or almost in in the $60s. Thus, at $69.91, NYSE:FI is in a personal buy-zone.

Conservative Targets into 2028:

$85.00 (+21.6%)

$100.00 (+43.0%)

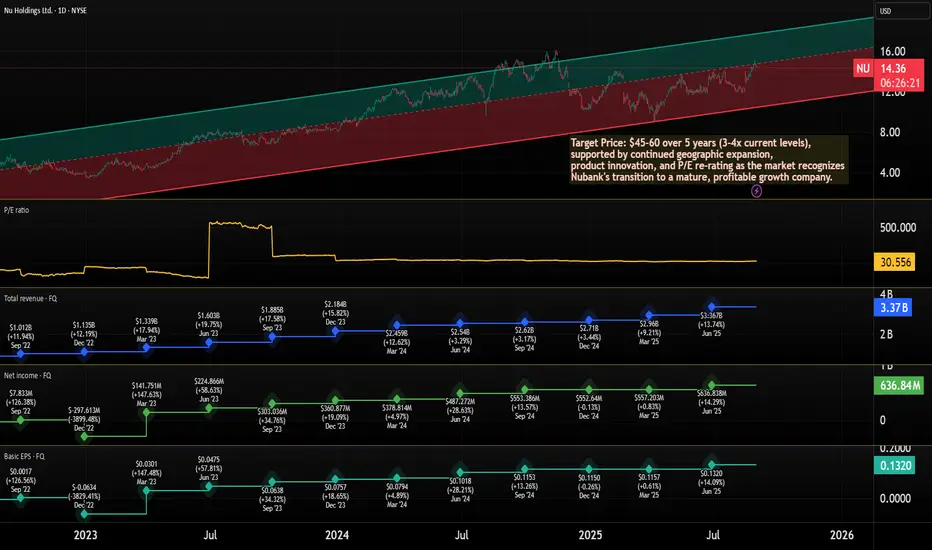

Nu Holdings (NU) AnalysisCompany Overview:

NYSE:NU is Latin America’s largest digital bank, offering mobile banking, credit cards, and investments—direct exposure to the region’s booming fintech market.

Key Highlights:

Scale & Growth: 123M customers (+18M YoY), adding ~1.5M/month.

Financial Momentum (Q2’25): Revenue $2.9B (+40% YoY); net income $487M (+143%)—driven by credit, investments, and cross-sell.

Geographic Expansion: Mexico (13M customers) and Colombia underscore a highly scalable, repeatable growth model.

Investment Outlook:

Bullish above: $13.50–$14.00

Target: $22.00–$23.00 — supported by accelerating monetization, market expansion, and category leadership.

#NuHoldings #Fintech #DigitalBanking #LatinAmerica #Stocks #Earnings #GrowthStock #EmergingMarkets #NU #Investing #FintechRevolution

SOFI — Bullish Breakout with Strong VolumeSOFI has broken out to a new all-time high with strong volume, signaling strong buying pressure and renewed bullish momentum.

The stock remains in a clear uptrend, trading above the 50-day EMA. Recently, SOFI rebounded perfectly at the EMA 50, confirming it as a strong dynamic support zone. The bullish pennant pattern breakout further strengthens the case for a trend continuation.

The uptrend line is still intact, and as long as the price holds above the EMA 50, the bullish outlook remains valid.

Entry Price : 31.00 - 32.00

Stop Loss: Below EMA 50 (~26.80–26.90)

Targets: 35.00 and 38.00

NET — AI Infrastructure Leader Launches Stablecoin InnovationCompany Overview:

Cloudflare, Inc. NYSE:NET is a global leader in cloud connectivity and cybersecurity, delivering secure, scalable, and high-performance infrastructure for the modern internet. The company is evolving into a key enabler of AI-driven applications, with its Workers platform gaining strong enterprise traction to power large-scale intelligent workloads.

Key Catalysts:

Fintech breakthrough: The launch of the NET Dollar stablecoin bridges AI, cloud, and financial infrastructure, enabling automated machine-to-machine (M2M) payments and introducing new recurring revenue models.

Enterprise growth: Added 219 new large customers in Q2 2025, highlighting accelerating adoption and market leadership.

AI ecosystem expansion: Increasing integration of Cloudflare’s edge computing network within enterprise AI frameworks positions it at the core of the next-generation digital economy.

Investment Outlook:

Bullish above: $188–$190

Upside target: $380–$390, supported by AI infrastructure dominance, fintech innovation, and accelerating enterprise demand.

