Why Gold Remains the Dominant Macro Hedge into Q1 2026🔱 GOLD Q1 2026 MACRO SNAPSHOT — EXECUTIVE SUMMARY

✨ Structural bull trend remains dominant into Q1 2026 as macro + flow regime stays supportive

🟡 Primary macro unlock: sustained suppression of real yields + soft USD regime

🚀 Convex upside risk driven by ETF re-allocation + options gamma reflexivity

🏦 Central-bank demand continues to anchor downside — pullbacks remain shallow and brief

🌍 Geopolitics (Iran / sanctions / energy risk) + Trump policy wildcard inject tail-risk premium

🧨 Trade / tariff escalation remains inflationary + growth-negative = gold-positive asymmetry

🧲 Options positioning introduces gamma squeeze risk near key psychological levels

🛡 Bull case intact unless real yields reprice sharply higher (low-probability base case)

🎯 Q1 bias: buy pullbacks within macro support zones; expect sharp upside bursts on catalysts

🏦 Strategic stance: accumulation on dips, monetize volatility spikes, respect gamma-driven extensions

📊 GOLD Q1 2026 — CATALYST SCORECARD

1️⃣ Fed Path & Real Yields — 9.2 / 10 (Primary Driver)

Lower or capped real yields remain the single most important determinant of gold’s medium-term trajectory. Entering Q1 2026, markets continue to price a regime where policy flexibility dominates over inflation-fighting urgency. Any growth wobble or labor-market softening reinforces this dynamic, keeping the opportunity cost of holding gold suppressed.

Why this matters in Q1:

Gold doesn’t need aggressive cuts — it needs confidence that real yields won’t rise. That condition remains intact.

________________________________________

2️⃣ Central-Bank Buying / De-Dollarization — 8.6 / 10 (Structural Floor)

Official-sector demand remains price-insensitive and persistent, led by EM reserve managers diversifying away from USD concentration. This flow acts less like momentum chasing and more like strategic balance-sheet allocation, creating durable downside support.

Why this matters in Q1:

Central banks reduce drawdown depth and shorten correction cycles — a critical structural tailwind.

________________________________________

3️⃣ U.S. Dollar Regime Shift — 8.4 / 10 (Mechanical + Psychological)

A softer or unstable USD regime boosts gold through two channels:

1. Mechanical FX translation for non-USD buyers

2. Erosion of the “confidence premium” embedded in USD assets during policy uncertainty

Why this matters in Q1:

Gold benefits not just from USD weakness, but from USD credibility risk — an underappreciated accelerant.

________________________________________

4️⃣ Trade / Tariff Shock Risk — 8.3 / 10 (Asymmetric Upside)

Tariffs are uniquely bullish for gold because they introduce:

• Inflation risk

• Growth uncertainty

• Policy unpredictability

This is one of the rare macro combinations where gold can rally even if risk assets struggle.

Why this matters in Q1:

Any renewed tariff escalation immediately feeds inflation hedging demand without requiring a recession trigger.

________________________________________

5️⃣ ETF & Institutional Allocation Flows — 8.0 / 10 (Trend Amplifier)

ETF flows confirm whether gold is a “trade” or a portfolio allocation. Recent behavior signals the latter. Once institutions reweight, flows tend to persist across quarters, not days.

Why this matters in Q1:

ETF demand converts macro tailwinds into price persistence, not just spikes.

________________________________________

6️⃣ Geopolitics (Iran, Sanctions, Energy Risk) — 7.8 / 10 (Event → Macro Bridge)

Geopolitics matters most when it threatens:

• Energy supply

• Shipping routes

• Sanctions spillovers

Iran-related escalation risk sits at the intersection of all three, making it materially relevant rather than headline noise.

Why this matters in Q1:

If energy prices stay elevated or volatile, geopolitical risk migrates directly into real yields and inflation expectations.

________________________________________

7️⃣ Trump Policy Wildcard — 7.6 / 10 (Fat-Tail Premium)

Markets price Trump-era policy not as a single forecast, but as distributional uncertainty:

• Tariffs

• Sanctions

• Diplomatic volatility

This raises implied volatility, FX uncertainty, and safe-haven demand before events occur.

Why this matters in Q1:

The wildcard embeds a persistent risk premium into gold rather than episodic spikes.

________________________________________

8️⃣ Gamma Squeeze / Options Reflexivity — 7.5 / 10 (Convex Accelerator)

Options positioning can force dealers into pro-cyclical hedging, meaning:

• Rising price → forced buying → further upside

• Particularly potent near psychological round levels

Why this matters in Q1:

Gamma effects don’t create trends — they accelerate existing ones, turning steady inflows into vertical price action.

________________________________________

🧠 Q1 2026 — How These Catalysts Interact (Key Insight)

Gold’s strength is not coming from a single driver, but from layered reinforcement:

• Real yields + USD define the trend

• Central banks + ETFs define the floor

• Tariffs + geopolitics + Trump wildcard define tail risk

• Gamma positioning defines speed and volatility

This is why pullbacks remain shallow and rallies tend to extend further than expected.

________________________________________

⚠️ What Would Actually Break the Bull Case?

Only scenarios that meaningfully raise real yields:

• Hawkish inflation surprise forcing policy re-tightening

• Sustained USD resurgence driven by growth dominance

• Abrupt de-escalation of trade and geopolitical risk combined with strong growth

Absent those, gold remains in a buy-the-dip regime.

________________________________________

✅ Bottom Line — Institutional Takeaway

Gold enters Q1 2026 with:

• A structural bid underneath price

• Convex upside risk on policy or geopolitical shocks

• Options-driven acceleration near key levels

This is not a market to fade strength blindly — it’s a market to manage exposure, harvest volatility, and accumulate on macro-supported pullbacks.

Gamma

How Investment Funds Really Make Money From Bitcoin📰 After years of closely following financial markets, one conclusion has become impossible for me to ignore:

most people fundamentally misunderstand how professional funds make money from Bitcoin.

Retail traders often assume funds operate the same way they do — buying low, selling high, and betting on direction.

If price goes up, they win.

If price goes down, they lose.

That assumption is overly simplistic — and largely incorrect.

🔍 For institutional funds, Bitcoin is not a directional gamble.

From what I’ve observed, large funds are not emotionally attached to whether Bitcoin rises tomorrow or drops next week.

Price direction is not their primary concern.

What truly matters is structure.

Funds are not rewarded for guessing the market correctly.

They are rewarded for controlling risk and systematically converting volatility into measurable returns.

🎯 Their real objective is volatility, not conviction.

When a fund allocates capital to Bitcoin, it is rarely driven by belief in a narrative or excitement around headlines.

They don’t follow influencers.

They don’t react to social media hype.

What they care about is quantifiable price movement.

Volatility is the raw input.

Mathematical models are the engine.

Decisions are driven by numbers, not emotions.

🧠 Buying Bitcoin does not automatically mean being bullish.

One of the most common misconceptions I encounter is the idea that institutional buying signals an expectation of higher prices.

In reality, a fund can purchase Bitcoin while remaining entirely neutral.

They can be delta-neutral, fully hedged, detached from market direction, and protected against both upside and downside moves.

This is why buying BTC is not a bet for them.

It is simply the first layer in a multi-stage trading structure.

📊 So how do funds actually profit from price movement?

