Relativity BULLS FOREX 100X 1H AlgorithmHi,

This system is prepared only for leveraged markets and only for Forex.

System parameters:

Timeframe = 1H (1 Hours)

Leverage = 100X

Position Size = %1 (0.01) Each Trade

System features :

- It targets the Risk /Reward Ratio of 1/3 and above. (Risk/Reward Ratio >= 3 )

- If a Take Profit Point has come in a successful trade but the parameter conformity has not deteriorated, system continues the trade.

- In this way, you can catch strong long trends several times a year.

But it is strict as stop-loss and avoids large declines,whipsaws whenever possible.

- The system tries to avoid unnecessary processes as much as possible.

This means less commission and less sideways market.

- Since it takes advantage of the reverse market, it is suitable not only for long and short but only for long position, ie "bulls".

But this neutralizes unnecessary processes.

- Stop-Loss points and Snow-take points are shown in red and green.

-However, if there is a small amount of follow-up available at the computer, it is recommended to put stop-loss only.

Because the system revises both stop-loss and take profit points according to the conditions formed.

Doing this in the right major long trend here allows you to be in trades.

-The system takes into account the risk and only opens transactions where the value corresponding to 100 leverage ratio is greater than the risk.

This provides as much protection from risk as possible.

-Alerts added.

***Since it is located in the most risky market, the forex market, a balanced algorithm has been optimized, considering that it has a very unstable structure similar to dilithrium crystals (same logic as investment bank trader test).

So if this algorithm was a person, it would be an incredibly disciplined but equally skeptical person =)

Also, like other systems, this system also uses ANN (Artificial Neural Networks).

About Backtest :

Since this system uses leveraged market, backtest results are not healthy.

But since it targets the 1/3 Risk Reward Rate (3.00),

we must look Ratio Avg Win/Loss and it must be over 0.5 because :

This ratio means: When we reach 33% of our correct trades in all our trades, we are at breakeven.

This is 100 - 33 = 66

33/66 = 0.5

So whenever this rate is over 0.5, we make a profit.

*** The fact that this ratio must over 0.75 (worst scenario) in terms of securing ourselves because there will be extra comission fees for worst scenario.

Above this ratios ,we can do successful snowball trades.(Because future contracts have loss of maturity and end dates)

And we achieve success cumulatively.

Important Note : This system is prepared only for these parameters.

NOTE :

The system has been prepared as a strategy to present success in a transparent manner.

Please check "Ratio Avg . Win / Avg Loss" rates in backtests.

Important Note 2 -

Although the system revises the stop and take profit points in the required parameters, the most accurate place is when the signal comes.

It should be entered when the signal comes as much as possible and if this did not happen,

trade must be opened in the nearest bars after the signal comes.

Best regards.

EDIT : Comission added. (%0.1)

Algotrading

Relativity BEARS FUTURES 50X 4H AlgorithmHi,

This system is prepared only for leveraged markets and for Futures and CFD markets.

Leveraged processing apply to cryptocurrency contracts that are also subject to.

System parameters:

Timeframe = 4H (4 Hours)

Leverage = 50X

Position Size = %1 (0.01) Each Trade

Market Direction : Short

System features :

- It targets the Risk /Reward Ratio of 1/3 and above. (Risk/Reward Ratio >= 3 )

- If a Take Profit Point has come in a successful trade but the parameter conformity has not deteriorated, system continues the trade.

- In this way, you can catch strong long trends several times a year.

But it is strict as stop-loss and avoids large declines,whipsaws whenever possible.

- The system tries to avoid unnecessary processes as much as possible.

This means less commission and less sideways market.

- Since it takes advantage of the reverse market, it is suitable not only for long and short but only for short position, ie "bears".

But this neutralizes unnecessary processes.

- Stop-Loss points and Snow-take points are shown in red and green.

-However, if there is a small amount of follow-up available at the computer, it is recommended to put stop-loss only.

Because the system revises both stop-loss and take profit points according to the conditions formed.

Doing this in the right major long trend here allows you to be in trades.

-The system takes into account the risk and only opens transactions where the value corresponding to 10 leverage ratio is greater than the risk.

This provides as much protection from risk as possible.

-Alerts added.

About Backtest :

Since this system uses leveraged market, backtest results are not healthy.

