LULU

LULU HOLIDAY LONGLULU has been falling hard in the past few months/weeks, down to support from March 2020 at $160~

With support from the bottom of the channel on this downtrend also meeting the support from over 5 years ago we see a confluence of support.

Also with a rising MACD and a rising RSI showing signs of volume and interest at this HUGE support line, I see an approximate 15%-35% return on investment.

The Financials on LULU also look very good with a P/E of 11.62 and little debt sitting at $1.76B. I find this to be a good thing because they have $1.16B of cash equivalents and a market cap of over $21B so little to no stress in the financials

I am not a financial advisor, and the information in this post is for educational or discussion purposes only. Please do your own research and consult a licensed professional before making any investment or trading decisions.

New All Time Highs - Bullish Price ActionToday the S&P500 made new all time highs.

It was a perfect breakout trend day and breakout.

Today we were able to trim and take profits on some of our long exposure.

We trimmed and sold NASDAQ:AMZN NYSE:SNAP NASDAQ:TEM NYSE:SMR

When the market is giving you all time highs and higher highs its always a good time to pair back longs.

Tomorrow we have some employment data that could gap the market higher.

If we can confirm a weekly chart breakout the probabilities of hitting 7k on spx is very likely.

Moon City Incoming! $250! NEXT!Price action has been very bullish over the past few days and if this 4HR demand holds (Red box), $250 can be next!

Calculate Your Risk/Reward so you don't lose more than 1% of your account per trade.

Every day the charts provide new information. You have to adjust or get REKT.

Love it or hate it, hit that thumbs up and share your thoughts below!

This is not financial advice. This is for educational purposes only.

$LULUShares of the athletic apparel retailer Lululemon (NASDAQ: LULU) surged by 4.1% during morning trading, propelled by positive earnings results from fellow retailer Dollar General. The discount retailer reported third-quarter net sales of $10.6 billion, a 4.6% year-over-year increase, driven primarily by improved customer traffic. As a result, Dollar General proceeded to raise its full-year financial guidance, signaling stronger-than-anticipated operational performance.

This optimistic report from a major national retailer was interpreted by the broader market as a sign of resilient consumer spending, particularly among value-conscious shoppers. Positive sentiment often flows through to related sectors, and in this case, it provided a tailwind for discretionary and apparel names—including premium brands like Lululemon—by easing fears of a near-term consumer pullback.

After its initial jump, Lululemon’s shares moderated slightly, closing the session at $189.71, still up 3.2% from the prior day’s close.

What Is the Market Telling Us?

Lululemon’s stock has exhibited notable volatility over the past year, with 13 separate moves greater than 5%. In this context, today’s advance of over 3% suggests the market views the broader retail sector data as meaningful—though not necessarily transformative for Lululemon’s own fundamental outlook. Rather, the move reflects relief and a reassessment of macroeconomic risk, as evidence of sustained consumer activity helps offset concerns about discretionary spending erosion.

This follows another recent positive move just 9 days prior, when shares gained 3% after analysts at BTIG reiterated a "Buy" rating ahead of Lululemon’s upcoming third-quarter earnings. BTIG maintained its price target of $303 per share, citing undervalued sentiment and expectations that results would meet or exceed guidance. That outlook was further supported by unusual bullish activity in the options market, indicating informed or speculative positioning in anticipation of a positive catalyst.

Technical Perspective and Price Targets

From a chart analysis standpoint, Lululemon’s price action is being monitored within a Fibonacci extension framework, which outlines the following upside take-profit targets:

First Target: $221.64 (0.236 Fibonacci level)

This represents the initial significant resistance zone, a breakout above which would signal regained bullish momentum.

Second Target: $260.21 (0.382 Fibonacci level)

A move to this area would indicate a stronger recovery trend and align closer with analyst price objectives.

Third Target: $291.38 (0.5 Fibonacci level)

This level serves as a more ambitious benchmark, approaching the upper range of analyst valuations and reflecting a scenario where both operational execution and market sentiment improve markedly.

Conclusion

In summary, today’s rally in Lululemon shares was less about company-specific news and more a sympathetic reaction to positive sector-wide data from Dollar General. It underscores the market’s ongoing sensitivity to consumer health indicators and its tendency to reprice discretionary stocks based on broader retail trends. While the move does not alter Lululemon’s core business narrative, it does reflect a slightly more favorable trading environment ahead of the company’s own earnings report. Investors will now watch to see if Lululemon can convert this macro-driven lift into sustained momentum by delivering results that validate both the recent analyst confidence and the technical pathway toward higher Fibonacci targets.