By combining spot exposure with derivatives, funds build positions that benefit from movement itself rather than predicting direction.

When price rises, positions are adjusted and partial exposure is sold at higher levels to rebalance risk and lock in gains.

When price falls, exposure is rebuilt at lower prices to restore balance.

🔁 Price moves higher → exposure is reduced at better levels

🔁 Price moves lower → exposure is increased at cheaper levels

🔁 The process repeats with discipline and precision, free from emotion

This systematic process is known as gamma scalping — the quiet, continuous profit mechanism behind institutional trading.

💰 Where do their real profits come from?

Not from news headlines.

Not from influencers.

Not from ETF narratives.

Profits are generated through continuous hedge adjustments, realized volatility exceeding expectations, direction-neutral structures, and strict mathematical discipline.

⛔ The only environment that truly challenges these strategies is when the market stops moving altogether.

🧭 Let me be direct with you, speaking as a market professional.

You are not BlackRock.

You do not have their infrastructure.

You do not have their capital, execution speed, or risk frameworks.

Attempting to interpret or replicate their actions without understanding the underlying structure will not improve your trading — it will only increase confusion.

✍️ My conclusion is straightforward:

Funds do not profit from predicting the future.

They profit from engineering outcomes.

They do not trade stories.

They do not trade emotions.

They do not trade social media noise.

🎯 They trade structure.

And you?

Stop obsessing over what institutions are doing.

Start focusing on what you should be doing.

That is the line between surviving in the market

and being quietly pushed out of it.

MSFT Potential Upside Squeeze SetupMSFT is currently forming a constructive structure with clearly defined levels.

On the downside, the 475 put support has been defended three separate times, signaling strong positioning interest and consistent absorption of selling pressure. Price continues to hold above the HVL , with an extremely narrow transition zone and a broadening upward-tilted positive GEX profile — all reinforcing structural stability.

If price breaks upward from the first call wall at 480 , this typically favors continuation rather than any sustained move lower.

Upside levels :

The next major call resistance sits at 500 — which also aligns with the 8/8 level on the MM grid system . This creates a very strong confluence, making 500 a significant resistance zone.

If price cleanly accepts and pushes through 500, dealer hedging flows can accelerate, potentially triggering an upside squeeze — with an initial upside extension capped near 520 .

If momentum continues to build above 500, the next substantial call resistance sits at 520 , currently the second-largest call wall on the chain.

As long as price remains above HVL and the 475 support zone holds, the risk-reward skew favors continuation to the upside, with 480 as the trigger level and 500 as the speculative call-positioning target .

However — critical risk scenario:

If 475 breaks and we do not see a fast rebound from the 470/460 negative squeeze zone , this could initiate a sharp downward move and a trend shift. Currently, the largest protective put concentration sits at 475 — and the put side only begins to melt if price can reclaim 480 .

At least based on the aggregated options chain, MSFT is now under immense compression with clear trigger points .

MSFT tightening under GEX squeeze pressure

How Funds Actually Make Money From BitcoinIf you spend more than five minutes on Crypto TikTok (YouTube or X are not much different), you’d think the entire market depends on:

- who “bought the dip,”

- who “sold the top,”

- and which whale “decided” to pump or dump.

The screamers with flashy thumbnails and zero understanding yell:

- “BlackRock is buying—BULLISH!”

- “Whales are selling—CRASH INCOMING!”

- “Institutions are entering the market!!!”

- No nuance.

- No structure.

- No clue.

Because here’s the truth:

What BlackRock buys or sells is almost irrelevant to you.

Funds do not make money the way TikTok believes.

They don’t need Bitcoin to go up.

They don’t need Bitcoin to go down.

They need one thing:

Movement. Volatility. Math.

Let’s destroy the hype and show how funds actually make money.

1. Why “BlackRock is buying BTC” tells you absolutely nothing

Retail sees a headline:

“ETF inflows: +5,000 BTC today!”

And jumps to conclusions:

“They know something!”

“Price HAS to go up!”

“Institutions are bullish!”

No.

A fund can buy BTC and still be:

- 100% hedged

- delta-neutral

- directionally flat

- risk-neutral

- fully protected against price movement

The purchase is not a bet.

It’s a component of a structured position.

Buying BTC is just Step 1.

What matters is Step 2, 3, 4, 5…—all the parts TikTok doesn’t even know exist.

2. Why TikTok “analysts” have no idea what they’re talking about

If someone:

- screams in every video,

- says “bullish” or “bearish” 40 times a minute,

- thinks “institutions pump price,”

- doesn’t know what delta, gamma, basis, hedging, ATM straddles are…

…then they are not explaining institutional flow.

They are farming views and likes, not teaching markets.

Let’s be blunt:

If you can’t explain a delta-neutral hedge, your opinion about what BlackRock “plans to do” or "is doing" is worthless.

So let’s walk through how a real fund uses BTC to print money without caring if price goes up or down.

3. How a real fund makes money from volatility (step-by-step, using $100,000 BTC)

Assume:

- BTC price = $100,000

- A fund wants exposure to volatility, not direction

- They buy a BTC ATM straddle (call + put at 100k)

- Delta ≈ 0

- Gamma > 0 → the part that generates money

- They also own BTC spot for hedging.

- Let’s say the fund holds 1 BTC worth $100,000 as inventory for hedge adjustments.

At the start:

Delta-neutral. No directional risk.

Now let’s see how they profit.

Step 2 – BTC goes up 10% → $110,000

Straddle delta becomes +0.5 BTC.

The fund is unintentionally long 0.5 BTC.

To go back to neutral:

The fund sells 0.5 BTC at $110,000.

Cash received:

0.5 × 110,000 = $55,000

Theoretical cost basis (100k):

0.5 × 100,000 = $50,000

👉 Profit from hedge = $55,000 – $50,000 = $5,000

Plus, the straddle increased in value due to volatility.

Step 3 – BTC drops 10% → $90,000

Now straddle delta flips negative: –0.5 BTC

To get back to neutral:

The fund buys 0.5 BTC at $90,000.

Cash paid:

0.5 × 90,000 = $45,000

If they later sell that BTC at the baseline of 100k:

👉 Profit = $50,000 – $45,000 = $5,000

Again, without needing BTC to go up or down, “as predicted.”

This is called:

Gamma scalping — the quiet, relentless engine behind institutional P&L.

Up move → sell high.

Down move → buy low.

Repeat. Print. Sleep.

4. Where does the REAL profit come from?

A fund earns from:

- hedge adjustments (buy low, sell high, but mathematically—not emotionally)

- straddle appreciation as realized volatility exceeds implied volatility

- basis differences between spot and futures

- neutrality to direction, allowing consistent compounding

They make money even if Bitcoin swings between 95k–105k for weeks.

The only time they lose?

When BTC does NOT move.

Because then the straddle premium decays.

That's it.

Nothing to do with faith, predictions, narratives, influencers, or ETF flows.

5. So why should YOU ignore what BlackRock is doing?

Because:

- You are not BlackRock.

- You do not run a delta-neutral book.

- You do not make money from gamma exposure.

- You do not scalp intraday hedges on $100M positions.

- You do not capture basis spreads across spot and derivatives.

- You do not have a trading desk rebalancing risk every hour.

But the TikTok screamers will still tell you:

“Institutional buying = bullish!”

“Institutional selling = bearish!”

