Can Oxygen Absorption Forge a Wireless Revolution?Peraso Inc. (NASDAQ: PRSO) operates at the intersection of geopolitics, physics, and semiconductor innovation in the 60GHz millimeter-wave spectrum. As Western governments dismantle Chinese telecommunications infrastructure through "Rip and Replace" initiatives, Peraso emerges as a strategic beneficiary—offering North American-designed silicon fabricated through TSMC that meets "Clean Network" standards. The company's technology leverages a peculiar quirk of atmospheric physics: oxygen molecules absorb 60GHz signals within 1-2 kilometers, creating both a limitation and a strategic advantage. This phenomenon enables spatial isolation for frequency reuse and inherent physical-layer security, positioning Peraso's solutions as ideal for dense urban wireless networks, military tactical communications, and next-generation VR/AR devices requiring multi-gigabit wireless bandwidth.

The company's leadership, veterans of the Intellon-to-Atheros-to-Qualcomm acquisition chain, brings proven expertise in standardizing emerging connectivity technologies. Peraso holds nine Standard Essential Patents for IEEE 802.11ay (WiGig), creating licensing leverage across any manufacturer building compliant high-speed wireless devices. Despite Q3 2025 revenue reaching $3.2 million (up 45% sequentially) and expanding gross margins by 56%, the stock remains deeply undervalued, as evidenced by Mobix Labs' hostile $1.30/share takeover attempt, which represents a 53% premium. The company has successfully transitioned from its legacy MoSys memory business to become a pure-play 60GHz specialist, securing design wins in defense applications and partnerships with major fixed wireless access providers.

Peraso's investment thesis is based on three pillars: geopolitical tailwinds that are forcing Western infrastructure operators toward trusted suppliers, the irreplaceable physics of 60GHz in solving spectrum congestion, and a patent portfolio that positions the company as either a future licensing powerhouse or an attractive acquisition target. The primary risks include aggressive cash burn requiring frequent dilution, execution challenges in reaching fragmented WISP customers, and the inherent volatility of micro-cap semiconductor stocks. For investors seeking asymmetric exposure to the "Wireless Fiber" revolution, where capital-efficient mmWave bridges replace expensive fiber deployments, Peraso represents a contrarian deep-tech opportunity in an overlooked corner of the connectivity market.

Patentportfolio

Can One Shot Silence a Disease Forever?Benitec Biopharma has emerged from clinical obscurity to platform validation with unprecedented Phase 1b/2a trial results showing a 100% response rate across all six patients treated with BB-301, their gene therapy for Oculopharyngeal Muscular Dystrophy (OPMD). This rare genetic disorder, characterized by progressive swallowing difficulties that can lead to fatal aspiration pneumonia, has no approved pharmaceutical treatments. Benitec's proprietary "Silence and Replace" approach uses DNA-directed RNA interference to simultaneously shut down production of the toxic mutant protein while delivering a functional replacement, a sophisticated dual-action mechanism delivered via a single AAV9 vector injection. The clinical data revealed dramatic improvements, with one patient experiencing an 89% reduction in swallowing burden, essentially normalizing their eating experience. The FDA's subsequent Fast Track Designation for BB-301 underscores the regulatory conviction in this approach.

The company's strategic positioning extends well beyond a single asset. November 2025 marked a transformative capital event with a $100 million raise at $13.50 per share, nearly triple the $4.80 pricing from just 18 months prior, anchored by a $20 million direct investment from Suvretta Capital, which now controls approximately 44% of outstanding shares. This institutional validation, coupled with a fortress balance sheet providing runway into 2028-2029, has fundamentally de-risked the investment thesis. The manufacturing partnership with Lonza ensures scalable, GMP-compliant production while avoiding geopolitical supply chain risks that plague competitors reliant on Chinese CDMOs. With robust IP protection extending into the 2040s and Orphan Drug Designation providing additional market exclusivity, Benitec operates in a competitive vacuum, as no other clinical-stage programs target OPMD.

The broader implications position Benitec as a platform leader rather than a single-product company. The "Silence and Replace" architecture addresses a fundamental limitation of traditional gene therapy: it can treat autosomal dominant disorders where toxic mutant proteins render simple gene replacement ineffective. This unlocks an entire class of previously undruggable genetic diseases. The company's leadership, including CEO Dr. Jerel Banks (who brings both M.D./Ph.D. credentials and biotechnology equity research experience) and board member Dr. Sharon Mates (who guided Intra-Cellular Therapies to a $14.6 billion acquisition by J&J), suggests preparation for either commercial scale-up or strategic acquisition. With potential pricing power in the $2-3 million range per treatment based on comparable gene therapies, and an enterprise value of approximately $250 million against a multi-billion dollar revenue opportunity, Benitec represents a compelling asymmetric risk-reward profile at the vanguard of curative genetic medicine.

