MU — Time for a CorrectionFollowing our previous idea:

We have been rising for a long time, and it appears that it is time for a correction.

Let’s define the initial targets for the first corrective move.

Key targets:

376 — local correction

346

327

The potential move from the current level is 16–20%.

We expect further downside going forward.

---

Subscribe and leave a comment.

You’ll get new ideas faster than anyone else.

---

MU

Micron Technology - Here comes the ultimate reversal!🥊Micron Technology ( NASDAQ:MU ) is soon collpasing:

🔎Analysis summary:

Micron Technology is clearly retesting a major resistance trendline. We can also see that Micron Technology is somewhat overextended and ready for a healthy correction. All it needs now is bearish confirmation and we could see a decent rejection in the near future.

📝Levels to watch:

$350

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

Micron Technology - The bullrun will end today!🏒Micron Technology ( NASDAQ:MU ) is now starting a correction:

🔎Analysis summary:

Over the course of the past couple of months, Micron Technology rallied an expected +350%. However, with the current retest of major resistance, it is quite likely that this bullrun will end soon. Just wait for sufficient bearish confirmation after this long rally.

📝Levels to watch:

$350

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

MU - Continuing UptrendReturning to Micron Technology.

From the previous idea: the minimum corrective target was reached, and the upward move continues.

The current move is viewed as a large wave 5 .

Most probable targets:

- 321

- 365

MU Micron Technology Options Ahead of EarningsIf you haven`t bought MU before the rally:

Now analyzing the options chain and the chart patterns of MU Micron Technology prior to the earnings report next week,

I would consider purchasing the 247.5usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $8.10.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Quantum Leap: $QTUM Continuation Pattern has triggered.The Defiance Quantum ETF (QTUM) is showing a classic bullish continuation pattern after a spectacular 2025. Following a sharp rally, the price has been consolidating in a tight range near its 52-week high of $117.12.

The Technical Setup: We are seeing a clear consolidation phase—likely a cup and handle / or continuation inverse head and shoulders Both have the same price objective—just above the 50-day moving average ($114.36).

This 'pause' in the trend is healthy and suggests that the previous uptrend is ready to resume.

FUNDAMENTAL DRIVER:

2026 is being labeled a potential 'inflection year' for the industry.

IBM is targeting quantum advantage by the end of this year with its 120-qubit Nighthawk processor, while IonQ aims for systems up to 256 qubits.

Diversified Exposure: Unlike betting on a single stock, QTUM holds 84 different companies, spreading risk across hardware, software, and machine learning leaders like Microsoft, Alphabet, and NVIDIA.

Massive Market Growth: Analysts estimate the quantum computing market could grow from $0.8 billion in 2025 to over $1 billion in 2026, with some projections suggesting a nearly $2 trillion value creation potential by 2035.

Sustained Inflows: The ETF has seen net AUM growth of over $2.39 billion in the last year, proving that institutional capital is rotating heavily into this sector.

What's your take? Is the quantum sector ready for another parabolic move?

MICRON scripted blue-print. More than -50% sell-off expected.Micron Technology (MU) is on an amazing long-term rally since the April 2025 Low, currently on the 6th straight green month (1M candle) and 8th in the last 9 months. Its historic price action however shows that this remarkable uptrend may be coming to an end as the price is approaching the top of its 17-year Channel Up (started after the 2008 U.S. Housing Crisis).

Technically, this post April 2025 rally, is the Bullish Leg of this Channel Up and it already broke above the 0.786 Channel Fibonacci, a level that has only broken 3 times in total, with the last being in June 2018.

At the same time, it is close to completing a +601.35% rise, which despite being unusually high, Micron has done such rally 3 times in the past. The remarkable feat is that all those rallies where exactly +601.35%!

Last but not least, the 1M RSI is massively overbought and is approaching Resistance 2 (89.00), which was last seen on the June 2014 High.

All those factors collectively, force a huge bearish dynamic long-term. At best, we may see this rally exhaust near $440 on the short-term, thus fulfilling the +601.35% Bullish Leg blue-print but on the long-term the value of selling give much higher return.