But since it targets the 1/3 Risk Reward Rate (3.00),

we must look Ratio Avg Win/Loss and it must be over 0.5 because :

This ratio means: When we reach 33% of our correct trades in all our trades, we are at breakeven.

This is 100 - 33 = 66

33/66 = 0.5 (Ratio Avg. Win / Avg Loss )

So whenever this rate is over 0.5, we make a profit.

*** The fact that this ratio is over 0.70-1.00 in terms of securing ourselves because there is a maturity in the future indicates that we are doing

successful snowball trades.(Because future contracts have loss of maturity and end dates)

And we achieve success cumulatively.

Important Note : This system is prepared only for these parameters.

These parameters are designed for Futures and CFDs.

It doesn't work in spot markets and Forex Markets.

NOTE :

The system has been prepared as a strategy to present success in a transparent manner.

Please check "Ratio Avg . Win / Avg Loss" rates in backtests.(Especially preferred financial instruments what you trade generally)

Important Note 2 -

Although the system revises the stop and take profit points in the required parameters, the most accurate place is when the signal comes.

It should be entered when the signal comes as much as possible and if this did not happen,

trade must be opened in the nearest bars after the signal comes.

If the position is not closed, renew your position in the new month by observing the maturity conditions.

Here you should pay attention to the maturity, the cost of transportation.

Because the more time to maturity, the more advantageous it will be.

Best regards.

Relativity BULLS FUTURES 50X 4H AlgorithmHi,

This system is prepared only for leveraged markets and for Futures and CFD markets.

Leveraged processing apply to cryptocurrency contracts that are also subject to.

System parameters:

Timeframe = 4H (4 Hours)

Leverage = 50X

Position Size = %1 (0.01) Each Trade

System features :

- It targets the Risk /Reward Ratio of 1/3 and above. (Risk/Reward Ratio >= 3 )

- If a Take Profit Point has come in a successful trade but the parameter conformity has not deteriorated, system continues the trade.

- In this way, you can catch strong long trends several times a year.

But it is strict as stop-loss and avoids large declines,whipsaws whenever possible.

- The system tries to avoid unnecessary processes as much as possible.

This means less commission and less sideways market.

- Since it takes advantage of the reverse market, it is suitable not only for long and short but only for long position, ie "bulls".

But this neutralizes unnecessary processes.

- Stop-Loss points and Snow-take points are shown in red and green.

-However, if there is a small amount of follow-up available at the computer, it is recommended to put stop-loss only.

Because the system revises both stop-loss and take profit points according to the conditions formed.

Doing this in the right major long trend here allows you to be in trades.

-The system takes into account the risk and only opens transactions where the value corresponding to 10 leverage ratio is greater than the risk.

This provides as much protection from risk as possible.

-Alerts added.

About Backtest :

Since this system uses leveraged market, backtest results are not healthy.

But since it targets the 1/3 Risk Reward Rate (3.00),

we must look Ratio Avg Win/Loss and it must be over 0.5 because :

This ratio means: When we reach 33% of our correct trades in all our trades, we are at breakeven.

This is 100 - 33 = 66

33/66 = 0.5

So whenever this rate is over 0.5, we make a profit.

*** The fact that this ratio is over 0.70-1.00 in terms of securing ourselves because there is a maturity in the future indicates that we are doing

successful snowball trades.(Because future contracts have loss of maturity and end dates)

And we achieve success cumulatively.

Important Note : This system is prepared only for these parameters.

These parameters are designed for Futures and CFDs.

It doesn't work in spot markets and Forex Markets.

NOTE :

The system has been prepared as a strategy to present success in a transparent manner.

Please check "Ratio Avg . Win / Avg Loss" rates in backtests.

Important Note 2 -

Although the system revises the stop and take profit points in the required parameters, the most accurate place is when the signal comes.

It should be entered when the signal comes as much as possible and if this did not happen,

trade must be opened in the nearest bars after the signal comes.

If the position is not closed, renew your position in the new month by observing the maturity conditions.

Here you should pay attention to the maturity, the cost of transportation.

Because the more time to maturity, the more advantageous it will be.

Best regards.

Relativity BEARS FUTURES 10X 1D AlgorithmHi,

This system is prepared only for leveraged markets and for Futures and CFD markets.

Leveraged processing apply to cryptocurrency contracts that are also subject to.