Can a Wristband Read Your Mind Before You Move?Wearable Devices Ltd. (NASDAQ: WLDS) is pioneering a radical shift in human-computer interaction through its proprietary neural input interface technology. Unlike invasive brain-computer interfaces or basic gesture-recognition systems, the company's Mudra Band and Mudra Link decode subtle neuromuscular signals at the wrist, enabling users to control digital devices through intent rather than physical touch. What distinguishes WLDS from competitors like Meta's surface electromyography (sEMG) solutions is its patented capability to measure not just gestures, but quantifiable physical forces, including weight, torque, and applied pressure, opening applications far beyond consumer electronics into industrial quality control, extended reality (XR) environments, and mission-critical defense systems.

The company's strategic value lies not in hardware sales but in its planned evolution into a neural data intelligence platform. WLDS is executing a four-phase roadmap that transitions from consumer adoption (Phases 1-2) to data monetization through its Large Motor-Unit Action Potential Model (LMM), a continuously learning biosignal platform expected to launch by 2026. This proprietary dataset, generated from millions of user interactions, positions WLDS to offer high-margin licensing services to OEMs and enterprise clients, particularly in predictive health monitoring and cognitive analytics. With partnerships including Qualcomm and TCL-RayNeo, the company is building the infrastructure for what it envisions as the industry-standard neural interaction platform.

However, WLDS operates in a market defined by extraordinary potential and substantial execution risk. The global brain-computer interface market is projected to reach $6.2 billion by 2030, yet current wireless neural interface revenues remain modest at an estimated $1.5 billion by 2035, suggesting either a massive untapped opportunity or significant adoption barriers. The company's lean 26-34 person operation, $522,000 in 2024 revenue, and extreme stock volatility (Beta: 3.58, 52-week range: $1.00-$14.67) underscore its early-stage profile. Success hinges entirely on converting consumer adoption into the proprietary biosignal data required to train the LMM platform, which in turn must prove sufficiently valuable to command enterprise licensing agreements at scale.

WLDS represents a calculated bet on the convergence of AI, wearable computing, and neurotechnology, a company that could either establish the foundational infrastructure for touchless interaction across XR, healthcare, and defense sectors or struggle to bridge the gap between technological capability and market validation. Its military contracts and robust IP portfolio covering force-measurement capabilities provide technical credibility, but the path to ubiquitous platform adoption (Phase 4) requires flawless execution across consumer seeding, data accumulation, and B2B conversion, a multiyear journey with no guarantee of arrival.

Can a $251 Billion Backlog Predict the Future?RTX Corporation has positioned itself at the intersection of escalating global defense imperatives and the recovery of commercial aviation, generating a formidable $251 billion backlog that provides unprecedented revenue visibility. The company reported strong Q3 2025 results with sales of $22.5 billion (up 12% year-over-year) and raised its full-year guidance, driven by double-digit organic growth across all segments. This performance reflects RTX's dual-market advantage: surging defense spending, with global military expenditure reaching $2.7 trillion in 2024 and NATO's new 5% GDP target by 2035, combined with recovering commercial aviation demand projected to exceed 12 billion passengers by 2030.

RTX's technological superiority centers on proprietary Gallium Nitride (GaN) semiconductor innovations that power next-generation radar systems, creating substantial barriers to entry. The company's LTAMDS radar delivers twice the power of legacy Patriot systems while eliminating battlefield blind spots, and the newly launched APG-82(V)X radar enhances fighter aircraft capabilities against advanced threats. Major contracts underscore this dominance, including a $5 billion Army award for the Coyote counter-drone system, which extends through 2033. RTX has committed over $600 million to manufacturing expansion this year alone, with the Redstone Missile Integration Facility expansion specifically targeting increased production of Standard Missile variants and counter-hypersonic solutions.

On the commercial side, Pratt & Whitney's GTF Advantage engine achieved EASA certification in Q4 2025, resolving earlier durability challenges with a design targeting double the time-on-wing compared to prior models. This breakthrough secures RTX's control over the A320neo and A220 fleets, guaranteeing decades of high-margin maintenance, repair, and overhaul revenue. Collins Aerospace's global network of over 70 MRO sites and flexible AssetFlex program capitalizes on supply chain constraints that force airlines to invest more heavily in fleet maintenance rather than new aircraft purchases.