And as far as a potential Target for this upcoming Bear Cycle is concerned, the 0.236 Channel Fibonacci level is the strongest candidate as virtually all major corrections since 2011 have hit that trend-line before the market bottomed. As this chart shows, the 0.236 Fib level has been touched 6 times since 2011, with the market hitting at least its 1M MA50 (blue trend-line) in the process on a minimum -50% decline. The 1M MA100 (green trend-line) has been its true long-term Support since July 2016.

As a result, it is highly probable that Micron drops below the 1M MA50 and hits the 0.236 Fib at around $140 before the market bottoms and turns into a long-term Buy again. At the same time, it is useful to keep an eye on the 1M RSI and Support Zone 1. This has given the last 3 major Buy Signals since December 2018. As a result, if the stock hits that level before reaching $140, we will turn into long-term buyers regardless of the price.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

MU Trade ideaI am waiting for next target 309 to take short position targeting 257, this crazy stock will keep moving upward for sure and correction happens with high %, lets see this week if reached 309 only 5% far.

Micron Technology - This bullrun is still not over!💵Micron Technology ( NASDAQ:MU ) can rally a final +25%:

🔎Analysis summary:

Micron Technology retested major support in mid 2025. After we then witnessed textbook bullish confirmation, it was clear that this stock will rally. With the recent move of +300%, Micron Technology is almost back at major resistance, but it can rally another +25% first.

📝Levels to watch:

$300

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

Breaking: Micron Technology, Inc. (MU) Spike 17% Yesterday The price of Micron Technology, Inc. (NASDAQ: NASDAQ:MU ) Spike 17% yesterday , further extending gains to extended market sessions on Friday albeit notable stocks like GPW:NIKE , NASDAQ:TSLA and NASDAQ:VMAR all nosedived.

In another news, Micron Technology (NASDAQ: MU) rallied some 15% today after reporting top- and bottom-line growth for its fiscal Q1 that Morgan Stanley dubbed the “best in the history of the US semis industry” outside of Nvidia.

For the current quarter, the memory-chip maker forecast adjusted earnings of $8.42 per share on $18.7 billion in revenue, well above Wall Street expectations of $4.78 per share and $14.2 billion in sales.

Following the post-earnings surge, Micron stock is trading a remarkable 300% higher than its year-to-date low.

Technically, NASDAQ:MU stock might experience some respite before peaking liquidity up. The 38.2% Fib retracement level is the possible level for NASDAQ:MU to consolidate before reaching higher levels.

About MU

Micron Technology, Inc. designs, develops, manufactures, and sells memory and storage products in the United States, Taiwan, Singapore, Japan, Malaysia, China, India, and internationally. It operates through the Cloud Memory Business Unit (CMBU); Core Data Center Business Unit (CDCBU); Mobile and Client Business Unit (MCBU); and Automotive and Embedded Business Unit (AEBU) segments.

MU: false breakout at the upper boundary of the rangeThis analysis is based on the Initiative Analysis (IA) method.

Hello traders and investors!

Micron Technology (MU) shares are currently trading in a sideways range. At this stage, the active initiative belongs to the seller.

At the upper boundary of the range, a false breakout was formed — a breakout above the range high on increased volume.

After that, the seller engulfed the buyer’s candle, which strengthens the seller’s position within the range.

It is also worth noting that the key candle of the seller’s initiative — the candle with the highest volume (marked as IC on the chart) — also belongs to the seller, confirming supply-side control.

Potential seller targets:

first target — 223.33

second target — 214.75

The blue band on the chart represents the minimum price range of the candle in which at least 50% of the volume was traded, helping to more accurately identify the zone of market participant activity.

Wishing you profitable trades!

Micron’s AI Pivot: A 2025 Strategic & Geopolitical AnalysisThe “AI Supercycle” has finally matured from a buzzword into a tangible balance sheet reality. As of mid-December 2025, Micron Technology (MU) stands at a critical inflection point. With the Federal Reserve lowering rates to 3.75% and the semiconductor industry grappling with an unprecedented divergence between enterprise boom and consumer stagnation, Micron has aggressively repositioned itself. The upcoming fiscal Q1 2026 earnings report on December 17 represents more than a financial update; it is a referendum on CEO Sanjay Mehrotra’s high-stakes gamble on High Bandwidth Memory (HBM).