LULU 1D - stretching into a comebackOn the daily chart of Lululemon Athletica (LULU), a clean AB=CD pattern is forming, signaling a potential end to the correction and the beginning of a new upward wave. The price has tested the strong buy zone between 164–167, aligned with a major daily support level and rising volume - a classic setup indicating that buyers are regaining control.

Technically , the structure is highly symmetrical, RSI shows a bullish divergence, and the 50-day moving average is starting to turn upward - all suggesting a possible trend reversal. The first upside target for this pattern is $230, followed by a second target at $340, which corresponds to the 1.272 and 1.618 Fibonacci extensions.

From a fundamental standpoint, Lululemon remains a powerhouse in the premium activewear market, maintaining strong brand loyalty even amid competition from Nike and Alo. The company continues to expand its men’s line and footwear segment, which now accounts for over 25% of total revenue. International growth remains robust, with new stores opening in South Korea, the UAE, and Germany. Lululemon’s shift toward higher-margin online sales and more efficient logistics continues to strengthen its profitability.

In the latest quarterly report (September 2025), revenue grew by 9% year-over-year, and EPS came in above Wall Street expectations. High customer retention - over 90% repeat purchase rate - and stable gross margins create a solid foundation for a mid-term recovery in the stock.

Tactical plan: watch for entries within the 164–167 buy zone, consider partial profit-taking near $230, and target $340 if momentum extends. Just like in yoga, patience and balance lead to the best results.

Lululemon Athletica | LULU | Long at $165.00Lululemon $NASDAQ:LULU. If you don't think the US is in a recession, examine most retail stocks right now. But this doesn't mean doom and gloom are here from a US government/news narrative - in fact, the complete opposite. AI and tech are solely propping up the US stock market ... but pay no attention to the issues behind the curtain! Once interest rates start dropping, trading and investing are going to get wild before the cracks open up.

Okay, off my soap box...

NASDAQ:LULU entered by "crash" simple moving average zone (green lines) today after earnings. Competition is finally catching up to the company, but expansion into China and other foreign areas *may* revive them in the next 1-2 years. While most analysts are relatively bullish, I'll stay centered. I wouldn't be surprised if the stock dips into the $140's and $150's in the near-term. Bigger news will have to come out for me to stay long-term, but I'm holding here or even lower. Additional entries will be made in the $140's-$150's to swap out the position I just made at $165.00 for the future.

Thus, at $165.00, NASDAQ:LULU is in a personal buy zone with the risk of a continued drop to the $140's and $150s. Christmas rally potential...

Targets into 2028:

$185.00 (+12.1%)

$197.00 (+19.4%)

Quant Signals V3LULU Weekly Signal — Contrarian Call Play LULU Weekly Signal | 2025-12-09

Instrument: LULU

Direction: BUY CALLS (Contrarian)

Confidence: 58% (Low conviction)

Expiry: 2025-12-12 (3 days)

Strike Focus: $180.00

Entry Range: $11.75 – $12.45 (Mid: $12.10)

Target 1: $14.80 (+25%)

Target 2: $16.65 (+40%)

Stop Loss: $9.50 (-20%)

Position Size: 2% of portfolio

Weekly Momentum: NEUTRAL (+0.22% 1W)

Options Flow: Bearish (PCR 2.61 → heavy put buying, contrarian opportunity)

Max Pain: $180.00

Analysis Summary

Katy AI Prediction: Gradual upward movement to $184.45 by expiry (+0.96%)

Technical Analysis: Price near weekly highs, VWAP $184.73, resistance $185, support $180

News Sentiment: Neutral, Telsey Advisory maintains $200 target (+9.5%)

Risk Level: MODERATE — low conviction trade; tight stop recommended

Competitive Edge: Contrarian call vs extreme put flow; aligned with Katy AI upward bias

Key Notes

Low conviction trade — monitor closely

3-day expiry → time decay risk

PCR 2.61 indicates bearish sentiment — opportunity for short-term upside

This can hit 40sBearish. Bearish Bearish !!! Falling knife ! $40s coming. Will buy when it hits high 30s and low 40s for a jumpt towards 80s. All the best !!