“Whales know something!”

They don’t know anything.

Especially not about institutional structure.

So here’s the punchline:

Watching what funds do—without understanding why they do it—is the fastest path to confusion in the best case and destruction in the worst.

You don’t have their:

- tools,

- capital,

- execution speed,

- risk models,

- mandate,

- or mathematical framework.

So trying to mimic them is not just pointless —it’s dangerous.

Final Lesson: Ignore the noise, ignore the hype, ignore the TikTok parade.

BlackRock doesn’t care about bull markets or bear markets.

BlackRock doesn’t need Bitcoin to moon.

BlackRock doesn’t panic when Bitcoin drops.

Because BlackRock doesn’t trade the story.

They trade the structure.

And unless you operate like a fund — stop pretending their moves matter to your trading.

You’re not them.

You don’t have their machinery.

You don’t have their volatility book.

So:

Stop watching what institutions do.

Start understanding what you should do.

That’s the difference between surviving and blowing up.

P.S: BlackRock and TikTok are used just as an example:)

$IWM — The Rate-Cut Leverage PlayLast week delivered one of those classic market paradoxes where everything that should be bearish suddenly became bullish:

layoffs → bullish

weak labor data → bullish

flat inflation → bullish

Why?

Because the market has now fully locked its focus on one thing only:

a Federal Reserve rate cut.

Volatility was sharp, price action even sharper, and the headlines kept flipping faster than most traders could adjust.

Let’s break down what actually happened — and what matters for the week ahead.

IWM GEX for 01/16/2025 expiration using TanukiTrade Options Overlay GRID System and the GEX Profile indicator

If the Fed cuts, small caps win the most — and last week proved it again.

IWM broke above the 250 call gamma level

Short-term gamma squeeze potential

Closed at new all-time highs

This is where rate-cut optimism expresses itself with maximum torque.

If the Fed turns dove on Wednesday → IWM can easily extend.

What is Gamma?🔎 What is Gamma?

Gamma Exposure (GEX) measures how much and how fast an option’s Delta changes as the underlying moves.

Why does this matter? Because when options shift, market makers must hedge, and their hedging can move markets.

Gamma = the “acceleration” of Delta.

Large gamma zones = areas where market makers must hedge aggressively.

These hedges often create temporary support or resistance levels.

Think of Gamma as the invisible hand shaping intraday price action.

⚡ Why is Gamma Important?

Market makers aren’t directional traders — they aim to stay delta-neutral. But depending on whether they’re in a positive or negative gamma environment, their hedges can either calm the market or fuel volatility.

✅ Positive Gamma

Dealers are net long calls.

Price Drop: They buy underlying to hedge → creates support.

Price Rise: They sell underlying to hedge → creates resistance.

Result: Market stays stable, moves are dampened.

❌ Negative Gamma

Dealers are net short puts.

Price Drop: They sell underlying to hedge → adds downward pressure.

Price Rise: They buy underlying to hedge → adds upward pressure.

Result: Market becomes unstable, moves are amplified (higher volatility, risk of squeezes).

📍 Key Gamma Levels to Watch

Zero Gamma:

Pivot point where hedging flows are balanced. Price often consolidates or pivots here.

Major Positive Gamma Zones:

Act as resistance (dealers sell into strength).

Major Negative Gamma Zones:

Act as support (dealers sell into weakness, but may cause bounces).

FOMC 100% Breakout (Check) - Key Resistance and 6500 Gamma PinFOMC was in fact a NOISE candle

So I measured the candle, projected a 100% breakout bullish and bearish

Bulls took the bait and ran higher, but still resistance @ 6700 seen today and hopefully

a short-term window to see a bit of a slide lower into some technical levels

EMA support levels

-watching the 21 period daily EMA

-watching the 50 period daily EMA

6550 FOMC candle lows from last week

6500 Gamma Pin with JP Morgan's quarterly collar trade

This is the first day in several weeks where I've seen some actual follow through

in negative gamma option flows

If futures grinds prices lower, the cascade may take hold and we can see a 100-200 point

selloff quickly in the S&P

I still like scooping up premium and buying the dips, but hopefully at more attractive levels

like 4-5% lower or even 8-10% lower

Let's see how it plays out. I'll be in the markets grinding per usual.

Thanks for watching!!!

From Mystery to Mastery: Options ExplainedIntroduction: Why Options Feel Complicated

Options are perhaps the most misunderstood instruments in trading. To the untrained eye, they seem like an impossible puzzle: strange terminology, an overwhelming options chain filled with numbers, and payoff diagrams that bend in multiple directions. Many traders dismiss them as “too complex,” or worse, confuse them with gambling.

But options are not about chance — they are about choice. Each contract offers the trader a way to shape risk, control exposure, and adapt to unique market conditions. While this flexibility comes with greater sophistication, it also unlocks a toolkit that no other instrument can match.

The visuals you can see at the top of this publication — an options risk profile with multiple legs and a snapshot of an options chain — illustrate this dual nature. At first glance, the visuals are busy, packed with strikes, expirations, premiums, and curved payoff lines. Yet these are the very tools that make options versatile. They can be combined to express bullish, bearish, neutral, or volatility-driven views with precision.

The goal of this article is to take the mystery out of options and highlight why their complexity is worth understanding. Step by step, we’ll explore how they work, how the Greeks shape outcomes, how different strategies can be structured, and why they play such a vital role when layered onto futures trading.

What Are Options?

At their simplest, options are contracts that give the buyer the right, but not the obligation, to buy or sell an asset at a predetermined price within a specific time period. That asset may be a stock, a futures contract, or even an index.

Two Building Blocks

Call Options: Give the right to buy the underlying at the strike price. Traders buy calls when they expect the underlying to rise.

Put Options: Give the right to sell the underlying at the strike price. Traders buy puts when they expect the underlying to fall.

The Price of an Option: The Premium

Option buyers pay a premium, while option sellers collect it. This premium reflects the market’s assessment of risk and probability, and it changes constantly with price, volatility, and time.

Intrinsic vs. Extrinsic Value

Intrinsic Value: The amount an option would be worth if it were exercised immediately. For example, a call with a strike below the current price has intrinsic value.

Extrinsic Value: The “time value” built into the premium — compensation for the uncertainty of where price may go before expiration.

Why Options Matter

Unlike buying or selling the underlying directly, options allow traders to shape their exposure: define maximum risk, set conditional payoffs, or even profit from time decay and volatility changes.

The above options chain screenshot illustrates how layered this world can be. Rows of strikes, bid-ask quotes, open interest, and implied volatility may look daunting at first. But each piece of data contributes to building strategies that fit specific objectives.

The Greeks Made Simple

If the options chain is the menu, then the Greeks are the ingredients that determine how a position behaves. Each Greek measures a different sensitivity, helping traders understand not just what they are trading, but how it will move as conditions change.

Delta (Δ)

Measures how much an option’s price will change for a one-point move in the underlying asset.

A delta of 0.50 means the option should gain about 0.50 units if the underlying rises by 1.

Traders often use delta as a proxy for probability of finishing in the money.

Gamma (Γ)

Tracks how much delta itself will change as the underlying moves.

High gamma means delta can shift rapidly, often near at-the-money strikes close to expiration.

This makes gamma a key driver of volatility in option prices.

Theta (Θ)

Represents time decay — the amount an option loses each day, all else equal.