#Cloudflare #AI #Stablecoin #Cybersecurity #Fintech #DigitalInfrastructure #EdgeComputing #Investing #NET

23 soon?Look bearish and may drop towards low 20s which can be a good buying opportunity.

All the best !!

Not a financial advise.

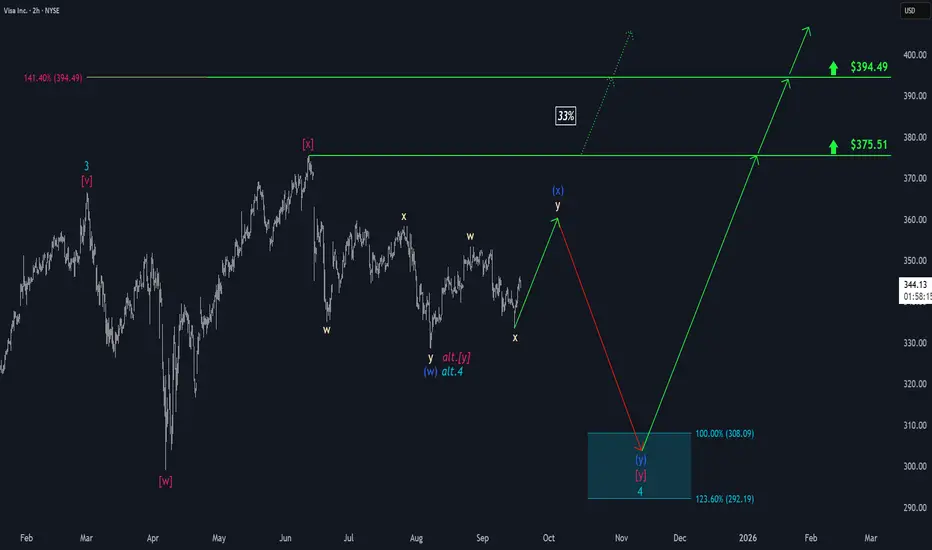

Visa: Corrective Upward MoveIn our primary scenario, we place Visa in the corrective upward move of blue wave (x). After the top, we expect the broader downward trend of turquoise wave 4 to take hold, which should push the stock into our turquoise Target Zone between $308.09 and $292.19. At that level, we anticipate a sustained reversal. From this low, a new upward impulse is likely: wave 5 should then have enough strength to lift price above the resistance levels at $375.51 and $394.49. However, an alternative scenario remains relevant: there is a 33% probability that the correction of wave alt.4 has already concluded. If so, the stock could immediately break above the resistance levels mentioned.

Undervalued Fintech Just Hit 110M Users: Nubank ($NU)The Case for Nubank NYSE:NU

Nubank is a combination of growth and value in the fintech space. I personally like it when, as an investor, I find a stock that is a growth and value stock simultaneously.

Nu is trading at a P/E of 31.5x, and the company is a compelling story with upside potential as Latin America's leading digital bank continues its rapid expansion.

The LATAM market still has lots of underbanked people, but Nubank offers the neobank and digital services necessary for those people.

The fact that it amassed 110 million clients in just a few years tells us something. The clients are mostly in Brazil, Mexico, and Colombia, but the company is planning expansion to other countries, including the US

Remarkable Financial Trajectory (2023-2025)

Revenue Growth Acceleration:

2023: $3.37B total revenue

Q2 2025 alone: $3.36B revenue. Q2 2025 alone had the same revenue as 2023. Truly impressive

Very strong quarter-over-quarter growth and operational leverage.

Key Financial Metrics Progression

P/E Evolution: From 90x+ (growth phase) → 31.5x (profitable growth phase)

Revenue CAGR: 63.4% demonstrating consistent market penetration

EPS Growth: 63.2% three-year average showing operational leverage

User Growth: 30M → 110M+ (4x in 5 years) with improving unit economics

Investment thesis: Why Nubank is undervalued

1. Valuation arbitrage

Current P/E: 31.5x vs. US fintech peer SoFi NASDAQ:SOFI at ~50x

Growth-adjusted valuation: 63% revenue growth at 31x P/E = 0.49 PEG ratio (anything under 1.0 is attractive)

International discount: Market applying "emerging market penalty" despite superior fundamentals

2. Proven Business Model Scalability

The 2023-2025 data eliminates key execution risks:

Growing profitability across multiple quarters

Growth maintained at scale (110M+ users, still growing)

Margin expansion demonstrating operational leverage

Multi-year consistency reducing one-time success concerns

3. Structural advantages in underserved arkets

Digital-first cost structure: 80%+ lower cost base than traditional banks

First-mover advantage: Dominant position in Brazil, early leadership in Mexico/Colombia

Network effects: Growing ecosystem creates switching costs and viral acquisition

Regulatory tailwinds: Government support for financial inclusion across Latin America

4. Multiple Expansion Catalysts

Near-term (1-2 years):

US market expansion announcement

Continued profitability growth reducing "emerging market risk" perception

Potential inclusion in major indices (MSCI, etc.)

