Micron's Hidden AI Memory Edge: Why the Market's Still Sleeping on This Stock

Even with all the talk about memory being in a down cycle and concerns around DRAM oversupply, I think the market is completely missing the bigger picture with Micron. In my view, the company is shifting in a big way and no one's really pricing that in yet. They're ramping up their high-bandwidth memory (HBM) efforts really fast, keeping inventory in check, holding margins surprisingly well, and going all in on the AI data infrastructure trend. This is not like the old DRAM swings we used to see. What we have now is a structural change where memory growth is tied directly to powering generative AI systems. That makes Micron a key part of the AI supply chain, especially with them now starting to ship HBM4 to their top customers. This latest HBM tech is going to play a big role in next-gen data centers and AI platforms. With demand for more power-efficient AI infrastructure picking up and Micron still trading cheap in my view, I'm rating the stock a Buy.

AI Is Reshaping the Memory Market

In my view, AI is no longer just a buzzword. It is quickly turning into a core part of how most businesses operate. McKinsey recently shared that by March 2025, around 71% of companies were using AI in at least one part of their business. That is a big jump from 55% the year before. As I see it, the rapid pace of AI adoption is now putting major strain on both chip supply and electricity use. This rise in AI use has also pushed demand for data center space much higher. And when there are more data centers, there is obviously a need for more GPUs, servers, and other AI infrastructure.

Now if we focus just on the memory side of things, which is where Micron fits in, AI workloads need a lot of memory bandwidth. That is because AI models have to move large amounts of data between processing cores very quickly. And that creates strong demand for high-bandwidth memory. I believe this is a big opportunity for companies like Micron. South Korean chipmaker SK Hynix forecasts that the market for high-bandwidth memory (HBM) chips, vital for AI, will expand by 30% annually until 2030. Two key drivers are behind this. First, large data centers are being built outside the US in more parts of the world, and that makes server DRAM a must-have, not just a cost item. Second, high-end smartphones with bigger memory needs are also helping keep demand stable even if unit sales have flattened out. The bigger point here is that demand from AI and data centers is now driving more of the growth in memory. That shift is pushing the industry toward higher-margin and more advanced memory products instead of low-end DRAM. If things keep moving in this direction, I expect Micron's focus on high-performance memory will help it break out of the typical boom-and-bust cycle and get priced more like a core tech infrastructure company.

HBM Demand Is Booming and Micron Is Getting Ready

I think it says a lot that both Google and Nvidia have chosen high-bandwidth memory, or HBM, as their go-to solution. Even though it costs around three times more per gigabyte than regular DRAM, these companies are still willing to pay for it. That tells me the performance benefits matter more than the price. Just take Nvidia's new Blackwell chips as an example. Their new racks are expected to need up to 20TB of HBM, which is a huge jump from just 1TB in the previous generation. That kind of increase clearly boosts demand for HBM, and Micron is right in the middle of this shift. They have already started shipping HBM3E and now HBM4, which just launched in June 2025. HBM4 brings more than 20 percent better power efficiency and over 60 percent better performance compared to earlier versions. I think this product could do very well.

What stands out to me is that HBM revenue is already running at over $6 billion a year, growing about 50 percent quarter over quarter. This is happening even before HBM4 starts to make a big impact. Also, all of Micron's HBM3E supply for 2025 has already been sold, and a large chunk of 2026 capacity is also spoken for. I expect that HBM4 will do even better, both in terms of demand and revenue. Now it is worth pointing out that Micron is still behind SK Hynix and Samsung in terms of HBM market share. SK Hynix leads with about 57 percent, Samsung follows with around 27 percent, and Micron is sitting at just 16 percent. But that is what makes Micron's recent progress even more impressive in my opinion. Samsung just lowered its profit outlook for Q2 due to weak AI chip sales. To me, that is a sign that Micron is gaining ground.

Micron's Q3 FY25 results support this. Revenue was up 37 percent YoY to $9.3 billion, and more importantly, it jumped 15.5 percent from the prior quarter. That tells me demand is picking up fast. Nvidia also said its upcoming Rubin chips will come with 12 stacks of HBM. That puts more pressure on suppliers, and Micron seems ready. Earlier this year, Nvidia's CEO Jensen Huang said Samsung had to redesign their HBM to even qualify. I believe Micron took that opportunity and is now much closer to its 20 to 25 percent HBM market share goal.

Margins Are Improving Because of Smarter Product Choices

Micron's margins have moved up over the past year, and I don't think it is just a short-term bounce. Gross margins are now in the mid-30s. That kind of improvement is being driven by a stronger product mix and smart decisions to avoid oversupplying areas with too much price risk. The clear outlier in all of this is HBM, which has been growing quickly and now makes up a larger part of total DRAM shipments.