Business Model Transformation: The Enterprise Pivot

Micron is executing one of the most radical structural pivots in its history. The decision to deprioritize, and in some regions effectively sunset, its consumer-facing Crucial brand by early 2026 signals a ruthless allocation of capital. Management has correctly identified that the consumer PC market is a low-margin drag. Instead, production capacity is being violently swung toward enterprise-grade DRAM and AI-centric storage. This moves Micron from a commodity volume player to a specialized, high-margin infrastructure partner for hyperscalers like Microsoft and AWS.

Technology & Innovation: The HBM Wars

Technological supremacy is now defined by the roadmap to HBM4. While SK Hynix initially led the HBM race, Micron’s aggressive rollout of HBM3E has closed the gap. The company’s 1-beta and upcoming 1-gamma nodes utilize extreme ultraviolet (EUV) lithography to deliver power efficiency metrics that rival Asian competitors. Patent analysis reveals a surge in filings related to 3D-stacking architecture and advanced packaging, confirming that Micron is building a defensive IP moat around its high-performance compute capabilities.

Geostrategy & Geopolitics: Navigating the Fracture

Micron operates on the fault line of the US-China chip war. The lingering effects of Beijing’s 2023 ban on Micron products have accelerated the company’s "China-Plus-One" strategy. In response, Micron has doubled down on domestic manufacturing, leveraging the US CHIPS Act to fund mega-fabs in New York and Idaho. This is not just expansion; it is geopolitical insurance. By embedding itself into the US national security apparatus, Micron mitigates the risk of losing Chinese market share while securing subsidized capital that lowers its long-term cost of production.

Macroeconomics: The Rate Cut Tailwind

The Federal Reserve’s cut to 3.75% this November provides a specific, quantifiable benefit to Micron. Semiconductor manufacturing is arguably the most capital-intensive industry on earth. Lower borrowing costs directly improve the Net Present Value (NPV) of Micron’s multi-billion dollar fab projects. Furthermore, a softer dollar environment boosts the competitiveness of US exports, providing a tailwind for Micron’s international revenue recognition in fiscal 2026.

Cybersecurity & Supply Chain Integrity

In an era of state-sponsored cyber espionage, hardware security is a premium feature. Micron has elevated its cybersecurity posture by securing ISO/SAE 21434 certification for automotive memory, a critical requirement for modern SDVs (Software-Defined Vehicles). This focus extends to the supply chain; rigorous "Zero Trust" protocols now govern raw material sourcing, addressing the vulnerabilities exposed by recent global logistics disruptions. This security-first branding allows Micron to charge a premium to defense and automotive clients who cannot afford compromised hardware.

Management & Leadership

Sanjay Mehrotra’s tenure has been defined by discipline. Unlike previous cycles where memory makers flooded the market, causing price crashes, current leadership has shown remarkable restraint in CapEx spending. The 2025 strategy focuses on "bit growth discipline"—matching supply strictly to demand. This oligopolistic behavior, shared tacitly by competitors, has successfully engineered a favorable pricing environment, driving gross margins back toward the 40%+ range.

Conclusion: The Verdict

Micron Technology in late 2025 is no longer just a cyclical memory stock; it is a derivative play on the AI infrastructure build-out. The risks—ranging from HBM yield issues to renewed geopolitical friction—are real. However, the company’s strategic withdrawal from low-margin consumer markets and successful capture of CHIPS Act incentives position it favorably. As investors look to December 17, the question is not if AI demand exists, but if Micron can manufacture fast enough to satisfy it.

MU - Continuing CorrectionWe are evaluating the chart from a technical perspective.

The correction is still in progress, and the structure suggests that wave C should begin forming.

Targets:

• First target: 225.5

• Second target: 192.5

---

Please subscribe and leave a comment.

You’ll get new information faster than anyone else.

---

MU – Trend Still Intact, EMA50 Bounce SetupMU - CURRENT PRICE : 220.00 - 222.00

Technical Reasons (Bullish Bias)

1️⃣ Price retesting strong dynamic support

Price is holding above the 50-day EMA, which has acted as support throughout the uptrend. Pullback into EMA50 often forms a bullish continuation point.

