Microsoft Struggling?Microsoft

Short Term - We look to Sell at 306.08 (stop at 317.41)

We look to sell rallies. We look to set shorts in early trade for a further test of the fragile looking support. Levels close to the 50% pullback level of 309.47 found sellers. The trend of lower highs is located at 315.00. Expect trading to remain mixed and volatile.

Our profit targets will be 272.25 and 254.00

Resistance: 300.00 / 310.00 / 320.00

Support: 270.00 / 260.00 / 240.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

Search in ideas for "MICROSOFT"

Microsoft Buy SetupMicrosoft - Short Term - We look to Buy at 303.35 (stop at 296.56)

We look to buy dips. Previous resistance, now becomes support at 300.00. Trading has been mixed and volatile. The bias is still for higher levels and we look for any dips to be limited.

Our profit targets will be 325.34 and 336.10

Resistance: 320.00 / 340.00 / 350.00

Support: 300.00 / 270.00 / 250.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

MICROSOFT - Long PositionStrong corporate earnings from Microsoft. Software giant Microsoft reported record quarterly revenue above $50 billion for the first time, beating expectations, and offered a rosy outlook for the current quarter last Tuesday. That helped boost stock market futures for the next day, though the gains were given back by volatility driven by an announcement from the Fed The Dow Drops as Powell Talks — and What Else Is Happening in the Stock Market Today The market sank as Chairman Jerome Powell signaled the possibility of many more rate increases than the stock market had been expecting.

Microsoft (MSFT) | The safest place to buy🔥Hello traders, Microsoft in daily timeframe , this analysis has been prepared in daily timeframe but has been published for a better view in 2 day timeframe.

It is better not to talk about the general nature of this wave and only explain the counted part of the wave.

Based on the counting of the first wave 1 and 2, it has ended in a very normal state and now we are inside the third wave.

From wave 3, waves 1, 2, and 3 are completed, and now wave 4 is formed. As we previously thought, wave 4 was formed in the form of a flat, and from this flat, waves a and b are completed, and the structure of wave c is formed.

Wave c is at the end of its trend, both in terms of the number of waves and the ratio between waves a and b of the flat, as well as the ratio of the depth of this correction to wave 4, but the probability of correction to Fibo will be 0.38 and then the wave starts breaking the green circle. 5 is approved.

This analysis is also fielded if the trend moves beyond the resistance indicated by the warning sign.

🙏If you have an idea that helps me provide a better analysis, I will be happy to write in the comments🙏

❤️Please, support this idea with a like and comment!❤️

Microsoft: Buying at Key Level Microsoft - Short Term - We look to Buy at 306.00 (stop at 290.00)

We look to buy dips. Previous resistance, now becomes support at 305.00. Trend line support is located at 310.00. We have a 61.8% Fibonacci pullback level of 280.00 from 350.00 to 306.74. The bias is still for higher levels and we look for any dips to be limited. Further upside is expected although we prefer to set longs at our bespoke support levels at 305.00, resulting in improved risk/reward.

Our profit targets will be 349.50 and 380.00

Resistance: 345.00 / 350.00 / 360.00

Support: 305.00 / 280.00 / 260.00

Disclaimer – Saxo Bank Group. Please be reminded – you alone are responsible for your trading – both gains and losses. There is a very high degree of risk involved in trading. The technical analysis, like any and all indicators, strategies, columns, articles and other features accessible on/though this site (including those from Signal Centre) are for informational purposes only and should not be construed as investment advice by you. Such technical analysis are believed to be obtained from sources believed to be reliable, but not warrant their respective completeness or accuracy, or warrant any results from the use of the information. Your use of the technical analysis, as would also your use of any and all mentioned indicators, strategies, columns, articles and all other features, is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness (including suitability) of the information. You should assess the risk of any trade with your financial adviser and make your own independent decision(s) regarding any tradable products which may be the subject matter of the technical analysis or any of the said indicators, strategies, columns, articles and all other features.

Please also be reminded that if despite the above, any of the said technical analysis (or any of the said indicators, strategies, columns, articles and other features accessible on/through this site) is found to be advisory or a recommendation; and not merely informational in nature, the same is in any event provided with the intention of being for general circulation and availability only. As such it is not intended to and does not form part of any offer or recommendation directed at you specifically, or have any regard to the investment objectives, financial situation or needs of yourself or any other specific person. Before committing to a trade or investment therefore, please seek advice from a financial or other professional adviser regarding the suitability of the product for you and (where available) read the relevant product offer/description documents, including the risk disclosures. If you do not wish to seek such financial advice, please still exercise your mind and consider carefully whether the product is suitable for you because you alone remain responsible for your trading – both gains and losses.

Microsoft (MSFT) | The best scenario for climbing📝Hello traders, Microsoft in daily timeframe , this analysis has been prepared in daily timeframe but has been published for a better view in 2 day timeframe.

It is better not to talk about the general nature of this wave and only explain the counting part.

Based on the counting of the first wave 1 and 2, it has ended in a very normal state and now we are inside the third wave.

