Structure Break ModelMAIN FEATURES

Supported Assets & Timeframe

This indicator is specifically designed and calibrated for 30 USDT trading pairs on the H4 timeframe, all of which have been actively traded for over 1,000 days, including:

BTCUSDT, ETHUSDT, XRPUSDT, BNBUSDT, SOLUSDT, TRXUSDT, DOGEUSDT, ADAUSDT, XLMUSDT, BCHUSDT,

ZECUSDT, LINKUSDT, HBARUSDT, UNIUSDT, LTCUSDT, AVAXUSDT, SHIBUSDT, DOTUSDT, AAVEUSDT, NEARUSDT,

ETCUSDT, ICPUSDT, FILUSDT, APTUSDT, ENSUSDT, ATOMUSDT, VETUSDT, QNTUSDT, CRVUSDT, INJUSDT

Using the script on other pairs or timeframes will trigger an automatic warning to prevent incorrect usage.

1. Structural Weakening Model (Core Logic)

At the heart of the system lies the Structural Weakening Model (SWM) — a multi-layered market-structure engine that identifies momentum exhaustion and confirms genuine reversals using pivot-based swing architecture.

Pivot Structure Mapping

The indicator continuously analyzes Pivot Highs and Pivot Lows (length = 5) to establish clean, stable swing structure.

Weakening Pattern Detection

The model evaluates directional fatigue by detecting pivot sequences:

2–6 Higher Lows → Weakening buyers → Potential SELL setup

2–6 Lower Highs → Weakening sellers → Potential BUY setup

This mechanism identifies “compression zones” where market pressure fades before a structural shift.

Breakout Confirmation Layer

A signal is only triggered when price breaks the final structural anchor of the pivot chain.

This ensures:

Optional Trend Filter (MA Alignment)

Users may select EMA, SMA, WMA, HMA and more.

Price above MA → BUY-only mode

Price below MA → SELL-only mode

This keeps signals aligned with broader market flow.

Visual Example – SELL Signal (TP Hit)

2. Signal Conditions (How the System Works)

SELL Setups

Triggered when:

Price forms 2–6 higher lows, signaling weakening buyers

Price breaks below the structural pivot anchor

(Optional) Price is below the MA filter

BUY Setups

Triggered when:

Price forms 2–6 lower highs, signaling weakening sellers

Price breaks above the structural pivot anchor

(Optional) Price is above the MA filter

Visual Example – SELL Signal (SL Hit)

3. Automatic Capital Management

The script integrates full risk-management utilities:

Starting capital (default 10,000 USDT)

Risk % per trade

Leverage (x10 → x100)

Automatic position sizing

Margin requirements

Real-time TP/SL calculations

This turns the indicator into not just a signal tool, but a complete trading assistant.

4. Flexible Stop-Loss System

Users may choose:

Swing-based SL (nearest structural pivot)

Fixed SL %

Custom TP based on R:R (1:1.5 → 1:5)

Default R:R = 1:2

SL/TP levels update instantly whenever settings change.

Input Settings Menu

5. Visual Interface

The chart displays:

Entry, TP, SL (extended 20 candles)

BUY/SELL labels

Real-time TP/SL hit status

Full info panel:

Latest signal

Entry price

TP/SL

Leverage

Risk %

Required margin

Win/loss & R statistics

Days on chart: The total number of trading days calculated from your chart’s visible data

All signals follow the exact same logic in historical and real-time charts.

Zero repainting.

6. Internal Backtest Engine (Not Official TradingView Backtesting)

The script includes an internal backtest calculator that evaluates:

SL methods

TP R:R settings

Signal quality

Aggregate R performance

⚠ This is an internal calculation tool, not the official TradingView Strategy Tester.

Its purpose is to help users understand how different settings behave when applied to past data.

7. 1-Day Free Trial

Users may message the author on TradingView to request:

1-day trial access

Ability to test signals in real-time

Compare different SL/RR settings

Verify that the indicator does not repaint

Inspect how the engine behaves on the supported 30-coin dataset

This allows users to evaluate the tool transparently before subscribing.

8. Market Coverage & Deep Backtest Basis This indicator is calibrated on the 30 largest USDT pairs, providing a deep historical dataset with stable liquidity and clearer structural swings. The long backtest range and high signal density help reduce noise and ensure more consistent behavior across different market conditions.

⚠ Disclaimer

This indicator is a quantitative analysis tool created for educational purposes only.

All “optimal settings” are derived from historical market behavior and do not guarantee future performance.

Market conditions change, and every trader must apply independent risk management.

Trading involves risk.

Use responsibly.

Bitcoin (Cryptocurrency)

Bitcoin Multibook v1.0 [Apollo Algo]Bitcoin Multibook v1.0 by Apollo Algo is an advanced market depth and order flow visualization tool that brings professional-grade multi-exchange order book analysis to TradingView. Inspired by Bookmap's multibook functionality and built upon LucF's original single "Tape" indicator concept, this tool aggregates real-time trading data from multiple Bitcoin exchanges into a unified tape display.

Credits & Attribution

This indicator is an evolution of the original "Tape" indicator created by LucF (TradingView: @LucF). The multibook enhancement and Bitcoin-specific optimizations were developed by Apollo Algo to provide traders with institutional-grade market microstructure visibility across major Bitcoin trading venues.

Purpose & Philosophy

Bitcoin leads the entire cryptocurrency market. By monitoring order flow across the primary Bitcoin exchanges simultaneously, traders gain crucial insights into:

Cross-exchange arbitrage opportunities

Institutional order flow patterns

Market maker positioning

True market sentiment beyond single-exchange data

Key Features

📊 Multi-Exchange Data Aggregation

Real-time tape from 3 major exchanges:

Binance (BTCUSDT)

Coinbase (BTCUSD)

Kraken (BTCUSD)

Customizable source inputs for any trading pair

Synchronized price and volume tracking

Exchange name identification in tape display

📈 Advanced Tape Display

Dynamic tape visualization with configurable line quantity (0-50 lines)

Directional flow indicators (+/- symbols for price changes)

Exchange identification for each trade

Volume precision control (0-16 decimal places)

Flexible positioning (9 screen positions available)

Real-time only operation for accurate order flow

🎯 Volume Delta Analysis

Real-time cumulative volume delta calculation

Divergence detection (price vs. volume direction)

Colored visual feedback for market sentiment

Total session delta displayed in footer

Cross-exchange delta aggregation

🚨 Smart Alert System

Marker 1: Volume Delta Bumps (⬆⬇)

Triggers on consecutive volume delta increases

Identifies momentum acceleration points

Filters out divergent movements

Marker 2: Volume Delta Thresholds (⇑⇓)

Fires when delta exceeds user-defined thresholds

Catches significant order imbalances

Excludes divergence conditions

Marker 3: Large Volume Detection (⤊⤋)

Highlights unusually large individual trades

Spots potential institutional activity

Direction-specific triggers

Configure Data Sources

Adjust exchange pairs if needed (e.g., for altcoin analysis)

Leave blank to disable specific exchanges

Use format: EXCHANGE:SYMBOL

Customize Display

Set tape line quantity based on screen size

Position the table for optimal visibility

Choose color scheme (text or background)

Adjust text size for readability

Configure Alerts

Enable desired markers (1, 2, or 3)

Set volume thresholds appropriate for your timeframe

Choose direction (Longs, Shorts, or Both)

Create TradingView alerts on marker signals

Trading Applications

Scalping (1-5 min)

Monitor tape speed for momentum shifts

Watch for cross-exchange divergences

Track large volume clusters

Use Marker 1 for quick momentum trades

Day Trading (5-60 min)

Identify accumulation/distribution phases

Spot institutional positioning

Confirm breakout validity with volume delta

Use Marker 2 for significant imbalances

Swing Trading (1H+)

Analyze volume delta trends

Detect smart money rotation

Time entries with order flow confirmation

Use Marker 3 for institutional footprints

Advanced Techniques

Cross-Exchange Arbitrage Detection

When price disparities appear between exchanges:

Immediate Opportunity: Price differences > 0.1%

Bot Activity: Rapid convergence patterns

Liquidity Vacuum: One exchange leading others

Divergence Trading Strategies

Volume delta diverging from price direction:

Absorption: Strong hands entering (price down, delta up)

Distribution: Smart money exiting (price up, delta down)

Reversal Setup: Sustained divergence over multiple bars

Institutional Footprint Recognition

Large volume characteristics:

Simultaneous Spikes: Same timestamp across exchanges

TWAP Patterns: Consistent volume over time

Iceberg Orders: Repeated same-size trades

Pine Script v6 Enhancements

Type Safety Improvements

Strict boolean type handling

Explicit type declarations

Enhanced error checking

Performance Optimizations

Improved request.security() function

Better memory management with arrays

Optimized table rendering

Modern Syntax Updates

indicator() instead of study()

Namespaced math functions (math.round())

Typed input functions (input.int(), input.float())

Performance Considerations

System Requirements

Real-time Data: Essential for tape operation

Multiple Security Calls: May impact performance

Array Operations: Memory intensive with high line counts

Table Rendering: CPU usage increases with tape size

Optimization Tips

Reduce tape lines for better performance

Increase volume filter to reduce noise

Disable unused markers

Use text-only coloring for faster rendering

Moon Boys LineWe have the 44 and 125 day moving averages. When they cross, the trend is bullish or bearish.