System parameters:

Timeframe = 1D (1 Day)

Leverage = 10x

Position Size = %1 (0.01) Each Trade

System features :

- It targets the Risk /Reward Ratio of 1/3 and above. (Risk/Reward Ratio >= 3 )

- If a Take Profit Point has come in a successful trade but the parameter conformity has not deteriorated, system continues the trade.

- In this way, you can catch strong long trends several times a year.

But it is strict as stop-loss and avoids large declines,whipsaws whenever possible.

- The system tries to avoid unnecessary processes as much as possible.

This means less commission and less sideways market.

- Since it takes advantage of the reverse market, it is suitable not only for long and short but only for short position, ie "bears".

But this neutralizes unnecessary processes.

- Stop-Loss points and Snow-take points are shown in red and green.

-However, if there is a small amount of follow-up available at the computer, it is recommended to put stop-loss only.

Because the system revises both stop-loss and take profit points according to the conditions formed.

Doing this in the right major long trend here allows you to be in trades.

-The system takes into account the risk and only opens transactions where the value corresponding to 10 leverage ratio is greater than the risk.

This provides as much protection from risk as possible.

-Alerts added.

About Backtest :

Since this system uses leveraged market, backtest results are not healthy.

But since it targets the 1/3 Risk Reward Rate (3.00),

we must look Ratio Avg Win/Loss and it must be over 0.5 because :

This ratio means: When we reach 33% of our correct trades in all our trades, we are at breakeven.

This is 100 - 33 = 66

33/66 = 0.5

So whenever this rate is over 0.5, we make a profit.

*** The fact that this ratio is over 0.70-1.00 in terms of securing ourselves because there is a maturity in the future indicates that we are doing

successful snowball trades.(Because future contracts have loss of maturity and end dates)

And we achieve success cumulatively.

Important Note : This system is prepared only for these parameters.

These parameters are designed for Futures and CFDs.

It doesn't work in spot markets and Forex Markets.

NOTE :

The system has been prepared as a strategy to present success in a transparent manner.

Please check "Ratio Avg . Win / Loss" rates in backtests.

Important Note 2 -

Although the system revises the stop and take profit points in the required parameters, the most accurate place is when the signal comes.

It should be entered when the signal comes as much as possible and if this did not happen,

trade must be opened in the nearest bars after the signal comes.

Here you should pay attention to the maturity, the cost of transportation.

Because the more time to maturity, the more advantageous it will be.

Best regards.

Relativity BULLS FUTURES 10X 1D AlgorithmHi,

This system is prepared only for leveraged markets and for Futures and CFD markets.

Leveraged processing apply to cryptocurrency contracts that are also subject to.

System parameters:

Timeframe = 1D (1 Day)

Leverage = 10x

Position Size = %1 (0.01) Each Trade

System features :

- It targets the Risk /Reward Ratio of 1/3 and above. (Risk/Reward Ratio >= 3 )

- If a Take Profit Point has come in a successful trade but the parameter conformity has not deteriorated, system continues the trade.

- In this way, you can catch strong long trends several times a year.

But it is strict as stop-loss and avoids large declines,whipsaws whenever possible.

- The system tries to avoid unnecessary processes as much as possible.

This means less commission and less sideways market.

- Since it takes advantage of the reverse market, it is suitable not only for long and short but only for long position, ie "bulls".

But this neutralizes unnecessary processes. (Short market direction, the system for bears will be published separately.)

- Stop-Loss points and Snow-take points are shown in red and green.

-However, if there is a small amount of follow-up available at the computer, it is recommended to put stop-loss only.

Because the system revises both stop-loss and take profit points according to the conditions formed.

Doing this in the right major long trend here allows you to be in trades.

-The system takes into account the risk and only opens transactions where the value corresponding to 10 leverage ratios is greater than the risk.

This provides as much protection from risk as possible.

-Alerts added.

About Backtest :

Since this system uses leveraged market, backtest results are not healthy.

But since it targets the 1/3 Risk Reward Rate (3.00),

we must look Ratio Avg Win/Loss and it must be over 0.5 because :

This ratio means: When we reach 33% of our correct trades in all our trades, we are at breakeven.

This is 100 - 33 = 66

33/66 = 0.5

So whenever this rate is over 0.5, we make a profit.

*** The fact that this ratio is over 0.70-1.00 in terms of securing ourselves because there is a maturity in the future indicates that we are doing

successful snowball trades.(Because future contracts have loss of maturity and end dates)

And we achieve success cumulatively.