2️⃣ Price still above the Ichimoku Cloud

Price is trading above the cloud, meaning long-term trend remains bullish. The cloud is thick — showing strong trend support. Latest pullback is testing the top of the cloud, usually a high-probability bounce area.

3️⃣ RSI turning up from mid-zone (not overbought)

RSI is around 50, which is a healthy reset in an uptrend. No overbought conditions → room for upside continuation.

4️⃣ Trend structure remains bullish

Higher highs & higher lows remain intact. Current candle shows buying interest at key support.

5️⃣ Market respects previous breakout area

Price pulled back to retest September–October breakout zone → classic break-and-retest setup.

ENTRY PRICE : 218.00 - 222.00

FIRST TARGET : 236.00

SECOND TARGET 260.00

SUPPORT : 201.00

MU long-term TAMicron is one of the strongest among semis, there's no need to wonder why it's holding up so good, it has plenty of heavy bullish volumes on weekly time frame which have started to correct recently yes, to be more precise since last week the mid-term has initiated the distribution, so now MU needs some time to balance everything. Watch the blue lines for the support to hold.

Micron Technology - The end will come soon!✂️Micron Technology ( NASDAQ:MU ) will create a top soon:

🔎Analysis summary:

Starting back in mid 2025, Micron Technology retested a major confluence of support. This retest was followed by an expected rally of about +250%. But soon, Micron Technology will create a short term top formation, followed by a healthy correction towards the downside.

📝Levels to watch:

$250

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

MU Trade Alert: Katy V3 Sees Late-Week UpsideMU | QuantSignals V3 Weekly Trade Alert (2025-11-21)

Signal Overview

Direction: BUY CALLS (LONG)

Confidence: 58% (Low Conviction)

Expiry: 2025-11-28 (7 days)

Strike: $212.50

Entry Price: $7.75

Target 1: $11.63 (+50%)

Target 2: $15.50 (+100%)

Stop Loss: $5.43 (-30%)

Position Size: 2% of portfolio

Market Context

Weekly Momentum: Bullish +3.64%

Flow Intel: Bearish PCR 2.31 → likely institutional hedging

Technical Support: $207.05 | Resistance: ~$230

Current Price Action: Strong late-week bullish trajectory, recovering from Nov 24 lows toward Katy target $224.11

Trade Rationale

Katy AI shows NEUTRAL overall confidence but a late-week bullish trend

PCR bearishness interpreted as hedging, not conviction, creating asymmetric opportunity

Friday gamma effects may accelerate price movement toward $224 target

Conservative sizing mitigates risk while capturing potential upside

⚠️ Risk Warning

Low Katy confidence → use small position size

Friday expiration → higher gamma risk

Mixed signals → consider scaling in cautiously

MU - Breakout of TriangleMU has broken out of an ascending triangle in green

This was along a strong trend line in white

Using prior highs predictions about a future channel come

Good buy following the breakout of triangle

Monthly chart

MU - Bullish Continuation Pattern ?MU - CURRENT PRICE : 204.00 - 205.00

The stock has surged nearly 70% since my previous buy call, demonstrating strong bullish momentum. I shared the link of my previous trading idea for reading purpose.

Currently, the price has broken out of a bullish flag pattern, indicating the potential for another leg higher. Estimate target of this bullish flag pattern is around 237.00. Support level is 179.00 (the low of 10 October 2025 candle).

Take note also this ascending in prices is also supported by rising in On Balance Volume (OBV) readings. (Look at the blue line at bottom of chart)

ENTRY PRICE : 203.00 - 205.00

TARGET : 237.00

SUPPORT : 179.00

Can Memory Chips Become Geopolitical Weapons?Micron Technology has executed a strategic transformation from commodity memory producer to critical infrastructure provider, positioning itself at the intersection of AI computing demands and U.S. national security interests. The company's fiscal 2025 performance demonstrates this pivot's success, with data center revenue surging 137% year-over-year to comprise 56% of total sales. Gross margins expanded to 45.7% as the company captured pricing power across both its advanced High-Bandwidth Memory (HBM) portfolio and traditional DRAM products. This dual-margin expansion stems from an unusual market dynamic: capacity reallocation toward specialized AI chips has created artificial supply constraints in legacy memory, driving price increases exceeding 30% in some segments. In contrast, HBM3E capacity through 2026 is already sold out.