The financial trajectory appears compelling: analysts project free cash flow will surge from $5.5 billion in 2023 to $9.9 billion by 2027, representing 15.5% annualized growth and compressing the price-to-FCF multiple from 31.3x to 17.3x. Wall Street maintains a consensus "Buy" rating across thirteen covering firms with zero sell recommendations. RTX's 60,000-patent portfolio, built on $7.5 billion in annual R&D spending, spans advanced materials, AI, autonomy, and next-generation propulsion, creating a self-reinforcing cycle where investment drives proprietary technology that secures long-term government contracts. With an affirmed BBB+ credit rating and stable outlook, RTX presents a structurally sound investment thesis built on geopolitical necessity, technological moats, and expanding cash generation.

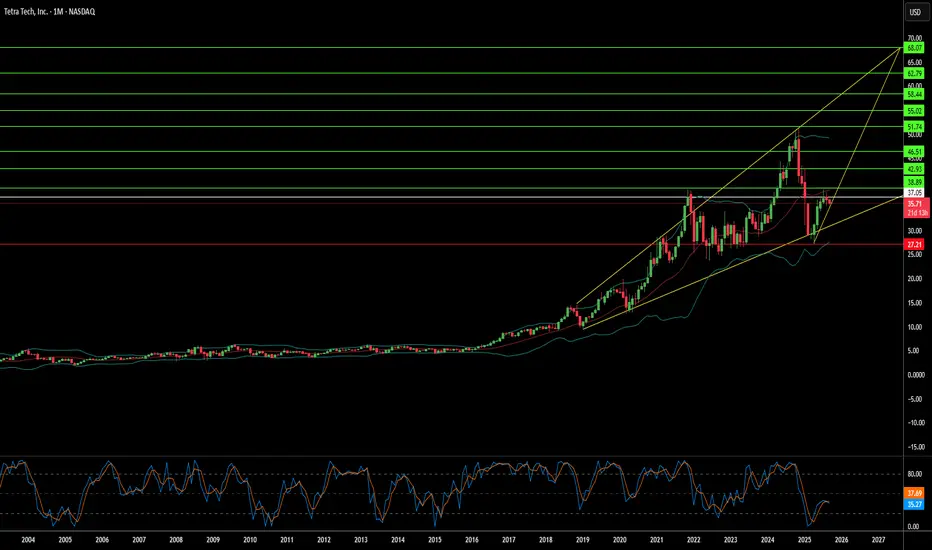

When Does Destruction Create Trillion-Dollar Opportunity?Tetra Tech's remarkable market surge represents a confluence of technological innovation and geopolitical opportunity that positions the Pasadena-based engineering firm at the epicenter of global reconstruction efforts. The company has distinguished itself through substantial intellectual property holdings—over 500 global patents across infrastructure and environmental technologies—and cutting-edge capabilities, including an AI innovation lab focused on robotics, cloud migration, and cognitive systems that automate complex engineering workflows. This technological foundation has translated into impressive financial performance, with the company reporting approximately 11% revenue growth year-over-year in Q3 2025 and maintaining a record backlog of $4.15 billion while earning "Moderate Buy" ratings from analysts with price targets in the low $40s.

The strategic value proposition extends far beyond traditional engineering services into the realm of conflict-zone reconstruction, where Tetra Tech's four decades of experience in war-torn regions uniquely position it for emerging opportunities. The company already maintains USAID contracts in conflict areas, including a $47 million project in the West Bank and Gaza, and has demonstrated critical capabilities in Ukraine through generator deployment, power grid restoration, and explosive ordnance clearance operations. These competencies align precisely with the skill sets required for large-scale reconstruction efforts, from debris removal and pipeline repair to the engineering of essential infrastructure systems, including roads, power plants, and water treatment facilities.

Gaza's reconstruction represents a potentially transformative business opportunity that could fundamentally alter Tetra Tech's trajectory. Conservative estimates place Gaza's infrastructure rebuilding needs at $18-50 billion over approximately 14 years, with immediate priorities including roads, bridges, power generation, water treatment systems, and even airport reconstruction. A major contract in this range—potentially $10-20 billion—would dwarf Tetra Tech's current market capitalization of approximately $9.4 billion and could significantly increase the company's annual revenue. The strategic importance is amplified by broader geopolitical initiatives, including proposed Gaza trade corridors linking Asia and Europe as part of U.S.-led stability plans that envision Gaza as a revived commercial hub.

Institutional investors have recognized this potential, with 93.9% of shares held by institutional owners and recent substantial position increases by firms like Paradoxiom Capital, which acquired 140,955 shares worth $4.1 million in Q1 2025. The convergence of global infrastructure demand—estimated at $64 trillion over the next 25 years—with Tetra Tech's proven expertise in high-stakes reconstruction projects creates a compelling investment thesis. The company's combination of advanced technology capabilities, extensive patent portfolio, and demonstrated success in complex geopolitical environments positions it as a primary beneficiary of the intersection between global instability and the massive capital deployment required for post-conflict reconstruction.