V-CORE Engine Free v1V-CORE Engine Free v1 — Public Release

This is a simplified trend-state visualiser from the V-CORE suite, designed for clean directional bias on crypto markets using 1H+ timeframes.

The engine runs fixed, non-editable internal logic with multi-stage trend confirmation.

No optimisation, no signals, no settings — just locked-in regime detection for educational and research use.

This free edition is a lightweight derivative of our internal V-CORE Engine architecture.

It includes only the essential background-state display while keeping all proprietary components sealed.

For additional V-CORE tools, future releases, or extended versions, please visit our TradingView profile.

MACD Forecast Colorful [DiFlip]MACD Forecast Colorful

The Future of Predictive MACD — is one of the most advanced and customizable MACD indicators ever published on TradingView. Built on the classic MACD foundation, this upgraded version integrates statistical forecasting through linear regression to anticipate future movements — not just react to the past.

With a total of 22 fully configurable long and short entry conditions, visual enhancements, and full automation support, this indicator is designed for serious traders seeking an analytical edge.

⯁ Real-Time MACD Forecasting

For the first time, a public MACD script combines the classic structure of MACD with predictive analytics powered by linear regression. Instead of simply responding to current values, this tool projects the MACD line, signal line, and histogram n bars into the future, allowing you to trade with foresight rather than hindsight.

⯁ Fully Customizable

This indicator is built for flexibility. It includes 22 entry conditions, all of which are fully configurable. Each condition can be turned on/off, chained using AND/OR logic, and adapted to your trading model.

Whether you're building a rules-based quant system, automating alerts, or refining discretionary signals, MACD Forecast Colorful gives you full control over how signals are generated, displayed, and triggered.

⯁ With MACD Forecast Colorful, you can:

• Detect MACD crossovers before they happen.

• Anticipate trend reversals with greater precision.

• React earlier than traditional indicators.

• Gain a powerful edge in both discretionary and automated strategies.

• This isn’t just smarter MACD — it’s predictive momentum intelligence.

⯁ Scientifically Powered by Linear Regression

MACD Forecast Colorful is the first public MACD indicator to apply least-squares predictive modeling to MACD behavior — effectively introducing machine learning logic into a time-tested tool.

It uses statistical regression to analyze historical behavior of the MACD and project future trajectories. The result is a forward-shifted MACD forecast that can detect upcoming crossovers and divergences before they appear on the chart.

⯁ Linear Regression: Technical Foundation

Linear regression is a statistical method that models the relationship between a dependent variable (y) and one or more independent variables (x). The basic formula for simple linear regression is:

y = β₀ + β₁x + ε

Where:

y = predicted variable (e.g., future MACD value)

x = independent variable (e.g., bar index)

β₀ = intercept

β₁ = slope

ε = random error (residual)

The regression model calculates β₀ and β₁ using the least squares method, minimizing the sum of squared prediction errors to produce the best-fit line through historical values. This line is then extended forward, generating a forecast based on recent price momentum.

⯁ Least Squares Estimation

The regression coefficients are computed with the following formulas:

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

Σ denotes summation; x̄ and ȳ are the means of x and y; and i ranges from 1 to n (number of observations). These equations produce the best linear unbiased estimator under the Gauss–Markov assumptions — constant variance (homoscedasticity) and a linear relationship between variables.

⯁ Regression in Machine Learning

Linear regression is a foundational model in supervised learning. Its ability to provide precise, explainable, and fast forecasts makes it critical in AI systems and quantitative analysis.

Applying linear regression to MACD forecasting is the equivalent of injecting artificial intelligence into one of the most widely used momentum tools in trading.

⯁ Visual Interpretation

Picture the MACD values over time like this:

Time →

MACD →

A regression line is fitted to recent MACD values, then projected forward n periods. The result is a predictive trajectory that can cross over the real MACD or signal line — offering an early-warning system for trend shifts and momentum changes.

The indicator plots both current MACD and forecasted MACD, allowing you to visually compare short-term future behavior against historical movement.

⯁ Scientific Concepts Used

Linear Regression: models the relationship between variables using a straight line.

Least Squares Method: minimizes squared prediction errors for best-fit.

Time-Series Forecasting: projects future data based on past patterns.

Supervised Learning: predictive modeling using labeled inputs.

Statistical Smoothing: filters noise to highlight trends.

⯁ Why This Indicator Is Revolutionary

First open-source MACD with real-time predictive modeling.

Scientifically grounded with linear regression logic.

Automatable through TradingView alerts and bots.

Smart signal generation using forecasted crossovers.

Highly customizable with 22 buy/sell conditions.

Enhanced visuals with background (bgcolor) and area fill (fill) support.

This isn’t just an update — it’s the next evolution of MACD forecasting.

⯁ Example of simple linear regression with one independent variable

This example demonstrates how a basic linear regression works when there is only one independent variable influencing the dependent variable. This type of model is used to identify a direct relationship between two variables.

⯁ In linear regression, observations (red) are considered the result of random deviations (green) from an underlying relationship (blue) between a dependent variable (y) and an independent variable (x)

This concept illustrates that sampled data points rarely align perfectly with the true trend line. Instead, each observed point represents the combination of the true underlying relationship and a random error component.

⯁ Visualizing heteroscedasticity in a scatterplot with 100 random fitted values using Matlab

Heteroscedasticity occurs when the variance of the errors is not constant across the range of fitted values. This visualization highlights how the spread of data can change unpredictably, which is an important factor in evaluating the validity of regression models.

⯁ The datasets in Anscombe’s quartet were designed to have nearly the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but look very different when plotted

This classic example shows that summary statistics alone can be misleading. Even with identical numerical metrics, the datasets display completely different patterns, emphasizing the importance of visual inspection when interpreting a model.

⯁ Result of fitting a set of data points with a quadratic function

This example illustrates how a second-degree polynomial model can better fit certain datasets that do not follow a linear trend. The resulting curve reflects the true shape of the data more accurately than a straight line.

⯁ What is the MACD?

The Moving Average Convergence Divergence (MACD) is a technical analysis indicator developed by Gerald Appel. It measures the relationship between two moving averages of a security’s price to identify changes in momentum, direction, and strength of a trend. The MACD is composed of three components: the MACD line, the signal line, and the histogram.

⯁ How to use the MACD?

The MACD is calculated by subtracting the 26-period Exponential Moving Average (EMA) from the 12-period EMA. A 9-period EMA of the MACD line, called the signal line, is then plotted on top of the MACD line. The MACD histogram represents the difference between the MACD line and the signal line.

Here are the primary signals generated by the MACD:

• Bullish Crossover: When the MACD line crosses above the signal line, indicating a potential buy signal.

• Bearish Crossover: When the MACD line crosses below the signal line, indicating a potential sell signal.

• Divergence: When the price of the security diverges from the MACD, suggesting a potential reversal.

• Overbought/Oversold Conditions: Indicated by the MACD line moving far away from the signal line, though this is less common than in oscillators like the RSI.

⯁ How to use MACD forecast?

The MACD Forecast is built on the same foundation as the classic MACD, but with predictive capabilities.

Step 1 — Spot Predicted Crossovers:

Watch for forecasted bullish or bearish crossovers. These signals anticipate when the MACD line will cross the signal line in the future, letting you prepare trades before the move.

Step 2 — Confirm with Histogram Projection:

Use the projected histogram to validate momentum direction. A rising histogram signals strengthening bullish momentum, while a falling projection points to weakening or bearish conditions.

Step 3 — Combine with Multi-Timeframe Analysis:

Use forecasts across multiple timeframes to confirm signal strength (e.g., a 1h forecast aligned with a 4h forecast).