It can have some support around 115 and may jump for some time before it hits 40s...

Not a financial advise.

LULU HOLIDAY LONGLULU has been falling hard in the past few months/weeks, down to support from March 2020 at $160~

With support from the bottom of the channel on this downtrend also meeting the support from over 5 years ago we see a confluence of support.

Also with a rising MACD and a rising RSI showing signs of volume and interest at this HUGE support line, I see an approximate 15%-35% return on investment.

The Financials on LULU also look very good with a P/E of 11.62 and little debt sitting at $1.76B. I find this to be a good thing because they have $1.16B of cash equivalents and a market cap of over $21B so little to no stress in the financials

I am not a financial advisor, and the information in this post is for educational or discussion purposes only. Please do your own research and consult a licensed professional before making any investment or trading decisions.

Premium Athleisure Brand with Strong Consumer Loyalty: BUYBuy Reason: Lululemon’s focus on quality, lifestyle branding and global expansion supports rapid revenue growth. Its innovation in product lines and strong direct-to-consumer channels contribute to robust earnings potential.

$NKE Inverse Head and Shoulder $117 to gap fillThe chart is currently forming a classic Inverse Head and Shoulders pattern, which is a bullish reversal setup. The left shoulder and head have already been established, and the right shoulder is in development, suggesting a potential breakout to the upside. The neckline resistance appears to be around the $73-$85 range. A confirmed breakout above this level could trigger a measured move toward the $117 gap fill, which aligns with a previous price gap and serves as a logical target for bullish momentum.

Key technical highlights:

Target Price: ~$117 (gap fill zone)

If volume confirms the breakout above the neckline, this setup could offer a strong risk/reward opportunity for traders. Keep an eye on RSI and MACD for confirmation of bullish momentum.

Macro & Technical Signals: IWM, Uranium, Dollar, Oil, ALAB, LULUIn todays video we discuss the breakdown in small caps and high beta stocks.

A macro shift could be unfolding today as we saw the dollar & oil rally all day.

Uranium & gold saw some distribution.

Financials reversed off the highs.

High Beta stocks that have rallied are softening up.

SPX has triggered a near term bearish pattern while losing the 7 day MA.

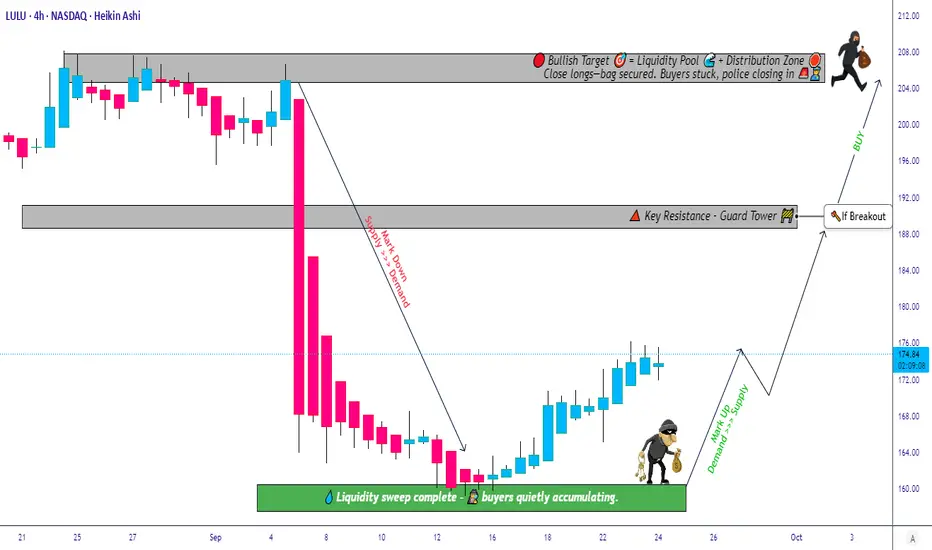

LULU Trade Plan – Buy Zones, Risk Levels, and Profit Goals🧘♂️ LULU "Lululemon Athletica Inc" – Thief Cash Flow Management Strategy 💰👟

Plan: 📈 Bullish (Swing / Day Trade)

🎯 Trade Setup

Entry (Thief Style Layering): Multiple limit buy layers placed like a thief sneaking in 🕵️♂️

$166.00

$168.00

$170.00

$172.00

(You can add more layers as per your own flow management)

Stop Loss (Thief SL): $160.00 ⚔️

Note: Dear Ladies & Gentlemen (Thief OG’s), I’m not recommending you set only my SL. Manage risk your way — you take money, then you make money.