Options are wasting assets; as expiration approaches, time value shrinks faster.

Option sellers often seek to benefit from theta, while buyers must overcome it.

Vega (ν)

Measures sensitivity to changes in implied volatility (IV).

A higher vega means the option’s value rises more when volatility increases.

Since IV often spikes in uncertain times, vega is crucial for traders who position around events.

Rho (ρ)

Tracks sensitivity to interest rate changes.

While less relevant in low-rate environments, rho matters for longer-dated options.

Why the Greeks Matter

Taken together, the Greeks form a multidimensional risk profile. A trader isn’t just long or short — they are exposed to directional risk (delta), acceleration (gamma), time decay (theta), volatility (vega), and interest rates (rho).

The earlier options risk profile diagram illustrates how these forces combine in multi-leg positions. Each curve on the graph reflects the complex interplay of the Greeks, showing why mastering them is essential for managing sophisticated strategies.

Core Options Strategies

Options can be as simple or as sophisticated as a trader chooses. At their core, all strategies are built from just two instruments — calls and puts — yet when combined, they create a vast range of payoff structures.

Directional Strategies

Long Calls: Buying a call gives upside exposure with limited downside (the premium paid).

Long Puts: Buying a put provides downside exposure with limited risk.

These are straightforward but carry the burden of time decay (theta).

Income Strategies

Covered Calls: Holding the underlying asset while selling a call against it. This generates premium income but caps upside.

Cash-Secured Puts: Selling a put while holding cash collateral. If assigned, the trader buys the underlying at the strike price.

Risk-Defined Spreads

Vertical Spreads: Buying one option and selling another at a different strike in the same expiration. This defines both maximum risk and reward.

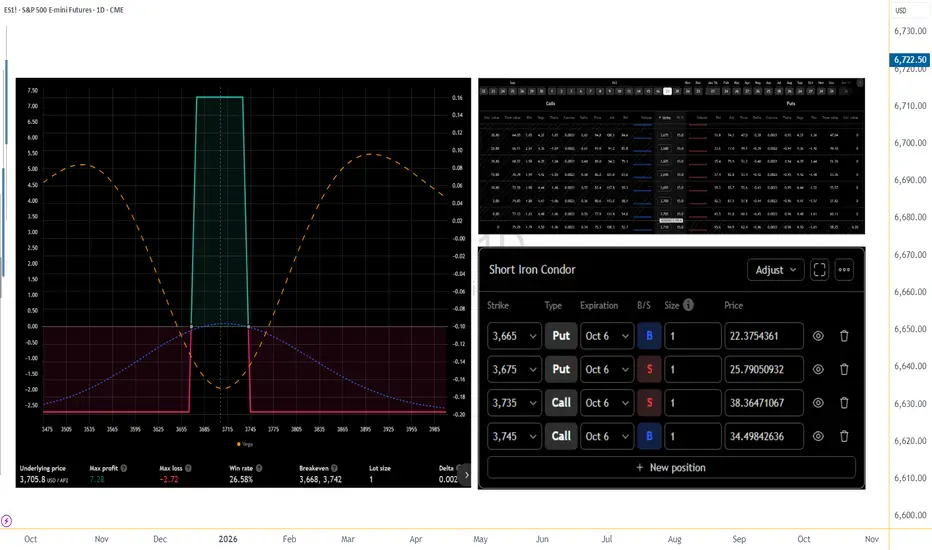

Iron Condors: A combination of spreads that profits if the underlying stays within a range. Risk and reward are defined upfront.

The above iron condor risk profile chart shows exactly how this works: profit is maximized in the middle range, while losses are capped outside the wings.

Why Structure Matters

Each strategy has its strengths and weaknesses, but the true value of options lies in their flexibility. Traders can design positions to fit directional views, volatility expectations, or income objectives — all with defined risk.

Options strategies are like tools in a kit: the more you understand their mechanics, the more precisely you can shape your market exposure.

Options on Futures

Most traders first encounter options through stocks, but options on futures open the door to even broader applications. While the mechanics are similar, there are key distinctions worth noting.

Underlying Differences

Stock options are tied to shares of a company.

Options on futures are tied to futures contracts — which themselves already embed leverage and expiration.

This layering adds both flexibility and complexity. A trader is essentially trading an option on a leveraged instrument.

Practical Use Cases

Hedging Commodity Risk: An airline might use crude oil futures to lock in prices, then overlay options to cap extreme scenarios while reducing hedging costs.

Speculating with Defined Risk: A trader bullish on gold can buy a call option on gold futures. The maximum loss is the premium, but the upside tracks leveraged futures moves.

Volatility Plays: Futures options often respond strongly to shifts in implied volatility, especially around key reports or geopolitical events.

Why They Matter

Options on futures give traders the ability to fine-tune exposures. Instead of committing to full futures leverage, a trader can scale in with options, controlling downside while keeping upside potential open.

They also broaden the range of strategies available. Futures already expand diversification; adding options introduces an entirely new layer of flexibility.

Index Options

Among the most widely traded options in the world are those based on equity indexes, such as the S&P 500 or Nasdaq-100. These instruments serve as essential tools for institutions and active traders alike.

Why Index Options Are Popular

Portfolio Hedging: Instead of hedging each stock individually, investors can use index puts to protect an entire portfolio.

Exposure Without Ownership: Index options allow participation in market moves without holding any individual company shares.

Liquidity and Depth: Index options often trade with deep volume and open interest, making them attractive for both large and small participants.

Volatility and the Options Surface

A key feature of index options is their relationship with volatility. The chart below — an implied volatility surface/skew diagram — shows how options with different strikes and maturities carry different implied volatilities.

Volatility Skew: Out-of-the-money puts often trade with higher implied volatility, reflecting demand for downside protection.

Term Structure: Near-term expirations may reflect event risk (such as earnings or Fed meetings), while longer maturities capture broader market uncertainty.

Why It Matters

Index options aren’t just directional bets. They are also instruments for trading volatility, sentiment, and risk itself. Institutions rely on them to hedge, while traders use them to capture shifts in implied volatility across strikes and expirations.

By understanding how skew and surfaces behave, traders can better interpret market expectations — not just where prices may go, but how uncertain participants feel about the path forward.

Risk Management with Options

Options provide unmatched flexibility — but that flexibility can tempt traders into overcomplicating positions or underestimating risk. Mastery comes from structuring trades with risk control at the core.

Defined vs. Undefined Risk

Defined-Risk Trades: Spreads and combinations such as verticals or iron condors cap both upside and downside. Maximum loss is known from the start.

Undefined-Risk Trades: Selling naked calls or puts exposes traders to potentially unlimited risk. While these strategies may generate steady premiums, one large adverse move can wipe out months or years of gains.

Managing Volatility Exposure

Volatility can shift rapidly, especially around earnings reports, central bank decisions, or geopolitical events.

A long option position benefits from rising implied volatility but suffers if volatility collapses.

A short option position gains from falling volatility but risks severe losses if volatility spikes.

Theta Decay and Time Management

Time decay (theta) erodes option premiums every day.

Buyers must ensure their directional or volatility edge is strong enough to overcome this drag.

Sellers must balance the benefit of theta decay against the risk of sharp, unexpected price moves.