Important Note : This system is prepared only for these parameters.

These parameters are designed for Futures and CFDs.

It doesn't work in spot markets.

NOTE :

The system has been prepared as a strategy to present success in a transparent manner.

Please check "Ratio Avg. Win / Loss" rates in backtests.

Important Note 2 -

Although the system revises the stop and take profit points in the required parameters, the most accurate place is when the signal comes.

It should be entered when the signal comes as much as possible and if this did not happen,

trade must be opened in the nearest bars after the signal comes.

Best regards.

BTC and ETH Long strategy - version 1I will start with a small introduction about myself. I'm now trading cryto currencies manually for almost 2 years. I decided to start after watching a documentary on the TV showing people who made big money during the Bitcoin pump which happened at the end of 2017.

The next day, I asked myself "Why should I not give it a try and learn how to trade".

This was in February 2018 and the price of Bitcoin was around 11500USD.

I didn't know how to trade. In fact, I didn't know the trading industry at all.

So, my first step into trading was to open an account with a broken. Then I directly bought 200$ worst of BTC . At that time, I saw the graph and thought "This can only go back in the upward direction!" :)

I didn't know anything about Stop loss, Take profit and Risk management.

Today, almost 2 years after, I think that I know how to trade and can also confirm that I still hold this bag of 200$ of bitcoin from 2018 :)

I did spend the 2 last years to learn technical analysis , risk management and leverage trading.

Today (14/05/2020), I know what I'm doing and I'm happy to see that the 2 last years have been positive in terms of gains. Of course, I did not make crazy money with my saving but at least I made more than if I would have kept it in my bank account.

Even if I like trading, I have a full time job which requires my full energy and lots of focus, so, the biggest problem I had is that I didn't have enough time to look at the charts.

Also, I realized that sometimes, neither technical analysis , nor fundamentals worked with crypto currency (at least for short time trading). So, as I have a developer background I decided to try to have a look at algo trading.

The goal for me was neither to make complex algos nor to beat the market but just to automate my trading with simple bot catching the big waves.

I then started to take a look at TV pine script and played with it.

I did my first LONG script in February 2020 to Long the BTC Market. It has some limitations but works well enough for me for the time being. Even if the real trades will bring me half of what the back testing shows, this will still be a lot more than what I was used to win during the last 2 years with my manual trading.

So, here we are! Below you will find some details about my first LONG script. I'm happy to share it with you.

Feel free to play with it, give your comments and bring improvements to it.

But please note that it only works fine with the candle size and crypto pair that I have mentioned below. If you use other settings this algo might loose money!

- Crypto pairs : XBTUSD and ETHXBT

- Candle size: 2 Hours

- Indicator used: Volatility , MACD (12, 26, 7), SMA (100), SMA (200), EMA (20)

- Default StopLoss: -1.5%

- Entry in position if: Volatility < 2%

AND MACD moving up

AND AME (20) moving up

AND SMA (100) moving up

AND SMA (200) moving up

AND EMA (20) > SAM (100)

AND SMA (100) > SMA (200)

- Exit the postion if: Stoploss is reached

OR EMA (20) crossUnder SMA (100)

Here is a summary of the results for this script:

XBTUSD : 01/01/2019 --> 14/05/2020 = +107%

ETHXBT : 01/01/2019 --> 14/05/2020 = +39%

ETHUSD : 01/01/2019 --> 14/05/2020 = +112%

It is far away from being perfect. There are still plenty of things which can be done to improve it but I just wanted to share it :) .

Enjoy playing with it....

Strategy BTBTBTBT — strategy for only long positional trading of top cryptocurrencies. BTCUSD and ETHUSD are best suited for this strategy.

The main idea of the strategy is to buy cryptocurrency with a leverage of up to 1: 3 when the market is growing, and get rid of cryptocurrency when the market is not growing or falling.

The strategy is working on a daily timeframe .

To determine the trend, the strategy uses a combination of indicators MA25 and MA99.

To determine overbought (pump) and oversold (dump), the strategy uses the oscillator "SPPO".

The strategy has three trading conditions:

1) SPPO SPPOoverBought - "pump" market. Close all long positions or leave a position with a micro-leverage of 1: 0.1 for a period of 28 days.