Take Profit Targets:

🎯 TP1: $190.00

🎯 TP2: $205.00

Again, Thief OG’s, I’m not recommending only my TP. Profit booking is your own hustle 💼.

🗝️ Strategy Key Points

Thief Strategy = Cash Flow Layering: placing multiple limit orders (instead of 1 big risky entry).

Flow Management: works best in bullish momentum swings when volatility gives chance to “steal” good entries.

Risk Discipline: thief’s survival = flexible SL & TP, not fixed.

🔗 Related Stocks & Correlations

NYSE:NKE (Nike): Competitor correlation. If Nike earnings show strength, LULU often benefits.

NYSE:UAA (Under Armour): Similar sector — watch sentiment shifts.

AMEX:SPY (S&P 500 ETF): LULU often tracks broad market sentiment.

AMEX:XLY (Consumer Discretionary ETF): Sector ETF, gives broader picture of consumer spending trends.

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

⚠️ Disclaimer: This is a Thief Style Trading Strategy — created for fun, education & vibes only. Not financial advice. Trade at your own risk.

#LULU #SwingTrading #DayTrading #StockMarket #ThiefStrategy #CashFlow #BullishSetup #TradingHumor #EditorPickVibes

Lululemon: Beaten-Down Athleisure GiantLululemon: Beaten-Down Athleisure Giant Amid #Earnings and #Stocks Trends Crash? $250 Recovery Target in Sight?

Lululemon (LULU) shares tanked 19% today to around $160 after Q2 2025 earnings missed estimates, with revenue at $2.4B (up 7% YoY but below $2.44B expected) and EPS dipping to $2.68 from $2.89 last year, prompting a slashed full-year outlook amid China slowdowns.

This extends a brutal 57% YTD plunge from $420 highs, but with a P/E now at 12x versus historical 30x averages, analysts are calling it a "screaming buy" at 40% below fair value.

Just as #Earnings racks up 8K mentions on X with post-report volatility exploding, and #Stocks trends highlight beaten-down consumer plays (e.g., LULU's RSI at 33 signaling oversold), the stock's premium brand and 15% international growth position it for a viral rebound in the $200B+ athleisure market.

But with guidance cuts, is LULU the undervalued turnaround story ready to warrior-pose back to $250, or will competition erode margins further? Let's unpack the fundamentals, SWOT, charts, and setups for September 17, 2025.

Fundamental Analysis

Lululemon's resilience shines in steady sales despite macro headwinds, with Q2 gross margins holding at 58% and international revenue surging 15%—but US softness and China inventory issues led to the outlook trim to $11.15–$11.3B for FY2025 (up 6–7% YoY from $10.7B).

Analysts forecast 2025 EPS of $14.50 (up 10% YoY), with buy ratings from 25 of 30 firms hiking targets to $250 amid #Earnings fallout creating a value entry. Trading at 40% below DCF fair value, LULU's undervaluation ties into #Stocks hype on oversold retail, but elevated inventory risks could pressure if consumer spending cools.

- **Positive:**

- Brand moat with 20%+ market share in premium yoga; $1.2B FCF TTM funds $6B buybacks, amplified by #Earnings dips as buy signals.

- International expansion (35% of sales) projects 12% CAGR, undervaluing the stock at 12x P/E vs. peers' 25x amid #Stocks rotation.

- Broader trends in wellness and athleisure (e.g., viral TikTok fitness) position LULU for 15% revenue growth rebound.

- **Negative:**

- Guidance cut reflects China woes (sales down 2%), clashing with #Earnings optimism if tariffs hit.

- Inventory pile-up at $1.5B risks markdowns, pressuring margins in a high-inflation environment.

SWOT Analysis

**Strengths:** Iconic brand loyalty and direct-to-consumer model (40% of sales) with 58% margins, amplified by #Earnings oversold bounce potential.

**Weaknesses:** US market saturation and China dependency (20% revenue); recent earnings miss exposes execution risks in #Stocks volatility.

**Opportunities:** Global store openings (50+ planned) tap #business trends; undervalued at 12x P/E amid 10% EPS growth and athleisure boom on social media.