Micron has also done a better job than most in managing inventory. While some companies are sitting on too much stock, Micron has been steadily cutting its days-of-inventory each quarter and ended well below seasonal levels. Bit shipments stayed in the mid-teens, which tells me they are still supplying what the market needs without going overboard. This kind of tight inventory control, paired with growing HBM content, tells me this is not just another short-term DRAM cycle. Most of Micron's DRAM sales now come from AI and data center customers. That is a big shift. Even if DRAM prices soften overall, I think Micron will still keep strong pricing power in HBM. As long as AI systems keep demanding faster and more efficient memory, HBM should stay valuable and help offset volatility elsewhere.

CapEx Is Up but It's Focused on High-Growth Areas

Some people might be concerned about Micron's big capital spending plans. But I think it is important to see where that money is going. It is not being spread across low-margin products. Most of it is going into high-growth, high-margin areas like HBM. Micron recently raised its capex forecast to $14 billion for FY25. That is about 38 percent of expected revenue, up from 35 percent earlier. I see that as a strong sign of confidence.

And the numbers back that up. Operating cash flow is at multi-year highs, and even with this capex ramp, free cash flow is still positive. That tells me these investments are already paying off. I believe we are watching Micron shift from a company tied to the memory cycle into one that benefits from long-term AI infrastructure growth. Mainstream DRAM supply remains cautious, but AI demand is driving enough growth to more than make up for it. In my view, Micron's returns on invested capital are finally starting to reflect the value of their R&D. They are turning investment into real gains in revenue and margins. On top of that, the balance sheet looks solid. There is no major leverage, and they have pushed out debt payments well into the next decade. Micron looks more and more like a long-term AI memory supplier to me, not just a cyclical DRAM name.

Micron's Valuation Still Doesn't Reflect Its Upside

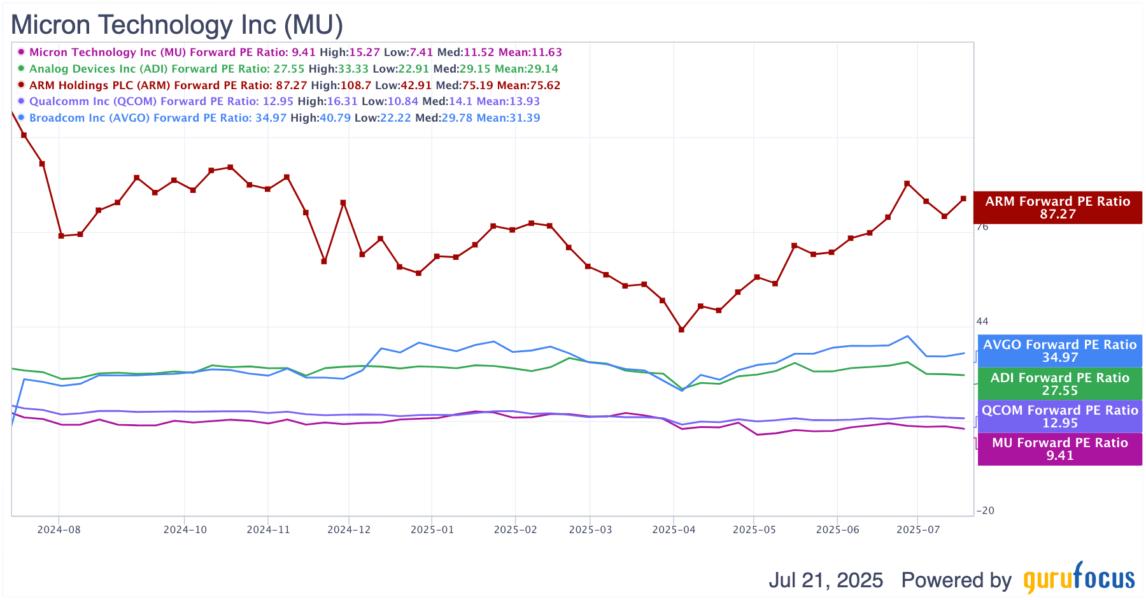

When I look at Micron's valuation right now, I see a big disconnect between its actual earnings potential and how the market is pricing the stock. The forward P/E has compressed to just 9.4x, which feels extremely cheap to meespecially considering that back in January, it was trading closer to 14.5x. That drop tells me the market hasn't fully priced in the company's growth outlook. Even more convincing to me is the PEG ratio. If I use forward earnings along with Wall Street's consensus growth expectations, Micron is trading at around 0.3x to 0.4x PEG. That's a long way from the 1.0x benchmark, which usually signals fair value. To me, that suggests Micron's growth story just isn't being acknowledged by the broader market yet.

To get a better sense of this, I compared Micron to a few peers in the semiconductor space like ADI, ARM, QCOM and AVGO. And what stood out immediately was that these names are all trading at much higher forward P/E multiplessome are even 2 to 3 times higher than Micron. I think this makes Micron look undervalued by comparison.