Position Sizing Still Matters

Even defined-risk strategies can compound losses if oversized. Options’ leverage allows traders to control significant exposure with relatively small premiums, making discipline in sizing just as important as with futures.

The Core Principle

Options don’t eliminate risk — they reshape it. Effective risk management means choosing strategies where the risk profile matches your conviction, market conditions, and tolerance for uncertainty.

Common Mistakes New Options Traders Make

Options open powerful opportunities, but without structure, beginners often fall into predictable traps. Recognizing these mistakes is the first step to avoiding them.

Chasing Cheap Out-of-the-Money Options

Many new traders are attracted to options with very low premiums, believing they offer “lottery ticket” potential. While the payoff looks appealing, the probability of expiring worthless is extremely high.

Ignoring Implied Volatility

Price direction isn’t the only driver of option value. A trader might buy a call, see the underlying rise, yet still lose money because implied volatility dropped. Treating options as simple directional bets ignores one of their most critical dimensions.

Overusing Undefined-Risk Positions

Naked calls and puts can seem attractive because of the steady income from premium collection. But without defined risk, these trades can expose traders to devastating losses when markets move sharply.

Mismanaging Time Decay

Theta works against buyers, and new traders often underestimate how fast options lose value near expiration. Buying short-dated options without accounting for theta can erode capital even when the underlying moves in the expected direction.

Forgetting the Exercise and Assignment Process

Options on futures and equities alike can be exercised or assigned. New traders often overlook the obligations that come with short positions, leading to unexpected futures or stock exposures.

Takeaway

Every mistake above comes from misunderstanding what options truly are: instruments shaped not only by direction, but also by time, volatility, and structure. Avoiding these pitfalls is what separates those who dabble from those who progress toward mastery.

Conclusion: From Complexity to Clarity

Options may seem intimidating at first glance. The crowded options chain, the curved payoff diagrams, and the alphabet soup of Greeks can overwhelm even experienced traders. Yet within this complexity lies unmatched versatility.

Options allow traders to:

Define risk with precision.

Express bullish, bearish, or neutral views.

Trade volatility and time as independent variables.

Hedge portfolios against unexpected events.

The charts in this article — from the iron condor risk profile to the volatility skew surface — highlight the breadth of possibilities. They show why options are not a single strategy, but a toolkit that adapts to any market condition.

The challenge is not to memorize every strategy, but to understand how the pieces fit together: calls, puts, Greeks, spreads, volatility, and time. Once these elements stop being a mystery, options transform from a confusing maze into a structured path toward mastery.

This article completes our From Mystery to Mastery trilogy. We began with Trading Essentials, laying the foundation. We advanced into Futures Explained, exploring leverage and diversification. Now, with Options Explained, we’ve reached the most versatile and sophisticated layer of trading.

The journey doesn’t end here. Futures and options will always evolve with markets, offering new challenges and opportunities. But with a structured process, disciplined risk management, and the mindset of continuous learning, traders can move confidently — from mystery to mastery.

From Mystery to Mastery trilogy:

Options add a powerful layer of flexibility to trading, whether used for directional plays, income strategies, or hedging. Since many actively traded options are written on futures contracts listed on CME Group exchanges, it’s important to note that chart data can sometimes be delayed. For those who wish to analyze these products in real time on TradingView, a CME Group real-time data plan is available: www.tradingview.com . Traders focused on short-term options strategies, where timing and volatility shifts matter most, will find real-time access particularly valuable.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

05/05 SPX Weekly Playbook - GEX Zone Outlook🔮 What-If Scenarios for This Week – Based on GEX Structure until Firday

Last week’s market momentum pushed the S&P 500 up by almost 3%, effectively erasing the price gap left behind on Liberation Day. The index also strung together nine straight days of gains—something we haven’t seen since late 2004.

Meanwhile, implied volatility dropped significantly, with the VIX touching its lowest level since the holiday, falling to around 22.5.

Several factors seem to have fueled this bullish tone, including a more measured approach from Trump on trade policies and strong quarterly results from major tech names like Microsoft and Meta.

Still, the nature of the buying raises questions—was this a thoughtful rotation, or just a broad sweep of optimism?

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

🔄 Chop Zone: 5650 – 5670 (wide transition zone)

🔹 Gamma Flip: 5615

🔺 Key Call Wall: 5725 (5800 potential shift)

🔻 Key Put Wall: 5500 (5400 major support below)

🔼 Upside Path

IF > 5670 → transition cleared →

➡️ 5700 stall / reaction

IF > 5725 → call wall breached →

➡️ Path to 5750 / 5775 → stall at 5800 (largest net call OI)

IF > 5800 → gamma resistance breaks down →

➡️ 5825/5850 zone opens up

🔽 Downside Path

IF < 5615 → gamma flip triggered →

➡️ 5500 = battle zone (massive put wall + high negative GEX)

IF < 5500 → negative gamma squeeze likely →

➡️ Stall zone: 5450 → flush to 5400

IF < 5400 → high-volatility regime →

➡️ Possible acceleration to 5375 / 5340 depending on IV spike

⚖️ Neutral Setup

IF 5650–5670 holds → dealer hedging = balanced →

➡️ Ideal for non-directional spreads / theta plays

➡️ Wait for breakout confirmation above 5670 or below 5615

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

🔍 Final Thoughts

We’ve seen a sharp rally since the Trump trade war scare, with barely any meaningful pullback. The market appears to be looking for one—as a breath. Based on current GEX positioning, there’s significantly more downside hedging than upside, especially in the mid-term May expirations.

That doesn’t necessarily mean we crash—but it does mean that moves lower can accelerate faster, while upward breakouts may require more energy or time. In this environment, consider:

Bearish or neutral spreads (put debit spreads, call credit spreads)

Volatility-based strategies

Avoiding naked upside trades unless we see a strong reclaim of 5725+

Stay safe and adapt—GEX doesn’t tell direction, but it does tell where the fire might start, beacuse of reflexting to hedging activity.

04/28 Weekly GEX AnalysisDETAILED IMAGE:

Here’s what the charts and indicators are showing right now until Friday.

We are approaching a key breakout zone.

🐂 🟢 IF the market breaks above the white bearish daily trendline, the next bullish target could be between 5515–5680.

🟦 ⚖️ The chop area is between 5435–5515.

Expect more back-and-forth moves here if the breakout fails.

🐻🔴 Watch out: if the price drops below 5435 or 5425, there’s little support left.

This could trigger a sharp sell-off ("Bearish Armageddon" scenario).

GEX profiles remain positive 🟢 across all near expirations — for now — suggesting that underlying support still exists, but we need to monitor any changes closely.

IVRank is still relatively high (30.9), meaning options are priced with a decent amount of implied volatility.

🟢Short-term sentiment is currently bullish, with some speculative activity picking up.

This suggests that traders are expecting less volatility over the next month compared to what we saw in the past week.

However, if we look at institutional positions focused on longer-term expirations (especially beyond 30 days on SPX/AM maturities), the picture remains bearish 🔴 or at least highly volatile.

These players are still strongly hedging against downside risks.

This confirms the broader point:

Even though price action managed to recover to pre-tariff-announcement levels — with very low trading volume — we’re not out of the woods yet.

Until we can break and hold above the key resistance bearish trend with HIGH BUY VOLUME (aka. momentum), we shouldn't expect a strong, stable GEX profile across all expirations like we had in the past.