Step 4 — Set Entry Conditions & Automation:

Customize your buy/sell rules with the 20 forecast-based conditions and enable automation for bots or alerts.

Step 5 — Trade Ahead of the Market:

By preparing for future momentum shifts instead of reacting to the past, you’ll always stay one step ahead of lagging traders.

📈 BUY

🍟 Signal Validity: The signal will remain valid for X bars.

🍟 Signal Sequence: Configurable as AND or OR.

🍟 MACD > Signal Smoothing

🍟 MACD < Signal Smoothing

🍟 Histogram > 0

🍟 Histogram < 0

🍟 Histogram Positive

🍟 Histogram Negative

🍟 MACD > 0

🍟 MACD < 0

🍟 Signal > 0

🍟 Signal < 0

🍟 MACD > Histogram

🍟 MACD < Histogram

🍟 Signal > Histogram

🍟 Signal < Histogram

🍟 MACD (Crossover) Signal

🍟 MACD (Crossunder) Signal

🍟 MACD (Crossover) 0

🍟 MACD (Crossunder) 0

🍟 Signal (Crossover) 0

🍟 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

📉 SELL

🍟 Signal Validity: The signal will remain valid for X bars.

🍟 Signal Sequence: Configurable as AND or OR.

🍟 MACD > Signal Smoothing

🍟 MACD < Signal Smoothing

🍟 Histogram > 0

🍟 Histogram < 0

🍟 Histogram Positive

🍟 Histogram Negative

🍟 MACD > 0

🍟 MACD < 0

🍟 Signal > 0

🍟 Signal < 0

🍟 MACD > Histogram

🍟 MACD < Histogram

🍟 Signal > Histogram

🍟 Signal < Histogram

🍟 MACD (Crossover) Signal

🍟 MACD (Crossunder) Signal

🍟 MACD (Crossover) 0

🍟 MACD (Crossunder) 0

🍟 Signal (Crossover) 0

🍟 Signal (Crossunder) 0

🔮 MACD (Crossover) Signal Forecast

🔮 MACD (Crossunder) Signal Forecast

🤖 Automation

All BUY and SELL conditions can be automated using TradingView alerts. Every configurable condition can trigger alerts suitable for fully automated or semi-automated strategies.

⯁ Unique Features

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

RT-Bitcoin Funding CandlesIntroduction

The RT-Bitcoin Funding Candles indicator and the RT-Bitcoin Spot vs Perp Funding indicator are designed to visualize Bitcoin funding conditions using estimated spot versus perpetual futures pricing. Together, they help traders see how funding has been behaving and where leveraged traders may be leaning over time. These two indicators are meant to be used together, and this write-up will cover how to utilize both tools.

The RT-Bitcoin Funding Candles indicator converts estimated funding information into custom candle colors on the chart. The RT-Bitcoin Spot vs Perp Funding indicator shows the same concept in a separate panel, similar to how many traders use RSI or other oscillators.

Both tools are intended as context layers around funding behavior, not standalone signal generators. RT-Bitcoin Funding Candles Indicator

The RT-Bitcoin Funding Candles indicator uses estimated differences between Bitcoin spot prices and perpetual futures prices to color each candle based on whether conditions are more aligned with bullish leveraged positioning or bearish spot-driven pressure.

In general terms: When perpetual futures trade at a premium to spot for extended periods, conditions are often associated with more aggressive leveraged long positioning.

When perpetual futures trade at a discount to spot, conditions can indicate stress on leveraged longs or periods where spot demand is stronger relative to perp. The indicator converts this estimated spot versus perp relationship into a color scale on the candles:

Bullish / Leveraged Funding Scale

Dark Blue → Blue → Light Blue → White

Bearish / Spot Funding Scale

Dark Red → Red → Orange → Yellow This allows traders to look at a BTC chart and quickly see whether estimated funding has been skewed toward leveraged longs or more spot-driven pressure during each candle.

Displaying Funding Candles On Top Of Price

By default, some chart layouts may draw the RT-Bitcoin Funding Candles indicator behind the main price candles. To make the funding candles fully visible: Right click on the RT-Bitcoin Funding Candles indicator on your chart.

Select Visual Order .

Choose Bring to Front . Once this is done, the funding candles will sit on top of or replace the normal bar colors, making the funding bias easier to see at a glance.

RT-Bitcoin Funding Candles Settings

The RT-Bitcoin Funding Candles indicator includes a small set of tuning options so traders can control which exchange data is used and how sensitive the color transitions are.

Key settings include:

Exchange Selection

Allows the trader to select which funding source is used for the calculation. Common options include: Binance, Deribit and Bybit. This lets traders align the indicator with the exchange they track most closely.

Smoothness Adjuster

Controls how sensitive the candle colors are to short-term changes in the spot versus perp relationship. Lower smoothing values will make colors react more quickly, but can be noisier. Higher smoothing values will make colors change less often, focusing on more persistent funding conditions. Customizing Funding Candle Colors

Traders who prefer different color palettes can customize the funding candle colors in the Style tab of the indicator settings. Open the RT-Bitcoin Funding Candles indicator settings.

Go to the Style tab.

Adjust the colors and opacities for each bullish and bearish funding color step.

This allows traders to keep the same logic while matching the visuals to their own chart themes.

RT-Bitcoin Spot vs Perp Funding Indicator

The RT-Bitcoin Spot vs Perp Funding indicator presents the same core concept in a separate, oscillator-style panel, similar to how traders might use RSI or other momentum tools.

Instead of recoloring the main candles, it plots lines that reflect how strong the estimated spot versus perp funding relationship has been over time. This can make it easier to compare current conditions to previous periods and to see when funding has moved into more extreme zones. RT-Bitcoin Spot vs Perp Funding Settings

The RT-Bitcoin Spot vs Perp Funding indicator provides a set of inputs so traders can tune how the estimated funding lines behave visually:

Premium Sensitivity

Controls how sensitive the plotted lines are to changes in the underlying estimated spot versus perp relationship. Higher sensitivity will cause the lines to move more aggressively. Lower sensitivity will smooth smaller fluctuations and focus on larger swings.

Premium Smoother

Applies additional smoothing to the raw estimated funding data. Because the underlying data can be noisy in its raw form, this setting helps reduce erratic spikes so that major shifts in funding are easier to read.

Exchange Toggles

Allows the trader to choose which exchanges are displayed in the panel. For example: Show or hide Binance funding lines.

Show or hide Deribit funding lines.

Show or hide Bybit funding lines. If multiple exchanges are enabled, multiple lines can be displayed for comparison.

Line Colors

Line colors and thickness can be adjusted in the Style tab. This makes it possible to:

Assign different colors to each exchange.

Emphasize key lines while de-emphasizing others. How Traders Commonly Use These Tools

The RT-Bitcoin Funding Candles and the RT-Bitcoin Spot vs Perp Funding indicators are typically used as part of a broader BTC workflow rather than on their own. Common usage patterns include: Context Around Extremes

Comparing current estimated funding conditions to past extremes to see when funding has become unusually one-sided relative to history.

Trend And Funding Alignment

Studying whether strong trends are being supported by consistent estimated leveraged funding, or whether price is moving against the prevailing estimated funding bias.

Multi Tool Confluence

Combining estimated funding candles or the spot versus perp panel with other tools such as RT-Main Indicator, Machine Learning Reversion Bands, or pivots to build a more complete picture of market conditions.

Exchange Comparison

Using the Spot vs Perp Funding panel to compare how different exchanges are pricing estimated funding at the same time and to see when one venue becomes an outlier. In all cases, these indicators are intended to provide an additional layer of information about how spot and perp markets have been behaving. They are not designed to be automatic entry or exit systems.

Important Note

The RT-Bitcoin Funding Candles and the RT-Bitcoin Spot vs Perp Funding indicators use chart-based calculations and publicly available pricing to approximate funding behavior. They do not access private exchange order books or actual liquidation feeds, do not reveal real trader positions, and cannot guarantee that any specific funding condition will lead to a particular price move.

These tools are intended to provide additional context around funding, positioning, and potential areas of interest. They are not standalone signal generators and should always be used together with your own analysis, testing, and risk management. Historical funding patterns or past interactions with these indicators do not guarantee future results.

🐋 Tight lines and happy trading!