From wave 3, waves 1, 2 and 3 are completed and now wave 4 is formed. We assume that wave 4 is formed in the form of a flat and from this flat 2 waves are needed to complete.

The end point of this wave, considering wave 2, which is a deep wave, can be around 0.23 and 0.38, and it is better to start the upward movement for wave 3 by hitting the trend line and breaking the upper side of the channel.

The target for Wave 3 is a multi-fibo collision.

If the warning sign is broken down, the field analysis is not done, but it returns to normal.

🙏If you have an idea that helps me provide a better analysis, I will be happy to write in the comments🙏

❤️Please, support this idea with a like and comment!❤️

MICROSOFT Would you consider $185 "a healthy pull back"?Just curious to know your opinion on that as the post August High flag (Channel Down) looks extremely similar to Microsoft's September - December 2019 sequence. The RSI is similar too. Since then it has touched the 1W MA50 (blue trend-line) one more time, last March (COVID sell-off).

So would you consider this a healthy pull-back or should it ring a few alarms?

** Please support this idea with your likes and comments, it is the best way to keep it relevant and support me. **

--------------------------------------------------------------------------------------------------------

!! Donations via TradingView coins also help me a great deal at posting more free trading content and signals here !!

🎉 👍 Shout-out to TradingShot's 💰 top TradingView Coin donor 💰 this week ==> TradingView

--------------------------------------------------------------------------------------------------------

Microsoft Holding 21 moving average, looking to retest backSince 2018 Microsoft has stuck with it's 21 EMA. After extending a bit there is a bearish engulfing pattern on the weekly chart. Microsoft Looking to retest back to the 21 EMA

MICROSOFT CORPORATION (MSFT) MONTHLY LONGWell, Microsoft Corporation (MSFT) just made it to the $1 trillion dollar mark. And it happens to be worth more than two times of Belgium's GDP. It also happens to be worth more than Appe and Amazon. What a day for them. Well as an investor, you would not want to buy the tops if there are not signs of a continuation. What's worse is that the price is making a parabolic move, reminiscent of Bitcoin. Well i don't think this is a bubble, or that there will be a sharp retracement, but i do expect some form of retracement and new players can buy after this retracement is finished. If the share price does not retrace, you could look at buying a breakout of a certain price level. Today i am not going deeper into technical analysis, but simply reflecting on this milestone. Toast to the equity market.

MICROSOFT: NO CONFIRMATIONSame with Google the same with Microsoft, last Jul the price move up until it hit the Upper-line of the channel and then it back downward, but if we zoom out the chart we can find that the price goes now as a sideways (flat), now the price in the middle so it's hard to guess the next move where it going to be (especially when market close). but I can tell about price current position that the next move has to be down so it can hit one of two powerful support's (the lower-line of the channel / the support line in 105.9 levels), after hitting one of these supports it makes sense for the price to go up.

Microsoft. There is still potential for the price to decline.Hello traders and investors!

Let's take a look at the situation with Microsoft stocks. I believe there is still potential for the price to decline.

Weekly Timeframe

On the weekly TF, there is an attempt to reverse the long trend. The first seller's impulse has been formed. The level of the last buyer’s impulse start is 445.66, and the level of the last seller’s impulse start is 468.35. The end of the last seller's impulse is at 385.58.

Key candle in the seller's impulse is from July 24 (largest volume in the impulse, marked as "KC" on the chart). It was tested by the buyer on August 19. The test level is 426.70. The buyer missed the 50% level of the seller's impulse (426.97) by 27 cents. Then, the buyer attacked the test level with two candles on increased volume, bringing the price above the 50% level, but the seller pushed the price back below the test level (426.70), forming a seller's zone above (red rectangle on the chart). Further price decline is likely, with the first target at 400.8, which is the start of the last buyer's sub-impulse on the weekly TF.

Daily Timeframe

On the daily TF, there’s a sideways range (formed on August 22, with point 4). The upper boundary is 432.15, and the lower boundary is 385.58. The relevant seller's vector is 6-7, with the first potential target being 400.8 (then 385.58).

The buyer's vector 5-6 broke above the upper boundary of the range, gathered volume, and the seller returned the price to the range, forming a seller's zone at the upper boundary. This zone was tested on September 26, after which the seller's continuation began. The buyer attempted a recovery on September 30 with increased volume but failed to deliver results. Yesterday, the seller engulfed the buyer's candle.

Highlights

On both the weekly and daily TFs, the priority is to look for selling opportunities. The last daily candle has increased volume, making it a good point to start looking for sell opportunities. On the daily TF, possible threats to short positions include the 50% level of the last buyer's impulse at 413.72 and the buyer's zone with an upper boundary at 410.65 (green rectangle on the chart).

It makes sense to consider buying opportunities when the buyer shows strength, for example, when interacting with the levels of 400 or 385 and defending them.

How to decode candle volumes is explained here

Good luck with your trading and investments!