GEX Analysis & Options “Game Plan”🔶 Short- and longer-term perspective in a high IV, negative GEX environment

🔶 KEY LEVELS & RANGES

Spot: 221

Gamma Flip / Transition: around 250 (the turquoise zone on the chart)

– This zone typically marks a “power shift.” If price decisively breaks above 250 and holds, market makers’ gamma positioning could flip from neutral/negative to positive.

Put Support: 200

– A large negative gamma position has accumulated here, making 200 a strong support level. If it breaks, the downside may accelerate.

Call Resistance: 400

– A major long-term “call wall” where a significant amount of OTM calls are concentrated. It’s more relevant to LEAPS; currently far from spot, so not a realistic short-term target.

Call Resistance #2: 300

– A medium-term bullish objective, still above the 200-day MA. You’d need to be strongly bullish to aim for ~300 by May (e.g., going for a 16-delta OTM call).

Short-Term / Intermediate GEX Levels:

– There are gamma clusters around 220–230 and 250–260 . These areas often see higher volatility, possible bounces, or stalls (chop) due to hedging flows.

🔶 WHATEVER SCENARIO – SHORT TERM (0–30 DAYS)

A) Upside Continuation / Rebound

– If TSLA closes above 225–230 , the next target is 240–250 (transition / gamma flip).

– If it breaks above 250 and holds (e.g., successful retest), market makers may shift to “long gamma,” fueling a quicker move to 260–270 .

– Resistance: 250, 300, with an extreme LEAPS-level at 400.

B) Downside Move / Bearish Break

– If price dips below ~220 and sustains, the next targets are 210–200 (major put wall / negative gamma).

– If 200 fails, negative gamma may magnify the sell-off. It’s an extreme scenario but still on the table given high IV and macro/geopolitical risks.

– Support: 210, 200 — likely stronger buying interest near 200, possibly a short-term bounce.

– The options chain suggests near-term hedging via puts for this scenario.

C) Chop / Sideways

– If TSLA stays in 210–230 , market makers (short options) might benefit from high IV/time decay.

– Negative GEX, however, can trigger sudden moves in either direction; caution is advised.

🔶 LONGER-TERM FOCUS (6–12 MONTHS, LEAPS)

NET GEX = -61.97M (negative territory) suggests longer-dated positioning is also put-heavy or carries notable negative gamma.

HVL / pTrans = 250 is a key pivot; cTrans+ = 400 is distant call resistance. Between these levels, there’s a mix of put/call dominance.

If Tesla undergoes a fresh growth phase (AI, robotaxi, energy storage, etc.) and clears 250/300 , 400 could become the next significant call wall — but that’s more of a multi-month horizon.

🔶 STRATEGY IDEAS (High IV Environment)

1. Short-Term Bearish

– If you’re bearish and expecting TSLA to test 220–210, consider a bear put spread or net credit put butterfly (lower debit) to leverage high IV.

– Targeting 200, but keep in mind negative gamma may accelerate downside movement.

2. Medium-Term “Contra” Bullish (bounce to 250)

– If GEX suggests a bounce off 210–220, consider a bull call spread (e.g., 220/240) or a net debit call butterfly (220/240/250).

– Be mindful of sudden swings, as we remain in negative gamma territory.

3. Longer-Term Bullish (>3–6 months)

– A call butterfly with upper strikes around 300–350 offers capped debit and higher potential payoff if a bigger rally materializes.

– A diagonal spread (selling nearer-dated calls, buying further-out calls) exploits elevated front-end IV.

4. Neutral / Range-Bound

– If TSLA stays in 200–250 , you could use Iron Condors (e.g., 200/260) to benefit from time decay and any IV collapse.

– Exercise caution: negative gamma can generate abrupt, directional moves, making a neutral stance riskier than usual.

🔶 ADDITIONAL NOTES & “BIG PICTURE”

High IV & Negative GEX: TSLA has a track record of large swings. Negative GEX can intensify sell-offs, while forced hedging might trigger rapid rebounds.

Preferred Structures: With expensive premiums, spreads (vertical, diagonal) and butterfly configurations generally fare better than plain long options (less vulnerable to time decay).

Potential Catalysts: AI announcements, Autopilot breakthroughs, new product lines, and macro changes can swiftly alter market dynamics. Keep tracking GEX updates and news flow; TSLA tends to respond dramatically to fresh developments.

🔶 Bottom line: From 221 spot, watch 210–200 on the downside and 240–250 on the upside short term. Medium-term bullish target = 300 , while 400 remains a far LEAPS scenario. High IV + negative gamma = fast, potentially volatile moves — so risk management and spread-based approaches are crucial.

Gamma Exposure Analysis SPY & VXX SPY Resistance at 570. The 570 level in SPY likely corresponds to a high gamma concentration for 0DTE (zero days to expiration) options. At this strike, market makers short gamma (i.e., net sellers of options) at this level would dynamically delta-hedge by selling SPY as the price approaches 570, creating selling pressure and resistance. Next resistance level 575.

For VXX , the 48 level likely represents a put-dominated gamma zone: If market makers are net long puts, they would buy VXX as prices decline toward 48 to hedge against further downside, creating support. Next support level 46.50

Bitcoin daily analysis based on IBIT Gamma ExposureIf IBIT surpasses the 48.00 level (which serves as a pivot), Bitcoin could rally toward the key 0DTE level at 50.50 (daily target)

Gamma Exposure on SPXToday marks the first day in a long time where we can observe some green, bullish levels on gamma exposure. The daily GexView indicator displays thin green lines, which represent the gamma exposure of zero-days-to-expire contracts. The thick lines, on the other hand, represent the total gamma exposure across all expiration contracts. This is a promising first step, especially if these lines persist over the next few days and continue to develop further.

02/26 Special GEX Outlook: NVDA Earnings, GEX LevelsNVDA Earnings Announcement 🔥

NVIDIA reports earnings today, after market close, and this release could create significant movement. Let’s dive right into the charts and see what the technicals are telling us!

With earnings so close, I typically look only at the nearest expiration, which in this case is 02/28 (Friday).

The implied move (IV) is around 10%, or approximately 12 points in either direction. That’s what the market has priced in for this binary event.

Key Observations

The price is hovering around the Transition Zone and very close to the HVL (High Volume Level) around 130–132.

This suggests the market maker is trying to remain delta-neutral leading into earnings. Once the report hits, expect potential volatility on Wall Street! 🚀

GEX Levels for Friday

🔴 Bearish Scenario

The bottom of the Transition Zone is at 126.

If price drops below 126, the next major put support is at 120 and extends to 115 (a negative gamma squeeze zone).

In other words, a breach of 126 could lead to a quick slide down to 120.

🟢Bullish Scenario

Major call resistance stands at 150, with a secondary call wall at 145.

Above 133 (top of the Transition Zone), calls dominate, meaning the path to 145–150 could open up if we break above the HVL.

Longer-Term Perspective 📊

We’re still in an overall uptrend, but history shows that even with positive surprises on 2 out of the last 4 earnings calls, the market had already priced in those expectations—often leading to a sell-the-news reaction.

I do not recommend trading right before the earnings with a binary mindset. It’s like walking into a casino and putting all your chips on red or black—it’s pure gamble! 🎰

Call pricing skew has been on a downward trend since DeepSeek (likely referencing a volatility event), indicating that call butterflies might not be as attractive on NVDA now as they were in the past few weeks.