RT-Bitcoin Spot vs Perp FundingIntroduction

The RT-Bitcoin Funding Candles indicator and the RT-Bitcoin Spot vs Perp Funding indicator are designed to visualize Bitcoin funding conditions using estimated spot versus perpetual futures pricing. Together, they help traders see how funding has been behaving and where leveraged traders may be leaning over time. These two indicators are meant to be used together, and this write-up will cover how to utilize both tools.

The RT-Bitcoin Funding Candles indicator converts estimated funding information into custom candle colors on the chart. The RT-Bitcoin Spot vs Perp Funding indicator shows the same concept in a separate panel, similar to how many traders use RSI or other oscillators.

Both tools are intended as context layers around funding behavior, not standalone signal generators. RT-Bitcoin Funding Candles Indicator

The RT-Bitcoin Funding Candles indicator uses estimated differences between Bitcoin spot prices and perpetual futures prices to color each candle based on whether conditions are more aligned with bullish leveraged positioning or bearish spot-driven pressure.

In general terms: When perpetual futures trade at a premium to spot for extended periods, conditions are often associated with more aggressive leveraged long positioning.

When perpetual futures trade at a discount to spot, conditions can indicate stress on leveraged longs or periods where spot demand is stronger relative to perp. The indicator converts this estimated spot versus perp relationship into a color scale on the candles:

Bullish / Leveraged Funding Scale

Dark Blue → Blue → Light Blue → White

Bearish / Spot Funding Scale

Dark Red → Red → Orange → Yellow This allows traders to look at a BTC chart and quickly see whether estimated funding has been skewed toward leveraged longs or more spot-driven pressure during each candle.

Displaying Funding Candles On Top Of Price

By default, some chart layouts may draw the RT-Bitcoin Funding Candles indicator behind the main price candles. To make the funding candles fully visible: Right click on the RT-Bitcoin Funding Candles indicator on your chart.

Select Visual Order .

Choose Bring to Front . Once this is done, the funding candles will sit on top of or replace the normal bar colors, making the funding bias easier to see at a glance.

RT-Bitcoin Funding Candles Settings

The RT-Bitcoin Funding Candles indicator includes a small set of tuning options so traders can control which exchange data is used and how sensitive the color transitions are.

Key settings include:

Exchange Selection

Allows the trader to select which funding source is used for the calculation. Common options include: Binance, Deribit and Bybit. This lets traders align the indicator with the exchange they track most closely.

Smoothness Adjuster

Controls how sensitive the candle colors are to short-term changes in the spot versus perp relationship. Lower smoothing values will make colors react more quickly, but can be noisier. Higher smoothing values will make colors change less often, focusing on more persistent funding conditions. Customizing Funding Candle Colors

Traders who prefer different color palettes can customize the funding candle colors in the Style tab of the indicator settings. Open the RT-Bitcoin Funding Candles indicator settings.

Go to the Style tab.

Adjust the colors and opacities for each bullish and bearish funding color step.

This allows traders to keep the same logic while matching the visuals to their own chart themes.

RT-Bitcoin Spot vs Perp Funding Indicator

The RT-Bitcoin Spot vs Perp Funding indicator presents the same core concept in a separate, oscillator-style panel, similar to how traders might use RSI or other momentum tools.

Instead of recoloring the main candles, it plots lines that reflect how strong the estimated spot versus perp funding relationship has been over time. This can make it easier to compare current conditions to previous periods and to see when funding has moved into more extreme zones. RT-Bitcoin Spot vs Perp Funding Settings

The RT-Bitcoin Spot vs Perp Funding indicator provides a set of inputs so traders can tune how the estimated funding lines behave visually:

Premium Sensitivity

Controls how sensitive the plotted lines are to changes in the underlying estimated spot versus perp relationship. Higher sensitivity will cause the lines to move more aggressively. Lower sensitivity will smooth smaller fluctuations and focus on larger swings.

Premium Smoother

Applies additional smoothing to the raw estimated funding data. Because the underlying data can be noisy in its raw form, this setting helps reduce erratic spikes so that major shifts in funding are easier to read.

Exchange Toggles

Allows the trader to choose which exchanges are displayed in the panel. For example: Show or hide Binance funding lines.

Show or hide Deribit funding lines.

Show or hide Bybit funding lines. If multiple exchanges are enabled, multiple lines can be displayed for comparison.

Line Colors

Line colors and thickness can be adjusted in the Style tab. This makes it possible to:

Assign different colors to each exchange.

Emphasize key lines while de-emphasizing others. How Traders Commonly Use These Tools

The RT-Bitcoin Funding Candles and the RT-Bitcoin Spot vs Perp Funding indicators are typically used as part of a broader BTC workflow rather than on their own. Common usage patterns include: Context Around Extremes

Comparing current estimated funding conditions to past extremes to see when funding has become unusually one-sided relative to history.

Trend And Funding Alignment

Studying whether strong trends are being supported by consistent estimated leveraged funding, or whether price is moving against the prevailing estimated funding bias.

Multi Tool Confluence

Combining estimated funding candles or the spot versus perp panel with other tools such as RT-Main Indicator, Machine Learning Reversion Bands, or pivots to build a more complete picture of market conditions.

Exchange Comparison

Using the Spot vs Perp Funding panel to compare how different exchanges are pricing estimated funding at the same time and to see when one venue becomes an outlier. In all cases, these indicators are intended to provide an additional layer of information about how spot and perp markets have been behaving. They are not designed to be automatic entry or exit systems.

Important Note

The RT-Bitcoin Funding Candles and the RT-Bitcoin Spot vs Perp Funding indicators use chart-based calculations and publicly available pricing to approximate funding behavior. They do not access private exchange order books or actual liquidation feeds, do not reveal real trader positions, and cannot guarantee that any specific funding condition will lead to a particular price move.

These tools are intended to provide additional context around funding, positioning, and potential areas of interest. They are not standalone signal generators and should always be used together with your own analysis, testing, and risk management. Historical funding patterns or past interactions with these indicators do not guarantee future results.

🐋 Tight lines and happy trading!

ADX Forecast Colorful [DiFlip]ADX Forecast Colorful

Introducing one of the most advanced ADX indicators available — a fully customizable analytical tool that integrates forward-looking forecasting capabilities. ADX Forecast Colorful is a scientific evolution of the classic ADX, designed to anticipate future trend strength using linear regression. Instead of merely reacting to historical data, this indicator projects the future behavior of the ADX, giving traders a strategic edge in trend analysis.

⯁ Real-Time ADX Forecasting

For the first time, a public ADX indicator incorporates linear regression (least squares method) to forecast the future behavior of ADX. This breakthrough approach enables traders to anticipate trend strength changes based on historical momentum. By applying linear regression to the ADX, the indicator plots a projected trendline n periods ahead — helping users make more accurate and timely trading decisions.

⯁ Highly Customizable

The indicator adapts seamlessly to any trading style. It offers a total of 26 long entry conditions and 26 short entry conditions, making it one of the most configurable ADX tools on TradingView. Each condition is fully adjustable, enabling the creation of statistical, quantitative, and automated strategies. You maintain full control over the signals to align perfectly with your system.

⯁ Innovative and Science-Based

This is the first public ADX indicator to apply least-squares predictive modeling to ADX dynamics. Technically, it embeds machine learning logic into a traditional trend-strength indicator. Using linear regression as a predictive engine adds powerful statistical rigor to the ADX, turning it into an intelligent, forward-looking signal generator.

⯁ Scientific Foundation: Linear Regression

Linear regression is a fundamental method in statistics and machine learning used to model the relationship between a dependent variable y and one or more independent variables x. The basic formula for simple linear regression is:

y = β₀ + β₁x + ε

Where:

y = predicted value (e.g., future ADX)

x = explanatory variable (e.g., bar index or time)

β₀ = intercept

β₁ = slope (rate of change)

ε = random error term

The goal is to estimate β₀ and β₁ by minimizing the sum of squared errors. This is achieved using the least squares method, ensuring the best linear fit to historical data. Once the coefficients are calculated, the model extends the regression line forward, generating the ADX projection based on recent trends.

⯁ Least Squares Estimation

To minimize the error, the regression coefficients are calculated as:

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

Σ = summation

x̄ and ȳ = means of x and y

i ranges from 1 to n (number of data points)

These formulas provide the best linear unbiased estimator under Gauss-Markov conditions — assuming constant variance and linearity.

⯁ Linear Regression in Machine Learning

Linear regression is a foundational algorithm in supervised learning. Its power in producing quantitative predictions makes it essential in AI systems, predictive analytics, time-series forecasting, and automated trading. Applying it to the ADX essentially places an intelligent forecasting engine inside a classic trend tool.