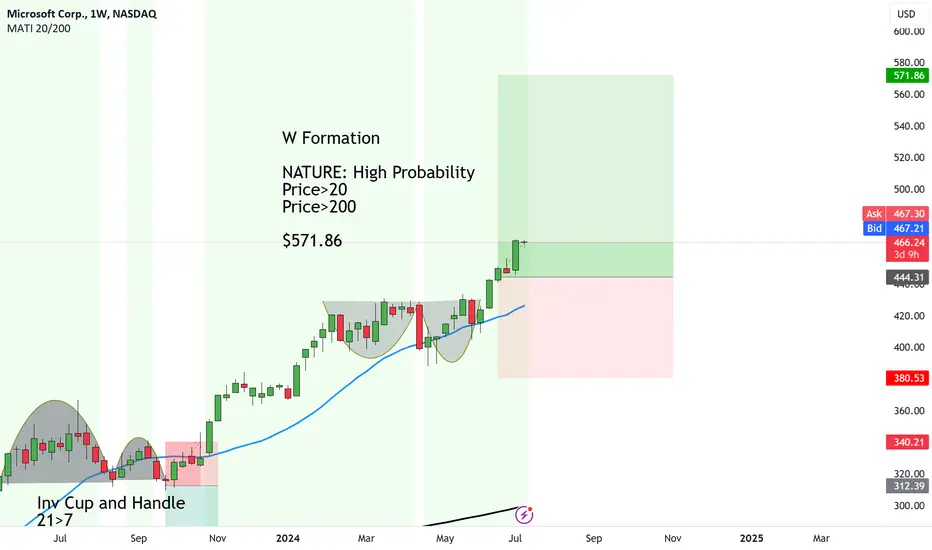

Microsoft following the tech footsteps or major upside to $571.8W Formation formed on Microsoft. The price broke up and out of the formation and now it's heading on up.

We see a similar trend with Apple and the Nasdaq so they are all following suites.

NATURE: High Probability

Price>20

Price>200

Target $571.86

MICROSOFT....SELL TO $232Microsoft stock is forming a bearish continuation from the partial head and shoulder formed between 24th February and 27th April this year. Hence I'm looking for a possible short of this stock. which will definitely closed between the 52 week range!!!

Microsoft bullish longThese are my thoughts on MSFT. They are meant to give you an idea, not trading advice.

My targets on Microsoft. Can't say much more than that.

Hope it can help you.

Please be careful, as the market never gives you certainties, only probabilities!

ALWAYS REMEMBER THIS WHEN YOU TRADE

Microsoft Manipulation - Not Posted by Bill GatesHello Traders.

Please see highlighted area of the chart.

What has Microsoft developed in the last 5 years to make them name-worthy?

Here's the answer: nothing.

-dysonring2050

MSFT | Microsoft’s $4 Billion OpenAI SurpriseMicrosoft’s September quarter included a surprising detail !

A $4.1 billion loss tied to its investment in OpenAI

That suggests OpenAI’s own losses are far deeper than expected around $15 billion in the most recent quarter.

The timing is notable. Microsoft and OpenAI just reworked their partnership, converting OpenAI into a for profit public benefit corporation (PBC). Under the new structure, Microsoft owns 27% of the company and has secured long-term access to its models. OpenAI, in turn, can now expand on other cloud providers, though it has committed to spending $250 billion on Azure.

For context, OpenAI is expected to bring in about $13 billion in revenue across all of 2025.

If the AI boom shows any cracks, this could be the place to watch. OpenAI’s heavy spending on infrastructure may eventually outpace its funding capacity, creating ripple effects for investors and suppliers. There’s plenty of money flowing for now, but at some point, the costs will catch up.

Here’s what stood out this quarter.

Today at a glance:

Microsoft’s Q1 FY26 results

The new OpenAI agreement

Key takeaways from the earnings call

What’s driving performance

1. Microsoft’s Q1 FY26

Income Statement:

Revenue up 18% year over year to $77.7 billion ($2.3 billion above estimates)

Gross margin steady at 69%

Operating margin 49%, up two points

EPS $4.13, beating by $0.47

Product and Service Highlights:

☁️ Server products and cloud services: $28.9 billion (+30%)

📊 M365 Commercial products and cloud services: $24.0 billion (+17%)

🎮 Gaming: $5.5 billion (-2%)

👔 LinkedIn: $4.7 billion (+10%)

🪟 Windows and Devices: $4.6 billion (+5%)

🔎 Search and news advertising: $3.7 billion (+15%)

💻 Other: $6.4 billion (+15%)

Core Segments: Microsoft reorganized its business lines last year to better reflect how it now operates.

Productivity and Business Processes: up 17% to $33.0 billion ($0.7 billion above forecasts), led by strong M365 growth and higher revenue per user from Copilot adoption.

Intelligent Cloud: up 28% to $30.9 billion ($0.7 billion beat), driven by Azure strength across workloads.

More Personal Computing: up 4% to $13.8 billion ($0.9 billion beat), helped by search ads and offsetting weaker Xbox hardware.

Microsoft Cloud revenue rose 25% to $49.1 billion and now makes up 63% of total sales. Growth was broad, powered by Azure and M365. Copilot use is growing fast, though its full revenue impact is still ahead.

Azure remains the main growth engine, showing no slowdown this quarter.