Fundamental Analysis 💡

NVIDIA is a hype stock, much like TSLA was a few years back. Its current price has factored in a lot of the future potential.

Based on FastGraphs and other valuation tools, NVDA 1.44%↑ seems overpriced relative to its underlying performance.

A correction might bring it closer to fair value (the “green zone”), like it did in October 2022.

Until then, I’m not considering it for a 5+ year long-term investment—no matter what the short-term price action is.

Conclusion & Post-Earnings Strategy 👉

We simply don’t know which direction NVDA will move after earnings.

Typically, implied volatility (IV) expands before earnings (~90% of the time) and collapses for the nearest expiration immediately afterward.

Even IV on farther-dated expirations can continue to drift lower for a week or two post-earnings.

My Plan

Since I haven’t opened a time spread trade, I’m focusing on post-earnings setups.

If NVDA makes a huge move (breaking out of the 120–150 range), I’ll likely wait at least one more day before placing any new position to let open interest (OI) restructure.

April expirations will be more interesting for me after the dust settles.

[02/03] SPX Weekly GEX OutlookSPX shifted into a strong sideways trend after recent market whipsaws, but premarket today saw a sharp sell-off.

Now, let’s break down the GEX levels set for Friday’s weekly expiration (first weekly expiry). These are already reflected in today’s GEX data—check them on your indicator!

COMMENT: This week, we’ve started updating our seamless GEX & options indicators before the market opens . This has been a long-standing request from users—especially 0DTE traders, who will likely benefit the most.

Key GEX Levels for SPX

📍 Highest Positive Call Wall (Call Resistance): 6075

Acted as resistance last Friday, as it often does initially.

📍 Sideways Zone: 6000-6070 (Transition Zone with GAMMA flip)

Wide Transition Zone → Expect high volatility or slow drifting within this range.

Easy flow between positive and negative GEX profiles, meaning potential sharp moves in either direction.

📍 Put Support (Sum 4DTE): 5900

Very deep support—market is clearly pricing in fear of a potential future drop.

📌Below 6000, there are only negative NetGEX strikes down to 5900, which signals a lack of strong support until that level.

What This Means for the Week

📊 SPX opened (gapped down) in negative GEX territory—if buyers don’t reclaim this zone, we are in for a highly volatile week, potentially with a spiking VIX.

🚫 No reason for bullish optimism unless we break above 6070—until then, expect uncertainty and potential downside pressure.

PS: FINAL GEX ZONE COLORING SHEET

[02/03] TSLA GEX Outlook for February expiration📌 Key Levels & GEX Insights

Gamma Flip Zone: ~400 (until Febr expiration)

Tight Transition Zone, Wide Clear Movement Range

Above 420 Call Resistance : Every strike has positive Net GEX, meaning a return to this range would likely support further balanced upside or sideways movement.

Below 375 : The next PUT support is at 350, so a break below this level could open the door for a deeper drop.

There are 3 weeks until expiration. IV and IVR remain high even after earnings.

Despite today’s selloff, the high call pricing skew is still attractive if we want to collect credit.

In this case, a call butterfly or broken-wing call butterfly could be worth considering—but strictly based on GEX levels.

PS: FINAL GEX ZONE COLORING SHEET

[02/03] AAPL GEX Outlook for February expirationWhile iPhone sales faced some challenges, Apple’s diversified revenue streams and high-margin services business continue to showcase the company’s resilience. The stock initially reacted positively after earnings, but the broader market disagreed during open hours, leading to a sell-off on Friday.

Now, let’s analyze the GEX chart together. For NASDAQ:AAPL , I’ve chosen the First Monthly Expiration (Febr 21), as multiple high gamma exposure expirations align with this date. Since we trade stocks and ETFs over a broader timeframe, rather than day trading, this is the most relevant perspective.

Key GEX Levels & Market Implications

📌 Uncertainty Below 250

Friday’s sell-off and today’s premarket action have weakened the outlook.

GAMMA FLIP ZONE:

AAPL is currently in the 230-237.5 Transition Zone, meaning price action can shift quickly in either direction.

📌 Break Below 230?

A move below 230 would open the door to 220.

📌 Put Support at 220

Implied volatility (IV) remains high, making this an attractive setup for a potential neutral post-earnings trade.

With a 220-250 range, we remain well inside the OTM 16-delta zone for March expiration, which is ideal for premium selling strategies for high IV.

PS: FINAL GEX ZONE COLORING SHEET

[01/20] GEX Outlook: Decision, Key Levels and Looming VolatilityLooking at the GEX levels through Friday, we can see that since mid-December, the market has been moving in a slightly downward channel.

Above 6000–6025: A call gamma squeeze is expected.

Between 5925 and 6000: A sideways “chop zone.”

Below 5925: The high-volatility zone begins, with 5800–5850 acting as our major support/resistance level characterized by heavy put dominance.

Below that level lies a “total denial zone.” We’ve seen this scenario before—think back to the red candle on December 18, when the price broke below that threshold. This “red zone” is currently around 5800, so below 5925 we can anticipate large-amplitude moves.

At this point, the market still does not seem worried about significant volatility. Until Friday, all NETGEX values for every expiration are positive , so market participants are pricing in more of a sideways movement. We haven’t yet seen a big pickup in volatility.

I’m not pessimistic, but keep in mind that Trump’s inauguration might usher in a high-volatility period—something the market and many retail traders haven’t experienced in a while. Better safe than sorry.

Weekly GEX Insights: 01/13 SPX dropTotal Correction? What Can an Options Trader Do in This Situation? How Far Might We Fall This Week? We’ll tackle these questions in this week’s options newsletter!

It looks like the new president hasn’t even been sworn in yet, but the market is already reacting with fear to every statement he makes. Last week’s economic data didn’t help ease those concerns either.

SPX Weekly Analysis

Friday’s red candle set a bearish tone heading into this week. Everyone is predicting and pricing in a potential market apocalypse, and I keep getting the same question: “Greg, how far can we fall?”

My answer remains the same: we can fall indefinitely—nobody can know for certain ahead of time.

What we can do, however, is analyze our charts and use the our weekly GEX profile to identify the key levels, so we can better understand the market’s dynamics.

Examining expirations through Friday, every NETGEX profile is negative , so we can expect volatile movements this week. We’re currently trading below the HVL level, which means that market makers are likely to move in tandem with retail traders. This typically results in bigger swings.

We already saw this heightened volatility last week—just look at the size of the candles, and you can tell how quickly sentiment can shift.

Below 5965 (the HVL level), we are in a high volatility zone what lies underneath?

1st Support Range: 5780–5800

5800: Currently the strongest PUT support level on the downside. A correction may pause here due to profit-taking.

Right beneath this level is the previous gap-fill zone. Remember, these areas function as ranges rather than single lines, as I’ve highlighted down to 5780. This could easily be a take-profit target for traders playing gap fills—an approach that’s quite popular.

2nd Support Range: 5700–5650 (Very Strong)

Starting at 5700: We encounter another robust PUT support zone.

This area is reinforced by previous lows, previous highs, and the 4/8 grid boundary from our indicator.

Even if nowhere else, many expect at least a local rebound to occur within these levels.

Putting it all together, it’s clear that the weekly trading range is shaping up to be roughly between 5680 and 5965, expecting big & volatile moves.

