Can L3Harris Justify Its Nearly 40x Price-to-Earnings Premium?L3Harris Technologies has positioned itself as the "Trusted Disruptor" in the global defense landscape, bridging the gap between traditional aerospace giants and agile technology innovators. Operating across space, air, land, sea, and cyber domains, the company aligns with the most critical national security priorities at a time when global defense spending is projected to reach $2.6 trillion by the end of 2026, an 8.1% increase over 2025 levels. The geopolitical tailwinds are substantial: the war in Ukraine has prompted massive European rearmament, with Russia spending nearly $157 billion on defense in 2025 alone and NATO members targeting 5% of GDP for defense by 2035. Meanwhile, China's military expansion is driving unprecedented spending across the Indo-Pacific region, with Asia-Pacific defense budgets now exceeding $530 billion annually. L3Harris is strategically positioned to capture these opportunities through its global reach and technological edge, having recently secured a $2.2 billion contract for Korea's Airborne Early Warning & Control system.

The company reported that 2025 was a "clear inflection point" with full-year revenue of $21.9 billion, a 3% increase and even stronger organic growth of 5%. Its book-to-bill ratio of 1.3x signals a record order pipeline, and the company's aggressive cost management drove adjusted segment operating margins to 15.8% for the full year. However, fourth-quarter results revealed complexities: revenue of $5.6 billion missed forecasts by 2.95% due to a 43-day government shutdown that delayed contract awards and export approvals. Despite this, adjusted EPS of $2.86 beat consensus estimates, reflecting the success of the "LHX NeXt" operational excellence initiative. The stock slipped 3.7% following the earnings announcement, as management's 2026 guidance of $11.30-$11.50 per share fell below analyst expectations of $12.44, raising concerns about supply chain complications and program turbulence.

A transformative development emerged in early 2026 with the Department of War's launch of its "Acquisition Transformation Strategy." L3Harris became the first partner in this novel framework, receiving a $1 billion investment in its Missile Solutions business through a convertible preferred equity structure. The company plans to IPO this unit in the second half of 2026, creating a pure-play missile solutions provider focused on critical programs like PAC-3, THAAD, Tomahawk, and Standard Missile. Beyond munitions, L3Harris continues to advance cutting-edge aerospace and mission systems, including the AERIS next-generation AEW&C platform, the MC-55A Peregrine multi-intelligence aircraft, and autonomous systems ranging from the T7 unmanned ground vehicle to hybrid VTOL aircraft developed with Joby Aviation. With a global patent portfolio of 3,908 patents, over 36% currently active, and deep expertise in cybersecurity, space exploration, and counter-unmanned systems, L3Harris remains a cornerstone of the modern defense industrial base. However, investors must weigh the company's exceptional positioning against its rich valuation of nearly 40x P/E, which suggests the market has already priced in significant future success, leaving little room for execution missteps.

L3harris

Can L3Harris Redefine Defense and Space Frontiers?L3Harris Technologies stands at the crossroads of innovation and resilience, captivating investors and strategists with its bold vision. JPMorgan’s recent price target hike to $240 reflects confidence in its focus on margin expansion and cash flow, spotlighted during its investor day. Yet, this financial optimism intertwines with ambitious proposals—like doubling the EA-37B Compass Call fleet—challenging fiscal realities while addressing Indo-Pacific threats. What if a company could turn budgetary constraints into catalysts for growth? L3Harris dares to answer, blending pragmatism with a forward-leaning stance that intrigues and inspires.

On the technological front, L3Harris pushes boundaries with AI-driven autonomy and precision firepower. Its partnership with Shield AI fuses the DiSCO™ system with Hivemind software, promising real-time adaptability in electromagnetic warfare—a leap that could redefine battlefield dominance. Simultaneously, breakthroughs like long-range precision fires from VTOL platforms and rugged EO/IR systems for land missions showcase a relentless drive to equip warfighters for multi-domain challenges. Imagine a future where machines anticipate threats faster than humans can blink—L3Harris is crafting that reality, urging us to question the limits of human-machine synergy.

Beyond Earth, L3Harris powers NASA’s Artemis V with the newly assembled RS-25 engine, merging cost efficiency with cosmic ambition. This duality—mastering defense while reaching for the stars—positions the company as a paradox worth pondering. Can one entity excel in the gritty pragmatism of war and the boundless dreams of exploration? As L3Harris navigates tight budgets, evolving threats, and technological frontiers, it challenges readers to envision a world where resilience and imagination coexist, daring us to rethink what’s possible in a single corporate footprint.

Raytheon - A Potential Earnings Pump To WatchEveryone wants to get rich quick. Because getting rich quick means you:

a) Get rich

b) Quick

Then you can wear big ugly sunglasses, a crappy t-shirt, flipflops, sit on the beach, eat a lot of meat, drink a lot of alcohol, and be promiscuous with women.

This is the modern human's dream, right?

And so everyone loves to speculate on potential earnings pumps and dumps.

There really is more to aim for in life.

Raytheon is one of the U.S. Military Industrial Complex cornerstones and is more or less a weapons mill for the NATO proxy war in Ukraine, which is of note because of the recent escalations of the conflict and how it can affect the U.S. Petrodollar, and thus bonds, oil, gold, equities, everything.