3) Closing> MA25 > MA99 - uptrend in the market. We open the "long" position with a leverage of 1: 3.

If market conditions do not meet the above criteria, then the strategy does not have open positions.

Input parameters

Recommended timeframe D1.

FastLength - period for fast MA. Default = 25.

SlowLength - period of slow MA. Default = 99.

SPPOoverSold - trigger for determining the dump in the market. Default = -30.

SPPOoverBought - trigger to determine the pump in the market. Default = 35.

SPPOmaxForLong - the maximum value of SPPO for opening a long position. Default = 10.

LeverageLong - leverage when entering the market with a "long" signal. Default = 3.

LeveragePamp - the amount of leverage when entering the market with a "pump" signal. Default = 0.1.

LeverageDamp - the amount of leverage when entering the market with a "dump" signal. Default = 1.

Log equity chart - If true, use a logarithmic scale for a graph of equity. Default = false.

Gap Trading Strategy: CME BitcoinI created a strategy which finds gaps on CME Futures market for Bitcoin, BTC1! and opens a long or short position on the crypto exchange depending on what kind of gap was found (up or down) on CME.

Up gap: today open price > previous day high price

Down gap: today open price < previous day low price

Two lines below the main chart show when gaps appear. The green line represents the size of up gaps, when it crosses zero it gives a long signal. The red line - represents the size of down gaps, when it crosses zero - short signal.

Instead of having to look between multiple charts, this simply overlays the past weeks open and close should a gap appear.

Usage:

Strategy flips long / short depending of indicator signals. It could cut the position by stop loss or take profit.

Features:

ability to set stop loss and take profit in %

ability to set delta for gaps (if you want to filter small ones)

ability to choose strategy type. Standart: Long Up/Short Down || Inverse: Short Up/Long Down.

Backtesting:

Backtested on BTCPERP ( FTX ) and XBTUSD (Bitmex).

It shows a low drawdown, a small number of trades and 50% of profit for the 2020.

For example, I set high delta for down gaps to filter small ones

Strategy doesn't repaint.

TS - Trading Algorithm Strategy - Crypto, Forex & StocksWhat does the TS - Algorithm do?

-- Plots trend following, high probability signals.

-- These signals do not repaint and can be used confidently to enter or exit a trade.

What markets can this indicator be used on?

-- Forex

-- Stocks

-- Commodities

-- Cryptocurrencies

What time-frames can this indicator be used on?

-- This indicator can be used on 1m, 3m , 5m, 10m, 15m, 30m, 1hr, 2hr, 3hr, 4hr, 6hr, 8hr, 12hr, Daily, Weekly, Bi-Weekly and Monthly time-frames.

-- This is a trend following algorithm, so low as there is good volume , volatility and price history of an asset, the model can perform.

Does this indicator repaint?

-- No

Premium Tradespot Script - Trial access and Information

-- Trial access offered

-- PM me directly to request trial access to the scripts or for more information.

TS - Long Term Trading Algorithm - StrategyStrategy to the bespoke TS - Trading Algorithm. Highly profitable cryptocurrency trading model.

This script is long only profitable strategy- there is a script coming in the next few days for shorter timeframe long & short trading.

- Backtesting is from 2017.

- 0.05% commission

- 100% capital allocation per trade.

Access to both the backtesting strategy & indicator is paid - PM me for details.

Intraday Trend Following Algorithm [Bitduke]Description :

Trend following strategy that constantly adjusts to volatility and avoids of most whipsaws; rapidly moves up or down according to a quickly changing market. Great strategy for high volatile markets, like crypto market.

Based on a couple of special moving averages with integrated smoother which helps to avoid whipsaws.

Backtesting

Backtested on BTCPERP ( FTX ). It shows much better results on 4h timeframe (more than 222% YTD) and relatively low drawdown which allows you to use up to x3 leverage without a fear of huge losses. I.e if we have 5% drawdown for this strategy and using x3 leverage then to be prepared to 15% drawdown maximum in this case.

Initial Capital: $1000

Capital per trade: $1000

Including fee: 0.075% (buy + sell) side, type "taker"

When we get a signal (green/red column on chart) algo opens a trade by the next candle open price.

Others:

Risk management: Stop loss/Take profit in %

Strategy doesn't repaint .

----------

To access: sign up on FTX using ref link from my signature.

Squeeze Momentum Strategy SL TP v2Improved version of my Squeeze Momentum Strategy.