**Threats:** Rivals like Nike/Lululemon eroding share; economic slowdown crimping discretionary spend during viral #Earnings discussions.

Technical Analysis

On the daily chart, LULU shows a sharp V-bottom after the 19% gap-down, bouncing from $155 support in a multi-month downtrend, with volume spiking on post-earnings panic and mirroring #Earnings volatility. The monthly RSI at 33 screams oversold, echoing 2009/2014 bounces. Current price: $160, with VWAP at $165 as intraday pivot.

Key indicators:

- **RSI (14-day):** At 25, deeply oversold—classic bounce setup amid #Stocks surges. 📈

- **MACD:** Histogram flipping positive post-selloff, crossover imminent for reversal. ⚠️

- **Moving Averages:** Price below 21-day EMA ($180) but above 200-day SMA ($220)—death cross avoided.

Support/Resistance: Key support at $155 (today's low), resistance at $170 (50-day SMA) and $200 (Fib retrace). Patterns/Momentum: Oversold hammer candle targets $190; fueled by #Earnings momentum. 🟢 Bullish signals: Volume exhaustion low. 🔴 Bearish risks: Break below $155 eyes $140 on further guidance fears.

Scenarios and Risk Management

- **Bullish Scenario:** Reclaim $170 on retail rotation or soft CPI data targets $200 short-term, then $250 by year-end; buy pullbacks to $155, especially if #Earnings narrative shifts to value.

- **Bearish Scenario:** Drop below $155 eyes $140 (52-week low); watch for inventory news amid #Stocks fade triggering 10% more downside.

- **Neutral/Goldilocks:** Range-bound $155–$170 if data mixed and #Earnings cools, suiting covered calls pre-holidays.

Risk Tips: Use stops at $152. Risk 1-2% per trade. Diversify to avoid correlation traps with #Earnings-linked retail like NKE.

Conclusion/Outlook

Overall, a bullish bias if LULU holds $155, supercharged by today's #Earnings and #Stocks trends, affirming its undervalued status with 50%+ upside on international rebound. But watch Q3 comps and China updates for confirmation—this fits September's value rotation amid beaten-down consumer hype. What’s your take? Warrior pose into LULU dip or sitting out the volatility? Share in the comments!

Lululemon stretching into valueGoing long on LULU here. It's been beaten down to what I'd call fair value at under 15x earnings. So so oversold it could easily bounce to 240 maybe a lot higher on some positive news

LULU Lululemon Athletica Options Ahead of EarningsIf you haven`t sold LULU before the previous earnings:

Now analyzing the options chain and the chart patterns of LULU Lululemon Athletica prior to the earnings report this week,

I would consider purchasing the 195usd strike price Puts with

an expiration date of 2025-10-17,

for a premium of approximately $14.05.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

BUY NOW $LULU EASY MONEYRSI (14) 39.15

P/E 13.65 as of 08/13/2025

Buy now and you will thank me later.

This is super sale

3000 Percent Gain on This Stock!OCTO had a massive mump today on the back of BMNR & Tom Lee getting involved.

This company went from zero to basically hero....caution buying this hype.

OPEN saw a negative bearish reversal from the highs. Likely giving a near term top.

Lulu went from red to green - daily bottoming tail.

Our markets continue to show casino tendencies.

Can Innovation Survive Strategic Drift?Lululemon Athletica's shares plummeted 18% in premarket trading on September 5, 2025, following a dramatic reduction in annual sales and profit guidance that marked the second guidance cut of the year. The company's stock has declined by 54.9% year-to-date, resulting in a market capitalization of $20.1 billion. This drop in stock value comes as a reaction from investors to disappointing Q2 results, which showed only 7% revenue growth, reaching $2.53 billion. Additionally, there was a concerning 3% decline in comparable sales in the Americas, despite strong international growth of 15%.

The perfect storm hitting Lululemon stems from multiple converging forces. The Trump administration's removal of the *de minimis* exemption on August 29, 2025, eliminated duty-free treatment for shipments under $800, creating an immediate $240 million gross profit headwind in fiscal 2025 that's projected to reach $320 million in operating margin impact by 2026. This policy change particularly damages Lululemon's supply chain strategy, as the company previously fulfilled two-thirds of its U.S. e-commerce orders from Canadian distribution centers to bypass duties, while relying heavily on Vietnam (40% of manufacturing) and China (28% of fabrics) for production.