MU Data by GuruFocus

Consensus estimates are projecting Micron's EPS to grow from about $7.80 in FY25 to around $12 in FY26. That's a more than 50 percent YoY jump. And yet the stock is still priced below a 15x multiple. I take that as a sign that investors still see this as a cyclical high point, rather than the beginning of something more sustainable. But I don't see it that way at all.I believe this kind of earnings growth isn't just part of a temporary cycle. The HBM and high-performance DRAM business that Micron is building is anchored in multi-year supply contracts, and that makes the revenue a lot more predictable. It's not about spot prices going up or downit's about committed volume at fixed prices with top-tier customers. On top of that, the nature of HBM production, which includes complex packaging and advanced interconnects, creates switching costs that competitors can't easily match. That gives Micron a strong moat.

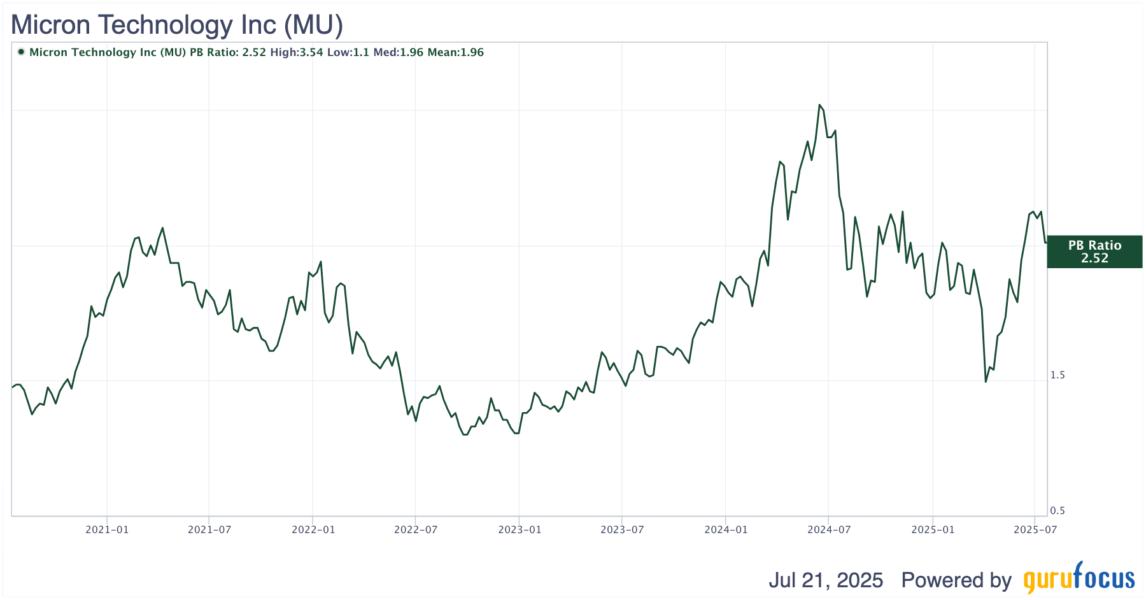

I also think the book value tells a similar story. Right now, Micron trades at around 2.6x its book value. But in past upcycles, it has usually moved closer to 3.2x. If I assume that Micron is on track to deliver sustained upside from here, I think there's still plenty of room for re-rating. In my view, the stock still has upside on both earnings and book value multiples as the business continues to scale into AI-driven demand.

MU Data by GuruFocus

Guru Activity Suggests Underappreciated Upside

Another sign that the market may be underestimating Micron is the level of institutional conviction still backing the stock. PRIMECAP Management (Trades, Portfolio), a long-term growth-focused investor, holds over 37 million sharesrepresenting 3.34 percent of total shares outstanding. While they trimmed their position slightly, they still have nearly 3 percent of their entire portfolio in Micron. Likewise, value-focused names like HOTCHKIS & WILEY and Brandes Investment Partners have continued adding to their positions, signaling confidence in Micron's long-term setup. HOTCHKIS & WILEY, for example, increased their stake by over 1.5 percent this past quarter. HOTCHKIS & WILEY's deep value approach fits right in with Micron's current multiple compression story, while PRIMECAP's growth mindset shows they're banking on earnings climbing steadily over the next few years.

What's especially interesting to me is the massive new buying activity from Lee Ainslie (Trades, Portfolio), who ramped up his fund's position by more than 2400 percent. That's not a minor rebalancing moveit's a sharp statement of conviction. Meanwhile, other well-regarded names like Joel Greenblatt (Trades, Portfolio) also added to their holdings, suggesting that smart money is quietly positioning for future upside. Despite a few reductions (most notably David Tepper (Trades, Portfolio) and Jeremy Grantham (Trades, Portfolio)), the overall trend in guru holdings still leans constructive. This kind of positioning, especially when paired with improving fundamentals and discounted valuation multiples, adds another layer to the argument that Micron is mispriced at current levels.

Conclusion

In summary, Micron's strong positioning in next-gen memory markets, particularly HBM, paired with a clearly mispriced valuation and growing institutional backing, creates an attractive setup for long-term investors. The market continues to price Micron as if its recent growth is cyclical and short-lived, ignoring the structural tailwinds and contractual stickiness behind much of its AI-driven upside. With upside levers ranging from multiple expansion to margin-accretive product mix shifts, I believe Micron offers an excellent risk-reward profile at current levels. I'm staying long and rate the stock a Buy.