Consumer M365 saw another acceleration, lifted by a price hike and a 7% increase in subscribers.

Xbox revenue leveled off after completing the Activision deal; Game Pass growth couldn’t offset weaker hardware sales.

Advertising grew 15%, matching Google Search’s pace from a much smaller base.

Cash Flow

Operating cash flow up 32% to $45.1 billion

Free cash flow up 33% to $25.7 billion

Balance Sheet

Cash and investments: $102 billion

Long-term debt: $35 billion

What It All Means ?! Azure demand still outpaces supply. Growth will fluctuate quarter to quarter. Both AWS and Google Cloud also picked up speed this period.

Capital spending surged. CapEx reached $34.9 billion (+74%), split between chips and data-center construction. Microsoft plans to double its data-center footprint within two years, front-loading investment to relieve Azure capacity limits.

Infrastructure challenges persist. Power and space remain constraints. Management expects Azure to grow 37% next quarter but warned that supply bottlenecks will continue.

Visibility improving. Commercial remaining performance obligations (RPO) rose 51% to $392 billion, mostly tied to long-term AI and infrastructure deals.

OpenAI weighed on results. “Other expenses” included a $4.1 billion loss from Microsoft’s stake in OpenAI, offset by positive interest income elsewhere.

Capital returns remain strong. Despite heavy spending, Microsoft returned $10.7 billion to shareholders through dividends and buybacks, unlike Amazon, which still doesn’t repurchase stock or pay dividends.

2. The New OpenAI Agreement

🤝 Microsoft + OpenAI Rewrite the Rules

The new deal changes how the two companies work together—and where they compete. Microsoft keeps its advantage in Azure scale for years to come, but OpenAI now has more flexibility to partner elsewhere and pursue AGI on its own path.

What Microsoft Gets:

A 27% stake in the new OpenAI public benefit corporation, valued around $135 billion.

Commercial rights to OpenAI models through 2032, including anything that comes after an AGI breakthrough.

A $250 billion commitment from OpenAI for Azure spending.

No more exclusive hosting OpenAI can now use other cloud providers.

If OpenAI claims to reach AGI, an independent panel must verify it.

Once AGI is confirmed (or by 2030, whichever comes first), revenue sharing ends and Microsoft’s research access narrows.

Microsoft can still work on AGI independently, but its compute use is limited if it’s built on OpenAI tech.

Why It Matters MoonMaster ?

These terms remove some valuation uncertainty for Microsoft, letting investors more clearly account for its OpenAI stake. The Azure commitment also helps justify record AI infrastructure spending with solid visibility into future demand. But OpenAI’s new freedom to fundraise and expand across multiple clouds and to build out new revenue streams like advertising puts more pressure on AWS and raises fresh competitive questions for Google.

🎮 Game Pass Under Pressure

Microsoft just raised prices and revamped Game Pass, and fans noticed! (here we go again)

What Changed ?! The Ultimate tier jumped 50% to $29.99 per month. Microsoft says the higher price comes with more content 400+ games, 75+ day-one titles, Ubisoft+ Classics, and 1440p cloud streaming but the increase is steep.

Dont miss KEEPER and Ninja Gaiden 4 on gamepass by the way!

PC Game Pass also rose from $11.99 to roughly $16.49 per month. The Call of Duty add-on discount quietly disappeared, and rollout timing varied by region.

Why Now ? Reports suggest Call of Duty: Black Ops 6 on day-one Game Pass last year boosted subscribers but cost as much as $300 million in lost full-price sales. The new pricing is meant to rebalance that trade-off.

Competitive Context:

Sony has nudged PlayStation Plus prices upward, but it doesn’t offer day one releases. That keeps full-price game sales healthier on PlayStation.

Microsoft’s Strategy:

CEO Satya Nadella described Xbox as a platform that spans devices—TVs, PCs, handhelds, and cloud apps so the console is “an endpoint, not the endpoint.” The goal is to make Xbox services available anywhere, even on rival platforms.

What It Means for Game Pass:

More devices mean a bigger audience, but less leverage from console exclusives. Growth will have to come from higher average revenue per user (through tiering, add-ons, and premium pricing) and from monetizing major IP titles at full price when it makes sense.

Bottom Line:

Game Pass is shifting from a growth-at-any-cost model to a premium subscription bundle built around strong content. The “everything is Xbox” approach broadens reach but reduces the old lock-in advantage. The key will be whether higher ARPU and pricing discipline can offset churn from price hikes. If not, Sony could keep its lead while regulators keep a close eye on consolidation.

3. Earnings Call Takeaways

On AI Scale and Capacity: “We will increase our total AI capacity by over 80% this year and roughly double our total data center footprint over the next two years. Fairwater (WI) alone will scale to 2 GW.”

Azure’s supply limits are real. Microsoft is front-loading construction to catch up with demand.

On Demand Signals: “Microsoft Cloud revenue hit $49 billion, up 26%. Commercial RPO climbed 50% to nearly $400 billion, with an average contract duration of about two years.”