Changes:

Possible to change source: ohlc4, hl2, hlc3, close

Enter your stop loss and take profit in %, NOT ticks

Working and robust even without take profit / stop loss

Yearly drawdown lower than 20%

Backtesting

Backtested on BTCPERP (FTX). It shows much better results on 1h timeframe (about 200% yearly, 55% in 2020) and relatively low drawdown to date.

Initial Capital: $1000

Capital per trade: $1000

Including fee: 0.075% (buy + sell) side, type "taker"

Strategy doesn't repaint.

Shortly about Squeeze Momentum Indicator:

This is a derivative of John Carter's "TTM Squeeze" volatility indicator, as discussed in his book "Mastering the Trade" (chapter 11).

----------

To access : sign up on FTX using ref link from my signature.

Swing Algo V1.1Here I present an upgrade to 'Swing Algo V1'. For differences to V1, see below.

This indicator can be used for e.g. swing algorithmic trading. It will give Buy/Long and Sell/Short signals on the chart. This algorithm uses a combination of several (custom) functions and rules to find good entry points for trend trading. After many iterations and tests I came up with this particular setup, which is highly optimized for the $ETH/$USD trading pair on the daily (D) timeframe. It is however possible to change algorithmic parameters within the indicator settings to tune this swing algorithm for other assets and timeframes. You don't need any programming skills or similar abilities to navigate this indicator.

Also you can choose the backtest time interval to test the perfomance of this algorithm for different time windows and different trading pairs. Here various backtesting parameters (e.g. trading fees) can be customized. Additionally to the TradingView Strategy Tester you can also plot your equity directly on the chart to get a sense for the performance. For this you can also scale the equity graph to e.g. match the starting point of your equity with some price point on the chart to get a direct comparison to 'Buy & Hold' strategies over time.

Note: In general it seems that cryptocurrencies are rather swing-algorithm-friendly, while I cannot recommend trading classical assets like stock or indices (e.g. S&P 500) with this indicator (although you can of course try to find good setups).

This indicator (and all other content I provide) is no financial advice. If you use this indicator you agree to my Terms and Conditions which can be found on my Twitter profile linked on my TradingView profile or in my signature.

Differences to Swing Algo V1:

- Changed the oscillator part of the algorithm with a better suited one (at least) for the ETH/USD trading pair.

- Improved net profits by roughly 20% in comparison to V1 for ETH/USD on daily timeframe

- Reduced Max. Drawdown by roughly 1/4 in comparison to V1 for ETH/USD on daily timeframe

- However for other assets and timeframes V1 might perform better than V1.1. I leave you with both options to play so that you can find the best solution for a given trading pair.

For access please contact me via DM on TradingView or on Twitter (linked on my TradingView profile and my signature). People who purchased access to any 'Swing Algo 1.x' get access to all other 'Swing Algo V1.x' indicators automatically ('Swing Algo V1' counts as 'Swing Algo V1.0').

hamster-bot HiDeep strategy// DESCRIPTION OF STRATEGY

HiDeep Strategy

Author foresterufa

This is a counter-trending strategy that is gradually gaining a position against the trend at the best price.

A prerequisite for completing a position is the price exit from the internal channel on the chart and the appearance of the HiDeep indicator.

The condition for closing the position is touching the opposite side of the internal channel.

A condition for facilitating closure along the middle line of the channel, with high price volatility , is that the price touches the border of the external channel.

Input signals are generated by HiDeep indicators. Closing a position by moving averages.