DXY - The US Petrdollar And The "Prigozhin Coup" In Russia

Geopolitically, the conflict between China and the International Rules Based Order is heating up. The current edict is to "de-risk but not decouple" from China (notice they never say "from the Chinese Communist Party"?).

In mid-June CEO Hayes was quoted by the propaganda machines as stating that decoupling from China was pretty much impossible because of all the parts and components that are manufactured in the mainland.

What this means, if you ask me, is that going forward, certain companies are going to have a very hard time meeting their target EPS and revenue estimates.

Raytheon may very well be one of them, as foreshadowed by a salvo of sanctions the Xi Jinping administration placed on them and Lockheed Martin.

The situation in China is very volatile right now. The IRBO wants control of China when the CCP falls. Xi Jinping and the other nationalists want to make sure that outside forces do not steal the motherland.

And so one day soon, we may find that Xi has thrown away the CCP in the middle of the U.S. night, and the markets will have themselves a series of consecutive red days like we've all never seen before.

Xi can weaponize the crimes against humanity that the Party and the Jiang Zemin faction have committed in the persecution of Falun Gong that started on July 20, 1999, and use the truth to protect both himself and China.

Organ harvesting and genocide of a group of 100 million spiritual cultivators with upright faith is certainly enough of a weapon to handle all the threats the motherland can be facing.

So why do you care about this if you're trading Raytheon?

Because a basic principle of markets is they go up when big money is selling and go down when big money is buying.

Raytheon and other military companies ironically never really pumped following the QE recovery from the COVID pandemic dump.

It wasn't until the Ukraine War began that Raytheon finally ran the highs.

And then it retraced.

That kind of retrace is actually really bullish and what bulls should want to see if they want their $145 billion~ company to become a $1.4 trillion company.

But the problem with the theory is more manifest on the weekly charts:

31 weeks of ranging and no breakout is not bullish.

And yet, after taking lows, it continues to recover. The most notable price swing is the $105 to $92 leg that just occurred.

I feel that Raytheon has some fundamental hidden bearish divergences to it and this is why it has traded this way all along, with the ultimate purpose of selling a lot high, and then selling it all above the all time high.

This hidden divergence, I think, is that U.S.-based companies may find themselves cut off from the Chinese supply chain in the very near future.

Only to tip all the bulls on their backs like stranded turtles and then dump and dump and dump and dump and not come back.

So I believe that with the setup at hand, the catalyst is actually the July earnings.

But if you look back at previous earnings, Raytheon doesn't have major pumps. It can go a bit and then it will run after.

Implied volatility on options for the July 28 expiry are only 20%, slightly higher than the 17% average.

But before we get there, I expect we're going to see prices return to the $92-93 range and give the best buying opportunity.

The catalyst for this, I believe, will simply be market-wide correction, which I outline in the following two posts:

Nasdaq - The Great Bear Trap

And

SPX/ES - An Analysis Of The 'JPM Collar'

In summary, there will be a shakeout in equities that will probably not be long lived, even if it's violent.

And after that, things will make their final run up, many of which will set new highs or new 52W highs, etc.

What's left for the remainder of 2023 and the start of 2024 doesn't look like it's going to be very pleasant, to speak frankly.

So make sure if you see Raytheon at a new high, you don't go getting ahead of yourself, longing the top.

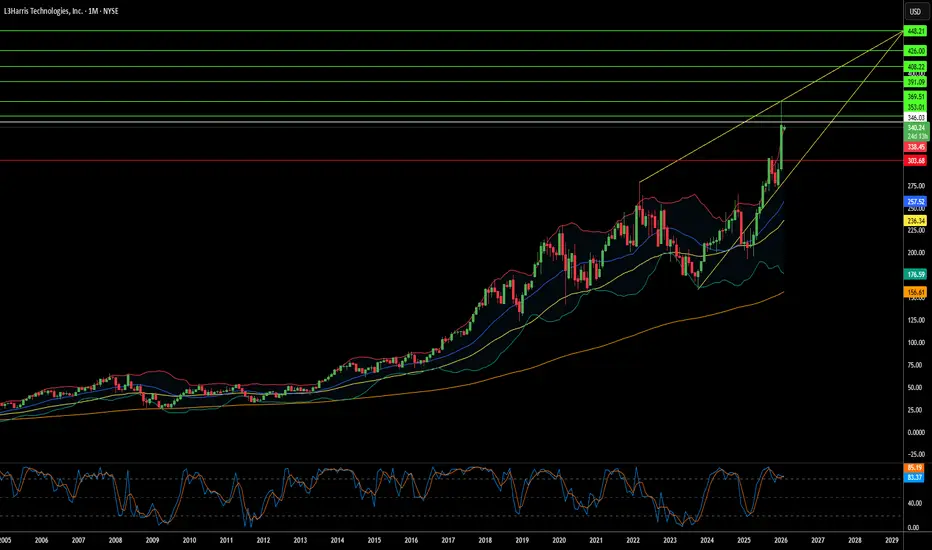

L3Harris up for a new uptrend as it bags a $500 million deal?I believe L3Harris is poised to go up the next couple of months. Yesterday showed a high volume up bar during the pullback to the horizontal support line.