Undervalued Fintech Just Hit 110M Users: Nubank ($NU)The Case for Nubank NYSE:NU

Nubank is a combination of growth and value in the fintech space. I personally like it when, as an investor, I find a stock that is a growth and value stock simultaneously.

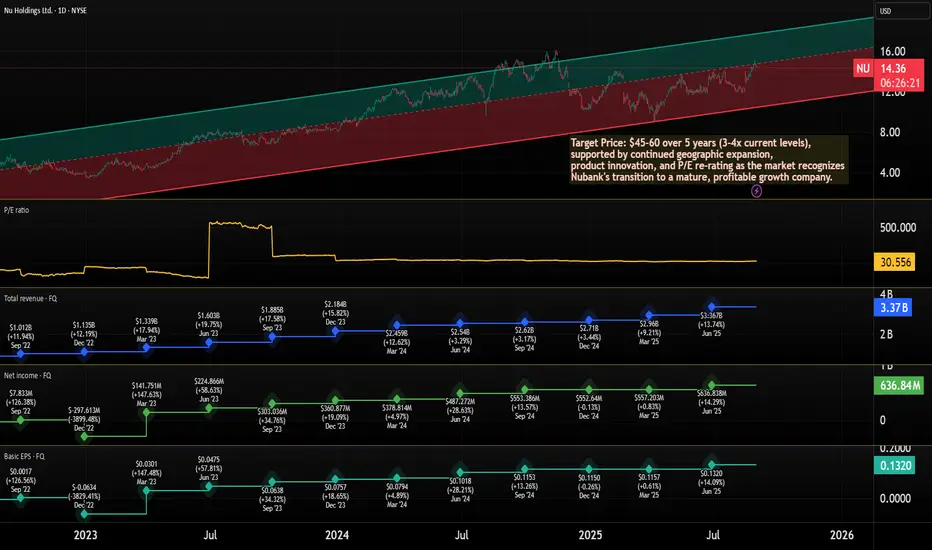

Nu is trading at a P/E of 31.5x, and the company is a compelling story with upside potential as Latin America's leading digital bank continues its rapid expansion.

The LATAM market still has lots of underbanked people, but Nubank offers the neobank and digital services necessary for those people.

The fact that it amassed 110 million clients in just a few years tells us something. The clients are mostly in Brazil, Mexico, and Colombia, but the company is planning expansion to other countries, including the US

Remarkable Financial Trajectory (2023-2025)

Revenue Growth Acceleration:

2023: $3.37B total revenue

Q2 2025 alone: $3.36B revenue. Q2 2025 alone had the same revenue as 2023. Truly impressive

Very strong quarter-over-quarter growth and operational leverage.

Key Financial Metrics Progression

P/E Evolution: From 90x+ (growth phase) → 31.5x (profitable growth phase)

Revenue CAGR: 63.4% demonstrating consistent market penetration

EPS Growth: 63.2% three-year average showing operational leverage

User Growth: 30M → 110M+ (4x in 5 years) with improving unit economics

Investment thesis: Why Nubank is undervalued

1. Valuation arbitrage

Current P/E: 31.5x vs. US fintech peer SoFi NASDAQ:SOFI at ~50x

Growth-adjusted valuation: 63% revenue growth at 31x P/E = 0.49 PEG ratio (anything under 1.0 is attractive)

International discount: Market applying "emerging market penalty" despite superior fundamentals

2. Proven Business Model Scalability

The 2023-2025 data eliminates key execution risks:

Growing profitability across multiple quarters

Growth maintained at scale (110M+ users, still growing)

Margin expansion demonstrating operational leverage

Multi-year consistency reducing one-time success concerns

3. Structural advantages in underserved arkets

Digital-first cost structure: 80%+ lower cost base than traditional banks

First-mover advantage: Dominant position in Brazil, early leadership in Mexico/Colombia

Network effects: Growing ecosystem creates switching costs and viral acquisition

Regulatory tailwinds: Government support for financial inclusion across Latin America

4. Multiple Expansion Catalysts

Near-term (1-2 years):

US market expansion announcement

Continued profitability growth reducing "emerging market risk" perception

Potential inclusion in major indices (MSCI, etc.)

Medium-term (3-5 years):

Cross-border payments and remittance products

Small business lending expansion

Insurance and wealth management scaling

Geographic Expansion: The untapped opportunity

Brazil (Mature Market)

Market-leading position providing stable cash flow foundation

Still room for product penetration (insurance, wealth management)

Mexico/Colombia (Growth Markets)

Early-stage penetration with massive TAM

2025 data suggests strong traction in these markets

US Expansion (Game Changer)

Management indicated plans for US market entry

Could unlock premium US fintech valuations (40-50x P/E multiples)

Remittance corridor between US and Latin America represents $100B+ opportunity

Risk-Reward Analysis

Conservative 5-Year Scenario:

Earnings growth: 25% CAGR (conservative given 63% current growth) = 3x earnings in 5 years

Multiple expansion: P/E re-rating to 45x (still below SoFi's 50x) = 43% upside

Combined effect: 3x earnings × 1.43x multiple = 4.3x total return

Base Case Assumptions:

Revenue growth slows to 20-25% annually (from current 63%)

P/E expands to 40-45x as profitability matures

US expansion adds 20-30% valuation premium

Target: 3-4x returns over 5 years

Why Now??

Valuation Opportunity: 31.5x P/E for 63% growth company is historically cheap

Proven Execution: 2023-2025 data eliminates major execution risks

Market Inefficiency: US investors underweight due to "foreign" perception

Catalyst Pipeline: US expansion, product launches, and regulatory tailwinds

Target Price: $45-60 over 5 years (3-4x current levels), supported by continued geographic expansion, product innovation, and P/E re-rating as the market recognizes Nubank's transition to a mature, profitable growth company.

Conclusion

Nubank in 2025 is no longer a speculative fintech play - it's a proven, profitable, growing financial services powerhouse trading at a discount to inferior peers. The combination of 63% revenue growth, sustainable profitability, massive TAM, and 31.5x P/E creates an asymmetric risk-reward opportunity rarely seen in public markets.