⯁ Visual Interpretation

Imagine an ADX time series like this:

Time →

ADX →

The regression line smooths these values and projects them n periods forward, creating a predictive trajectory. This forecasted ADX line can intersect with the actual ADX, offering smarter buy and sell signals.

⯁ Summary of Scientific Concepts

Linear Regression: Models variable relationships with a straight line.

Least Squares: Minimizes prediction errors for best fit.

Time-Series Forecasting: Predicts future values using historical data.

Supervised Learning: Trains models to predict outcomes from inputs.

Statistical Smoothing: Reduces noise and highlights underlying trends.

⯁ Why This Indicator Is Revolutionary

Scientifically grounded: Based on rigorous statistical theory.

Unprecedented: First public ADX using least-squares forecast modeling.

Smart: Uses machine learning logic.

Forward-Looking: Generates predictive, not just reactive, signals.

Customizable: Flexible for any strategy or timeframe.

⯁ Conclusion

By merging ADX and linear regression, this indicator enables traders to predict market momentum rather than merely follow it. ADX Forecast Colorful is not just another indicator — it’s a scientific leap forward in technical analysis. With 26 fully configurable entry conditions and smart forecasting, this open-source tool is built for creating cutting-edge quantitative strategies.

⯁ Example of simple linear regression with one independent variable

This example demonstrates how a basic linear regression works when there is only one independent variable influencing the dependent variable. This type of model is used to identify a direct relationship between two variables.

⯁ In linear regression, observations (red) are considered the result of random deviations (green) from an underlying relationship (blue) between a dependent variable (y) and an independent variable (x)

This concept illustrates that sampled data points rarely align perfectly with the true trend line. Instead, each observed point represents the combination of the true underlying relationship and a random error component.

⯁ Visualizing heteroscedasticity in a scatterplot with 100 random fitted values using Matlab

Heteroscedasticity occurs when the variance of the errors is not constant across the range of fitted values. This visualization highlights how the spread of data can change unpredictably, which is an important factor in evaluating the validity of regression models.

⯁ The datasets in Anscombe’s quartet were designed to have nearly the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but look very different when plotted

This classic example shows that summary statistics alone can be misleading. Even with identical numerical metrics, the datasets display completely different patterns, emphasizing the importance of visual inspection when interpreting a model.

⯁ Result of fitting a set of data points with a quadratic function

This example illustrates how a second-degree polynomial model can better fit certain datasets that do not follow a linear trend. The resulting curve reflects the true shape of the data more accurately than a straight line.

⯁ What is the ADX?

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ How to use the ADX?

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

Strong Trend: When the ADX is above 25, indicating a strong trend.

Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

Neutral Zone: Between 20 and 25, where the trend strength is unclear.

⯁ Entry Conditions

Each condition below is fully configurable and can be combined to build precise trading logic.

📈 BUY

🅰️ Signal Validity: The signal will remain valid for X bars .

🅰️ Signal Sequence: Configurable as AND or OR .

🅰️ +DI > -DI

🅰️ +DI < -DI

🅰️ +DI > ADX

🅰️ +DI < ADX

🅰️ -DI > ADX

🅰️ -DI < ADX

🅰️ ADX > Threshold

🅰️ ADX < Threshold

🅰️ +DI > Threshold

🅰️ +DI < Threshold

🅰️ -DI > Threshold

🅰️ -DI < Threshold

🅰️ +DI (Crossover) -DI

🅰️ +DI (Crossunder) -DI

🅰️ +DI (Crossover) ADX

🅰️ +DI (Crossunder) ADX

🅰️ +DI (Crossover) Threshold

🅰️ +DI (Crossunder) Threshold

🅰️ -DI (Crossover) ADX

🅰️ -DI (Crossunder) ADX

🅰️ -DI (Crossover) Threshold

🅰️ -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

📉 SELL

🅰️ Signal Validity: The signal will remain valid for X bars .

🅰️ Signal Sequence: Configurable as AND or OR .

🅰️ +DI > -DI

🅰️ +DI < -DI

🅰️ +DI > ADX

🅰️ +DI < ADX

🅰️ -DI > ADX

🅰️ -DI < ADX

🅰️ ADX > Threshold

🅰️ ADX < Threshold

🅰️ +DI > Threshold

🅰️ +DI < Threshold

🅰️ -DI > Threshold

🅰️ -DI < Threshold

🅰️ +DI (Crossover) -DI

🅰️ +DI (Crossunder) -DI

🅰️ +DI (Crossover) ADX

🅰️ +DI (Crossunder) ADX

🅰️ +DI (Crossover) Threshold

🅰️ +DI (Crossunder) Threshold

🅰️ -DI (Crossover) ADX

🅰️ -DI (Crossunder) ADX

🅰️ -DI (Crossover) Threshold

🅰️ -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

🤖 Automation

All BUY and SELL conditions are compatible with TradingView alerts, making them ideal for fully or semi-automated systems.

⯁ Unique Features

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

Background Colors: "bgcolor"

Background Colors: "fill"

CDVI – First Crypto Dominance Volatility Index by Armi GoldmanThe Crypto Dominance Volatility Index (CDVI) is the first volatility-based indicator designed specifically to analyze the stability and instability of dominance flows in the crypto market.

Instead of measuring price volatility, CDVI focuses on the volatility of market dominance itself — a structural driver behind capital rotation cycles such as Bitcoin Season, Altseason, accumulation zones, and macro cycle transitions.

CDVI transforms dominance changes into a clear volatility index that highlights compression, expansion, and regime shifts.

How it works

CDVI calculates the absolute or percentage-based realized volatility of your chosen dominance benchmark (BTC.D, TOTAL.D, or any dominance index available on TradingView).

The indicator then:

1. Smooths the volatility curve using adjustable parameters

2. Builds a long-term mean to identify regime structure

3. Computes percentile zones over a rolling lookback window

4. Highlights high-risk and low-risk dominance conditions using color-coded backgrounds

This creates a clean, noise-reduced volatility representation of the dominance market.

Why it looks like this

The CDVI curve is intentionally smooth and cyclical because dominance volatility behaves differently from price volatility:

• Dominance tends to trend slowly, then spike violently during rotation phases

• Periods of prolonged compression often occur before large macro moves

• Volatility bursts cluster during transitions (e.g. BTC → Alts, cycle tops, market-wide repricing)

The percentile zones (90% / 10%) give structural thresholds for extreme conditions.

Background color reveals when dominance volatility enters these extremes, creating visually clear “regime blocks.”

How to interpret CDVI

High CDVI (above the 90th percentile):

• Dominance instability

• Capital rotation phases are active

• Market is repricing sector allocations

• Often appears near Altseason tops or bottoms

• Signals caution for trend traders and opportunity for rotation traders

Low CDVI (below the 10th percentile):

• Compression and calm dominance

• Accumulation and structural balance

• Often precedes major expansions in Bitcoin or Alt markets

• Useful for anticipating cycle transitions before they break out

Long-term mean:

• Helps identify when the market is in a high-vol or low-vol regime

• Crossings around the mean often coincide with early cycle shifts

How to use CDVI in practice

1. Cycle Timing

Use CDVI to detect when the market moves from calm → expansion or expansion → exhaustion.

Low CDVI usually precedes major moves. High CDVI often marks transition turbulence.

2. BTC vs Altcoins Rotation

Combine CDVI with BTC.D / TOTAL2 / TOTAL3 to detect rotation windows.

High CDVI = dominance is unstable → rotations happen.

Low CDVI = dominance is stable → trending environment.

3. Risk Management

High CDVI suggests elevated structural risk (dominance shifting).

Low CDVI supports directional conviction.

4. Confluence with Price

When both price volatility and dominance volatility expand together → macro transition.

When price is volatile but CDVI is flat → noise, not structural change.

Who this indicator is for

• Cycle analysts

• Macro crypto traders

• BTC vs Alts rotation traders

• Portfolio allocators

• Long-term investors looking at structural market phases

CDVI is designed as a clean, structural tool for understanding volatility not of price — but of market power distribution.

Dumb Money Flow - Retail Panic & FOMO# Dumb Money Flow (DMF) - Retail Panic & FOMO

## 🌊 Overview

**Dumb Money Flow (DMF)** is a powerful **contrarian indicator** designed to track the emotional state of the retail "herd." It identifies moments of extreme **Panic** (irrational selling) and **FOMO** (irrational buying) by analyzing on-chain data, volume anomalies, and price velocity.