That $368 billion backlog gives Microsoft strong revenue visibility and supports its aggressive AI spending.

On CapEx and Cash Flow: “We now expect FY26 CapEx growth to be higher than FY25.”

The spending peak isn’t here yet. Management wants to secure market share while demand stays strong.

On Copilot and Agent Adoption:

“We now have 900 million monthly active users of AI features. First-party Copilots topped 150 million MAU. Copilot chat adoption rose 50% quarter over quarter. Agent users doubled. PwC added 155,000 seats this quarter, with over 200,000 now deployed and 30 million interactions in six months.”

The shift from AI “features” to autonomous agents is accelerating. Usage is deepening, suggesting pricing power and future revenue growth.

On AI Bubble Concerns and Concentration Risk:

“We’ve been short on capacity for many quarters. Demand continues to rise. We avoid overly concentrated deals and are building a flexible fleet for both first- and third-party use”

In short, Microsoft’s expansion isn’t reckless. Its contracts match the lifespan of its infrastructure, keeping the risk of overbuilding low.

4. What Moves the Needle

🔌 Azure Demand: OpenAI’s $250 billion Azure commitment gives Microsoft strong visibility into future AI workloads, but execution risk remains high. Watch cloud market share trends.

☁️ Multi-Cloud Dynamics: OpenAI can now work with AWS (likely the main beneficiary). Oracle’s outlook improves with funding clarity. Google could face pressure if OpenAI pushes into ads and browser-based agents.

💸 CapEx Supercycle: Microsoft expects AI infrastructure spending to top $110 billion in FY26. Profitability depends on keeping data centers highly utilized as competition ramps up.

🧠 Copilot Monetization: The potential is still huge, but Microsoft must convert free or bundled users into paid seats. Sales teams are focused on packaging and attach-rate growth.

🎮 Gaming Mix: New Game Pass tiers and Activision titles will test whether Microsoft can lift ARPU and engagement while console sales normalize.

⚖️ Regulatory Headwinds: The EU already forced Microsoft to unbundle Teams, and regulators in the UK and EU continue to scrutinize AI and cloud partnerships. Pricing and bundling rules could shift again.

Let’s see how far Microsoft can drive it before the tank runs dry..

Microsoft's Remarkable Ascent in AI: A Key to its 40% YTD Stock Microsoft's Remarkable Ascent in AI: A Key to its 40% YTD Stock Surge

Microsoft's stock has experienced an impressive 40% year-to-date surge, driven significantly by its dominant position in the realm of artificial intelligence (AI). With its early investments in AI, Microsoft has gained a substantial lead over its competitors. Companies like Amazon and Alphabet have been playing catch-up in the first half of the year, striving to match Microsoft's strides in the AI arena.

However, Microsoft's strength extends beyond AI, as it boasts a portfolio of high-performing productivity services with millions of users worldwide. This strong brand recognition and extensive user base position Microsoft as a potential go-to choice for anyone seeking AI services. Here are three key insights that savvy investors are aware of regarding Microsoft's current standing:

Charting a Course Towards $10 Billion in AI Revenue:

During the recent Goldman Sachs Communacopia & Technology Conference, Microsoft's Chief Financial Officer, Amy Hood, reaffirmed the company's ambitious projection: the AI division is poised to surge past the $10 billion revenue milestone at an unprecedented pace, surpassing all previous business endeavors.

Microsoft's strategic investment of $1 billion in the ChatGPT developer, OpenAI, in 2019, has been instrumental in catalyzing its ascendancy in the AI realm. This partnership has granted Microsoft exclusive licenses to numerous OpenAI AI models, leading to transformative enhancements across various in-house platforms. Iconic products like Word, Excel, Bing, and Azure have all undergone substantial AI-driven upgrades. Furthermore, Microsoft's subscription-based Microsoft 365 office suite is on the brink of introducing an array of AI-infused products, ushering in a new era of productivity.

The transformative potential of AI extends across various industries, including education, healthcare, consumer goods, robotics, autonomous vehicles, and more. Persuading businesses to integrate AI tools into their daily operations holds great promise, and Microsoft is well-positioned to capitalize on this trend.

With a commanding presence through its cloud platform, Azure, and an extensive suite of productivity tools, Microsoft is poised to become the preferred destination for enterprises seeking AI services to enhance operational efficiency. The combination of iconic brands—Windows, Office, and Azure—may give Microsoft an edge over formidable rivals like Amazon in the AI-driven landscape.

Strategic Investment in the Semiconductor Arena:

Microsoft's deep involvement in semiconductor technology lays a strong foundation for the long-term growth of the AI market. Recognizing the importance of robust hardware in the AI industry, Microsoft has made steady investments in various chip manufacturers to diversify the ecosystem, which has long been dominated by Nvidia.

Earlier this year, Bloomberg reported Microsoft's substantial financial and engineering support for Advanced Micro Devices (AMD) in its AI chip expansion efforts. This month, the chip startup d-Matrix secured $110 million in funding, with Microsoft among its prominent backers.