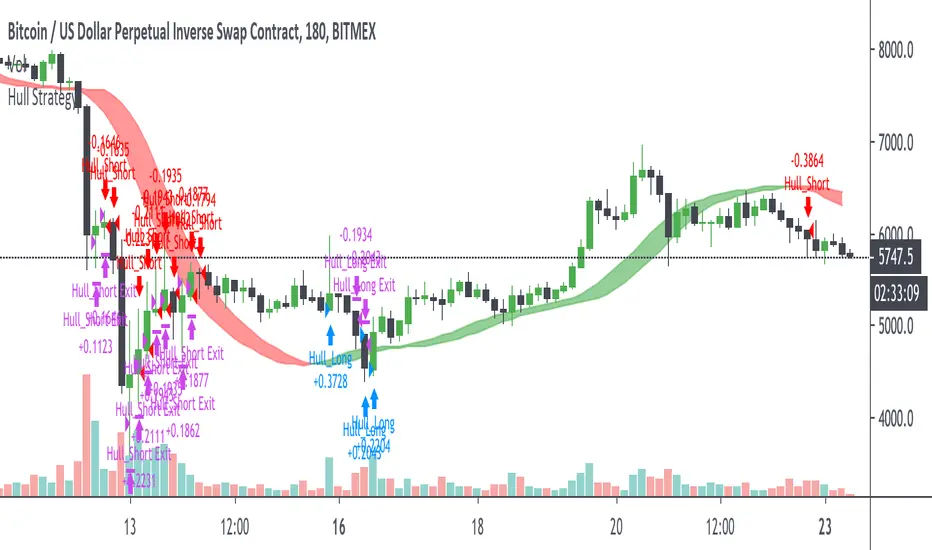

Hull Strategy [Bitduke]Description

The Hull Moving Average (HMA) was developed by Alan Hull for the purpose of reducing lag, increasing responsiveness while at the same time eliminating noise. Its calculation is elaborate and makes use of the Weighted Moving Average (WMA).

It uses two lagged hull moving averages at the intersection of which a change in trend is determined.

Risk Management

Risk is managed by limiting the loss per trade (in%) using stop loss variable.

Improvements

Can be improved by experiments with stop loss and take profit.

Backtesting

Bitmex XBTUSD

Timeframe 3H

Stop 2%, take profit : n/a

193.5% profit

22.42% drawdown

FTX BTC-PERP

Timeframe 3H

Stop 2%, take profit : n/a

187.5% profit

14.79% (!) drawdown

FTX SHIT-PERP

Timeframe 3H

Stop 2%, take profit : n/a

112.5% profit

13.79% (!) drawdown

Reticulata Enhanced - StrategyThis script is the backtesting for Reticulata Enhanced.

Building on our core script - Reticulata, the enhanced version features several requested extras to give you more flexibility with your trading style.

What is Reticulata Enhanced?

The Reticulata core leverages a blend of MA/RSI strategies mixed with the Bull Bear Bots optimised logic for risk management. This enhanced version takes it a step further with additional risk management features:

Trailing Stop

Fixed Stop

Fixed Stop, but move at TP

Trend confirmation

Usage

Using the indicator is as simple as:

1. Select the strategy, or combination of strategies you want to use

2. If desired, select one or more of the available trend filters

3. Adjust your stop options

4. Review backtest results

Markets

Like the core, the enhanced algo also supports a range of markets and timeframes, including the majors (EURUSD, etc...) in Forex and a variety of Cryptocurrencies including Bitcoin (BTC/XBT etc...).

All of our scripts are designed for manual traders but are ready to use with automated trading bots.

Swing Algo V1This indicator can be used for e.g. swing algorithmic trading. It will give Buy/Long and Sell/Short signals on the chart. This algorithm uses a combination of several (custom) functions and rules to find good entry points for trend trading. After many iterations and tests I came up with this particular setup, which is highly optimized for the $ETH/$USD trading pair on the daily (D) timeframe. It is however possible to change algorithmic parameters within the indicator settings to tune this swing algorithm for other assets and timeframes. You don't need any programming skills or similar abilities to navigate this indicator.

Also you can choose the backtest time interval to test the perfomance of this algorithm for different time windows and different trading pairs. Here various backtesting parameters (e.g. trading fees) can be customized. Additionally to the TradingView Strategy Tester you can also plot your equity directly on the chart to get a sense for the performance. For this you can also scale the equity graph to e.g. match the starting point of your equity with some price point on the chart to get a direct comparison to 'Buy & Hold' strategies over time.

Note: In general it seems that cryptocurrencies are rather swing-algorithm-friendly, while I cannot recommend trading classical assets like stock or indices (e.g. S&P 500) with this indicator (although you can of course try to find good setups).

This indicator (and all other content I provide) is no financial advice. If you use this indicator you agree to my Terms and Conditions which can be found on my twitter profile linked in my signature.

hamster-bot REP strategyThe strategy basically contains RSI + EMA + Parabolic = REP.