Remember, CPI and PPI data are coming out on Tuesday and Wednesday, which could trigger additional volatility.

When looking at SPX, SPY, or /ES futures, my opinion is that the rapidly spiking implied volatility (IV) during a market drop, along with a PUT pricing skew, can present favorable opportunities for options traders. The distance to the strongest lower support zone is around 100–150 points, so you could:

Trade directionally for the short term—hoping to be either right or wrong quickly, or

Try to profit from the market situation in a more strategic way (which is what I typically do).

Personally, I prefer the second approach:

I’ll open short-term (a few days) credit put ratio spreads for a small credit, which gives me a wide breakeven range and a big “tent” on the downside.

11/18 Volatility Zones: Gamma Squeeze, Chop, and Support LevelsWeekly GEX Levels for SPX:

The SPX analysis from last week’s free newsletter seems to have played out well. If you recall, based on the weekly GEX levels, there were no significant gamma levels below 5950. As soon as the price dropped below that, we saw the anticipated red gap-down to 5850 by Friday.

With Friday's move, SPX shifted from a positive NETGEX range to a negative one:

Let’s not forget: a negative gamma range means that market makers move in the same direction as retail traders, increasing the likelihood of stronger price movements, regardless of the market’s direction. Until the 5900 HVL level is reclaimed, I don’t expect this to change. As we saw today, there was a nice bounce off this level with a rejection, making it a tough resistance to break.

If it does manage to break through, there’s currently a call gamma wall at 5925. Clearing this level could open the door to higher ranges again.

While the week is still long, if the market fails to regain stability by Friday, breaking below the major 5850 PUT gamma wall could lead to another rapid move down, similar to last Friday, targeting the 5810–5800 range.

Gamma Squeeze Zones for SP:SPX & AMEX:SPY this week:

Above 5925:

Gamma squeeze zone, where upward momentum can accelerate.

Chop Zone:

Between 5900 and 5930: Sideways movement expected, with the market consolidating in this range.

High Volatility Zone:

Below 5900: High volatility zone, indicating increased intensity in market movements.

Market Makers Hedging Behavior Shift Zone:

Around 5900: A critical zone where market makers may adjust their hedging strategies.

Call Resistance:

Below 5940: Reduced volatility expected as call resistance limits upward movement.

Put Support Levels:

Around 5850: Highest negative NETGEX/PUT support level.

Between 5810 and 5800: Additional put support levels acting as key supports; if 5850 broken, turbulence is expected.

IV and Skew Data:

IVR: 16.9 increasing

IV Average: 14.9 increasing

PUT pricing skew: 31.5%

GEX levels of SPX for Weekly Option TradersAlthough the SPX is currently trading within a relatively neutral positive gamma range, it’s worth taking a closer look at what the week might hold.

This week, SPX is moving between critical resistance and support levels, which are showing significant options activity. The 5900 level is the key CALL resistance, acting as the gamma wall for the next 7 days (7DTE) . This suggests that as long as the price remains below this level, it will face strong resistance in moving higher. If the market breaks through this level, it could signal a bullish breakout, leading to increased turbulence.

🟨 DETAILED VIEW:

In case of a breakout, keep an eye on the second weaker CALL wall at 5925 and the third weaker CALL wall at 5940, which are the next potential resistance levels once the market moves past the 5900 gamma wall. These levels could play a pivotal role in the price’s upward movement and indicate further buying pressure.

🔶 HVL Level and Gamma Environment: 5830

The 5830 level represents the High Volatility Level (HVL), which determines whether we are in a positive or negative gamma environment. If SPX closes below this level, we enter the negative gamma zone, which could lead to increased market volatility. This could result in sharper price movements during the week if this level does not hold. In that case, the PUT supports come into focus.

The 5750 level marks the strongest PUT support, providing substantial downward support for the market. However, before reaching this level, it’s important to consider the emerging PUT wall at 5765, which may stop the price from falling lower. This could act as an intermediate support, slowing or even halting a decline before the 5750 level comes into play.

🔶 Implied Volatility and Time-Based Strategic Opportunities NOW

The decrease in implied volatility, as shown by the IV and IVx indicators, signals a calmer market environment. Based on IV rank and average IV levels, volatility is running lower, which presents good opportunities for various spread strategies, especially time spreads that can be optimized between the 11/01 and 11/04 time frame.

Key levels above could fuel further market movement throughout the week if a breakout occurs. CALL/PUT gamma levels on the options chain strongly outline the potential resistance and support levels, but these levels can change dynamically, especially if SPX breaks through the 5900 level.

🔶 SPX Key Levels This Week:

5900 CALL resistance – Main gamma wall, strong resistance.

5925 and 5940 – Second and third weaker CALL walls, offering additional resistance if broken.

5830 HVL – Key level determining the gamma environment.

5765 PUT wall – Emerging intermediate PUT support, which could slow a decline.

5750 PUT support – Strongest PUT gamma wall and support.

Keep these levels in mind throughout the week, as they will likely influence market movements and the volatility environment. By applying the right options strategies, this information can help you structure profitable positions.

11/04 Weekly SPX Market Analysis with seamless GEX levelsThe U.S. presidential election is on November 5, and this week we can expect increased volatility due to the uncertainty. For options traders, one thing is certain: volatility will likely rise leading up to the election, peak around the results, and then gradually subside as the “fireworks” end. It’s essential to consider this in every trading decision.

While the current Implied Volatility (IVx) isn’t extremely high, the IV Rank (IVR) is quite strong at 41, and this is likely to remain due to the increasing uncertainty. Based on the blue OTM (Out of The Money) delta curves, the market is currently pricing in a strong downward movement for the week, aligning with the negative gamma zone and negative gamma profile. For a bullish shift, we would need a strong push above 5845 to enter positive gamma territory (HVL level is the battleneck).

⏩ The 5700 level is a key PUT support across multiple timeframes. If this level breaks, turbulence is expected, with increased downward movement likely to follow, first to 5650 and potentially down to 5600, where larger PUT gamma walls are located.

⏩ According to the 16-delta OTM curve, a close above the previous all-time high is less likely. If there’s a strong breakout to the upside, the positive gamma threshold stands at 5850, and above this, buyer pressure could extend up to 5925.

⏩ I consider the 5700-5845 range as a “chop zone,” where high volatility is expected this week. In this zone, bears and bulls will be in constant battle, and I do not expect a clear trend. I focused on Friday’s expiration in this analysis, as market outlooks remain highly uncertain ahead of the election.

The strong PUT pricing skew is a natural phenomenon and is expected to increase, especially since we are in a negative gamma zone. For December expirations, PUT options cost nearly twice as much as CALL options, as shown by our oscillator for 12/20 expiry.

There’s already ~6% IV backwardation between the 11/08 and 11/11 expirations, making this ideal for time spreads. However, caution is warranted—front-month PUT calendar and diagonal spreads can easily turn negative if front IV rises more than back IV.

Remember! It’s not mandatory to trade during highly uncertain periods! Staying out of the market is also a position, and sitting in cash is actually the safest choice, especially in a volatile week like this.

⏩ You can check my previous week's analysis, every one was accurate, I hope this one will useful too.

10/28 SPX

10/21 SPX

10/14 SPX

10/28 QQQ

10/14 QQQ