D-Matrix focuses on the "inference" facet of AI processing, avoiding direct competition with Nvidia in training large AI models. Microsoft's investment strategy here represents strategic diversification, aligning with a distinct segment of the chip market, separate from its engagements with AMD and Nvidia.

While d-Matrix's 2023 revenue projection is around $10 million, primarily from chip testing, it anticipates substantial growth as demand for AI chips rises. The company targets annual revenues ranging from $70 million to $75 million within the next two years.

Sustained Dividend Growth:

Unlike tech giants like Amazon and Alphabet, which have forgone dividend offerings, Microsoft has remained a dividend-friendly player, positioning itself at the forefront of the market. The company boasts a dividend yield of 0.81%, a notable figure compared to Apple's 0.53%.

What truly underscores Microsoft's appeal to dividend-seeking investors is its consistent upward trajectory in dividend yield over the past decade. Microsoft's cash dividend has grown from $0.28 in 2013 to an impressive $0.68 this year. As Microsoft expands its presence in the AI landscape, which is projected to sustain a robust compound annual growth rate of 32% until 2030, the potential for amplified earnings augments the possibility of further dividend increases.

While Microsoft's dividend yield may not rival that of industry peers like Verizon, which offers a substantial yield of approximately 7%, the company's unwavering commitment to growth solidifies its status as an attractive investment proposition, making its stock increasingly compelling.

In conclusion, Microsoft's strategic positioning in the AI industry, its investments in the semiconductor sector, and its consistent dividend growth make it a standout choice for investors seeking long-term value and potential growth in their portfolios.

MICROSOFT STOCK PREDICTIONS FOR 2016 AND 20172016/11/18. Microsoft stock forecast for next months and years.

Microsoft stock price predictions for November 2016.

The forecast for beginning of November 58. Maximum value 61, while minimum 54. Averaged Microsoft stock price for month 58. Price at the end 57, change for November -1.72%.

Microsoft stock predictions for December 2016.

The forecast for beginning of December 57. Maximum value 59, while minimum 53. Averaged Microsoft stock price for month 56. Price at the end 56, change for December -1.75%.

Microsoft stock price predictions for January 2017.

The forecast for beginning of January 56. Maximum value 59, while minimum 53. Averaged Microsoft stock price for month 56. Price at the end 56, change for January 0.00%.

Microsoft stock predictions for February 2017.

The forecast for beginning of February 56. Maximum value 60, while minimum 54. Averaged Microsoft stock price for month 57. Price at the end 57, change for February 1.79%.

Microsoft stock price predictions for March 2017.

The forecast for beginning of March 57. Maximum value 64, while minimum 56. Averaged Microsoft stock price for month 59. Price at the end 60, change for March 5.26%.

Microsoft stock predictions for April 2017.

The forecast for beginning of April 60. Maximum value 61, while minimum 55. Averaged Microsoft stock price for month 59. Price at the end 58, change for April -3.33%.

Microsoft stock price predictions for May 2017.

The forecast for beginning of May 58. Maximum value 65, while minimum 57. Averaged Microsoft stock price for month 60. Price at the end 61, change for May 5.17%.

Microsoft stock predictions for June 2017.

The forecast for beginning of June 61. Maximum value 61, while minimum 55. Averaged Microsoft stock price for month 59. Price at the end 58, change for June -4.92%.

Microsoft stock price predictions for July 2017.

The forecast for beginning of July 58. Maximum value 65, while minimum 57. Averaged Microsoft stock price for month 60. Price at the end 61, change for July 5.17%.

Microsoft stock predictions for August 2017.

The forecast for beginning of August 61. Maximum value 61, while minimum 55. Averaged Microsoft stock price for month 59. Price at the end 58, change for August -4.92%.

Microsoft stock price predictions for September 2017.

The forecast for beginning of September 58. Maximum value 61, while minimum 55. Averaged Microsoft stock price for month 58. Price at the end 58, change for September 0.00%.

Microsoft stock predictions for October 2017.

The forecast for beginning of October 58. Maximum value 63, while minimum 55. Averaged Microsoft stock price for month 59. Price at the end 59, change for October 1.72%.

Microsoft stock price predictions for November 2017.

The forecast for beginning of November 59. Maximum value 65, while minimum 57. Averaged Microsoft stock price for month 61. Price at the end 61, change for November 3.39%.

Microsoft stock predictions for December 2017.

The forecast for beginning of December 61. Maximum value 68, while minimum 60. Averaged Microsoft stock price for month 63. Price at the end 64, change for December 4.92%.

Microsoft stock price predictions for January 2018.

The forecast for beginning of January 64. Maximum value 69, while minimum 61. Averaged Microsoft stock price for month 65. Price at the end 65, change for January 1.56%.

BLUE CHANNEL- Monthly and Weekly UP

Double Lines- Peak of .com bubble and All-Time High from 1999/2000 *Broken

Microsoft | Fundamental Analysis | MUST READ | LONG SETUP ⚡️The market was on the upswing yesterday as receding fears of Omicron strain and renewed expectancy for the "Build Back Better" bill led to significant gains in stocks. Amid all the exciting moves in battered cyclical stocks and small-cap stocks, another important story -- actually, two stories -- surrounding technology star Microsoft may have slipped past your attention. These headlines were not only important in and of themselves, but also in terms of what they connote for Microsoft's growth prospects.