Entry: RSI

Trend Filter: EMA

Exit: Trailing Stop Parabolic

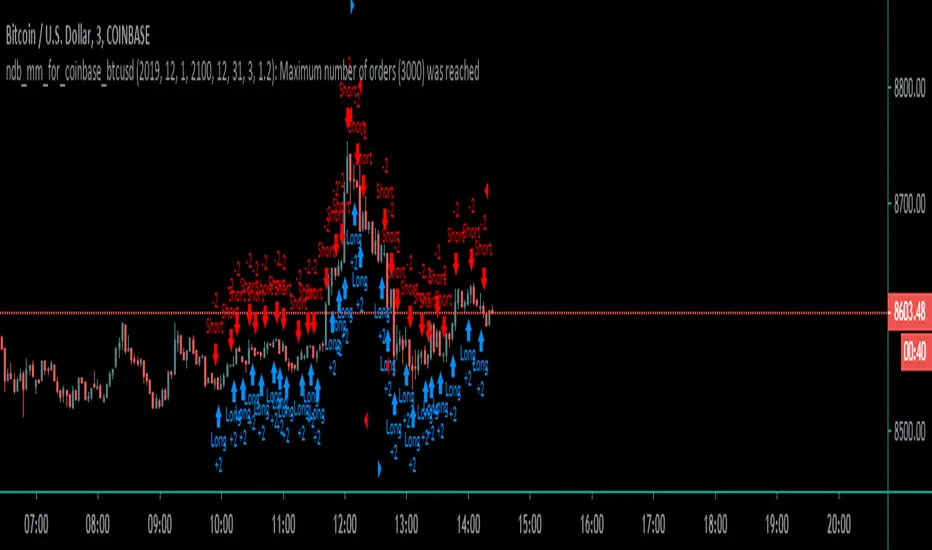

Coinbase_3-MIN_HFT-StrategyThis conceptual strategy trades against the short-term trend. The first position can be either long or short.

In the short-term, prices fluctuate up and down on wide spread exchanges.

And if the price moves to one side, the price tends to return to its original position momentarily.

This strategy set stop order. Stop price is calculated with upper and lower shadows.

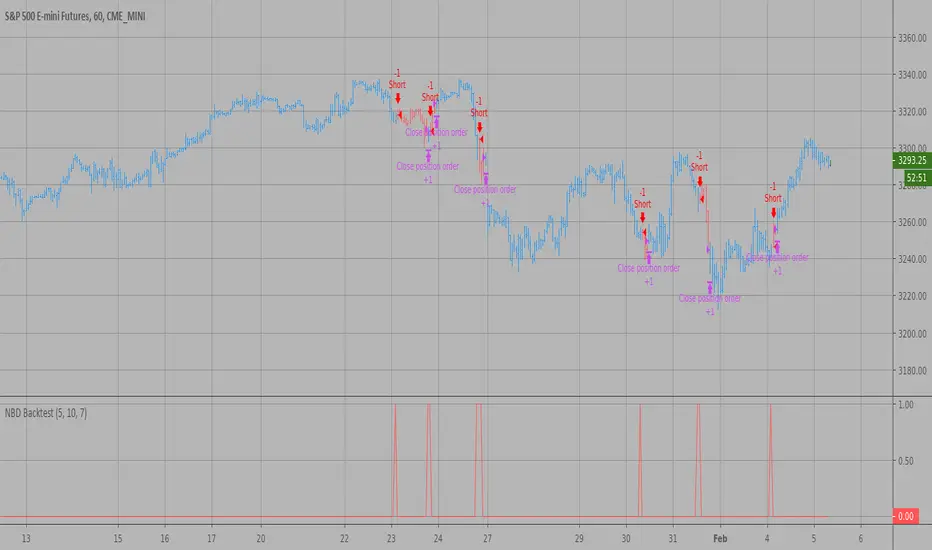

Combo Backtest 123 Reversal & CMOaDisparity Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related CMOaDisparity Index article is copyrighted material from Stocks & Commodities Dec 2009

My strategy modification.

WARNING:

- For purpose educate only

- This script to change bars colors.

hamster-bot CCI_PSARTrending strategy using indicators:

Commodity Channel Index (CCI) www.tradingview.com(CCI)

Parabolic SAR (SAR) www.tradingview.com(SAR)

The trend is determined by PSAR indicator on the higher timeframe.

Signals of buy/sell by CCI indicator

N Bars Down Backtest Evaluates for n number of consecutive lower closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

N Bars Up Backtest Evaluates for n number of consecutive higher closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.