In crypto markets, retail traders often buy the top (FOMO) and sell the bottom (Panic). This indicator helps you do the opposite: **Buy when the herd is fearful, and Sell when the herd is greedy.**

---

## 🧠 How It Works

The indicator combines multiple data points into a single **Sentiment Index** (0-100), normalized over a 90-day period to ensure it always uses the full range of the chart.

### 1. Panic Index (Bearish Sentiment)

Tracks signs of capitulation and fear. High values contribute to the **Panic Zone**.

* **Exchange Inflows:** Spikes in funds moving to exchanges (preparing to sell).

* **Volume Spikes:** High volume during price drops (panic selling).

* **Price Crash (ROC):** Rapid, emotional price drops over 3 days.

* **Volatility (ATR):** High market nervousness and instability.

### 2. FOMO Index (Bullish Sentiment)

Tracks signs of euphoria and greed. High values contribute to the **FOMO Zone**.

* **Exchange Outflows:** Funds moving to cold storage (HODLing/Greed).

* **Profitable Addresses:** When >90% of holders are in profit, tops often form.

* **Parabolic Rise:** Rapid, unsustainable price increases.

---

## 🎨 Visual Guide

The indicator uses a distinct color scheme to highlight extremes:

* **🟢 Dark Green Zone (> 80): Extreme FOMO**

* **Meaning:** The crowd is euphoric. Risk of a correction is high.

* **Action:** Consider taking profits or looking for short entries.

* **🔴 Dark Burgundy Zone (< 20): Extreme Panic**

* **Meaning:** The crowd is capitulating. Prices may be oversold.

* **Action:** Look for buying opportunities (catching the knife with confirmation).

* **🔵 Light Blue Line:**

* The smoothed moving average of the sentiment, helpful for seeing the trend direction.

---

## 🛠️ How to Use (Trading Strategies)

### 1. Contrarian Reversals (The Primary Strategy)

* **Buy Signal:** Wait for the line to drop deep into the **Burgundy Panic Zone (< 20)** and then start curling up. This indicates that the worst of the selling pressure is over.

* **Sell Signal:** Wait for the line to spike into the **Green FOMO Zone (> 80)** and then start curling down. This suggests buying exhaustion.

### 2. Divergences

* **Bullish Divergence:** Price makes a **Lower Low**, but the DMF Indicator makes a **Higher Low** (less panic on the second drop). This is a strong reversal signal.

* **Bearish Divergence:** Price makes a **Higher High**, but the DMF Indicator makes a **Lower High** (less FOMO/buying power on the second peak).

### 3. Trend Confirmation (Midline Cross)

* **Crossing 50 Up:** Sentiment is shifting from Fear to Greed (Bullish).

* **Crossing 50 Down:** Sentiment is shifting from Greed to Fear (Bearish).

---

## ⚙️ Settings

* **Data Source:** Defaults to `INTOTHEBLOCK` for on-chain data.

* **Crypto Asset:** Auto-detects BTC/ETH, but can be forced.

* **Normalization Period:** Default 90 days. Determines the "window" for defining what is considered "Extreme" relative to recent history.

* **Weights:** You can customize how much each factor (Volume, Inflows, Price) contributes to the index.

---

**Disclaimer:** This indicator is for educational purposes only. "Dumb Money" analysis is a probability tool, not a crystal ball. Always manage your risk.

**Indicator by:** @iCD_creator

**Version:** 1.0

**Pine Script™ Version:** 6

---

## Updates & Support

For questions, suggestions, or bug reports, please comment below or message the author.

**Like this indicator? Leave a 👍 and share your feedback!**

Smart Money Flow - Exchange & TVL Composite# Smart Money Flow - Exchange & TVL Composite Indicator

## Overview

The **Smart Money Flow (SMF)** indicator combines two powerful on-chain metrics - **Exchange Flows** and **Total Value Locked (TVL)** - to create a composite index that tracks institutional and "smart money" movement in the cryptocurrency market. This indicator helps traders identify accumulation and distribution phases by analyzing where capital is flowing.

## What It Does

This indicator normalizes and combines:

- **Exchange Net Flow** (from IntoTheBlock): Tracks Bitcoin/Ethereum movement to and from exchanges

- **Total Value Locked** (from DefiLlama): Measures capital locked in DeFi protocols

The composite index is displayed on a 0-100 scale with clear zones for overbought/oversold conditions.

## Core Concept

### Exchange Flows

- **Negative Flow (Outflows)** = Bullish Signal

- Coins moving OFF exchanges → Long-term holding/accumulation

- Indicates reduced selling pressure

- **Positive Flow (Inflows)** = Bearish Signal

- Coins moving TO exchanges → Preparation for selling

- Indicates potential distribution phase

### Total Value Locked (TVL)

- **Rising TVL** = Bullish Signal

- Capital flowing into DeFi protocols

- Increased ecosystem confidence

- **Falling TVL** = Bearish Signal

- Capital exiting DeFi protocols

- Decreased ecosystem confidence

### Combined Signals

**🟢 Strong Bullish (70-100):**

- Exchange outflows + Rising TVL

- Smart money accumulating and deploying capital

**🔴 Strong Bearish (0-30):**

- Exchange inflows + Falling TVL

- Smart money preparing to sell and exiting positions

**⚪ Neutral (40-60):**

- Mixed or balanced flows

## Key Features

### ✅ Auto-Detection

- Automatically detects chart symbol (BTC/ETH)

- Uses appropriate exchange flow data for each asset

### ✅ Weighted Composite

- Customizable weights for Exchange Flow and TVL components

- Default: 50/50 balance

### ✅ Normalized Scale

- 0-100 index scale

- Configurable lookback period for normalization (default: 90 days)

### ✅ Signal Zones

- **Overbought**: 70+ (Strong bullish pressure)

- **Oversold**: 30- (Strong bearish pressure)

- **Extreme**: 85+ / 15- (Very strong signals)

### ✅ Clean Interface

- Minimal visual clutter by default

- Only main index line and MA visible

- Optional elements can be enabled:

- Background color zones

- Divergence signals

- Trend change markers

- Info table with detailed metrics

### ✅ Divergence Detection

- Identifies when price diverges from smart money flows

- Potential reversal warning signals

### ✅ Alerts

- Extreme overbought/oversold conditions

- Trend changes (crossing 50 line)

- Bullish/bearish divergences

## How to Use

### 1. Trend Confirmation

- Index above 50 = Bullish trend

- Index below 50 = Bearish trend

- Use with price action for confirmation

### 2. Reversal Signals

- **Extreme readings** (>85 or <15) suggest potential reversal

- Look for divergences between price and indicator

### 3. Accumulation/Distribution

- **70+**: Accumulation phase - smart money buying/holding

- **30-**: Distribution phase - smart money selling

### 4. DeFi Health

- Monitor TVL component for DeFi ecosystem strength

- Combine with exchange flows for complete picture

## Settings

### Data Sources

- **Exchange Flow**: IntoTheBlock real-time data

- **TVL**: DefiLlama aggregated DeFi TVL

- **Manual Mode**: For testing or custom data

### Indicator Settings

- **Smoothing Period (MA)**: Default 14 periods

- **Normalization Lookback**: Default 90 days

- **Exchange Flow Weight**: Adjustable 0-100%

- **Overbought/Oversold Levels**: Customizable thresholds

### Visual Options

- Show/Hide Moving Average

- Show/Hide Zone Lines

- Show/Hide Background Colors

- Show/Hide Divergence Signals

- Show/Hide Trend Markers

- Show/Hide Info Table

## Data Requirements

⚠️ **Important Notes:**

- Uses **daily data** from IntoTheBlock and DefiLlama

- Works on any chart timeframe (data updates daily)

- Auto-switches between BTC and ETH based on chart

- All other crypto charts default to BTC exchange flow data

## Best Practices

1. **Use on Daily+ Timeframes**

- On-chain data is daily, most effective on D/W/M charts

2. **Combine with Price Action**

- Use as confirmation, not standalone signals

3. **Watch for Divergences**

- Price making new highs while indicator falling = warning

4. **Monitor Extreme Zones**

- Sustained readings >85 or <15 indicate strong conviction

5. **Context Matters**

- Consider broader market conditions and fundamentals

## Calculation

1. **Exchange Net Flow** = Inflows - Outflows (inverted for index)

2. **TVL Rate of Change** = % change over smoothing period

3. **Normalize** both metrics to 0-100 scale

4. **Composite Index** = (ExchangeFlow × Weight) + (TVL × Weight)

5. **Smooth** with moving average

## Disclaimer

This indicator uses on-chain data for analysis. While valuable, it should not be used as the sole basis for trading decisions. Always combine with other technical analysis tools, fundamental analysis, and proper risk management.