Two days ago, the European Commission approved Microsoft's upcoming deal with Nuance Communications. Microsoft announced a $16 billion deal with Nuance back in April, but its prospects have never been entirely certain. Microsoft is a large and powerful technology company, which means antitrust concerns are always a danger to any deal -- especially a big one. The Nuance deal is the second-largest for Microsoft after its 2016 acquisition of LinkedIn.

But Microsoft seems to know what it's doing when it targets a company. That wasn't evident last year when executives of most FAANG stocks had to testify before Congress about their market power. And Europe has been particularly tough on big tech companies in recent years, even tougher than the U.S.

Nevertheless, the commission concluded that the Nuance acquisition would not significantly reduce competition in artificial intelligence (AI) in health care. Now that the merger is set to take place, Nuance's AI capabilities are expected to strengthen Microsoft's already strong cloud-based healthcare services.

During the merger, CEO Satya Nadella said: "Nuance provides a level of AI at the point of care and is a pioneer in the real-world application of enterprise AI. AI is a critical technology priority, and healthcare is its most relevant application. Together with our partner ecosystem, we will put advanced AI solutions in the hands of professionals everywhere to drive better decisions and create more meaningful connections, accelerating the growth of Microsoft Cloud for Healthcare and Nuance."

Over the past two years, Microsoft has managed to maintain outstanding cloud growth through the introduction of industry clouds. It looks like Nuance will fill some of the gaps in Microsoft's healthcare capabilities.

With the ability to still make large and meaningful acquisitions, MSFT seems to have an advantage over some competitors who seem to be attracting more antitrust attention for some reason. This ability may let it support growth longer than skeptics believe.

Following this good news, Microsoft wasted no time in announcing another acquisition. This time Microsoft will acquire digital advertising technology company Xandr from AT&T. Xandr is the result of a merger of AT&T's own digital advertising capabilities with AppNexus, the programmatic advertising company it acquired for $1.6 billion in 2018.

AT&T had hoped to turn Xandr into a powerful programmatic advertising company, but apparently, the scale wasn't enough to justify keeping it. AT&T has recently sought to sell non-core assets to pay down debt in anticipation of the spin-off and merger of WarnerMedia with Discovery. The terms of the deal have not been disclosed, so we don't know how much Microsoft will pay.

Microsoft will likely try to merge Xandr with Bing, its second-ranked search engine, to create better programmatic and artificial intelligence-driven advertising capabilities. Bing is often something of secondary consideration for Microsoft investors, but it's not worth telling management. Microsoft seems intent on developing its digital advertising capabilities to compete with the dominant "walled gardens" of digital advertising, especially since privacy restrictions could open up competitive opportunities.

While many are willing to settle for Microsoft's enterprise software alone, the tenacity to push into other areas of growth is admirable and is music to the ears of this happy shareholder. If there is any danger of over-diversifying the business away from core capabilities, as AT&T has done, it has not manifested itself in Microsoft's financial performance.

After rising 43% over the past 12 months, marking another successful year for the market, and finding itself just below historic highs at $327 per share, Microsoft may have investors wondering if the company can continue that streak. After all, it's harder to grow fast the bigger you get.

However, people said this a few years ago about Microsoft when the stock price was still in double digits. Earnings in several of the company's core businesses remain strong, and these two new acquisitions demonstrate management's tenacity in pursuing growth across an impressive portfolio.

MICROSOFT'S Fiscal 2023 Q4 Results: Assessing Growth and....Microsoft's Fiscal 2023 Q4 Results: Assessing Growth and Profitability

Investors are eagerly anticipating Microsoft's fiscal 2023 fourth-quarter results, set to be unveiled on July 25. The upcoming report holds significance as it is expected to include the company's outlook for fiscal year 2024, making it a crucial event for evaluating Microsoft's growth opportunities, profitability, and cash demand trends.

When considering Microsoft as an investment, three key factors set it apart from others.

Diverse Business:

Microsoft's strength lies in its diverse business offerings. Unlike companies that focus on specific industries or technologies, Microsoft provides exposure to various growth niches, including enterprise cloud services, AI, productivity software, and more. Owning Microsoft allows investors to capitalize on multiple expansion opportunities under one brand, thereby reducing the risks associated with heavy reliance on a single sector.

High Profitability:

Despite some fluctuations in financial metrics since the peak of the pandemic in 2021 and early 2022, Microsoft remains one of the most efficient generators of cash and profits in the market. In the last quarter, the company achieved an impressive 15% year-over-year increase in operating income, resulting in $22.4 billion in profit on $53 billion in sales. This high level of profitability reinforces Microsoft's position as a robust and stable investment option.

As the report is released, investors should focus on these essential growth indicators and look beyond short-term sales volatility to assess Microsoft's long-term potential. The company's diverse business and strong profitability make it an attractive investment opportunity for those seeking stability and growth in their portfolio.