Beyond geopolitical pressures, Lululemon faces internal strategic failures that have amplified external headwinds. CEO Calvin McDonald acknowledged the company had become "too predictable with our casual offerings" and "missed opportunities to create new trends," which led to prolonged product life cycles, especially in lounge and casual wear, accounting for 40% of sales. The company is facing increasing competition from emerging brands such as Alo Yoga and Vuori in the premium segment. At the same time, it is dealing with pressure from private-label imitations that provide similar fabric technology at much lower prices. This trend is especially challenging in markets where consumers are more price-sensitive.

Despite maintaining an impressive portfolio of 925 patents globally, protecting unique fabric blends, and investing in next-generation bio-based materials through partnerships with companies like ZymoChem, Lululemon's core challenge lies in the disconnect between its robust intellectual property and innovation capabilities versus its inability to translate these strengths into timely, trend-setting products. The company’s future strategy requires decisive actions in three key areas: refreshing our products, implementing strategic pricing to counteract tariff costs, and optimizing the supply chain. All of this must be done while navigating a challenging macroeconomic environment, where American consumers are cautious and Chinese consumers are increasingly opting for local brands over premium foreign alternatives.

Stock Opportunity: LULULEMON & AVGO EARNINGSNASDAQ:LULU just reported earnings of $2.53B vs $2.54B est

They did beat on the EPS side $3.10 vs $2.85

Lululemon is now the second cheapest its ever been in its history on a PE basis. Behind the GFC crisis in 2008.

They have slashed their guidance and profit forecasts...which seem to be the final shakeout.

Lulu filled a massive weekly technical gap going back to Covid.

NASDAQ:AVGO reported earnings: Rev $15.95B vs $15.83B

EPS $1.69 vs $1.54

This institutional semiconductor stock is crushing Vol and staying flat-ish in afterhours.

We took a position in Lulu.

LULU Earnings Alert: Big Beat Potential! 208Call Plays

🚀 **LULU Earnings Trade Setup (2025-09-04)** 🚀

**Market Bias:** **Moderate Bullish** 📈

**Confidence:** 72% ✅

**Trade Idea:**

🎯 **Instrument:** LULU

🔀 **Direction:** LONG CALL

💵 **Strike:** \$208.00

📅 **Expiry:** 2025-09-05 (Weekly)

💰 **Entry Price:** \$12.10

📈 **Profit Target:** \$36.30 (200%+ return)

🛑 **Stop Loss:** \$6.05 (50% of premium)

📏 **Size:** 1 contract

⏰ **Entry Timing:** Pre-earnings close (AMC on 2025-09-04)

**Rationale:**

* Strong fundamental beat history: 100% last 8 quarters 💪

* Durable margins & high earnings quality 🏆

* Asymmetric upside if modest beat + guidance lift ⚡

* Risk: IV crush & binary guidance shock ⚠️

**Key Levels:**

* Support: \$185–\$190 🛡️

* Resistance: \$208–\$215 🔝

* Expected gap on beat: \~\$215–\$220

* Expected move (implied): \~9–11%

**Risk/Reward:**

* Max loss: \$1,210

* Reward potential: \$2,420 → **2:1+ asymmetric upside**

* Breakeven: \$217.10

**Execution Notes:**

* Use **limit orders or algo** to reduce slippage

* Exit **by market open post-earnings** or at profit/stop targets

* IV crush expected: 30–50% ⚡

**Options Liquidity:**

* 205 call OI: 1,205 ✔️

* Ask/Bid: 12.10 / 11.85

* Sufficient for single-leg trade

📊 **Trading JSON (for exact execution)**

```json

{

"instrument": "LULU",

"direction": "call",

"strike": 208.0,

"expiry": "2025-09-05",

"confidence": 72,

"profit_target": 36.30,

"stop_loss": 6.05,

"size": 1,

"entry_price": 12.10,

"entry_timing": "pre_earnings_close",

"earnings_date": "2025-09-04",

"earnings_time": "AMC",

"expected_move": 9.5,

"iv_rank": 0.75,

"signal_publish_time": "2025-09-04 14:33:52 UTC-04:00"

}

``

Getting ready for the run!- NASDAQ:LULU is getting ready for the reversal run!

- beaten down name YTD, cheapest valuation in a decade.

- international expansion will work out in the long run despite creating capex headwins in the shorter timeframe