Medium-term (3-5 years):

Cross-border payments and remittance products

Small business lending expansion

Insurance and wealth management scaling

Geographic Expansion: The untapped opportunity

Brazil (Mature Market)

Market-leading position providing stable cash flow foundation

Still room for product penetration (insurance, wealth management)

Mexico/Colombia (Growth Markets)

Early-stage penetration with massive TAM

2025 data suggests strong traction in these markets

US Expansion (Game Changer)

Management indicated plans for US market entry

Could unlock premium US fintech valuations (40-50x P/E multiples)

Remittance corridor between US and Latin America represents $100B+ opportunity

Risk-Reward Analysis

Conservative 5-Year Scenario:

Earnings growth: 25% CAGR (conservative given 63% current growth) = 3x earnings in 5 years

Multiple expansion: P/E re-rating to 45x (still below SoFi's 50x) = 43% upside

Combined effect: 3x earnings × 1.43x multiple = 4.3x total return

Base Case Assumptions:

Revenue growth slows to 20-25% annually (from current 63%)

P/E expands to 40-45x as profitability matures

US expansion adds 20-30% valuation premium

Target: 3-4x returns over 5 years

Why Now??

Valuation Opportunity: 31.5x P/E for 63% growth company is historically cheap

Proven Execution: 2023-2025 data eliminates major execution risks

Market Inefficiency: US investors underweight due to "foreign" perception

Catalyst Pipeline: US expansion, product launches, and regulatory tailwinds

Target Price: $45-60 over 5 years (3-4x current levels), supported by continued geographic expansion, product innovation, and P/E re-rating as the market recognizes Nubank's transition to a mature, profitable growth company.

Conclusion

Nubank in 2025 is no longer a speculative fintech play - it's a proven, profitable, growing financial services powerhouse trading at a discount to inferior peers. The combination of 63% revenue growth, sustainable profitability, massive TAM, and 31.5x P/E creates an asymmetric risk-reward opportunity rarely seen in public markets.

Pagaya Technologies (PGY) AnalysisCompany Overview:

Pagaya Technologies NASDAQ:PGY is a fintech innovator leveraging AI-driven underwriting to scale across consumer credit, real estate, auto financing, and POS lending. Its diversified lending mix reduces reliance on personal loans while expanding growth opportunities.

Strategic Drivers:

Strong Partnerships: Backed by 31 financial institutions, enabling broad origination capacity.

Guidance Upgrade: Management raised 2025 outlook to $10.5–$11.5B in network volume, $1.25–$1.325B in revenue, and $345–$370M in adjusted EBITDA.

Execution Strength: Clear momentum toward becoming a leading U.S. lending platform.

Investment Outlook:

Bullish above: $23–$24.

Upside target: $43–$45, supported by AI-driven lending growth, partnerships, and upgraded guidance.

📢 PGY—AI-powered fintech scaling into a top-tier U.S. lending platform with accelerating revenue and EBITDA growth.

#PGY #Fintech #AI #ConsumerCredit #Lending #GrowthStocks #AutoLoans #POSFinancing

SOFI LEAP Call Setup: Long-Term Fintech Moonshot?

# 🚀 SOFI LEAP Call Setup: Long-Term Fintech Moonshot? 💎📈 (2025-08-22)

📊 **Market Consensus Recap**

* 📈 Weekly RSI: 84.3 → strong bullish momentum

* 📉 Monthly RSI: 63.1 → fading momentum, overextended zone (99.1% of 52-week range)

* 💵 Institutional Flow: Neutral (Call/Put OI ratio = 1.00)

* 🌪 Volatility: Favorable (low VIX = good LEAP environment)

* ⚠️ Risk: Extreme valuation → caution on new entries

---

# 🎯 TRADE PLAN

* 🏦 Instrument: **\ NASDAQ:SOFI **

* 📈 Direction: **CALL (LONG)**

* 🎯 Strike: **27.00**

* 💵 Entry: **6.00**

* 🛑 Stop Loss: **4.20 (-30-40%)**

* 🎯 Profit Target: **11.40**

* 📅 Expiry: **2026-09-18**

* 📏 Size: **1 contract**

* 📈 Confidence: **75%**

* ⏰ Entry Timing: **Market Open**

---

⚠️ **Key Risks**

* 🚨 Overvalued at near 52-week high (99.1%)