Pricey Stock:

In terms of valuation, Microsoft is considered a pricey stock, with investors having to pay a premium for its valuable assets. Presently, Microsoft stock is valued at over 12 times its annual sales, comparable to the faster-growing Palo Alto Networks. However, in comparison, Apple offers a relatively better bargain with a valuation of 8 times its sales, while Amazon is even cheaper at less than 3 times its sales.

While there is a possibility that Microsoft's valuation may decrease in the coming quarters, particularly if the company reports disappointing sales results in late July or forecasts challenges in the upcoming operational year, the more likely scenario is that the business will continue to gain market share in various significant global tech industries. Additionally, any cyclical downturn in its operating system segment or consumer tech devices division is expected to be short-lived.

Considering Microsoft's bright long-term outlook, industry-leading profit margins, ample cash flow, and rising dividend payments, it emerges as an incredibly attractive stock to consider adding to your portfolio. For tech stock investors who prefer a less risky approach in a fast-moving industry, Microsoft provides an excellent opportunity to gain exposure to major trends while investing in one of the most valuable companies in the world.

Microsoft | Fundamental Analysis | SHORTOn Tuesday, Microsoft announced its intention to acquire video game giant Activision Blizzard in a deal worth $75 billion, or $68.7 billion based on Activision's net cash position. That corresponds to a price of $95 a share, up from Activision's share price of $65 last Friday, but still below Activision's 52-week high of $104.53.

If the deal passes antitrust scrutiny, it could be a clever move. In fact, the deal is reminiscent of Warren Buffett's approach to value investing at his Berkshire Hathaway conglomerate. Given Buffett's close friendship with former Microsoft chairman Bill Gates, it is not surprising that Microsoft is making reasonable acquisitions at reasonable prices during its mature growth phase.

Activision Blizzard has a leading portfolio of video game franchises, including Call of Duty, Candy Crush, Overwatch, and many others. With such a high market capitalization, it is one of the world's largest pure-play video game developers, ranking fifth in total game revenue worldwide.

Recently, however, the company found itself "on the operating table," so to speak. Last summer, California regulators filed a lawsuit against Activision, accusing it of widespread sexual harassment and gender pay inequality. In November, about a fifth of Activision's employees signed a petition urging CEO Bobby Kotick, who has led the company for more than 30 years, to leave. Although the company has taken various steps to correct apparent misconduct, including firing or disciplining more than 80 employees and altering some internal rules, Activision stock has not recovered and is down more than 35 percent from its February 2021 highs.

Although Microsoft is paying a substantial premium to last week's market price, the valuation is about 25 times this year's average earnings estimate of $3.80. If you pay attention to Activision's net cash position, the valuation drops to about 23. That's a pretty reasonable price for Activision's "drama-free," given the strength of its franchises and the way it has traded in the past.

Even if Microsoft gets a reasonable price for a separate Activision, Activision could be even more profitable in Microsoft's hands than as an independent company.

Given the turmoil in Activision's management, The Wall Street Journal reported that Kotick is likely to leave his post after the deal closes. Thus, new leadership and a culture change at Activision itself could help bring key talent and reinvigorate the business after the current employee crisis.

And just as streaming video platforms are spending heavily on their own content, video games, too, are moving to a subscription-based streaming package model. CEO Satya Nadella has doubled down on spending on native content for Microsoft's Game Pass, which Microsoft said in a press release reached more than 25 million subscribers, up from 18 million in early 2021. Activision itself has 400 million monthly active players, so it's reasonable to assume that some of those users will switch to Game Pass, which Microsoft promotes as "Netflix for gaming."

Finally, in an interview with CNBC on Tuesday, Kotick said that as games increasingly move into the metaverse, gaming companies will need technology expertise that Activision may not have, and it will probably be difficult to attract from the big tech companies -- especially given recent employee problems. Therefore, it does make sense to sell the company to a large tech giant with a variety of technology expertise. Microsoft, of course, has such expertise in abundance, thanks to its Azure cloud platform, Xbox gaming platform, and Hololens AR/VR headset.

While the ZeniMax acquisition went off without a hitch, Microsoft may be pushing the limits of its acquisition capabilities with this deal, given Activision's sheer size. At the time of writing, Activision's stock was only trading to the $82 mark, which leaves a lot of room below the $95 acquisition price. This seems to indicate a certain amount of skepticism about completing the deal.

Microsoft has been very good at avoiding antitrust regulators in Washington, who are instead mostly going after other FAANG stocks, particularly those related to social media. However, Microsoft is also not done with two other noteworthy acquisitions in the process in medical AI and advertising technology. Given the speed and size of the new deals, Microsoft could face a lot of resistance to buying Activision.

Nevertheless, if the deal goes through, it's a huge win and terrific use of the enormous $130 billion cash pile on Microsoft's balance sheet. Microsoft is doing great in the cloud computing and enterprise software markets, and that business alone would be enough for management to rest on its laurels. But to see management working hard to grow its consumer-oriented businesses -- search advertising and video games -- is refreshing. First-rate capital allocation and relentless pursuit of growth is another reason Microsoft deserves its high praise.