Micron's technological leadership centers on power efficiency and manufacturing innovation that translate directly into customer economics. The company's HBM3E solutions deliver bandwidth exceeding 1.2 TB/s while consuming 30% less power than competing 8-high configurations—a critical advantage for hyperscale operators managing electricity costs across massive data center footprints. This efficiency edge is reinforced by scientific advances in manufacturing, particularly the mass production deployment of 1γ DRAM using Extreme Ultraviolet lithography. This node transition delivers over 30% more bits per wafer than previous generations while reducing power consumption by 20%, creating structural cost advantages that competitors must match through heavy R&D investment.

The company's unique position as America's sole HBM manufacturer has transformed it from a component supplier to a strategic national asset. Micron's $200 billion U.S. expansion plan, supported by $6.1 billion in CHIPS Act funding, aims to produce 40% of its DRAM capacity domestically within a decade. This geostrategic positioning grants preferential access to U.S. hyperscalers and government projects requiring secure, domestically sourced components, a competitive moat independent of immediate technological specifications. Combined with a robust intellectual property portfolio covering 3D memory stacking and secure boot architectures, Micron has established multiple defensive layers that transcend typical semiconductor industry cycles, validating an investment thesis for sustained high-margin growth through structural rather than cyclical drivers.

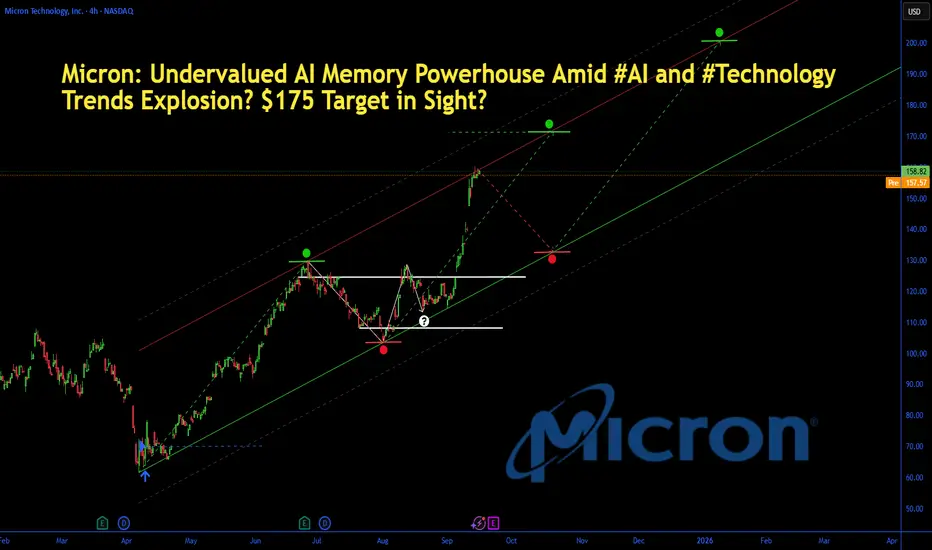

Micron: AI Memory Powerhouse Amid #AI and #TechnologyMicron: Undervalued AI Memory Powerhouse Amid #AI and #Technology Trends Explosion? $175 Target in Sight?

Micron (MU) shares hit a new 52-week high of $158.28 today, up 1.2% amid surging AI data center demand and institutional buying, with the stock soaring 86.8% YTD on memory chip tailwinds.

As Q4 fiscal 2025 earnings loom on September 23—projecting 58% EPS jump to $1.29 on $8.7B revenue—analysts have hiked targets to $175, implying 10%+ upside. Just as #AI racks up 17K mentions and #technology trends with 46K on X today (fueled by AI video generators and chip hype), Micron's HBM3E tech for Nvidia GPUs positions it as the undervalued play in the $200B+ semiconductor memory market.

But with forward P/E at 12x, is MU set to ride the AI wave higher, or will supply gluts cap the rally? Let's unpack the fundamentals, SWOT, charts, and setups for September 17, 2025.

Fundamental Analysis

Micron's resurgence is driven by AI hyperscaler demand for high-bandwidth memory (HBM), with Q2 fiscal 2025 revenue hitting $9.3B (up 93% YoY) and data center sales doubling to $2.2B.