* 📉 Potential correction to \$15–\$18 before next leg

* 📰 Macro/news shocks may hit fintech sentiment

---

# 📌 Hashtags

\#SOFI #OptionsTrading #LEAPs #StockMarket #LongTermInvesting #BullishSetup #Fintech #OptionsFlow #SmartMoney #TradingSignals #BreakoutTrading #SwingTrade

IBKR – Scaling Globally with Automation, Innovation, and InflowsCompany Snapshot:

Interactive Brokers NASDAQ:IBKR is delivering explosive growth, driven by unmatched automation, deep market access, and strong global demand for low-cost, self-directed investing.

Key Catalysts:

Account Growth Surge 🚀

Q2 saw 250,000 new accounts, pushing 2024’s total to 528,000+—already surpassing all of 2023. This signals powerful user acquisition at scale, especially in volatile and rate-sensitive environments.

Global Expansion 🌐

Rising momentum from international clients and introducing brokers positions IBKR as a top gateway for U.S. equity and options access worldwide.

Product Innovation 🧠

Thousands of platform upgrades in Q2 alone, including:

IBKR InvestMentor app for educational engagement

“Investment Themes” tool, simplifying access to trend-driven strategies

These add stickiness and improve the user experience.

Strong Financial Engine 💵

Record net interest income of $860M (+9% YoY), driven by:

Elevated client cash balances

Robust securities lending revenue

IBKR’s business model thrives on rate volatility and market churn, offering powerful operating leverage.

Investment Outlook:

Bullish Entry Zone: Above $56.00–$57.00

Upside Target: $80.00–$82.00, supported by client growth, global reach, and rate-sensitive earnings strength.

📈 IBKR is a rare fintech that’s both profitable and rapidly scaling—making it a top pick for exposure to the next wave of digital brokerage adoption.

#Fintech #IBKR #InteractiveBrokers #SelfDirectedInvesting #TradingPlatforms #BrokerageGrowth #InterestIncome #GlobalMarkets #TechInFinance #RetailInvesting #InvestMentor #OptionsTrading #ScalableFinance

AFRM Pre Earnings Triangle BreakAFRM has broken the symmetrical triangle to the upside. If this holds we could see a strong rally into earnings. I would want to see strong volume added to this equation for the move up to be confirmed.

My STOP on this position would be a daily candle close back under the trendline with confirming volume. A retest of the triangle would be my spot to add to the position.

LC EARNINGS PLAY – STRIKE WHILE IT'S HOT!**

🚨 **LC EARNINGS PLAY – STRIKE WHILE IT'S HOT!** 🚨

📅 **Earnings Season Heat Check: LC | Jul 29**

💰 **Positioning for a Post-Earnings POP!**

---

🔥 **The Setup:**

LC’s earnings momentum is real –

📈 TTM Rev Growth: **+13.1%**

💹 EPS Surprise Rate: **150% avg**

📊 75% Beat Rate History

💵 Analyst Consensus: **Strong Buy (1.8/5)**

---

📉 **Technical Tailwind:**

✅ Price above 20D + 200D MA

✅ RSI: **60.07** – room to run

📈 Volume Spike: **+61% above 10-day avg**

🚀 Options flow targeting **\$14 CALLS** w/ OI: **864** / Vol: **737**

---

📌 **TRADE IDEA**

🎯 Buy: **\$14.00 Call @ \$0.70**

📆 Exp: **Aug 15, 2025**

🎯 Target: **\$2.10** (Risk/Reward = 1:3)

🛑 Stop: **\$0.35**

---

⚠️ **Earnings Risk:** IV crush real.

🎯 Exit within 2 hours **post-EPS** if no move.

Macro tailwinds + financial sector rotation = 🚀 fuel.

**Beta = 2.45** → Big move potential incoming!

---

🧠 Confidence Level: **75%**

⏰ Timing: Pre-Earnings Close

🧾 Model-Driven Strategy | No Hype, Just Edge.

---

💥 Let’s ride the LC earnings wave – \$15+ in sight! 💥

\#LendingClub #LC #EarningsPlay #OptionsTrading #TradingView #StocksToWatch #CallOption #Fintech #SwingTrade #EarningsHustle #BullishSetup #IVCrush #EarningsGamma #ShortTermTrade