On-chain data reflects blockchain activity but may lag price action. Use this indicator as part of a comprehensive trading strategy.

---

## Credits

**Data Sources:**

- IntoTheBlock: Exchange flow metrics

- DefiLlama: Total Value Locked data

**Indicator by:** @iCD_creator

**Version:** 1.0

**Pine Script™ Version:** 6

---

## Updates & Support

For questions, suggestions, or bug reports, please comment below or message the author.

**Like this indicator? Leave a 👍 and share your feedback!**

BTC Future CME Cross-Market DetectorProject Spec: BTC CME Cross-Market Detector

1. Project Overview

Indicator Name

CME Cross-Market Detector

Objective

To identify high-probability trade setups by detecting and confirming "smart money" activity across two distinct market venues simultaneously: a primary crypto exchange (e.g., Bybit, Binance) and the institutional CME futures market.

Core Philosophy

Price movements are often preceded by the positioning of large, institutional players ("smart money"). While their activity can be seen on any single exchange, the signal becomes exceptionally reliable when the same footprint appears at the same time in both the broader crypto derivatives market and the highly regulated institutional futures market. This dual-market confirmation acts as a powerful noise filter, isolating signals that have a higher probability of follow-through.

2. Key Concepts & Signal Logic

The indicator's entire foundation rests on confirming that specific conditions are met on two datasets at the same time: (1) The user's current chart (e.g., BYBIT:BTCUSDT) and (2) The CME Bitcoin Futures chart (CME:BTC1!).

Smart Volume Analysis

To gauge buying vs. selling pressure, the total volume of a single candle is algorithmically split. This is not a perfect science but an effective estimation based on the candle's structure.

Buying Pressure is considered proportional to the distance the price closed from the low. Buying Pressure ≈ Total Volume × ((Close - Low) / (High - Low))

Selling Pressure is considered proportional to the distance the price closed from the high. Selling Pressure ≈ Total Volume × ((High - Close) / (High - Low))

Signal Trigger Conditions

For a potential signal to be identified on each market independently, two conditions must be met:

Volume Spike: The volume of the current candle must be significantly higher than the recent average volume (e.g., >150% of the 20-period moving average). This shows a sudden, high level of interest.

Pressure Imbalance: The estimated buying pressure must overwhelm the selling pressure by a certain factor (e.g., 3x), or vice versa for a sell signal. This indicates a clear directional intent.

The Final Confirmed Signal

A signal is only considered valid and plotted on the chart when the Signal Trigger Conditions (both Volume Spike and Pressure Imbalance) are met on both the primary chart and the CME chart on the very same candle.

3. Signal Strength Calculation

The percentage shown on the chart is a Signal Strength Score (0-100%), which rates the quality and conviction of the confirmed signal.

The score is calculated as follows:

Base Score Calculation (0-100 points): A base score is calculated for each market (primary and CME) by combining two factors:

Volume Component (0-50 pts): Measures the intensity of the volume spike. A 300% volume spike will score higher than a 150% spike.

Imbalance Component (0-50 pts): Measures the intensity of the buy/sell pressure ratio. A 5x imbalance will score higher than a 3x imbalance.

Advanced Modifiers (Bonus Points): The base score is then enhanced with bonus points for favorable conditions:

Trend Alignment (+10 pts): A buy signal that occurs during a clear uptrend receives extra points.

Candle Structure (+10 pts): A buy signal on a candle with a long lower wick (indicating rejection of lower prices) receives extra points.

Final Averaged Score: The final percentage you see is the average of the two individual strength scores calculated for the primary exchange and the CME market.

4. Visualization

Energy Waves: Signals are displayed as circles. Green for Buy Signals (below the candle) and Red for Sell Signals (above the candle).

Dynamic Sizing: The size of the circle directly reflects the Signal Strength Score, categorized into four distinct levels (e.g., 10%+, 40%+, 60%+, and 80%+) for at-a-glance interpretation.

Percentage Labels: Each signal is plotted with its precise, final strength score for clear analysis.

5. Summary: Steps to Replicate the Logic

To recreate this indicator, follow these high-level steps for each candle on the chart:

Gather Data: Fetch the Open, High, Low, Close, and Volume data for the primary chart asset AND for the corresponding CME Bitcoin Futures symbol (CME:BTC1!).

Calculate Buy/Sell Pressure: For both datasets, use the "Smart Volume Analysis" formula to estimate the buying and selling pressure for the current candle.

Check for Volume Spikes: For both datasets, calculate a simple moving average of the volume. Check if the current candle's volume exceeds this average by a set threshold (e.g., 150%).

Check for Pressure Imbalance: For both datasets, check if the buying pressure is greater than the selling pressure by a set multiplier (e.g., 3.0), or vice versa.

Confirm the Signal: A final signal is only valid if the conditions from both Step 3 and Step 4 are true for both datasets on the same candle.

Calculate Strength: If a signal is confirmed, compute a strength score (0-100) for each dataset based on the intensity of the volume spike and pressure imbalance. Add bonus points for confluence factors like trend alignment.

Finalize and Plot: Average the two strength scores from each market. Plot a colored, sized circle on the chart that visually represents this final averaged score, and display the score as a text label.

Last but not least, the idea of the indicator is inspired by 52SIGNAL

BTC ETF Flow Monitor🚀 Bitcoin ETF Flow Monitor - Track Institutional Money Flows

Monitor real-time dollar flows across major Bitcoin ETFs with this professional-grade indicator inspired by Dune Analytics. Perfect for tracking institutional sentiment and Bitcoin adoption trends.

📊 Key Features: • Real Dollar Flows : Display actual estimated flows in millions USD, not abstract indices

• 5 Major ETFs : IBIT (BlackRock), FBTC (Fidelity), ARKB (ARK), BITB (Bitwise), GBTC (Grayscale)

• Dune Analytics Style : Clean, professional visualization with meaningful thresholds

• Smart Alerts : Get notified of significant flow changes and BTC price divergences

• Enhanced Summary Table : Live stats including total flows, trends, and market sentiment

💡 How It Works: Combines volume, price action, and momentum to estimate institutional dollar flows. Positive values = inflows (buying pressure), negative values = outflows (selling pressure). Scale shows millions of USD for easy interpretation.

🎯 Perfect For:

- Tracking institutional Bitcoin adoption

- Identifying accumulation/distribution phases

- Spotting divergences between ETF flows and BTC price

- Understanding market sentiment shifts

⚡ Professional Grade: Built with advanced Pine Script techniques, optimized performance, and real-world trading applications in mind.

BTC -50% Crash to Recovery ZoneGeneral Overview This is a macro-analysis tool designed to visualize the true duration of Bitcoin’s "Suffering & Recovery Cycles." Unlike standard oscillators that only signal oversold conditions, this script highlights the entire timeline required for the market to flush out leverage and return to All-Time Highs (ATH).

Operational Logic The algorithm tracks Bitcoin’s historical All-Time High (ATH).

The Trigger: It activates automatically when the price drops 50% below the last recorded ATH.

The "Recovery Zone": Once triggered, the chart background turns red (indicating a "Drawdown" state). This zone remains active persistently, even during intermediate relief rallies.

The Reset: The zone deactivates only when the price breaks above the previous ATH, marking the official start of a new Price Discovery phase.

How to Read It

Red Background: We are officially in a Bear Market or Recovery Phase. The asset is technically "underwater." For the long-term investor with a low time preference, this visually defines the accumulation window.

Red Horizontal Line: Indicates the "Target." This is the exact price level of the old ATH that Bitcoin must reclaim to close the bearish cycle.

No Background Color: We are in Price Discovery. The market is healthy and pushing for new highs.

The Financial Lesson This indicator visually demonstrates a fundamental market truth: "Price takes the elevator down, but takes the stairs up." It shows that after a halving of value (-50%), Bitcoin may take months or years to recover previous levels, helping investors filter out the noise of short-term pumps that fail to break the macro-bearish structure.

[CASH] Crypto And Stocks Helper (MultiPack w. Alerts)ATTENTION! I'm not a good scripter. I have just learned a little basics for this project, stolen code from other public scripts and modified it, and gotten help from AI LLM's.