Analysts forecast 2025 revenue of $38.5B (up 50% YoY), as HBM capacity ramps to 250K wafers amid #AI trends exploding on social media. Trading at 18% below fair value per DCF, MU's undervaluation shines with gross margins rebounding to 37%—but cyclical DRAM risks could flare if PC demand softens.

- **Positive:**

- AI boom ties into today's #technology hype, with HBM3E sales projected at $2.5B in FY2025; institutional stakes rising signal confidence.

- Q2 EPS beat of $1.18 (vs. $1.00 est.) and $1.6B FCF undervalues the stock at 12x forward earnings vs. sector 25x.

- Broader trends in edge AI and automotive chips position MU for 20%+ CAGR, amplified by #AI video generator virality.

- **Negative:**

- Inventory overhang from prior cycles could pressure pricing, clashing with #technology optimism if China trade tensions escalate.

- High capex ($8B annually) strains balance sheet if AI adoption slows amid economic jitters.

SWOT Analysis

**Strengths:** Leadership in DRAM/NAND with 20%+ market share; AI-optimized HBM tech generates 50%+ gross margins, amplified by #AI relevance in data centers.

**Weaknesses:** Cyclical exposure to consumer electronics; $7.8B net debt limits agility in a volatile #technology market.

**Opportunities:** HBM ramp to meet Nvidia/AMD demand unlocks $5B+ revenue; undervalued at 12x P/E amid 58% EPS growth and #AI boom on X.

**Threats:** Supply chain disruptions from geopolitics; competition from Samsung/SK Hynix capitalizing on #technology trends.

Technical Analysis

On the daily chart, MU is in a parabolic uptrend, breaking 52-week highs after consolidating above $140 support, with volume exploding on AI news and mirroring #AI volatility spikes. The weekly shows a cup-and-handle breakout from summer lows, now accelerating higher. Current price: $158.28, with VWAP at $156 as intraday pivot.

Key indicators:

- **RSI (14-day):** At 74, overbought but fueled by momentum—watch for consolidation amid #technology surges. 📈

- **MACD:** Bullish crossover with surging histogram, confirming AI-driven acceleration; minimal divergence. ⚠️

- **Moving Averages:** Price crushing 21-day EMA ($145) and 50-day SMA ($130), golden cross locked in.

Support/Resistance: Key support at $150 (recent breakout and 50-day SMA), resistance at $165 (Fib extension) and $175 (analyst target). Patterns/Momentum: Cup-and-handle targets $200; strong buy signals. 🟢 Bullish signals: Volume on earnings hype. 🔴 Bearish risks: Overbought RSI could pull back 5-8% on profit-taking.

Scenarios and Risk Management

- **Bullish Scenario:** Smash $165 on earnings beat or #AI catalyst targets $175 short-term, then $200 by year-end. Buy dips to $150 for entries tied to tech trends.

- **Bearish Scenario:** Breach $150 eyes $140 (200-day EMA); supply news amid #technology fade could retrace 10%.

- **Neutral/Goldilocks:** Range-bound $150–$165 if data mixed and #AI cools, ideal for straddles pre-earnings.

Risk Tips: Set stops 3% below support ($145.50) to tame volatility. Risk 1-2% per trade. Diversify with NVDA or SMH to hedge semi correlations.

Conclusion/Outlook

Overall, a bullish bias if MU holds $150, supercharged by today's #AI and #technology trends, cementing its undervalued status with 40%+ upside on memory demand. But watch September 23 earnings for confirmation—this fits September's chip rotation amid viral AI hype. What’s your take? Bullish on MU amid #AI chip trends or fading the rip? Share in the comments!

Micron Technology - New all time highs!💰Micron Technology ( NASDAQ:MU ) is heading for new highs:

🔎Analysis summary:

More than a decade ago, Micron Technology entered into a significant long term rising channel pattern. Recently, we witnessed an expected rally of about +120%, perfectly rejecting support. But with the current all time high retest, we will also see a bullish breakout in the near future.

📝Levels to watch:

$140

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

$MU Tradespoon – Long Entry $168.60Tradespoon model generated long signal for NASDAQ:MU . Predicted range: $168.60–$176.40. Trend: +3.16%. NASDAQ:MU