If you want recognition from stolen code please tell me to give you the credit you deserve.

The script is not completely finished yet and contains alot of errors but my friends and family wants access so I made it public.

_________________________________________________________________________________

CASH has multiple indicators (a true all-in-one multipack), guides and alerts to help you make better trades/investments. It has:

- Bitcoin Bull Market Support Band

- Dollar Volume

- 5 SMA and 5 EMA

- HODL Trend (a.k.a SuperTrend) indicator

- RSI, Volume and Divergence indicators w. alerts

More to come as well, like Backburner and a POC line from Volume Profile.

Everything is fully customizable, appearance and off/on etc.

More information and explainations along with my guides you can find in settings under "Input" and "Style".

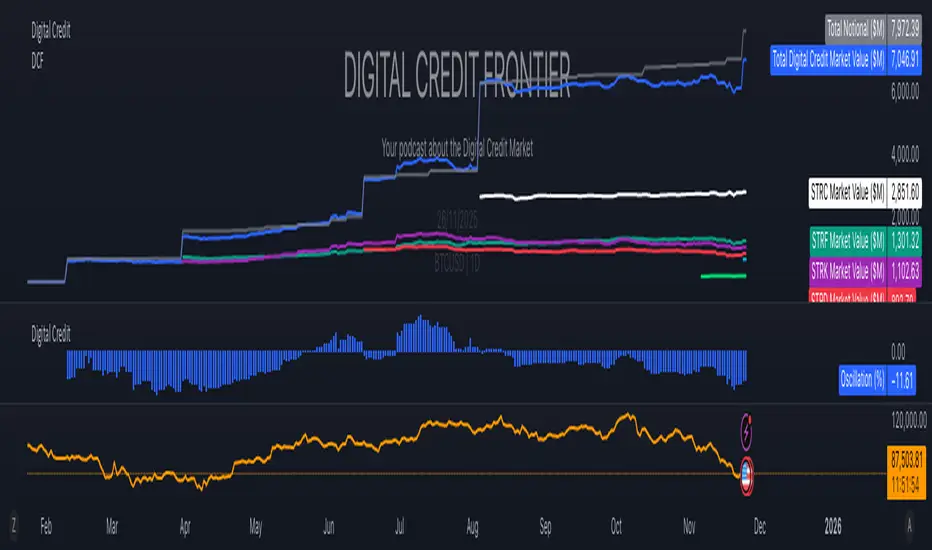

Digital Credit Market ValueDigital Credit Frontier

Script for tracking total notional value and total market value for the Digital Credit Market. Needs be manually updated. You can open it twice to get the total value in one pane and the oscillator in the other pane.

Pi Cycle BTC Top + Pre-Alert BandsPi Cycle BTC Top + Pre-Alert Bands is an advanced implementation of the classic Pi Cycle Top model, designed for Bitcoin cycle analysis on higher timeframes (especially 1D BTCUSD/BTCUSD·INDEX).

The original Pi Cycle Top uses two moving averages:

• 111-day SMA (short MA)

• 350-day SMA ×2 (long MA)

A Pi Top is signaled when the 111 SMA crosses above the 350×2 SMA. Historically, this has occurred near major BTC cycle highs.

This script extends that idea with a 3-step early-warning sequence:

• Pi Green – early compression: short/long MA ratio crosses upward into the green band (convergence from below is required).

• Pi Yellow – mid-cycle warning: only fires if a valid Green has already occurred in the same cycle.

• Pi Cycle Top – final top: the classic Pi Cycle cross, limited to one top signal per cycle. After a top, no new Yellow or Top signals can appear until a new Green event starts the next cycle.

Background shading shows the active phase (Green / Yellow / late-cycle zone), so you can see at a glance where BTC is within its Pi-based macro structure.

All logic is non-repainting: request.security() uses lookahead_off and no future data is accessed.

Typical use

This indicator is intended as a macro-cycle timing and risk-awareness tool, not a stand-alone entry system. Many traders use it to:

• Watch for Pi Green as the start of a potential late-cycle advance.

• Treat Pi Yellow as a rising-risk environment and tighten risk management.

• Use the Pi Cycle Top as a historical high-risk zone where large profit-taking or hedging may be considered.

Always combine this with your own analysis (trend, volume, on-chain, macro) before making decisions.

How to set alerts

Add the indicator to your chart (1D BTCUSD or BTCUSD·INDEX recommended).

Click Alerts → Condition → Pi Cycle BTC Top + Pre-Alert Bands.

Choose one of:

• Pi Cycle – Green Pre-Alert (early convergence)

• Pi Cycle – Yellow Pre-Alert (after Green only)

• Pi Cycle – TOP (Single per Cycle, after Green)

Use “Once per bar close” for higher-timeframe reliability.

Disclaimer

This tool is for educational and analytical purposes only. The Pi Cycle concept is based on historical behavior and does not guarantee future results. This is not financial advice; always do your own research and manage risk appropriately.

[Algoros] BTC Major Trendline# BTC Major Trendline - Long-Term Bitcoin Trend Analysis

## Overview

BTC Major Trendline is a comprehensive technical analysis tool designed to track Bitcoin's long-term bullish trajectory using historically significant price points. This indicator establishes a primary upward trendline anchored to two major Bitcoin cycle lows, along with optional parallel channels and Fibonacci-based price projections.

## ⚠️ Important Requirements

**This indicator requires a Bitcoin chart with sufficient historical data dating back to at least April 2013.**

**✅ Recommended Charts:**

- `INDEX:BTCUSD` - Bitcoin Index (comprehensive history)

- `BITSTAMP:BTCUSD` - Bitstamp Bitcoin (default setting)

**❌ Will NOT work properly on:**

- Charts with limited history (Like hourly charts)

- Exchanges that launched after 2013

- Altcoin pairs or other cryptocurrencies

If the indicator doesn't display correctly, switch to one of the recommended Bitcoin charts above.

## Key Features

### 📈 Primary Trendline

- Anchored to two historically significant lows:

- **Start Point**: July 6, 2013 - Early Bitcoin accumulation phase

- **End Point**: November 21, 2022 - FTX collapse bottom

- Automatically calculates and extends the trendline based on these anchor points

- Displayed as a solid orange line

### 🔷 Parallel Channel Line (Optional)

- Creates an upper boundary by connecting historical high points:

- April 10, 2013 and June 11, 2017

- Helps identify potential resistance zones and channel breakouts

- Displayed as a blue dotted line for easy distinction

### 🎯 Fibonacci Trendline Multipliers (Optional)

- Seven Fibonacci-based projection lines: **1.6x, 2x, 3x, 5x, 8x, 13x, and 21x**

- Each multiplier creates a parallel trendline above the main trend

- Color-coded from teal to maroon for clear visual separation

- Useful for identifying potential profit-taking zones and long-term price targets

### 📉 Negative Fibonacci Trendlines (Optional)

- Seven division-based support lines: **÷1.6, ÷2, ÷3, ÷5, ÷8, ÷13, and ÷21**

- Projects downward channels below the main trendline

- Displayed in yellow tones for easy identification

- Helps identify extreme oversold conditions and potential bounce zones

## Customization Options

- **Symbol Input**: Track any Bitcoin pair with sufficient history (default: BITSTAMP:BTCUSD)

- **Show/Hide Components**: Toggle parallel line, Fibonacci multipliers, and negative Fibonacci lines independently

- **Line Extension**: Extend lines right, left, both directions, or none

- **Multi-Timeframe Compatible**: View on any timeframe once loaded on a compatible chart

## How to Use

1. **Setup**: First, open a Bitcoin chart with sufficient history (INDEX:BTCUSD or BITSTAMP:BTCUSD recommended)

2. **Trend Confirmation**: The main orange trendline represents the long-term bullish trajectory. Price staying above this line suggests the bull market remains intact.

3. **Channel Trading**: Use the parallel line (blue dotted) as a potential upper boundary for the long-term channel.

4. **Price Targets**: Enable Fibonacci multiplier lines to identify ambitious long-term price targets during bull runs. Higher multipliers (13x, 21x) represent parabolic extension zones.

5. **Support Identification**: Enable negative Fibonacci lines to spot potential support zones during corrections or bear markets.

6. **Risk Management**: Breaking below the main trendline could signal a shift in long-term trend, warranting caution.

## Technical Implementation

- Uses `request.security()` to fetch precise daily prices at historical timestamps

- Requires access to Bitcoin price data from April 2013 onwards